Emerging Markets

Executive Summary Credit Demand Collapsed

Credit Demand Collapsed

Credit Demand Collapsed

Business activity data from April showed a broad-based contraction in China’s economy. Credit growth tumbled as demand collapsed. Bank loan expansion slowed by the most in nearly five years and annual change in new household loans declined to an all-time low. Exports decelerated sharply in April. China’s export sector faces headwinds from Omicron-related supply chain disruptions and weakening global demand for goods. Export growth will rebound following the resumption of business activity in China’s major cities, but is set to decelerate from 2021 as external demand for goods weakens. The PBOC lowered the 5-year loan prime rate (LPR) by 15bps last Friday, following a cut in the floor rate of first-home mortgages to 20bp below the benchmark. These moves will help to arrest the ongoing deep contraction in the property market. However, these policies alone will not generate strong recovery in housing demand, amid near-term Covid-related disruptions and dampened household income growth. Barring major lockdowns, China’s economy will likely bottom around mid-2022. We expect a muted recovery in the second half of the year, despite an acceleration in policy easing. From a cyclical perspective, we continue to recommend a neutral allocation to Chinese onshore stocks in a global portfolio. Bottom Line: China’s economy has been hit by a relapse in demand and Covid-induced production disruptions. The economy will likely bottom by mid-year, but the ensuing recovery may be subdued. A Subdued Recovery In 2H 2022 A broad-based contraction in China’s economy in April reflects hit by a combination of slumping domestic demand and Covid-related disruptions. Growth in retail sales and industrial production contracted from a year ago and home sales shrunk further. Economic activity will rebound when the current Covid wave is under control and lockdown restrictions are lifted. However, we expect a much more muted recovery in the second half of this year compared with two years ago when China’s economy staged an impressive V-shaped recovery as it emerged from the first wave of lockdowns in spring 2020. Presently, reported virus cases have steadily declined in cities in the Yangtze River region, including Shanghai which aims to lift its lockdown on June 1st. The number of regions and cities under stringent confinement also fell. However, China firmly maintains its dynamic zero-Covid policy, which means tight mobility restrictions and some forms of lockdowns will occur across the country on a rolling basis going forward. China’s leadership has stepped up its pro-growth policy measures, such as a 15bps cut in the 5-year LPR last week. Given the pace of credit expansion collapsed in April and private-sector sentiment remains in the doldrums, a recovery will not be imminent or strong despite this rate cut (Chart 1). In the near term, the poor economic outlook in China, coupled with jitters in the global equity market, will continue to depress the performance of Chinese stocks in absolute terms (Chart 1, bottom panel). From a cyclical perspective, we maintain our neutral view on China’s onshore stocks and underweight view on China’s investable stocks within a global equity portfolio. China’s economy is set to underwhelm investor expectations and stock prices probably are unlikely to outperform their global counterparts (Chart 2). Chart 1Weak Economic Fundamentals Undermine Stock Performance

Weak Economic Fundamentals Undermine Stock Performance

Weak Economic Fundamentals Undermine Stock Performance

Chart 2Too Early To Upgrade Chinese Stocks In A Global Portfolio

Too Early To Upgrade Chinese Stocks In A Global Portfolio

Too Early To Upgrade Chinese Stocks In A Global Portfolio

Qingyun Xu, CFA Associate Editor qingyunx@bcaresearch.com Credit Growth Slowed Notably As Loan Demand Slumps Credit expansion in April relapsed, as lockdowns exacerbated the weakness in business activity and further depressed the demand for credit. Bank loan growth plummeted to its worst level in almost five years (Chart 3). Notably, annual change in new household loans origination contracted the most since data collection began because Covid lockdowns and the property market slump sapped consumers’ willingness to borrow (Chart 4). In addition, household propensity to spend declined to an all-time low, highlighting that bleak sentiment will continue to curb demand for loans (Chart 4, bottom panel). Moreover, a rapid deceleration in corporate medium-and long-term loans versus soaring short-term bill financing indicates corporates’ weak demand for credit and investment (Chart 5). The deterioration in corporate sentiment is also reflected in business condition surveys (Chart 6). Chart 3Subdued TSF Growth Due To Collapsed Loan Demand

Subdued TSF Growth Due To Collapsed Loan Demand

Subdued TSF Growth Due To Collapsed Loan Demand

Chart 4Annual Change In New Household Loans Contracted The Most In April

Annual Change In New Household Loans Contracted The Most In April

Annual Change In New Household Loans Contracted The Most In April

Chart 5Corporate Demand For Credit Remains in The Doldrums …

Corporate Demand For Credit Remains in The Doldrums...

Corporate Demand For Credit Remains in The Doldrums...

Chart 6... And Unlikely To Turn Around Soon Despite Accommodative Monetary Conditions

...And Unlikely To Turn Around Soon Despite Accommodative Monetary Conditions

...And Unlikely To Turn Around Soon Despite Accommodative Monetary Conditions

Chart 7Early Signs Of Authorities Loosening Their Grip On Shadow Banking

Early Signs Of Authorities Loosening Their Grip On Shadow Banking

Early Signs Of Authorities Loosening Their Grip On Shadow Banking

Local government bond issuance unexpectedly moderated in April after most of the front-loaded local government special purpose bonds (SPBs) was issued in Q1. In the January-April period this year, the amount of SPBs issuance was RMB 1.41 trillion. The SPBs quota for 2022 is 3.65 trillion, along with 1.1 trillion of SPB proceeds that can be carried over from last year. Given that most of the planned SPBs will be issued by the end of June, we will likely see a peak in SPB issuance in Q2.This entails about RMB 3 trillion of SPBs will be issued in May-June. The intensified SPB issuance will underpin total social financing (TSF) growth in the next two to three months. However, barring an increase in the SPB quota or an approval to issue Special Treasury bonds as occurred in 2H 2020, the support from government bonds issuance to TSF will likely decline sharply in the second half of this year. Notably, there has been stabilization in shadow bank financing growth, although it remains below zero (Chart 7). It may be an early sign that China’s leadership is allowing some shadow banking activity; a meaningful relaxation of local governments’ shadow banking activity would be positive for infrastructure investment. Exports: Weaker Than Last Year China’s exports growth softened sharply in April, led by an extensive reduction in shipments to major developed markets (Chart 8). In addition, exports by product group also indicate a wide ranging slowdown in both exports of lower-end consumer goods and tech products (Chart 9). The softness in China’s exports reflects Omicron-related supply chain and logistical disruptions along with a weakening external demand for goods. Chart 8China's Exports To Developed Markets Fell

China's Exports To Developed Markets Fell

China's Exports To Developed Markets Fell

Chart 9A Broad-Based Decline Among Categories of Exported Goods

A Broad-Based Decline Among Categories of Exported Goods

A Broad-Based Decline Among Categories of Exported Goods

Chart 10Weakening Global Demand For Goods

Weakening Global Demand For Goods

Weakening Global Demand For Goods

South Korean exports, a bellwether for global trade, have also been easing in line with Chinese exports, which indicates dwindling global demand for manufacturing goods (Chart 10). In addition, the sharp underperformance of global cyclical stocks versus defensives heralds a worldwide manufacturing downturn (Chart 11). Falling US demand for consumer goods corroborates diminishing external demand (Chart 12). China’s exports will likely rebound from its April levels when manufacturing production resumes in Shanghai and supply-chain interruptions subside in the Yangtze River Delta region. Nonetheless, we expect a contraction in exports this year, as global consumer demand for goods dwindles. Chart 11Global Manufacturing Sector Is Heading Into A Downturn

Global Manufacturing Sector Is Heading Into A Downturn

Global Manufacturing Sector Is Heading Into A Downturn

Chart 12External Demand For Chinese Export Goods Is Dwindling

External Demand For Chinese Export Goods Is Dwindling

External Demand For Chinese Export Goods Is Dwindling

Recovery In China’s Manufacturing Sector Will Be Muted In 2H 2022 Manufacturing production growth contracted in April at the fastest rate since data collection began. The contraction was due to Covid-induced production troubles and weak demand (Chart 13). Chart 13Manufacturing Output Growth Contracted The Most Since Data Reporting Began

Manufacturing Output Growth Contracted The Most Since Data Reporting Began

Manufacturing Output Growth Contracted The Most Since Data Reporting Began

Chart 14Mounting Product Inventory

Mounting Product Inventory

Mounting Product Inventory

Chart 15Chinese Manufacturing Output And Capacity Utilization Face Headwinds From Weakening Exports

Chinese Manufacturing Output And Capacity Utilization Face Headwinds From Weakening Exports

Chinese Manufacturing Output And Capacity Utilization Face Headwinds From Weakening Exports

The inventory of finished products soared to the highest point in the past 10 years due to port closures and domestic logistical issues (Chart 14). Even when the impact of the current Covid wave wanes in the second half of this year, destocking pressures will dampen manufacturing production. In addition, Chinese manufacturing output and capacity utilization face headwinds from decelerating exports (Chart 15). While upstream industries, such as the mining, resources and materials sectors, benefit from strong pricing trends, profit margins for middle-to-downstream manufacturers remain very subdued (Chart 16). The large gap between prices for producer goods and consumer goods is a reflection of the inability of manufacturers to pass on higher input costs to consumers (Chart 17). Elevated input cost pressures and, hence, disappointing corporate profits, will continue to curb manufacturing investments and production in 2H 2022. Chart 16Manufacturing Sector's Profit Margins Are Further Squeezed

Manufacturing Sector's Profit Margins Are Further Squeezed

Manufacturing Sector's Profit Margins Are Further Squeezed

Chart 17Manufacturers Are Under Rising Cost Pressures

Manufacturers Are Under Rising Cost Pressures

Manufacturers Are Under Rising Cost Pressures

Housing Market Outlook Remains Gloomy The PBOC lowered the 5-year LPR by 15bps from 4.6% to 4.45% on May 20, the largest LPR rate cut since 2019. The easing measure followed a reduction in first-home mortgages to 20bps below the benchmark announced on May 15. The national-level mortgage rate floor and benchmark rate drops are clear signals that policymakers are ramping up policy easing measures in the property sector, given the failure of previous efforts to revive housing demand. Historically, mortgage rates tend to lead household loans and home sales by two quarters, suggesting that the housing market may see some improvement by year-end (Chart 18). However, as we pointed out in previous reports, without large-scale and direct fiscal transfers to consumers to boost household income, these housing measures will unlikely generate a strong rebound in household sentiment and home purchases (Chart 19). Chart 18Mortgage Rates Tend To Lead Consumer Loans And Home Sales By Two Quarters

Mortgage Rates Tend To Lead Consumer Loans And Home Sales By Two Quarters

Mortgage Rates Tend To Lead Consumer Loans And Home Sales By Two Quarters

Chart 19Housing Market Sentiment Shows Little Signs Of Revival

Housing Market Sentiment Shows Little Signs Of Revival

Housing Market Sentiment Shows Little Signs Of Revival

Lockdowns in April exacerbated the slump in all housing market indicators, with the exception of a moderate improvement in floor space completed (Chart 20). Home prices, which tend to lead housing starts, decelerated even more in April following seven consecutive month-to-month declines. Moreover, our housing price diffusion index suggests that home prices on a year-on-year basis will contract in the next six to nine months, a further drop from the current 0.7% growth (Chart 21, top panel). Falling home prices will curb housing starts and construction activity (Chart 21, bottom panel). In addition, real estate developers’ financing conditions have not improved because the “three red lines” policy is still in place and home sales have collapsed (Chart 22). Chart 20A Further Deterioration In Housing Market Indicators In April

A Further Deterioration In Housing Market Indicators In April

A Further Deterioration In Housing Market Indicators In April

Chart 21Housing Prices Are Set To Contract In 2H 2022

Housing Prices Are Set To Contract In 2H 2022

Housing Prices Are Set To Contract In 2H 2022

Chart 22Slumping Home Sales Exacerbate Real Estate Developers’ Funding Woes

Slumping Home Sales Exacerbate Real Estate Developers' Funding Woes

Slumping Home Sales Exacerbate Real Estate Developers' Funding Woes

A Collapse In Household Consumption Due To Covid Confinement Measures City lockdowns have taken a heavy toll on China’s household consumption. Both retail sales and service sector business activity experienced their deepest contractions since March 2020 (Chart 23). Notably, the growth of online goods sales slipped under zero in April, below that recorded in early 2000 and the first contraction since data collection began. Furthermore, both core and service consumer prices (CPI) weakened again in April, reflecting lackluster consumer demand (Chart 24). Chart 23Chinese Retail Sales Contracted The Most Since March 2020

Chinese Retail Sales Contracted The Most Since March 2020

Chinese Retail Sales Contracted The Most Since March 2020

Chart 24Weak Core And Service CPIs Also Reflect Lackluster Household Demand

Weak Core And Service CPIs Also Reflect Lackluster Household Demand

Weak Core And Service CPIs Also Reflect Lackluster Household Demand

Labor market dynamics went downhill rapidly. The nationwide urban unemployment rate rose to its highest level since mid-2020, while the unemployment rate among younger workers climbed to an all-time high (Chart 25). Meanwhile, sharply slowing wage growth since mid-2021 has contributed to a deceleration of household income (Chart 26). The gloomy sentiment on future income also impedes a household’s willingness to consume (Chart 27). Chart 25Labor Market Situation Is Dramatically Worse

Labor Market Situation Is Dramatically Worse

Labor Market Situation Is Dramatically Worse

Chart 26Household Income Growth Has Been Falling

Household Income Growth Has Been Falling

Household Income Growth Has Been Falling

All in all, China’s household consumption will be hindered not only by renewed threats from flareups in domestic COVID-19 cases, but also by a worsening labor market situation and depressed household sentiment in the medium term. Chart 27Poor Sentiment On Funture Income Contributes To Consumers' Unwillingness To Spend

Poor Sentiment On Funture Income Contributes To Consumers' Unwillingness To Spend

Poor Sentiment On Funture Income Contributes To Consumers' Unwillingness To Spend

Table 1China Macro Data Summary

A Subdued Recovery In 2H 2022

A Subdued Recovery In 2H 2022

Table 2China Financial Market Performance Summary

A Subdued Recovery In 2H 2022

A Subdued Recovery In 2H 2022

Strategic Themes Cyclical Recommendations

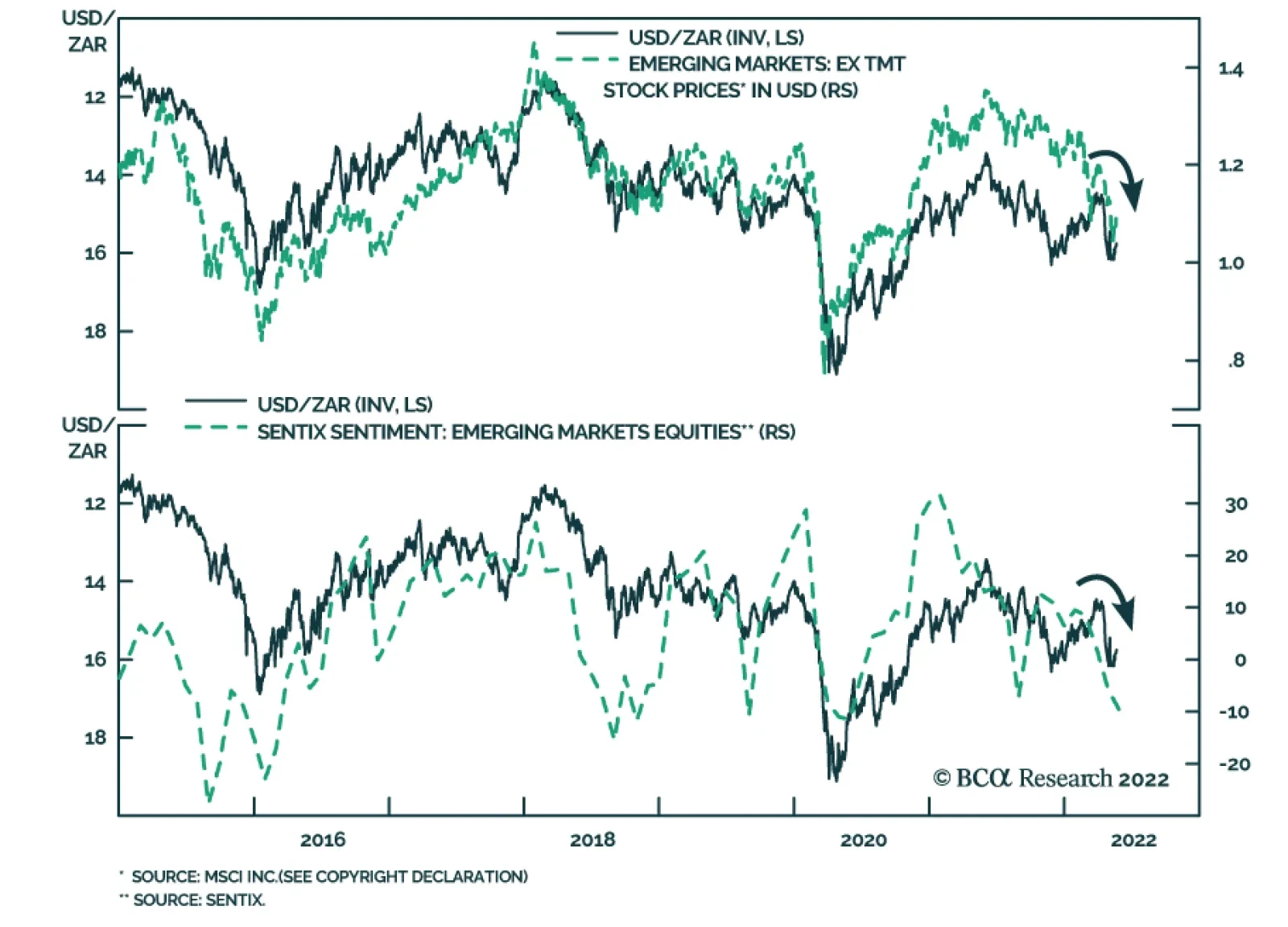

After a resilient first quarter, the South African rand experienced a sharp late-April selloff that brought it back down near late-2021 lows. However, the currency has been appreciating over the past week, recouping some of the losses. Is the rand likely to…

Executive Summary Villains Still Lurking

Villains Still Lurking

Villains Still Lurking

European assets and the euro already discount a significant worsening of Europe’s economic outlook. If the global economic situation were to stabilize, then European assets would be a buy at current levels. However, there remain very large risks lurking over the outlook. First, a further deterioration in energy flows between Russia and the EU is a major threat to the European economic outlook. Second, the ECB delivering the seven rate hikes priced in the June 2023 Euribor contract would be painful for the European economy. Third, further selloff in the US equity market could translate into more pain for European equities. And fourth, the weakness in the Chinese economy and aggressive monetary tightening in the broader EM space outside China are additional risks. These risks loom large enough, so that investors should avoid bottom-fishing the market. Wait until greater clarity emerges or valuations improve further. Bottom Line: Don’t be a hero. European assets and the euro are probably in the process of bottoming. However, the probability of a very significant additional decline is large enough that investors should continue to emphasize capital preservation over return maximization. Also, continue to favor defensives over cyclical assets. After declining nearly 8% since its January 2021 peak, the euro is down another 7% so far this year. Meanwhile, the Dow Jones Euro STOXX 50, which has plunged 17% since its January 5, 2022 apex, or 22% in US dollar terms, trades at 11.2 times 2023 earnings estimates. At these valuations, European assets already discount a major growth slump in Europe. Is it time to buy European assets, to favor cyclicals versus defensives, and to buy the euro? At face value, the answer is “yes,” but uncertainty abounds, which means that capital preservation remains paramount. As a result, we recommend investors avoid bottom-fishing European assets. They should wait for a safer entry point, rather than trying to pick through the market trough. Plenty Of Risks Four main risks cast a long shadow on the performance of European assets: The evolution of the energy crisis, the potential for an ECB policy mistake, the threat of a worsening US selloff, and the instability in EM. The Energy Crisis It’s official: Sweden and Finland are applying to join NATO. Turkey’s objection will create delays in the process, but it will not stop it. Turkey needs protection against Russia, and it needs help to support the lira. Turkey’s acquiescence, therefore, will be bought. What is genuinely surprising is Russia’s silence. President Putin threatened to flex Russia’s military muscles if Sweden and Finland were to abandon their neutrality. Yet, he now has “no problem” with their bid to join the alliance. We are skeptical, especially as the EU is aiming to ban Russian oil imports by the end of the year. Based on these observations, we continue to see a further deterioration in energy flows between Russia and the EU as a major threat to the European economic outlook. It is far from a guaranteed outcome, but its probability is elevated enough (more than 30%) and so impactful that any investment strategy must account for it. Chart 1Rebuilding Nat Gas Stocks Is A Must

Don’t Be A Hero

Don’t Be A Hero

Chart 2Low-Income Households Are At Risk

Don’t Be A Hero

Don’t Be A Hero

Moreover, European nations continue to pay a premium for their energy and are trying to rebuild their natural gas inventory ahead of winter (Chart 1). Thus, the energy market continues to carry a significant recession risk for the Eurozone. Lower-income households already spend a substantial portion of their income on utilities and transportation costs, and their consumption is highly sensitive to the evolution of energy prices (Chart 2). A Policy Mistake We consider a rate hike in July a policy mistake, but it would be a true error if the ECB ratified the pricing currently embedded in the €STR curve (Chart 3). Why would a rate hike constitute a policy mistake? The EU’s inflation spike is not a reflection of strong domestic demand. It reflects foreign factors over which the ECB has no control. Energy prices drive European inflation and are passing-through to core CPI (Chart 4). Yet, wage growth remains tepid at 2.6%. Hiking rates will not bring about the additional energy supply Europe needs to tame inflation. Chart 3Too Far Too Fast

Too Far Too Fast

Too Far Too Fast

Chart 4European Inflation Is Energy inflation

European Inflation Is Energy inflation

European Inflation Is Energy inflation

Chart 5The US Is Lifting Prices Around The World

The US Is Lifting Prices Around The World

The US Is Lifting Prices Around The World

Even the analysis of the ECB is conflicted. On May 11, Executive Board Member Isabel Schnabel highlighted the need for an imminent interest rate hike, yet she also underscored the global nature of the current inflation outbreak. Goods prices in Europe not only reflect higher input costs, but they also bear the imprint of the excess demand in the US, which is lifting the price of goods prices around the world (Chart 5). However, an ECB rate hike will do little to tame US demand for manufactured goods. In the monetary policy realm, only aggressive tightening by the Fed will have the desired effect, which will trickle down to lower European inflation. Thus, European interest rate hikes will accentuate consumption weaknesses already visible across the region more than they will slow inflation. While a few rate hikes will not have a major impact, the seven rate hikes priced in the June 2023 Euribor contract would be disastrous as long as Europe is hamstrung by the current relative price shock. We remain long this contract. Worsening US Equity Selloff Investors seem to be waking up to the reality that US consumers are facing the same difficult predicament as European consumers: rising energy and food prices and contracting real incomes. The recent earnings call by Walmart was a shock that caused an 8% drubbing for consumer staples and a 7% fall in consumer discretionary equities. Until US inflation clearly peaks, investors will have to evaluate how much deeper the pain for consumers may run. Moreover, since consumers have begun to cut their discretionary spending in response to strained budgets, the ability of firms to pass on rising input costs is dwindling. Hence, investors will have to handicap the risks to margins as well. Chart 6Fed Put Not Exercised

Fed Put Not Exercised

Fed Put Not Exercised

US inflation also impacts the Fed’s outlook. Until inflation has decelerated for a few months, the Fed will remain comfortable with tighter financial conditions. This means that the strike price of the so-called Fed put is inversely proportional to inflation, especially since FCIs are far from tight (Chart 6). As a result, inflation or energy prices must soften before the Fed can begin to send comforting signals to the market. Chart 7Where Walmart Goes, So Does The Market?

Where Walmart Goes, So Does The Market?

Where Walmart Goes, So Does The Market?

The US market has cheapened significantly, and a floor should be close; but the risks remain considerable. A very smart investor with whom we regularly chat highlighted that we have not yet seen a full-fledged liquidation. Only once energy stocks have also been purged will the necessary condition for a bottom be met (since only then will all the speculative activity have been cleared). In fact, the recent poor performance of Walmart highlights the risk that the S&P 500 could suffer one last down leg to 3500, since over the past 12 years, WMT often leads the SPX (Chart 7). Another 300 points decline in the US benchmark could translate into significant selling pressure in the Euro STOXX, because it sports an elevated beta. EM Instability EM are still facing ample risks, which could easily dislodge the prospects of European firms servicing these economies. As a result, EM constitute another major threat for European equities. Chart 8Less COVID In Shanghai and Jilin

Less COVID In Shanghai and Jilin

Less COVID In Shanghai and Jilin

The outlook for China remains fraught with risks. National COVID cases are declining as a result of the collapse in cases in the Shanghai and Jilin provinces (Chart 8). However, Omicron is spreading around the nation, with broadening lockdowns in Beijing and Tianjin. The one certainty is that the Chinese Communist Party remains wedded to its zero-COVID policy. Considering the size of the country and how contagious the various Omicron variants are, rolling lockdowns and their deleterious impact on activity are here to stay. China therefore remains a source of downside risk for global goods demand. Unemployment is surging, and the PMIs are extremely weak, suggesting a contraction in GDP is coming. Moreover, households continue to deleverage (Chart 9). The CNY’s weakness confirms the risks to earnings growth in Europe, and the yield spread between China and the US points to further downside in the RMB (Chart 10, top panel). Interestingly, the weakness of the yen could also drag the CNY lower because of competitive pressures. Chester Ntonifor, BCA’s Chief Foreign Exchange strategist recommends investors sell CNY/JPY. Historically, a depreciating CNY/JPY portends weakness in European stock prices (Chart 10, bottom panel). Chart 9Chinese Growth Problems

Chinese Growth Problems

Chinese Growth Problems

Chart 10A Weaker CNY Augurs Poorly For European Stocks

A Weaker CNY Augurs Poorly For European Stocks

A Weaker CNY Augurs Poorly For European Stocks

The broader EM space outside of China is also a source of risk. EM countries are tightening monetary policy, which is slowing economic activity in nations already exposed to declining Chinese imports. Additionally, as Arthur Budaghyan shows, the strength in the dollar is tightening EM financial conditions and invites further increases in EM policy rates because of the inflationary impact of depreciating currencies. An additional tightening in EM financial conditions in response to this toxic mix will invite greater downside for European equities (Chart 11). Bottom Line: European equities already reflect enough of a valuation cushion to compensate for a significant slowdown in European growth. However, ample risks to global growth still lurk in the background. If these risks materialize, European stocks could selloff another 15% or so. Moreover, the overvaluation of cyclical stocks relative to defensive ones has now been purged, but China’s economic weakness remains a major handicap (Chart 12). Consequently, don’t be hero: avoid bottom-fishing European assets, especially cyclical ones. Chart 11Brewing EM Troubles

Brewing EM Troubles

Brewing EM Troubles

Chart 12Cyclicals At Risk From China

Cyclicals At Risk From China

Cyclicals At Risk From China

Is it Time to Buy the Euro? After falling below 1.04, EUR/USD has rebounded to 1.055. Is it time to buy the euro? The euro now embeds a large discount that reflects fears of a recession and stagflation in the Eurozone. A purchasing power parity model developed by BCA’s Foreign Exchange Strategy team that accounts for the differences in consumption baskets in Europe and the US shows that EUR/USD is trading at its deepest discount to fair value since 2001. Moreover, BCA’s Intermediate-term timing model, which is based on an augmented interest rate parity framework, confirms that EUR/USD is cheap. Additionally, BCA’s Intermediate-Term Technical Indicator is massively oversold (Chart 13). For the euro to bottom durably, the dollar needs to reverse its rally. The combination of net speculative positions on the DXY and BCA’s Dollar Capitulation Index point to elevated chances of an imminent peak (Chart 14). Chart 13The Euro's Large Risk Premium

The Euro's Large Risk Premium

The Euro's Large Risk Premium

Chart 14The Over Extended Dollar

The Over Extended Dollar

The Over Extended Dollar

Despite this backdrop, three of the aforementioned risks to European stocks translate into threats to the euro: A Russian energy embargo would cause a much more severe European recession. Two weeks ago, we highlighted a Bundesbank study which showed that such a cutoff would curtail German growth by 5% point for 2022. We also highlighted that this shock would cause a temporary but significant increase in inflation. This combination would be poisonous for the euro, and it carries a roughly 30% probability. A policy mistake in the Euro Area would cause a period of significant spread widening in the periphery. Such shocks often prompt a widening in the breakup risk-premium for the euro. This risk premium pushes EUR/USD lower. Chart 15Chinese Assets Matter To The Euro

Chinese Assets Matter To The Euro

Chinese Assets Matter To The Euro

Chinese growth problems often hurt the euro as well as European stocks. A fall in the Chinese stock-to-bond ratio often leads to a weaker EUR/USD, since both variables are correlated to Chinese economic activity. Additionally, a depreciating CNY is also synonymous with a softer euro because a declining renminbi hurts European exporters (Chart 15). Further weaknesses in the S&P 500 no longer guarantee a fall in EUR/USD. Investors are worried about the US equity outlook because they are extrapolating the impact on consumers of rising energy and food prices. They are applying the template of what is going on in Europe to US households, which means that they are pricing in a convergence of US growth toward European growth (barring the three additional shocks highlighted in the bullet points above). Related Report European Investment StrategyIs UK Stagflation Priced In? Bottom Line: From a technical and valuation perspective, the rebound in the euro that began this week could last longer. However, several exceptional risks could prevent this bounce from morphing into a durable rally. The significant odds of a Russian energy embargo stand at the top of the list of concerns, but so does the possibility of a policy mistake in Europe as well China’s problems. Thus, even if the euro is bottoming, don’t be a hero and wait on a safer entry point to focus on capital preservation. In fact, BCA’s Foreign Strategy team is now selling EUR/JPY. Within a European context, a short GBP/CHF position is attractive as a portfolio hedge. The Swiss National Bank seems more tolerant of a higher CHF as a vehicle to tame growing inflationary pressures, while the UK faces significant risks. Mathieu Savary, Chief European Strategist Mathieu@bcaresearch.com Tactical Recommendations Cyclical Recommendations Structural Recommendations

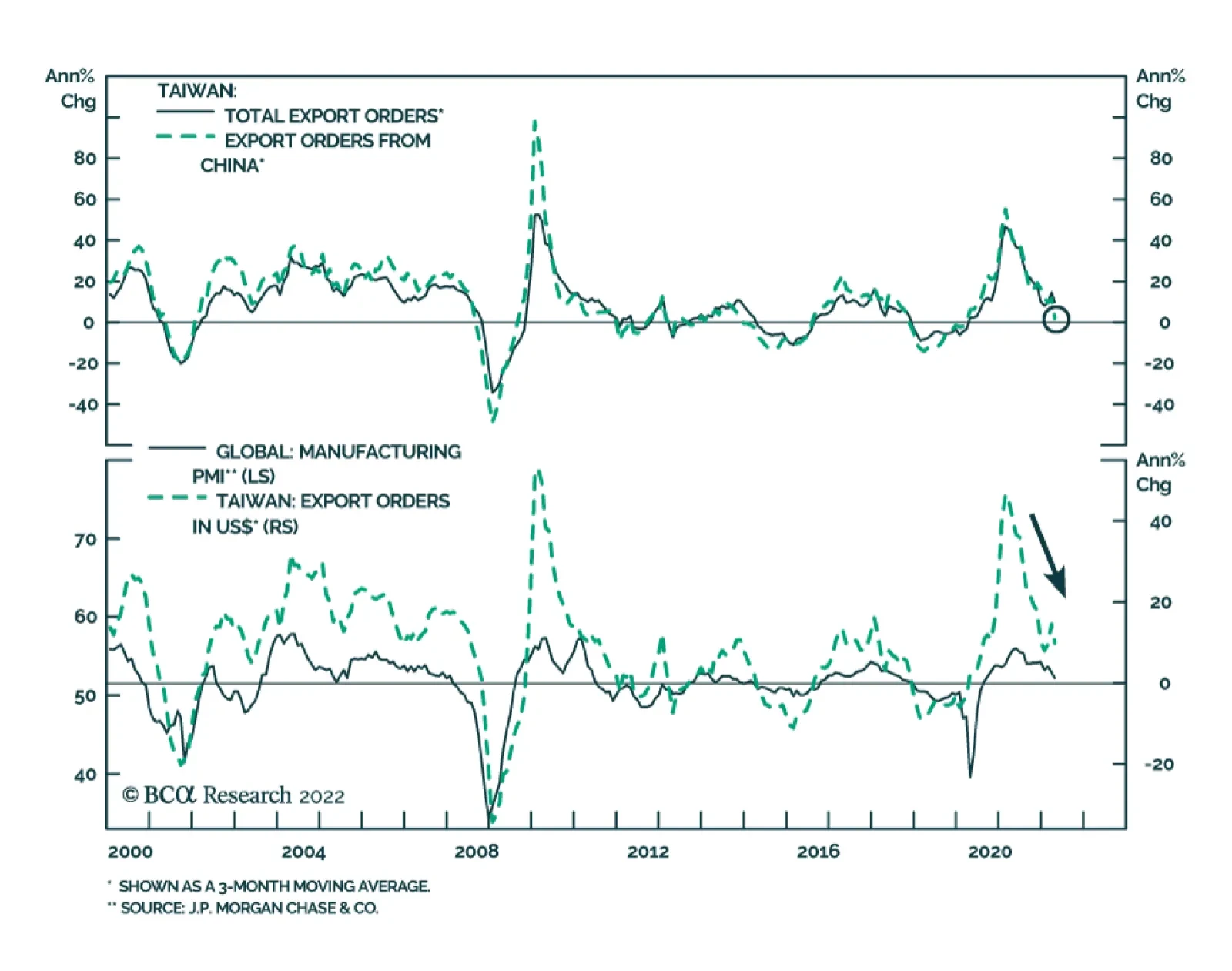

Taiwanese export orders for April sent a negative signal about the global manufacturing cycle. Overall export orders contracted by 5.5% y/y, a massive disappointment to expectations of a slowdown in the annual rate of increase from 16.8% in March to 11.5%.…

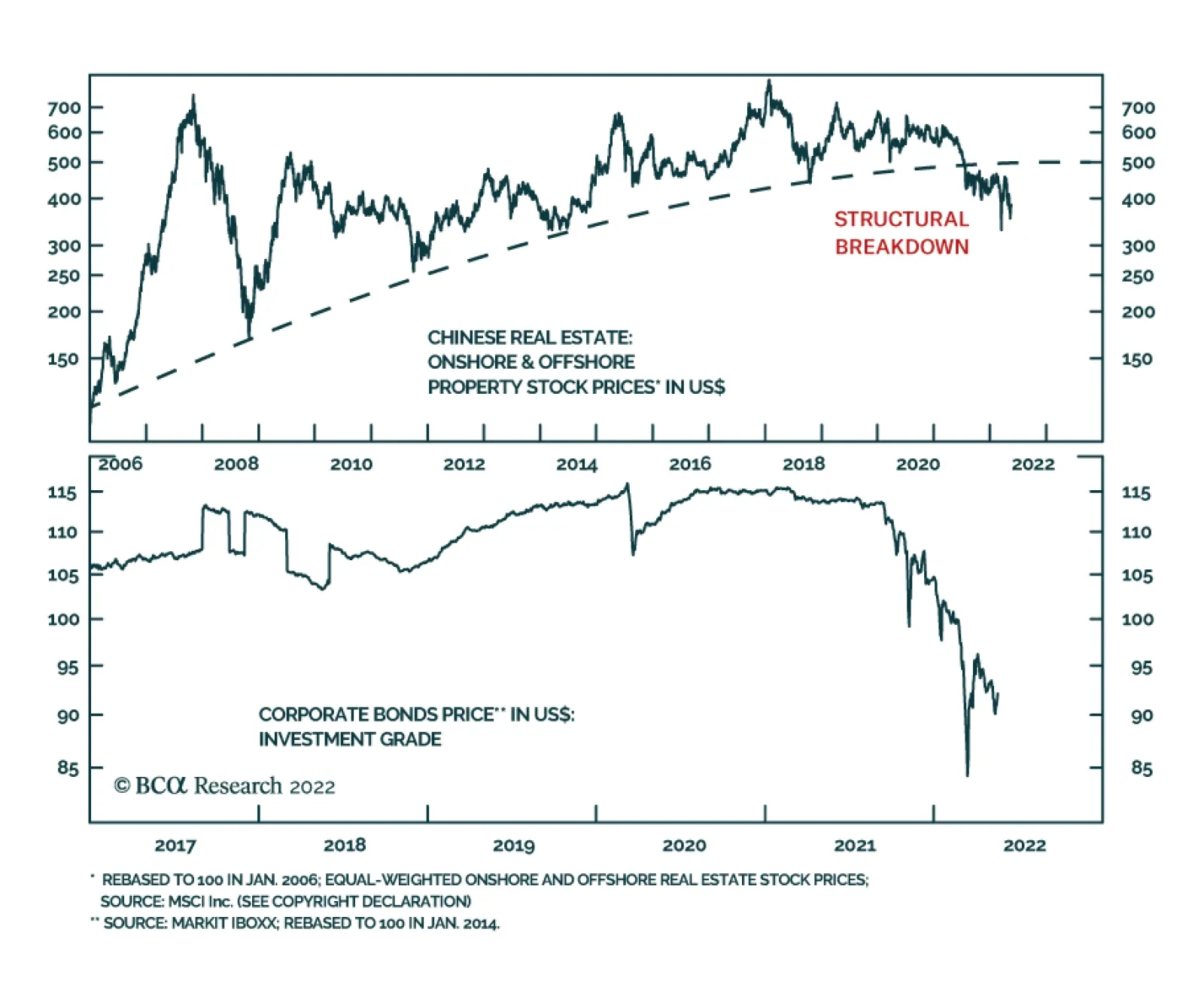

The PBoC reduced the five-year loan prime rate – the mortgage reference rate – by 15bps on Friday to 4.45%, below expectations of 4.55%. This marks the latest attempt by Chinese policymakers to revive the housing market. Earlier in the week, financial…

Executive Summary Indian Voter’s Economic Miseries Are Ascendant

Indian Voter's Economic Miseries Are Ascendant

Indian Voter's Economic Miseries Are Ascendant

India has a strong strategic geopolitical position but is likely to face turbulence in the short term. This is because India remains expensive, and investors worry if the record political stability shown by India since 2014 can last. We highlight that the ruling Bhartiya Janata Party (BJP) may lose some seats in the near term. India’s most populous states could witness a few cases of social conflict as economic miseries grow. India may also temporarily resort to a degree of fiscal populism. But the BJP will be able to hold power for a third consecutive term in 2024, that too with a simple majority. The burst of fiscal populism will be temporary. Moreover, the next tier of India’s most populous states are well-positioned to drive India’s growth story in the long run. We urge investors to tactically short India / long Brazil financials given that India may see some turbulence in the short run. Strategic investors should consider long India tech / short China tech. Trade Recommendation Inception Date Return SHORT INDIA / LONG BRAZIL FINANCIALS 2022-02-10 12.5% Bottom Line: The ruling political party in India may face some political setbacks in the short term. It could even resort to fiscal populism. But the ruling party in a base case, should be able to retain power for a third term in 2024. On a tactical timeframe we advise caution on India but remain constructive on a strategic horizon. Feature The woods are lovely, dark and deep, But I have promises to keep, And miles to go before I sleep, And miles to go before I sleep. – Robert Frost, Stopping By Woods On A Snowy Evening (New Hampshire, 1923) The protagonist in this famous poem is overwhelmed by the beauty of the wintry woods, but then must stay vigilant about the here and now. The situation that confronts an investor into India today, is surprisingly similar. India has a strong strategic geopolitical position, a position that has strengthened following the Ukraine war. However, Indian markets might face turbulence in the short term. This is because India remains expensive and its ability to keep promises (about high degrees of political stability or about its fiscal discipline) could be tested on a tactical time horizon. In specific, investors with exposure to India worry about three politico-economic challenges: The Anti-Incumbency Challenge Related Report Geopolitical StrategyIndia's Politics: Know When To Hold 'Em, Know When To Fold 'Em 13 September 2013 is a key date in India’s modern history. On this day the Bhartiya Janata Party (BJP) announced Narendra Modi as BJP’s prime ministerial (PM) candidate just a few months ahead of the 2014 general elections. From 13 September 2013 till date, MSCI India has incidentally outperformed MSCI EM by a resounding 94.8%. In 2013, markets celebrated the rise of the Modi-led BJP government since such a dispensation was new, and it promised to deliver structural reform. But now when general elections will be held in 2024, the BJP must deal with a middling report card on reforms and a two-term anti-incumbency to boot. Given this clients worry if 2024 could see India go back to an era of coalition governments? The Fiscal Challenge India under BJP has displayed impressive degrees of fiscal discipline. With rising inflation now adding to Indian voters’ miseries and with a loaded state election calendar due in 2023, investors ask if India’s notable streak of fiscal fortitude can last? The Demographics Challenge As China’s weak demographic future becomes clearer, India’s youthful demographics keep attracting paeans. This is partially responsible for the fact that India has traded at a five-year average premium of 54.5% to China on forward price to earnings. With increasing reports of communal violence and inflation-related protests breaking out in India, investors also worry about India’s so-called demographic dividend and how best to play the game? In a foundational GPS Special Report published in 2018 we had made the point that, “Predicting political outcomes is difficult, but to generate geopolitical alpha investors should focus on ‘beating the spread’ not predicting the match winner”. At a time when there is much uncertainty about India’s immediate future, we highlight three key base case predictions with respect to India. By highlighting these key predictions, we hope investors can position themselves for generating geopolitical alpha. We conclude the report with actionable investment recommendations. India’s High Political Stability, Likely To Stay In 2024 Chart 1Bhartiya Janata Party’s (BJP) Win In India In 2014 Was Historic

Indian Politics: The Woods Are Lovely...

Indian Politics: The Woods Are Lovely...

The Bhartiya Janata Party (BJP) stormed into power in 2014. Its assumption of power under PM Modi’s leadership was historic. This is because this was the first time since 1984 that a single political party had managed to secure a simple majority on its own steam (Chart 1). The rise of BJP in this resurrected avatar marked a structural break from the past, in three distinct ways: End To Instability Of Nineties: The rise of BJP 2.0 in 2014 marked an end to the political instability seen in the nineties when governments struggled to complete their full five-year terms. This is a problem that India’s South Asian neighbors like Sri Lanka and Pakistan are yet to overcome. End Of Coalition Politics Of Early 2000s: BJP’s rise in 2014 also marked an end to the coalition politics of the early 2000s. While three coalition governments in India managed to complete their five-year terms from 1999-2014, the reform agenda over this period was often held at ransom by smaller coalition partners. India’s ability to break away from coalition governments back in 2014 was commendable given that several developing countries as well as developed countries still have coalition governments at the helm. Regime Continuity: The BJP’s rise in 2014 and their re-election in 2019 meant that the same political party was able to hold power in India (that too with a simple majority) for a decade. Other EMs have not seen this quality of continuity over the last few years. Owing to this streak of unprecedented political stability that India has been able to offer since 2014, India has attracted a high premium relative to democratic EM peers (Chart 2). But with India’s general elections due in 2024, investors into India are keen to know if India will continue to attract this high political stability premium. This worry is justified for two sets of reasons: (1) The last time any government in India was able to pull off three consecutive full five-year terms, was way back in the sixties. There is no recent precedent to BJP’s pursuit for a third consecutive term in India. (2) The most recent election held in India’s largest state i.e., Uttar Pradesh saw the BJP retain power but saw its seat count fall by 18%. This, investors worry could be an indicator of BJP losing traction in the politically critical region of northern India. Reading the tea leaves left behind after all recent elections suggests that India is most likely to see a single political party maintain a simple majority for a third consecutive term in 2024. BJP’s footprint northern in India will be dented owing to anti-incumbency. But despite this, the BJP should be able to maintain a simple majority at the national level in 2024. This is because the BJP appears to be working on deploying a crucial strategy i.e., to offset declines in north India with gains elsewhere. India’s northern states account for 45% of India’s population. Whilst the BJP’s rise in 2014 was pivoted on this geography, its ability to retain power beyond a decade will be dependent on its ability to offset losses in India’s sprawling north with gains in other large states. Interestingly, the BJP’s predecessor i.e., the Congress party had to deal with the reciprocal of this problem. The Congress party stayed in power for a decade (from 2004-14) owing to support from southern and western Indian states. But then the Congress party’s reign could not last beyond a decade because it failed to break into northern India (Chart 3); at a time when it was losing popularity in India’s west and south. Chart 2India Has Been Trading At A Premium To EM Democracies

India Has Been Trading At A Premium To EM Democracies

India Has Been Trading At A Premium To EM Democracies

Chart 3Congress Party-Led UPA Alliance Could Not Break Into North India

Indian Politics: The Woods Are Lovely...

Indian Politics: The Woods Are Lovely...

The fact that the BJP is now working to straddle both i.e. (1) its traditional base in the north and west as well as (2) new geographies in the east and south is evident from the recent election results: 2019 General Elections: Even as BJP’s seat count in the north Indian states of Uttar Pradesh and Bihar fell in 2019 (Chart 3) it managed to offset this decline by increasing presence in India’s east (in states like West Bengal and Orissa) and in India’s south (in states like Karnataka and Telangana). Consequently, the share of BJP’s seats accounted for by major states outside north India notably increased in 2019 from 2014 (Chart 4). Recent State Elections: The BJP has evidently been able to offset losses in its core northern base (in states like Uttar Pradesh), by increasing its presence in India’s east (in states like West Bengal and Bihar) (Chart 5). Chart 4BJP Is Growing Its Influence Outside North India

Indian Politics: The Woods Are Lovely...

Indian Politics: The Woods Are Lovely...

Chart 5BJP Is Offsetting Losses In North With Gains In East

Indian Politics: The Woods Are Lovely...

Indian Politics: The Woods Are Lovely...

Chart 6In a Base Case, BJP Should Cross The Halfway Mark At 2024 General Elections

Indian Politics: The Woods Are Lovely...

Indian Politics: The Woods Are Lovely...

In fact, it is critical to note that state elections are due in Gujarat in December 2022, where the BJP is highly likely to lose seat share as it faces a five-term anti-incumbency. Given that Gujarat as a region too is part of BJP’s core voter base, BJP’s seat losses in Gujarat could trigger a wave of selling on India’s bourses. If this leads India’s expensive valuations to be driven down, then this could present a buying opportunity because as long as the BJP keeps compensating for losses in traditional constituencies with inroads into newer realms (like say Karnataka where state elections are due in May 2023 or in Rajasthan and Madhya Pradesh where elections are due in end-2023); BJP’s standalone seat count in 2024 is highly likely to cross the half-way mark (Chart 6). To conclude, we re-iterate our constructive outlook on India on a strategic horizon, in view of the high probability of regime continuity lasting in this EM beyond a decade. In a worst-case scenario, we expect a BJP-led coalition to assume power in India in 2024 but this coalition too will be stable and should need the support of a maximum of two regional parties. Bottom Line: The BJP will lose seat share in parts of north and west India but should be able to retain power in 2024 by offsetting these losses with gains in India’s east and south. Most recent election results confirm that the BJP is working meticulously to make this formula work. If BJP’s political losses in its traditional constituencies triggers a market correction, then this should be used as a buying opportunity by strategic investors. Fiscal Risks In India Are Not Dead; They Will Surface, Before Receding Again In 1952 when India’s first national assembly was formed, left-leaning parties were the mainstay of India’s national politics. Back then a left-of-center party i.e., the Congress Party was in power with +70% seats in the national assembly. Then, the leftist Communist Party of India (CPI) was the second largest political party. As the decades went by left-leaning policies kept losing importance in India but the left-of-center national parties influenced Indian politics in a big way right up until 2014. Cut to 2014, the rise of the Bhartiya Janata Party (BJP) meant that the mainstay of Indian politics now became right-of-center politics. Left-leaning parties became too insignificant to matter at the national level with the Congress Party and the Communist Party of India (M) now cumulatively accounting for only about 11% seats in the national assembly. India’s political pendulum swinging to the right was accompanied by another key development i.e., India’s fiscal management became more prudent (Chart 7). Doles and transfer payments were restrained, and efforts were also made to shore-up tax revenues. But does the BJP-led transition to right-of-center politics mean that left-of-center politics in India are dead, as are the associated risks of fiscal populism? The Indian bond market seems to think so. India’s 10-year bond yield is up only 85 bps since 1 Jan 2020 to date, which is lower than a 106 bps increase seen in the US or 573 bps increase seen in a large emerging market like Brazil. Notwithstanding the superior fiscal discipline maintained by BJP-led governments so far, it is worth asking if this streak of fiscal resilience can last over the next two years? We highlight that even as the right-of-center BJP will remain a force to reckon with, we expect the BJP’s fiscal policy to temporarily swerve to the left owing to three sets of reasons: Miseries Breed Populism: It is true that recent BJP-led governments have maintained superior fiscal discipline (Chart 7). However high levels of inflation are known to feed populist tendencies of governments globally. India will be no exception to this trend because economic miseries of India’s median voter have worsened over the last six months (Chart 8). Chart 7BJP Led Governments Have Maintained Tighter Fiscal Deficits In India

Indian Politics: The Woods Are Lovely...

Indian Politics: The Woods Are Lovely...

Chart 8Economic Miseries Of India's Median Voter Have Been Worsening

Economic Miseries Of India's Median Voter Have Been Worsening

Economic Miseries Of India's Median Voter Have Been Worsening

Chart 9Government Spends Tend To Pick Up In The Run-Up To General Elections

Indian Politics: The Woods Are Lovely...

Indian Politics: The Woods Are Lovely...

Political Cycle: History also suggests that there is a cyclical element to fiscal laxity in India. Populism as a theme tends to become more defined in the two years leading to a general election (Chart 9). This cyclicality in fiscal expansion could also be driven by the fact that India tends to have a loaded state election calendar in the year just before a general election. Competition: As the BJP’s reign matures, it will increasingly face competition from regional parties (Chart 10). Given that most major regional political parties in India operate on the segment between the center and the left of political spectrum (Chart 10), BJP may see sense in metamorphosizing its fiscal policy into one which is closer to the left, albeit temporarily. Chart 10Regional Parties Like SP And AAP Could Grow Their National Footprint

Indian Politics: The Woods Are Lovely...

Indian Politics: The Woods Are Lovely...

Chart 11India’s Debt Levels Are High And Rising

Indian Politics: The Woods Are Lovely...

Indian Politics: The Woods Are Lovely...

It is worth noting that as compared to major EMs, India’s debt levels are high today (Chart 11). Against this backdrop an expansion of India’s fiscal deficit could result in turbulence in Indian markets. Bottom Line: The BJP is highly likely to temporarily switch to an expansive fiscal policy stance in the run up to the 2024 general elections. This shift will be driven by the need to retain power in the face of rising miseries of its median voter and to overcome competition from influential regional players. Most Populous Regions, May Not Necessarily Be Drivers Of India’s Growth The ‘demographic dividend’ narrative is often used to justify a bullish stance on India. But such a narrative oversimplifies India’s investment case and may even yield poor investment outcomes. India’s demographics power its consumption engine, but the same demographics can also be a liability sometimes. This is because while India is young, its populace is also poor and large. The combination of a massive population (that creates pressure on limited resources) and nascent institutions (that are yet to ensure a fair use of resources) is at the heart of corruption in India. For instance, the coming to light of the 2G-spectrum scam a decade ago on 16 November 2010 saw Indian markets correct by 6% over the next ten days. Hence ‘corruption’ is one of the ways in which India’s demographics can end-up being a drag on India’s investment returns. Chart 12Six Indian States Account For India’s Political Nucleus

Indian Politics: The Woods Are Lovely...

Indian Politics: The Woods Are Lovely...

With China’s population likely to have peaked last year, India’s population which is likely to peak in the 2040s - keeps attracting investor interest. In this report we peel the onion around India’s demographics in a way that allows investors to make the most of its demographics, whilst avoiding pitfalls associated with the same. We highlight that paradoxically; India’s most populous states may not be the main drivers of India’s growth over the next decade. On the other hand, investing in the ‘next eight’ most populous states, could present a superior opportunity to profit from India’s demographics. Six Indian states account for more than half of India’s population (Chart 12) and each of these states are larger than Germany or Turkey in terms of population (Map 1). Despite being populous, these states could emerge as flashpoints of social conflict over the next decade. This is because it is possible that these states’ economic growth fails to be brisk enough to meet aspirations of its vast populace. Early signs of this phenomenon are evident from the fact that these states’ share in India’s population has been rising, but their share in national income has fallen (Chart 13). Today these six states account for more than half of India’s population but generate less than half of its national GDP (Chart 14). Map 1India’s Most Populous States, May Not Necessarily Lead On Growth

Indian Politics: The Woods Are Lovely...

Indian Politics: The Woods Are Lovely...

Chart 13Most Populous States Of India, Are Not Necessarily Leading On Growth

Indian Politics: The Woods Are Lovely...

Indian Politics: The Woods Are Lovely...

Chart 14Next Eight Largest States Of India Are Economically Dynamic

Indian Politics: The Woods Are Lovely...

Indian Politics: The Woods Are Lovely...

Despite accounting for the lion’s share of India’s population, these six states’ growth potential could be compromised by: Economic Weakness: Primary sectors account for an unusually large share of the local economies of the most populous states today (Chart 15). Social Complexity: Most of the populous states are also characterized by greater social complexity as compared to other Indian states (Chart 16). In other words, their populations are young but are also poor and more heterogenous, which in turn exposes these states to a higher risk of social conflict. Chart 15Primary Activities Account For A Large Chunk Of Populous States’ GDP

Indian Politics: The Woods Are Lovely...

Indian Politics: The Woods Are Lovely...

Chart 16The Risk Of Social Conflict Is Higher, In The More Populous States

Indian Politics: The Woods Are Lovely...

Indian Politics: The Woods Are Lovely...

Leverage: The debt to GDP ratio of the more populous states often tends to be higher too (Chart 17). Now contrary to the situation in India’s most populous states, India’s ‘next eight’ largest states (by population) could emerge as hubs of economic dynamism (Map 1). This is because: Faster Growth: These states' share in national GDP is growing faster than the pace at which their share in India’s population is growing (Chart 13). As of today, the next eight states account for less than a third of India’s population but more than a third of India’s national income (Chart 14). Fewer Constraints: The next eight most populous states have more modern economic structures (Chart 15), lower risk of social conflict (Chart 16) and mildly superior public finances (Chart 17). Last but not the least, the ‘next eight’ states are poised favorably from a political perspective as well. This is because the Bhartiya Janta Party (i.e., BJP) has a weak footprint in these states (Chart 18) and will be keen to offer supportive economic policies to win over their median voter. Chart 17More Populous States, Also Can Be More Leveraged

Indian Politics: The Woods Are Lovely...

Indian Politics: The Woods Are Lovely...

Chart 18Next Eight Most Populous States Likely To Attract More Political Attention Going Forward

Indian Politics: The Woods Are Lovely...

Indian Politics: The Woods Are Lovely...

Bottom Line: While the demographic dividend that India enjoys is real, its benefits will not be spread uniformly across India’s geographies. For instance, some of the most populous states of India could lag on the growth front. To profit from India’s demographics and yet mitigate risks associated with the same, we urge investors to build portfolios that maximize exposure to the second tier of populous states in India. Investment Conclusion The Bhartiya Janta Party (BJP) in India appears set to emerge as the first party in India’s modern history to retain power beyond a decade with a simple majority. But to pull off this rare feat, it will have to metamorphosize and may exhibit some changes such as: Develop a focus on regions that are outside its core constituency, in a bid to offset anti-incumbency in its core constituencies. Sharpen its policy focus on the next tier of populous states, given that some of these states have greater growth potential and given that the BJP’s footprint in the second tier of populous states has room to grow. Adopt an expansive fiscal policy in the run up to the 2024 elections, to combat the rising economic miseries of India’s median voter. To play these dynamics, we urge clients to consider the following trades: Strategic Trades For clients with a holding period mandate of more than 12 months, we urge such investors to go strategically long Indian tech / short Chinese tech (Chart 19). The trade allows investors to play the unique and high degrees of political stability that India will offer on a strategic horizon. Chart 19Strategic Trade: Long Indian Tech / Short Chinese Tech

Strategic Trade: Long Indian Tech / Short Chinese Tech

Strategic Trade: Long Indian Tech / Short Chinese Tech

Chart 20Tactical Trade: Short India / Long Brazilian Financials

Tactical Trade: Short India / Long Brazilian Financials

Tactical Trade: Short India / Long Brazilian Financials

Moreover, it is notable the Indian tech industry’s key bases are concentrated in Karnataka, Andhra Pradesh and Telangana. All three states fall within the next tier of populous states of India. Thus, this trade allows investors to maximize exposure to both an economically vibrant region and sector of India. Tactical Trades For investors with a holding period mandate of less than 12 months, a trade that can be activated to profit from India’s short-term geopolitical risks is to short India / long Brazilian Financials (Chart 20). This allows investors to profit from the cyclical risks that will affect India (1) as commodity prices stay high and (2) as rising economic miseries fan fiscal risks. Ritika Mankar, CFA Editor/Strategist ritika.mankar@bcaresearch.com Strategic Themes Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months) Regional Geopolitical Risk Matrix

Listen to a short summary of this report. Executive Summary The US Inflation Surprise Index Has Rolled Over

Goldilocks: A Skeptical Q&A

Goldilocks: A Skeptical Q&A

Global equities are nearing a bottom and will rally over the coming months as inflation declines and growth reaccelerates. While equity valuations are not at bombed-out levels, they have cheapened significantly. Global stocks trade at 15.3-times forward earnings. We are upgrading tech stocks from underweight to neutral. The NASDAQ Composite now trades at a forward P/E of 22.6, down from 32.9 at its peak last year. The 10-year Treasury yield should decline to 2.5% by the end of the year, which will help tech stocks at the margin. The US dollar has peaked. A weakening dollar will provide a tailwind to stocks, especially overseas bourses. US high-yield spreads are pricing in a default rate of 6.2% over the next 12 months, well above the trailing default rate of 1.2%. Favor high-yield credit over government bonds within a fixed-income portfolio. Bottom Line: The recent sell-off in stocks provides a good opportunity to increase equity allocations. We expect global stocks to rise 15%-to-20% over the next 12 months. Back to Bullish We wrote a report on April 22nd arguing that global equities were heading towards a “last hurrah” in the second half of the year as a Goldilocks environment of falling inflation and supply-side led growth emerges. Last week, we operationalized this view by tactically upgrading stocks to overweight after having downgraded them in late February. This highly out-of-consensus view change, coming at a time when surveys by the American Association of Individual Investors and other outfits show extreme levels of bearishness, has garnered a lot of attention. In this week’s report, we answer some of the most common questions from the perspective of a skeptical reader. Q: Inflation is at multi-decade highs, global growth is faltering, and central banks are about to hike rates faster than we have seen in years. Isn’t it too early to turn bullish? A: We need to focus on how the world will look like in six months, not how it looks like now. Inflation has likely peaked and many of the forces that have slowed growth, such as China’s Covid lockdown and the war in Ukraine, could abate. Q: What is the evidence that inflation has peaked? And may I remind you, even if inflation does decline later this year, this is something that most investors and central banks are already banking on. Inflation would need to fall by more than expected for your bullish scenario to play out. A: That’s true, but there is good reason to think that this is precisely what will happen. Overall spending in the US is close to its pre-pandemic trend. However, spending on goods remains above trend while spending on services is below trend (Chart 1). Services prices tend to be stickier than goods prices. Thus, the shift in spending patterns caused goods inflation to rise markedly with little offsetting decline in services inflation. To cite one of many examples, fitness equipment prices rose dramatically, but gym membership fees barely fell (Chart 2). Chart 1Total US Consumer Spending Is Almost Exactly At Its Pre-Pandemic Trend, But The Composition Of Spending Remains Skewed

Total US Consumer Spending Is Almost Exactly At Its Pre-Pandemic Trend, But The Composition Of Spending Remains Skewed

Total US Consumer Spending Is Almost Exactly At Its Pre-Pandemic Trend, But The Composition Of Spending Remains Skewed

Chart 2Asymmetries Matter: Firms Manufacturing Sports Equipment Jacked Up Prices, But Gyms Barely Cut Prices

Asymmetries Matter: Firms Manufacturing Sports Equipment Jacked Up Prices, But Gyms Barely Cut Prices

Asymmetries Matter: Firms Manufacturing Sports Equipment Jacked Up Prices, But Gyms Barely Cut Prices

As goods demand normalizes, goods inflation will come down. Meanwhile, the supply of goods should increase as the pandemic winds down, and hopefully, a detente is reached in Ukraine. There are already indications that some supply-chain bottlenecks have eased (Chart 3). Q: Even if supply shocks abate, which seems like a BIG IF to me, wouldn’t the shift in spending towards services supercharge what has been only a modest acceleration in services inflation so far? A: Wages are the most important driver of services inflation. Although the evidence is still tentative, it does appear as though wage inflation is peaking. The 3-month annualized growth rate in average hourly earnings for production and nonsupervisory workers slowed from 7.2% in the second half of 2021 to 3.8% in April (Chart 4). Assuming productivity growth of 1.5%, this is consistent with unit labor cost inflation of only slightly more than 2%, which is broadly consistent with the Fed’s CPI inflation target.1

Image

Chart 4Wage Pressures May Be Starting To Ease

Wage Pressures May Be Starting To Ease

Wage Pressures May Be Starting To Ease

Image

Moreover, a smaller proportion of firms expect to raise wages over the next six months than was the case late last year according to a variety of regional Fed surveys (Chart 5). The same message is echoed by the NFIB small business survey (Chart 6). Consistent with all this, the US Citi Inflation Surprise Index has rolled over (Chart 7). Chart 6... Small Business Owners Included

... Small Business Owners Included

... Small Business Owners Included

Chart 7The US Inflation Surprise Index Has Rolled Over

The US Inflation Surprise Index Has Rolled Over

The US Inflation Surprise Index Has Rolled Over

Q: What about the “too cold” risk to your Goldilocks scenario? The risks of recession seem to be rising. A: The market is certainly worried about this outcome, and that has been the main reason stocks have fallen of late. However, we do not think this fear is justified, certainly not in the US (Chart 8). US households are sitting on $2.3 trillion excess savings, equal to about 14% of annual consumption. The ratio of household debt-to-disposable income is down 36 percentage points from its highs in early 2008, giving households the wherewithal to spend more. Core capital goods orders, a good leading indicator for capex, have surged. The homeowner vacancy rate is at a record low, suggesting that homebuilding will be fairly resilient in the face of higher mortgage rates. Q: It seems like the Fed has a nearly impossible task on its hands: Increase labor market slack by enough to cool the economy but not so much as to trigger a recession. You yourself have pointed out that the Fed has never achieved this in its history. A: It is correct that the unemployment rate has never risen by more than one-third of a percentage point in the US without a recession occurring (Chart 9). That said, there are three reasons to think that a soft landing can be achieved this time.

Image

Chart 9When Unemployment Starts Rising, It Usually Keeps Rising

When Unemployment Starts Rising, It Usually Keeps Rising

When Unemployment Starts Rising, It Usually Keeps Rising

First, increasing labor market slack is easier if one can raise labor supply rather than reducing labor demand. Right now, the participation rate is nearly a percentage point below where it was in 2019, even if one adjusts for increased early retirement during the pandemic (Chart 10). Wages have risen relatively more at the bottom end of the income distribution. This should draw more low-wage workers into the labor force. Furthermore, according to the Federal Reserve, accumulated bank savings for the lowest-paid 20% of workers have been shrinking since last summer, which should incentivize job seeking (Chart 11). Chart 10Labor Participation Has Further Scope To Recover

Labor Participation Has Further Scope To Recover

Labor Participation Has Further Scope To Recover

Chart 11Depleted Savings Will Force More Lower-Wage Workers Into The Labor Market

Depleted Savings Will Force More Lower-Wage Workers Into The Labor Market

Depleted Savings Will Force More Lower-Wage Workers Into The Labor Market

Second, long-term inflation expectations remain well contained, which makes a soft landing more likely. Median expected inflation 5-to-10 years out in the University of Michigan survey stood at 3% in May, roughly where it was between 2005 and 2013 (Chart 12). Median expected earnings growth in the New York Fed Survey of Consumer Expectations was only slightly higher in April than it was prior to the pandemic (Chart 13). Chart 12Consumer Long-Term Inflation Expectations Have Risen But Remain Relatively Low

Consumer Long-Term Inflation Expectations Have Risen But Remain Relatively Low

Consumer Long-Term Inflation Expectations Have Risen But Remain Relatively Low

Chart 13US Consumers Do Not Expect Wages To Grow At A Much Higher Rate Than In The Pre-Pandemic Period

US Consumers Do Not Expect Wages To Grow At A Much Higher Rate Than In The Pre-Pandemic Period

US Consumers Do Not Expect Wages To Grow At A Much Higher Rate Than In The Pre-Pandemic Period

A third reason for thinking that a soft landing may be easier to achieve this time around is that the US private-sector financial balance – the difference between what the private sector earns and spends – is still in surplus (Chart 14). This stands in contrast to the lead-up to both the 2001 and 2008-09 recessions, when the private sector was living beyond its means. Q: You have spoken a lot about the US, but the situation seems dire elsewhere. Europe may already be in recession as we speak! A: The near-term outlook for Europe is indeed challenging. The euro area economy grew by only 0.8% annualized in the first quarter. Mathieu Savary, BCA’s Chief European Strategist, expects an outright decline in output in Q2. To no one’s surprise, the war in Ukraine is weighing on European growth. The Bundesbank estimates that a full embargo of Russian oil and gas would reduce German real GDP by an additional 5% on top of the damage already inflicted by the war (Chart 15). Chart 14The US Private-Sector Financial Balance Remains In Surplus

The US Private-Sector Financial Balance Remains In Surplus

The US Private-Sector Financial Balance Remains In Surplus

Chart 15Germany’s Economy Will Sink Without Russian Energy

Goldilocks: A Skeptical Q&A

Goldilocks: A Skeptical Q&A

While such a full embargo is possible, it is not our base case. In a remarkable about-face, Putin now says he has “no problems” with Finland and Sweden joining NATO, provided that they do not place military infrastructure in their countries. He had previous threatened a military response at the mere suggestion of NATO membership. In any case, there are few signs that Putin’s increasingly insular and dictatorial regime would respond to an oil embargo or other economic incentives. The wealthy oligarchs who were supposed to rein him in are cowering in fear. It is also not clear if Europe would gain any political leverage over Russia by adopting policies that push its own economy into a recession. It is worth noting that the price of the December 2022 European natural gas futures contract is down 39% from its peak at the start of the war (Chart 16). It is also noteworthy that European EPS estimates have been trending higher this year even as GDP growth estimates have been cut (Chart 17). This suggests that the analyst earnings projections were too conservative going into the year. Chart 16European Natural Gas Futures Are High But Below Their Peak

European Natural Gas Futures Are High But Below Their Peak

European Natural Gas Futures Are High But Below Their Peak

Chart 17European And US EPS Estimates Have Been Trending Higher This Year

European And US EPS Estimates Have Been Trending Higher This Year

European And US EPS Estimates Have Been Trending Higher This Year

Chart 18Chinese Property Sector: Signs Of Contraction

Chinese Property Sector: Signs Of Contraction

Chinese Property Sector: Signs Of Contraction

Q: What about China? The lockdowns are crippling growth and the property market is in shambles. A: There is truth to both those claims. The government has all but said that it will not abandon its zero-Covid policy anytime soon, even going as far as to withdraw from hosting the 2023 AFC Asian Cup. While the number of new cases has declined sharply in Shanghai, future outbreaks are probable. On the bright side, China is likely to ramp up domestic production of Pfizer’s Paxlovid drug. Increased availability of the drug will reduce the burden of the disease once social distancing restrictions are relaxed. As far as the property market is concerned, sales, starts, completions, as well as home prices are all contracting (Chart 18). BCA’s China Investment Strategy expects accelerated policy easing to put the housing sector on a recovery path in the second half of this year. Nevertheless, they expect the “three red lines” policy to remain in place, suggesting that the rebound in housing activity will be more muted than in past recoveries.2 Ironically, the slowdown in the Chinese housing market may not be such a bad thing for the rest of the world. Remember, the main problem these days is inflation. To the extent that a sluggish Chinese housing market curbs the demand for commodities, this could provide some relief on the inflation front. Q: So bad news is good news. Interesting take. Let’s turn to markets. You mentioned earlier that equity sentiment was very bearish. Fair enough, but I would note the very same American Association of Individual Investors survey that you cited also shows that investors’ allocation to stocks is near record highs (Chart 19). Shouldn’t we look at what investors are doing rather than what they’re saying? A: The discrepancy may not be as large as it seems. As Chart 20 illustrates, investors may not like stocks, but they like bonds even less. Chart 19Individual Investors Still Hold A Lot Of Stock

Individual Investors Still Hold A Lot Of Stock

Individual Investors Still Hold A Lot Of Stock

Image

Chart 20B... But They Like Bonds Even Less

... But They Like Bonds Even Less

... But They Like Bonds Even Less

Chart 21Global Equities Are More Attractively Valued After The Recent Sell-Off

Global Equities Are More Attractively Valued After The Recent Sell-Off

Global Equities Are More Attractively Valued After The Recent Sell-Off

Global equities currently trade at 15.3-times forward earnings; a mere 12.5-times outside the US. The global forward earnings yield is 6.7 percentage points higher than the global real bond yield. In 2000, the spread between the earnings yield and the real bond yield was close to zero (Chart 21). It should also be mentioned that institutional data already show a sharp shift out of equities. The latest Bank of America survey revealed that fund managers cut equity allocations to a net 13% underweight in May from a 6% overweight in April and a net 55% overweight in January. Strikingly, fund managers were even more underweight bonds than stocks. Cash registered the biggest overweight in two decades. Q: Your bullish equity bias notwithstanding, you were negative on tech stocks last year, arguing that the NASDAQ would turn into the NASDOG. Given that the NASDAQ Composite is down 29% from its highs, is it time to increase exposure to some beaten down tech names? A: Both the cyclical and structural headwinds facing tech stocks that we discussed in These Three High-Flying Equity Sectors Could Come Crashing Back Down To Earth and The Disruptor Delusion remain in place. Nevertheless, with the NASDAQ Composite now trading at 22.6-times forward earnings, down from 32.9 at its peak last year, an underweight in tech is no longer appropriate (Chart 22). A neutral stance is now preferable. Chart 22Tech Stock Valuations Have Returned To Earth

Tech Stock Valuations Have Returned To Earth

Tech Stock Valuations Have Returned To Earth

Q: I guess if bond yields come down a bit more, that would help tech stocks? A: Yes. Tech stocks tend to be growth-oriented. Falling bond yields raise the present value of expected cash flows more for growth companies than for other firms. While we do expect global bond yields to eventually rise above current levels, yields are likely to decline modestly over the next 12 months as inflation temporarily falls. We expect the US 10-year yield to end the year at around 2.5%. Q: A decline in US bond yields would undermine the high-flying dollar, would it not? A: It depends on how bond yields abroad evolve. US Treasuries tend to be relatively high beta, implying that US yields usually fall more when global yields are declining (Chart 23). Thus, it would not surprise us if interest rate differentials moved against the dollar later this year. Chart 23US Treasuries Have A Higher Beta Than Most Other Government Bond Markets

US Treasuries Have A Higher Beta Than Most Other Government Bond Markets

US Treasuries Have A Higher Beta Than Most Other Government Bond Markets

It is also important to remember that the US dollar is a countercyclical currency (Chart 24). If global growth picks up as pandemic dislocations fade and the Ukraine war winds down, the dollar is likely to weaken. Chart 24The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

Image

A wider trade deficit could also imperil the greenback. The US trade deficit has increased from US$45 billion in December 2019 to US$110 billion. Equity inflows have helped finance the trade deficit, but net flows have turned negative of late (Chart 25). Finally, the dollar is quite expensive – 27% overvalued based on Purchasing Power Parity exchange rates. Q: Let’s sum up. Please review your asset allocation recommendations both for the next 12 months and beyond. A: To summarize, global inflation has peaked. Growth should pick up later this year as supply-chain bottlenecks abate. The combination of falling inflation and supply-side led growth will provide a springboard for equities. We expect global stocks to rise 15%-to-20% over the next 12 months. Historically, non-US stocks have outperformed their US peers when the dollar has been weakening (Chart 26). EM stocks, in particular, have done well in a weak dollar environment Chart 26Non-US Stocks Will Benefit From A Weaker US Dollar

Non-US Stocks Will Benefit From A Weaker US Dollar

Non-US Stocks Will Benefit From A Weaker US Dollar

Chart 27The Market Is Too Pessimistic On Default Risk

The Market Is Too Pessimistic On Default Risk

The Market Is Too Pessimistic On Default Risk

Within fixed-income portfolios, we recommend a modest long duration stance over the next 12 months. We favor high-yield credit over safer government bonds. US high-yield spreads imply a default rate of 6.2% over the next 12 months compared to a trailing 12-month default rate of only 1.2% (Chart 27). Chart 28Falling Inflation Will Buoy Consumer Sentiment

Falling Inflation Will Buoy Consumer Sentiment

Falling Inflation Will Buoy Consumer Sentiment

Our guess is that this Goldilocks environment will end towards the end of next year. As inflation comes down, real wage growth will turn positive. Consumer confidence, which is now quite depressed, will improve (Chart 28). Stronger demand will cause inflation to reaccelerate in 2024, setting the stage for another round of central bank rate hikes. Peter Berezin Chief Global Strategist peterb@bcaresearch.com Follow me on LinkedIn Twitter Footnotes 1 The Federal Reserve targets an average inflation rate of 2% for the Personal Consumption Expenditures (PCE) index. Due to compositional differences between the two indices, CPI inflation has historically averaged 30-to-50 basis points higher than PCE inflation. This is why the Fed effectively targets a CPI inflation rate of 2.3%-to-2.5%. 2 The People’s Bank of China and the housing ministry issued a deleveraging framework for property developers in August 2020, consisting of a 70% ceiling on liabilities-to-assets, a net debt-to-equity ratio capped at 100%, and a limit on short-term borrowing that cannot exceed cash reserves. Developers breaching these “red lines” run the risk of being cut off from access to new loans from banks, while those who respect them can only increase their interest-bearing borrowing by 15% at most. Global Investment Strategy View Matrix

Goldilocks: A Skeptical Q&A

Goldilocks: A Skeptical Q&A

Special Trade Recommendations Current MacroQuant Model Scores

Goldilocks: A Skeptical Q&A

Goldilocks: A Skeptical Q&A

Listen to a short summary of this report. Executive Summary EUR/JPY And The DXY: Unsustainable Gap

EUR/JPY And The DXY: Unsustainable Gap

EUR/JPY And The DXY: Unsustainable Gap

Three interrelated themes are likely to play out by the end of 2022 – peak Fed hawkishness, continued central bank convergence, and nascent green shoots in global economic growth. We are playing the first theme via an outright short DXY position. We are also hedging this bet through a short EUR/JPY trade, a corresponding play on the second theme. Betting on nascent green shoots in economic growth can be expressed via a long Aussie position, or more prudently, a short CHF/SEK bet. We are long a CAD and NOK basket against the RUB, a play on an eventual recovery in oil demand, and the premium that these blends will continue to command relative to Russian oil. Finally, most of our trades remain at the crosses due to elevated FX volatility which has boosted safe-haven demand for the dollar. The admission of Sweden and Finland into NATO could increases the risk of miscalculation on the part of Russia, which will continue to prop near-term safe-haven demand for the dollar. RECOMMENDATIONS INCEPTION LEVEL inception date RETURN Short EUR/JPY 133.28 2022-05-12 -0.73 Bottom Line: Continue to focus on relative value trades at the crosses, until signs emerge that FX volatility is peaking, which will be more conducive for direct USD bets. Feature Chart 1Dollar Capitulation Occurs At Record Valuation And A Record Deficit

Dollar Capitulation Occurs At Record Valuation And A Record Deficit

Dollar Capitulation Occurs At Record Valuation And A Record Deficit