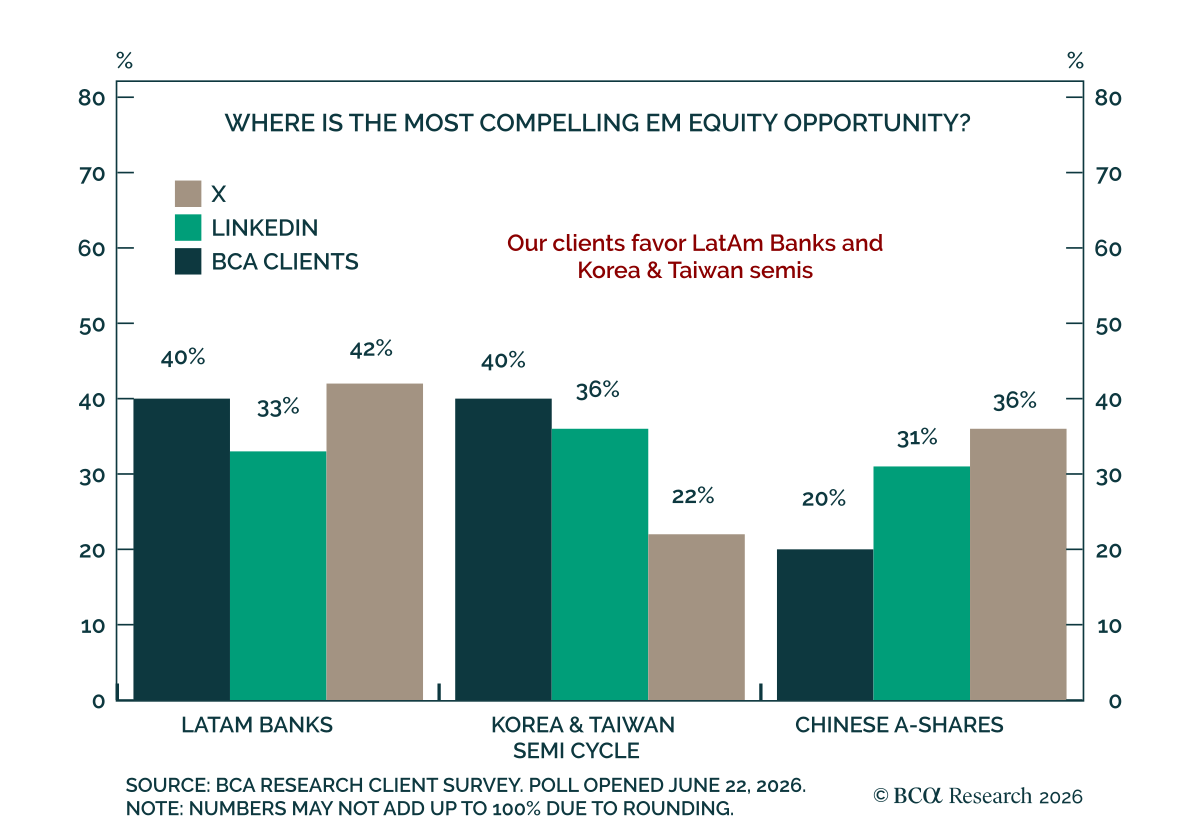

Emerging Markets

Our Portfolio Allocation Summary for July 2026.

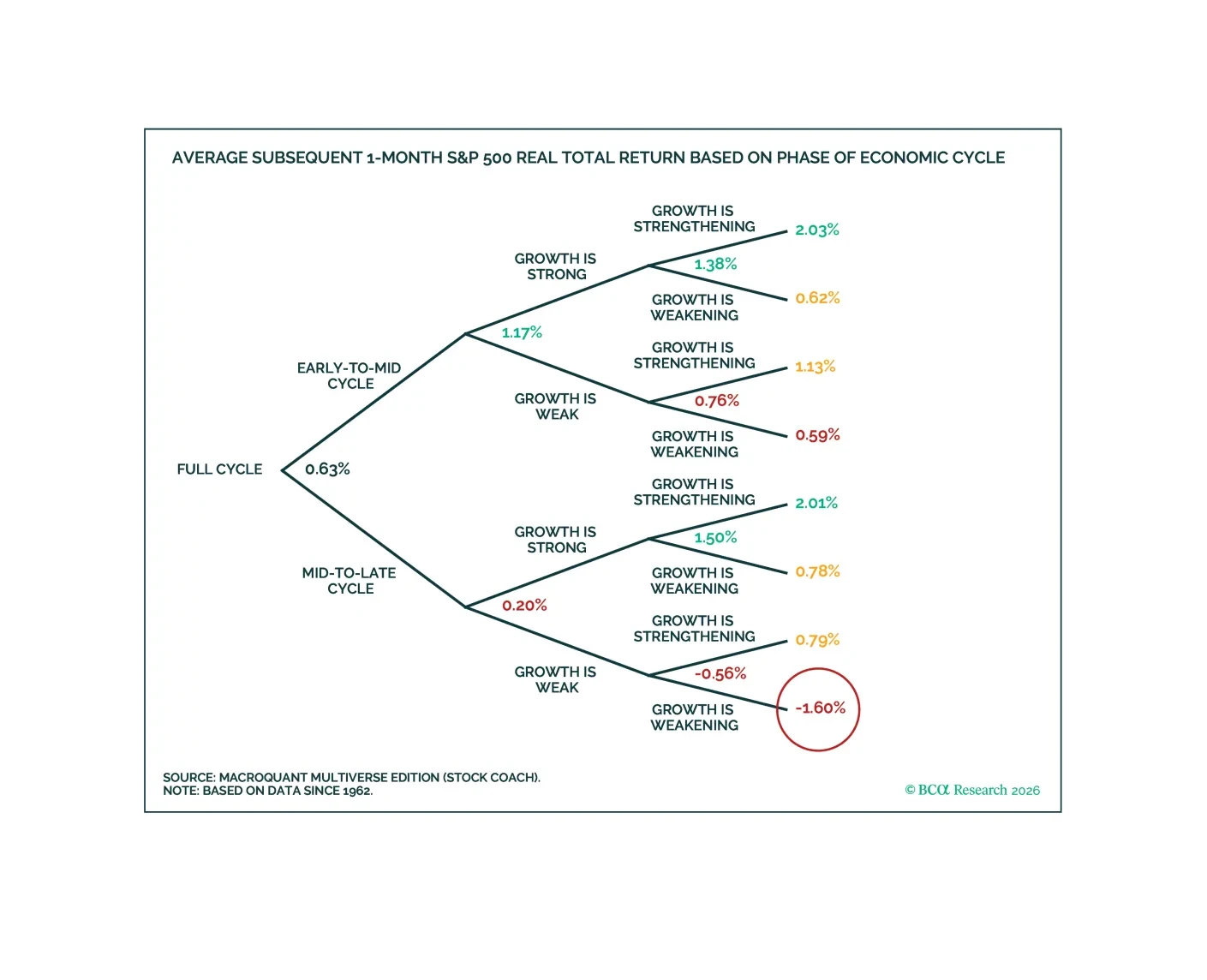

MacroQuant recommends underweighting equities and adopting a benchmark duration stance in fixed-income portfolios. The model is very positive on the US dollar, bearish on gold, neutral on copper, and bullish on oil.

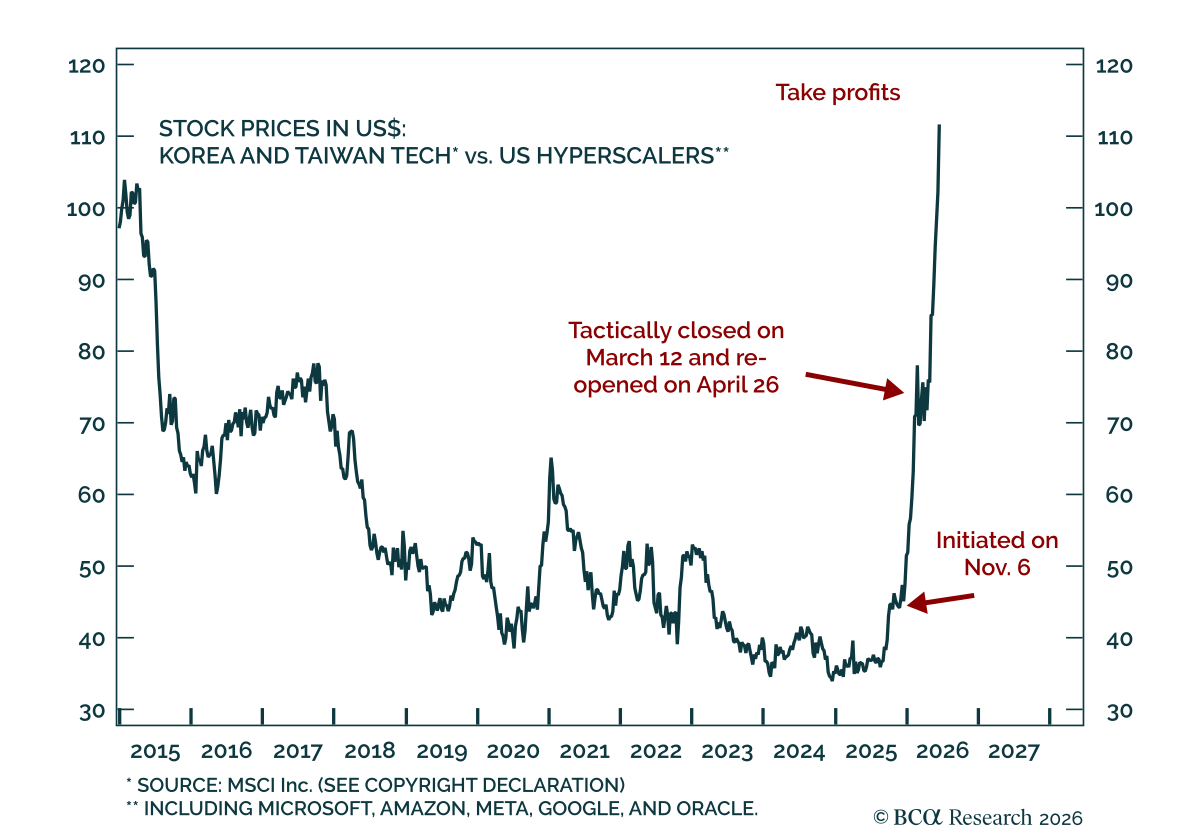

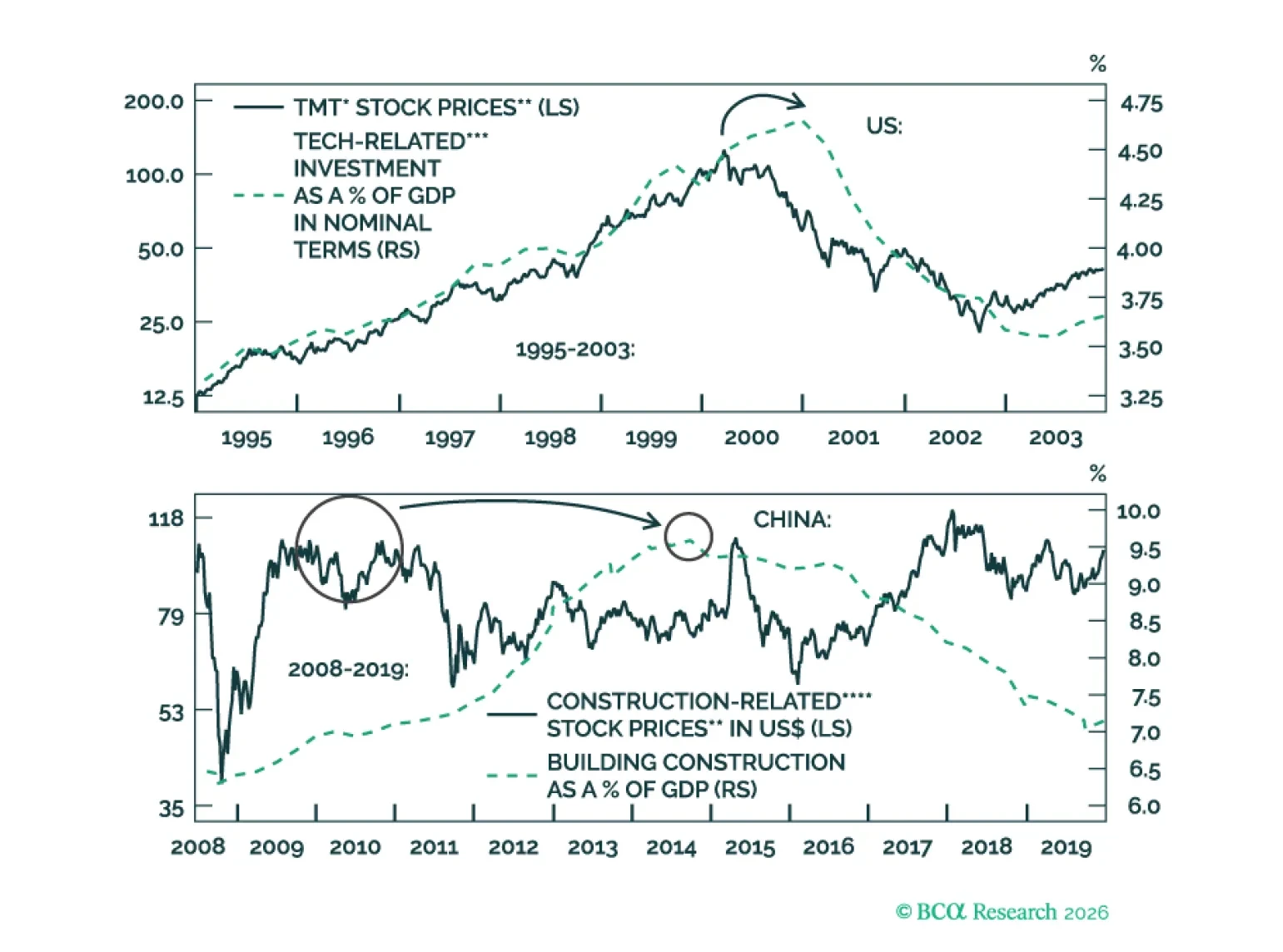

AI is transformative, yet tech stocks may not produce positive returns. Market cycles have not disappeared. Greed and fear will still produce large share price fluctuations. Meanwhile, US inflation is the key near-term risk. Global non-tech capex aspirations also look overstated.

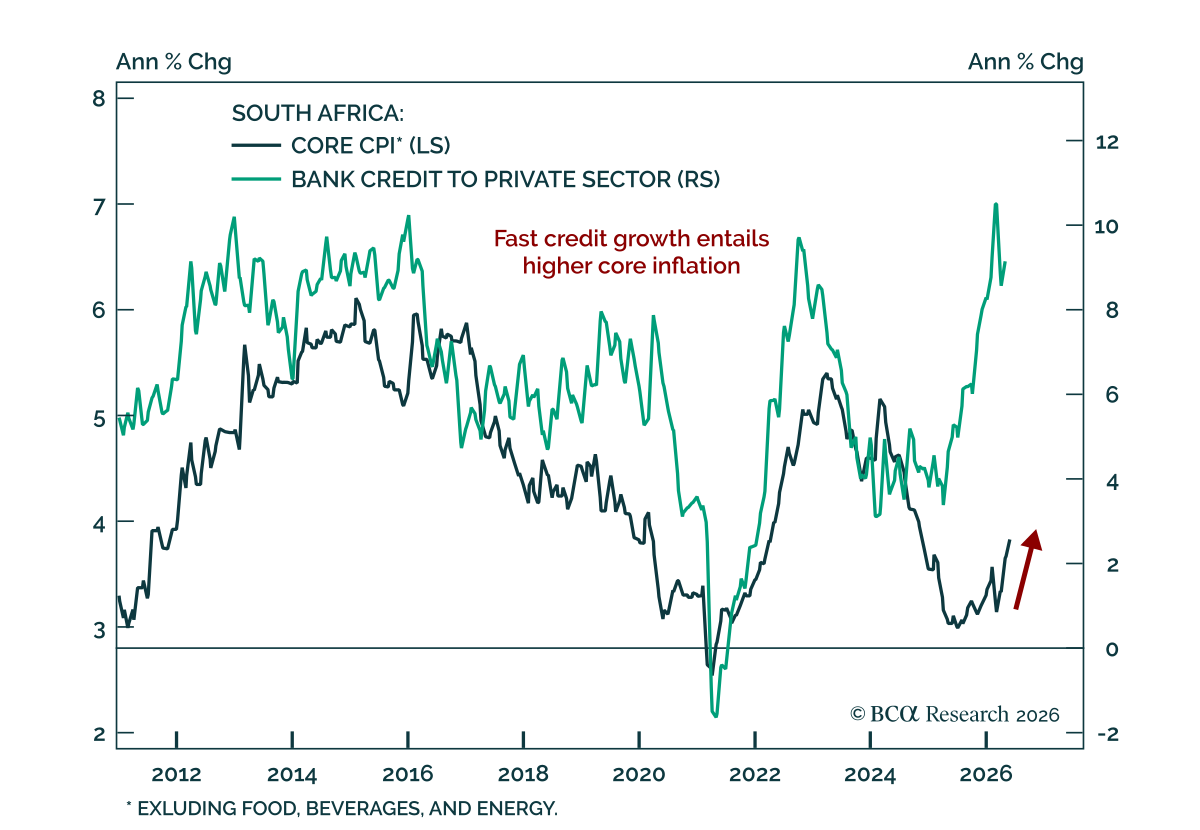

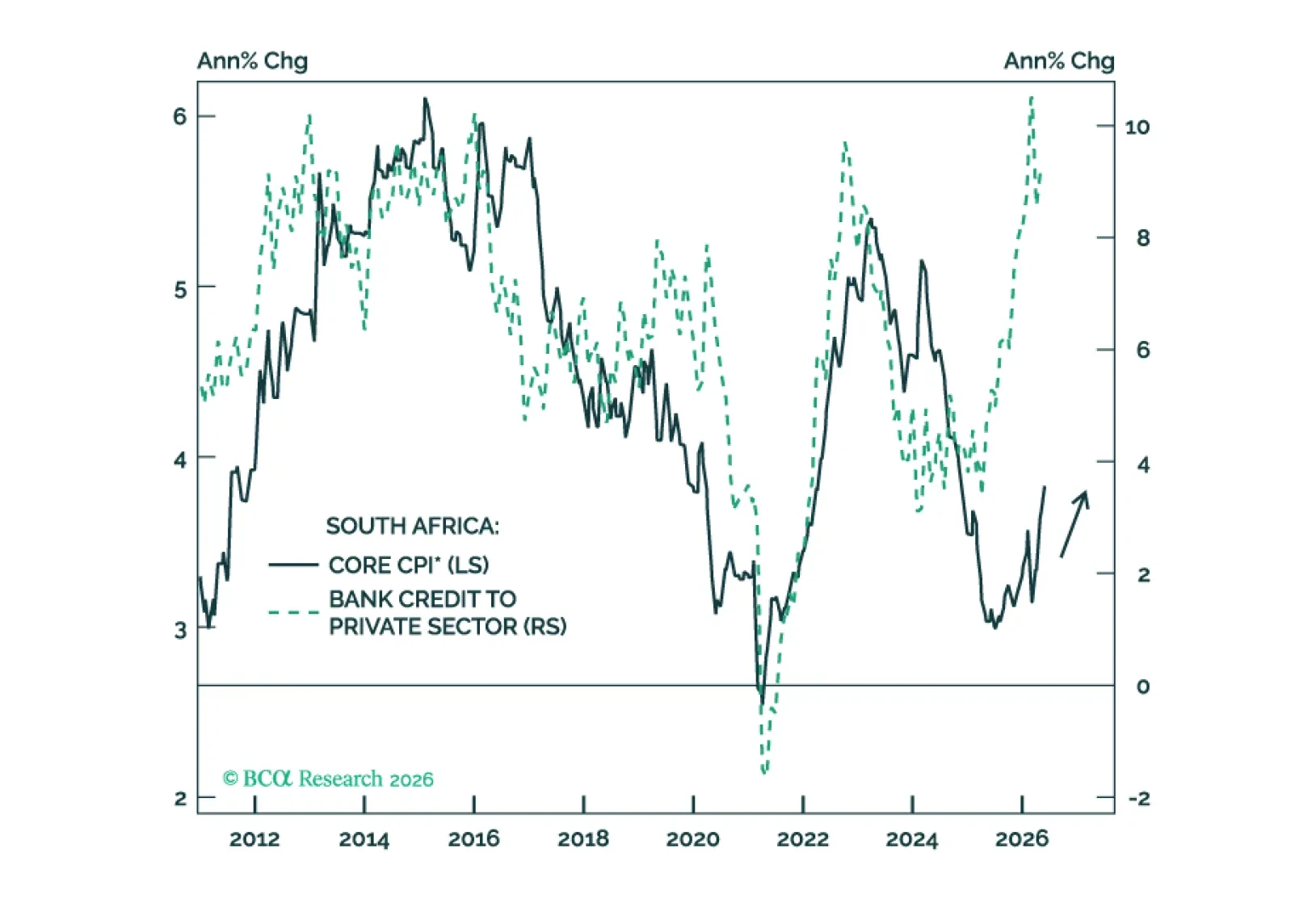

South Africa’s ambitious reform agenda will take time to bear fruit. Meanwhile, the country faces a stagflationary squeeze as inflation rises while growth slows. South African stocks, bonds, and currency are all vulnerable.

Our Portfolio Allocation Summary for June 2026.