Economy

This Strategy Insight presents our view on today’s rate cut by the Bank of England as well as the budget announced by the UK government last week.

The prospect of a new trade war more than offsets the other pro-business parts of Trump’s agenda. With the labor market already weakening going into the election, we are raising our 12-month US recession probability from 65% to 75%.

Our thoughts on the bond market’s reaction to the election and this afternoon’s FOMC meeting.

Our US Political strategists assessed the magnitude of the Republican sweep and discuss the path ahead as they take control of Washington. The GOP sweep was a resounding victory as they also clinched the popular vote. The “Blue Wall” (Wisconsin, Michigan,…

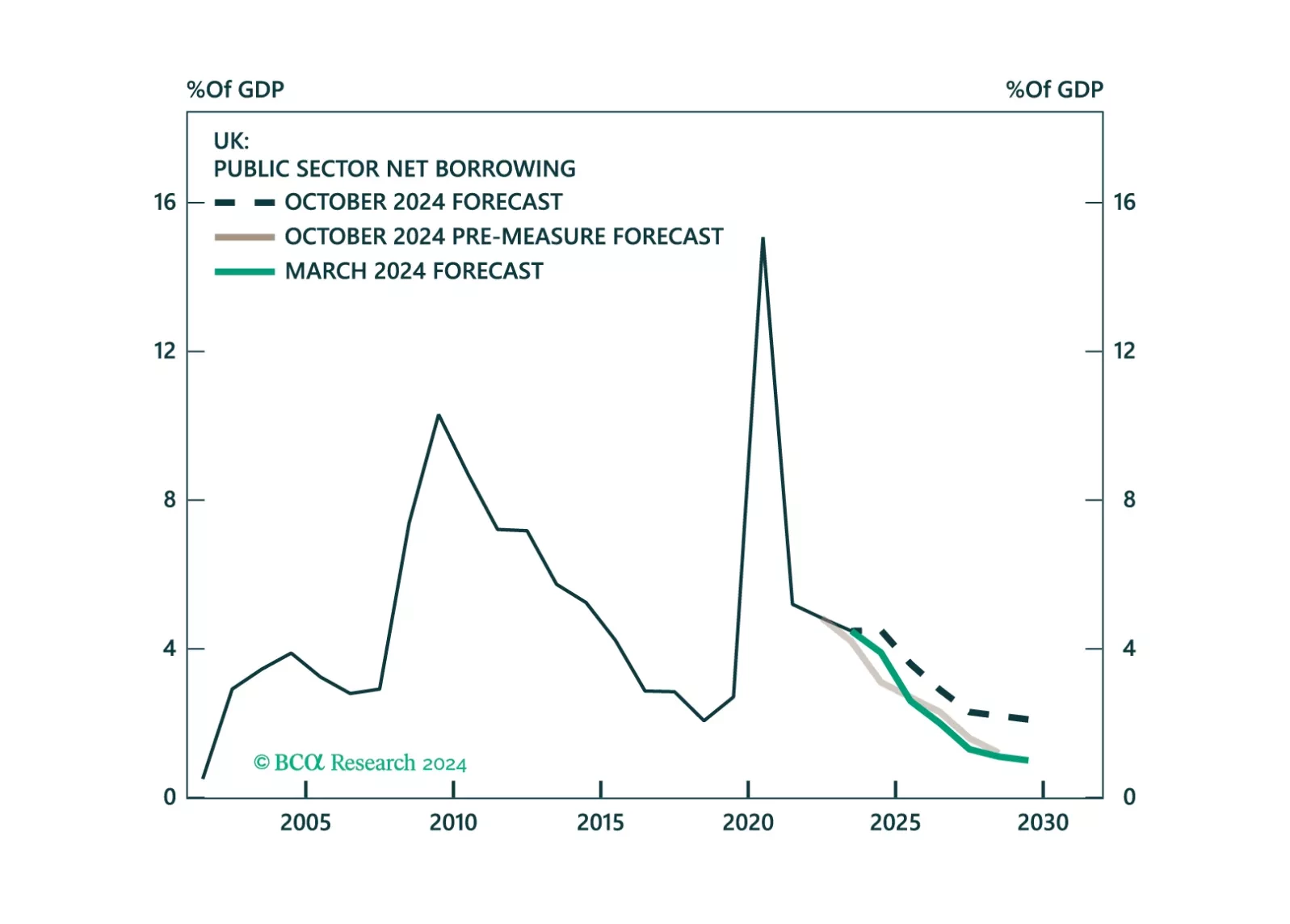

The Bank of England cut its policy rate in line with expectations to 4.75%, but it signaled a more gradual pace of cuts as it increased its inflation forecast following last week’s budget. A 25 bps cut with hawkish guidance strikes the balance the BoE…

The Federal Reserve cut interest rates by 25 bps as expected yet introduced uncertainty on the timing of its next move. The statement was relatively unchanged, except for the removal of a segment from September highlighting they had gained greater confidence…

We spent last week visiting our clients in China. In this report, we share some of the key questions from the client meetings as well as our responses.

Will the prospect of expanding trade tensions lead to more Chinese stimulus, and create an opportunity for Chinese equities? Not necessarily, as the election results were already factored in our EM and China strategists’ views. The Trump victory is not a…

The bond market had long anticipated a Trump 2.0 administration, but bond yields still spiked as a Trump victory materialized. What’s the path ahead for US rates? Our US bond strategists believe 10-year yields can go up further in the near-term, but will…

Although foreseen by our US & Geopolitical strategists, a “Red Sweep” now makes the macro environment more volatile. After convening for our BCA Live & Unfiltered meeting, we offer three main takeaways. First, 2024 is not 2016. To begin with, a…