Economy

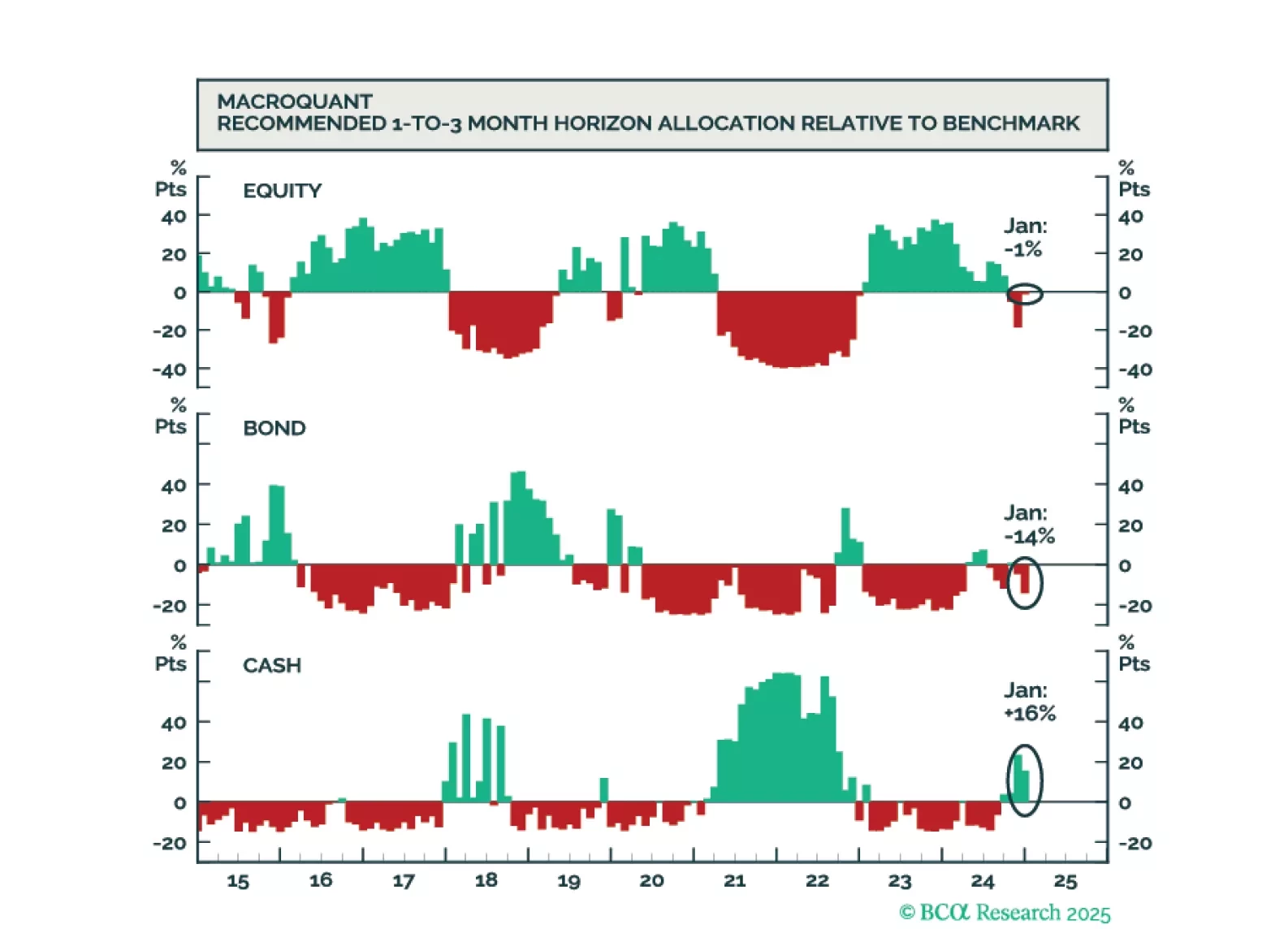

While the US economy could remain upright on the tightrope for a while longer, it will inevitably fall, leading to a major bear market in stocks. We will be looking to our MacroQuant model for guidance on when to turn fully defensive. We are not there yet.

There is no better way to gauge the macro policies of the new US administration than being privy to President Donald Trump’s discussions with the new Treasury Secretary, Scott Bessent. While we do not have inside information, we have put the pieces of the puzzle together to help clients see the big picture. This report presents our take on a hypothetical conversation between President Trump and Scott Bessent that led to the latter’s appointment as Treasury secretary.

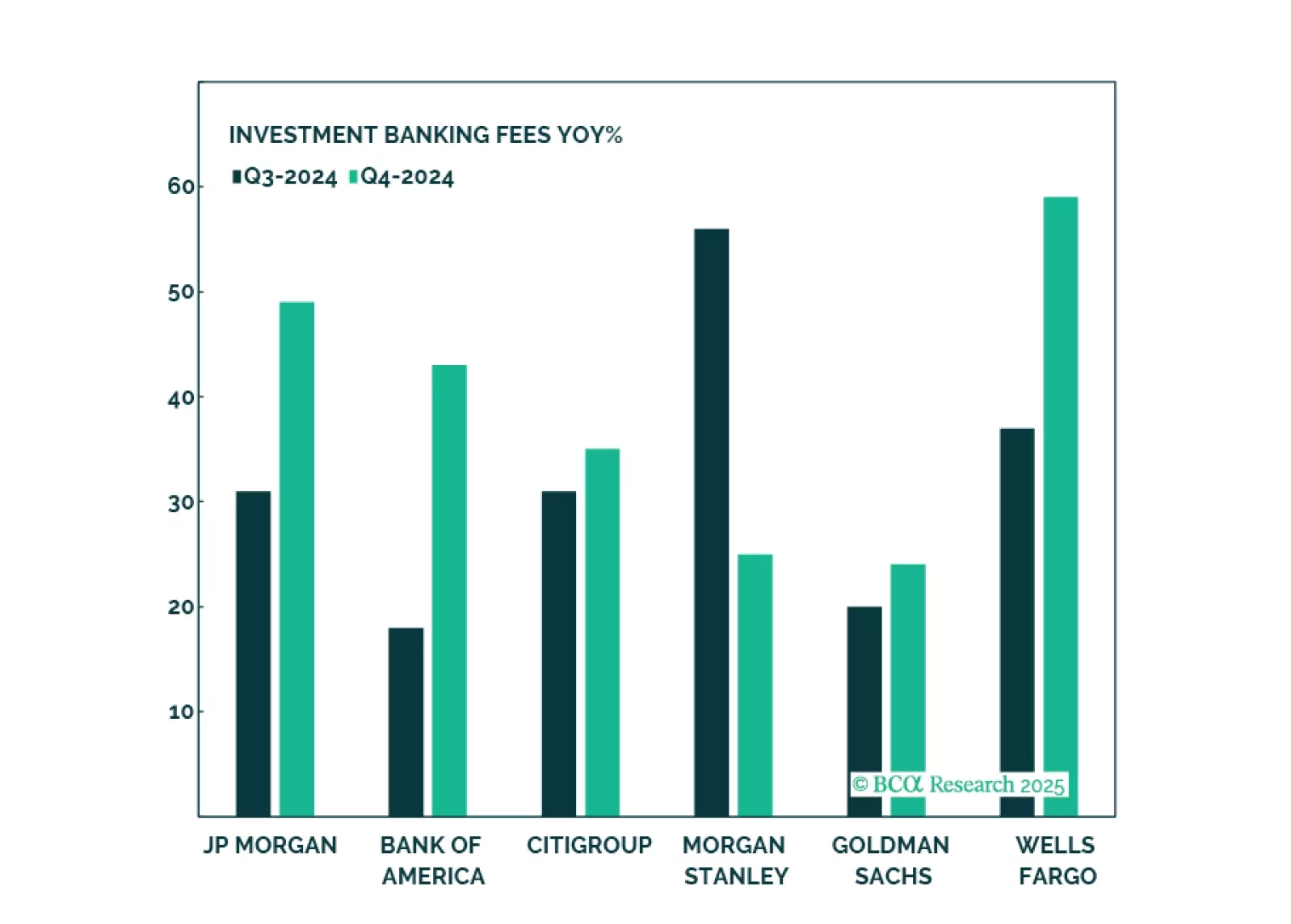

Banks have had an amazing run, and while such strong performance is unlikely to repeat, there is still oomph left in the trade thanks to a more favorable regulatory environment, stronger demand for loans, a steeper yield curve, and a strong pipeline of capital market activity. Key risks are further tightening of monetary policy and an increase in bad loans. We reiterate our overweight on Capital Markets, Diversified Banks, and Regional Banks.