Economy

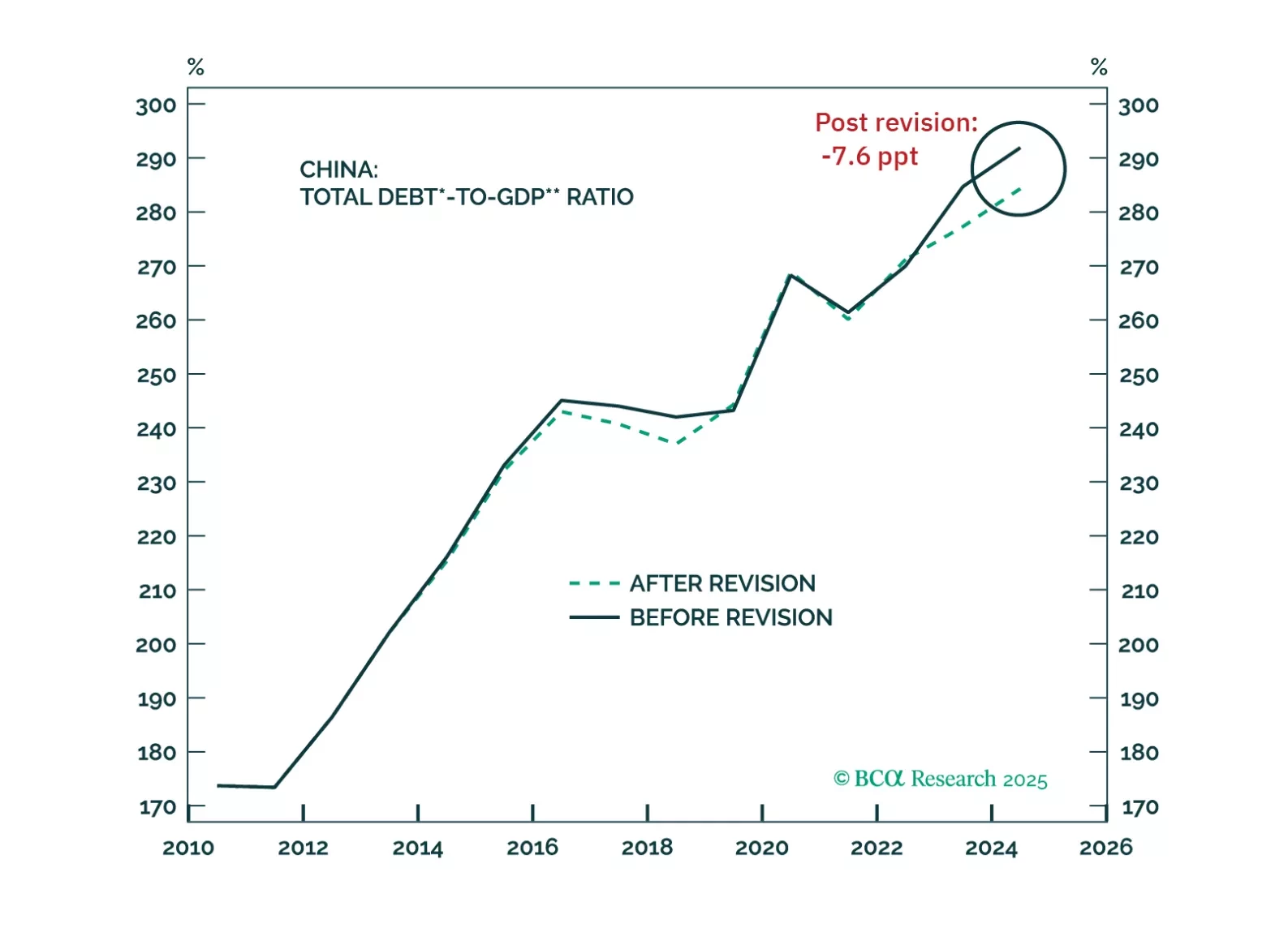

In this week’s report, we present our key takeaways from China's two notable adjustments recently implemented: an upward revision to its 2023 GDP and the reduction of the USD weighting in the RMB Exchange Rate Index.

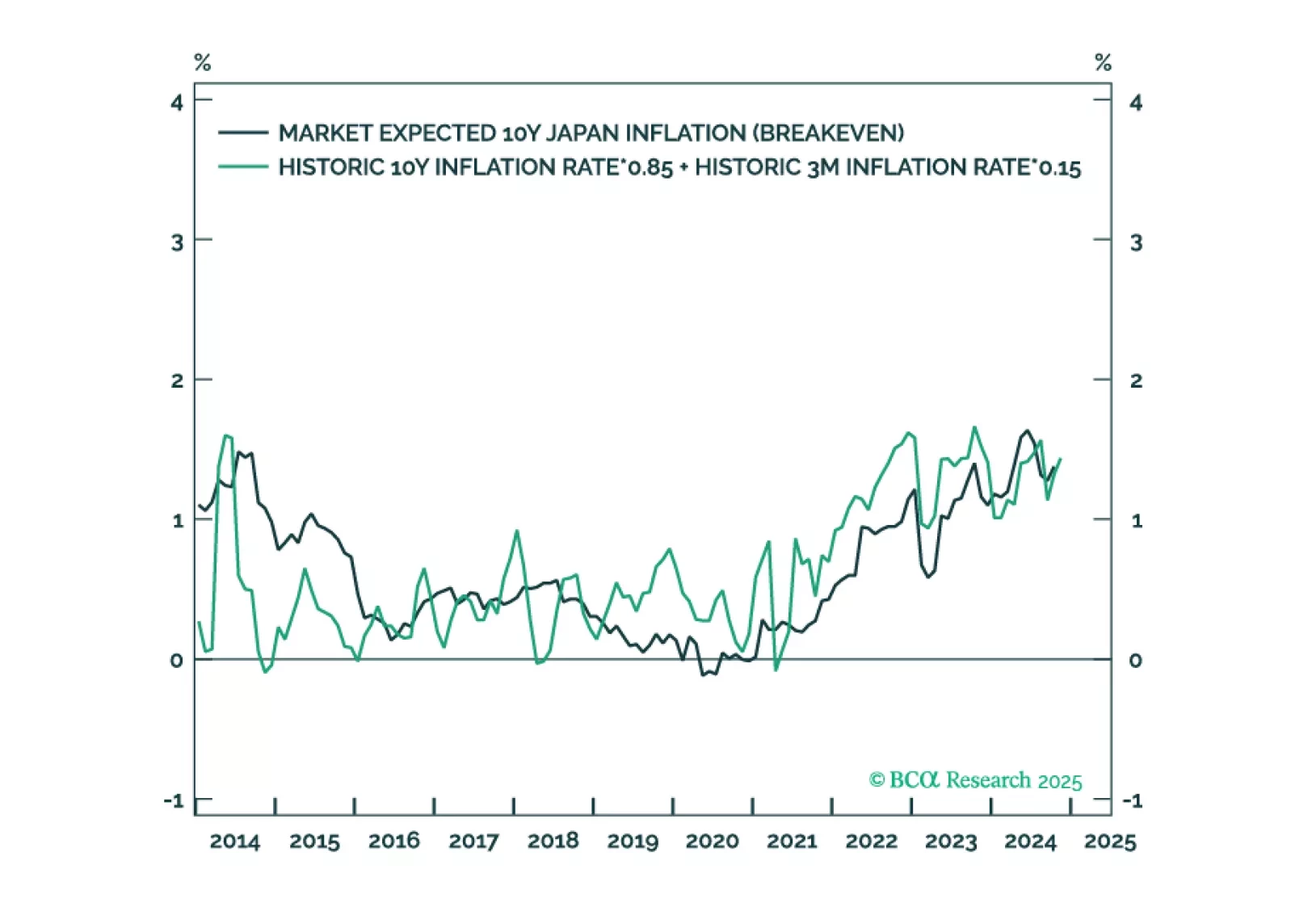

In most developed economies, rising inflation expectations will lift them further above the 2 percent target, limiting the scope for further interest rate cuts. But in Japan, rising inflation expectations will lift them up to the BoJ’s 2 percent target, removing the BoJ’s justification for its zero-interest rate policy. The normalisation of Japan’s monetary policy poses a big structural risk to stocks because Japan has been the main source of financial market liquidity, and thereby, of rising stock market valuations. From a timing perspective though, wait until the complexities of the price trends in USD/JPY and/or Nasdaq versus 30-year T-bond have collapsed. Plus: go tactically long copper.

Our Portfolio Allocation Summary for January 2025.