Emerging Markets

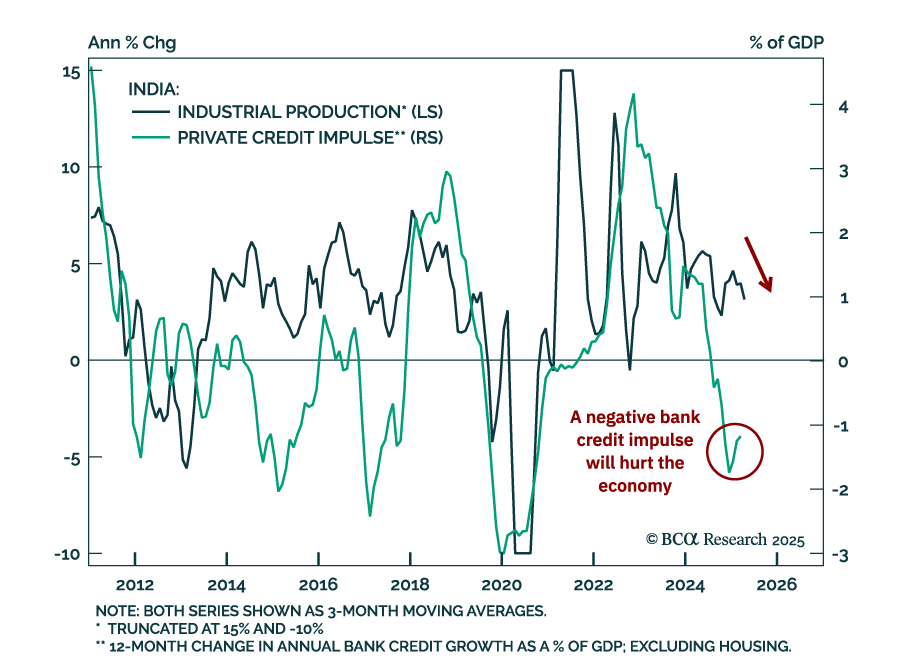

Industrial activity in India is deteriorating, which will weigh on a stock market that’s priced for perfection. Indian industrial production slowed to 2.7% year-on-year in April compared to 3.9% in March. The economic slowdown will gain traction in…

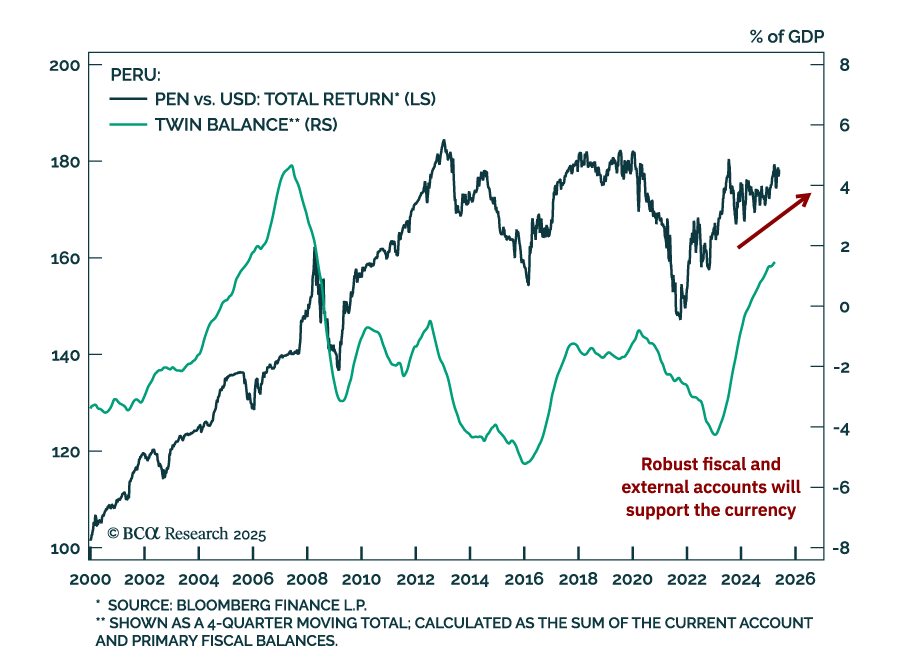

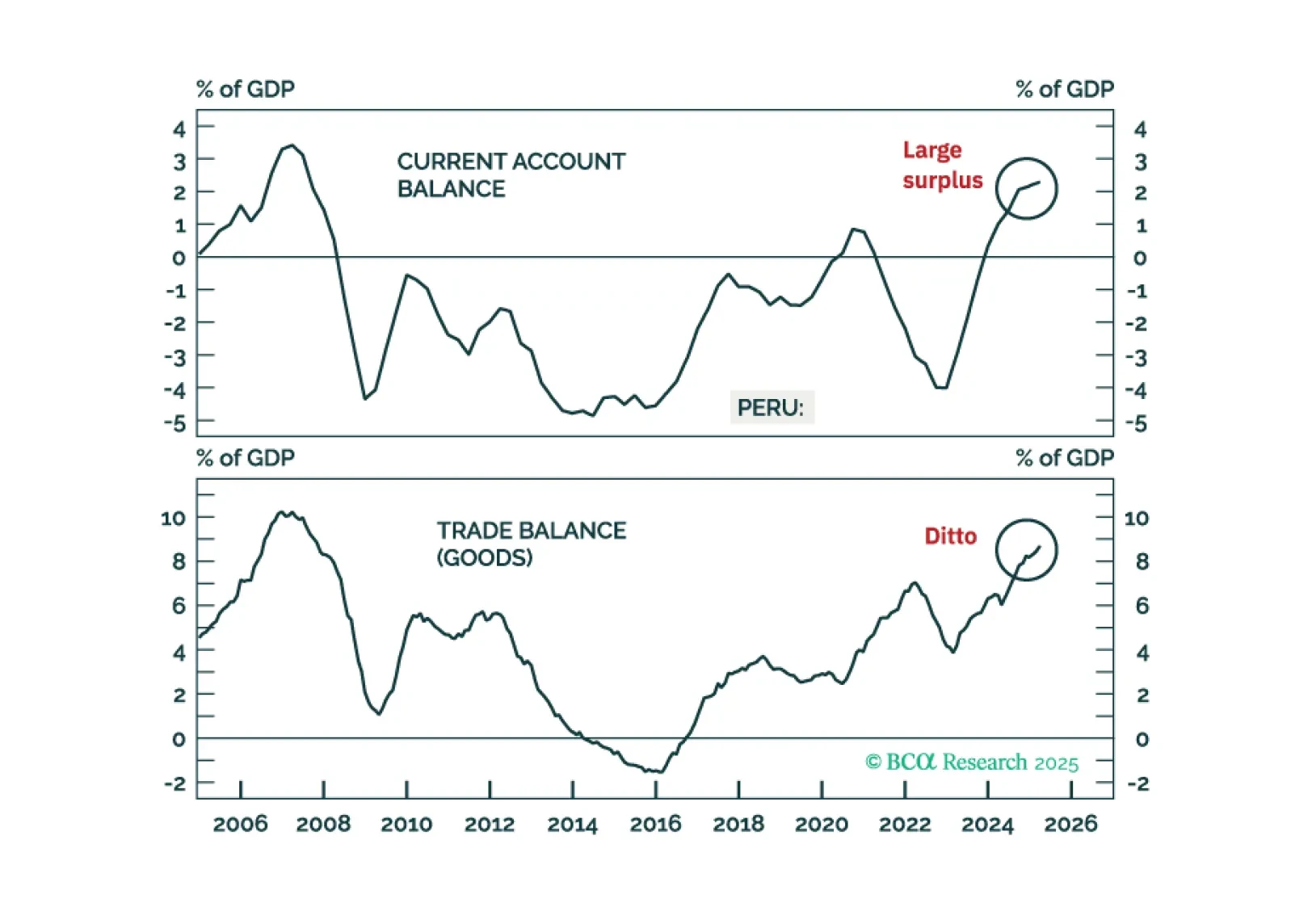

Peru’s economic resilience will help its markets outperform their EM peers. A global growth downturn will weigh on EM assets in absolute terms, but Peruvian markets offer attractive tradeable opportunities. The Andean nation has much better macro…

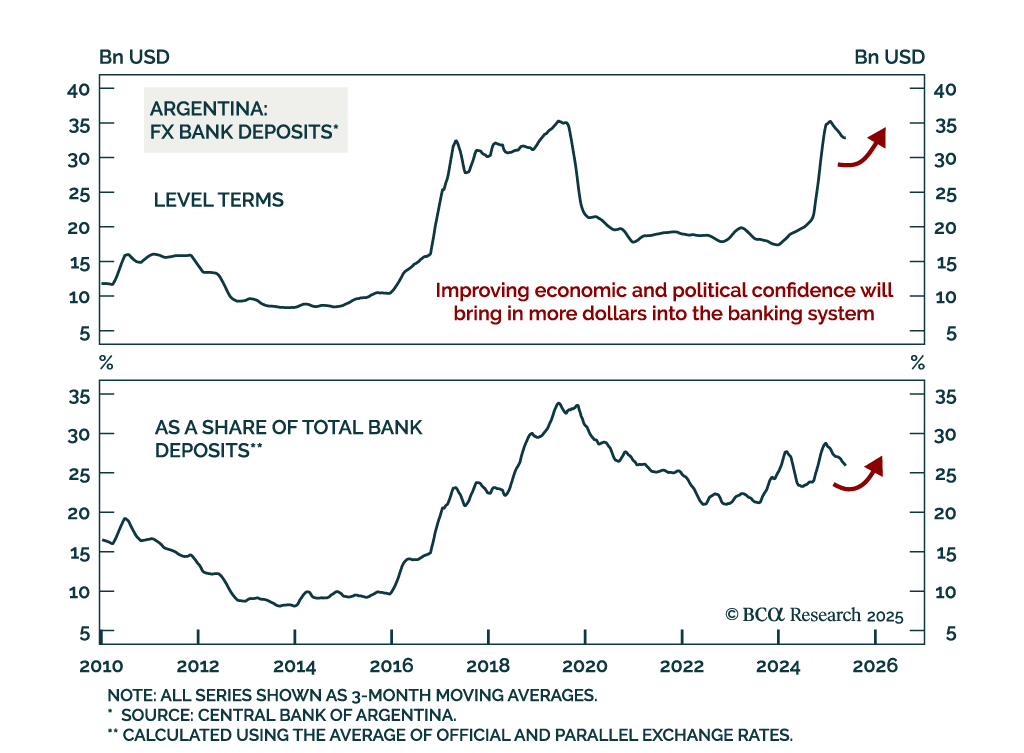

The latest political developments in Argentina increase the odds of further liberalizing reforms and solidify the economy’s structural upside. First, the libertarian governing party came out on top in Buenos Aires’ legislative elections. While municipal…

Peru’s economic resilience will help its markets outperform their EM peers. Domestic macro fundamentals are robust, and strong external accounts will lead to a stable-to-strengthening currency versus the US dollar. Overweight Peruvian equities, local bonds, and sovereign credit relative to their respective EM benchmarks, and go long 10-year domestic bonds (currency unhedged).

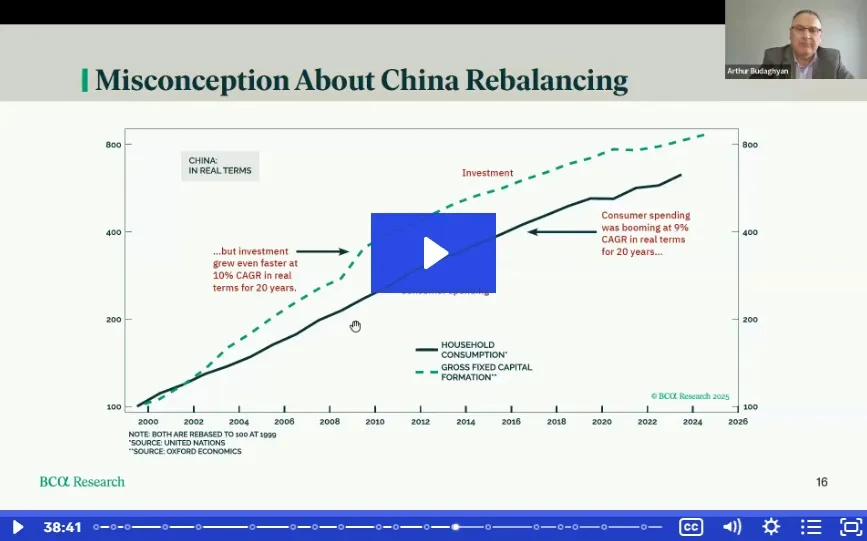

We are pleased to share the replay of Emerging Markets Webcast "China's Rebalancing, Global Trade, And The US Dollar", hosted by Chief EM & China Strategist Arthur Budaghyan.

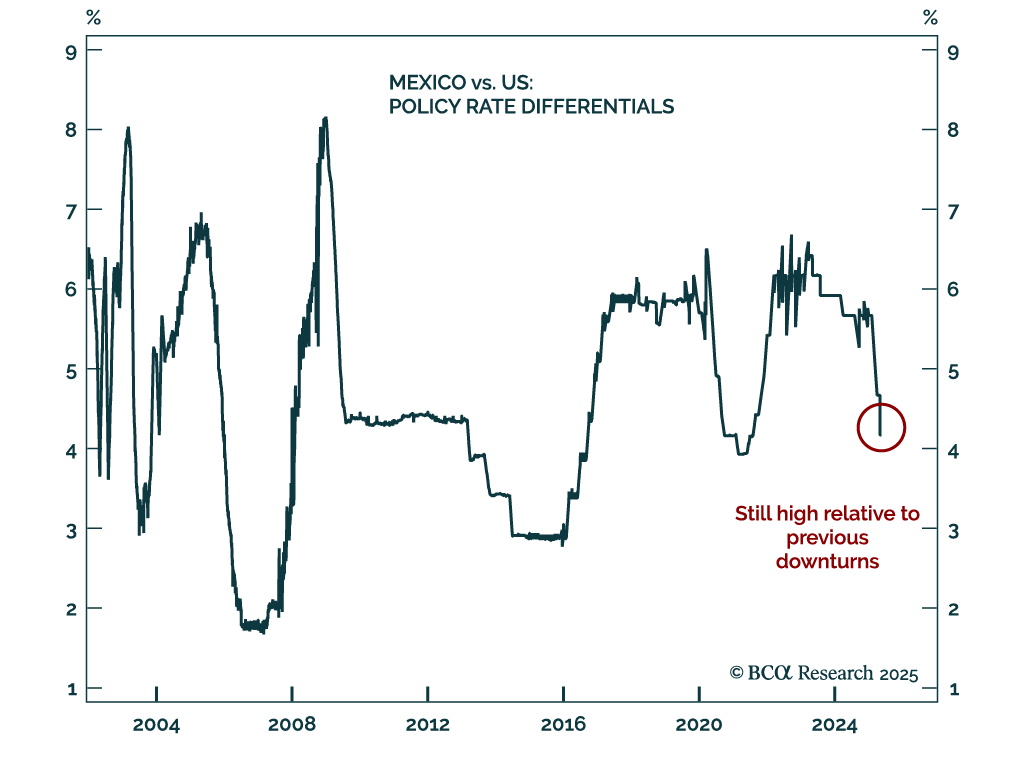

Banxico’s 50 bps rate cut reinforces our bullish view on Mexican bonds, with easing likely to continue as inflation falls and growth slows. The central bank unanimously lowered its policy rate to 8.5%, and we expect further cuts ahead as Mexico heads toward a…

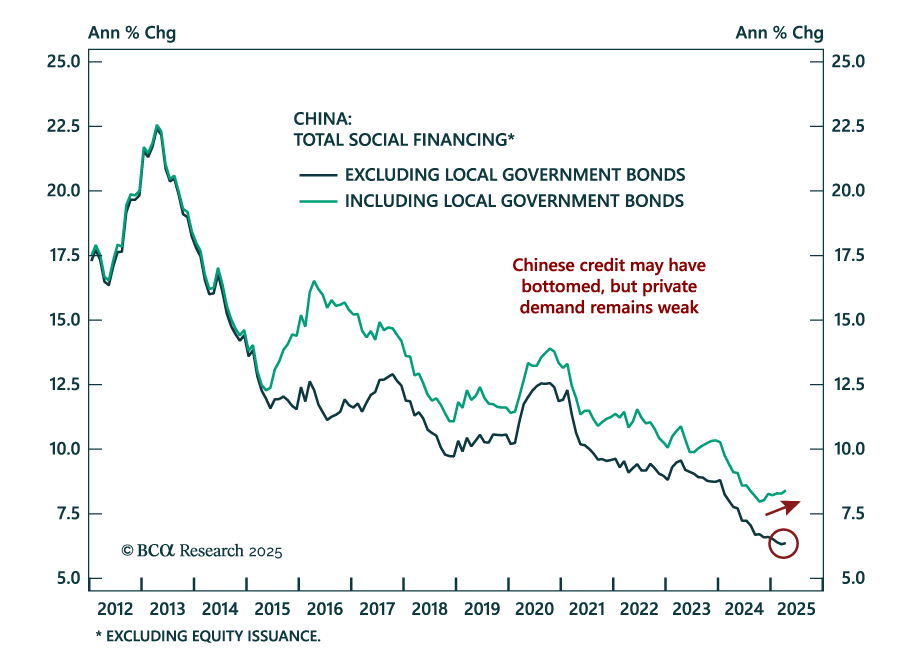

China’s weak April credit data reinforces the case for defensive positioning, with policy aimed at stability, not recovery. New yuan loans and aggregate financing both rose less than expected. While credit growth may have bottomed, it remains public-sector…

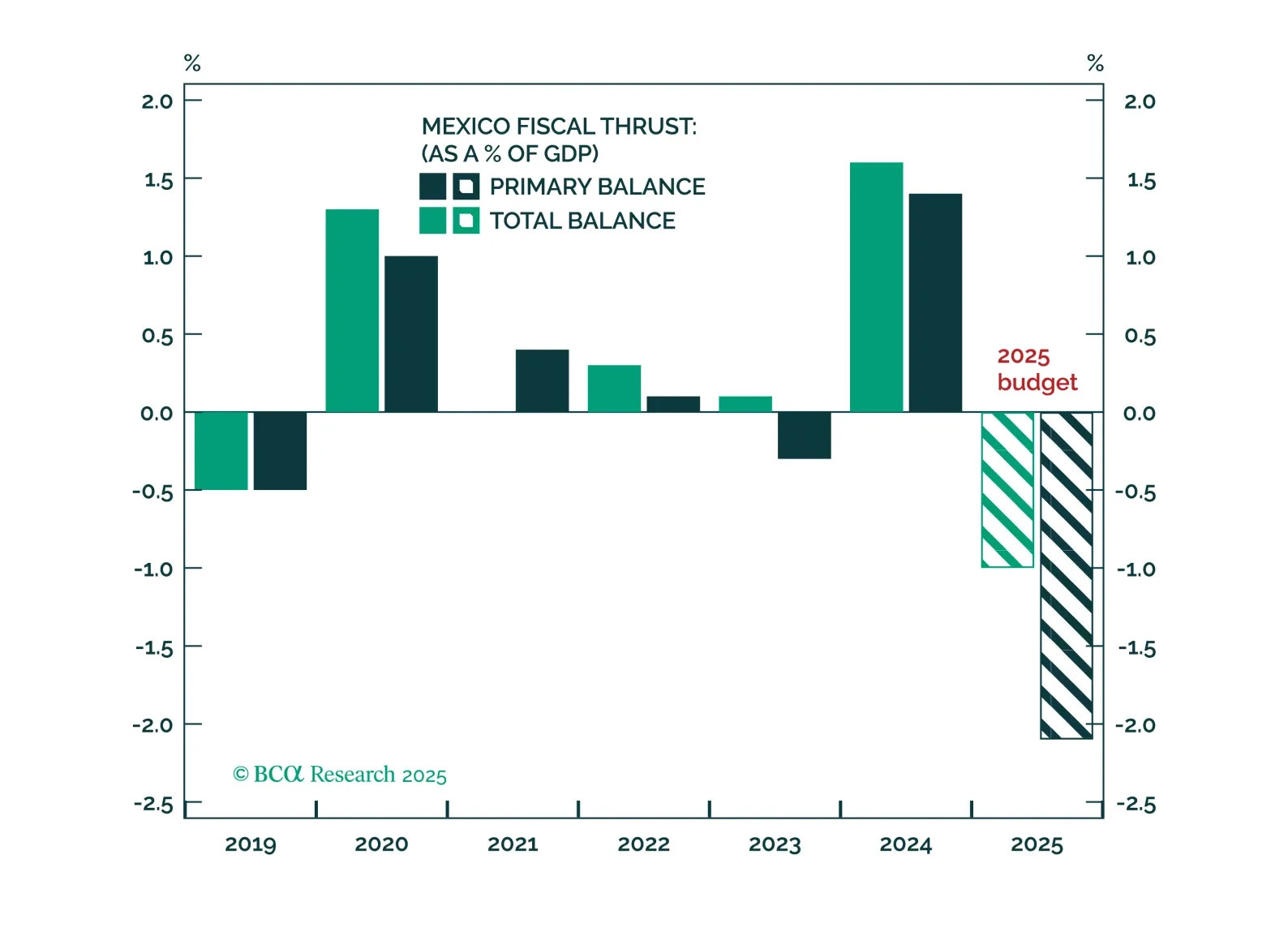

Short-term pain from Trump-related concessions, fiscal tightening amid a US and Mexican slowdown, and rising labor slack will weigh further on Mexican assets. But long-run, policy direction will capitalize on the nearshoring trend and resume the trend of Mexican asset outperformance relative to other emerging markets.

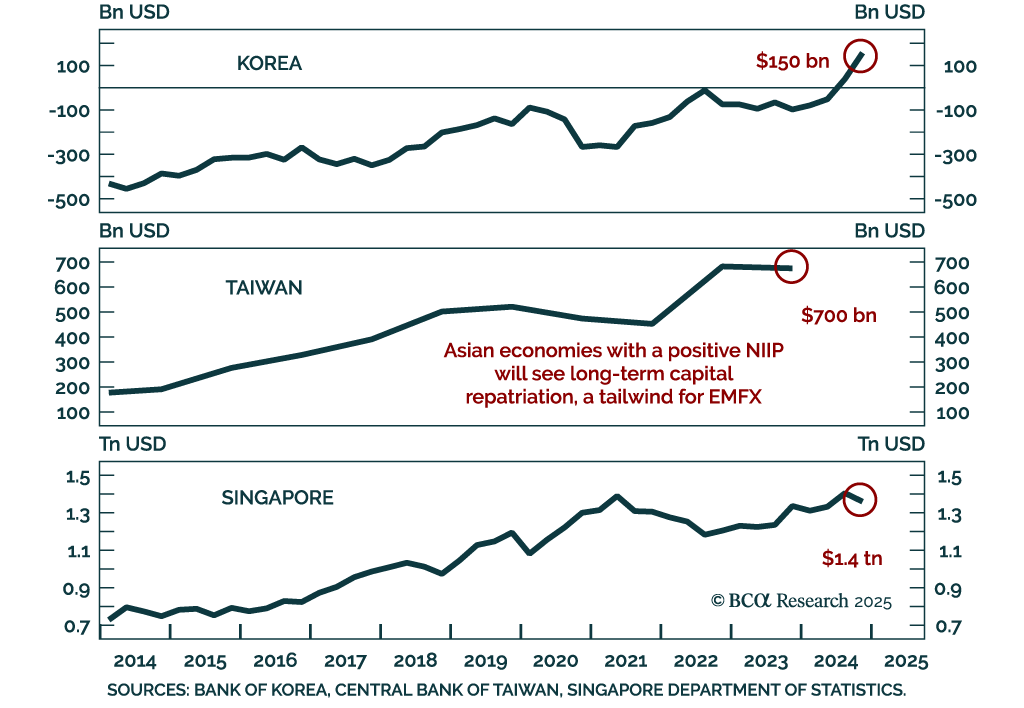

Our EM strategists see rising odds of a structural regime shift in Emerging Asian currencies. However, they expect a USD rebound and are looking to close short positions in IDR, PHP, and TWD. Severe deflationary shocks will drive down interest rates across…

Our Portfolio Allocation Summary for May 2025.