Elections

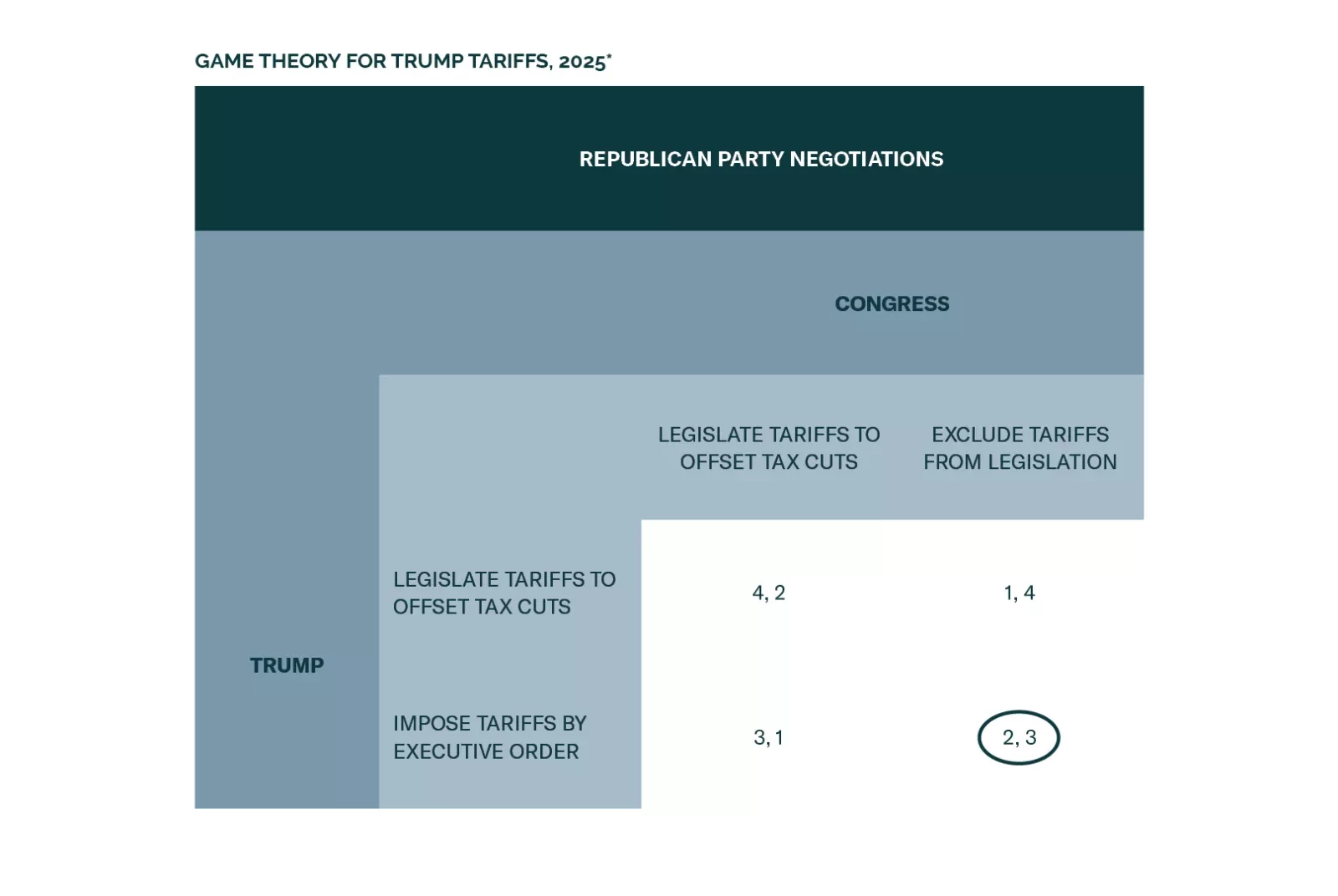

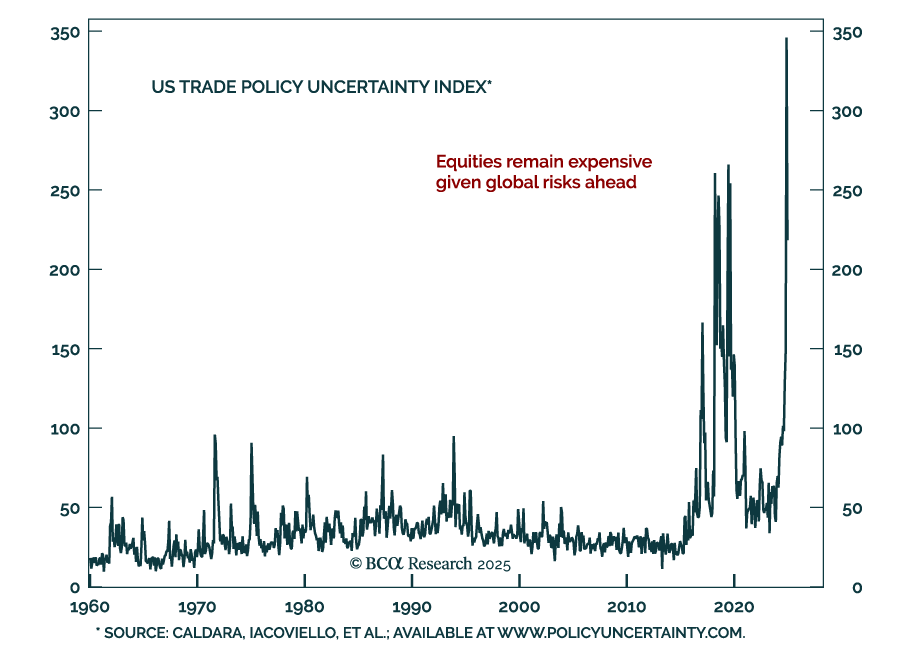

Simple games allow us to model several of the Trump administration’s most disruptive policies in 2025. We find that markets face an increase in volatility as Congress expands the budget, Trump implements tariffs on the world, China retaliates, and Taiwan tensions persist. A ceasefire in Ukraine is a marginally positive outcome for Europe, although it is not a long-term peace treaty.

Our Emerging Markets strategists put together a hypothetical conversation between President Trump and Treasury Secretary nominee Scott Bessent on what economic policy would look like for the Trump 2.0 administration. Secretary Bessent is expected…

President Trump’s inaugural speech outlined his second term agenda. The theme was that the US will become “far more exceptional” than it already is. Trump pledged to reverse America’s decline, rebalance the justice system, streamline government, protect…

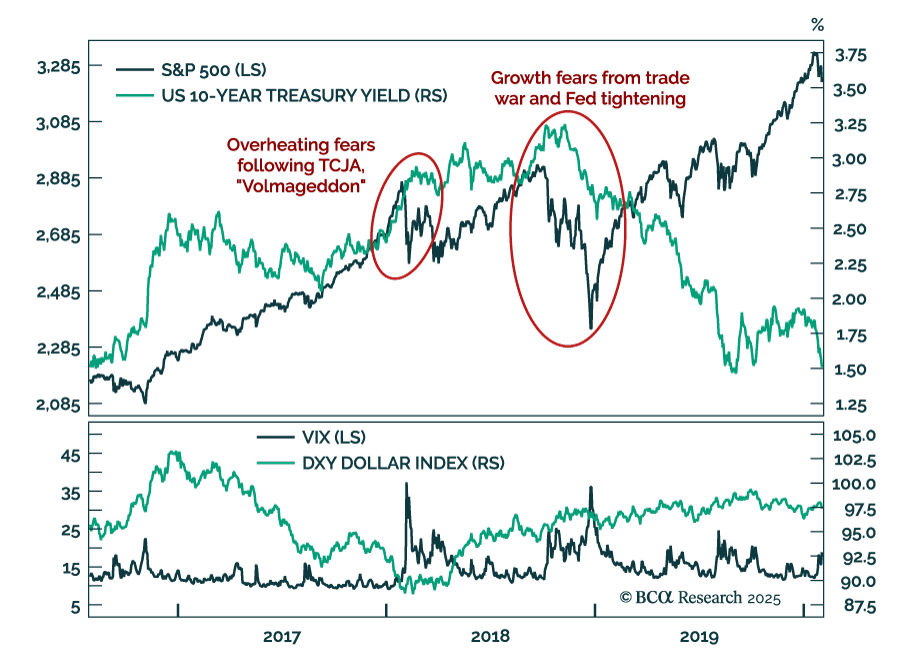

We look at President Trump’s first mandate for lessons on how markets would likely react to different policies. On the fiscal front, the 2017 Tax Cuts and Jobs Act (TCJA) was the first pro-cyclical stimulus in decades. Markets pushed back, as the early 2018…

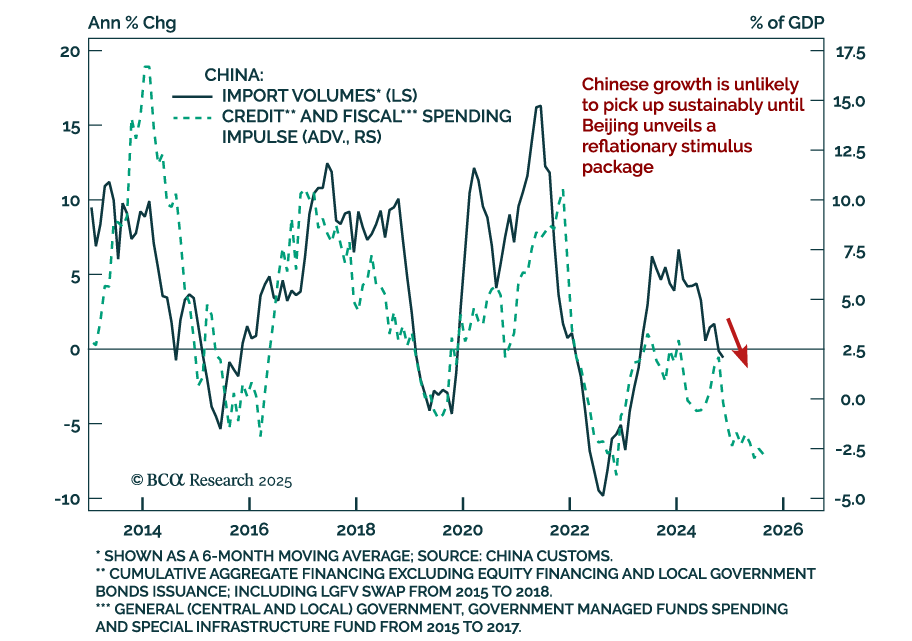

China’s December trade data was positive, with exports in USD terms rebounding to 10.7% y/y from 6.7% in November, and imports rebounding to 1.0% from -3.9%. Taken at face value, the numbers are positive for both the Chinese and global economies. However, our…

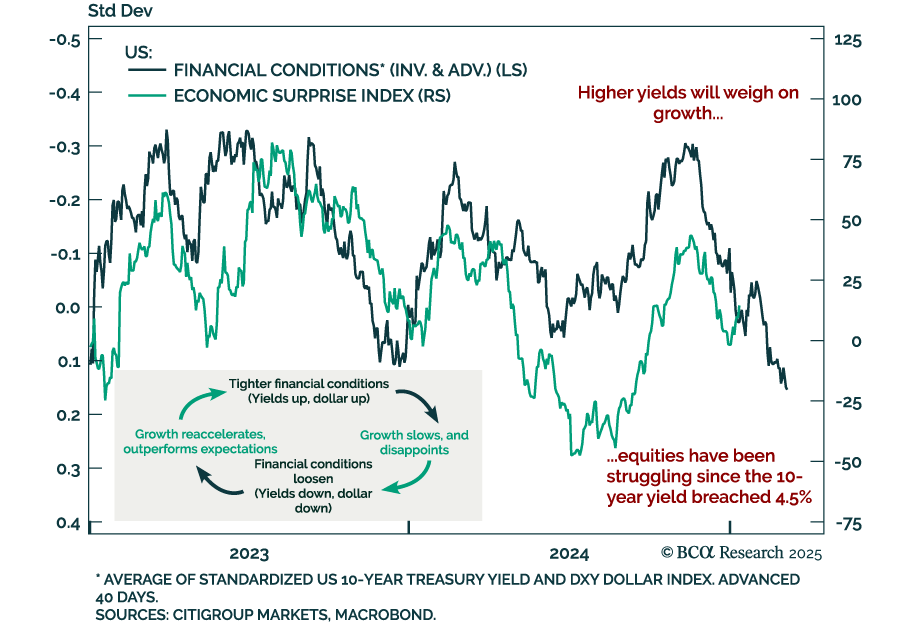

The global economy is subject to numerous cycles displaying reflexivity and feedback loops. One of these is the relationship between financial conditions and growth. Given this relationship, economic strength can plant the seeds of its own demise.Markets are…

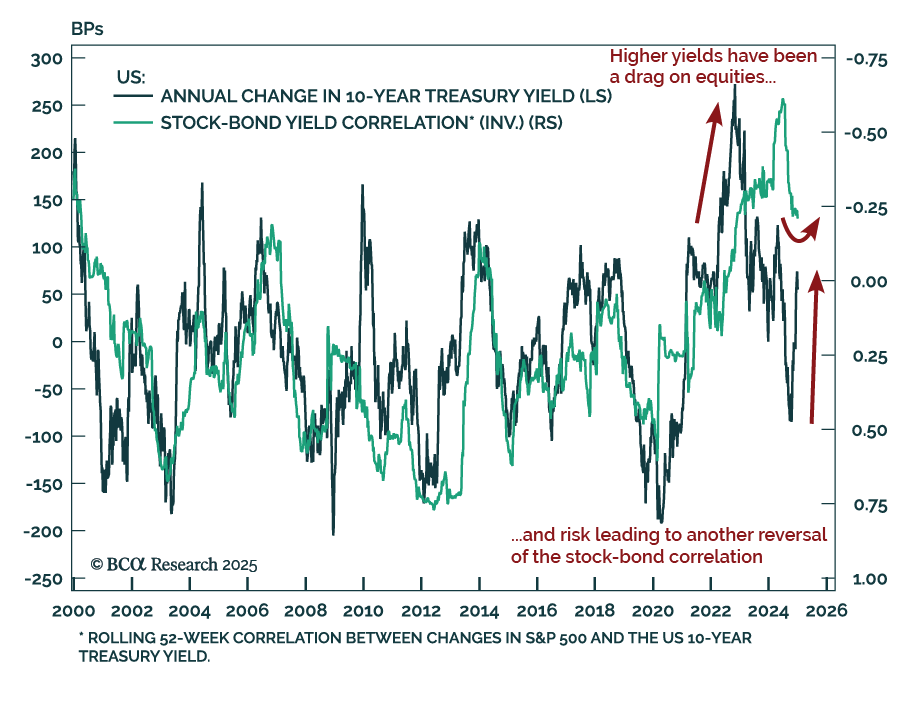

The post-COVID inflation impacted the most important cross-asset relationship: the stock-bond correlation. Higher inflation expectations pushed yields higher, leading to a correction in bond and stock prices. As price pressures receded, bond yields fell and…

Our GeoMacro strategists published their Alpha Report, outlining their view that President Trump will have to pare back his fiscal ambitions to avoid a bond market riot. The long end of the US bond market continues to sell off, reinforcing our…

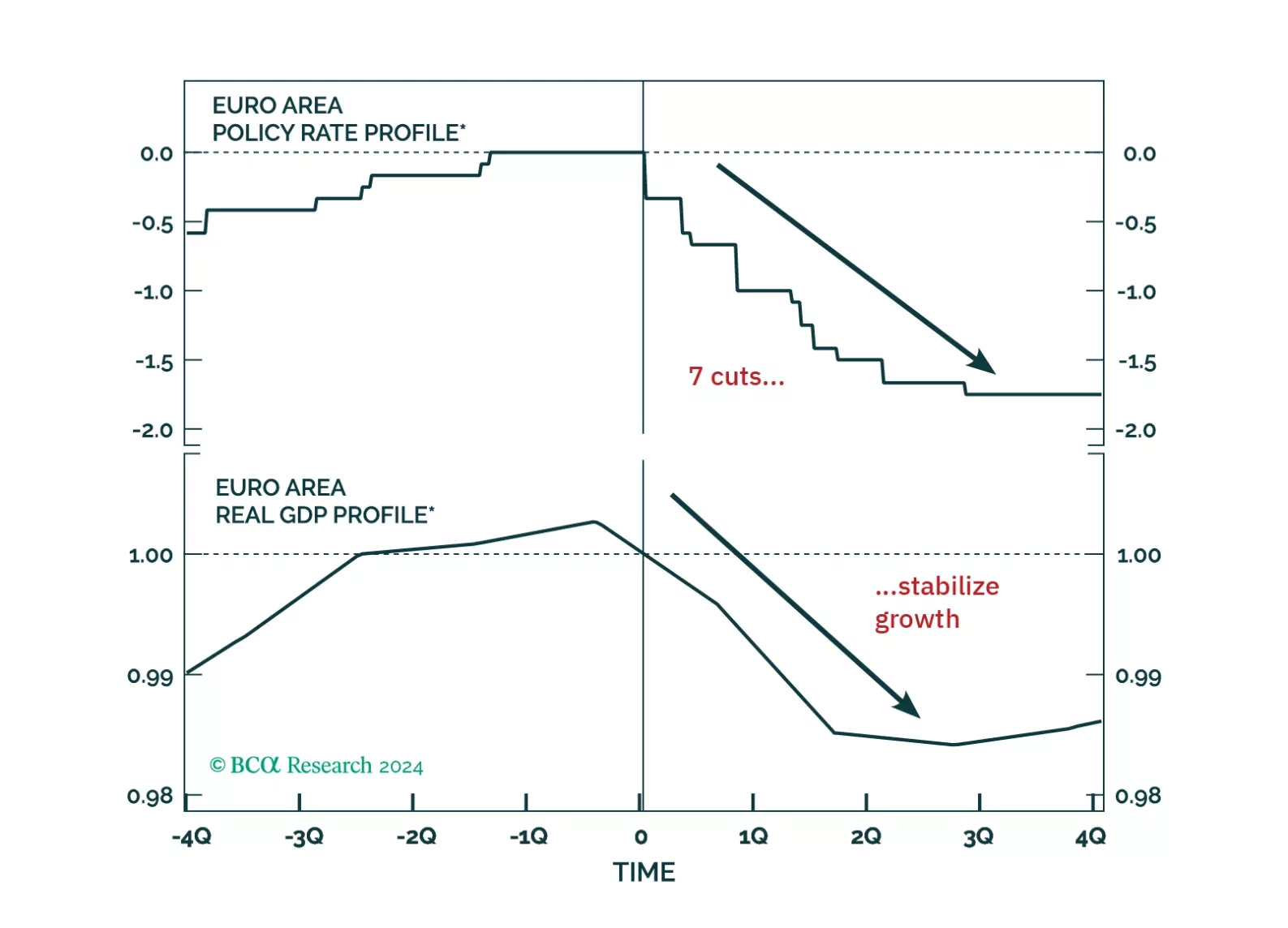

For our last publication of the year, we explore five key themes that will dominate the European macro landscape and markets next year. While the start of 2025 will be challenging for European assets, the latter part will offer some much-needed relief.

Our Geopolitical Strategy team published their annual outlook, and see three trends shaping 2025. First, Congress is expected to pass tax cuts by the end of 2025, providing a fiscal thrust of 0.9% of GDP in 2026. This stimulus will likely…