Emerging Markets

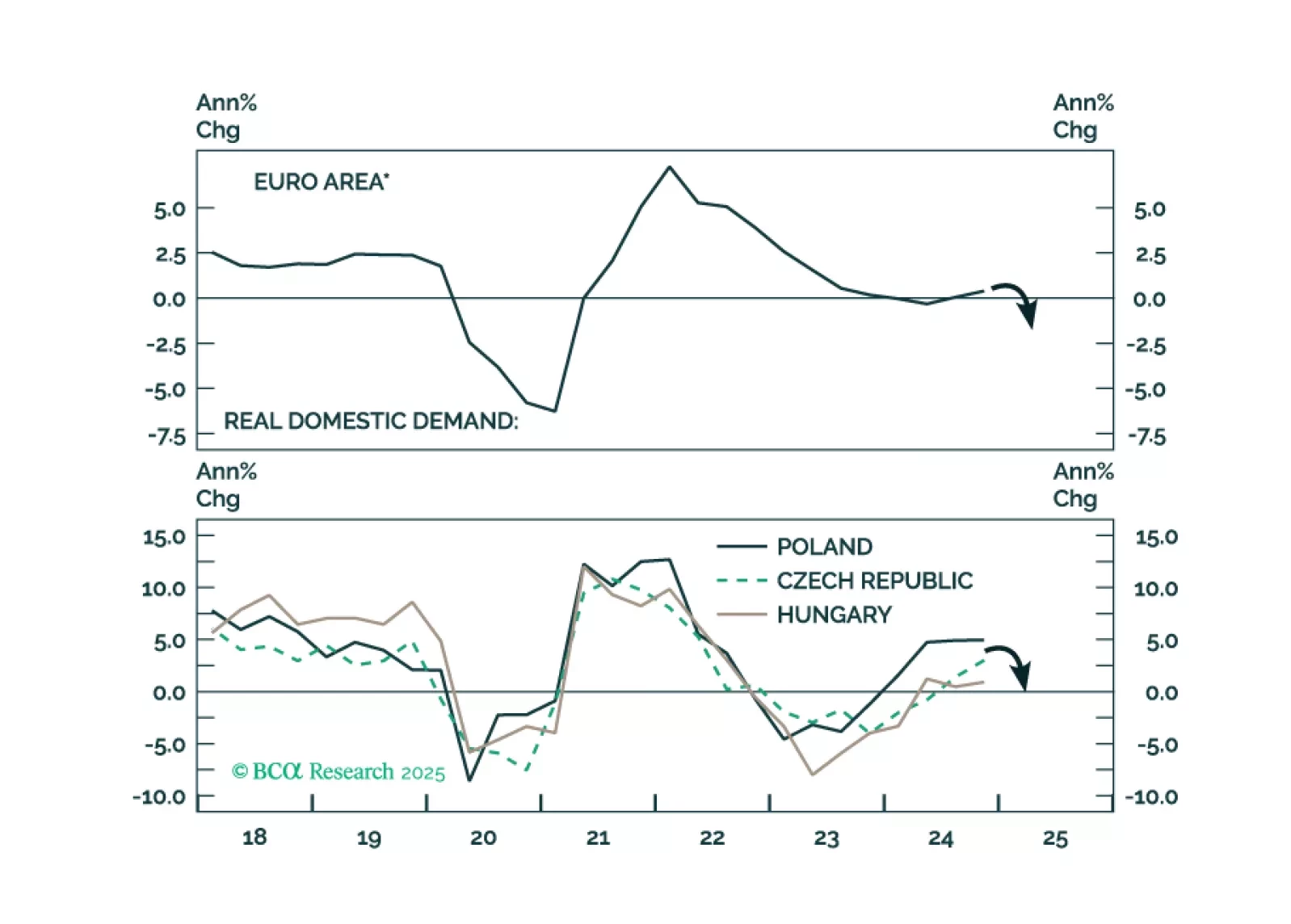

The European economies are facing a major deflationary shock. We recommend that investors stay long a basket of Central European (CE3) domestic bonds. They should also upgrade CE3 bonds and stocks in their respective EM portfolios.

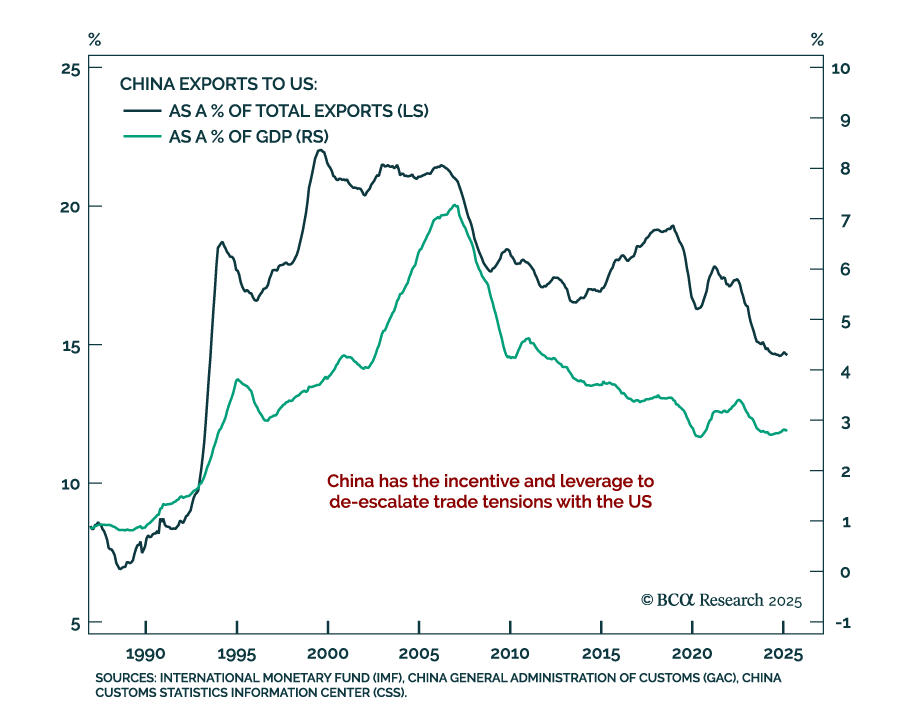

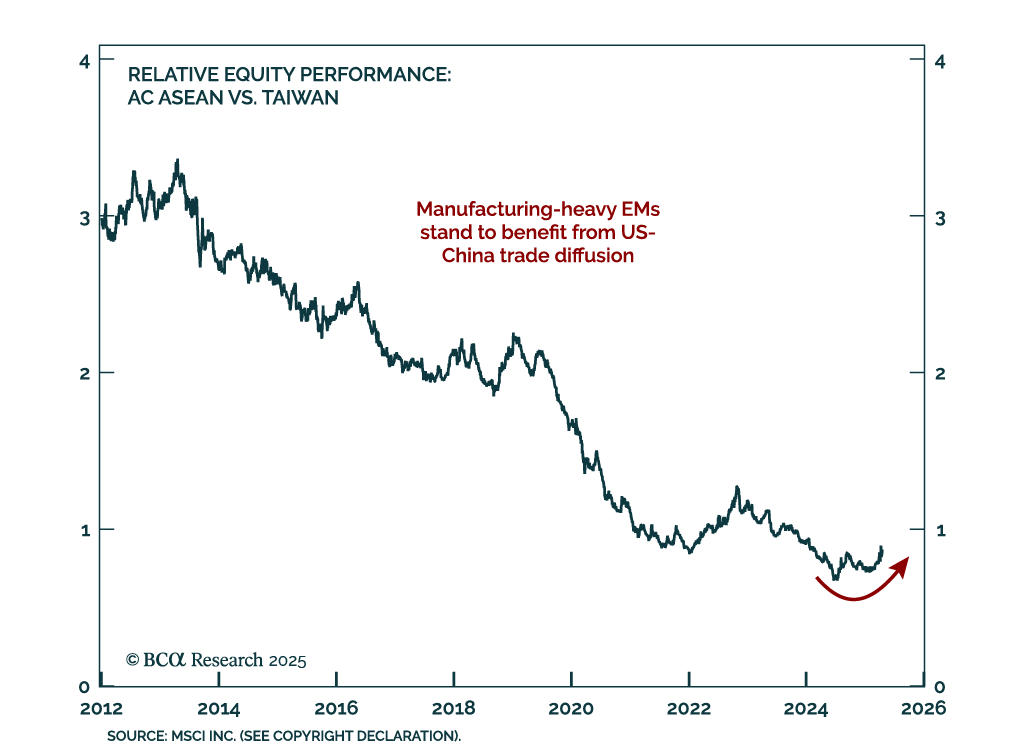

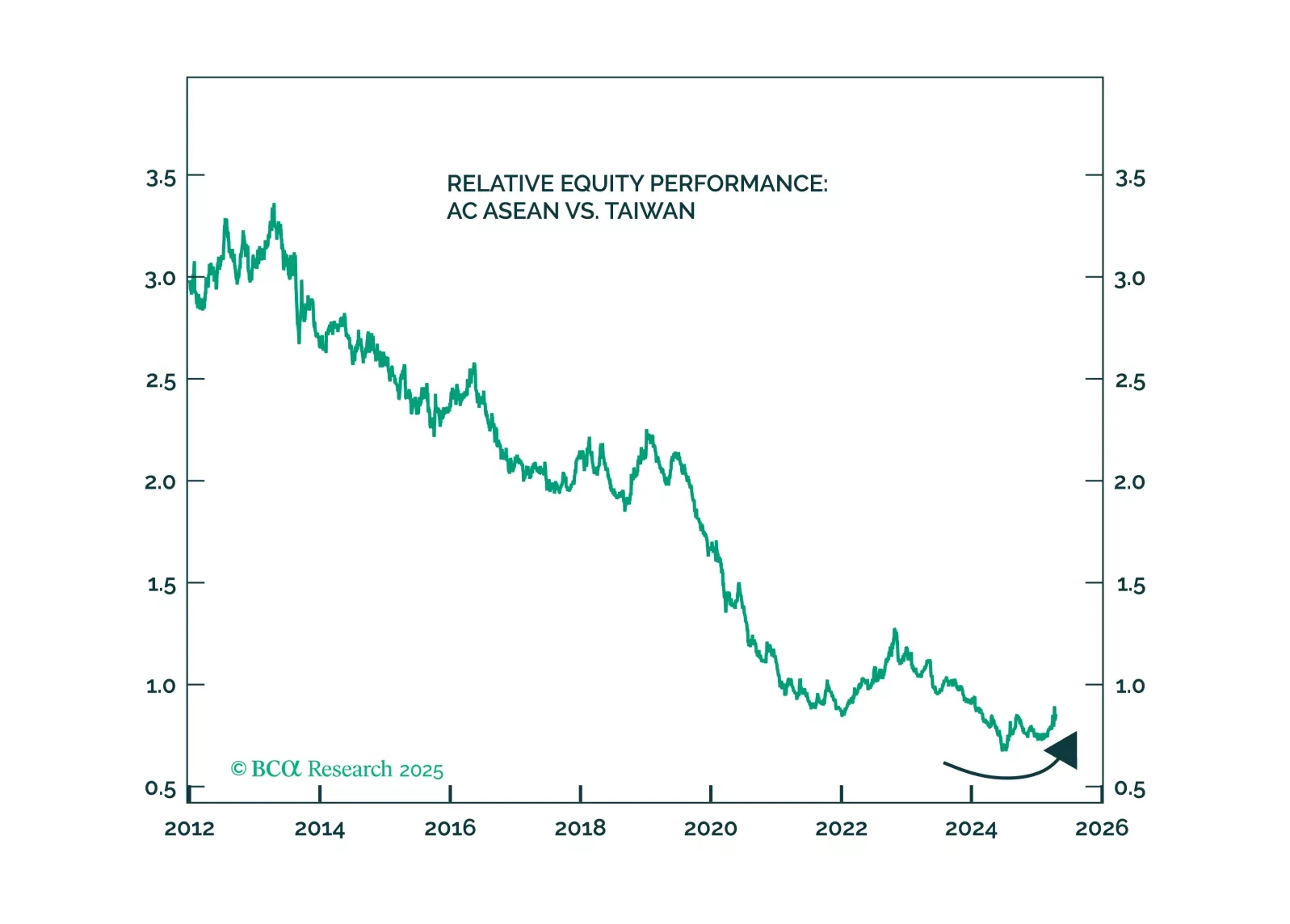

Upgrade the odds of a full-scale war in the Taiwan Strait from 5% to 10%. Rapid escalation of US-China economic war raises the probability of tensions spilling into the military-strategic domain. Investors should buy insurance against this tail risk while it is cheap. Meanwhile, use this year’s trade shock and equity volatility to increase allocation to EM manufacturing states.

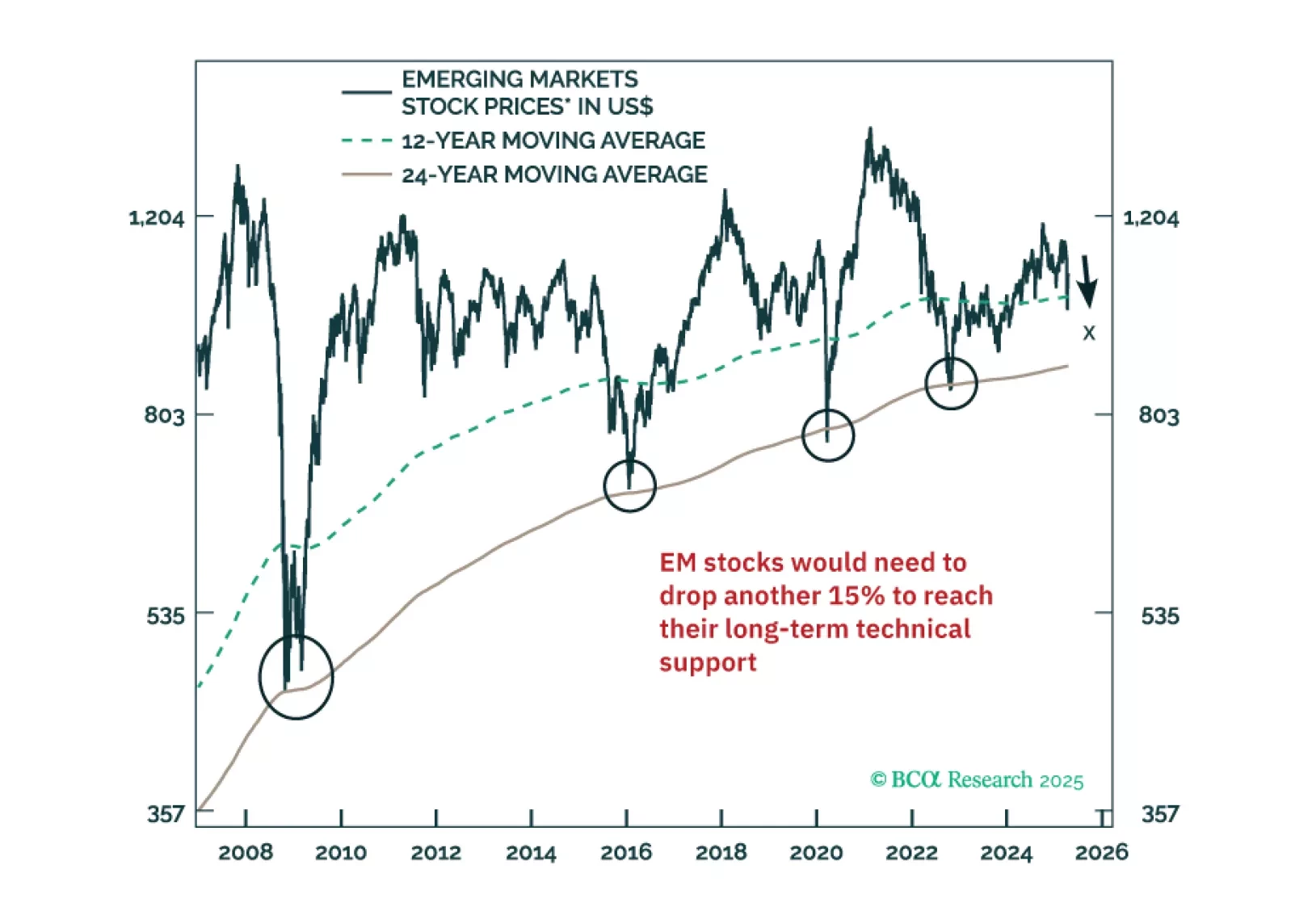

Even after policymakers retract their prejudicial actions, financial markets might continue selling off. We compare the current tariff shock with two past episodes when policy reversals did not produce market turnarounds: (1) the RMB devaluation in August 2015, and (2) the US Congress's initial rejection of the TARP bank bailout program in 2008. In addition, we show numerous technical indicators illustrating at which levels the potential bottom in various equity markets could be.

Europe’s near-term outlook remains clouded by uncertainty, even after the tariff reprieve. Our latest update breaks down why the risks to growth, profits, and financial conditions are still skewed to the downside — with Sweden standing out as a key bellwether.

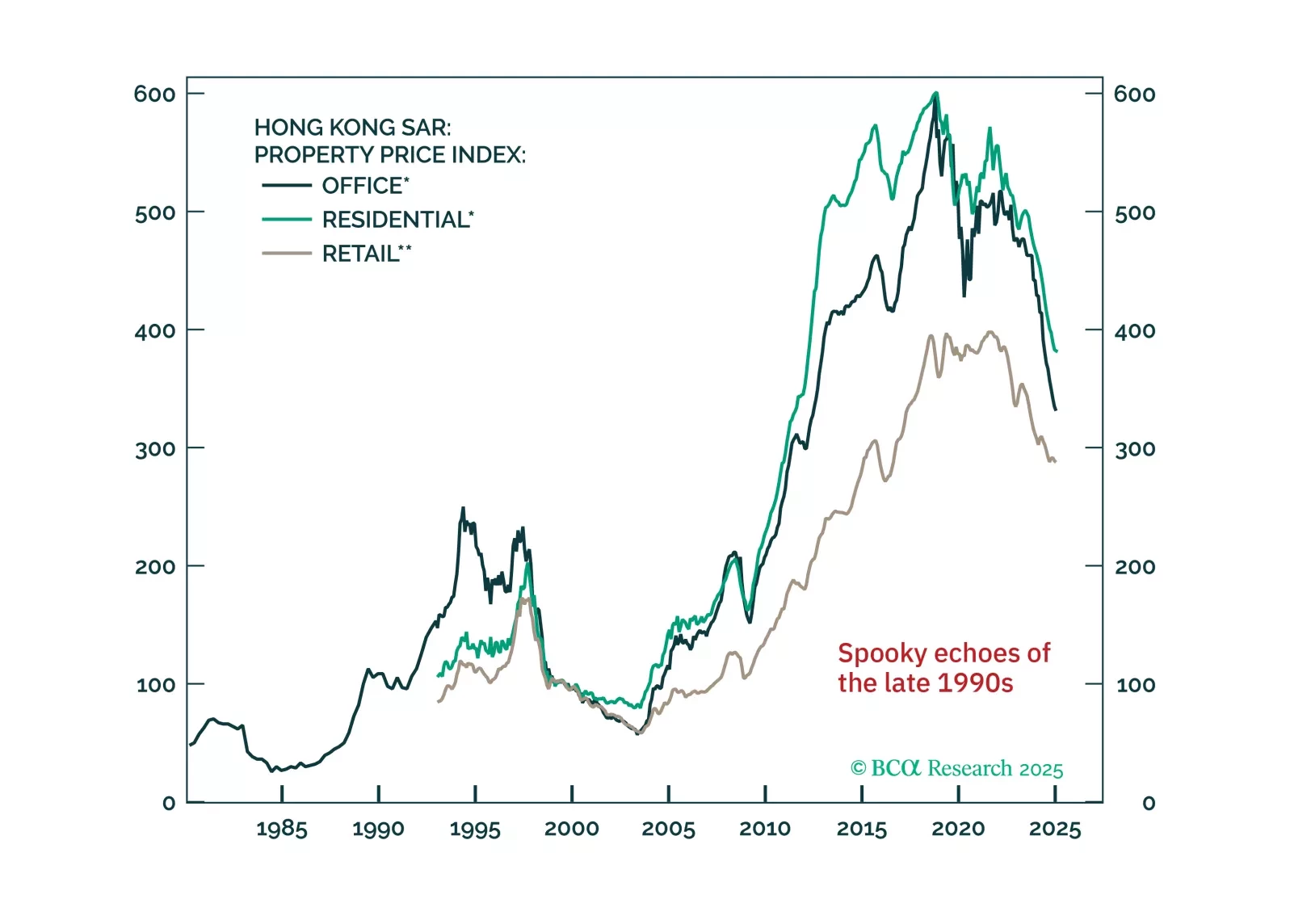

This week, we look at the sustainability of the HKD peg as the next whale to move markets, given what is happening to tariffs. After careful analysis, our bias is that it is here to stay. With the DXY dipping below 100, we are likely to see a rebound, which is actually bad news for the Hong Kong region of China, since it will tighten financial conditions. We have no new short-term trades, but if the peg broke, you want to be short HKD/JPY.