Economy

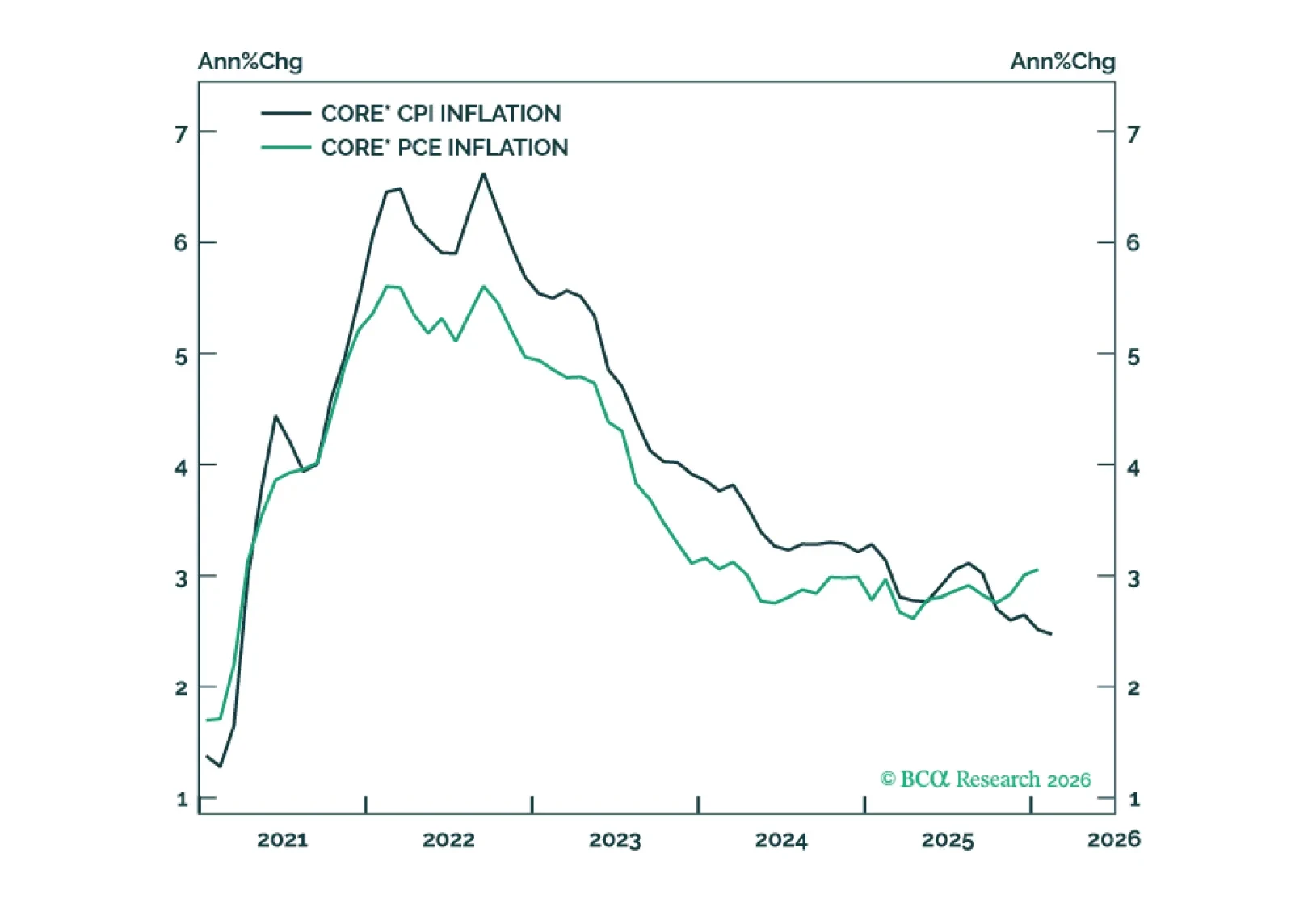

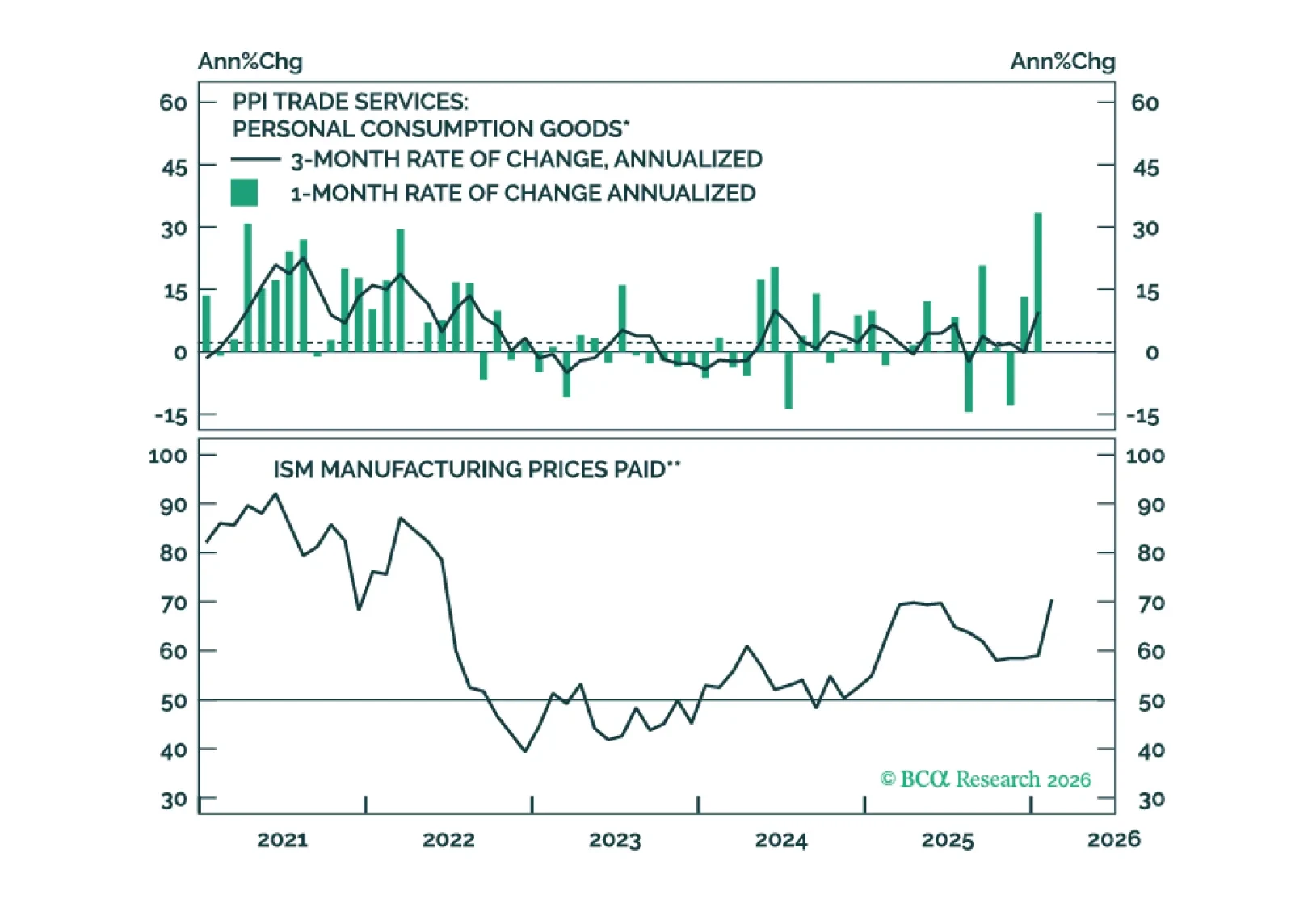

The gap between PCE and CPI inflation will narrow within the next few months, mostly driven by core PCE inflation converging toward its trimmed mean.

The spike in oil and gas prices has raised the odds of a global economic downturn. Combined with a more negative signal from our MacroQuant model, this warrants tactically downgrading stocks from neutral to underweight. Looking further ahead, the Iran war will lead to bigger defense budgets and a greater focus on energy self-sufficiency.

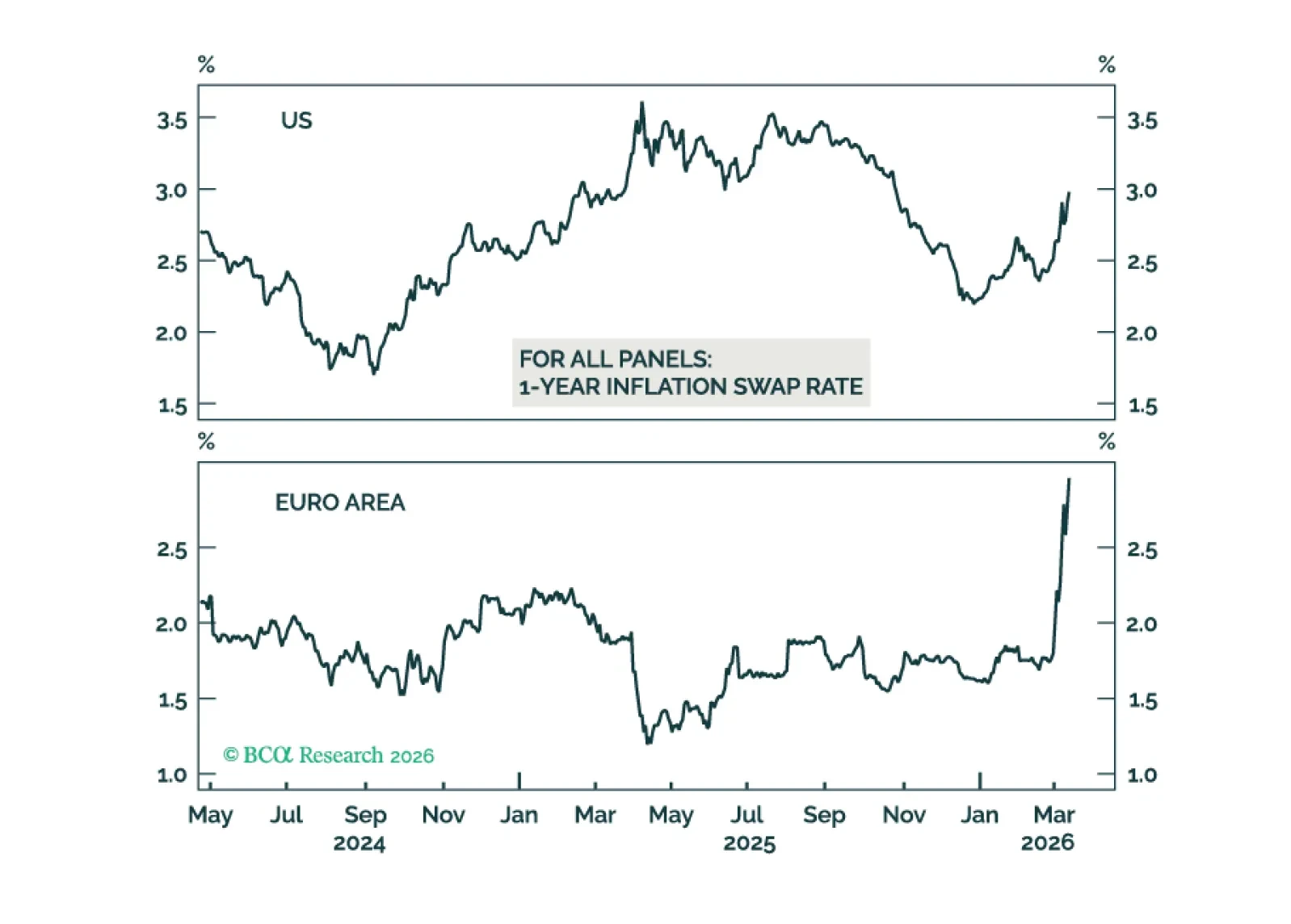

The recent oil price shock reinforces our view that inflation will surprise to the upside during the next few months but fall rapidly in H2 2026.

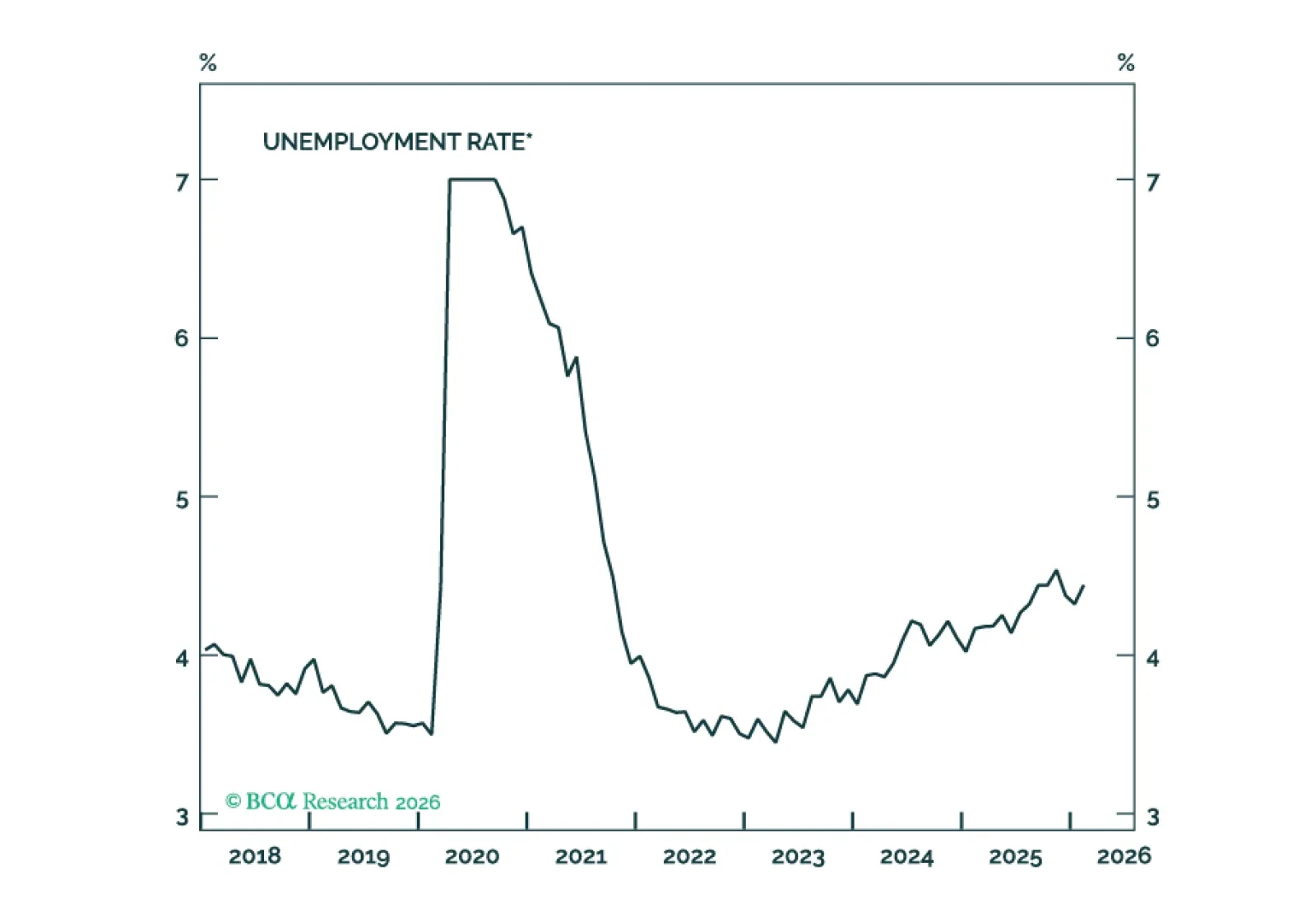

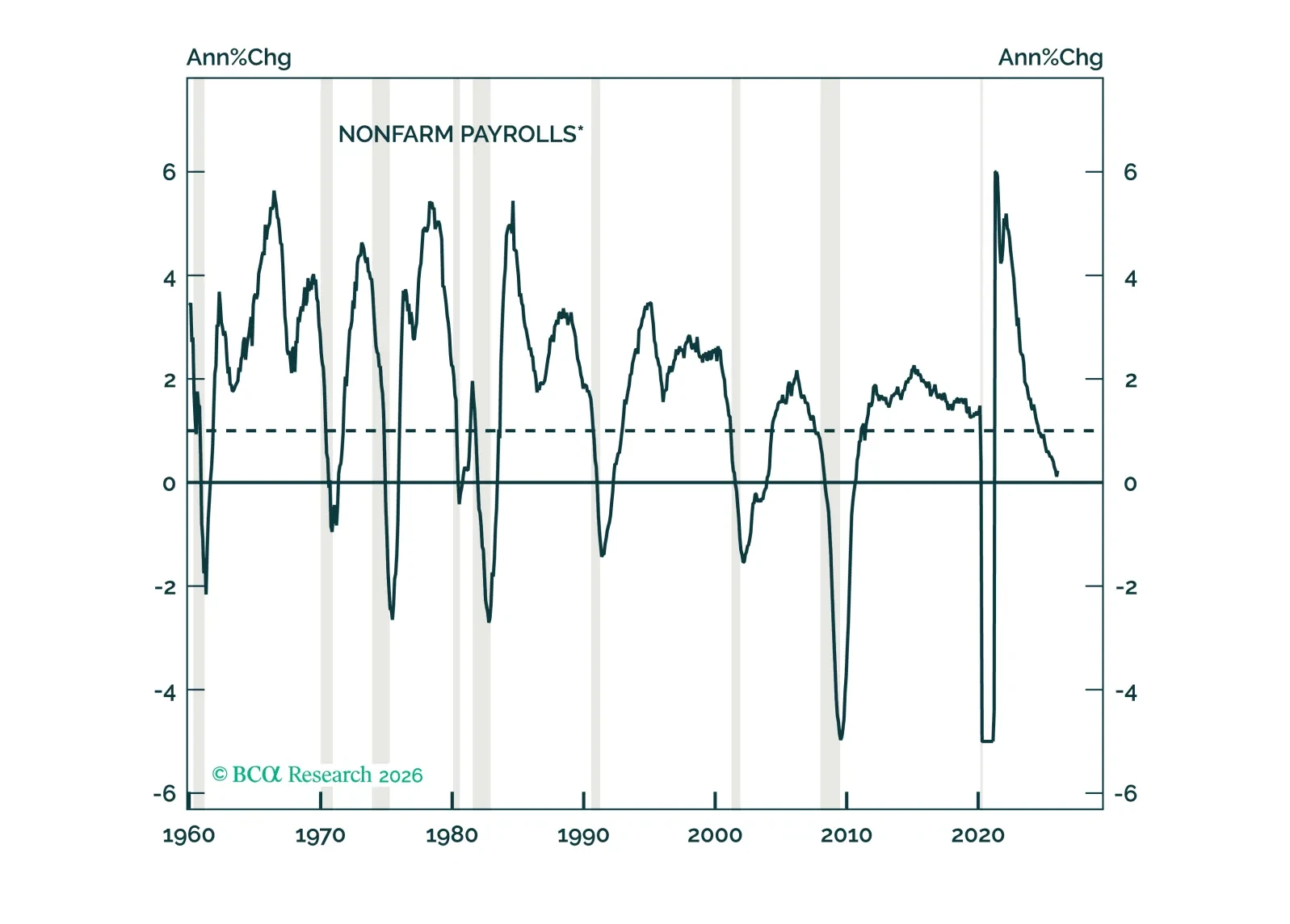

Looking through month-to-month volatility, job growth’s underlying trend is stable and consistent with a flat-to-slightly higher unemployment rate.

Our Portfolio Allocation Summary for March 2026.

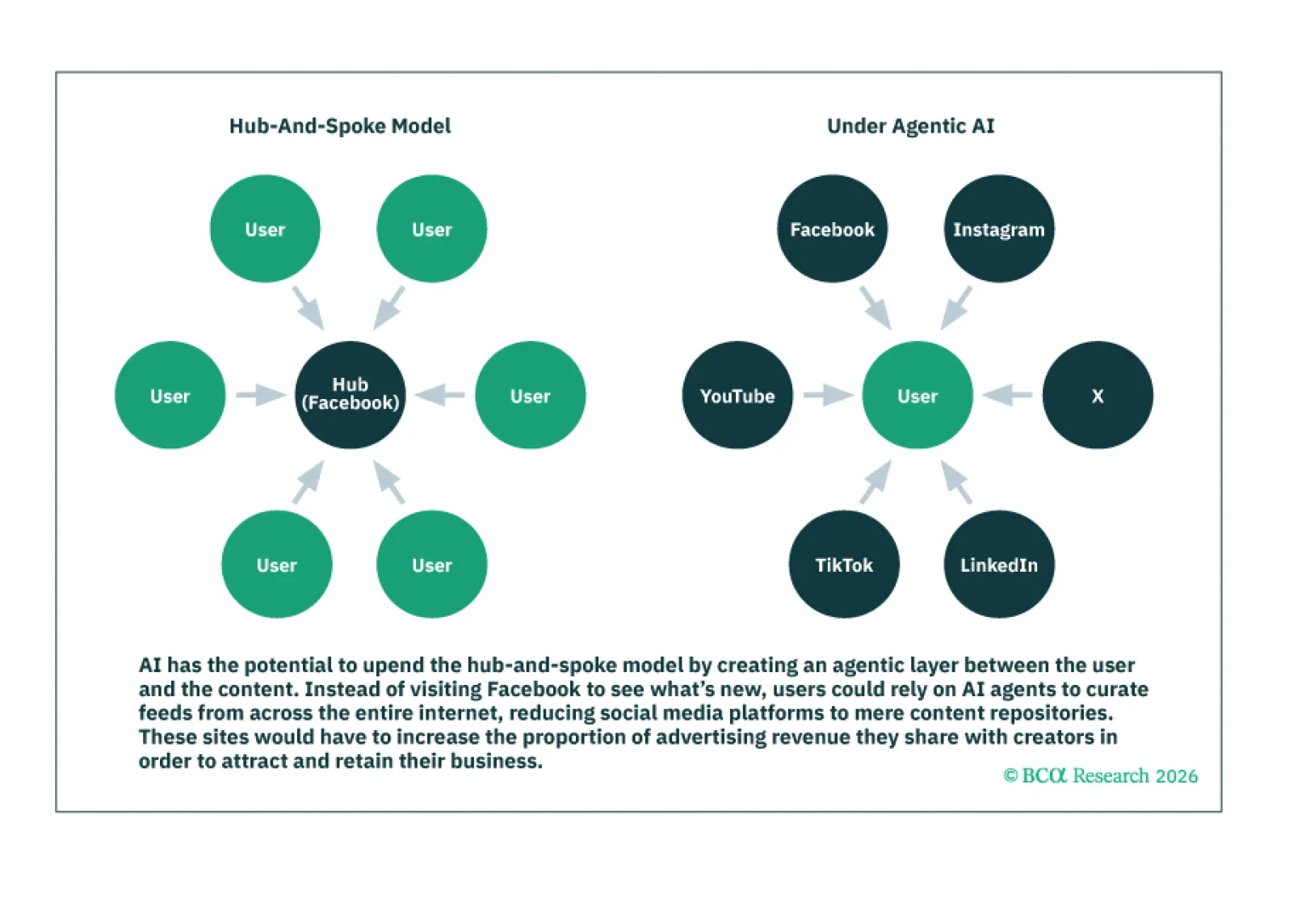

Tech companies have historically generated profits from three main sources: 1) economies of scale; 2) network effects; and 3) proprietary technologies. AI threatens to undercut all three sources.

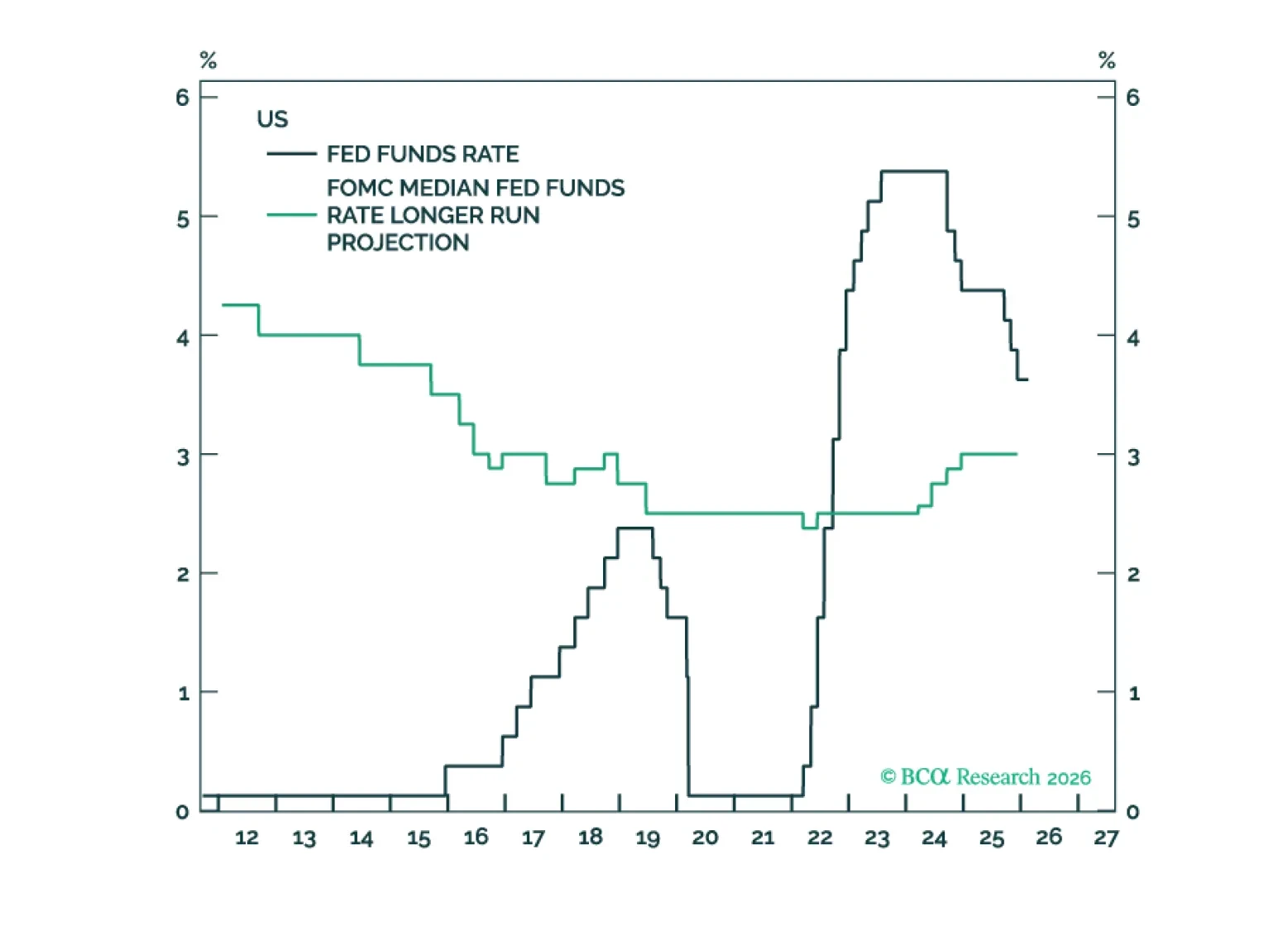

The neutral rate in the US is being propped up by a variety of forces that are at risk of reversing. These include the AI capex boom, large budget deficits, and the extraordinarily high level of household wealth. As such, interest rates are likely to surprise to the downside over the next few years.

The annual benchmark payrolls revisions revealed that the labor market has been weaker for longer than initially reported. The probability that a crack in consumption is just around the corner is much reduced and we have therefore dialed back our recession expectations. Though our asset allocation recommendations remain neutral across the board, we are more optimistic than we were at the beginning of the year.

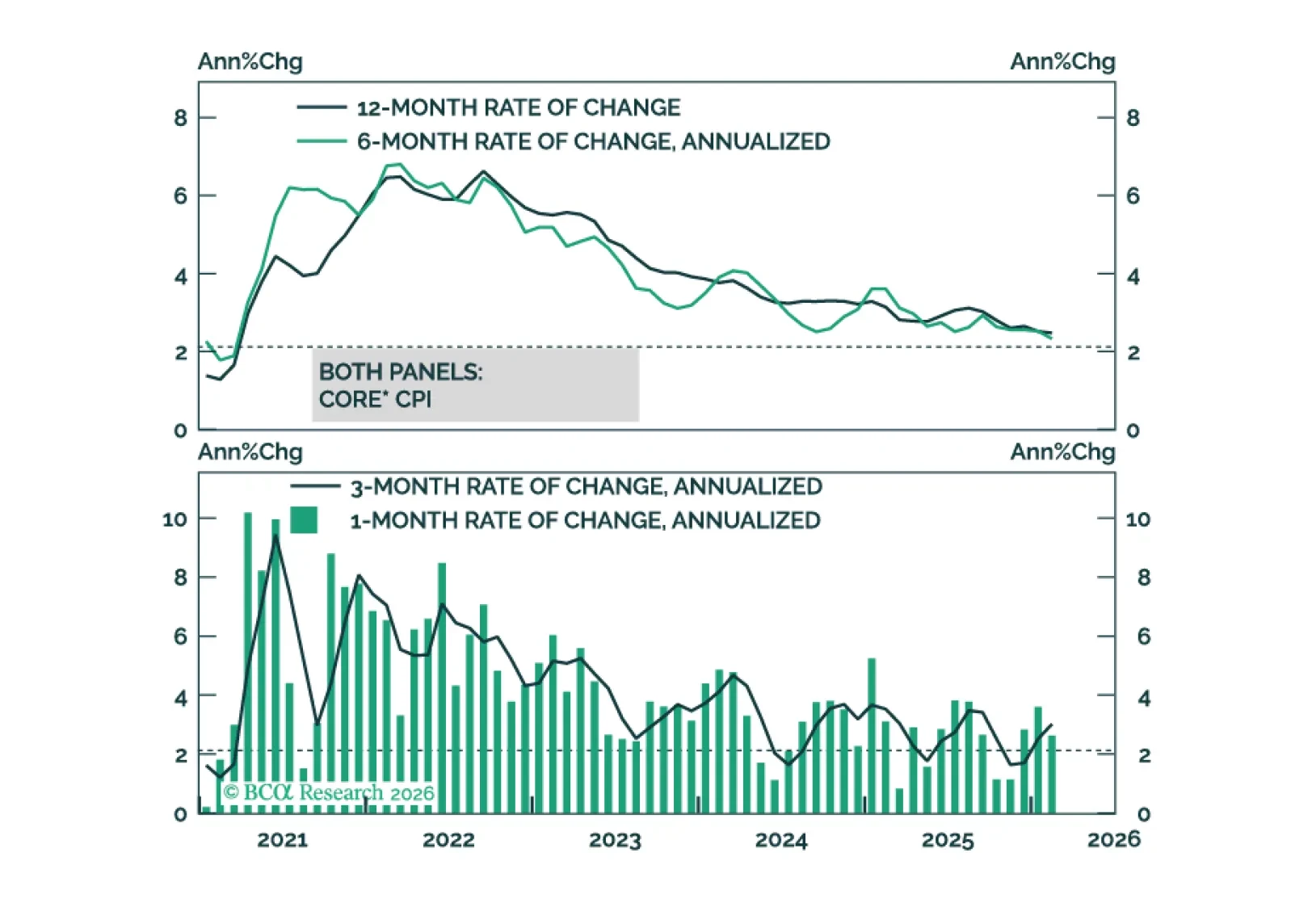

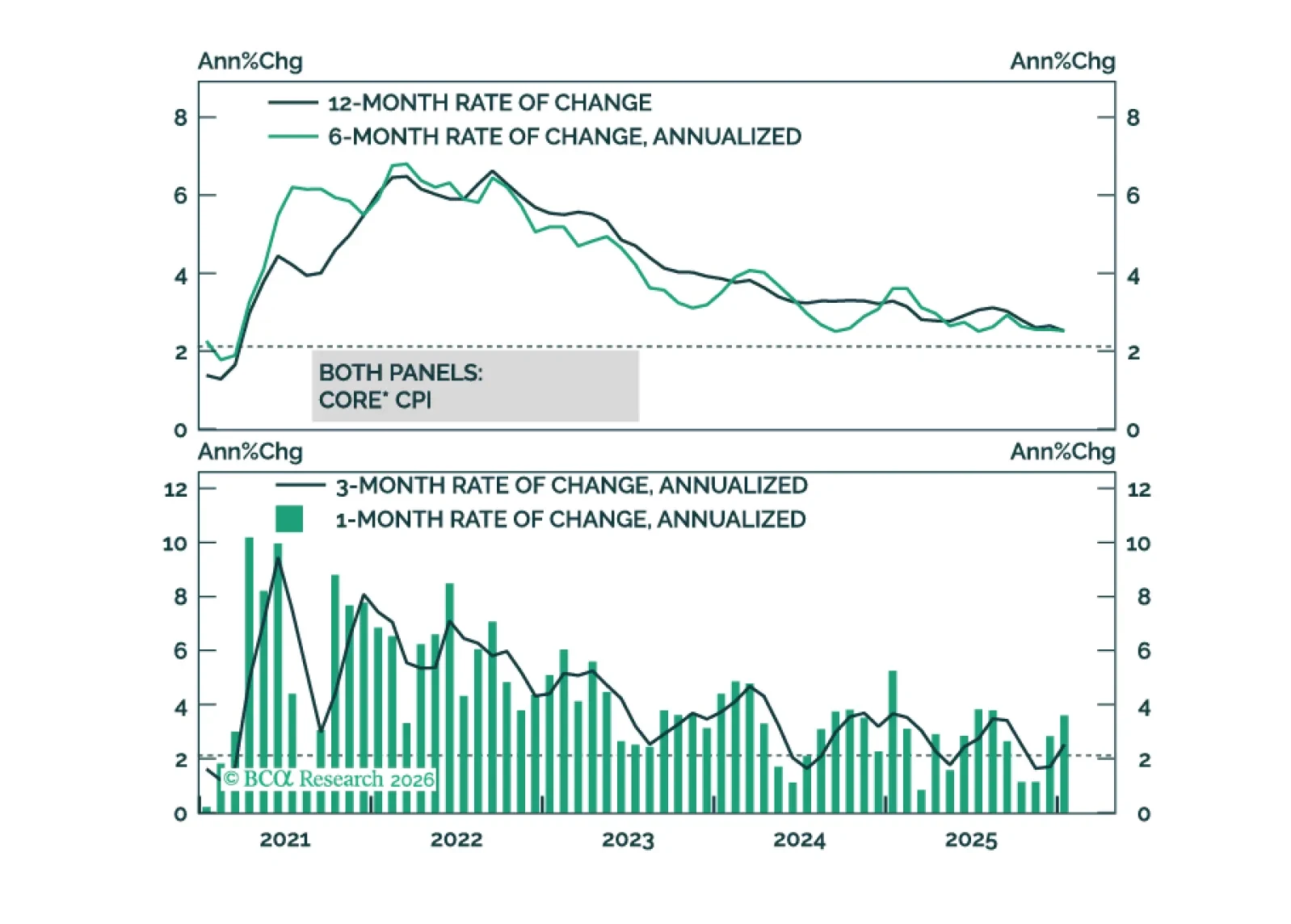

Core inflation will get close to the Fed’s 2% target by the end of this year.

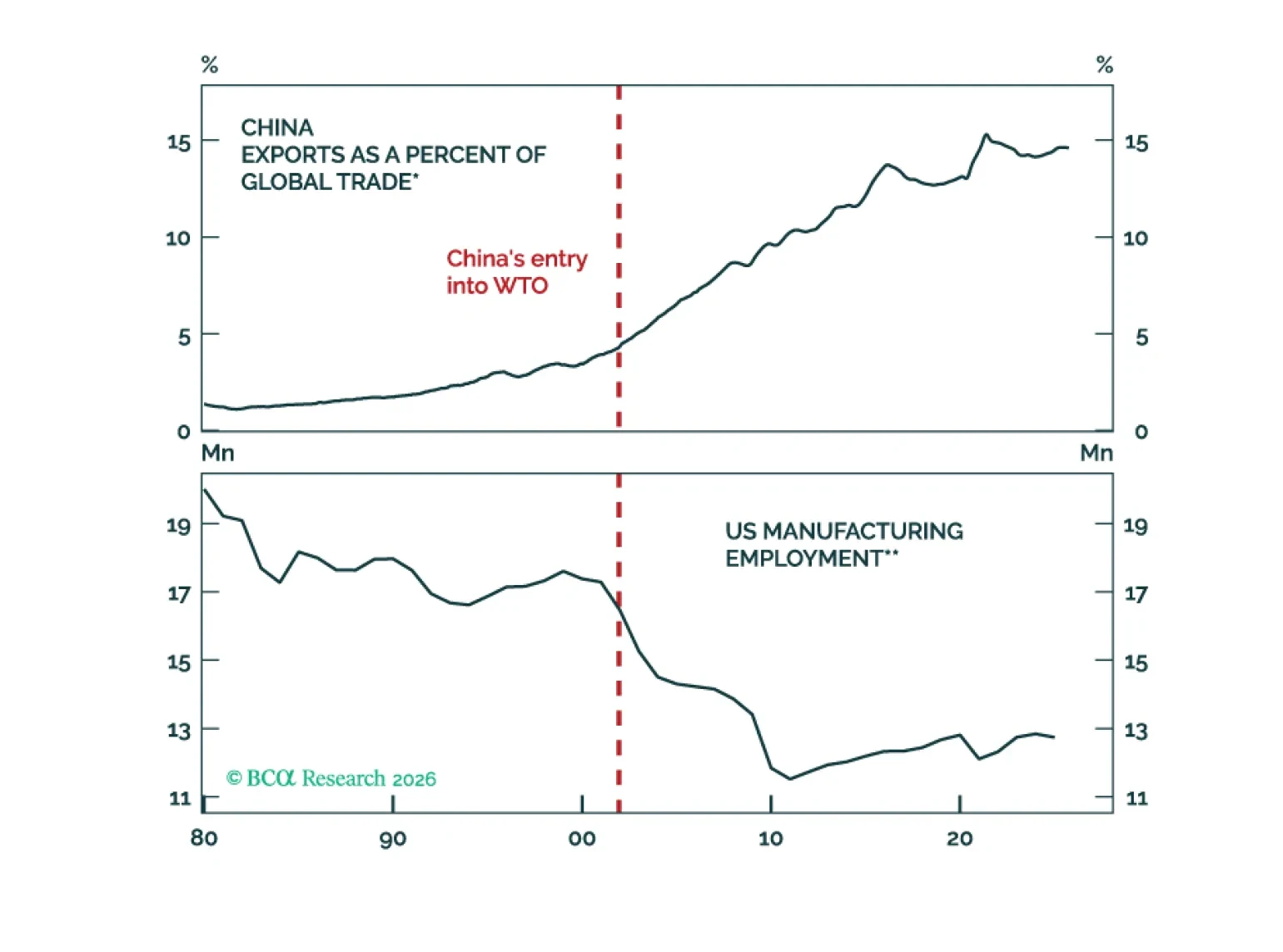

If humanoid robots were to become substitutable for workers, the AI age could lead to rapid growth in the size of the effective global labor force. The result could be a larger version of the “China shock,” which followed China’s entry into the global economy.