Economy

President Donald Trump’s political capital is moderate, as he frontloaded his most disruptive policies within the first year.

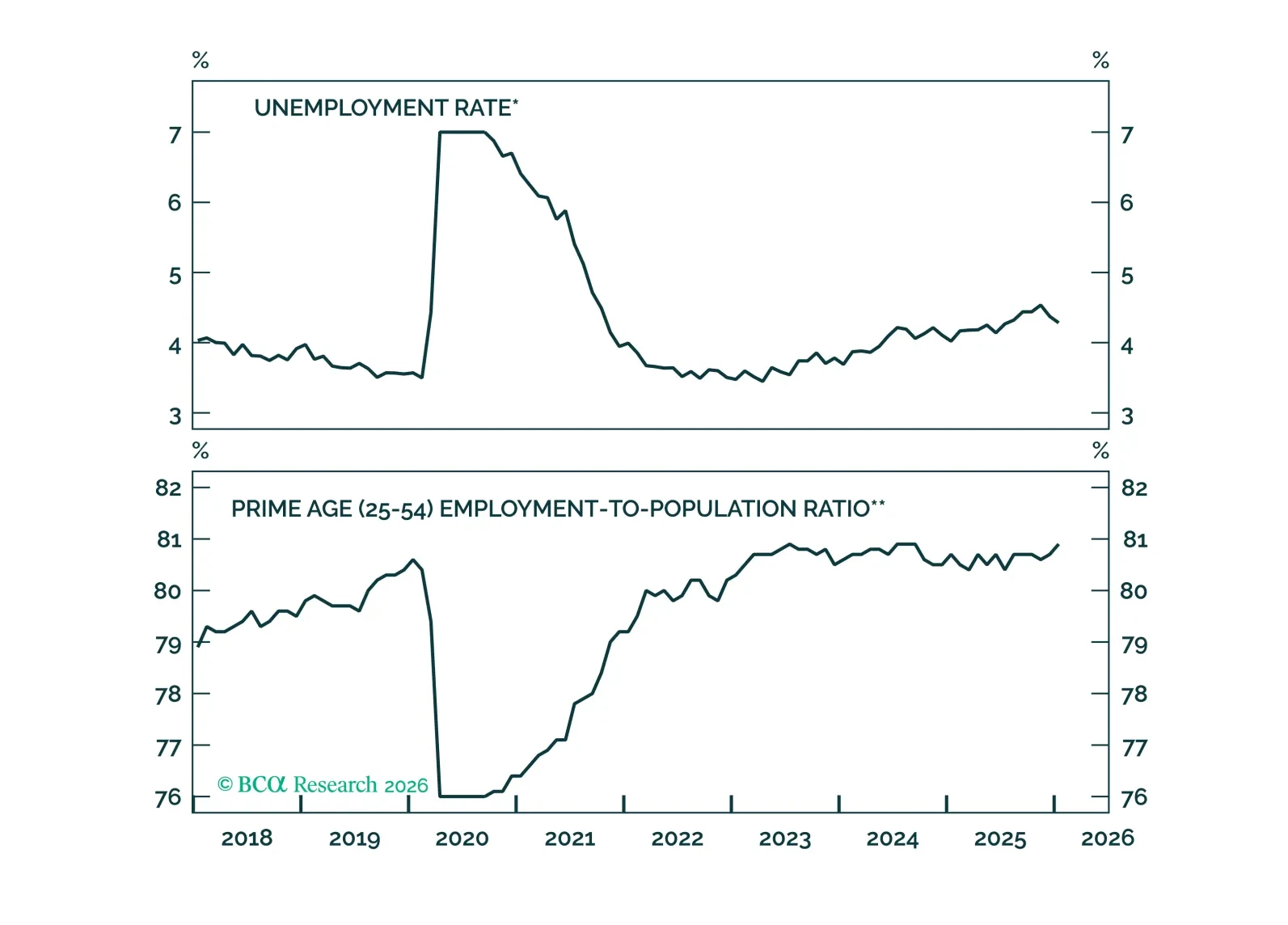

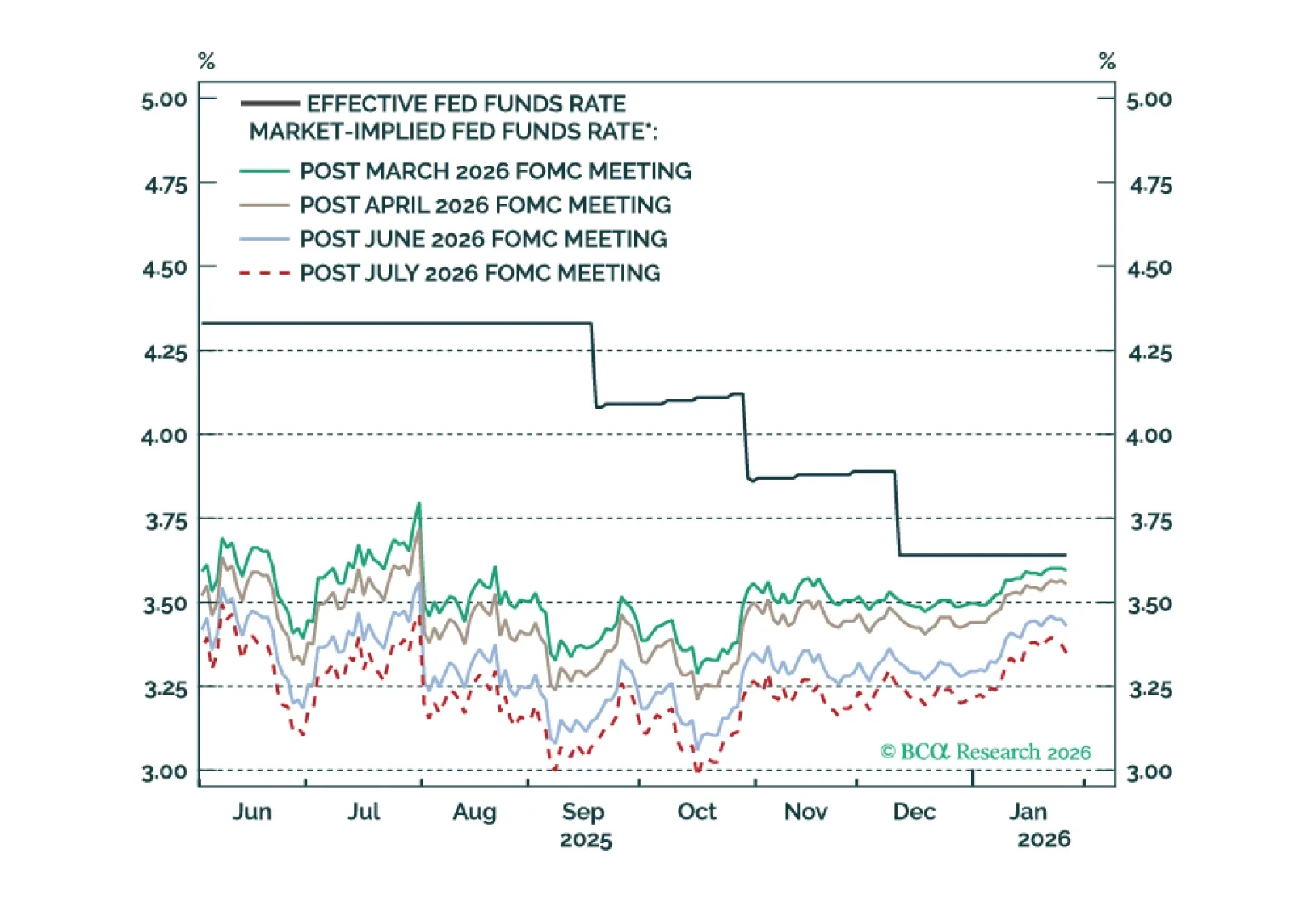

The labor market tightened in January, significantly lowering the odds of a H1 2026 rate cut. Rate cuts driven by lower inflation are still likely in H2 2026.

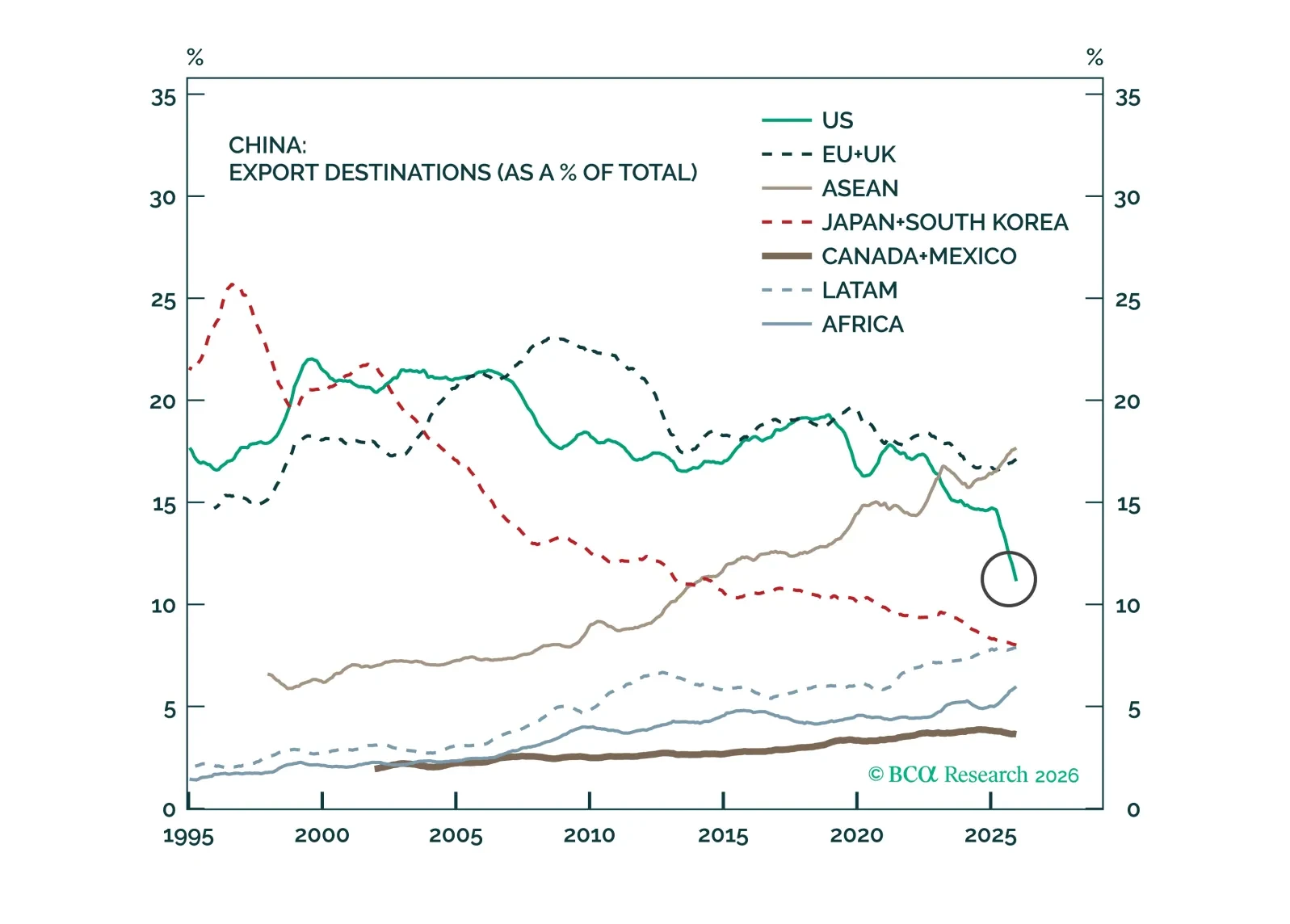

China is providing limited stimulus, promoting tech and trade, and maintaining a tariff truce with the US in 2026. Structural flaws and great power struggle continue to cast dark clouds over the long run.

The US residential real estate market remains soft. While the decline in mortgage rates is a positive, it is too early to bet on housing becoming the engine of growth for the US economy this year.

Our Portfolio Allocation Summary for February 2026.

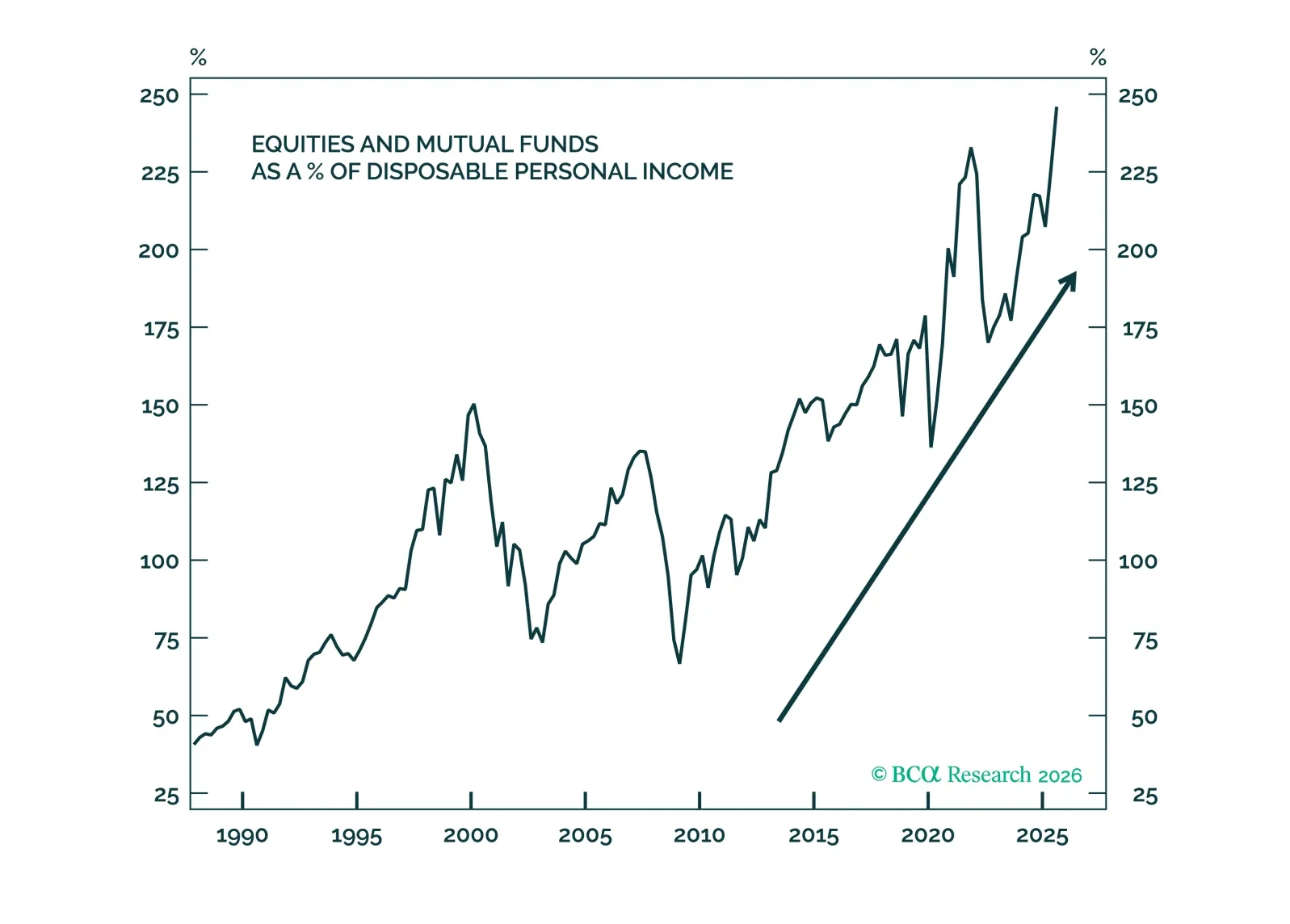

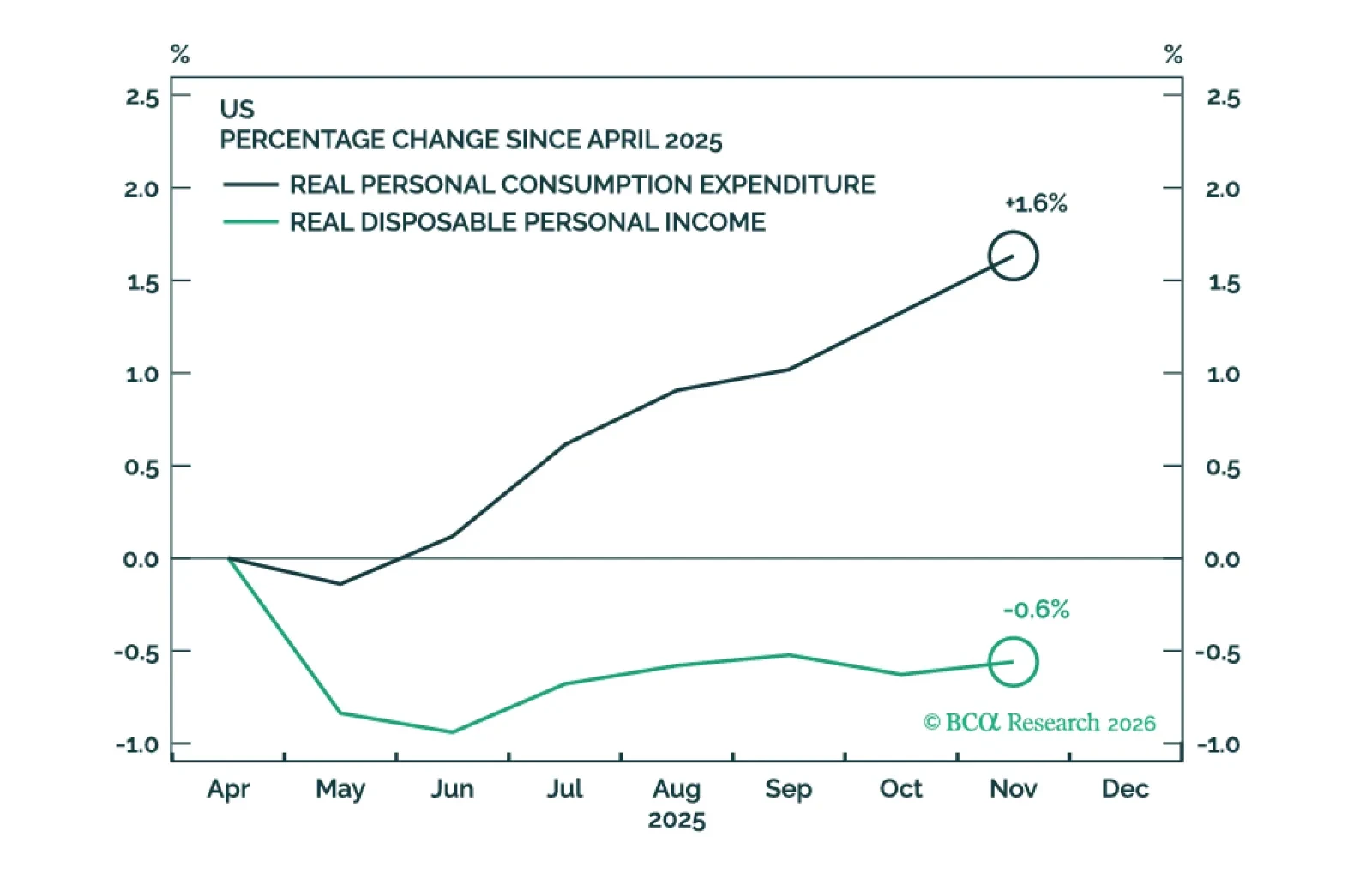

It appears that households have been able to spend more than they’ve earned since May by dipping into their swollen brokerage accounts. Bulked-up equity holdings could herald a future where consumption is more sensitive to stock market ups and downs. That’s great in bull markets but could be an unexpected drag on activity when the next bear arrives.

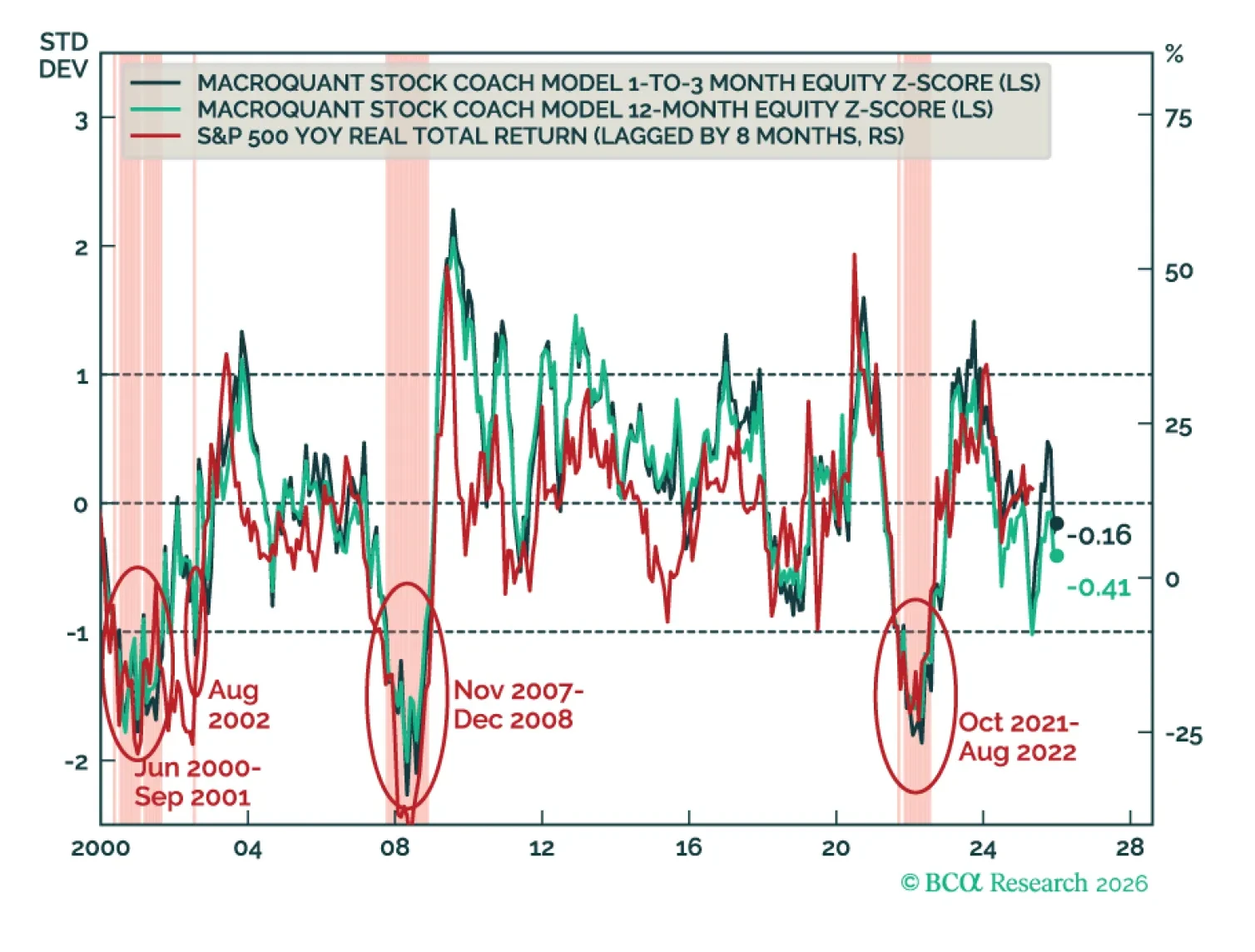

MacroQuant recommends a slight underweight in equities, favors a below-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, has upgraded oil and copper to overweight, and is bullish on gold.

The Fed will keep rates on hold in H1 2026, but dovish policy surprises are likely in the second half of the year.

Recent economic data have been reasonably firm. We will cut our 12-month US recession probability to 40% from 50% if the Supreme Court strikes down President Trump’s tariffs. This would take our scenario-weighted year-end 2026 price target for the S&P 500 to 6375 from 6200.

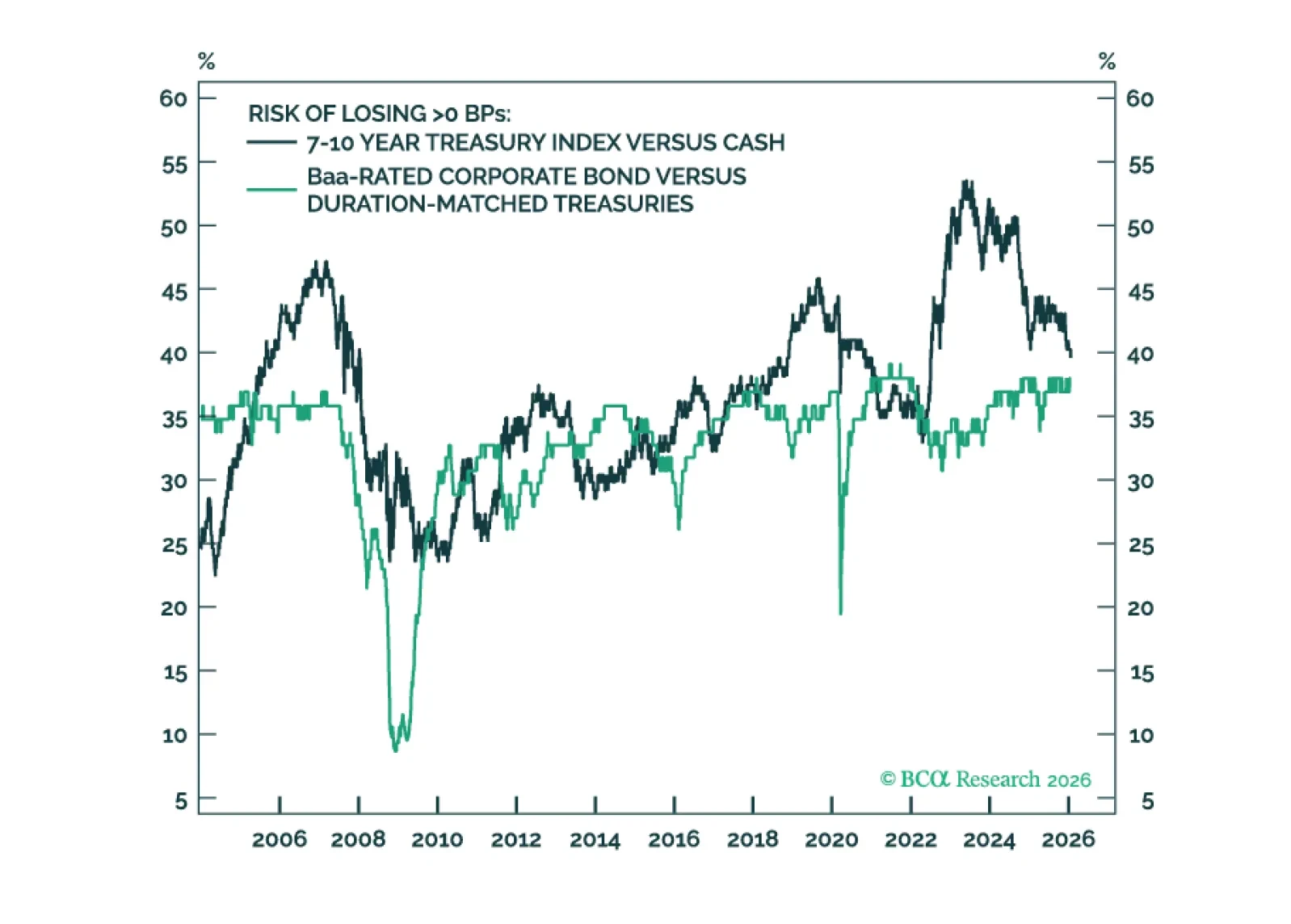

The 10-year Treasury term premium is now competitive with Baa- and Ba-rated credit spreads. Even without term premium compression, duration carry trades could outperform credit carry trades in a low rate vol environment.