Economy

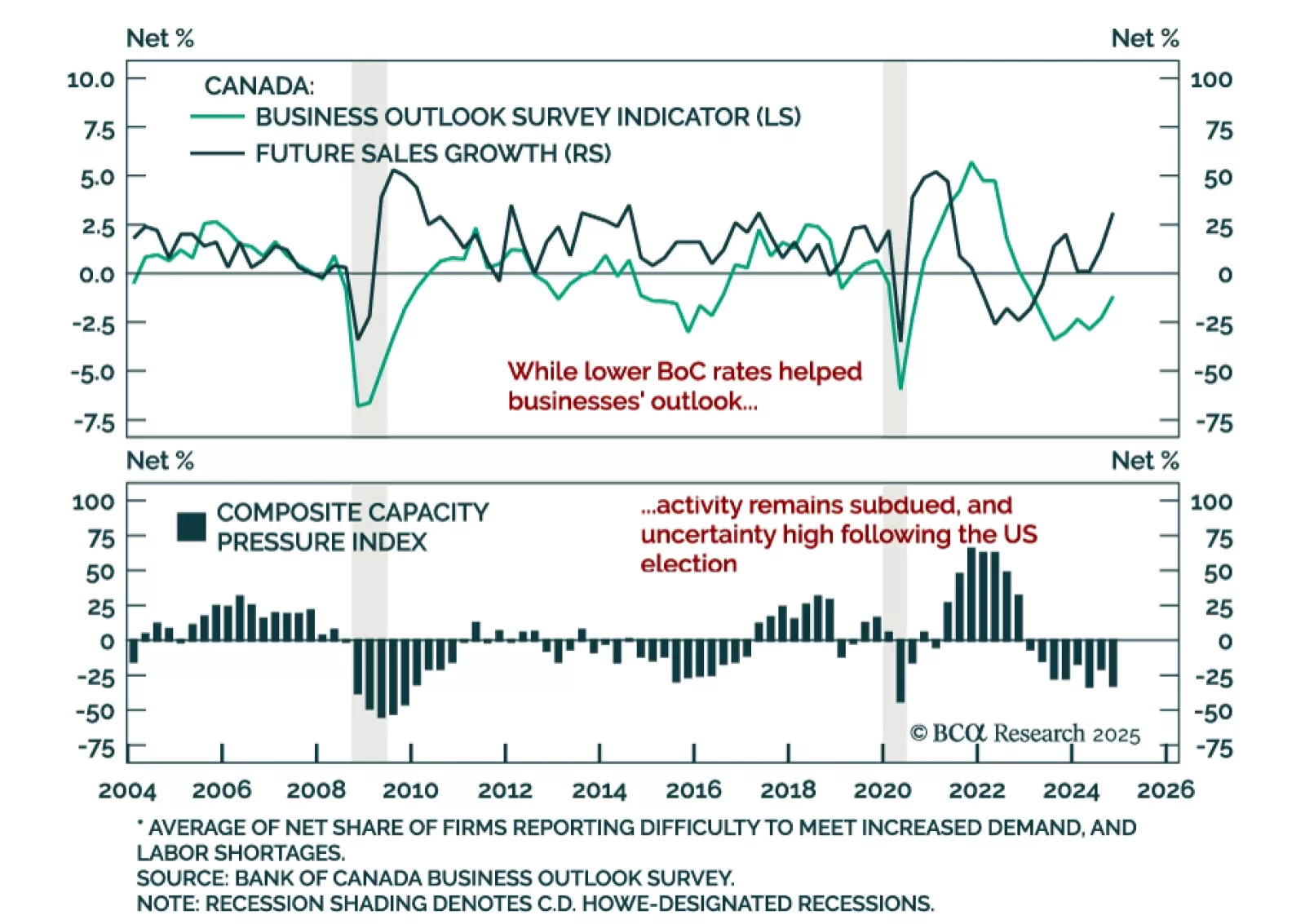

The Q4 2024 Bank of Canada’s Business Outlook Survey showed improving business optimism, with the overall index ticking up to -1.2, and a net 31% of surveyed businesses expecting higher sales, compared to 13% in Q3. Improved expectations reflect looser…

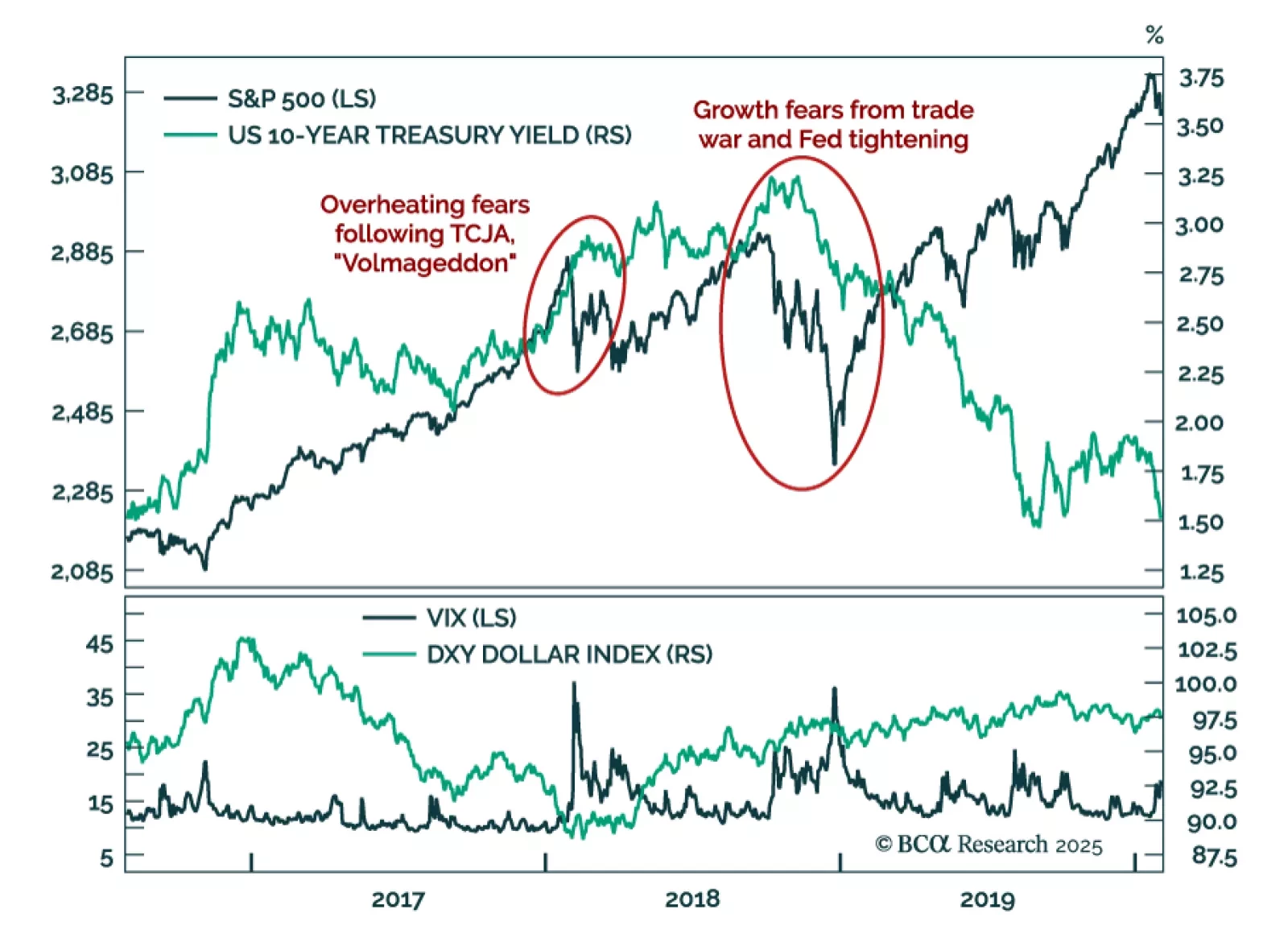

We look at President Trump’s first mandate for lessons on how markets would likely react to different policies. On the fiscal front, the 2017 Tax Cuts and Jobs Act (TCJA) was the first pro-cyclical stimulus in decades. Markets pushed back, as the early 2018…

President Trump’s inaugural speech outlined his second term agenda. The theme was that the US will become “far more exceptional” than it already is. Trump pledged to reverse America’s decline, rebalance the justice system, streamline government, protect…

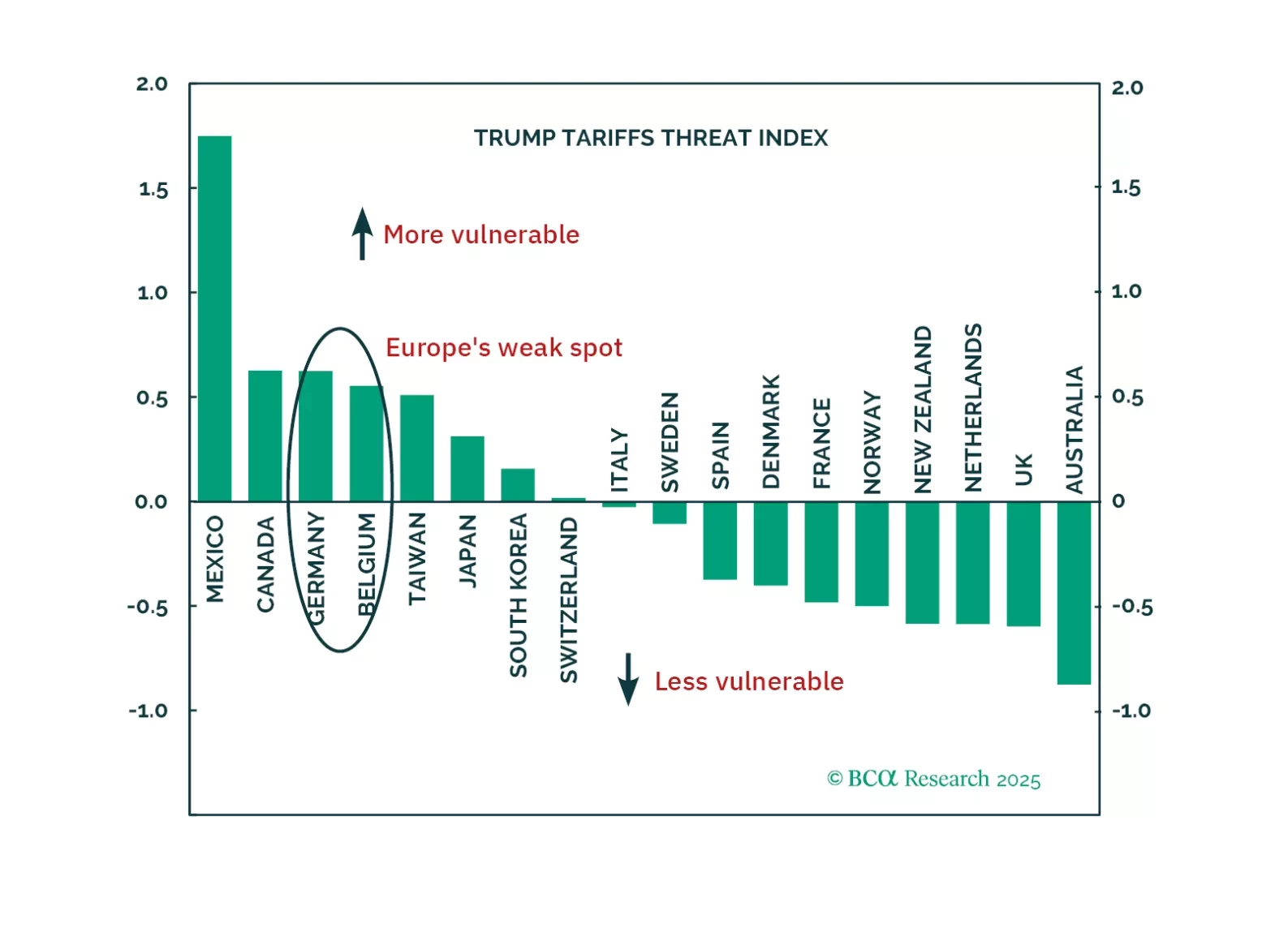

President Trump is about to be inaugurated. Investors often assume all his policies will hurt Europe, but the reality is more nuanced.

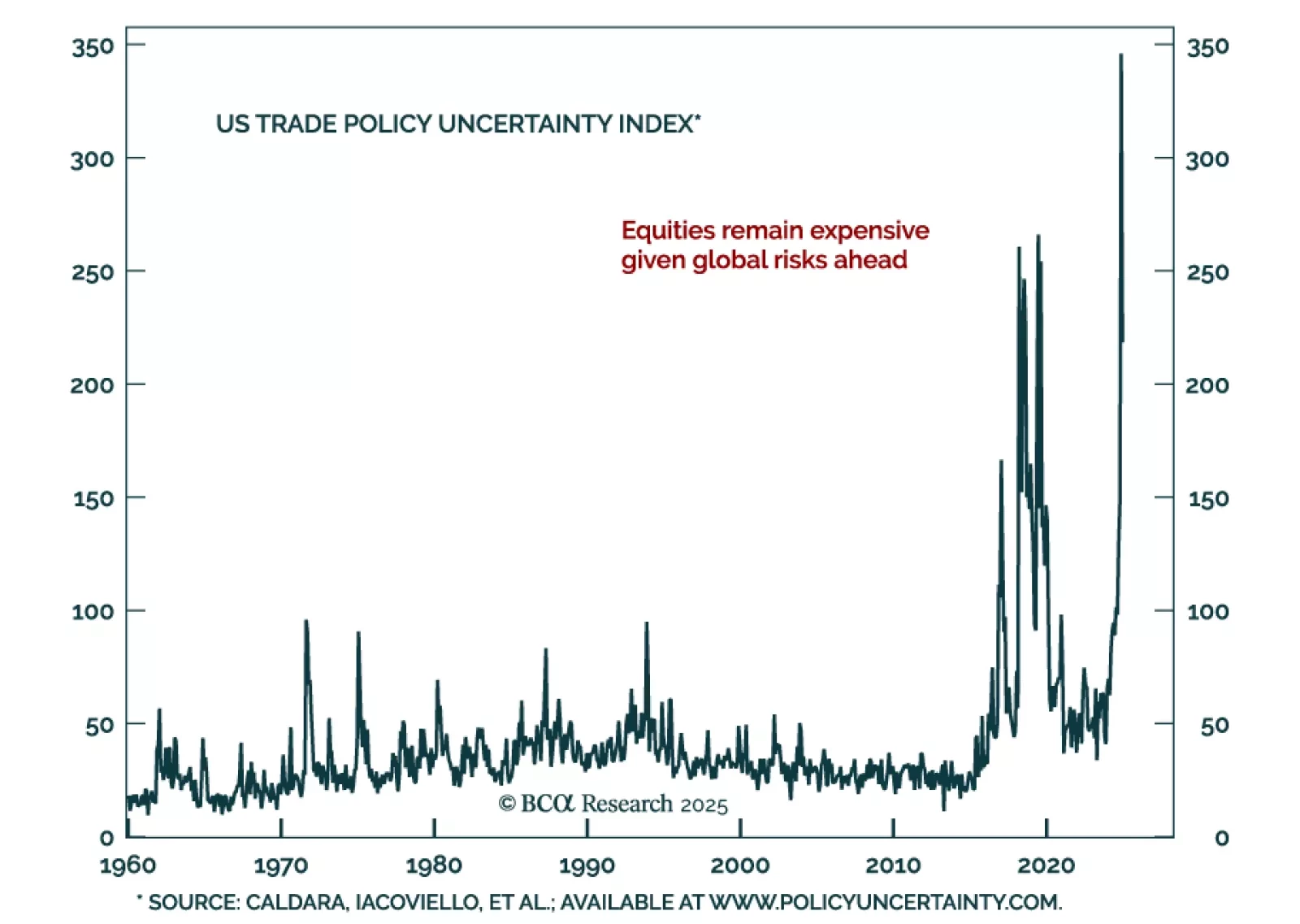

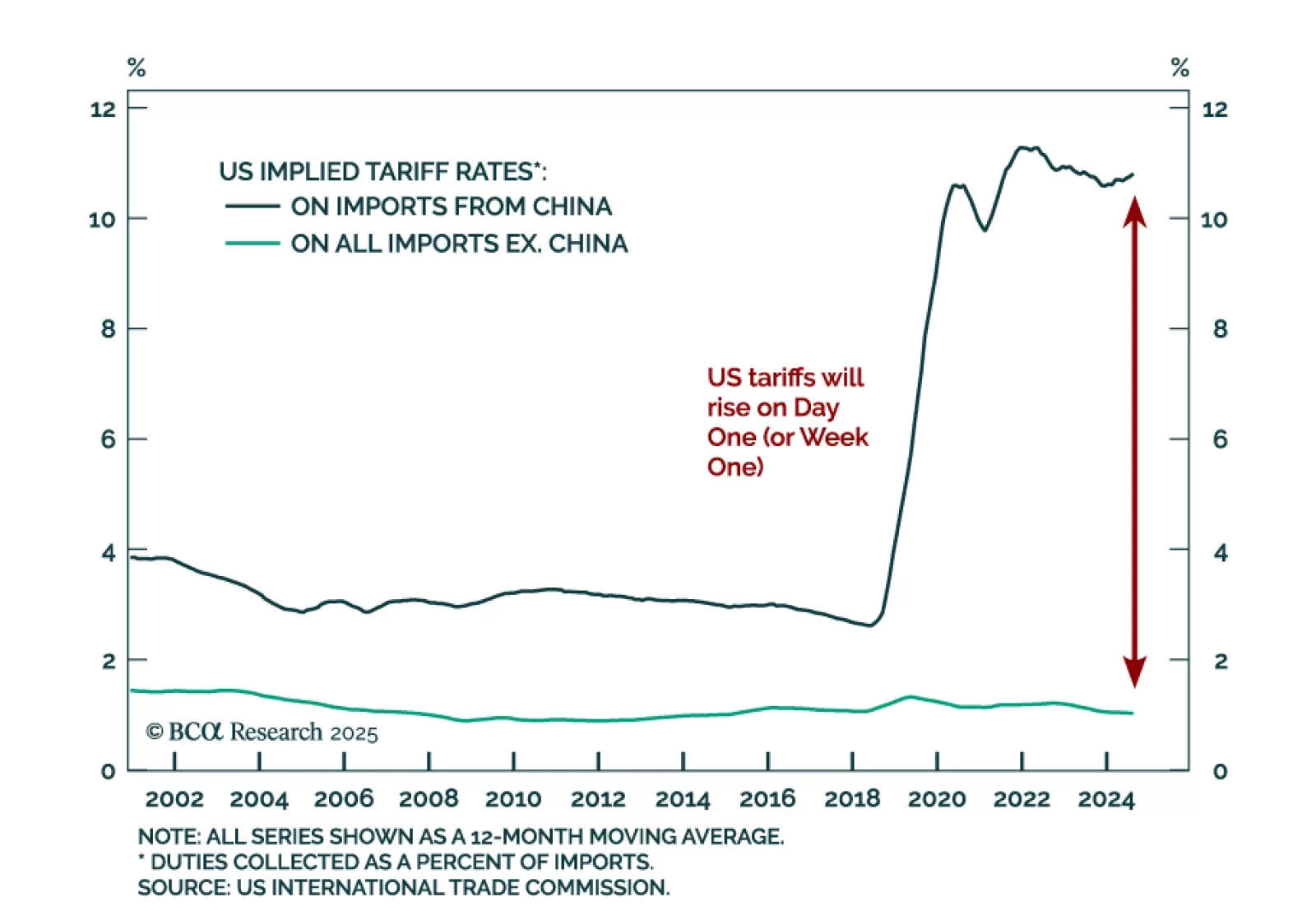

US Tariffs Will Rise On Day One (Or Week One)

…

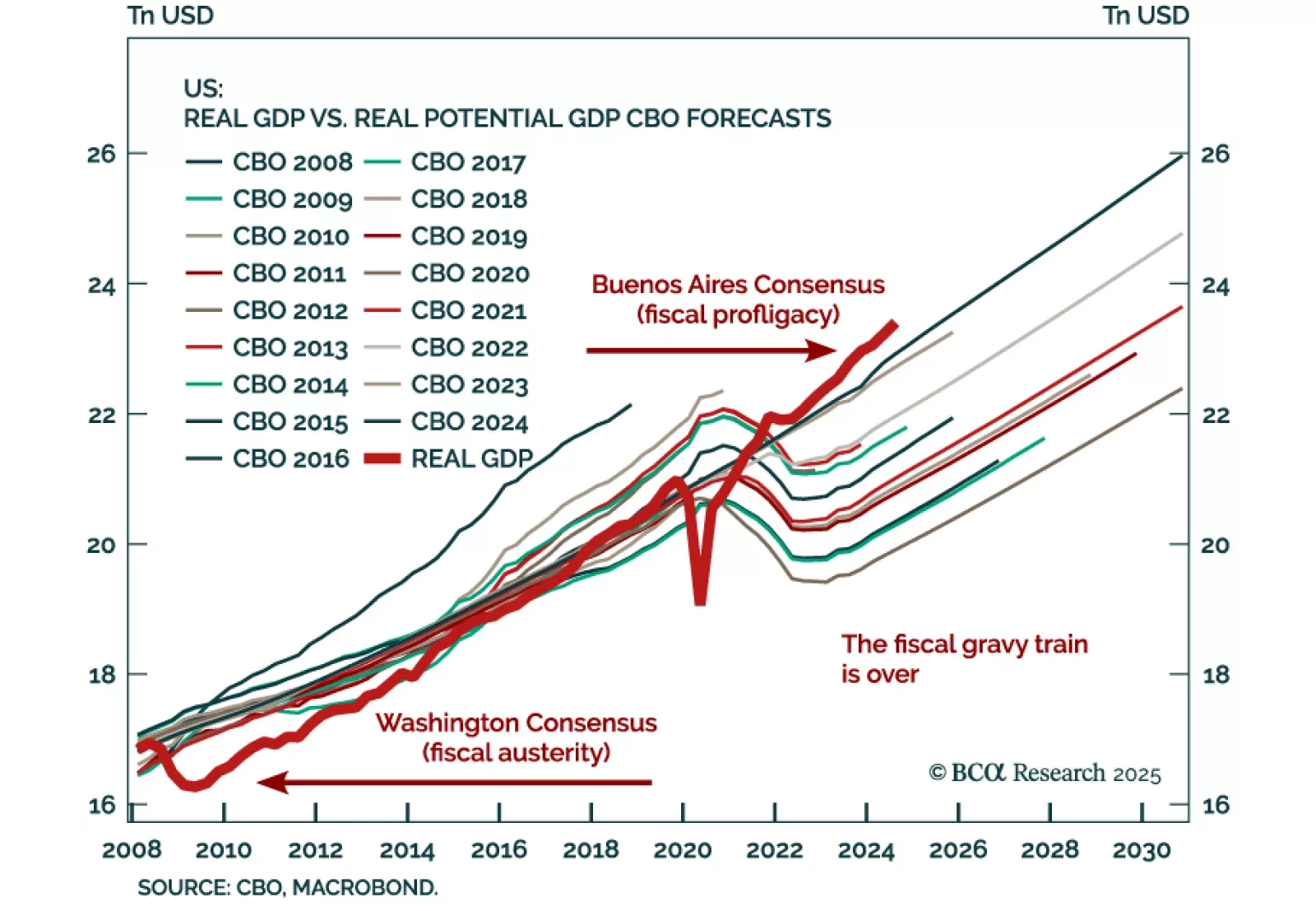

Our Chart Of The Week comes from Marko Papic, Chief Strategist of our GeoMacro Strategy service. Marko has argued that the most important macro story over the past decade has been the transition from the Washington Consensus, promoting fiscal conservatism, to…

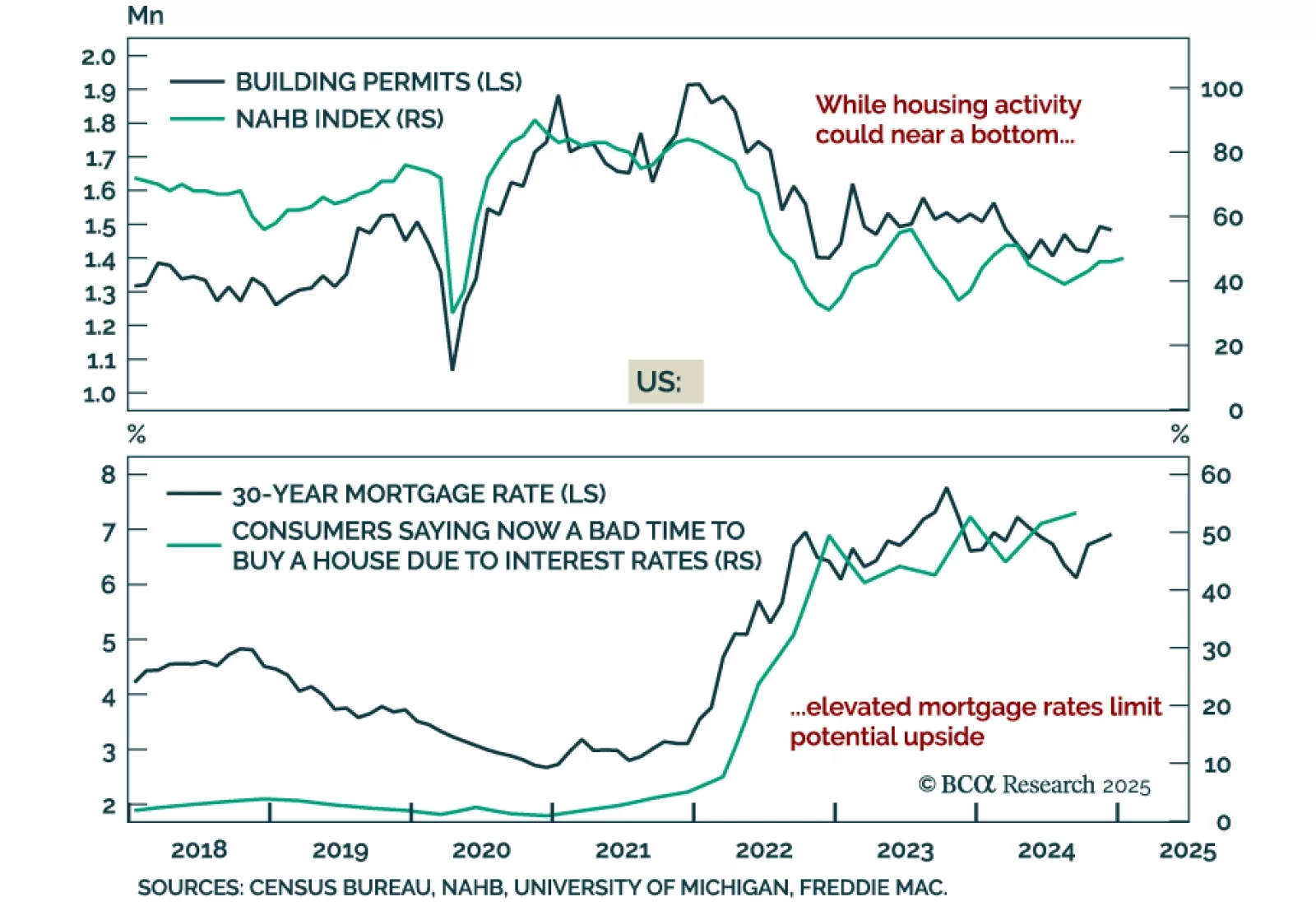

US December housing data was strong, with housing starts printing above estimates at 1.49m, an acceleration from an upwardly-revised 1.29m in November. Building permits also surprised positively at 1.483m, but still decreased from 1.493m a month prior. The…

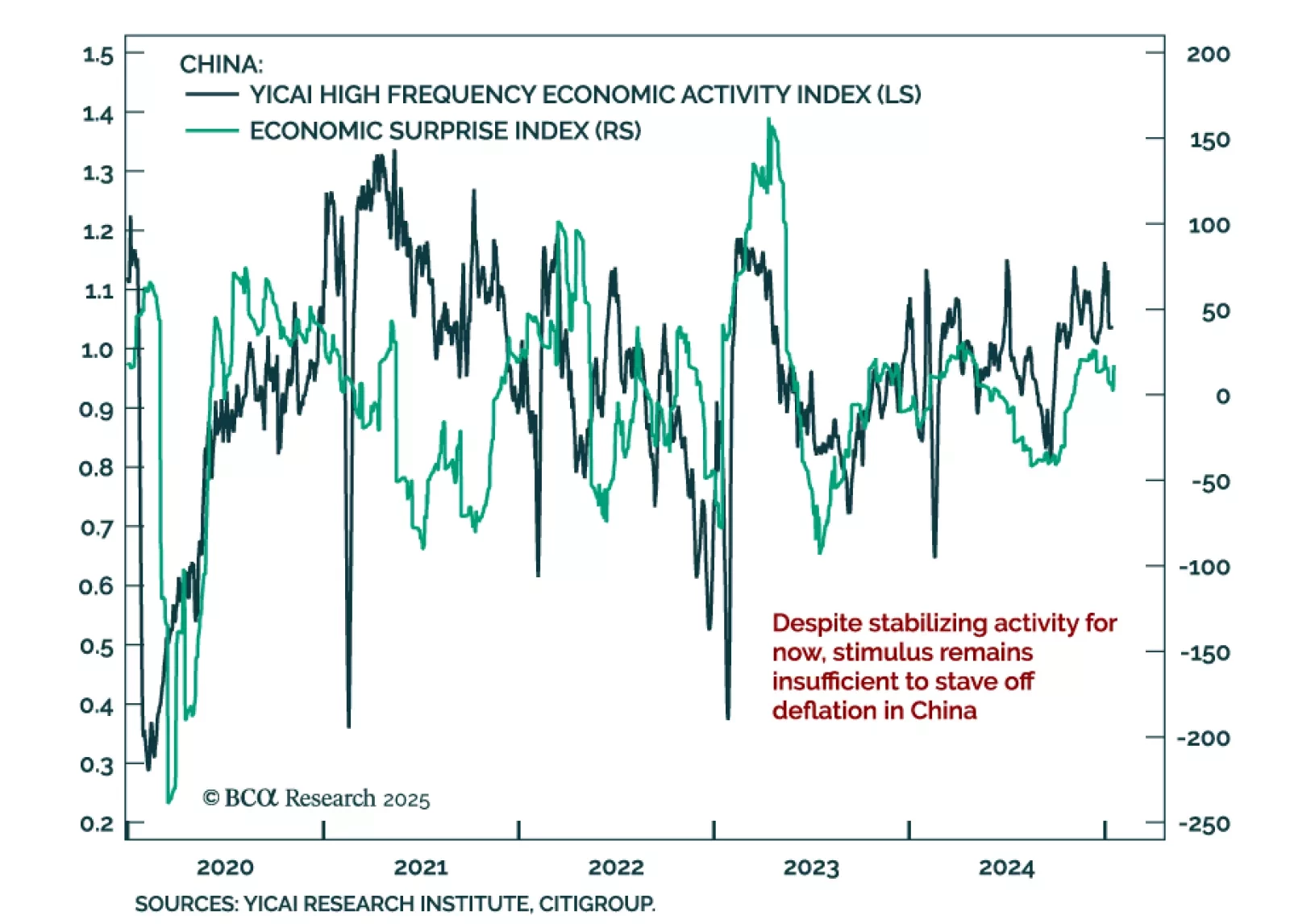

Chinese activity was decent in December, with GDP growth topping the 5% target for 2024. Industrial production growth ticked up to 6.2% y/y from 5.4% in November. Retail sales also picked up, increasing to 3.7% from 3.0% a month prior. New and used home…

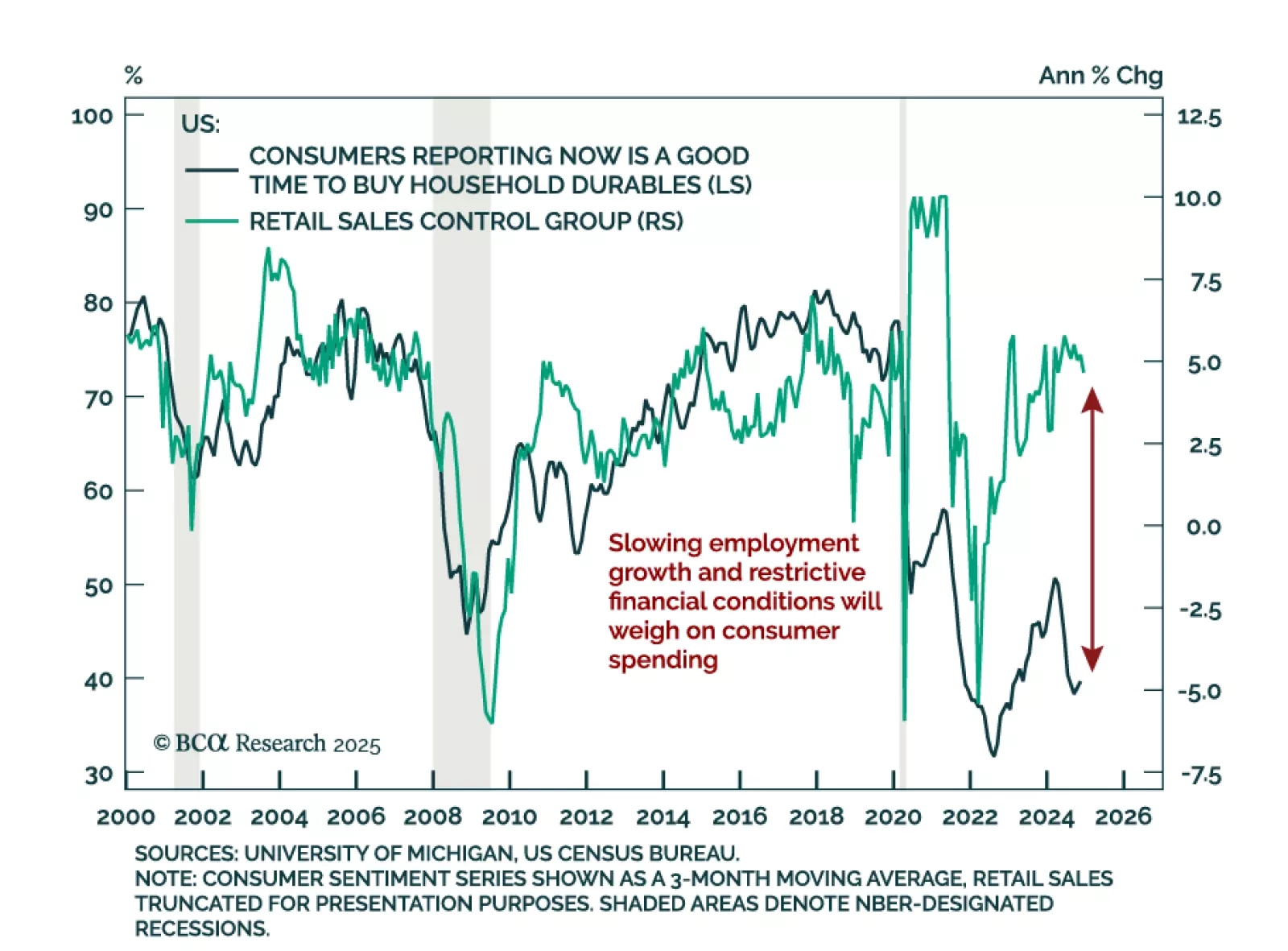

December US retail sales missed estimates, with the headline number printing at 0.4% m/m, a decline from an upwardly revised 0.8% in November. On the positive side, the control group beat estimates at 0.7%. Netting it all out, the report was uninspiring,…

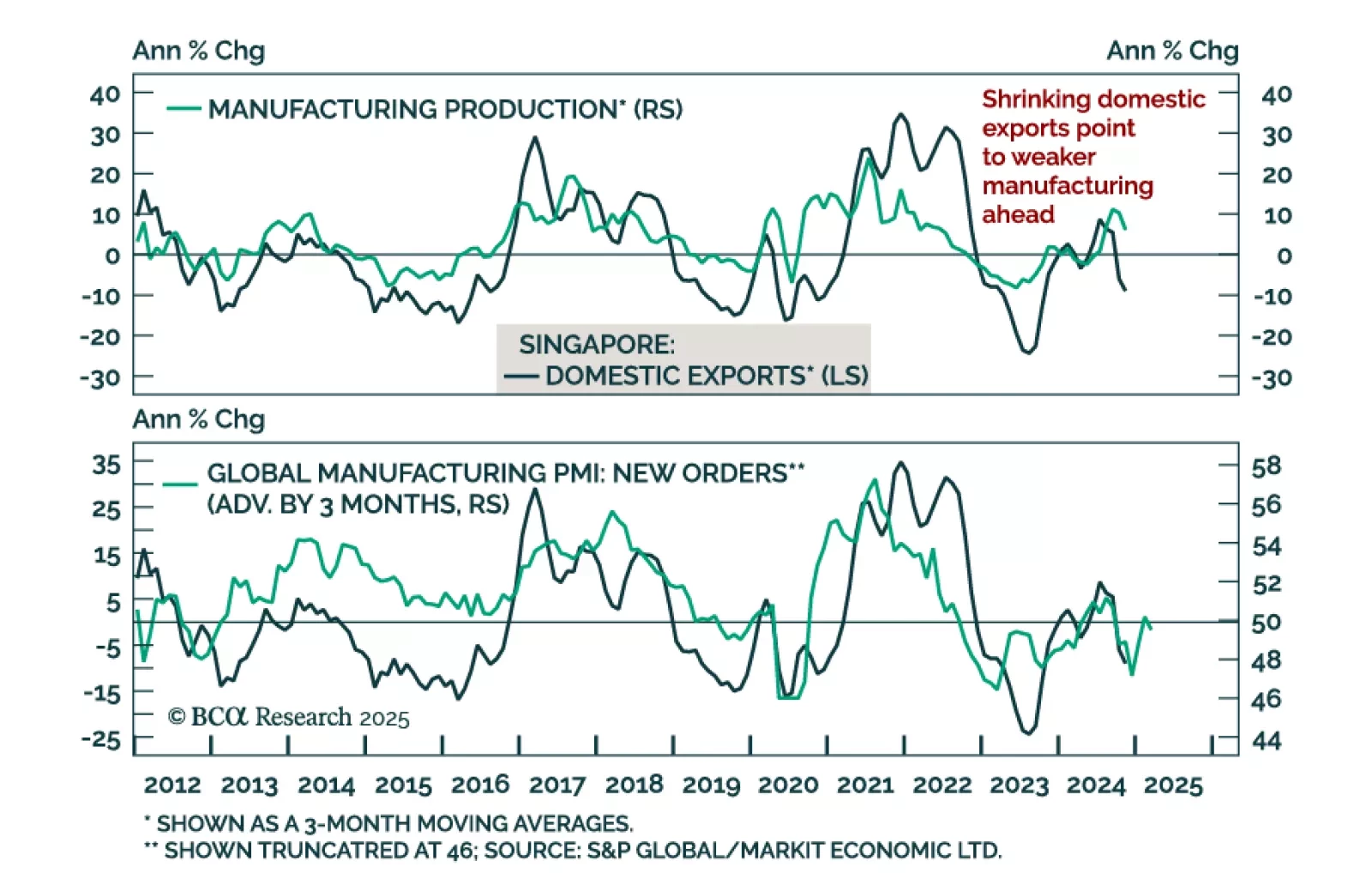

Shrinking Domestic Exports Point

To Weaker Manufacturing Ahead

…