Emerging Markets

BCA Research's Geopolitical Strategy and Commodity & Energy Strategy services have published a Special Report that argues that commodity markets will face growing supply challenges over the next decade as the competition between the US and China…

The Bank of Korea (BoK) hiked its benchmark interest rate by 25bps to 0.75% yesterday, becoming the first major Asian central bank to begin dialing back pandemic-era monetary stimulus. The move was somewhat contentious, with one dissenting vote and only 16 of…

Highlights Commodity markets will face growing supply challenges over the next decade as the US and China prepare for war, if only to deter war. Chinese President Xi Jinping's push for greater self-reliance at home and supply chain security abroad is reinforced by the West’s focus on the same interests. The erosion of a single rules-based global trade system increases the odds of economic and even military conflict. The competition for security is precipitating a reforging of global supply chains and a persistent willingness to use punitive measures, which can escalate into boycotts, embargoes, and even blockades (i.e. not only Huawei). The risk of military engagements will rise, particularly along global chokepoints and sea lanes needed to transport vital commodities. Import dependency and supply chain risk are powerful drivers of decarbonization efforts, especially in China. On net, geopolitical trends will keep the balance of commodity-price risks tilted to the upside. Commodity and Energy Strategy remains long commodity index exposure on a strategic basis via the S&P GSCI and the COMT ETF. Note: Even in the short term, a higher geopolitical risk premium is warranted in oil prices due to US-Iran conflict. Feature The Chinese Communist Party (CCP) under President Xi Jinping has embarked on a drive toward autarky, or economic self-sufficiency, that has enormous implications, especially for global commodities. Beijing believes it can maintain central control, harness technology, enhance its manufacturing prowess, and grow at a reasonable rate, all while bulking up its national security. The challenge is to maintain social stability and supply security through the transition. China lives in desperate fear of the chaos that reigned throughout most of the twentieth and twenty-first centuries, which also enabled foreign domination (Chart 1). The problem for the rest of the world is that Chinese nationalism and assertive foreign policy are integral aspects of the new national strategy. They are needed to divert the public from social ills and deter foreign powers that might threaten China’s economy and supply security. Chart 1China Fears Any Risk Of Another ‘Century Of Humiliation’

US-China: War Preparation Pushes Commodity Demand

US-China: War Preparation Pushes Commodity Demand

The chief obstacle for China is the United States, which remains the world leader even though its share of global power and wealth is declining over time. The US is formally adopting a policy of confrontation rather than engagement with China. For example, the Biden administration is co-opting much of the Trump administration's agenda. Infrastructure, industrial policy, trade protectionism, and the “pivot to Asia” are now signature policies of Biden as well as Trump (Table 1).1 Table 1US Strategic Competition Act Highlights Return Of Industrial Policy, Confrontation With China

US-China: War Preparation Pushes Commodity Demand

US-China: War Preparation Pushes Commodity Demand

Many of these policies are explicitly related to the strategic aim of countering China’s rise, which is seen as vitiating the American economy and global leadership. Biden’s Trump-esque policies are a powerful indication of where the US median voter stands and hence of long-term significance (Chart 2). Thus competition between the US and China for global economic, military, and political leadership is entering a new phase. China’s drive for self-reliance threatens the US-led global trade system, while the US’s still-preeminent geopolitical power threatens China’s vital lines of supply. Chart 2US Public’s Fears Are China-Centric

US-China: War Preparation Pushes Commodity Demand

US-China: War Preparation Pushes Commodity Demand

Re-Ordering Global Trade The US’s and China’s demonstrable willingness to use tariffs, non-tariff trade barriers, export controls, and sanctions cannot be expected to abate given that they are locked in great power competition (Chart 3). More than likely, the US and China will independently pursue trade relations with their respective allies and partners, which will replace the mostly ineffective World Trade Organization (WTO) framework. The WTO is the successor to the rules-based and market-oriented system known as the General Agreement on Tariffs and Trade (GATT), which was formed following World War II. The GATT’s founders shared a strong desire to avoid a repeat of the global economic instability brought on by World War I, the Great Crash of 1929, and the retreat into autarky and isolationism that led to WWII. Chart 3US and China Imposing Trade Restrictions

US and China Imposing Trade Restrictions

US and China Imposing Trade Restrictions

This inter-war period saw domestically focused monetary policies and punishing tariffs that spawned ruinous bouts of inflation and deflation. Minimizing tariffs, leveling the playing field in trading markets, and reducing subsidization of state corporate champions were among the GATT's early successes. The WTO, like the GATT before it, has no authority to command a state to change its economy or the way it chooses to organize itself. At its inception the GATT's modus vivendi was directed at establishing a rules-based system free of excessive government intrusion and regulation. If governments agreed to reduce their domestic favoritism, they could all improve their economic efficiency while avoiding a relapse into autarky and the military tensions that go with it.2 The prime mover in the GATT's founding and early evolution – the USA – firmly believed that exclusive trading blocs had created the groundwork for economic collapse and war. These trading blocs had been created by European powers with their respective colonies. During the inter-war years the revival of protectionism killed global trade and exacerbated the Great Depression. After WWII, Washington was willing to use its power as the global hegemon to prevent a similar outcome. Policymakers believed that European and global economic integration would encourage inter-dependency and discourage protectionism and war. The fall of the Soviet Union reinforced this neoliberal Washington Consensus. Countries like India and China adopted market-oriented policies. The WTO was formed along with a range of global trade deals. Ultimately the US and the West cleared the way for China to join the trading bloc, hoping that the transition from communism to capitalism would eventually be coupled with social and even political liberalization. The world took a very different turn as the United States descended into a morass of domestic political divisions and foreign military adventures. China seized the advantage to expand its economy free of interference from the US or West. The West failed to insist that liberal economic reforms keep pace.3 Moreover, when China joined the WTO in 2001, the organization was in a state of "regulatory stalemate," which made it incapable of dealing with the direct challenges presented by China.4 Today President Xi has consolidated control over the Communist Party and directs its key economic, political, and military policymaking bodies. He has deepened party control down to the management level of SOEs – hiring and firing management. SOEs have benefited from Xi’s rule (Chart 4). But now the West is also reasserting the role of the state in the economy and trade, which means that punitive measures can be brought to bear on China’s SOEs. Chart 4State-Owned Enterprises Benefit From Xi Administration

State-Owned Enterprises Benefit From Xi Administration

State-Owned Enterprises Benefit From Xi Administration

What Comes After The WTO? The CCP has shown no interest in coming around to the WTO's founding beliefs of government non-interference in the private sector. For example, it is doubling down on subsidization and party control of SOEs, which compete against firms in other WTO member states. Nor has the party shown any inclination to accept a trade system based on the GATT/WTO founding members' Western understanding of the rule of law. These states represent market-based economies with long histories of case law for settling disputes. Specifically, China’s fourteenth five-year plan and recent policies re-emphasize the need to upgrade the manufacturing sector rather than rebalancing the economy toward household consumption. The latter would reduce imbalances with trade deficit countries like the US but China is wary of the negative social consequences of too rapidly de-industrializing its economy. It wants to retain its strategic and economic advantage in global manufacturing and it fears the social and political consequences of fully adopting consumer culture (Chart 5). Chart 5China’s Economic Plans Re-Emphasize Manufacturing, Not Consumption

US-China: War Preparation Pushes Commodity Demand

US-China: War Preparation Pushes Commodity Demand

The US, EU, and Japan have proposed reform measures for the WTO aimed at addressing “severe excess capacity in key sectors exacerbated by government financed and supported capacity expansion, unfair competitive conditions caused by large market-distorting subsidies and state owned enterprises, forced technology transfer, and local content requirements and preferences.”5 But these measures are unlikely to succeed. China disagrees with the West’s characterization. In 2018-19, during the trade war with the US, Beijing contended that WTO members must “respect members’ development models.” China formally opposes “special and discriminatory disciplines against state-owned enterprises in the name of WTO reform.”6 In bilateral negotiations with the US this year, China’s first demand is that the US not to oppose its development model of “socialism with Chinese characteristics” (Table 2). Table 2China’s Three Diplomatic Demands Of The United States (2021)

US-China: War Preparation Pushes Commodity Demand

US-China: War Preparation Pushes Commodity Demand

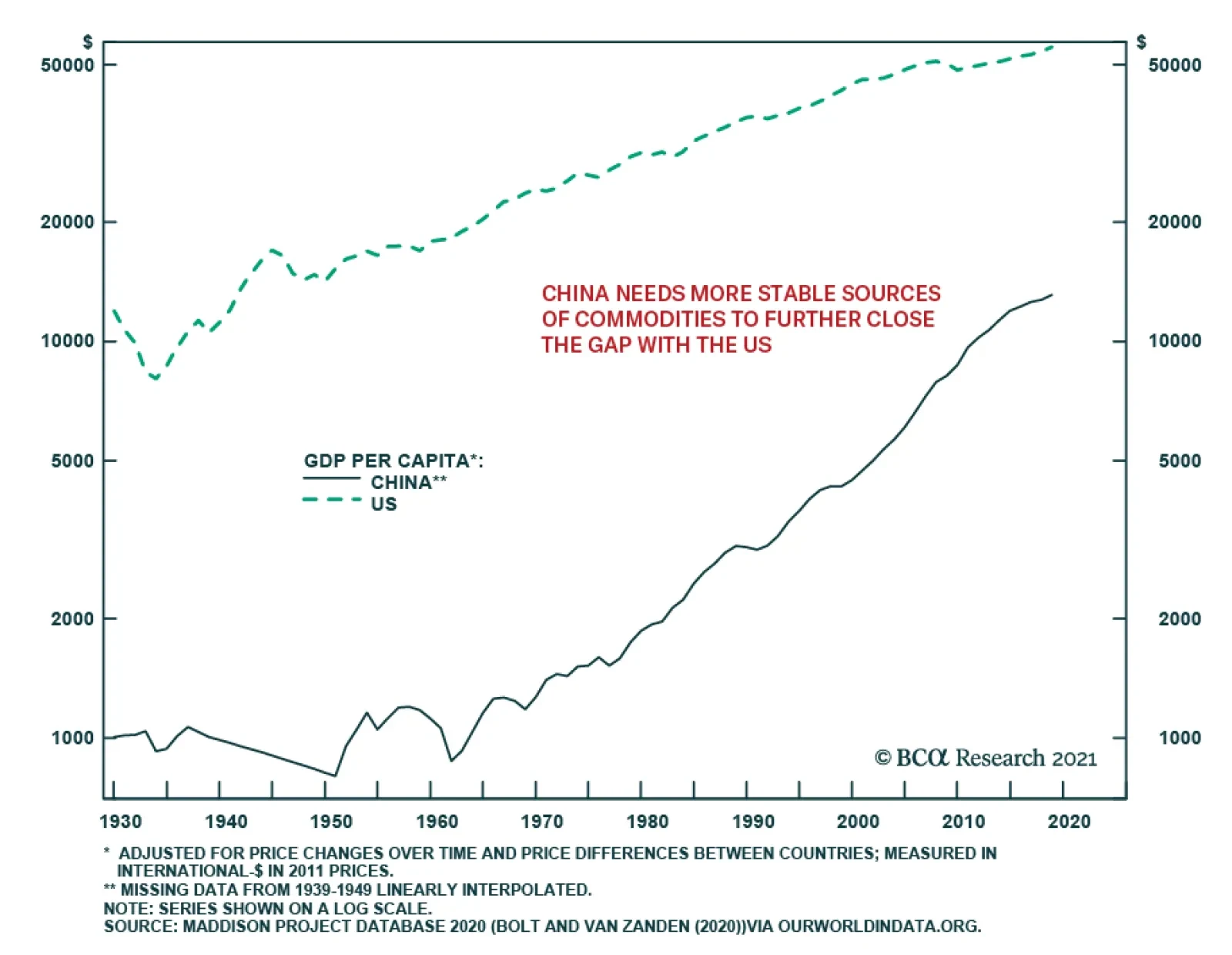

Yet it is hard for the US not to oppose this model because it involves Beijing using the state’s control of the economy to strengthen national security strategy, namely by the fusion of civil and military technology. Going forward, the Biden administration will violate the number one demand that Chinese diplomats have made: it will attempt to galvanize the democracies to put pressure on China’s development model. China’s demand itself reflects its violation of the US primary demand that China stop using the state to enhance its economy at the expense of competitors. If a breakdown in global trading rules is replaced by the US and China forming separate trading blocs with their allies and partners, the odds of repeating the mistakes of the inter-bellum years of 1918-39 will significantly increase. Tariff wars, subsidizing national champions, heavy taxation of foreign interests, non-tariff barriers to trade, domestic-focused monetary policies, and currency wars would become more likely. China’s Strategic Vulnerability The CCP has delivered remarkable prosperity and wealth to the average Chinese citizen in the 43 years since it undertook market reforms, and especially since its accession to the WTO in 2001 (Chart 6). China has transformed from an economic backwater into a $15.4 trillion (2020) economy and near-peer competitor to the US militarily and economically.7 This growth has propelled China to the top of commodity-importing and -consuming states globally for base metals and oil. We follow these markets closely, because they are critical to sustaining economic growth, regardless of how states are organized. Production of and access to these commodities, along with natural gas, will be critical over the next decade, as the world decarbonizes its energy sources, and as the US and China address their own growth and social agendas while vying for global hegemony. Decarbonization is part of the strategic race since all major powers now want to increase economic self-sufficiency and technological prowess. Chart 6CCPs Remarkable Success In Growing Chinas Economy

CCPs Remarkable Success In Growing Chinas Economy

CCPs Remarkable Success In Growing Chinas Economy

Over recent decades China has become the largest importer of base metals ores (Chart 7) and the world's top refiner of many of these metals. In addition, it is the top consumer of refined metal (Chart 8). Chart 7China Is World’s Top Ore Importer

US-China: War Preparation Pushes Commodity Demand

US-China: War Preparation Pushes Commodity Demand

Chart 8China Is Worlds Top Refined Metal Consumer

China Is Worlds Top Refined Metal Consumer

China Is Worlds Top Refined Metal Consumer

By contrast, the US is not listed among ore importers or metals consumers in the Observatory of Economic Complexity (OEC) databases we used to map these commodities. This reflects not only domestic supplies but also the lack of investment and upgrades to the US's critical infrastructure over 2000-19.8 Going forward, the US is trying to invest in “nation building” at home. An enormous change has taken shape in strategic liabilities. In the oil market, the US went from being the world's largest importer of oil in 2000, accounting for more than 24% of imports globally, to being the largest oil and gas producer by 2019, even though it still accounted for more than 12% of the world's imports (Chart 9). In 2000, China accounted for ~ 3.5% of the world's oil imports and by 2019 it was responsible for nearly 21%. China is far behind per capita US energy consumption, given its large population, but it is gradually closing the gap (Chart 10). Overall energy consumption in China is much higher than in the US (Chart 11). Chart 9US Oil Imports Collapse As Shale Production Grows

US-China: War Preparation Pushes Commodity Demand

US-China: War Preparation Pushes Commodity Demand

Chart 10Energy Use Per Capita In China Far From US Levels...

Energy Use Per Capita In China Far From US Levels...

Energy Use Per Capita In China Far From US Levels...

Chart 11China Is World’s Largest Primary Energy Consumer

US-China: War Preparation Pushes Commodity Demand

US-China: War Preparation Pushes Commodity Demand

China's impressive GDP growth in the twenty-first century is primarily responsible for China's stunning growth in imports and consumption of oil (Chart 12) and copper (Chart 13), which we track closely as a proxy for the entire base-metals complex. Chart 12Global Oil Demand Forecast Remains Steady Chinas GDP Drives Oil Consumption, Imports

Global Oil Demand Forecast Remains Steady Chinas GDP Drives Oil Consumption, Imports

Global Oil Demand Forecast Remains Steady Chinas GDP Drives Oil Consumption, Imports

Chart 13Global Oil Demand Forecast Remains Steady Chinas GDP Drives Refined Copper Consumption And Ore Imports

Global Oil Demand Forecast Remains Steady Chinas GDP Drives Refined Copper Consumption And Ore Imports

Global Oil Demand Forecast Remains Steady Chinas GDP Drives Refined Copper Consumption And Ore Imports

China’s importance in these markets points to an underlying strategic weakness, which is its dependency on imports. This in turn points to the greatest danger of the breakdown in US-China relations and the global trade system. The Road To War? China is extremely anxious about maintaining supply security in light of these heavy import needs. Its pursuit of economic self-sufficiency, including decarbonization, is driven by its fear of the US’s ability to cut off its key supply lines. China’s first goal in modernizing its military in recent years was to develop a naval force capable of defending the country from foreign attack, particularly in its immediate maritime surroundings. Historically China suffered from invaders across the sea who took advantage of its weak naval power to force open its economy and exploit it. Today China is thought to have achieved this security objective. It is believed to have a high level of capability within the “first island chain” that surrounds the coast, from the Korean peninsula to the Spratly Islands, including southwest Japan and Taiwan (Map 1).9 China’s militarization of the South China Sea, suppression of Hong Kong, and intimidation of Taiwan shows its intention to dominate Greater China, which would put it in a better strategic position relative to other countries. Map 1China’s Navy Likely Achieved Superiority Within The First Island Chain

US-China: War Preparation Pushes Commodity Demand

US-China: War Preparation Pushes Commodity Demand

China’s capability can be illustrated by comparing its naval strength to that of the United States, the most powerful navy in the world. While the US is superior, China would be able to combine all three of its fleets within the first island China, while the US navy would be dispersed across the world and divided among a range of interests to defend (Table 3). China would also be able to bring its land-based air force and missile firepower to bear within the first island chain, as opposed to further abroad.10 Table 3China’s Naval Growth Enables Primacy Within First Island Chain

US-China: War Preparation Pushes Commodity Demand

US-China: War Preparation Pushes Commodity Demand

In this sense China is militarily capable of conquering Taiwan or other nearby islands. President Xi Jinping had in fact ordered China’s armed forces be capable of doing so by 2020.11 Taiwan continues to be the most significant source of insecurity for the regime. True, a military victory would likely be a pyrrhic victory, as Taiwan’s wealth and tech industry would be destroyed, but China probably has the raw military capability to defeat Taiwan and its allies within this defined space. However, this military capability needs to be weighed against economic capability. If China seized military control of Taiwan, or Okinawa or other neighboring territories, the US, Japan, and their allies would respond by cutting off China’s access to critical supplies. Most obviously oil and natural gas. China’s decarbonization has been impressive but the reliance on foreign oil is still a fatal strategic vulnerability over the next few years (Chart 14). China is rapidly pursuing a Eurasian strategy to diversify away from the Middle East in particular. But it still imports about half its oil from this volatile region (Chart 15). The US navy is capable of interdicting China’s critical oil flows, a major inhibition on China’s military ambitions within the first island chain. Chart 14Chinas Energy Diversification Still Leaves Vulnerabilities

Chinas Energy Diversification Still Leaves Vulnerabilities

Chinas Energy Diversification Still Leaves Vulnerabilities

Of course, if the US and its allies ever blockaded China, or if China feared they would, Beijing could be driven to mount a desperate attack to prevent them from doing so, since its economic, military, and political survival would be on the line. Chart 15China Still Dependent On Middle East Energy Supplies

China Still Dependent On Middle East Energy Supplies

China Still Dependent On Middle East Energy Supplies

The obvious historical analogy is the US-Japan conflict in WWII. Invasions that lead to blockades will lead to larger invasions, as the US and Japan learned.12 However, the lesson from WWII for China is that it should not engage the US navy until its own naval power has progressed much further. In the event of a conflict, the US would be imposing a blockade at a distance from China’s naval and missile forces. When it comes to the far seas, China’s naval capabilities are extremely limited. Military analysts highlight that China lacks a substantial naval presence in the Indian Ocean. China relies on commercial ports, where it has partial equity ownership, for ship supply and maintenance (Table 4). This is no substitute for naval basing, because dedicated military facilities are lacking and host countries may not wish to be drawn into a conflict. Table 4China’s Network Of Part-Owned Ports Across The World: Useful But Not A Substitute For Military Bases

US-China: War Preparation Pushes Commodity Demand

US-China: War Preparation Pushes Commodity Demand

Further, Beijing lacks the sea-based air power necessary to defend its fleets should they stray too far. And it lacks the anti-submarine warfare capabilities necessary to defend its ships.13 These capabilities are constantly improving but at the moment they are insufficient to overthrow US naval control of the critical chokepoints like the Strait of Hormuz or Strait of Malacca. While China’s naval power is comparable to the US’s Asia Pacific fleet (the seventh fleet headquartered in Japan), it is much smaller than the US’s global fleet and at a much greater disadvantage when operating far from home. China’s navy is based at home and focused on its near seas, whereas US fleet is designed to operate in the far seas, especially the Persian Gulf, which is precisely the strategic area in question (Chart 16).14 China is gradually expanding its navy and operations around the world, so over time it may gain the ability to prevent the US from cutting off its critical supplies in the Persian Gulf. But not immediately. The implication is that China will have to avoid direct military conflict with the United States until its military and naval buildup has progressed a lot further. Chart 16China’s Navy At Huge Disadvantage In Distant Seas

US-China: War Preparation Pushes Commodity Demand

US-China: War Preparation Pushes Commodity Demand

Meanwhile Beijing will continue diversifying its energy sources, decarbonizing, and forging supply chains across Eurasia via the Belt and Road Initiative. What could go wrong? We would highlight a few risks that could cause China to risk war even despite its vulnerability to blockade: Chart 17China’s Surplus Of Males Undergirds Rise In Nationalism

US-China: War Preparation Pushes Commodity Demand

US-China: War Preparation Pushes Commodity Demand

Domestic demographic pressure. China is slated to experience a dramatic bulge in the male-to-female ratio over the coming decade (Chart 17).15 A surfeit of young men could lead to an overshoot of nationalism and revanchism. This trend is much more important than the symbolic political anniversaries of 2027, 2035, and 2049, which analysts use to predict when China’s military might launch a major campaign. Domestic economic pressure. China’s turn to nationalism reflects slowing income growth and associated social instability. An economic crisis in China would be worrisome for regional stability for many reasons, but such pressures can lead nations into foreign military adventures. Domestic political pressure. China has shifted from “consensus rule” to “personal rule” under Xi Jinping. This could lead to faulty decision-making or party divisions that affect national policy. A leadership that carefully weighs each strategic risk could decay into a leadership that lacks good information and perspective. The result could be hubris and belligerence abroad. Foreign aggression. Attempts by the US or other powers to arm China’s neighbors or sabotage China’s economy could lead to aggressive reaction. The US’s attempt to build a technological blockade shows that future embargoes and blockades are not impossible. These could prompt a war rather than deter it, as noted above. Foreign weakness. China’s capabilities are improving over time while the US and its allies lack coordination and resolution. An opportunity could arise that China’s strategists believe they cannot afford to miss. Afghanistan is not one of these opportunities, but a US-Iran war or another major conflict with Russia could be. The breakdown in global trade is concerning because without an economic buffer, states may resort to arms to resolve disputes. History shows that military threats intended to discourage aggressive behavior can create dilemmas that incentivize aggression. The behavior of the US and China suggests that they are preparing for war, even if we are generous and assume that they are doing so only to deter war. Both countries are nuclear powers so they face mutually assured destruction in a total war scenario. But they will seek to improve their security within that context, which can lead to naval skirmishes, proxy wars, and even limited wars with associated risks of going nuclear. Investment Takeaways The pursuit of the national interest today involves using fiscal means to create more self-sufficient domestic economies and reduce international supply risks. Both China and the West are engaged in major projects to this end, including high-tech industrialization, domestic manufacturing, and decarbonization. These trends are generally bullish for commodities, even though they include trends like military modernization and naval expansion that could well be a prelude to war. War itself leads to commodity shortages and commodity price inflation, but of course it is disastrous for the people and economies involved. Fortunately, strategic deterrence continues to operate for the time being. The underlying geopolitical trend will put commodity markets under continual pressure. A final urgent update on oil and the Middle East: The US attempt to conduct a strategic “pivot” to Asia Pacific faces a critical juncture. Not because of Afghanistan but because of Iran. The Biden administration will have trouble unilaterally lowering sanctions on Iran after the humiliating Afghanistan pullout. The new administrations in both Iran and Israel are likely to establish red lines and credible threats. A higher geopolitical risk premium is thus warranted immediately in global oil markets. Beyond short-term shows of force, everything depends on whether the US and Iran can find a temporary deal to avoid the path to a larger war. But for now short-term geopolitical risks are commodity-bullish as well as long-term risks. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 There are also significant differences between Biden and Trump in other areas such as redistribution, immigration, and social policy. 2 See Ravenhill, John (2020), Regional Trade Agreements, Chapter 6 in Global Political Economy, which he edited for Oxford University Press, particularly pp. 156-9. 3 “As time went by, the United States realized that Communism not only did not retreat, but also further advanced in China, with the state-owned economy growing stronger and the rule of the Party further entrenched in the process." See Henry Gao, “WTO Reform and China Defining or Defiling the Multilateral Trading System?” Harvard International Law Journal 62 (2021), p. 28, harvardilj.org. 4 See Mavroidis, Petros C. and Andre Sapir (2021), China and the WTO, Why Multilateralism Still Matters (Princeton University Press) for discussion. See also Confronting the Challenge of Chinese State Capitalism published by the Center for Strategic & International Studies 22 January 2021. 5 Gao (2021), p. 19. 6 Gao (2021), p. 24. 7 Please see China's GDP tops 100 trln yuan in 2020 published by Xinhuanet 18 January 2021. 8 We excluded 2020 because of the COVID-19 pandemic's effects on supply and demand for these ores, metals and crude oil. 9 See Captain James Fanell, “China’s Global Navy Strategy and Expanding Force Structure: Pathway To Hegemony,” Testimony to the US House of Representatives, May 17, 2018, docs.house.gov. 10 Fanell (2018), p. 13. 11 He has obliquely implied that his vision for national rejuvenation by 2035 would include reunification with Taiwan. Others suggest that the country’s second centenary of 2049 is the likely deadline, or the 100th anniversary of the People’s Liberation Army. 12 The US was a major supplier of oil to Japan, and in 1941 it froze Japan's assets in the US and shut down all oil exports, in response to Japan's military incursion into China in the Second Sino-Japanese War of 1937-45. Please see Anderson, Irvine H. Jr. (1975), "The 1941 De Facto Embargo on Oil to Japan: A Bureaucratic Reflex," Pacific Historical Review, 44:2, pp. 201-231. 13 See Jeffrey Becker, “Securing China’s Lifelines Across the Indian Ocean,” China Maritime Report No. 11 (Dec 2020), China Maritime Studies Institute, digital-commons.usnwc.edu. 14 See Rear Admiral Michael McDevitt, “Becoming a Great ‘Maritime Power’: A Chinese Dream,” Center for Naval Analyses (June 2016), cna.org. 15 For discussion see Major Tiffany Werner, “China’s Demographic Disaster: Risk And Opportunity,” 2020, Defense Technical Information Center, discover.dtic.mil.

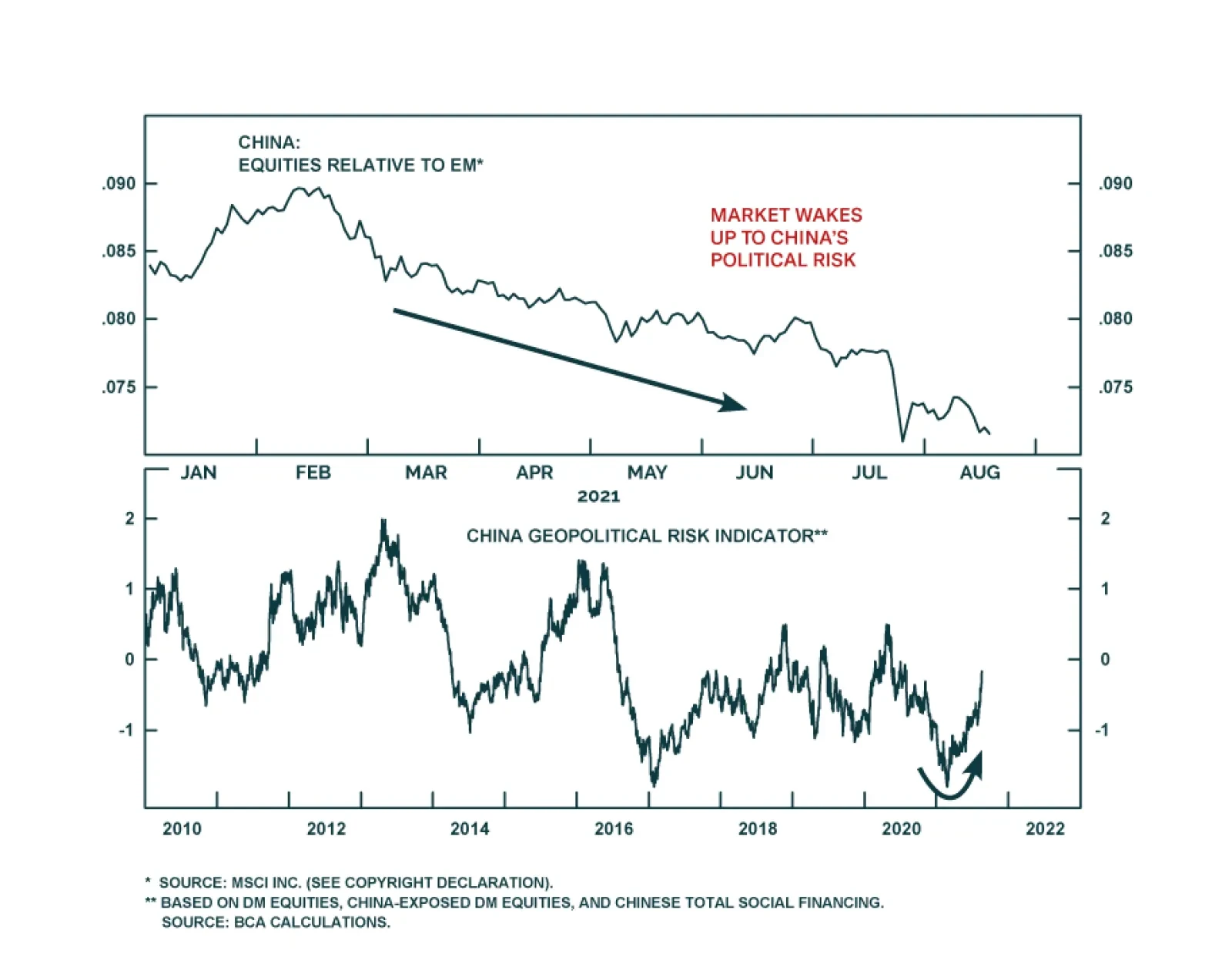

Highlights The decline in the US and UK July services PMIs underscores that pandemic control measures are not the only manner by which COVID-19 impacts the services sector of the economy. A slowdown in Q3 growth in advanced economies from the Delta surge is now all but inevitable. The fact that highly-vaccinated advanced economies have experienced a sharp rise in new cases due to the Delta variant underscores that true herd immunity, as envisioned for most of the pandemic, will likely prove elusive. Consequently, investors need to shift their framework from the idea of herd immunity to that of “NAHRI”: the non-accelerating hospitalization rate of immunity. The vaccination rate is the most obvious indicator of progress towards NAHRI, but immunity from previous infections is also an important contributor. Reasonable estimates of unreported COVID-19 infections suggest that investors have good reason to believe that the US and most other major advanced economies will be above NAHRI, or at least very close to it, at some point in Q4. On a 6-12 month time horizon, economic growth in advanced economies, as well as the trend in financial markets, is not likely to be driven by the Delta variant of COVID-19. Extremely easy monetary policy, pent up savings, and robust revenue growth will support economic growth and the trend in stock prices – despite the fact that analyst earnings expectations are clearly too high. The recent underperformance of China-sensitive assets has been driven by a regulatory crackdown by Chinese authorities on new economy companies, which reflects new socio-political and economic shifts. Chinese stocks are now oversold and could bounce in the near-term, but we would still recommend favoring developed market equities within a global ex-US equity allocation until Chinese policy turns reflationary. Investors should continue to favor stocks versus bonds in a multi-asset portfolio over the coming year, with the proviso that the impact from the Delta variant is likely to cause a near-term growth disappointment. High single-digit earnings growth, coupled with some pressure on multiples, continues to point to mid-single-digit returns from US equities. Within a global equity allocation, we would recommend that investors favor global ex-US stocks, whose outperformance is not dependent on that of EM. Value versus growth, and small caps versus large, will likely benefit from an uptrend in long-maturity bond yields. We recommend that investors favor short USD positions, in response to a likely downtrend in the dollar over the coming year. Feature Chart I-1Meaningful Vaccination Progress Continues Everywhere Except Africa

Meaningful Vaccination Progress Continues Everywhere Except Africa

Meaningful Vaccination Progress Continues Everywhere Except Africa

Over the past month, the Delta variant-driven phase of the pandemic has continued to worsen in several advanced economies, arrayed against a continual improvement in the immunity of the world’s population. Chart I-1 highlights that, outside of Africa, the share of the population that is fully vaccinated against COVID-19 is rising at a robust pace of roughly 10 percentage points per month. But in advanced economies with elevated rates of vaccination compared to the rest of the world, new confirmed cases of COVID-19 accelerated in August, driven in most cases by the Delta variant. Chart I-2 highlights that in the UK, the epicenter of the Delta surge, new cases have begun to rise again after having peaked in late July. UK hospitalizations remain low relative to what has occurred since the onset of the pandemic (panel 2 of Chart I-2), but the US has experienced a more significant rise due to its comparatively low vaccination rate. In addition, reflecting a disparity in vaccination rates within the US that we have highlighted, has a strong political dimension.1 Chart I-3 illustrates that ICU capacity utilization (relative to peak staffed ICU beds) has risen sharply in red states, back above its all-time high. ICU usage in blue states is also rising, but it remains 10 percentage points below its prior peak. Chart I-2UK Hospitalizations Remain Stable, Despite Elevated Case Counts

UK Hospitalizations Remain Stable, Despite Elevated Case Counts

UK Hospitalizations Remain Stable, Despite Elevated Case Counts

Chart I-3Lowly Vaccinated US States Are Suffering The Most From Delta

Lowly Vaccinated US States Are Suffering The Most From Delta

Lowly Vaccinated US States Are Suffering The Most From Delta

When discussing the pandemic and its economic impact in past Bank Credit Analyst reports, we have emphasized the importance of hospitalizations as the core driver of policymaker decisions about pandemic control measures. In turn, we have focused on control measures as an important driver of economic activity because these measures clearly impede households’ ability to consume many services. Chart I-4Surging Cases Impact Services Activity, Even Without Pandemic Control Measures

Surging Cases Impact Services Activity, Even Without Pandemic Control Measures

Surging Cases Impact Services Activity, Even Without Pandemic Control Measures

But Chart I-4 underscores that control measures are not the only manner by which the pandemic impacts the services sector of the economy. The chart highlights that the Markit services PMI has fallen sharply in July and August in both the US and UK economies, two countries that have few or no pandemic control measures still in place. This is strong evidence that fear and general risk aversion among some consumers is affecting services spending. Given that hospitalizations have remained relatively well controlled in the UK, this also suggests that the impact on consumer sentiment is emerging mostly from new case counts rather than from published hospitalization rates. Chart I-5 highlights that the University of Michigan's Index of Consumer Sentiment fell sharply in August to essentially a 10-year low, providing further evidence that a slowdown in Q3 growth in advanced economies from the Delta surge is now all but inevitable. Chart I-6 highlights that this has not yet been reflected in consensus expectations for growth, suggesting that near-term growth disappointments are likely. Chart I-5A Q3 Growth Slowdown Is Now All But Inevitable...

A Q3 Growth Slowdown Is Now All But Inevitable...

A Q3 Growth Slowdown Is Now All But Inevitable...

Chart I-6...Which Is Not Currently Reflected In Consensus Expectations For Growth

...Which Is Not Currently Reflected In Consensus Expectations For Growth

...Which Is Not Currently Reflected In Consensus Expectations For Growth

Shifting Focus From Herd Immunity To NAHRI The fact that highly vaccinated advanced economies have experienced a sharp rise in new cases due to Delta underscores that true herd immunity, as envisioned for most of the pandemic, will likely prove elusive. This point was underscored earlier this month in public comments by the head of the Oxford Vaccine Group,2 who noted that even relatively small rates of transmission from “breakthrough cases” of vaccinated individuals means that anyone who is unvaccinated will likely be exposed to COVID-19 at some point over the coming months or years. From an economic standpoint, this may not be problematic if the spread of the disease among the unvaccinated is slow, as it would allow hospitals time to process COVID patients without risking an overrun of the system (and thus would likely not necessitate a response from policymakers). But the lack of an achievable herd immunity is clearly a risk if community transmission of the Delta variant is high among unvaccinated individuals, even in a scenario where overall vaccination rates are elevated. Consequently, investors need to shift their framework from the idea of herd immunity to that of “NAHRI”: the non-accelerating hospitalization rate of immunity. This concept is borrowed from the idea of NAIRU (the non-accelerating inflation rate of unemployment), and signifies the point at which sufficient immunity has been reached in a country – either through vaccination or past infection – that results in a stable pace of COVID-19 hospitalizations in the absence of any pandemic control measures or precautionary behavior on the part of consumers. Once NAHRI is reached with no control measures and a pre-pandemic rate of interpersonal contact, the pandemic will be effectively over. Chart I-7The US Vaccination Rate Has Picked Up Modestly

The US Vaccination Rate Has Picked Up Modestly

The US Vaccination Rate Has Picked Up Modestly

One clear difficulty with this perspective is that NAHRI is unknown, making it challenging to determine how close a given economy is to a stable pace of COVID-related hospitalization. The experience of the UK over the past month, with an elevated case count yet stable hospitalizations, may suggest that they are close or approaching a stable-hospitalization immunity rate, although investors will still need to watch the UK closely over the coming weeks to confirm if this is the case. The vaccination rate is the most obvious indicator of progress toward NAHRI, and on this front the US has further to go. Chart I-7 highlights that while the pace of first doses administered in the US has risen over the past two months in response to the Delta wave, it will still take until the end of October or early November for the US to reach levels that have been attained by other advanced economies. The introduction of widespread vaccination mandates, as well as the incentive effects of vaccination passports, might raise this rate over the coming weeks. This is even more likely given the FDA's full approval of the Pfizer/BioNTech vaccine this week. But; immunity from previous infections will also contribute to reaching NAHRI, which raises the question of how many unreported COVID-19 infections have occurred since the onset of the pandemic. This is especially important given recent evidence that a previous COVID-19 infection among those who are unvaccinated appears to provide as much protection against the Delta variant as double-dose vaccination does for those without a previous infection (Chart I-8). Chart I-8A Previous COVID-19 Infection Appears To Offer Strong Protection Against The Delta Variant

September 2021

September 2021

In the US, the Center for Disease Control estimates that from February 2020 to May 2021 only 1 in 4.2 COVID-19 infections were reported, suggesting that there were approximately 120 million total infections during that period. That would be quite positive for the economic outlook if accurate, as it would imply that the true immunity rate in the US is probably much closer to NAHRI than the vaccination rate would imply. However, it is also possible that the Center's estimate is too high, which is what some surveys of Americans seem to suggest. In mid-to-late February, a Pew Research survey reported that 25% of US adults had either tested positive for COVID-19, tested positive for antibodies against the SARS-COV-2 virus, or were confident that they already contracted the virus. This compares with 8.5% of the US population with a confirmed case of COVID-19 at that time, suggesting that the true ratio of reported cases to total infections is closer to 1:3. Chart I-9 highlights what the true US immunity rate might look like compared with the published vaccination rate based on different estimates of unreported infections. The chart highlights that a 1:3 ratio of reported cases to total infections implies an additional 10 percentage points of immunity, which would bring US first-dose vaccination rates in line with those of other DM countries. When combined with a slow but still ongoing rise in first doses administered, as well as emergency use eligibility of children under 12 years old targeted by the end of September, investors have good reason to believe that the US and most other major advanced economies will be above NAHRI, or at least very close to it, at some point in Q4. Chart I-9The True US Immunity Rate May Be A Lot Higher Than The Vaccination Rate Would Suggest

September 2021

September 2021

A Permanent Shift In Consumer Behavior? The inability to reach true herd immunity, combined with the recent slowdown in services activity in response to a surge in cases from the Delta variant, raises the issue of whether altered consumer behavior will persist beyond the next few months. Chart I-10A Positive Sign That The Delta Wave May Be Abating

A Positive Sign That The Delta Wave May Be Abating

A Positive Sign That The Delta Wave May Be Abating

In our view, the answer is: probably not. First, Chart I-10 makes the simple point that the transmission rate is already falling in advanced economies, suggesting that fears of a complete explosion in new cases beyond previous highs are unfounded. Second, the behavior of consumers over the past two months has been reasonable, but is unlikely to continue once nations begin to approach NAHRI. The Delta variant is still relatively new, and its higher transmissibility, as well as its seemingly higher hospitalization rate for those who are unvaccinated, has understandably given some consumers pause over the past few months (even those who are vaccinated). This is likely especially true among adults with young children in their household, given that they are not currently able to receive a vaccine and given a significant rise in pediatric cases that has occurred in some countries. But the reality is that the world will have to live with the existence of COVID-19 permanently, which consumers, investors, and policymakers will all soon come to accept and normalize. It will become endemic, and receiving annual booster shots against the disease may become a permanent ritual for people around the world. In advanced economies, once most or all individuals who wish to be vaccinated have had the chance to receive their shot, it seems unlikely that periodic waves of rising cases among the unvaccinated will be seen as a threat to individual health, especially if the increase in hospitalizations is limited and the viability of the health care system is not under threat. Beyond Delta: The Economy And Financial Markets In A Year’s Time On a 6-12 month time horizon, economic growth in advanced economies, as well as the trend in financial markets, is not likely to be driven by the Delta variant of COVID-19. Instead, the cyclical investment outlook will continue to depend on the factors that we have discussed in several previous reports: Extremely Easy Monetary Policy: Chart I-11 illustrates the 10-year US Treasury yield relative to trend nominal GDP growth. The chart highlights that long-maturity US government bond yields have not been this low relative to trend growth since the late-1970s, which will continue to support domestic demand even if growth moderates over the coming year. Excess Savings: A waning growth impulse from fiscal policy will likely weigh on real goods spending, which is roughly 10 percent higher than its pre-pandemic trend (Chart I-12). But services spending, which accounts for about 70% of overall consumer spending, is still 5% below its pre-COVID trend and will be supported by the deployment of a significant amount of excess savings that have accumulated over the course of the pandemic. Some of these excess savings have probably been deployed to pay down debt, but a sizeable portion likely remains to support services spending. Chart I-13 highlights that the gap in spending is fairly broad-based across different services categories, underscoring that a recovery in services spending is not overly-dependent on the return of a particular type of consumer spending behavior. Chart I-11US Monetary Policy Is Extraordinarily Easy

US Monetary Policy Is Extraordinarily Easy

US Monetary Policy Is Extraordinarily Easy

Chart I-12Pent-Up Savings Will Support Services Spending

Pent-Up Savings Will Support Services Spending

Pent-Up Savings Will Support Services Spending

Robust Revenue Growth: The equity market is likely to be supported by strong revenue growth over the coming year, even if it modestly disappoints current expectations. Chart I-14 presents bottom-up analysts’ expectations for S&P 500 sales per share growth over the coming year, alongside a proxy for nominal growth expectations (12-month forward expectations for real GDP growth plus 2 percentage points). The chart highlights that, while expectations for sales growth are modestly above what our proxy would suggest, nominal growth expectations are the strongest they have been in over a decade. Chart I-13Missing Services Spending Is Broad- Based Across Spending Categories

September 2021

September 2021

Chart I-14S&P 500 Revenue Growth Is Likely To Be Strong Over The Coming Year...

S&P 500 Revenue Growth Is Likely To Be Strong Over The Coming Year...

S&P 500 Revenue Growth Is Likely To Be Strong Over The Coming Year...

On the latter point, while revenue growth will likely support the equity market, expectations for earnings are now clearly too high. Chart I-15 highlights that bottom-up analysts are calling for 18% earnings growth over the coming year – after what has already been a very impressive earnings recovery – and for profit margins to expand by a full percentage point from what is already a new high. Chart I-16 presents a long-term perspective on corporate profit margins, highlighting how stretched they have become even relative to the uptrend of the past three decades. Chart I-15...Even Though Earnings Expectations Are Clearly Too High

...Even Though Earnings Expectations Are Clearly Too High

...Even Though Earnings Expectations Are Clearly Too High

Chart I-16US Profit Margins Are Very Elevated, Even Given The Past Three Decade's Uptrend

US Profit Margins Are Very Elevated, Even Given The Past Three Decade's Uptrend

US Profit Margins Are Very Elevated, Even Given The Past Three Decade's Uptrend

Chart I-17 highlights that earnings expectations usually disappoint, given the perennial optimism of bottom-up analyst expectations. The chart shows that they historically disappoint on the order of 5 percentage points, but that a 10 percentage point miss would not be so uncommon. Thus, EPS growth that is in line with the revenue growth proxy shown in Chart I-14 will not likely weigh on investor sentiment. China And EM Stocks As a final point about the macro and cyclical investment outlook, Chart I-18 highlights that our Market-Based China Growth Indicator has fallen below the boom/bust line for the first time since the middle of last year. We highlighted in last month’s report that China would not likely provide the global economy with a growth impulse until Chinese policy turns reflationary, and financial assets that are sensitive to Chinese economic growth are now flashing a warning sign. We therefore continue to believe that a normalization in services spending in advanced economies remains the likely impulse for global growth over the coming year. Chart I-17A 10% Earnings Miss Over The Coming Year Would Not Be Unprecedented

A 10% Earnings Miss Over The Coming Year Would Not Be Unprecedented

A 10% Earnings Miss Over The Coming Year Would Not Be Unprecedented

Chart I-18Chinese Growth Proxies Are Performing Poorly

Chinese Growth Proxies Are Performing Poorly

Chinese Growth Proxies Are Performing Poorly

However, at least a part of the recent underperformance of China-sensitive assets has been driven by the spectacular underperformance of broadly-defined tech stocks in China since late-May (Chart I-19). The selloff in Chinese tech stocks has been triggered by a regulatory crackdown by Chinese authorities on new economy companies, which reflects new socio-political and economic shifts in China – which are thus not likely to be transitory. Still, Chinese stocks are now oversold even in absolute terms (Chart I-20), raising the question of whether EM stocks overall are due for a bounce. Chart I-19Some Of The Recent EM Underperformance Reflects The Chinese Regulatory Crackdown

Some Of The Recent EM Underperformance Reflects The Chinese Regulatory Crackdown

Some Of The Recent EM Underperformance Reflects The Chinese Regulatory Crackdown

Chart I-20Chinese Stocks Are Oversold In Absolute Terms

Chinese Stocks Are Oversold In Absolute Terms

Chinese Stocks Are Oversold In Absolute Terms

In the short term, the answer is yes, but over a 6-12 month time horizon we would still recommend favoring developed market equities within a global ex-US equity allocation. First, while policy from China may eventually act as a catalyst for EM equities, BCA’s China strategists do not believe that Chinese policymakers have yet reached the “pain point” that would signal regulatory and monetary policy easing. Second, China and EM more generally is comparatively tech heavy, and thus will face headwinds on a relative basis if value outperforms growth over the coming year (as we expect). Chart I-21EM Stocks Do Not Offer A Compelling Value Catalyst Versus DM Ex-US

EM Stocks Do Not Offer A Compelling Value Catalyst Versus DM Ex-US

EM Stocks Do Not Offer A Compelling Value Catalyst Versus DM Ex-US

Third, Chart I-21 highlights that EM stocks offer no compelling value proposition relative to DM ex-US equities. EM stocks are modestly cheap on a 12-month forward P/E basis (trading at a 13% discount), but this has been true historically – with the exception of a brief period from mid-2007 to mid-2008. Relative to the past decade, EM valuation is at roughly average levels versus global ex-US stocks, suggesting that Chinese policy and sector performance trends are likely to be the key drivers for EM performance relative to non-US equities. Investment Conclusions Chart I-22Favor DM Ex-US Vs. US, And Value Vs. Growth, Over The Coming Year

Favor DM Ex-US Vs. US, And Value Vs. Growth, Over The Coming Year

Favor DM Ex-US Vs. US, And Value Vs. Growth, Over The Coming Year

In Section 2 of this month’s report, we explain why the Fed’s maximum employment criterion is likely to be reached earlier than investors and the Fed itself expects. This suggests that equity multiples may come under pressure over the coming year as long-maturity government bond yields rise. However, we noted above that earnings are likely to grow at a high single-digit pace, and that this is likely to support the uptrend in US stock prices as developed economies approach or surpass the non-accelerating hospitalization rate of immunity from COVID-19 and the world continues to move toward to a post-pandemic state. In combination with our expectation of rising government bond yields, investors should thus continue to favor stocks versus bonds in a multi-asset portfolio over the coming year, with the proviso that the impact from Delta is likely to cause a near-term growth disappointment. On a 12-month time horizon, high single-digit earnings growth coupled with some pressure on multiples continues to point to mid-single-digit returns from US equities. Within a global equity allocation, we would recommend that investors favor global ex-US stocks. The outperformance of the latter is not dependent on the outperformance of emerging markets, as Chart I-22 highlights that DM ex-US equities now trade at close to a 30% discount relative to their US counterparts – an extreme reading that partially reflects the extraordinary discount of global value versus growth stocks (panel 2). The trend in value versus growth is strongly correlated with the trend in financials versus broadly-defined technology stocks, and rising long-maturity bond yields favor the earnings of the former and weigh on the multiples of latter. Chart I-23 highlights that global small cap stocks may also outperform over the coming year, given their fairly strong correlation with long-maturity bond yields since the start of the pandemic. Finally, as we have noted in previous reports, the US dollar is a reliably counter-cyclical currency over 12-month periods. The recent bounce in the US dollar in the face of rising stock prices has deviated from this relationship, but only modestly so (Chart I-24). A similar deviation occurred in Q1 of this year, and was resolved with the dollar, not stock prices, moving lower. Consequently, we recommend that investors favor short USD positions, in response to a likely downtrend in the dollar over the coming year. Chart I-23Small Cap Stocks Will Likely Outperform If Long-Maturity Bond Yields Rise

Small Cap Stocks Will Likely Outperform If Long-Maturity Bond Yields Rise

Small Cap Stocks Will Likely Outperform If Long-Maturity Bond Yields Rise

Chart I-24A Pro-Risk Investment Stance Argues For A Dollar Downtrend

A Pro-Risk Investment Stance Argues For A Dollar Downtrend

A Pro-Risk Investment Stance Argues For A Dollar Downtrend

Jonathan LaBerge, CFA Vice President The Bank Credit Analyst August 26, 2021 Next Report: September 30, 2021 II. The Return To Maximum Employment: It May Be Faster Than You Think When defining maximum employment, many investors focus on the state of the labor market that prevailed as of February 2020. However, the US labor market was beyond maximum employment levels at the onset of the COVID-19 pandemic, suggesting that the Fed is likely to raise interest rates before the unemployment rate falls back to 3.5%. This assumes that the Fed deems the ongoing recovery in the labor market to be “broad-based and inclusive,” given revisions to the FOMC’s Statement on Longer-Run Goals and Monetary Policy Strategy last August. The extraordinary nature of the COVID-19 pandemic has indeed had an outsized impact on some demographic segments of the labor market, but most of these effects already have or are likely to be reversed as the overall unemployment rate continues to fall. A permanent decline in the participation rate, relative to pre-pandemic levels, is likely given ongoing demographic trends. Even if the recent behavioral impact of retirements is overdone, the demographic impact of retirement on the participation rate suggests that the Federal Reserve may hit its maximum employment objective by next summer, barring a long-lasting impact on US economic activity from the Delta variant of COVID-19. In a 2H 2022 rate hike scenario, the fair value of the 10-year Treasury yield will be 2.2%-2.3% next year, which the market is not priced for. This underscores that investors should maintain a short duration position within a fixed-income portfolio, and that equity investors should favor value over growth stocks on a 12-month time horizon. The cyclical outlook for monetary policy in the US rests heavily, if not exclusively, on the length of time needed to return to maximum employment. In this report, we argue that a complete return to the state of the labor market as of February 2020 is probably not required for the Fed’s maximum employment objective to be met, because the jobs market was likely beyond maximum employment at that time. In addition, we highlight that the broad-based and inclusive nature of the Fed's maximum employment objective is objective will not delay the first Fed rate hike beyond what the trajectory of the unemployment rate would suggest, as the odds of a persistent negative impact on demographic segments of the labor market no longer seem meaningful. In fact, the one partial exception that we can identify – retirement – argues for an earlier return to maximum employment. We conclude by noting that a first Fed rate hike is possible by the middle of next year, barring a long-lasting impact on US economic activity from the Delta variant of COVID-19 or if the Fed’s inflation liftoff criteria are no longer met. Normalized levels of inflation expectations, as well as reasonable estimates of a closed output gap over the coming year, suggest that inflation itself will remain liftoff-consistent barring a significant shock to growth or a major disinflationary/deflationary supply-side event. A 2022 rate hike is not currently reflected in market pricing, underscoring that investors should remain short duration within a fixed-income portfolio. Equity investors should expect a meaningful rise in stock market volatility as long-maturity yields rise over the coming year, and should favor value over growth stocks once fears of the likely impact of the Delta variant on near-term economic growth abate. Defining “Maximum Employment” Chart II-1Last Cycle, Rates Began To Rise Before Maximum Employment Was Reached

Last Cycle, Rates Began To Rise Before Maximum Employment Was Reached

Last Cycle, Rates Began To Rise Before Maximum Employment Was Reached

Last September, the Fed’s official shift to an average inflation targeting regime represented a significant break from how the Fed conducted monetary policy in the past. The shift replaced what was previously a “symmetric” 2% inflation target with the goal of achieving inflation that averages 2% over time, meaning that monetary policy is no longer strictly forward-looking. According to the Fed's previous framework, monetary policy should start to tighten before the economy reaches its full employment level, in anticipation that further declines in the unemployment rate will likely lead to accelerating inflation. For example, during the last economic cycle, the Fed began to raise interest rates in December 2015, when the unemployment rate stood at 5% (Chart II-1). But the Fed's new regime implies that the onset of tightening should begin later, the criteria for which was explicitly laid out in the September 2020 FOMC statement: “The Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and expects it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee's assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.” In addition, while the Fed’s statutory mandate from Congress has always included the pursuit of maximum employment as an objective of monetary policy, revisions to the FOMC’s Statement on Longer-Run Goals and Monetary Policy Strategy last August explicitly noted that the maximum level of employment is a “broad-based and inclusive goal.” This has left many investors questioning when the Fed’s maximum employment criterion will be reached, with some market participants believing that a complete return to the state of the labor market that prevailed as of February 2020 will be required before the Fed lifts interest rates. But there are three arguments suggesting that the US labor market was beyond maximum employment levels at the onset of the COVID-19 pandemic: 1. Chart II-2 highlights that the February 2020 unemployment rate ranked at the 5th percentile of its post-WWII history, and was at its lowest level since the late-1960s. While it is true that the unemployment rate would have been higher for most of the last economic expansion based on December 2007 age-adjusted participation rates, Chart II-3 highlights that this effect had waned by the end of 2019. This underscores that the pre-pandemic unemployment rate likely reflected very low labor market slack. Chart II-2The US Labor Market Was Likely Beyond Maximum Employment Levels Prior To The Pandemic

September 2021

September 2021

2. The February 2020 unemployment rate stood at 3.5%, which is at the very low end of the Fed’s NAIRU estimates, and meaningfully below the CBO’S long- and short-term NAIRU projections (Chart II-4). Given that NAIRU estimates signify the level of unemployment that is consistent with a steady inflation rate, this implies that 3.5% is likely below the “maximum employment” unemployment rate. Chart II-3The Part Rate Had Mostly Normalized Just Prior To COVID-19

The Part Rate Had Mostly Normalized Just Prior To COVID-19

The Part Rate Had Mostly Normalized Just Prior To COVID-19

Chart II-4A 3.5% Unemployment Rate Is Likely Below NAIRU

A 3.5% Unemployment Rate Is Likely Below NAIRU

A 3.5% Unemployment Rate Is Likely Below NAIRU

Chart II-5Wage Growth Accelerated In Response To A Sub-4% Unemployment Rate

Wage Growth Accelerated In Response To A Sub 4% Unemployment Rate

Wage Growth Accelerated In Response To A Sub 4% Unemployment Rate

3. The pre-pandemic trend in wage growth also supports the notion that the labor market was past maximum employment levels at that time. Chart II-5 highlights that average hourly earnings and the Atlanta Fed’s median wage growth tracker were both accelerating in 2018/2019, and Chart II-6 highlights that real average hourly earnings growth of production and nonsupervisory employees was close to its 90th percentile historically at the end of 2019. This underscores that the Fed is likely to raise interest rates before the unemployment rate falls back to 3.5%, assuming that the ongoing recovery in the labor market is deemed by the Fed to be “broad-based and inclusive.” Chart II-6Real Average Hourly Earnings Growth Was At Its 90th Percentile Historically Prior To COVID-19

September 2021

September 2021

Breadth, Inclusivity, And Participation Chart II-7The "She-cession" Is Over

The "She-cession" Is Over

The "She-cession" Is Over

The extraordinary nature of the COVID-19 pandemic has indeed had an outsized impact on some demographic segments of the labor market, but most of these effects have already reversed or are likely to as the overall unemployment rate continues to fall. And as we highlight below, the one partial exception that we can identify – retirement – in fact argues for an earlier return to maximum employment. We focus our demographic segment analysis on four main categories: 1. employment by gender; 2. race; 3. wage level and education; and 4. the impact on labor force participation from retirement. Gender Chart II-7 highlights the impact of the pandemic on the US labor market by gender. In 2020, the impact of the pandemic fell disproportionately on women. The unemployment rate rose close to 13 percentage points for women from February to April of last year, versus a 10 percentage point rise for men. In addition, the recovery in the participation rate last year was less robust for women, who disproportionately cited family responsibilities as the basis for not participating in the labor force. However, Chart II-7 also highlights that the disproportionate labor market impact of the pandemic on women is now over, with the female unemployment rate closer to its pre-pandemic level than for men, with a similar recovery in the participation rate. The difference in wage growth, relative to February 2020 levels, is also now smaller for women than for men. Thus, barring the development of a new divergence over the coming year, there is no longer any basis for the Federal Reserve to distinguish between men and women in the labor market recovery. Chart II-8Black Unemployment And Labor Force Participation Has Mostly Normalized

Black Unemployment And Labor Force Participation Has Mostly Normalized

Black Unemployment And Labor Force Participation Has Mostly Normalized

Race Chart II-8 highlights the impact of the pandemic on the US labor market by race. In this case, it is clear that a disproportionately negative effect on Black employment persisted for longer than it did for women. But it is also clear that the Black unemployment rate is now roughly the same magnitude above its February 2020 level as is the case for the overall unemployment rate. In June, the Black labor force participation rate had actually recovered more than the overall participation rate, although it did decline meaningfully in July. The Black labor force participation rate has shown itself to be highly volatile since the onset of the pandemic, and we doubt that the July reading marks a decoupling from the overall participation rate. It is also true that median non-white wage growth has decelerated significantly more than median white wage growth during the pandemic, but this has occurred from a very elevated starting point. Median non-white wage growth was growing a full percentage point above median white wage growth just prior to the pandemic, compared with a half a percentage point below today. This deceleration has likely occurred as a lagged impact from the larger rise in Black unemployment noted above, which has now dissipated – suggesting that nonwhite wage growth is not likely to meaningfully lag over the coming year. Two additional points highlight that Black unemployment, labor force participation, and wages are likely to be highly correlated with overall labor market trends over the coming year. First, Chart II-9 highlights that in 2019 Black workers were underrepresented in management / professional and natural resources / construction / maintenance occupations, and overrepresented in service and production / transportation / material moving occupations. Given that services spending remains below its pre-pandemic trend, it is likely that the Black unemployment rate will continue to decline as the gap in leisure and hospitality and other services employment closes further relative to pre-pandemic levels. Chart II-9Black Unemployment Will Fall As Services Spending Recovers

September 2021

September 2021

Second, Table II-1 highlights that Black survey respondents to the Census Bureau’s Household Pulse Survey located in New York and California are reporting lower and only modestly higher levels, respectively, of lost employment income than is the case for Black workers in the US overall. Given that services employment in these two states, particularly New York, are the most likely to be negatively impacted by persistent “work-from-home” effects, Table II-1 suggests that Black services employment is not likely to lag gains in overall services employment. Wage Level And Education Chart II-10 highlights wage growth for those with a high school diploma or less, for low-skilled workers, and for those in the lowest average wage quartile, and Charts II-11A & II-11B highlight the impact of the pandemic on the unemployment and participation rates by education. Table II-1No Evidence Of A Negative “Work-From- Home” Effect On Black Unemployment

September 2021

September 2021

Chart II-10Wage Growth By Education And Skill Level Is Largely Unchanged

Wage Growth By Education And Skill Level Is Largely Unchanged

Wage Growth By Education And Skill Level Is Largely Unchanged

Chart II-11AThe Least Educated Workers Still Need To See More Job Gains…

The Least Educated Workers Still Need To See More Job Gains...

The Least Educated Workers Still Need To See More Job Gains...

Chart II-11B…But This Will Occur As Services Spending Improves

...But This Will Occur As Services Spending Improves

...But This Will Occur As Services Spending Improves

On the wage front, Chart II-10 makes it clear that there are no major negative differences between those with limited education, limited skills, or limited pay and the overall trend in wage growth relative to pre-pandemic levels. Reflecting a shortage of workers in some services industries, wages for 1st quartile wage earners and low-skilled workers are accelerating, and are poised to reach their highest level since 2008. On the employment and participation front, Charts II-11A & B show that the job market recovery has been less pronounced for high school graduates and those with less than a high school diploma. But, we believe – with high conviction – that this reflects the industry composition of the existing employment gap, which skews heavily towards service and leisure & hospitality. These jobs tend to require less formal education and training, and to offer less pay. Given this, and similar to the case for Black employment, low education employment growth is unlikely to meaningfully diverge from the trend in overall services employment over the coming year. The Impact Of Retirement On Labor Force Participation Chart II-12Most Of The Pandemic Decline In Labor Force Participation Has Occurred Due To Retirement

...But This Will Occur As Services Spending Improves

...But This Will Occur As Services Spending Improves

Chart II-12 presents a breakdown of the change in overall labor force participation from Q4 2019 to Q2 2021 by nonparticipation category. The chart is based off the Atlanta Fed’s Labor Force Participation Dynamics dataset, and employs some Bank Credit Analyst estimates to seasonally adjust the impact of some categories in the first half of this year and to align it with the actual change in the published monthly seasonally-adjusted participation rate. The chart underscores that, while family responsibilities and those who are not in the labor force but who want a job (the shadow labor force) have been important contributors to the decline in labor force participation since the onset of the pandemic, retirement has been the single most important factor driving the participation rate lower. This sharp drop in labor force participation from retirement likely reflects the decision of some older workers to bring forward their retirement date by a year or two, although a recent study from the Kansas City Fed suggests that the non-demographic component of the recent surge in retirements has mainly been driven by a decline in the number of retirees rejoining the labor force.3 But demographic effects are important, and Chart II-13 highlights that the participation rate has fallen at a rate of roughly 30 basis points per year on average since 2008, reflecting the aging of the population. Chart II-13 is consistent with the age-adjusted participation rate that we showed in Chart II-3 above, and underscores that, even though the recent decline in the participation rate due to retirement is overdone, a permanent decline relative to pre-pandemic levels is likely the result of ongoing demographic trends. In our view, the Federal Reserve is unlikely to regard a demographically-driven decline in the overall participation rate as evidence that the labor market recovery has fallen short of the Fed’s maximum employment objective. It is possible that a return of the working age participation rate to its pre-pandemic level will be viewed as a condition for maximum employment, but Chart II-14 highlights that progress on this front is already more advanced. Chart II-13A Full Recovery To The Pre-Pandemic Labor Force Participation Rate Is Unlikely

A Full Recovery To The Pre-Pandemic Labor Force Participation Rate Is Unlikely

A Full Recovery To The Pre-Pandemic Labor Force Participation Rate Is Unlikely

Chart II-14The Working Age Participation Rate Has Recovered More Than The Overall Part Rate

The Working Age Participation Rate Has Recovered More Than The Overall Part Rate

The Working Age Participation Rate Has Recovered More Than The Overall Part Rate

A lower overall participation rate results in a faster decline in the unemployment rate for any given level of employment growth. Given that there are minimal-to-no remaining labor market divergences along other demographic dimensions of the labor market that aren’t simply correlated with the overall unemployment rate, the implication of a permanently lower participation rate is that the Federal Reserve is likely to hit its maximum employment objective earlier than market participants, and the Fed itself, are currently expecting. Timing The Return To Maximum Employment, And The First Fed Rate Hike Table II-2 presents the average monthly nonfarm payroll growth that will be required to reach a 3.8% unemployment rate, a level that Fed Vice Chair Richard Clarida recently affirmed would in his view likely constitute maximum employment.4 The values shown in the table assume the trend participation rate shown in Chart II-13 above, as well as a recent average of monthly population growth. Table II-2The Return To Maximum Employment May Be Faster Than You Think

September 2021

September 2021

The table highlights that the unemployment rate is likely to fall to 3.8% following the creation of roughly 4.3 million additional jobs. If the monthly change in nonfarm payrolls continues to grow at its average over the past 3 months, this threshold will be met in January 2022 – essentially a full year before the Fed and market participants expect interest rates to begin to rise. Based instead on a simple linear trend of nonfarm payrolls since late last year, the unemployment rate is likely to fall to 3.8% by sometime next summer. As we highlighted above, the Fed has been explicit that its conditions for raising the funds rate are the following: Labor market conditions have reached levels consistent with the Committee's assessments of maximum employment Inflation has risen to 2 percent Inflation is on track to moderately exceed 2 percent for some time. Currently, the second and third conditions for liftoff are present, suggesting that a first rate hike is possible by the middle of next year, barring a long-lasting impact on US economic activity from the Delta variant of COVID-19. We agree that inflation will slow significantly from its current pace over the coming year as pandemic-induced supply-side factors wane, which some investors have noted may put the Fed’s inflation criteria back into play. But we doubt that the Fed will narrowly focus on the year-over-year growth rate in the core PCE deflator – which will be strongly influenced by base effects next year from this year’s comparatively elevated price level – when judging its second and third liftoff criteria. Instead, the Fed is likely to focus on the prevailing “run rate” of inflation that excludes prices experiencing any disinflationary effects of supply-chain normalization. Chart II-15 illustrates one important reason that the Fed’s inflation criteria will remain “checked” over the coming year. The chart shows that the pandemic, especially last year’s fiscal response to it, has “normalized” important measures of inflation expectations (based on an interval of 2004 to today). We noted in a report earlier this year that inflation is determined by both the degree of economic slack and inflation expectations, a framework that the Fed and many economists refer to as the “modern-day Phillips Curve.”5 Chart II-15The Fed’s Inflation Liftoff Criteria Are Likely To Stay “Checked”

The Fed's Inflation Liftoff Criterion Are Likely To Stay "Checked"

The Fed's Inflation Liftoff Criterion Are Likely To Stay "Checked"

Many investors feel that the Phillips Curve has failed to predict weak inflation over the past decade, but we noted in our report that this perception is due to a singular focus on the economic slack component of the modern-day version of the curve – to the exclusion of inflation expectations – and a failure to consider the lasting impact of sustained periods of a negative output gap on those expectations. Chart II-16A Closed Output Gap Will Support Liftoff-Consistent Inflation

A Closed Output Gap Will Support Liftoff-Consistent Inflation

A Closed Output Gap Will Support Liftoff-Consistent Inflation

Chart II-16 highlights that both market and Fed economic projections imply a positive output gap within the next 12 months, suggesting that inflation itself will remain liftoff-consistent barring a significant shock to growth or a major disinflationary/deflationary supply-side event. Declines in the prices of goods that have surged as a result of the disruption of global supply chains could potentially lower inflation expectations over the coming year, but our sense is that this is only likely in a scenario in which the prices of these goods fall below their pre-pandemic levels (which we do not currently expect). Investment Implications There are three key investment implications of a potentially faster return to maximum employment than is currently anticipated by investors and the Fed. First, Chart II-17 highlights that the market is not priced for a first Fed rate hike by next summer, and Table II-3 highlights that a sizeable majority of respondents to the New York Fed’s Survey of Primary Dealers do not expect a single rate hike in 2022. Chart II-18 highlights that the fair value of the 10-year Treasury yield a year from today is 2.2%-2.3% in a 2H 2022 rate hike scenario, underscoring that a short duration stance is warranted within a fixed-income portfolio over the coming year – barring a long-lasting impact on economic activity from the Delta variant of COVID-19. Chart II-17The Market Is Not Fully Priced For A Quick Return To Maximum Employment

The Market Is Not Fully Priced For A Quick Return To Maximum Employment

The Market Is Not Fully Priced For A Quick Return To Maximum Employment

Table II-3Market Participant Surveys Show No Hike Expectations Next Year

September 2021

September 2021

Chart II-18Investors Should Maintain A Short-Duration Fixed-Income Stance

Investors Should Maintain A Short-Duration Fixed-Income Stance

Investors Should Maintain A Short-Duration Fixed-Income Stance

Second, while a 2.2%-2.3% 10-year Treasury yield would not necessarily be negative for stock prices on a sustained basis, Chart II-19 shows that it would bring the equity risk premium (ERP) within its 2002-2007 range. The level of the 10-year yield that is consistent with that range has fallen relative to pre-pandemic levels and is now clearly below the trend rate of economic growth, due to a significant run-up in equity market multiples. This underscores that stocks are the most dependent on T.I.N.A., “There Is No Alternative,” than at any other point since the global financial crisis. It is unclear what ERP investors will require to contend with the myriad risks to the longer-term economic outlook, many of which are political or geopolitical in nature and which did not exist in the early 2000s. Chart II-19Now, Stocks Are Increasingly Dependent On Low Bond Yields