Emerging Markets

Russia’s conflict with the West will escalate and trigger more bad news for risky assets this fall. Beyond that, stalemate looms. Latin American equities present a potential opportunity once the macro and geopolitical backdrop improve.

This week we present our Portfolio Allocation Summary for October 2022.

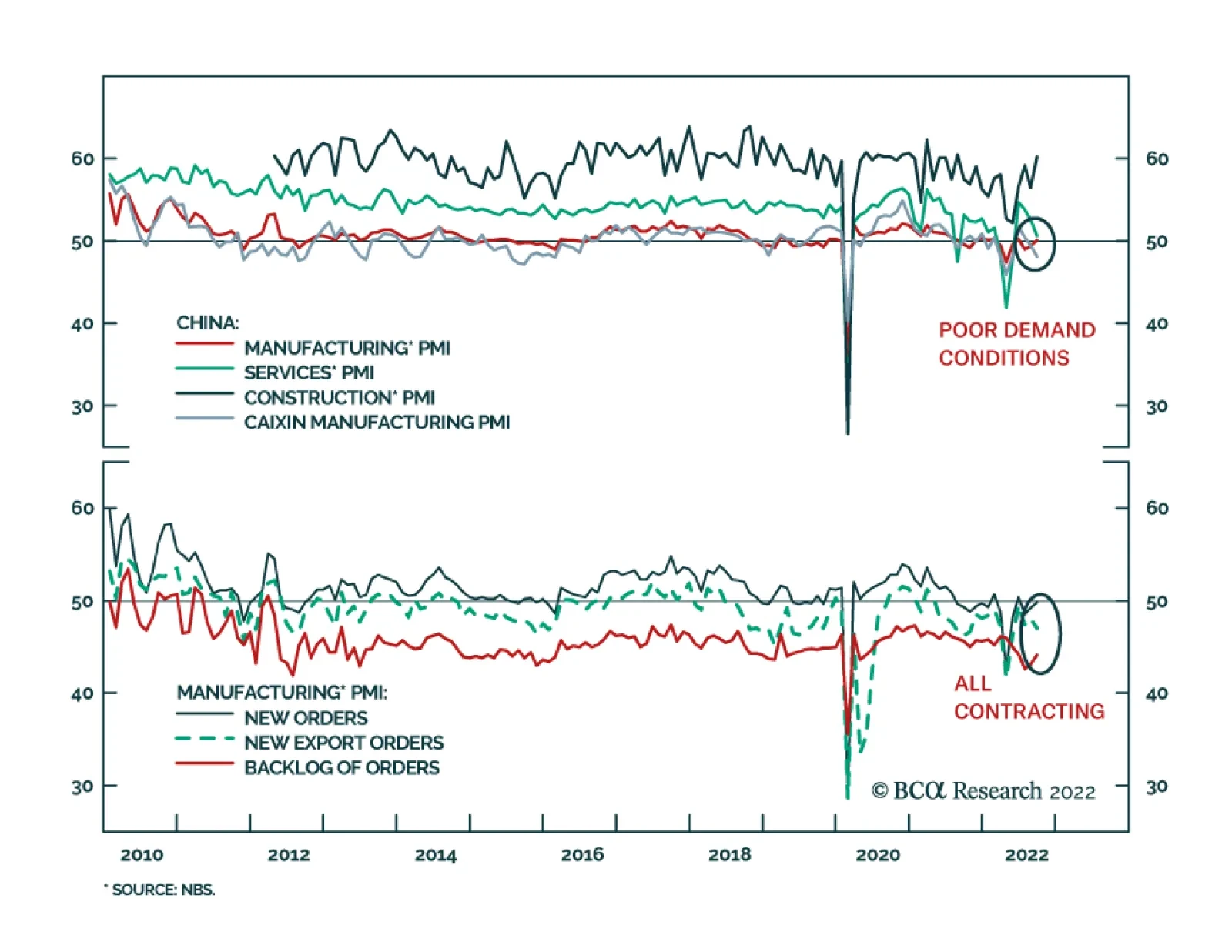

China’s Official PMI data continues to paint a bleak picture of domestic demand conditions. Although the manufacturing index increased by 0.5 points, at 50.1 it is barely above the boom-bust line, and instead suggests that activity in this sector has…

Investors should go long US treasuries and stay overweight defensive versus cyclical sectors, large caps versus small caps, and aerospace/defense stocks. Regionally we favor the US, India, Southeast Asia, and Latin America, while disfavoring China, Taiwan, Hong Kong, eastern Europe, and the Middle East.

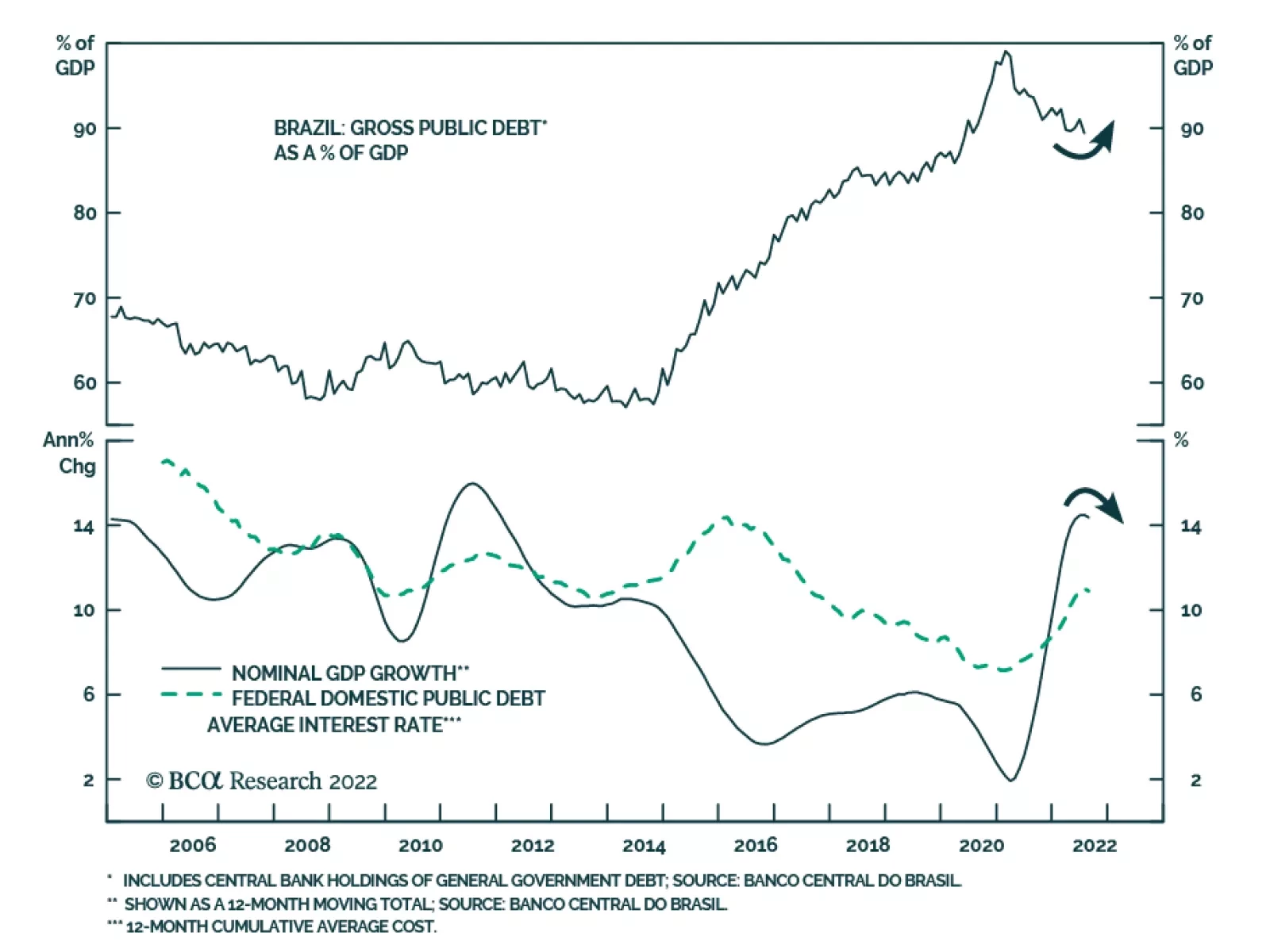

Opinion polls ahead of Brazil’s election this weekend suggest that odds are in favor of a victory for former President Luiz Inácio Lula da Silva. While a runoff election on October 30 will be needed if no candidate gains more than 50% of the ballot, more…

Executive Summary EU Metal Industry Under Threat

EU Energy Crisis, Strong USD Imperil Bloc’s Metals Industry

EU Energy Crisis, Strong USD Imperil Bloc’s Metals Industry

Russia’s threat to cut off all remaining exports of natural gas to the EU via Ukraine will further imperil the bloc’s struggling metals industry, particularly aluminum smelting – where half of its capacity already has been shut – and zinc refining. The EU will have to prioritize energy security over its renewable-energy goals, given the challenges its manufacturing industries will confront for the next 3-5 years. Surging imports of raw copper concentrates and unwrought metal will consolidate the global dominance of China’s copper refiners, which sharply increased their treatment and refining charges this week. The US likely will see more investment in metals mining and refining on the back of the EU distress, which realistically cannot be addressed until gas and power prices fall to levels that allow them to sustain their operations. Bottom Line: Ongoing supply shocks to the EU’s base-metals industry will force the bloc to prioritize energy security over its renewable-energy goals. This will drive the bloc’s demand for liquified natural gas (LNG) and oil higher, even after short-term measures to increase LNG intake and distribution capacity are completed over the next 2-3 years. We expect the equities of oil and gas producers to outperform metals miners over this period. After being stopped out, we will be re-instating our long XOP ETF position at tonight’s close. Feature Earlier this month, Eurometaux, the EU metals lobbying group, published a memo to the European Commission drawing attention to “Europe’s worsening energy crisis and its existential threat to our future.”1 This is not hyperbole. At the heart of the industry’s woes is a chronic shortage of energy – in any form – for industrial use. Utilities are signing long-term LNG supply contracts to address this shortage, but they can expect to wait 3-4 years or more before gas arrives on Europe’s shores.2 Spot and one-off cargoes will become available over that time, but most of the existing LNG production is under long-term contract. Oil, coal, and nuclear energy are available for power generation, industrial applications and space-heating, and they increasingly are being used in the bloc, but these too are constrained.3 Measures to address the chronic energy shortage hammering the EU base-metals industry will take years to effect, and could come too late to meaningfully preserve existing refining capacity, which has been contracting for years (Chart 1).4 Most of the EU’s metals production is accounted for by aluminum, copper and zinc, which are extremely energy intensive, copper only less so (Chart 2). The surge in LNG prices following Russia's invasion of Ukraine propelled electricity prices higher, given gas is the marginal fuel for EU power generation (Chart 3). This crushed zinc and aluminum refining. Half of the EU’s aluminum smelter capacity – ~ 1mm MT – will be curtailed or shuttered this year, according to European Aluminum.5 Chart 1EU Metal Industry Under Threat

EU Energy Crisis, Strong USD Imperil Bloc’s Metals Industry

EU Energy Crisis, Strong USD Imperil Bloc’s Metals Industry

Chart 2EU Metals Are Extremely Energy Intensive

EU Energy Crisis, Strong USD Imperil Bloc’s Metals Industry

EU Energy Crisis, Strong USD Imperil Bloc’s Metals Industry

Chart 3EU Power Price Surge Crushes Metals Refining

EU Energy Crisis, Strong USD Imperil Bloc’s Metals Industry

EU Energy Crisis, Strong USD Imperil Bloc’s Metals Industry

The surge in European electricity prices and the resulting curtailment or shuttering of zinc refining paced the 2.6% y/y decline in global output in 1H22, which took global production down to 6.77mm MT, according to the International Lead and Zinc Study group. Europe accounts for ~ 15% of global zinc refining.6 Refined zinc consumption fell 3% y/y in 1H22 to 6.74mm MT. China Bingeing On Copper Global refined copper output in the January – July 2022 period slightly outpaced usage – with 3% growth in the former and 2.6% growth in the latter, according to the International Copper Study Group (ICSG). On the back of this report, we lowered our expected supply growth estimate to 3% this year, (Chart 4). This brings our estimate for total supply down by ~400k MT vs. our previous iteration to 25.3mm MT. We are keeping our estimate of 2023 supply growth rate at ~ 4.5%. Our copper demand estimate is a function of real GDP estimated by the World Bank, and remains at just under 26mm MT and 27.2 mm MT for 2022 and 2023 respectively. As a result of the lower 2022 production growth rate, our forecasted copper deficit has widened to ~ 605k tons in 2022 and 480k tons in 2023. The mismatch in supply and demand levels will keep inventories in China and the West under pressure (Charts 5A and 5B). Chart 4Copper Supply Estimate Lowered

Copper Supply Estimate Lowered

Copper Supply Estimate Lowered

Chart 5AChinese Copper Inventories Continue To Draw

Chinese Copper Inventories Continue to Draw

Chinese Copper Inventories Continue to Draw

Chart 5BAs Do Stocks In The West

As Do Stocks In The West

As Do Stocks In The West

China’s imports of copper condensates – the raw material used to make refined copper – surged to 16.65mm tons over January – August 2022, up 9% y/y. Imports of unwrought and semi-fabricated copper were up 8% over the same period at 3.9mm MT, according to Mysteel.com. As is to be expected, treatment and refining charges at Chinese smelters also moved higher: for 3Q22, refiners were charging $93/MT, up $13 from 2Q22 levels and $23/MT from 4Q21, according to Reuters. These charges increase when raw-material supplies increase, and vice versa. This is meant to be a floor charged for refining concentrates to produce refined copper. Real USD Matches US PPI After Re-Opening In an unusual turn of events, the USD Real Effective Exchange Rate (REER) has been moving higher along with the US Producer Price Index for all commodities. This trend started as the global economy accelerated its re-opening in 2021 (Chart 6). The USD has a profound affect on commodity prices: Most globally traded commodities are denominated in USD, funded in USD and invoiced in USD. This is the channel through which the Fed’s monetary policy impacts commodity buyers ex-US. A stronger dollar means commodities in local-currency terms are more expensive, and vice versa. It also means production costs in states that do not peg their currencies to the USD go down, and vice versa. Chart 6Real USD Gains With US PPI During Reopening

Real USD Gains With US PPI During Reopening

Real USD Gains With US PPI During Reopening

Given the USD’s elevated level, copper prices in local-currency terms will continue to face a massive headwind on the demand side, and a massive tailwind on the production side. For households and firms buying commodities, or durable goods with a lot of metals in them (copper, stainless steel, etc.), Fed policy has a direct effect on how their budgets get allocated.7 In the short and long run macroeconomic variables such as the USD influence copper prices by increasing the cost of copper ex-US when the dollar rallies, and vice versa. Fundamental variables like tight inventories, which arise when demand is consistently above supply, impart an upward price bias to the copper forward curve (backwardation increases as inventories decrease). Domestic economic factors matter, too. Copper prices have been pummeled by the meltdown of China’s property sector, which has been the growth engine for the country’s economy, accounting for ~ 30% of its copper demand. The USD has remained well bid following Russia’s invasion of Ukraine, presenting a powerful headwind to commodity prices in general. This is particularly true for refined copper, given China accounts for more than 50% of total global consumption. China’s RMB dropped 11.4% vs. the USD from the start of the year to now. This has not stood in the way of a sharp increase in imports of the copper ore and refined metal this year, despite the country’s weak economic performance. Given China’s property-market slowdown and its zero-tolerance COVID-19 policy and its attendant lockdowns, it is difficult to pinpoint a cause for its increased copper demand. It may be opportunistic purchasing – buying the metal when prices are far lower than their peak earlier this year – or it could signal a post-Communist Party Congress increase in economic activity (e.g., more fiscal stimulus hitting the system) officials are preparing for. Investment Implications The EU’s metals-refining sector faces existential challenges as a result of the bloc’s energy crisis. Significant employers – not just the metal refiners – will be confronting limited energy supply and higher costs for years, given the tightness in conventional energy markets – oil, gas and coal. The renewable-energy sector also faces daunting challenges, as a result of difficulties faced by metals refiners and the energy crisis they presently confront. It is worthwhile noting that none of the renewables technology is possible without metals. Given the abundant lessons re reliance on a single supply source Russia’s invasion of Ukraine has provided, we expect investment in US metals mining and refining to increase, as consumers of copper, aluminum and zinc seek to diversify away from Chinese dominance of this sector. This will take time to build out, just as the increase in LNG supplies will take time. This likely will keep a bid under the USD, as manufacturing, mining and refining capex investment shifts to the US. We expect the EU’s drive to secure conventional energy will drive the bloc’s demand for liquified natural gas (LNG) and oil higher, even after currently planned short-term measures to increase LNG intake and distribution capacity are completed over the next 2-3 years. After being stopped out this past week, we will be re-instating our long XOP ETF position on tonight’s close, consistent with our view. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Ashwin Shyam Research Analyst Commodity & Energy Strategy ashwin.shyam@bcaresearch.com Commodities Round-Up Energy: Bullish. European Commission President Ursula von der Leyen proposed additional economic sanctions against Russia yesterday including extending price caps on oil to third countries, following the call-up of reserves in Russia last week, and a veiled threat to use nuclear weapons against Ukraine. In a related matter, Gazprom, the state-owned gas producer and trading company, threatened to cut off the remaining gas sales to Europe via Ukraine – close to half the ~ 80mm cm /d still being sold via pipeline to the continent (Chart 7). It is apparent the EU has been anticipating a full shut-off of Russian pipeline gas shipments, which likely motivates von der Leyen’s proposal. Any proposal to increase sanctions on Russia would have to be unanimously approved. Base Metals: Bullish. In a boost to prospective Chile copper production, a BHP executive indicated he expects regulatory uncertainties in the largest copper producing state to ease. BHP mentioned earlier this year that legal certainty in Chile would be key to investing over USD 10 billion in the state. Earlier this month, Chilean voters rejected a constitution, which, among other things, could have curtailed mining operation by including new taxes and environmental regulations. Precious Metals: Neutral. In their Q2 platinum balances report, the World Platinum Investment Council (WPIC) expects FY 2022 surplus to rise more than 50% vs. its Q1 estimates to 974k oz. Weak platinum ETF demand resulting from a strong USD and rising interest rates is expected to outweigh operational constraints in South African and North American mining operations. Bolstering supply is the fact that Russian platinum – which constitutes ~11% of global supply – has been reaching buyers. However, this security of supply may not last. Once buyers’ long-term contracts for Russian platinum end, as in the case with aluminum, companies may self-sanction, turning to the spot market and other producing states instead. For palladium, SFA Oxford sees the metal's surplus dropping to ~92% y/y, as demand is expected to increase and production is forecast to fall (Chart 8). Chart 7

EU Energy Crisis, Strong USD Imperil Bloc’s Metals Industry

EU Energy Crisis, Strong USD Imperil Bloc’s Metals Industry

Chart 8

Palladium Balances Expected To Drop

Palladium Balances Expected To Drop

Footnotes 1 Please see Europe’s non-ferrous metals producers call for emergency EU action to prevent permanent deindustrialisation from spiralling electricity and gas prices, posted by Eurometaux 6 September 2022. 2 See, e.g., Exclusive: German utilities close to long-term LNG deals with Qatar, sources say published by reuters.com 20 September 2022. 3 For additional discussion, please see Energy Security Rolls Over EU's ESG Agenda, which we published 28 July 2022. It is available at ces.bcaresearch.com. 4 Please see Agenda for a resilient European metals supply for the green and digital transitions, posted by Eurometaux in mid-2020. 5 Please see Reconciling growth and decarbonisation amidst the energy crisis, posted by European Aluminium May 2022. 6 Please see Column: European smelter hits mean another year of zinc shortfall published by reuters.com 17 May 2022. 7 Please see "Global Dimensions of U.S. Monetary Policy" by Maurice Obstfeld, which appeared in the February 2020 issue of International Journal of Central Banking for an in-depth discussion and analysis. Investment Views and Themes Strategic Recommendations Trades Closed in 2022

Please note I will be hosting a live webcast on September 29, 2022 at 9:00 AM HKT for the APAC region. I will discuss the global/China/EM macro outlooks and financial market implications. For clients in the Americas and EMEA, we had a webcast on September 28, 2022. You can access the replay via this link. Arthur Budaghyan Executive Summary Global Semi Stock Prices: Further Downside Ahead

Global Semi Stock Prices: Further Downside Ahead

Global Semi Stock Prices: Further Downside Ahead

Global semiconductor stock prices are still vulnerable to meaningful downside over the next three months. Global semi consumption will contract due to the corresponding waning demand of smartphones, personal computers, and other consumer electronics. Global semi demand in sectors of automobiles and datacenters will continue growing. However, such an increase in demand cannot offset the demand reduction in other sectors. Semiconductor consumption in China has entered a contraction phase. Semiconductor inventories have swelled. Alongside a sharp upsurge in chip production capacity, this increase in inventories will lead to chip price deflation in the next nine months. Nevertheless, the structural outlook for global semiconductor demand remains constructive. We are waiting for a better entry point for semi stocks. Bottom Line: There is more downside in global semiconductor share prices as well as Taiwanese and Korean tech stocks. We will seek to recommend buying semiconductor stocks when a more material decline in semi companies’ profits is priced in their share prices. At the moment, we are downgrading Taiwanese stocks from neutral to underweight relative to the EM equity benchmark but are maintaining an overweight stance on the Korean bourse within an EM equity portfolio. The global semiconductor equity index is breaking below its technical support (Chart 1). The implication is that these share prices are in an air pocket and investors should not chase a declining market. Based on previous cycles, we expect global semiconductor stocks to bottom late this year or early next year and semi sales to trough in 2023Q2. In the previous five cycles, global semi stocks always bottomed before global semi sales and lead times varied from three-to-six months. Chart 2 shows that Taiwan’s semiconductor new export orders lead global semi sales by about three months, and they continue to point to considerable downside in the global semi-industry. Chart 1Global Semi Stocks: Breaking Down

Global Semi Stocks: Breaking Down

Global Semi Stocks: Breaking Down

Chart 2Global Semi Sales: More Downside Ahead

Global Semi Sales: More Downside Ahead

Global Semi Sales: More Downside Ahead

The semiconductor industry has a history of cyclicality. Shortages have been followed by oversupply, which has led to declining prices, revenues, and profits for semi producers. This time is no exception Global Semi Sales: A Cyclical Slump Underway Global semiconductor demand began its downward trajectory in May of this year and will continue to slide in the next three-to-six months. Both the volume and value of China’s semiconductor imports are in a deep contraction and China’s imports from Taiwan have also plummeted (Chart 3). China is the world’s largest consumer of semiconductors, accounting for 35% of global demand. We expect semi sales to remain in contraction in China and to shrink in regions outside China in the next six-to-nine months (Chart 4). Chart 3China's Semi Imports Plummeted

China's Semi Imports Plummeted

China's Semi Imports Plummeted

Chart 4Semi Sales Will Contract Across Regions

Semi Sales Will Contract Across Regions

Semi Sales Will Contract Across Regions

There are several important reasons for the retrenchment worldwide. First, the lockdowns around the world in 2020 and 2021 generated an unprecedented increase in online activities and a corresponding surge in demand for smartphones/PCs/tablets/game consoles/electronic gadgets. This was the main driving force for the boom in global semiconductor sales from 2020Q3 to 2022Q1. The excessive demand for consumer goods and electronics has run its course and global demand will sag in the next six months. As we have been contending since early this year, global exports are set to contract. Households that bought these goods in the past two years probably will not make new purchases in the near term. In addition, declining real disposable income and rising interest rates will constrain consumer spending. Smartphones, PCs, tablets, home appliances, and other household electronic goods consume about half of global semi output. In addition, rising job uncertainties resulting from China’s dynamic zero-COVID policy and slowing household income growth will curb consumption within China. Here are our takeaways for each segment: Chart 5China's Output Of Mobile Phones And PCs Has Been Shrinking

China's Output Of Mobile Phones And PCs Has Been Shrinking

China's Output Of Mobile Phones And PCs Has Been Shrinking

Mobile phones: Mobile phones are the largest contributor to global semi sales, with a share of 31% as of 2021, based on the data from World Semiconductor Trade Statistics (WSTS). According to the International Data Corporation (IDC), global smartphone shipments are set to decline by 6.5% year-over-year in volume terms in 2022. Smartphone OEMs cut their orders drastically in 2022 because of high inventories and low demand, with no signs of an immediate recovery. China accounts for 67% of global mobile phone production and its mobile phone production has been contracting (Chart 5, top panel). Traditional PCs and tablets: Based on data from the IDC, global traditional PC1 and tablet shipments are set to decline by 12.8% year-over-year in 2022 and by an additional 2.6% next year in volume terms. Computer production in China, which is the world’s largest computer producer and exporter, also shows massive downsizing (Chart 5, bottom panel). Home appliances: China is also the largest producer and exporter of air conditioners (ACs), washing machines, refrigerators, and freezers. Except for a slight growth in AC output in response to heatwaves in China and Europe, China’s output of other home appliances will shrink. Globally, these industries accounted for about half of all semiconductor sales in 2021. Given the overconsumption of these goods worldwide over the past two years, we expect a material decline in these sectors in the next six-to-nine months. Second, automobiles, servers, and industrial electronics, which together account for about 30% of global semi sales, will have positive single-digit growth going forward. Yet, such an increase will not be enough to offset the lost demand from the consumer electronic goods sector in the next six-to-nine months. Chart 6Global Auto Production Will Rise

Global Auto Production Will Rise

Global Auto Production Will Rise

Automotive (accounts for 11% of world chip demand): The chip shortage in this sector has eased only moderately. Auto output levels in major producing countries remain well below their pre-pandemic levels (Chart 6). In light of improved foundry capacity, semiconductor producers will be able to produce automotive chips and reduce lingering shortages. However, for most chips to automakers, there are no supply shortages. Only a small number of categories of automotive chips, such as microcontrollers (MCU) and insulated-gate bipolar transistors (IGBT), are still in tight supply. Given that the total automotive sector only accounted for about 5% of total global semi sales last year, the recovery in global automobile output will contribute only limited growth to global semi sales. Servers (account for 10% of world chip demand): The surge in online activities resulted in greater demand for cloud services and remote work applications, both of which require computer servers. Total server demand is comprised of data servers for cloud providers and private enterprises, with the former as the main driving force in recent years. Data center expansion among cloud service providers will be driven by 5G, automotive, cloud gaming, and high-performance computing. After expanding by 10% last year, the pace of annual growth in global server shipments will likely be more moderate, to about 5%-6% in the next couple of quarters. Chart 7Global Industrial Demand For Chips Is Set to Decelerate

Global Industrial Demand For Chips Is Set to Decelerate

Global Industrial Demand For Chips Is Set to Decelerate

Industrial electronics (account for 9% of world chip demand): The growth rate in semi demand for this sector is falling. The global manufacturing new order-to-inventory ratio has plunged, and global manufacturing production is set to decline for the rest of this year and through to 2023H1 (Chart 7). Nevertheless, given structural tailwinds for industrial electronics, we expect semi demand in this sector to dip to single-digit growth in the near term rather than to contract. Third, with semiconductor inventories having surged, new orders for chips, and hence their production, will plummet. The length and intensity of the chip shortage, which started in 2020H2, triggered stockpiling among a broad range of customers, including manufacturers of smartphones and other consumer electronics. Moreover, the recent slowdown in smartphone/PC demand increased the inventory of silicon chips. Chart 8Semiconductor Inventory Overhang

Semiconductor Inventory Overhang

Semiconductor Inventory Overhang

China had also stockpiled semiconductors from 2020Q2 to 2021Q4. With faltering demand, the country will continue its destocking process in the next couple of quarters. Semiconductor inventories in Taiwan and Korea have surged, corroborating the fact that the current cyclical downturn in the global semi sector will be a severe one (Chart 8). Hence, businesses in the semi supply chain will continue to draw upon their inventories rather than increase their semiconductors orders. This will reduce semiconductor demand meaningfully in the coming months. Bottom Line: The cyclical slump in worldwide semiconductor sales has further to go, with the sector’s sale volumes and prices projected to contract in the next six months. Semi producers will experience a substantial decline in their profits. Comparing Cycles Previous cycles may provide insight in the downside of the cyclical slump in global semi sales. In the previous five cycles, global semi sales experienced a contraction, ranging from 7% to 45% (Table 1). In the current cycle, global semi sales still had 7% year-over-year growth in 2022Q2 (Chart 9). Table 1Six Cyclical Downturns In Global Semiconductor Market

Have Global Semi Stocks Hit Bottom?

Have Global Semi Stocks Hit Bottom?

Chart 9Global Semi Stocks And Global Semi Sales Global Semiconductor Market: Sales & Share Prices

Global Semi Stocks And Global Semi Sales Global Semiconductor Market: Sales & Share Prices

Global Semi Stocks And Global Semi Sales Global Semiconductor Market: Sales & Share Prices

In fact, the current downturn could be deeper than the one between 2018 and 2019 (when sales contracted by 16%) for the following reasons: Sales of both cell phones and PCs will likely dwindle further this time than they did in 2018 to 2019. The pandemic boosted demand for consumer electronics, but this also brought forward future demand. In comparison with 2018, the current cycle might have a longer replacement cycle for mobile phones and PCs. Unlike 2019, global demand for consumer goods will likely contract rather than decelerate. This has ramifications for the duration and magnitude of the semi downturn. Economic growth, and job and income uncertainties in China are much worse now than they were between 2018 and 2019. These factors will likely lead to a bigger cut in IT spending by both consumers and businesses, resulting in a larger downturn in global semi demand in this cycle. The tech battle between the US and China is more intense than in it was from 2018 to 2019. In mid-2018, the U.S. imposed a 25% tariff on Chinese imports of semiconductor goods, including machines and flat panel displays. China retaliated by imposing its own 25% tariff on U.S. exports of semiconductor goods, such as test equipment. This month, the US imposed new restrictions on NVIDIA and AMD in relation to selling artificial intelligence chips to Chinese customers. The US also plans to curb further its shipments of chipmaking tools to China. These plans will cut China’s imports of high-end semi products, for which producers enjoy high profit margins. In addition, the shortage of these chips will stall the development and sales of many consumer products within China, which will thereby reduce demand for other types of chips needed for consumer products. Chart 10Rapid Semi Capacity Expansion Worldwide

Rapid Semi Capacity Expansion Worldwide

Rapid Semi Capacity Expansion Worldwide

Global semi capacity expansion has recently been much stronger in current cycle than it was in the 2016-2018 cycle. This may lead to a bigger supply surplus in this cycle than in the last one. It takes about 18-24 months, on average, to build a new semiconductor fabrication plant. Thus, large capital expenditures by semi producers in 2021-22 entail considerable new supply in 2023-24. According to IC Insights, the annual wafer capacity growth rates were 6.5% in 2020, 8.5% in 2021 and 8.7% in 2022. This compares with 4%-6.5% between 2016 and 2018 (Chart 10). Rapid capacity expansion typically leads to price deflation for chips and is therefore negative for the semi producers’ profitability and their share prices. Are global semi stock prices already pricing bad news? We do not think so. Nearly all major players saw a drop in revenues in the past cycle. In sharp contrast, only Intel’s revenues have dropped so far in the current cycle (Chart 11). Global semi stock prices will continue falling as companies report shrinking sales and earnings in the next couple of quarters. In former cycles when global semi stocks bottomed, investor sentiment – as measured by the net EPS revisions – was more downbeat than it is currently (Chart 12). Chart 11More Semi Companies' Sales Are Likely To Contract

More Semi Companies' Sales Are Likely To Contract

More Semi Companies' Sales Are Likely To Contract

Chart 12Global Semi Stock Prices: Net EPS To Drop More

Global Semi Stock Prices: Net EPS To Drop More

Global Semi Stock Prices: Net EPS To Drop More

Bottom Line: The global semiconductor sector’s cyclical slump could be deeper than it was in the 2018-2019 cycle. Hence, shares prices will fall considerably more than they did in late 2018. Ramifications For Taiwanese And Korean Markets Taiwanese and Korean semiconductor stock prices will probably continue to fall in absolute terms. The former recently broke its three-year moving average and the latter its six-year moving average (Chart 13). Chart 13Taiwanese And Korean Semi Stock Prices Will Fall Further

Taiwanese And Korean Semi Stock Prices Will Fall Further

Taiwanese And Korean Semi Stock Prices Will Fall Further

Chart 14TSMC: Smartphone And HPC Make 81% Of Revenue

Have Global Semi Stocks Hit Bottom?

Have Global Semi Stocks Hit Bottom?

For TSMC, the smartphone sector still accounts for 38% of revenues (Chart 14). Hence, a contraction in global smartphone sales in the next six-to-nine months could hurt the company’s top and bottom lines considerably. Meanwhile, the high-performance computing (HPC) sector became the largest contributor of TSMC revenues with a 43% share. A slowdown in data center investment and a decrease in GPU demand due to falling bitcoin prices will also materially affect the company’s profitability. In addition, the US government’s AI chips export restriction policy will decrease NVIDIA and AMD AI sales to China. According to NVIDIA’s news release, approximately US$400 million in potential chip sales to China (including Hong Kong) will likely be subject to this new restriction. AI chips are manufactured by TSMC with its advanced node technology and have a high-profit margin. Hence, the new policy will negatively impact TSMC’s revenues and profits. For Samsung, the memory market is in a free-fall due to plummeting demand (Chart 15). TrendForce expects the average overall DRAM price to drop by 13-18% in 2022Q4 because of high inventories in the supply chain and stagnant demand. The semi shipment-to-inventories ratios for both Taiwan and South Korea nosedived, pointing to lower semi stock prices in these two markets (Chart 16). Chart 15Samsung: Vulnerable To Sinking Prices Of Memory Chips

Samsung: Vulnerable To Sinking Prices Of Memory Chips

Samsung: Vulnerable To Sinking Prices Of Memory Chips

Chart 16Semi Shipments-to-Inventory Ratios Plunged In Taiwan And Korea

Semi Shipments-to-Inventory Ratios Plunged In Taiwan And Korea

Semi Shipments-to-Inventory Ratios Plunged In Taiwan And Korea

Bottom Line: Both TSMC and Samsung stock prices have more downside over the next three months. Equity Valuations And Investment Conclusions The global semiconductor stock index in USD terms has tumbled by 45% from its recent peak. Multiples of semiconductor stocks are near their long-term average levels (Chart 17 and 18). These multiples could undershoot as they did in 2018-2019, which means even more downside is ahead. Chart 17Multiples Of Semi Stocks Could Undershoot

Multiples Of Semi Stocks Could Undershoot

Multiples Of Semi Stocks Could Undershoot

Chart 18Multiples Of Semi Stocks Could Undershoot

Multiples Of Semi Stocks Could Undershoot

Multiples Of Semi Stocks Could Undershoot

Aside from the profit outlook, higher US bond yields are also causing multiple compression for global semiconductor stocks (Chart 19). As to the allocation to semi stocks within an EM equity portfolio, we recommend downgrading Taiwan from a neutral allocation to underweight and reiterate an overweight stance on the KOSPI. The US-China geopolitical confrontation will escalate in the coming years and Taiwan is at the epicenter of this. These are relative calls, that is against the EM benchmark (Chart 20). We remain negative on their absolute performance. Chart 19Higher US Bond Yields = Multiple Compression In Global Semi Stocks

Higher US Bond Yields = Multiple Compression In Global Semi Stocks

Higher US Bond Yields = Multiple Compression In Global Semi Stocks

Chart 20Downgrade Taiwan To Underweight Relative To The EM Benchmark

Downgrade Taiwan To Underweight Relative To The EM Benchmark

Downgrade Taiwan To Underweight Relative To The EM Benchmark

Finally, the structural outlook for global semiconductor demand remains constructive. We are waiting for a better entry point. We would recommend buying semiconductor stocks after pricing in a more material contraction in semi companies’ revenues and profits. Ellen JingYuan He Associate Vice President ellenj@bcaresearch.com Footnotes 1 Traditional PCs are comprised of desktops, notebooks and workstations.

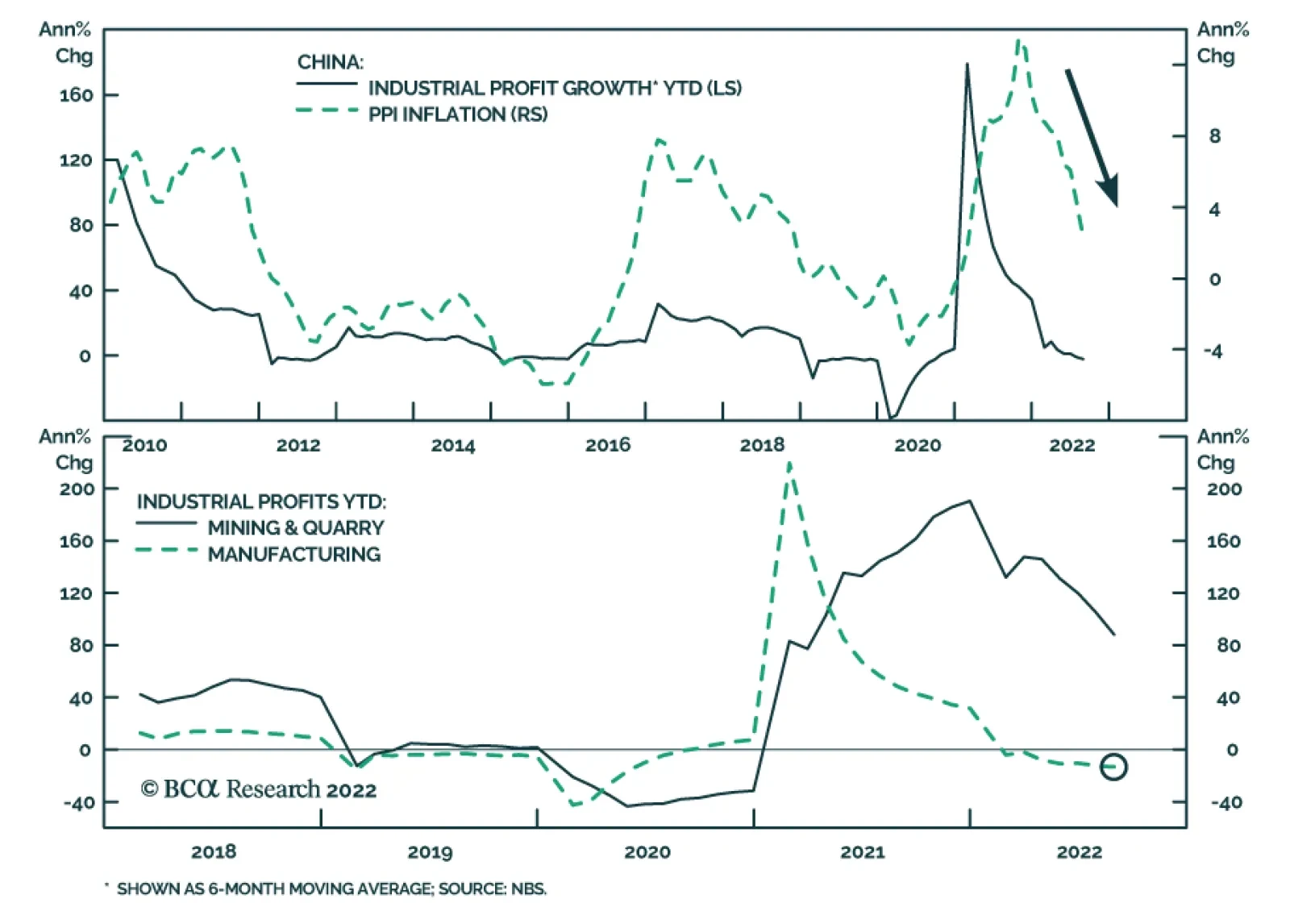

Chinese industrial profit growth contracted for the second consecutive month on a year-to-date year-on-year basis in August, falling 2.1% y/y in the first eight months of the year. The deterioration is broad-based across industries. However, the weakness…

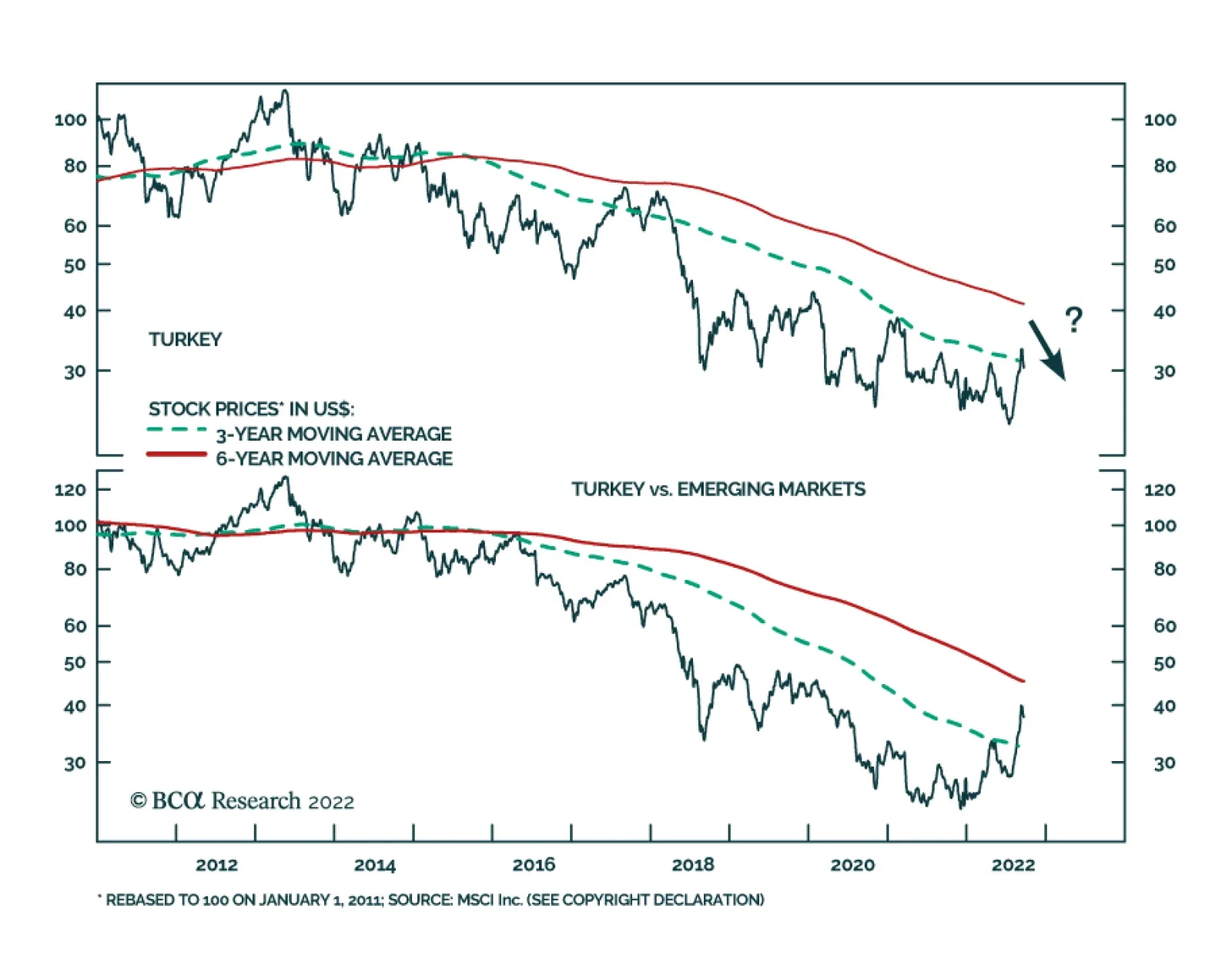

BCA Research’s Emerging Markets Strategy & Geopolitical Strategy services conclude that the Turkish equity rally will soon fade. Turkish stocks have outperformed their Emerging Markets counterparts this year in common currency terms even though the…

Executive Summary Turkey is staring into an abyss: economic crisis that will morph into political crisis in the June 2023 election cycle. President Erdoğan will pursue populist economic policies and foreign policy adventurism to try to stay in power, leading to negative surprises and “black swan” risks over the coming 9-12 months. While Erdoğan and the ruling party are likely to be defeated in elections, which is good news, investors should not try to front-run the election given high uncertainty. Neither Turkey’s economy and domestic politics nor the global economy and geopolitics warrant a bullish view on Turkish assets. GEOPOLITICAL STRATEGY Recommendation (TACTICAL) Initiation Date Return LONG JPY/TRY 2022-09-23 Erdoğan’s Net Negative Job Approval

Turkey: Before And After Erdoğan

Turkey: Before And After Erdoğan

Bottom Line: The Lira will depreciate further versus the dollar. Both Turkish stocks and local currency bonds merit an underweight stance in an EM basket. EM sovereign credit investors, however, should be neutral on Turkish sovereign credit relative to the EM sovereign credit benchmark. Feature Turkey – now technically Türkiye – is teetering on the verge of a national meltdown. The inflation rate is the fastest in G20 countries, both because of a domestic wage-price spiral and soaring global food and fuel prices. President Recep Tayyip Erdoğan and his Justice and Development Party (AKP) have been in power since 2002, making them highly vulnerable to demands for change in the general election slated for June 18, 2023. Yet Erdoğan is a strongman who won a popular vote to revise the constitution in 2017 and increase his personal power over institutions. His populist Islamist movement is starkly at odds with the country’s traditional elite, including the secular military establishment. Given the poor state of the economy, Erdoğan will likely lose the 2023 election but he could refuse to leave office … or he could win the election and be ousted in a coup d'état, as happened in Turkey in 1960, 1971, and 1980.1 Meanwhile Turkey is beset by foreign dangers – including war in Ukraine and instability in the Middle East. Erdoğan will try to use foreign policy to bolster his popular standing. Turkey has inserted itself in various regional conflicts and could instigate conflicts of its own. While global investors are eager to buy steeply discounted Turkish financial assets ahead of what could be a monumental change in national policy in 2023, the country is extremely unstable. It is a source of “black swan” risks. The best bet is to remain underweight Turkish assets unless and until a pro-market election outcome shakes off the two-decade trend toward economic ruin. Turkish Grand Strategy Turkey is permanently at a crossroads. The land-bridge between Europe and Asia, it is secular and cosmopolitan but also Islamist and traditional. Its past consists of the greatness of empires – Byzantine, Ottoman – while its present consists of a frustrating search for new opportunities in a chaotic regional context. The core of the country consists of the disjointed coastal plains around the Bosporus and Dardanelles straits and the Sea of Marmara, where Istanbul is located. The Byzantine and Ottoman empires were seated on this strategic location at the juncture of the world’s east-west trade. To secure this area, the Turks needed to control the larger Anatolian peninsula – Asia Minor – to prevent roving Eurasian powers from invading, just as they themselves had originally invaded from Central Asia. During times of greatness the Turks could also expand their empire to control the Balkan peninsula and Danube river valley up to Vienna, Crimea and the Black Sea coasts, and the eastern Mediterranean island approaches. During the Ottoman empire’s golden days Turkish power extended all the way into North Africa, Mesopotamia, the Nile river valley, and Mecca and Medina. The empire – and the Islamic Ottoman Caliphate – collapsed in 1924 after centuries of erosion and the catastrophes of World War I. Subsequently Turkey emerged as a secular republic. It adapted to the post-WWII world order by allying with the United States and NATO, in conflict with the Soviet Union which encircled the Turks on all sides. The Russians are longstanding rivals of Turkey, notably in the Black Sea and Crimea, and Stalin wanted to get his hands on the Dardanelles and Bosporus straits. Hence alliance with the US and NATO fulfilled one of the primary demands of Turkish grand strategy: a navy that could defend the straits and Turkish interests in the Black Sea and eastern Mediterranean. The collapse of the Soviet Union seemed to usher in an era of opportunity for Turkey. Turkey benefited from democratization, globalization, and foreign capital inflows. But then America’s wars and crises, Russia’s resurgence, and Middle Eastern instability created a shatter-belt surrounding Turkey, impinging on its national security. In this context of limited foreign policy options, Turkey’s domestic politics coalesced around Erdoğan, the AKP, political Islam, and investment-driven economic growth. Erdoğan and the AKP represent the Anatolian, religious, and Middle Eastern interests in Turkey, as opposed to the maritime, secular, and Euro-centric interests rooted in Istanbul. This point can be illustrated by observing that the poorer interior regions have grown faster than the national average over the period of AKP rule, whereas the more developed coastal regions have tended to lag (Map 1). Voting patterns from the 2018 general election overlap with these economic outcomes. The AKP has steered investment capital into the interior to fund infrastructure and property construction while currency depreciation, rather than productivity enhancement, has merely maintained the status quo with the manufacturing export sector in the coastal regions (Chart 1). Map 1Turkey’s Anatolian Model And The Struggle With The Coasts

Turkey: Before And After Erdoğan

Turkey: Before And After Erdoğan

Chart 1Turkey's Export Competitiveness

Turkey's Export Competitiveness

Turkey's Export Competitiveness

Today Turkey faces three distinct obstacles to its geopolitical expansion: Russian aggression: Russia’s resurgence, especially with the seizure of Crimea in 2014 and broader invasion of Ukraine in 2022, threatens Turkey’s interests in the Black Sea and eastern Mediterranean. Turkey must always deal with Russia carefully but over the past 14 years Russia has become belligerent, forcing Turkey to come to terms with Putin while maintaining the NATO alliance. Today Erdoğan tries to mediate the conflict as it does not want to encourage Russian aggression but also does not want NATO to provoke Russia. For instance, Turkey is willing to condone Finland and Sweden joining NATO but only if the West grants substantial benefits to Turkey itself. Ultimately Turkish ties with Russia are overrated. For both economic reasons and grand strategic reasons outlined above, Turkey will cleave to the West (Chart 2). Chart 2Turkey Still Linked To The West

Turkey: Before And After Erdoğan

Turkey: Before And After Erdoğan

Chart 3Turkish Energy Ties With Russia

Turkey: Before And After Erdoğan

Turkey: Before And After Erdoğan

Western liberal hegemony: The EU and NATO foreclosed any Turkish ambitions in Europe. The EU has consolidated with each new crisis while rejecting Turkish membership. This puts limits on Turkish access to European markets and influence in the Balkans. Turkey has guarded its independence jealously against the West. After the Cold War the US expected Turkey to serve American interests in the Middle East and Eurasia. The EU expected it to serve European interests as an energy transit state and a blockade against Middle Eastern refugees. But Turkish interests were often sidelined while its domestic politics did not allow blind loyalty to the West. This led Turkey to push back against the West and cultivate other options, such as deeper economic ties with Russia and China. Turkish dependency on Russian energy is substantial and Turkey has tried to play a mediating role in Russia’s conflict with NATO (Chart 3). Recently Turkey offered to join the Shanghai Cooperation Organization (SCO), a military alliance of Asian powers. However, as with trade, Turkish defense and security ties with the Russo-Chinese bloc are ultimately overrated (Chart 4). There is room for some cooperation but Turkey is not eager to abandon American military backing in a period in which Russia is threatening to control the Black Sea rim, cut off grain exports arbitrarily, and use tactical nuclear weapons. Chart 4Turkey’s Defense Alliance With The West

Turkey: Before And After Erdoğan

Turkey: Before And After Erdoğan

Middle Eastern instability: The Middle East is a potential area for Turkey to increase influence, especially given the AKP’s embrace of political Islam. Turkey benefits from regional economic development and maintains relations with all players. But the region’s development is halting and Turkey is blocked by competitors. The US toppled Iraq in 2003, which strengthened Iran’s regional clout over the subsequent decades. But Iran is not stable and the US has not prevented Iran from achieving nuclear breakout capacity. Turkey cannot abide a nuclear-armed Iran. At the same time, the US continues to support Israel and the Gulf Arab monarchies, which oppose Turkey’s combination of Islam and democratic populism. Russia propped up Syria’s regime in league with Iran, which threatens Turkey’s border integrity. Developments in Syria, Iraq, and Iran have all complicated Turkey’s management of Kurdish militancy and separatism. Kurds make up nearly 20% of Turkey’s population and play a central role in the country’s political divisions. Erdoğan’s Anatolian power base is antagonistic toward the Kurds and regional Kurdish aspirations. China’s strategic rise brings both risks and rewards for Turkey but China is too distant to become the focus of Turkish strategy: China’s dream of reviving the Silk Road across Eurasia harkens back to the glory days of Ottoman power. The Belt and Road Initiative and other investments help to develop Central Asia and the Middle East, enabling Turkey to benefit once again as the middleman in east-west trade (Chart 5). Chart 5Turkey Benefits From East-West Trade

Turkey Benefits From East-West Trade

Turkey Benefits From East-West Trade

But insofar as China’s Eurasian strategy is successful, it could someday impinge on Turkish ambitions, particularly by buttressing Russian and Iranian power. In recent years Erdoğan has experimented with projecting Turkish power in the Middle East (Syria), North Africa (Libya), the Caucasus (Armenia), and the eastern Mediterranean (Cyprus). He cannot project power effectively because of the obstacles outlined above. But he can manipulate domestic and foreign security issues to try to prolong his hold on power. Bottom Line: Boxed in by Russian aggression, western liberal hegemony, and Middle Eastern instability, Turkey cannot achieve its geopolitical ambitions and has concentrated on internal development over the past two decades. However, the country retains some imperial ambitions and these periodically flare up in unpredictable ways as the modern Turkish state attempts to fend off the chaotic forces that loom in the Black Sea, Middle East, North Africa, and Caucasus. The Erdoğan regime is focused on consolidating Anatolian control of Turkey and projecting military power abroad so that the military does not become a political problem for his faction at home. Erdoğan’s Domestic Predicament President Erdoğan has stayed in power for 20 years under the conditions outlined above but he faces a critical election by June 18, 2023 that could see him thrown from power. The result will be extreme political turbulence over the coming nine months until the leadership of the country is settled by hook or by crook. Erdoğan has pursued a strongman or authoritarian leadership style, especially since domestic opposition emerged in the wake of the Great Recession. By firing three central bankers, he has pressured the central bank into running an ultra-dovish monetary policy, producing a 12% inflation rate prior to the Covid-19 pandemic and an 80% inflation rate today. He has also embraced populist fiscal handouts and foreign policy adventurism. Taken together his policies have eroded the country’s political as well as economic stability. From the last general election in 2018 to the latest data in 2022: Real household disposable income growth has fallen from -7.4% to -18.7% (Chart 6). Chart 6Real Incomes Falling

Real Incomes Falling

Real Incomes Falling

Chart 7Turkish Activity Slows Ahead Of Election

Turkish Activity Slows Ahead Of Election

Turkish Activity Slows Ahead Of Election

The manufacturing PMI has fallen from 49.0 to 47.4 (Chart 7). Consumer confidence has fallen from 92.1 to 72.2 (Chart 8). Chart 8Consumer Confidence: Not Better Off Than At Last Election

Consumer Confidence: Not Better Off Than At Last Election

Consumer Confidence: Not Better Off Than At Last Election

Chart 9Erdoğan’s Net Negative Job Approval

Turkey: Before And After Erdoğan

Turkey: Before And After Erdoğan

Bad economic news is finally altering public opinion, with polls now shifting against the president and incumbent party: Since the pandemic erupted, Erdoğan’s approval rating has fallen from a peak of 57% to 40% today. Disapproval has Erdoğan’s risen to 54%, leaving him a net negative job approval (Chart 9). Bear in mind that Erdoğan won the election with 52.6% of the vote in 2018, only slightly better than the 51.8% he received in 2014 and well below the 80% that his AKP predecessor received in 2007. Meanwhile the AKP, which never performs as well as Erdoğan himself, has fallen from a 45% support rate to 30% today in parliamentary polls, dead even with the main opposition Republican People’s Party (Chart 10). The AKP won 42.6% of the vote in 2018, down from 49.5% in the second election of 2015, 49.8% in 2011, and 46.6% in 2007. Chart 10Justice And Development Party Neck And Neck With Republican Opposition

Turkey: Before And After Erdoğan

Turkey: Before And After Erdoğan

The gap between Erdoğan and his Republican rivals has narrowed sharply since the global food and fuel price spike began to bite in late 2021 (Chart 11). Chart 11Erdoğan Faces Tough Re-Election Race

Turkey: Before And After Erdoğan

Turkey: Before And After Erdoğan

However, the 2023 election is not straightforward. There are several caveats to the clear anti-incumbent tendency of economic and political data: Soft Economic Landing? The election takes place in nine months, enough time for surprises to salvage Erdoğan’s presidential campaign, given his and his party’s heavily entrenched rule. For example, it is possible – not probable – that Russia will resume energy exports, enabling Europe to recover, and that central banks will achieve a “soft landing” for the global economy. Turkey’s economy would bounce just in time to help the incumbent party. This is not what we expect (see below) but it could happen. Foreign Policy Victories? Erdoğan could achieve some foreign policy victories. He has negotiated a tenuous deal with Russia and Ukraine, along with the UN, to enable grain exports out of Odessa. He could build on this process to negotiate a broader ceasefire in Ukraine. He could also win major concessions from the US and NATO to secure Finnish and Swedish membership in that bloc. If he did he would come off looking like a grand statesman and might just buy another term in office. Unfortunately what is more likely is that Erdoğan will pursue an aggressive foreign policy in an attempt to distract voters from their bread-and-butter woes, only to destabilize Turkey and the region further. Stolen Election? Erdoğan revised the constitution in 2017 – winning 51.4% of the votes in a popular referendum – to give the presidency substantial new powers across the political system. Using these powers he could manipulate the election to produce a favorable outcome or even cling to power despite unfavorable election results. He does not face nearly as powerful and motivated of a liberal establishment as President Trump faced in 2020 or as Brazilian President Jair Bolsonaro faces in 2022. As noted Erdoğan has a contentious relationship with the Turkish military, so while investors cannot rule out a stolen election, they also cannot rule out a military coup in reaction to an attempted stolen election. Thus the election could produce roughly four outcomes, which we rank below from best to worst in terms of their favorability for global investors: 1. Best Case: Decisive Opposition Victory – 25% Odds – A resounding electoral defeat for the AKP would reverse its unorthodox economic policies in the short term and serve as a lasting warning to future politicians that populism and economic mismanagement lead to political ruin. This outcome would also provide the political capital and parliamentary strength necessary to impose tough reforms and restore a semblance of macroeconomic stability. 2. Good Case: Narrow AKP Defeat – 50% Odds – A narrow or contested election would produce a weak new government that would at least put a stop to the most inflationary AKP policies. It would improve global investor sentiment around Turkey’s eventual ability to stabilize its economy. The new government would lack the ability to push through structural reforms but it could at least straighten out the affairs of the central bank so as to ensure a cycle of monetary policy tightening, which would stabilize the currency. 3. Bad Case: Narrow AKP Victory – 15% Odds – A narrow victory would force the AKP to compromise with opposition parties in parliament and pacify social unrest. Foreign adventurism would continue but harmful domestic policies would face obstructionism. 4. Worst Case: Decisive AKP Victory – 10% Odds – A resounding victory for the ruling party would vindicate Erdoğan and his policies despite their negative economic results, driving Turkey further down the path of authoritarianism, populism, money printing, currency depreciation, and hyper-inflation. He could also be emboldened in his foreign adventurism. Bottom Line: We expect Erdoğan and the AKP to be defeated and replaced. However, Turkey is in the midst of an economic and political crisis and the next 12 months will bring extreme uncertainty. The election could be indecisive, contested, stolen, or overthrown. The aftermath could be chaotic as well as the lead-up. If the AKP stays in power then investors will abandon Turkey and its economy will suffer a historic shock. Therefore investors should underweight Turkey – at least until the next phase in the economic downturn confirms our forecast that the AKP will fall from power. Macro Outlook: Fade The Equity Rally Chart 12Turkish Stock Rally Will Fade Soon; Stay Underweight This Market Versus EM

Turkish Stock Rally Will Fade Soon; Stay Underweight This Market Versus EM

Turkish Stock Rally Will Fade Soon; Stay Underweight This Market Versus EM

The Turkish economy is beset by hyper-inflation. Headline consumer prices are rising at upwards of 80% and core inflation is 65%. Yet Turkish government 10-year bond yields are low and falling: they are down to 11% currently, from a high of 24% at the beginning of the year. Turkish stocks have also outperformed their Emerging Markets counterparts this year in common currency terms even though the lira has been the worst performing EM currency (Chart 12). So, what’s going on in this market? The answer is hidden in the slew of unorthodox policies adopted by the authorities. These measures caused massive distortions in both the economy and the markets. Specifically, late last year, despite very high inflation, the central bank began to cut policy rates encouraging massive loan expansion. As a result, both local currency loans and money supply surged. Which, in turn, completely unhinged inflation (Chart 13). As inflation rose, so did government bond yields. In a bid to keep government borrowing costs low, policymakers changed several bank regulations to force commercial banks to buy government bonds.2 The upshot was that the bond yields stopped tracking inflation and instead began to fall even as inflation skyrocketed. The rampant inflation meant Turkish non-financial firms’ nominal sales skyrocketed. Indeed, sales of all MSCI Turkey non-financials companies have risen by 40% in US dollar terms and 200% in local currency (Chart 14). Chart 13Massive Bank Credit And Money Growth Completely Unhinged The Inflation

Massive Bank Credit And Money Growth Completely Unhinged The Inflation

Massive Bank Credit And Money Growth Completely Unhinged The Inflation

This was at a time when policy rates were being cut. The policy rate has fallen to 12% today from 19% a year earlier. Firms’ local currency real borrowing costs have fallen deeply into negative territory (Chart 15). It helped reduce firms’ costs significantly. Chart 14Surging Sales Amid Deeply Negative Real Borrowing Costs Boosted Firms' Profits

Surging Sales Amid Deeply Negative Real Borrowing Costs Boosted Firms' Profits

Surging Sales Amid Deeply Negative Real Borrowing Costs Boosted Firms' Profits

Chart 15Policy Rates Are Being Cut Even As The Inflation Reigns Havoc

Policy Rates Are Being Cut Even As The Inflation Reigns Havoc

Policy Rates Are Being Cut Even As The Inflation Reigns Havoc

Chart 16Wage Costs Have Risen Too, But Not As Much As Inflation

Wage Costs Have Risen Too, But Not As Much As Inflation

Wage Costs Have Risen Too, But Not As Much As Inflation

Meanwhile, even though wage growth accelerated, it still fell short of inflation, and therefore of nominal sales of the firms (Chart 16). Firms’ wage costs did not rise as much as their prices. All this boosted non-financial firms’ margins. Total profits have risen by 35% in US dollar terms from a year earlier (200% in lira terms). Chart 17The Deluge Of Money Has Led All Kinds Of Asset Prices To Skyrocket

The Deluge Of Money Has Led All Kinds Of Asset Prices To Skyrocket

The Deluge Of Money Has Led All Kinds Of Asset Prices To Skyrocket

On their part, listed financials’ profits have surged by 50% in USD terms and 220% in local currency terms. They benefited both from surging interest income due to rapid loan growth and from massive capital gains on their holding of government securities (see Chart 14 above). All this is reflected in Turkish companies’ earnings per share as well. The spike in EPS has propped up Turkish stocks for past few months. Over the past year, not only have corporate profits and share prices surged, but also house prices have skyrocketed by 170% in local currency terms and 30% in USD terms (Chart 17). In sum, the abnormally low nominal and deeply negative real borrowing costs have produced a money/credit deluge, which has generated a massive inflationary outbreak and has inflated revenues/profits as well as various asset prices. The Lira To Depreciate Further This macro setting is a recipe for a major currency sell-off. First, Europe – the destination of 90% of Turkish exports – will likely slide into recession over the coming year (Chart 18). Chart 18A Slowing Europe Will Materially Dent Turkish Growth Too

A Slowing Europe Will Materially Dent Turkish Growth Too

A Slowing Europe Will Materially Dent Turkish Growth Too

A fall in exports will widen Turkey’s current account deficit. Notably, imports will not fall much since the authorities are pursuing easy money policy. Second, the lack of credible macro policies as well as political crisis will assure that foreign capital escapes Turkey. Turkey will find the current account deficit nearly impossible to finance. Third, the country’s net foreign reserves, after adjusting for the central bank’s foreign currency borrowings and commercial banks’ deposits with the central bank, stand at minus 30 billion dollars. In other words, the central bank now has large net US dollar liabilities. As such, it has little wherewithal to defend the currency. There are very high odds that the lira depreciation will accelerate in the months ahead. Fourth, the slew of unorthodox measures taken by the Turkish authorities will encourage banks to buy more government local currency bonds to suppress the government’s borrowing costs. When commercial banks buy government securities from non-banks, they create money “out of thin air.” Hence, the ongoing money supply deluge will continue. This is bearish for the currency. Notably, the economy will likely enter into recession next year – and yet core inflation will stay very high (30% and above). Recent unorthodox bank regulations are meant to encourage a certain kind of lending – loans to farmers, exporters, and small and medium-sized businesses – while discouraging other kinds. Consequently, the overall loan growth will likely slow in nominal terms. There are already signs that credit is decelerating on the margin (Chart 19). Given the very high inflation, slower credit growth will likely lead to a liquidity crunch for many businesses – forcing them to curtail their activity. Chart 19Bank Credit Will Decelerate Due To Many Unorthodox Bank Regulations

Bank Credit Will Decelerate Due To Many Unorthodox Bank Regulations

Bank Credit Will Decelerate Due To Many Unorthodox Bank Regulations

Chart 20Bank Loans Are Already Contracting in Real Terms: Not a Good Omen For Real GDP

Bank Loans Are Already Contracting in Real Terms: Not a Good Omen For Real GDP

Bank Loans Are Already Contracting in Real Terms: Not a Good Omen For Real GDP

Indeed, in real terms (deflated by core CPI), local currency loan growth has already slipped into negative territory. This is a bad omen for the overall economy: contracting real loan growth is a harbinger of recession (Chart 20). In short, Turkey is looking into an abyss: a recession amid high inflation (i.e., stagflation) as well as a brewing political crisis (with Erdoğan likely doubling down on unorthodox and populist policies). All this point to another period of a large currency depreciation. While the country will likely change direction to avoid the abyss, investors should wait to allocate capital until after the change in direction is confirmed. Investment Takeaways The Turkish lira will fall much more vis-à-vis the US dollar in the year ahead. Both Turkish stocks and local currency bonds merit an underweight stance in an EM basket. EM sovereign credit investors, however, should be neutral on Turkish sovereign credit relative to the EM sovereign credit benchmark. Turkey is involved in an economic crisis that will devolve into a political crisis over the election cycle. While Erdoğan and the AKP are likely to fall from power as things stand today, they are heavily entrenched and will be difficult to remove, creating large risks of an indecisive or contested election in 2023 that will increase rather than decrease policy uncertainty and the political risk premium in Turkish assets. As a strongman leader Erdoğan has consolidated political power in his own hands, so there is no one to take the blame for the country’s economic mismanagement – other than foreigners. Hence there is a distinct risk that his foreign policy adventurism will escalate between now and next year, resulting in significant military conflicts or saber-rattling. These will shake out western investors who try to speculate on the likelihood that the election or the military will oust Erdoğan and produce sounder national and economic policies. That outcome is indeed likely but Erdoğan is not going without a fight. Our Geopolitical Strategy also recommends tactically shorting the lira versus the Japanese yen in light of global slowdown, extreme geopolitical risk, and the Bank of Japan’s desire to prevent the yen from falling too far. Matt Gertken Chief Geopolitical Strategist mattg@bcaresearch.com Rajeeb Pramanik Senior EM Strategist rajeeb.pramanik@bcaresearch.com Andrija Vesic Consulting Editor Footnotes 1 Sinan Ekim and Kemal Kirişci, “The Turkish constitutional referendum, explained,” Brookings Institution, April 13, 2017, brookings.edu. 2 The central bank replaced an existing 20% reserve requirement ratios for credits with a higher 30% treasury bond collateral requirement. Lenders will have to cut interest rates on commercial loans (except for loans to farmers, exporters, and SMEs). Otherwise, banks will have to maintain additional securities. Strategic Themes Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months) Regional Geopolitical Risk Matrix