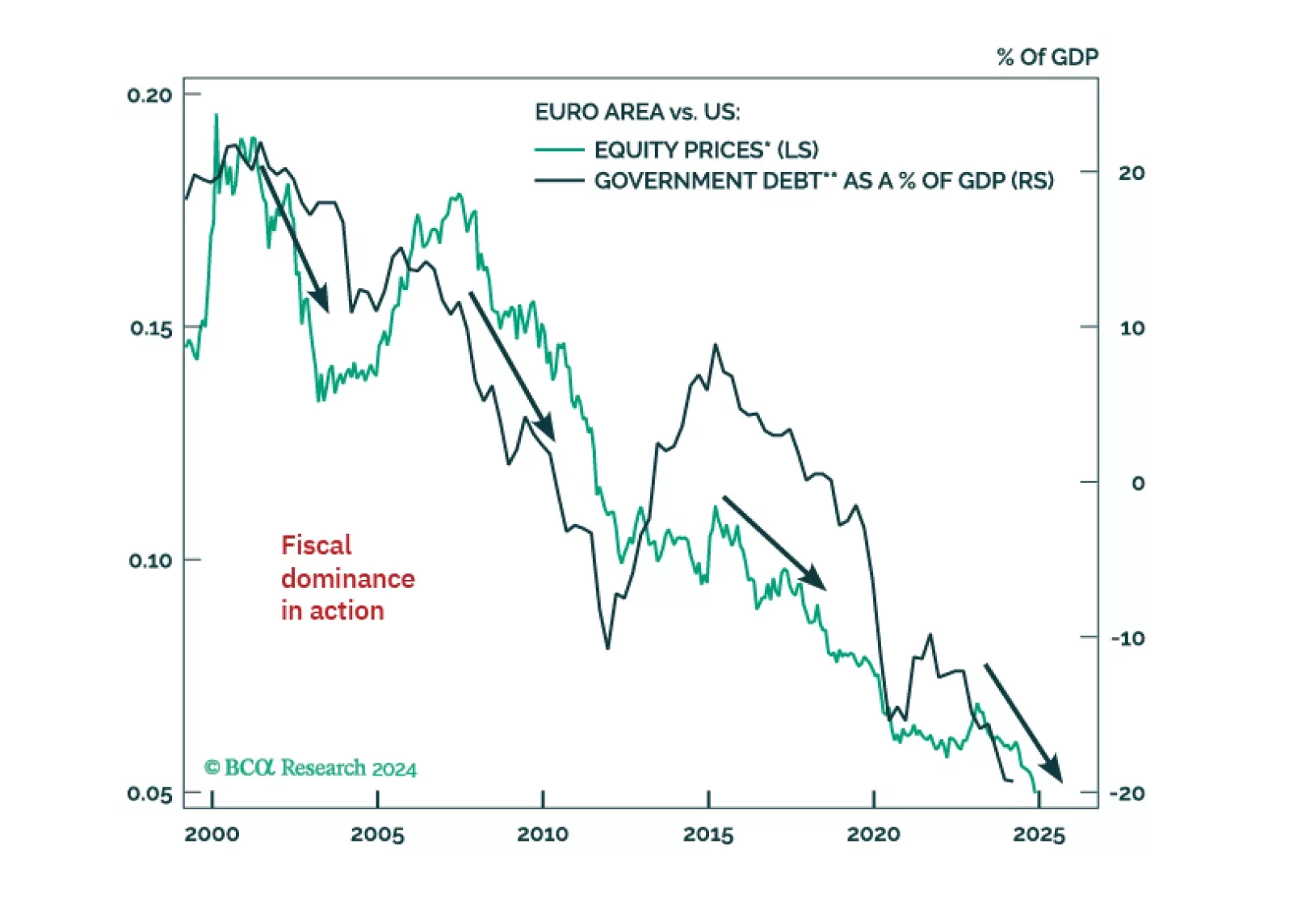

Highlights Portfolio Strategy The strong U.S. dollar is tightening global liquidity conditions, putting the post-election jump in stock prices at risk unless growth imminently accelerates. The spike in large cap industrial stocks represents a massive knee-jerk overreaction and we are adding the sector on our high conviction underweight list. Take profits in the S&P air freight & logistics group and cut to neutral, and downgrade the S&P electrical components & equipment group to underweight. Recent Changes S&P Air Freight & Logistics - Take profits of 6% and reduce to neutral. S&P Electrical Components & Equipment - Trim to underweight from neutral. S&P Industrials Sector - Add to our high-conviction underweight list. Table 1 Feature Equities are still in a post-election honeymoon phase. The savage reaction in the bond market has not yet backlashed onto the broad stock market. Instead it has sparked a rapid and powerful rotation in intra-sector capital flows. The danger is that an unwinding of the momentum trade in the bond market is being misinterpreted as a pro-growth, pro-cyclical investment shift. Investors appear to be equating a potential increase in economic growth with better profitability. However, basing equity strategy on unknown future policies is fraught with risk, as is equating GDP with corporate profits. Trump's signature policies, protectionism and fiscal spending, are inflationary and U.S. dollar bullish, and the timing of implementation and ultimate size of spending programs, remain anyone's guess. In a closed economy driven more by consumption than investment, a strong currency can be supportive via increased purchasing power and a dampening in corporate sector input costs. But what's good for the economy should not be automatically extrapolated through to profits. Net earnings revisions fall when the currency is strong (Chart 1). Capital has won out handily vs. labor since the Great Recession, which allowed profits to boom even though economic growth was below-potential. This is changing. Labor costs are now on the upswing, and productivity has deteriorated. If the economy strengthens, it may only serve to boost wage inflation. If labor expenses accelerate, it becomes even more critical for corporate sector sales to regain traction in order to offset the squeeze on profit margins. However, just under half of S&P 500 sales come from abroad. A strong U.S. dollar means the U.S. will be importing deflationary pressures, undermining pricing power. U.S. dollar appreciation also saps growth in developing countries. Emerging market capital spending is already contracting (Chart 2), and as shown last week, financial strains are flaring back up. Ergo, U.S. companies will be less competitive, and selling into weaker demand growth abroad. Chart 1A Strong Dollar Will Sink Profits... Chart 2... And Hit Global Growth Chart 3 shows that S&P 500 sales typically contract during major dollar bull markets. A recovery has only occurred once currency depreciation occurs. The equity market reaction has been mixed during these periods, as a strong dollar has capped growth and pushed down Treasury yields, supporting a valuation expansion. We do not recommend positioning for a bullish equity outlook, given already overvalued conditions and the rise in government bond yields. It is notable that the inflation component of yields has done the heavy lifting, rather than an upgrading in economic expectations (Chart 4). In other words, there is a sequencing issue, a strong currency saps profits now, while stimulus may only arrive much later. U.S. dollar-based global financial liquidity is now contracting as a consequence of U.S. dollar strength (Chart 4). If excess liquidity and low rates were the argument for supporting high valuations previously, tighter liquidity and rising rates can't also justify current multiples, especially if global growth is soft. As discussed in our November 3, 2014 Special Report, currency strength favors a mostly non-cyclical, domestically-oriented portfolio structure. One of our favored themes over the past few months has been to tilt portfolios in favor of domestic vs. globally-oriented industries. With the U.S. dollar breaking above its trading range, a catalyst now exists to spur an imminent recovery in the domestic vs. global share price ratio. The latter had become extremely oversold as the U.S. dollar consolidated and the Chinese economy began to stabilize, but economic fundamentals are shifting decisively back in favor of the U.S. The U.S. PMI is already making small strides vs. the Chinese and euro area PMI (Chart 5, second panel), heralding a rebound in the cyclical share price momentum. Chart 3No Sales Recovery Ahead Chart 4Tighter Liquidity, Rising Inflation Chart 5Domestic Will Beat Global World export growth remains anemic, and world export prices continue to deflate, albeit at a lesser rate. Sagging Asian currencies warn that trade is at risk, over and above protectionist rhetoric and/or policies. When compared with the reacceleration in U.S. retail sales, the outlook for domestic-sourced profits is even brighter. We reiterate our theme of tilting to domestic vs. globally-oriented industries. The bottom line is that the outlook for the broad averages has soured as a consequence of a strong dollar, rising yields and the prospect for tighter Fed policy. These dynamics augur well for domestic vs. global bias, small vs. large caps and defensive vs. cyclical sector strategy. This week we are taking some cyclicality out of our portfolio following the wild market gyrations in the past two weeks. Taking Advantage Of The Industrials Sector Overreaction... Industrials have vaulted higher, in relative terms, on the back of hopes for rampant fiscal stimulus and infrastructure spending as far as the eye can see, ignoring any negatives that may arise from protectionist policies and tighter monetary conditions. While defense contractors may see an increase in activity (we continue to recommend an overweight in the BCA defense index), in aggregate, the surge in the large cap industrials sector is an opportunity to retool exposure from a position of strength. Large cap industrials companies garner approximately 45% of their revenue from outside the U.S. The industrials sector has the second worst track record among all sectors during U.S. dollar bull phases, trailing only the materials sector. Regression analysis shows that industrial sectors sales would contract by 4.5% for every 10% in the trade-weighted dollar (Chart 6). Without revenue growth, it is hard for industrial companies to generate good profitability, given high operating leverage. The U.S. dollar surge is a direct threat to any benefit from an increase in domestic infrastructure spending. Commodity prices key off the U.S. dollar. Emerging markets (EM) are also sensitive to the currency. A strong U.S. dollar undermines income in commodity producing countries, creates financial strains related to EM foreign currency denominated debt and reins in domestic liquidity in countries that need to intervene to stop their currencies falling too far lest capital flight and inflation occur. As noted last week, emerging market currencies are already rolling over, and CDX spreads have begun to widen (Chart 7). EM equity markets are underperforming the global benchmark, reinforcing the lack of a regional growth impulse (Chart 7). It is rare for the industrial sector to deviate from relative EM equity performance. There has been no evidence of EM deleveraging, and the back up in global bond yields represents a financial stress. If U.S. industrials stocks are a high-beta play on EM, then contrarians should beware recent sector action. Chart 6Top-Line Trouble Ahead Chart 7Sell The Spike Importantly, capital spending is in retreat. Business investment is a function of confidence and expected return on investment. The gap between the return on and cost of capital is narrowing fast (Chart 8). Free cash flow is paltry, especially in resource sectors, major industrial sector end markets. It is hard to envision a major capital spending turnaround if the U.S. dollar keeps climbing and the cost of capital backs up further. Policy ambiguity will act as a weight for at least the next few quarters. During this period, the negative profit impact of the contraction in private and public sector construction activity will ultimately re-exert a major influence on sector risk premia. It will take at least several quarters before any hoped for fiscal spending will benefit industrial companies. Industrials sector pricing power has shifted from a deep negative to neutral. However, that appears to represent an unwinding of the rate of change shock more than a resumption of conditions conducive to companies lifting selling prices. Chart 9 shows that capital goods import price are still deflating. As the Chinese currency devalues, putting downward pressure on its regional counterparts, deflationary pressures will re-intensify for U.S. industrial firms (Chart 9). Chart 8Fiscal Stimulus Is Needed... Right Now! Chart 9The Dollar Will Do Damage ...By Selling Electrical Components & Equipment ... In terms of specifics, were we not underweight machinery shares already, we would institute a high conviction underweight today. In addition, the S&P electrical equipment and components (ECE) index looks equally vulnerable. While less exposed to commodity prices than machinery stocks, ECE shares have benefited alongside the overall sector from the post-election buying frenzy. Hefty short positions likely played a large role in powering the spike (Chart 10), and we are uncomfortable with paying a premium valuation for a dubious earnings outlook, particularly given the sector's brutal long-term track record during U.S. dollar bull markets (Chart 11, top panel, the currency is shown inverted). From a cyclical perspective, it is premature to position for a reversal in the relative earnings bear market. New orders for electric equipment are sensitive to EM currency movements. The current message is that new orders are likely to languish (Chart 11). Relief is not imminent from domestic sources. Chart 11 shows that real investment spending on electrical equipment is contracting at a steep rate. That is consistent with the trend in overall construction spending, which represents a long-term headwind. It is no surprise that industry productivity growth is contracting (Chart 11), reinforcing that the path of least resistance for profits is lower. It would take a major resurgence in top-line growth to restore productivity to positive levels. The ECE industry is one of the few 'smokestack' parts of the economy to have added capacity in recent years. That is confirmed by persistent growth in ECE wage inflation (Chart 12). Without a pickup in demand, this backdrop is conducive to ongoing deflation (Chart 12, bottom panel). Sell into strength. Chart 10Short Covering Will Not Last... Chart 11... As Fundamentals Erode Chart 12Cost Structures Are Too High ...And Taking Profits In Air Freight Stocks ... Elsewhere, we are taking profits on our overweight S&P air freight & logistics index. While we only recently went overweight in early-September, a much shorter time horizon than our desired cyclical calls, we are concerned that the index has front run an improvement in global trade that may be slow to materialize. Our upgrade was predicated on a tightening in inventories relative to GDP, which boosts the need for just-in-time air freight services, as well as a pickup in emerging markets activity. However, our confidence in the latter has been shaken. Air freight stocks are a reflation play, and a surging U.S. dollar is a threat to global liquidity (Chart 13). Global revenue ton miles have already crested after a muted rebound (Chart 14, second panel). Chart 13A Reflation Play Chart 14Take Profits Moreover, protectionist/anti-globalization sentiment may heat up, representing a risk to a recovery in global trade. The IFO export expectations index continues to sink, a warning for relative forward earnings estimates (Chart 14). The contraction in transport and warehousing hours worked confirms that transport activity is not yet on the mend (Chart 14). Relative performance has a history of violent oscillations, and the price ratio has soared to the top end of its multiyear range. Thus, even though the structural increase in online sales bodes well for long-term growth, and value remains appealing, we are booking profits and reducing positions in this globally-exposed group back to neutral in order to de-risk in our portfolio. Bottom Line: Take profits of 6% in the S&P air freight & logistics index and reduce to neutral. Downgrade the S&P electrical equipment index to underweight and add the overall industrial sector to our high conviction underweight list. The ticker symbols for the stocks in these indexes are: BLBG: S5AIRF - UPS, FDX, CHRW, EXPD, and BLBG: S5ELCO - AME AYI EMR ETN ROK. Current Recommendations Current Trades Size And Style Views Favor small over large caps and growth over value.