Emerging Markets

Highlights Three distinct forces are likely to make South Asia’s geopolitical risks increasingly relevant to global investors. First, India’s tensions with China stem from China’s growing foreign policy assertiveness and India’s shift away from traditional neutrality toward aligning with the US and its allies. This creates a security dilemma in South Asia, just as in East Asia. Second, India’s economy is sputtering in the wake of the COVID-19 pandemic, adding fuel to nationalism and populism in advance of a series of important elections. India will stimulate the economy but it could also become more reactive on the international scene. Third, the US is withdrawing from Afghanistan and negotiating a deal with Iran in an effort to reduce the US military presence in the Middle East and South Asia. This will create a scramble for influence across both regions and a power vacuum in Afghanistan that is highly likely to yield negative surprises for India and its neighbors. Traditionally geopolitical risks in South Asia have a limited impact on markets. India’s growth slowdown and forthcoming fiscal stimulus are more relevant for investors. However, a sharp rise in geopolitical risk would undermine India’s structural advantages as the West diversifies away from China. Stay short Indian banks. Feature Geopolitical risks in South Asia are slowly but surely rising. India-Pakistan and China-India are well-known “conflict-dyads” or pairings. Historically, these two sets have been fighting each other over their fuzzy Himalayan border with limited global financial market consequences. But now fundamental changes are afoot that are altering the geopolitical setting in the region. Specifically, the coming together of three distinct forces could trigger a significant geopolitical event in South Asia. The three forces are as follow: Force #1: Sino-Indian Tensions Get Real About a year ago, Indian and Chinese troops clashed in Ladakh, a disputed territory in the Kashmir region. Following these clashes China reduced its military presence in the Pangong Tso area but its presence in some neighboring areas remains meaningful. Besides the troop build-up along India’s eastern border, China is building more air combat infrastructure in its India-facing western theatre. China’s major air bases have historically been concentrated in China’s eastern region, away from the Indian border (Map 1). Consequently, India has historically enjoyed an advantage in airpower. But China appears to be working to mitigate this disadvantage. Map 1Most Of China’s Major Aviation Units Are Located Away From India

South Asia: A Slowdown And A Showdown

South Asia: A Slowdown And A Showdown

Owing to China’s increased military focus along the Sino-India border, India’s threat perception of China has undergone a fundamental change in recent years. Notably, India has diverted some of its key army units away from its western Indo-Pak border towards its eastern border with China. India could now have nearly 200,000 troops deployed along its border with China, which would mark a 40% increase from last year.1 Turning attention to the Indo-Pak border, India’s problems with Pakistan appear under control for now. This is owing to the ceasefire agreement that was renewed by the two countries in February 2021. However, this peace cannot possibly be expected to last. This is mainly because core problems between the two countries (like Pakistan’s support of militant proxies and India’s control over Kashmir) remain unaddressed. History too suggests that bouts of peace between the two warring neighbors rarely last long. These bouts usually end abruptly when a terrorist attack takes place in India. With both political turbulence and economic distress in Pakistan rising, the fragile ceasefire between India and Pakistan could be upended over the next six months. In fact, two events over the last week point to the fragility of the ceasefire: Two drones carrying explosives entered an Indian air force station located in Jammu and Kashmir (i.e. a northern territory that India recently reorganized, to Pakistan’s chagrin). Even as no casualties were reported, this attack marks a turning point for terrorist activity in India as this was the first-time terrorists used drones to enter an Indian military base. Hours later, another drone attack struck an Indian base at the Ratnuchak-Kaluchak army station, the site of a major terrorist attack in 2002. Chart 1China, Pakistan And India Cumulatively Added 41 Nuclear Warheads Over 2020

South Asia: A Slowdown And A Showdown

South Asia: A Slowdown And A Showdown

Given that the ceasefire was agreed recently, any further increase in terrorist activity in India over the next six months would suggest that a more substantial breakdown in relations is nigh. Distinct from these recent tensions, China’s troop deployment along India’s eastern arm and Pakistan’s presence along India’s western arm creates a strategic “pincer” that increasingly threatens India. India is naturally concerned. China and Pakistan are allies who have been working closely on projects including the strategic China-Pakistan Economic Corridor (CPEC). The CPEC is a collection of infrastructure projects in Pakistan that includes the development of a port in Gwadar where a future presence of the People's Liberation Army Navy (PLAN) is envisaged. Gwadar has the potential of providing China land-based access to the Indian Ocean. Trust in the South Asian region is clearly running low. Distinct from troop build-ups and drone-attacks, China, Pakistan, and India cumulatively added more than 40 nuclear warheads over the last year (Chart 1). China is reputed to be engaged in an even larger increase in its nuclear arsenal than the data show.2 From a structural perspective, too, geopolitical risks in the South Asian peninsula are bound to keep rising. When it comes to the conflicting Indo-Pak dyad, India’s geopolitical power has been rising relative to that of Pakistan in the 2000s. However, the geopolitical muscle of the Sino-Pak alliance is much greater than that of India on a standalone basis (Chart 2). Chart 2India Has Aligned With The QUAD To Counter The Sino-Pak Alliance

South Asia: A Slowdown And A Showdown

South Asia: A Slowdown And A Showdown

China’s active involvement in South Asia is responsible for driving India’s increasing desire to abandon its historical foreign policy stance of non-alignment. India’s membership in the Quadrilateral Security Dialogue (also known as the QUAD, whose other members include the US, Japan, and Australia) bears testimony to India’s active effort to develop closer relations with the US and its allies (Chart 2). India’s alignment with the US is deepening China’s and Pakistan’s distrust of India. Conventional and nuclear military deterrence should prevent full-scale war. But the regional balance is increasingly fluid which means geopolitical risks will slowly but surely rise in South Asia over the coming year and years. Force #2: A Growth Slowdown Alongside India’s Loaded Election Calendar The pandemic has hit the economies of South Asia particularly hard. South Asia historically maintained higher real GDP growth rates relative to Emerging Markets (EMs). But in 2021, this region’s growth rate is set to be lower than that of EM peers (Chart 3). History is replete with examples of a rise in economic distress triggering geopolitical events. South Asia is characterized by unusually low per capita incomes (Chart 4) and the latest slowdown could exacerbate the risk of both social unrest and geopolitical incidents materialising. Chart 3South Asian Economies Have Been Hit Hard By The Pandemic

South Asia: A Slowdown And A Showdown

South Asia: A Slowdown And A Showdown

Chart 4South Asia Is Characterized By Very Low Per Capita Incomes

South Asia: A Slowdown And A Showdown

South Asia: A Slowdown And A Showdown

To complicate matters a busy state elections calendar is coming up in India. Elections will be due in seven Indian states in 2022. These states account for about 25% of India’s population. State elections due in 2022 will amount to a high-stakes political battle. During state elections in 2021, the ruling Bharatiya Janata Party (BJP) was the incumbent in only one of the five states. In 2022, the BJP is the incumbent party in most of the states that are due for elections, which means it has the advantage but also has a lot to lose, especially in a post-pandemic environment. Elections kick off in the crucial state of Uttar Pradesh next February. Last time this state faced elections Prime Minister Narendra Modi was willing to go to great lengths to boost his popularity ahead of time. Specifically, he upset the nation with a large-scale and unprecedented de-monetization program. Given the busy state election calendar in 2022, we expect the BJP-led central government to focus on policy actions that can improve its support among Indian voters. Two policies in particular are likely to come through: Fiscal Stimulus Measures To Provide Economic Relief: India has refrained from administering a large post-pandemic stimulus thus far. As per budget estimates, the Indian central government’s total expenditure in FY22 is set to increase only by 1% on a year-on-year basis. But the expenditure-side restraint shown by India’s central government could change. With elections and a pandemic (which has now claimed over 400,000 lives in India), the central government could consider a meaningful increase in spending closer to February 2022. Map 2Northern India Views Pakistan Even More Unfavorably Than Rest Of India

South Asia: A Slowdown And A Showdown

South Asia: A Slowdown And A Showdown

India’s Finance Minister already announced a fiscal stimulus package of $85 billion (amounting to 2.8% of GDP) earlier this week. Whilst this stimulus entails limited fresh spending (amounting to about 0.6% of India’s GDP), we would not be surprised if the government follows it up with more spending closer to February 2022. Assertive Foreign Policy To Ward-Off Unfriendly Neighbors: India’s northern states are known to harbor unfavorable views of Pakistan (Map 2). The roots of this phenomenon can be traced to geography and the bloody civil strife of 1947 that was triggered by the partition of British-ruled India into the two independent dominions of India and Pakistan. Given the north’s unfavorable views of Pakistan and given looming elections, Indian policy makers may be forced to adopt a far more aggressive foreign policy response, to any terrorist strikes from Pakistan or territorial incursions by China. This kind of response was observed most recently ahead of the Indian General Elections in April-May 2019. An Indian military convoy was attacked by a suicide-bomber in early February 2019 and a Pakistan-based terrorist group claimed responsibility. A fortnight later the Indian air force launched unexpected airstrikes across the Line of Control which were then followed by the Pakistan air force conducting air strikes in Jammu and Kashmir. While the next round of Pakistani and Indian general elections is not due until 2023 and 2024, respectively, it is worth noting that of the seven state elections due in India in 2022, four are in the north (Uttar Pradesh, Punjab, Uttarakhand, and Himachal Pradesh). Force #3: Power Vacuum In Afghanistan The final reason to be wary of the South Asian geopolitical dynamic is the change in US policy: both the Iran nuclear deal expected in August and the impending withdrawal from Afghanistan in September. The US public has now elected three presidents on the demand that foreign wars be reduced. In the wake of Trump and populism the political establishment is now responding. Therefore Biden will ultimately implement both the Iran deal and the Afghan withdrawal regardless of delays or hang-ups. But then he will have to do damage control. In the case of Iran, a last-minute flare-up of conflict in the region is likely this summer, as the US, Israel, Saudi Arabia, and Iran underscore their red lines before the US and Iran settle down to a deal. Indeed it is already happening, with recent US attacks against Iran-backed Shia militias in Syria and Iraq. A major incident would push up oil prices, which is negative for India. But the endgame, an Iranian economic opening, is positive for India, since it imports oil and has had close relations with Iran historically. In the case of Afghanistan, the US exit will activate latent terrorist forces. It will also create a scramble for influence over this landlocked country that could lead to negative surprises across the region. The first principle of the peace agreement between the US and Afghanistan states that the latter will make all efforts to ensure that Afghan soil is not used to further terrorist activity. However, the enforceability of such a guarantee is next to impossible. Notably, the US withdrawal from Afghanistan will revive the Taliban’s influence in the region. This poses major risks for India, which has a long history of being targeted by Afghani terrorist groups. The Taliban played a critical role in the release of terrorists into Pakistan following the hijacking of an Indian Airlines flight in 1999. Furthermore, the Haqqani network, which has pledged allegiance to the Taliban, has attacked Indian assets in the past. Any attack on India deriving from the power vacuum in Afghanistan would upset the precarious regional balance. Whilst there are no immediate triggers for Afghani groups to launch a terrorist attack in India, the US withdrawal will trigger a tectonic shift in the region. Negative surprises emanating from Afghanistan should be expected. Investment Conclusions Chart 5Indian Banks Appear To Have Factored In All Positives

Indian Banks Appear To Have Factored In All Positives

Indian Banks Appear To Have Factored In All Positives

We reiterate the need to pare exposure to Indian assets on a tactical basis. India’s growth engine is likely to misfire over the second half of the Indian financial year. Macroeconomic headwinds pose the chief risk for investors, but major geopolitical changes could act as a negative catalyst in the current context. So we urge clients to stay short Indian Banks (Chart 5). Financials account for the lion’s share of India’s benchmark index (26% weight). India could opt for an unexpected expansion in its fiscal deficit soon. Whilst we continue to watch fiscal dynamics closely, we expect the fiscal expansion to materialize closer to February 2022 when India’s most populous state (i.e. Uttar Pradesh) will undergo elections. Over the long run, India’s sense of insecurity will escalate in the context of a more assertive China, stronger Sino-Pakistani ties, and a power vacuum in Afghanistan. For that reason, New Delhi will continue to shed its neutrality and improve relations with the US-led coalition of democratic countries, with an aim to balance China. This process will feed China’s insecurity of being surrounded and contained by a hegemonic American system. This security dilemma is a source of South Asian geopolitical risk that will become more globally relevant over time. China’s conflict with the US and western world should create incentives for India to attract trade and investment. However, its ability to do so will be contingent upon domestic political factors and regional geopolitical factors. Ritika Mankar, CFA Editor/Strategist ritika.mankar@bcaresearch.com Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 Sudhi Ranjan Sen, ‘India Shifts 50,000 Troops to China Border in Historic Move’, Bloomberg, June 28, 2021, bloomberg.com. 2 Joby Warrick, “China is building more than 100 missile silos in its western desert, analysts say,” Washington Post, June 30, 2021, washingtonpost.com.

Highlights Gold is – and always will be – exquisitely sensitive to Fed policy and forward guidance, as last month's "Dot Shock" showed (Chart of the Week). Its price will continue to twitch – sometimes violently – as the widening dispersion of views evident in the Fed dots keeps markets on edge and pushes forward rate expectations in different directions. Fed policy is important but will remain secondary to fundamentals in oil markets. Increasingly inelastic supply will force refiners to draw down inventories, which will keep forward curves backwardated. OPEC 2.0's production-management policy is the key driver here, followed closely by shale-oil's capital discipline. Between these market bookends are base metals, which will remain sensitive to Fed policy, but increasingly will be more responsive to tightening supply-demand fundamentals, as the pace of the global renewables and EV buildout challenges supply. The one thing these markets will share going forward is increasing volatility. Gold volatility will remain elevated as markets are forced to parse sometimes-cacophonous Fed forward guidance; oil volatility will increase with steeper backwardation; and base metals volatility will rise as fundamentals continue to tighten. We remain long commodity-index exposure (S&P GSCI and COMT ETF) and equity exposure (PICK ETF). Feature Gold markets still are processing last month's "Dot Shock" – occasioned by the mid-June move of three more Fed bankers' dots into the raise-rates-in-2022 camp at the Fed – and the sometimes-cacophonous forward guidance of post-FOMC meetings accompanying these projections. Following last month's meeting, seven of the 18 central bankers at the June meeting now favor an earlier rate hike. This dot dispersion fuels policy uncertainty. When policy uncertainty is stoked, demand for the USD typically rises, which generally – but not always – contributes to liquidation of dollar-sensitive positions in assets like commodities. This typically leads to higher price volatility.1 This is most apparent in gold, which is and always will be exquisitely sensitive to Fed guidance and the slightest hint of a change in course (or momentum building internally for such a change). This is what markets got immediately after the June meeting. When this guidance reflects a wide dispersion of views inside the Fed, it should come as no surprise that price volatility increases among assets that are most responsive to monetary policy. This dispersion of market expectations – as a matter of course – is intensified by discordant central-bank forward guidance.2 Fundamentals Reduce Oil's Sensitivity To Fed Policy Fed policy will always be important for the evolution of the USD through time, which makes it extremely important for commodities, since the most widely traded commodities are priced in USD. All else equal, an increase in the value of the USD raises the cost of commodities ex-US, and vice versa. Chart of the WeekGold Still Processing Dot Shock

Gold Still Processing Dot Shock

Gold Still Processing Dot Shock

Chart 2Oil Market Remains Tight...

Oil Market Remains Tight...

Oil Market Remains Tight...

The USD's impact is dampened when markets are fundamentally tight – e.g., when the level of demand exceeds supply, as is the case presently for oil (Chart 2).3 When this occurs, refiner inventories have to be drawn down to make up for supply deficits (Chart 3). This leads to a backwardation in the oil forward curves – i.e., prices of prompt-delivery oil are higher than deferred-delivery oil – reflecting the fact that the supply curve is becoming increasingly inelastic (Chart 4). This backwardation benefits OPEC 2.0 member states, as most of them have long-term supply contracts with customers indexed to spot prices, and investors who are long commodity-index exposure, as it is the source of the roll yield for these products.4 Chart 3Forcing Inventories To Draw...

Forcing Inventories To Draw...

Forcing Inventories To Draw...

Chart 4...And Backwardating Forward Curves

...And Backwardating Forward Curves

...And Backwardating Forward Curves

Copper's Sensitivity To Fed Policy Declining Supply-demand fundamentals in base metals – particularly in the bellwether copper market – are tightening, which, as the oil market illustrates, will make prices in these markets less sensitive to USD pressures going forward (Chart 5). We expect the copper forward curve to remain backwardated for an extended period (Chart 6), which will distance the evolution of copper prices from Fed policy variables (e.g., interest rates and the USD). Chart 5Copper USD Sensitivity Will Diminish As Balances Tighten

Copper USD Sensitivity Will Diminish As Balances Tighten

Copper USD Sensitivity Will Diminish As Balances Tighten

Chart 6Expect Persistent Backwardation In Copper

Expect Persistent Backwardation In Copper

Expect Persistent Backwardation In Copper

Indeed, our modeling suggests this already is occurring in the metals markets, as can be seen from the resilience of copper prices during 1H21, when China's fiscal and monetary stimulus was waning and, recently, during the USD's recent rally, which was an unexpected headwind generated by the Fed's June meeting. If, as appears likely, China re-engages in fiscal and monetary stimulus in 2H21, the global demand resurgence for metals, copper in particular, will receive an additional fillip. Like oil, copper inventories will have to be drawn down over the next two years to make up for physical deficits, which have been a persistent problem for years (Chart 7). Capex in copper markets has yet to be incentivized by higher prices, which means these physical deficits likely will widen as the world gears up for expanded renewables generation and the grids required to support them, not to mention higher electric vehicle (EV) demand. If, as we expect, copper miners do not invest in new greenfield mine projects – choosing instead to stay with their brownfield expansion strategies – the market will tighten significantly as the world ramps up its demand for renewable energy. This means copper's supply curve will, like oil's, become increasingly inelastic. At the limit – i.e., if new mining capex is not incentivized – price will be forced to allocate limited supply, and may even have to get to the point of destroying demand to accommodate the renewables buildout. Chart 7Supply-Demand Balance Tightening In Copper

Supply-Demand Balance Tightening In Copper

Supply-Demand Balance Tightening In Copper

A Word On Spec Positioning We revisited our modeling of speculative influence on these markets over the past couple of weeks, in anticipation of the volatility we expect and the almost-certain outcry from public officials that will ensue. Our modeling continues to support our earlier work, which found fundamentals are determinant to the evolution of industrial commodity prices. Using Granger-Causality and econometric analysis, we find prices mostly explain spec positioning in oil and copper, and not the other way around.5 We do find spec positioning – via Working's T Index – to be important to the evolution of volatility in WTI crude oil options, along with other key variables (Chart 8).6 That said, other variables are equally important to this evolution, including the St. Louis Fed's Financial Stress Index, EM equity volatility, VIX volatility and USD volatility. These variables are not useful in modeling copper volatility, where it appears fundamental and financial variables are driving the evolution of prices and, by extension, price volatility. We will continue to research this issue, and will continue to subject our results to repeated trials in an attempt to disprove them, as any researcher would do. Chart 8Oil Volatility Drivers

Oil Volatility Drivers

Oil Volatility Drivers

Investment Implications Gold will remain hostage to Fed policy, but oil and base metals increasingly will be charting a path that is independent of policy-related variables, chiefly the USD. There is no escaping the fact that gold volatility will increasingly be in the thrall of US monetary policy – particularly during the next two years as the Fed attempts to guide markets toward something resembling normalization of that policy.7 However, as the events of the most recent FOMC meeting illustrate, gold price volatility will remain elevated as markets are forced to parse oftentimes-cacophonous Fed forward guidance. This would argue in favor of using low-volatility episodes as buying opportunities in gold options – particularly calls, as we continue to expect gold prices to end the year at $2,000/oz. We also favor silver exposure via calls, expecting price to go to $30/oz this year. In oil and base metals, we continue to expect supply-demand fundamentals in these markets to tighten, which predisposes us to favor commodity index products. For this reason, we remain long commodity-index exposure – specifically the S&P GSCI index, which is up 6.8% since inception, and the COMT ETF, which is up 8.7% since inception. We expect the base metals markets to remain very well bid going forward, and remain long equity exposure in these markets via the PICK ETF, which we re-entered after a trailing stop was elected that left us with a 24% gain since inception at the end of last year. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Ashwin Shyam Research Associate Commodity & Energy Strategy ashwin.shyam@bcaresearch.com Commodities Round-Up Energy: Bullish US crude oil stocks (ex SPR) fell 6.7mm barrels in the week ended 25 June 2021, according to the US EIA. Total crude and product stocks were down 4.6mm barrels. Domestic crude oil production was unchanged at 11.1mm b/d over the reporting week. Total refined-product demand surpassed the comparable 2019 reporting period, led by higher distillate consumption (4.2mm b/d vs 3.8mm b/d). Gasoline consumption remains a laggard (9.2mm b/d vs 9.5mm b/d), as does jet fuel (1.4mm b/d vs 1.9mm b/d). Propane and propylene demand surged over the period, likely on the back of petchem demand (993k b/d vs 863k b/d). Base Metals: Bullish Base metals prices are moving higher in anticipation of tariffs being imposed by Russia to discourage exports beyond the Eurasian Economic Union, according to argusmedia.com. In addition to export tariffs on copper, aluminum and nickel, steel exports also will face levies to discourage material from leaving the EAEU (Chart 9). The tariffs are expected to remain in place from August through December 2021. Separately, premiums paid for high-quality iron ore in China (65% Fe) reached record highs earlier this week, as steelmakers scramble for supply, according to reuters.com. The premium iron ore traded close to $36/MT over benchmark material (62% Fe) this week. Precious Metals: Bullish Gold prices continue to move lower following the FOMC meeting on June 16. The yellow metal was down 0.6% y-o-y at $1762.80/oz as of Tuesday’s close after being up a little more than 13% y-o-y before the FOMC meeting earlier this month (Chart 10). We believe the USD rally, which, based on earlier research we have done, could be benefitting from safe-haven demand arising from global concern over the so-called Delta variant of COVID-19, which has spread to at least 85 countries. Public-health officials are fearful this could cause a resurgence in COVID-19 cases and additional mutations in the virus if vaccine distribution in EM states is not increased. Ags/Softs: Neutral Widely disparate weather conditions in the US west and east crop regions – drought vs cooler and wetter weather – appear to be on track to produce average crop yields for corn and beans this year, according to agriculture.com's Successful Farming. In regions where hard red spring wheat is grown, states experiencing low rainfall likely will have poor crops this year. Chart 9

"Dot Shock" Continues To Roil Gold; Oil … Not So Much

"Dot Shock" Continues To Roil Gold; Oil … Not So Much

Chart 10

US Dollar To Keep Gold Prices Well Bid

US Dollar To Keep Gold Prices Well Bid

Footnotes 1 We model gold prices as a function of financial variables sensitive to Fed policy – e.g., real rates and the broad trade-weighted USD – and uncertainty, which is conveyed via the Global Economic Policy Uncertainty (GEPU) index published by Baker, Bloom & Davis. 2 Please see Lustenberger, Thomas and Enzo Rossib (2017), "Does Central Bank Transparency and Communication Affect Financial and Macroeconomic Forecasts?" SNB Working Papers, 12/2017. The Swiss central bank researchers find "… the verdict about the frequency of central bank communication is unambiguous. More communication produces forecast errors and increases their dispersion. … Stated differently, a central bank that speaks with a cacophony of voices may, in effect, have no voice at all. Thus, speaking less may be beneficial for central banks that want to raise predictability and homogeneity among financial and macroeconomic forecasts. We provide some evidence that this may be particularly true for central banks whose transparency level is already high." (p. 26) 3 Please see OPEC 2.0 Vs. The Fed, published on February 8, 2018, for additional discussion. 4 Please see The Case For A Strategic Allocation To Commodities As An Asset Class, a Special Report we published on March 11, 2021 on commodity-index investing. It is available at ces.bcaresearch.com. 5 The one outlier we found was Brent prices, for which non-commercial short positioning does Granger-Cause price. Otherwise, price was found to Granger-Cause spec positioning on the long and short sides of the market. 6 Please see BCA Research's Commodity & Energy Strategy Weekly Report, "Specs Back Up The Truck For Oil," published on April 26, 2018, in which we introduce Holbrook Working's "T Index," a measure of speculative concentration in futures and options markets. It is available at ces.bcaresearch.com. Briefly, Working's T Index shows how much speculative positioning exceeds the net demand for hedging from commercial participants in the market. 7 Please see How To Re-Shape The Yield Curve Without Really Trying published by our US Bond Strategy group on June 22 for a deeper discussion of the outlook for Fed policy. Investment Views and Themes Strategic Recommendations Tactical Trades Commodity Prices and Plays Reference Table Trades Closed in 2021 Summary of Closed Trades

Image

BCA Research’s China Investment Strategy service published their mid-year outlook for China today. They maintain an underweight stance on Chinese stocks, but recommend investors watch for signs of policy easing. Pressures to support domestic demand will be…

China’s official manufacturing PMI inched down to 50.9 in June from 51.0 in May, extending its downward trend that started in March. Its sub-indexes, however, sent mixed signals. While the new export orders, production and input price components fell, new…

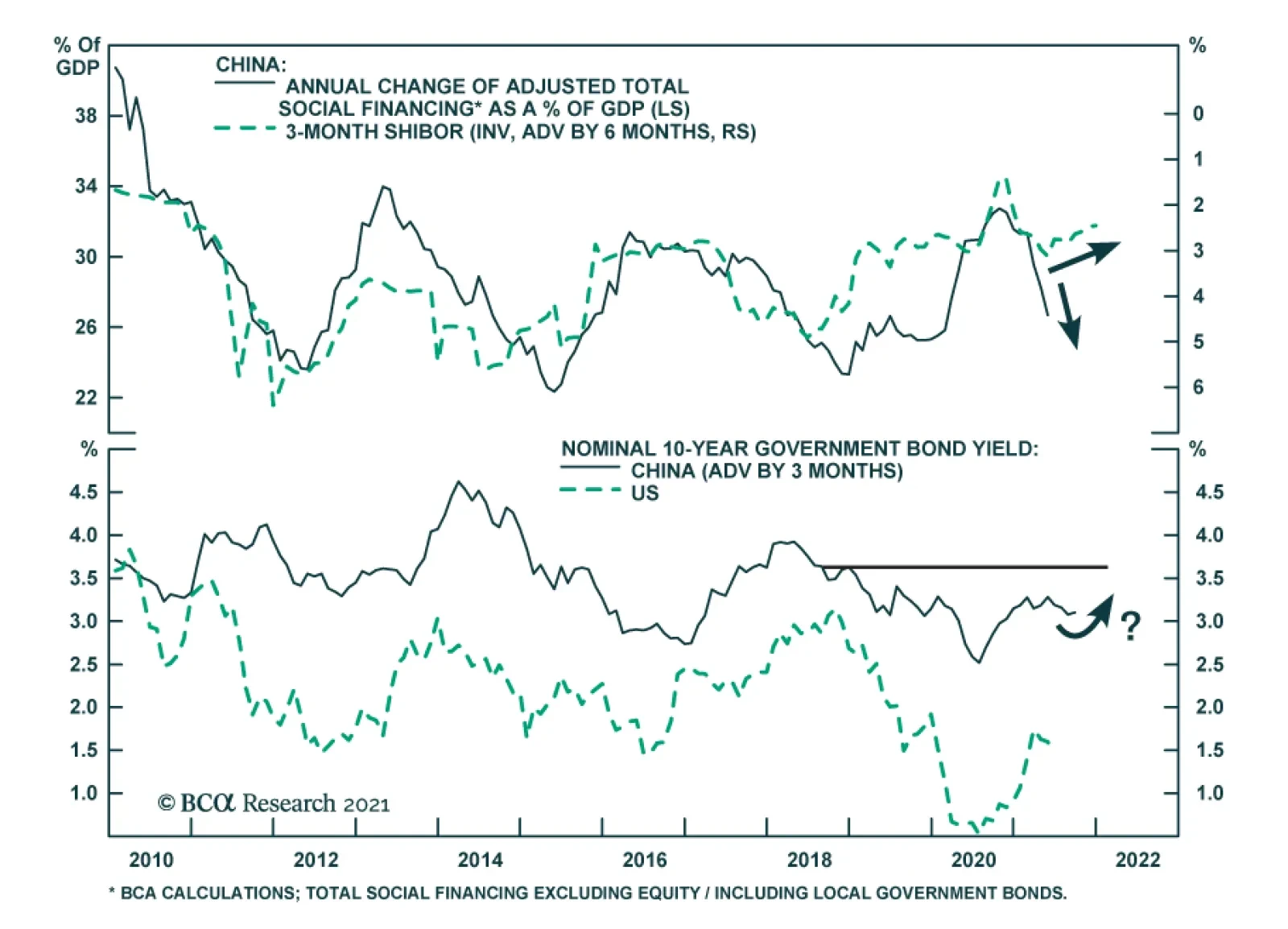

Dear Client, China Investment Strategy will take a summer break next week. We will resume our publication on July 14th. Best regards and we wish you a happy and healthy summer. Jing Sima, China Strategist Highlights A USD rebound and higher domestic bond yields pose near-term challenges to Chinese risk assets. A sharp deceleration in credit growth in the past seven months will lead to weaker-than-expected data from China’s old-economy sectors in the second half of the year. Robust global trade has propelled Chinese exports, allowing the country to pursue financial deleverage and structural reforms. However, next year policymakers will face increased pressure to support the domestic economy as the global economic recovery peaks and demand slows. Investors should maintain an underweight stance towards Chinese stocks in 2H21, but remain alert to any improvements in China’s policy tone. An easing monetary policy may signal a potential upgrade catalyst in 1H22. Feature Most recent macro figures confirm that China’s impressive economic upcycle has peaked. We expect that the official manufacturing and non-manufacturing PMIs, which will be released as this report is published, will come in modestly down. We maintain the view that a major relapse in economic activity is unlikely, but the strong tailwinds that have propelled China's recovery since Q2 last year have since abated and will lead to softer growth. Meanwhile, the rate of economic and export expansions has given Chinese policymakers confidence to scale back leverage and continue with market reforms. In the second half of the year, investors' sentiment towards Chinese stocks will be tested based on three risks: A rebound in the US dollar index. A tighter liquidity environment and higher interest rates. A weakening in macro indicators beyond market expectations. As the global economic recovery peaks into 2022, pressures to support the domestic economy will become more urgent if policymakers want to maintain an average rate of 5% real GDP growth in 2020 - 2022. The current policy settings are not yet favorable to overweight Chinese risk assets. Major equity indexes remain richly valued and the market could easily correct if domestic rates move higher. However, signs of policy easing may emerge by yearend, which would prompt us to shift our view to overweight Chinese stocks in both absolute and relative terms. The Case For A Dollar Rebound On a tactical basis (next three months), a rebound in the US dollar index may curb investors’ enthusiasm for Chinese stocks. A stronger dollar will give the RMB’s appreciation some breathing room and will be reflationary for China’s economy. However, in the short term a stronger USD will also lead to weaker foreign inflows to China’s equity markets. Chinese stock prices have become more closely and negatively correlated with the dollar index since early 2020 (Chart 1). A weaker dollar is usually accompanied by a global economic upturn and a higher risk appetite from investors, propelling more foreign portfolio flows to emerging markets (which includes Chinese risk assets). Although foreign inflows account for a small portion of the Chinese A-share market cap, global institutional investors’ sentiment has become more influential and has led fluctuations in Chinese onshore stock prices (Chart 2). Chart 1Closer Correlations Between Chinese Stocks And The Dollar Index

Closer Correlations Between Chinese Stocks And The Dollar Index

Closer Correlations Between Chinese Stocks And The Dollar Index

Chart 2Foreign Investors Matter To Chinese Onshore Stock Prices

Foreign Investors Matter To Chinese Onshore Stock Prices

Foreign Investors Matter To Chinese Onshore Stock Prices

Chart 3Rising Market Expectations For The Fed's Rate Liftoff

Rising Market Expectations For The Fed's Rate Liftoff

Rising Market Expectations For The Fed's Rate Liftoff

The US Federal Reserve delivered a slightly more hawkish surprise at its June FOMC meeting with the message that it will move the projected timing of its first fed fund rate liftoff from 2024 to 2023. Since then, market expectations have shifted from growth and inflation to focusing on the next monetary policy tightening phase, with the short end of the US yield curve rising sharply (Chart 3). Given that currency markets trade off the short end of the yield curve, higher US interest rate expectations will at least temporarily lift the US dollar. The timing and pace of the Fed’s tapering of asset purchases and rate hikes will be determined by how rapidly the US economy approaches the US central bank’s definition of “maximum employment.” BCA’s US Bond Investment strategist anticipates that sizeable and positive non-farm payroll surprises will start in late summer/early fall, which will catalyze a move higher in bond yields. As such, we expect additional upside risks in the dollar index in the coming months, which will discourage foreign investors’ appetite for Chinese equities. Bottom Line: A rebound in the dollar index will be a near-term downside risk to Chinese stocks. Risk Of Higher Chinese Interest Rates Another near-term risk to Chinese stock prices is a tightening in domestic liquidity conditions and a rebound in interest rates, particularly in Q3. Chart 4The PBoC Has Managed To Keep Domestic Rates Low While Pulling Back Overall Stimulus

The PBoC Has Managed To Keep Domestic Rates Low While Pulling Back Overall Stimulus

The PBoC Has Managed To Keep Domestic Rates Low While Pulling Back Overall Stimulus

So far this year the PBoC has kept liquidity conditions accommodative to avoid massive debt defaults, while allowing a faster deceleration in the pace of credit expansion and a sharp contraction in shadow banking (Chart 4). In the coming months, however, the trend may reverse. Even though we do not think China’s current inflation and growth dynamics warrant meaningful and sustainable monetary policy tightening, there is still room for rates to normalize to their pre-pandemic levels in the next few months. Our view is based on the following: First, there was a major delay in local government bond issuance in the first five months of the year. The supply of government bonds will pick up meaningfully in Q3 to meet the annual quota for 2021. An increase in government bond issuance will remove some liquidity from the banking system because the majority of these local government bonds are purchased by commercial banks. Adding to the liquidity gap is a large number of one-year, medium-term lending facility (MLF) loans that will be due in 2H21. Secondly, the PBoC may shift its policy tightening from reducing the volume of total credit creation (measured by total social financing) to raising the price of money. Credit growth (on year-over-year basis) in the first five months of 2021 dropped by three percentage points from its peak in Q4 last year, much faster than the 13-month peak-to-trough deceleration during the 2017/18 policy tightening cycle. As the rate of credit creation approaches the government’s target for the year, which we expect around 11%, the pressure to further compress credit expansion has eased into 2H21. China’s policy agenda is still focused on de-risking in the financial and real estate sectors, therefore, we expect policymakers to keep overall monetary conditions restrictive by raising the price of money. Furthermore, we do not rule out the possibility of a hike in mortgage rates. Chart 5Rising Risk For A Bear Flattening In Domestic Yield Curve In Q3

Rising Risk For A Bear Flattening In Domestic Yield Curve In Q3

Rising Risk For A Bear Flattening In Domestic Yield Curve In Q3

Lastly, as the Fed prepares market expectations for its rate liftoff and China’s domestic economy is still relatively solid, the PBoC may seize the opportunity to guide market-based interest rates towards their pre-pandemic levels. Thus, the market will likely price in tighter liquidity conditions while lowering expectations for the economy and inflation. The short end of the yield curve will rise faster than the longer end, resulting in a flattening of the curve (Chart 5). There is a nontrivial risk that the market will react negatively to tighter liquidity conditions and rising bonds yields, particularly when the economy is slowing. We mentioned in previous reports that rising policy rates and bond yields do not necessarily lead to lower stock prices, if rates are rising while credit keeps expanding and corporate profit growth accelerates. However, currently credit impulse has decelerated sharply, and corporate profit growth has most likely peaked in Q2. Therefore, even a small increase in bond yields or market expectations of higher rates will likely trigger risk asset selloffs. Bottom Line: Bond yields will move higher in Q3, risking market selloffs. Chinese Economy Standing On One Leg China’s economic fundamentals also pose downside risks to Chinese stock prices. Macro indicators on a year-over-year comparison will soften further in 2H21 when low base effects wane, although they will weaken from very high levels. This year’s sharp credit growth deceleration will start to drag down domestic demand, with the risk of corporate profits disappointing the market. A positive tailwind from global trade prevented China's old economy from decelerating more in the first half of the year. It is reflected in the nominal imports and manufacturing orders components in the BCA Activity Index (Chart 6). However, while rising commodity prices boosted the value of Chinese imports, the volume of imports has been moving sideways of late (Chart 7). Chart 6Our BCA Activity Index Is Still Rising...

Our BCA Activity Index Is Still Rising...

Our BCA Activity Index Is Still Rising...

Chart 7...But The Volume Of The Import Component Has Rolled Over

...But The Volume Of The Import Component Has Rolled Over

...But The Volume Of The Import Component Has Rolled Over

Chart 8Export Growth Is Moderating From Current Level

Export Growth Is Moderating From Current Level

Export Growth Is Moderating From Current Level

Moreover, China’s export volume is peaking as the reopening in other countries shifts consumer demand from goods to services. Strong export growth would likely decelerate and converge to global industrial production growth in the coming 12 months, even though a regression-based approach suggests that export growth will stay above trend-growth if global economic activity remains robust (Chart 8). All three components of the official Li Keqiang Index, which measures China’s industrial sector activity and incorporates electricity consumption, railway transportation and bank lending, have rolled over (Chart 9). Among the three components in BCA’s Li Keqiang Leading Indicator, only the monetary conditions index improved on the back of lower real rates. Contributions from the money supply and credit expansion components to the overall indicator have been negative (Chart 10). Chart 9The Official Li Keqiang Index Is Weakening...

The Official Li Keqiang Index Is Weakening...

The Official Li Keqiang Index Is Weakening...

Chart 10...So Is Our BCA Li Keqiang Leading Indicator

...So Is Our BCA Li Keqiang Leading Indicator

...So Is Our BCA Li Keqiang Leading Indicator

Chart 11Household Consumption Recovery Remains A Laggard

Household Consumption Recovery Remains A Laggard

Household Consumption Recovery Remains A Laggard

The recovery in household consumption remains well behind the industrial sector in the current cycle (Chart 11). We expect consumption and services to continue recovering very gradually. Apart from China’s long-standing structural issues, such as sliding household income growth and a high propensity to save, the cyclical recovery in consumption is dependent on China’s domestic COVID-19 situation. The country is on track to fully vaccinate 40% of its population by the end of June and 80% by year-end (Chart 12). However, hiccups in the service sector recovery are expected through 2H21, given China’s “zero tolerance” policy on confirmed COVID cases, which could trigger sporadic local lockdowns (Chart 13). Chart 12China Is Racing To Reach “Full Inoculation Rate” By Yearend

China Outlook: A Mid-Year Recap

China Outlook: A Mid-Year Recap

Chart 13Expect Some Hiccups In Service Sector Recovery In 2H21

Expect Some Hiccups In Service Sector Recovery In 2H21

Expect Some Hiccups In Service Sector Recovery In 2H21

Bottom Line: Any moderation in exports in the rest of 2021 may add to the slowdown in China’s economic activity. Don’t Count On Fiscal Support Chart 14Fiscal Spending Has Been Disappointing In 1H21

Fiscal Spending Has Been Disappointing In 1H21

Fiscal Spending Has Been Disappointing In 1H21

During the first five months of the year, fiscal spending has downshifted (Chart 14). The amount of local government special-purpose bonds (SPBs) issued was far less than in the same period of the past two years, and below this year’s approved annual quota. Although we expect fiscal support to increase into 2H21, backloading SPBs would qualify, at best, as a remedial measure rather than a meaningful boost to economic activity. The RMB3 trillion SPBs to be issued in 2H21 represent only about 10% of this year’s total credit expansion. To substantially boost credit impulse and economic activity, the pickup in SPB issuance will need to be accompanied by looser monetary policy and an acceleration in bank loans (Chart 15). We do not expect that liquidity conditions will remain as lax as in 1H21. Additionally, given that the central government’s focus is to rein in the leverage of local governments and their affiliated financial vehicles (LGFV), provincial officers have little incentive to take on more bank loans against a restrictive policy backdrop. Historically, a stronger fiscal impulse linked to hefty increases in local government bond issuance has not necessarily led to meaningful improvements in infrastructure investment, which has been on a structural downshift since 2017 (Chart 16). Following a V-shaped recovery in 2H20, the growth in infrastructure investment will likely continue to slide in 2H21 due to sluggish government spending. Chart 15Bank Loans Still Hold The Key To Stimulus Impulse

Bank Loans Still Hold The Key To Stimulus Impulse

Bank Loans Still Hold The Key To Stimulus Impulse

Chart 16Don't Count On SPBs To Meaningfully Boost Infrastructure Investment

Don't Count On SPBs To Meaningfully Boost Infrastructure Investment

Don't Count On SPBs To Meaningfully Boost Infrastructure Investment

Bottom Line: There are no signs that the overall policy stance is easing to facilitate a higher fiscal multiplier from an upturn in local government bond issuance. As such, fiscal support for infrastructure spending and economic activity will disappoint in 2H21 despite more SPB issuance. Investment Conclusions Monetary conditions may tighten in Q3 although credit growth will decelerate at a slower pace. Pressures to support domestic demand will be more pronounced next year as tailwinds abate from the global recovery and domestic massive stimulus. Our view is that Chinese authorities will likely ease on the policy tightening brake towards the end of this year and perhaps even signal some reflationary measures in early 2022. Therefore, while we maintain an underweight stance on Chinese stocks for the time being, investors should remain alert to any improvements in China's policy direction. In particular, any monetary policy easing by end this year/early 2022 may signal a potential catalyst to upgrade Chinese stocks to overweight in absolute terms. Although both Chinese onshore and investable equities are currently traded at a discount relative to global stocks, they are richly valuated compared with their 2017/18 highs (Chart 17). China's economy is slowing and the corporate sector has substantially increased its leverage in the past decade. We believe that the current discount in Chinese equities relative to global stocks is warranted. Chart 18 presents a forecast for A-share earnings growth in US dollars, based on earnings’ relationship with the official Li Keqiang index. The chart shows that while an earnings contraction is not probable, without more stimulus the growth rate may fall sharply in the next 12 months from its current elevated level. This aspect, combined with only a minor valuation discount relative to global stocks, paints an uninspiring outlook for Chinese onshore stocks. Chart 17Chinese Onshore Stocks Are Traded At A Slight Discount To Global Equities

Chinese Onshore Stocks Are Traded At A Slight Discount To Global Equities

Chinese Onshore Stocks Are Traded At A Slight Discount To Global Equities

Chart 18An Uninspiring Domestic Equity Earnings Outlook

An Uninspiring Domestic Equity Earnings Outlook

An Uninspiring Domestic Equity Earnings Outlook

Our baseline view is that Chinese authorities will be more willing to step up policy supports into 2022. Fiscal impulse will likely turn negative for most major economies next year and global economic recovery will have peaked. In this scenario, both China’s economy and stocks will have the potential to outperform their global peers next year. Jing Sima China Strategist jings@bcaresearch.com Cyclical Investment Stance Equity Sector Recommendations

Emerging Market equities have been underperforming the global market since early June and we think this trend will continue during the next few months. First, the Fed’s hawkish pivot in June is just a small sampling of things to come. US employment will…

Highlights Spread Product: The macro environment is highly supportive for spread product and it will likely remain supportive for the next 12-18 months, at least until the yield curve flattens to below 50 bps. Remain overweight spread product versus Treasuries in US bond portfolios. High-Yield: High-yield spreads still look fairly valued, or even slightly cheap, compared to our base case outlook for corporate defaults. Investors should continue to favor high-yield over investment grade corporates and maintain an overweight allocation to high-yield in US bond portfolios. EM Corporates: Within the A and Baa credit tiers, US bond investors should favor USD-denominated EM corporates over USD-denominated EM sovereigns and should favor both over US corporate bonds. Within the Aa credit tier, investors should favor USD-denominated EM sovereigns over USD-denominated EM corporates and should favor both over US corporate bonds. Feature Chart 1Fed Meeting Didn't Shock Credit Markets

Fed Meeting Didn't Shock Credit Markets

Fed Meeting Didn't Shock Credit Markets

Last week’s report looked at how the June FOMC meeting prompted a massive re-shaping of the Treasury curve.1 It didn’t discuss, however, the impact that June’s meeting had on credit spreads. There’s a simple reason for this. Corporate bond spreads didn’t move very much post-FOMC. In fact, neither investment grade nor high-yield spreads have widened significantly during the past two weeks, despite the Fed’s apparent “hawkish turn” (Chart 1). The VIX jumped briefly above 20 in the days following the Fed meeting but it has since re-discovered its lows (Chart 1, bottom panel). This week’s report considers whether the corporate bond market is too complacent. The first section updates our assessment of where we are in the credit cycle based on two indicators that did see large swings post-Fed. The second section updates our outlook for high-yield defaults and considers whether junk spreads continue to offer adequate compensation. Finally, the third section of this report presents an introductory look at valuation in the USD-denominated Emerging Market (EM) corporate sector. We find that, for the most part, investment grade EM corporates are attractively valued relative to EM sovereigns and US corporates of the same credit rating and duration. Credit Cycle Update Chart 2Credit Cycle Indicators

Credit Cycle Indicators

Credit Cycle Indicators

As we have repeatedly stated in past research, the slope of the yield curve is a very important credit cycle indicator.2 We have documented that spread product tends to outperform duration-matched Treasuries by a wide margin when the yield curve is steep. This outperformance tapers off once the 3-year/10-year Treasury slope falls below 50 bps and it falls off even more when the slope dips below zero.3 With that in mind, it is notable that the Treasury curve flattened dramatically following the June FOMC meeting (Chart 2). At 106 bps, the 3-year/10-year Treasury slope remains well above the 50 bps threshold that would start to get concerning for spread product. However, it’s likely that the yield curve will continue to flatten as we approach a Fed rate hike in 2022. In other words, we expect that monetary conditions will turn sufficiently restrictive for us to reduce our recommended spread product allocation within the next 12-18 months. On the other hand, one positive development for spread product returns is that the 5-year/5-year forward TIPS breakeven inflation rate declined following the June FOMC meeting. In fact, it is now below the 2.3% to 2.5% range that is consistent with the Fed’s inflation target (Chart 2, bottom panel). This is a positive development for spread product because the Fed will strive to ensure that monetary conditions stay accommodative at least until these long-dated inflation expectations are consistent with the 2.3% to 2.5% target. Or put differently, a rebound in long-maturity TIPS breakeven inflation rates back to the target range will slow the near-term pace of curve flattening, giving the credit cycle a small amount of extra running room. In short, the macro environment is highly supportive for spread product and it will likely remain supportive for the next 12-18 months, at least until the yield curve flattens to below 50 bps. Investment Grade Corporates The highly supportive macro environment applies to investment grade corporate bonds, just as it does to all spread sectors. However, investment grade corporates have the problem that valuation is extremely tight. Much like a flat yield curve environment, a tight spread environment tends to coincide with low excess corporate bond returns. However, our research reveals that tight spreads alone are not sufficient for investment grade corporates to underperform duration-matched Treasuries. Table 1 classifies each month since May 1973 based on the investment grade corporate bond spread and the 3/10 Treasury slope. It then shows a 90% confidence interval for corporate bond excess returns during the following 12 months. It shows that, even when the corporate bond spread is below 100 bps (it is 81 bps today), investment grade corporates still tend to outperform duration-matched Treasuries as long as the 3/10 Treasury slope is above 50 bps. Table 1Expected 12-Month Corporate Bond Excess Return* (BPs) Based On OAS And Yield Curve Slope

The Post-FOMC Credit Environment

The Post-FOMC Credit Environment

Bottom Line: The yield curve has started to flatten but it remains very steep, consistent with spread product outperforming duration-matched Treasuries. We remain overweight spread product versus Treasuries but will re-consider this position once the yield curve flattens to below 50 bps. We expect this could happen within the next 12-18 months. We maintain only a neutral allocation to investment grade corporate bonds because of stretched valuations. We see more attractive opportunities in high-yield corporates (see next section), municipal bonds, USD-denominated EM sovereigns and USD-denominated EM corporates (see final section below). High-Yield Default Update We last updated our default rate outlook in March.4 At that time, we concluded that junk spreads offered adequate compensation for expected default losses. Since then, we have received nonfinancial corporate sector profit and debt growth data for the first quarter of 2021, crucial inputs to our macro-based default rate model. Our macro-based model of the 12-month trailing speculative grade default rate is based on nonfinancial corporate sector gross leverage (i.e. pre-tax profits over total debt) and C&I lending standards (Chart 3). Lending standards enter our model with a lag, but we need a forward-looking estimate of gross leverage for our model to generate predictions. Chart 3Macro-Driven Default Rate Model

Macro-Driven Default Rate Model

Macro-Driven Default Rate Model

To estimate gross leverage we first model corporate profit growth based on real GDP (Chart 4) and assume that real GDP grows by 7% over the next four quarters, consistent with the Fed’s median forecast. This gives us a profit growth expectation of roughly 30%. Chart 4Profit & Debt Growth

Profit & Debt Growth

Profit & Debt Growth

We also need an estimate for corporate debt growth. Corporate debt exploded last year, growing 10% in 2020, but it then slowed to an annualized rate of 4% in Q1 2021. We think corporate debt growth will remain slow going forward. The nonfinancial corporate sector financing gap has been negative in each of the past four quarters (Chart 4, bottom panel), meaning that retained earnings have exceeded capital expenditures. In other words, firms have built up a lot of excess capital that can be deployed in place of debt to finance new investment opportunities. Table 2 shows our model’s predicted 12-month default rate based on different assumptions for profit and debt growth. If we assume corporate profit growth of 30% and corporate debt growth between 0% and 8%, then our model predicts that the 12-month default rate will fall from its current 5.5% to a range of 2.3% - 2.8%. Table 2Default Rate Scenarios

The Post-FOMC Credit Environment

The Post-FOMC Credit Environment

Next, we need to consider what sort of expected default rate is priced into the High-Yield index. Our analysis of historical junk spreads and returns suggests that we should require a minimum excess spread of 100 bps in the High-Yield index after subtracting default losses to be confident that junk bonds will outperform Treasuries.5 If we also assume a recovery rate of 40% on defaulted debt, then we calculate that the High-Yield index is fairly priced for a 12-month default rate of 2.9% (Chart 5). That is, junk spreads appear slightly cheap compared to the 2.3% - 2.8% range predicted by our macro model. Finally, it’s worth noting that actual corporate default events have been quite rare in recent months. In the first five months of 2021 we’ve seen between 1 and 3 default events per month. If we extrapolate that trend and assume we see 3 defaults per month going forward, then we calculate that the 12-month trailing default rate will fall to 2.0% by December, before leveling off at 2.2% (Chart 6). In other words, the recent trend has been one of significantly fewer defaults than predicted by our macro model Chart 5Spread-Implied Default Rate

Spread-Implied Default Rate

Spread-Implied Default Rate

Chart 6Recent Default Trends

Recent Default Trends

Recent Default Trends

Bottom Line: High-yield spreads still look fairly valued, or even slightly cheap, compared to our base case outlook for corporate defaults. Investors should continue to favor high-yield over investment grade corporates and maintain an overweight allocation to high-yield in US bond portfolios. An Attractive Opportunity In EM Corporates This week we present an introductory look at the risk/reward opportunity in USD-denominated EM corporate bonds. Specifically, we look at the investment grade Bloomberg Barclays USD-denominated EM Corporate & Quasi-Sovereign index. We compare this index to both the investment grade USD-denominated EM Sovereign index and the US Credit index.6 First, we look at recent performance trends and average index statistics (Table 3). Both the EM Corporate and EM Sovereign indexes have average credit ratings between A and Baa, so we compare their performance to the A-rated and Baa-rated US Credit indexes. We observe a significant option-adjusted spread (OAS) advantage in both the EM indexes, though part of the extra spread offered by the Sovereign index is compensation for its longer duration. The EM Corporate index sticks out as offering an extremely attractive OAS per unit of duration. Table 3Performance Trends & Index Statistics

The Post-FOMC Credit Environment

The Post-FOMC Credit Environment

As for performance, we see that the EM Corporate index experienced less of a drawdown (in excess return terms) during the COVID recession, though it has also returned less than both the EM Sovereign index and the Baa Credit index during the recent upswing. Chart 7Spreads Versus Credit Rating & Duration-Matched US Credit

The Post-FOMC Credit Environment

The Post-FOMC Credit Environment

Next, we look at each individual credit tier of both the EM Corporate & Quasi-Sovereign index and the EM Sovereign index, and we calculate the spread relative to a credit rating and duration-matched position in the US Credit index (Chart 7). In general, we see that both EM indexes offer a spread advantage versus duration-matched US Credit across all credit rating tiers. EM sovereigns look better than EM corporates in the Aa credit tier. This is the result of attractive spreads on the sovereign bonds of UAE and Qatar. However, EM corporates clearly dominate sovereigns in both the A and Baa credit tiers. Finally, we consider the risk/reward trade-off in our EM indexes by using our Excess Return Bond Map. Our Excess Return Bond Map shows the relationship between expected return (on the vertical axis) and risk (on the horizontal axis). In Chart 8A our risk measure is the 12-month spread widening required for each index to lose 100 bps versus a position in duration-matched Treasuries divided by that index’s historical spread volatility. It can be thought of as the number of standard deviations of spread widening required for the index to provide an excess return of -100 bps. A higher value corresponds to less risk, and vice-versa. Chart 8B uses the same risk measurement, only we use the spread widening required to lose 500 bps versus Treasuries to assess the risk of a large drawdown. Both Charts 8A and 8B use OAS as the measure of expected return. Chart 8AExcess Return Bond Map (100 BPs Loss Threshold)

The Post-FOMC Credit Environment

The Post-FOMC Credit Environment

Chart 8BExcess Return Bond Map (500 BPs Loss Threshold)

The Post-FOMC Credit Environment

The Post-FOMC Credit Environment

The first thing that sticks out in Charts 8A & 8B is that Baa-rated EM corporates offer greater expected return and less risk than the EM Sovereign index and the Baa US Credit Index. This is true whether our loss threshold is set at 100 bps or 500 bps. Unfortunately, we do not have sufficient data to split the EM Sovereign index by credit tier in these charts. A-rated EM corporates offer slightly less expected return than the EM Sovereign index but with significantly less risk, they also clearly dominate the A-rated US Credit Index. Aa-rated EM corporates appear to offer a similar risk/reward trade-off as the EM Sovereign index, though we know from Chart 7 that sovereigns have a spread advantage in the Aa credit tier. The bottom line is that USD-denominated EM corporates are attractively valued relative to investment grade US corporate bonds with the same duration and credit rating. EM corporates also look preferable to EM sovereigns in the A and Baa credit tiers. EM sovereigns are more attractive than EM corporates in the Aa credit tier. Within the A and Baa credit tiers, US bond investors should favor USD-denominated EM corporates over USD-denominated EM sovereigns and should favor both over US corporate bonds. Within the Aa credit tier, investors should favor USD-denominated EM sovereigns over USD-denominated EM corporates and should favor both over US corporate bonds. Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see US Bond Strategy / Global Fixed Income Strategy Weekly Report, “How To Re-Shape The Yield Curve Without Really Trying”, dated June 22, 2021. 2 Please see US Bond Strategy Weekly Report, “Lower For Longer, Then Faster Than You Think”, dated May 25, 2021. 3 We use the 3-year/10-year Treasury slope in place of the more widely tracked 2-year/10-year slope in our credit cycle research only because using the 3-year/10-year slope allows us to include more historical cycles in our analysis. 4 Please see US Bond Strategy Weekly Report, “That Uneasy Feeling”, dated March 30, 2021. 5 Please see page 33 of the US Bond Strategy Quarterly Chartpack, “Testing The Limits Of Transitory Inflation”, dated May 18, 2021. 6 The US Credit Index consists predominantly of US corporate bonds, but also some non-corporate credit such as: Sovereigns, Foreign Agencies, Domestic Agencies, Local Authority bonds and Supranationals. Fixed Income Sector Performance Recommended Portfolio Specification

BCA Research’s Geopolitical Strategy service recommends that on a tactical basis, investors stay defensive on global risk assets even if the cyclical outlook remains bright. The Xi administration’s re-centralization of policy has entailed mini-cycles of…

Highlights The US is withdrawing from the Middle East and South Asia and making a strategic pivot to Asia Pacific. The third quarter will see risks flare around Iran and the US rejoin the 2015 Iranian nuclear deal. The result is briefly negative for oil prices but the rise of Iran is a new geopolitical trend that will increase Middle Eastern risk over the long run. The geopolitical outlook is dollar bullish, while the macroeconomic outlook is getting less dollar-bearish due to China’s risk of over-tightening policy. Stay neutral USD and be wary of commodities and emerging markets in the third quarter. European political risk is bottoming. The German and French elections are at best minor risks. However, the continent is ripe for negative black swans, especially due to Russian aggression. Go tactically long global large caps and defensives. Feature Chart 1Three Key Views On Track (So Far)

Three Key Views On Track (So Far)

Three Key Views On Track (So Far)

We chose “No Return To Normalcy” as the theme of our 2021 outlook. While the COVID-19 vaccine promised economic recovery, we argued that normalization would create complacency regarding fundamental changes that have taken place in the geopolitical environment. A contradiction between an improving macroeconomic backdrop and a foreboding geopolitical backdrop would develop in 2021 and beyond. The “reflation trade” has begun to lose steam as we go to press. However, global recovery will still be the dominant story in the second half of the year as vaccination spreads. The question for the third quarter and the rest of the year is whether reflation will continue. As a matter of forecasting, we think it will. But as a matter of investment strategy, we are taking a more defensive stance until China relaxes economic policy. In our annual outlook we highlighted three key geopolitical views: (1) China’s headwinds, both at home and abroad (2) US détente with Iran and pivot to Asia (3) Europe’s opportunity. All three trends are broadly on track and can be illustrated by looking at equity performance in the relevant regions for the year so far: Chinese stocks sold off, UAE stocks rallied, and European stocks rallied (Chart 1). However, these trends are not exclusively tied to absolute equity performance. The most important question is what happens to global growth and the US dollar as these three key views continue. Stay Neutral On The Dollar It paid off for us to maintain a neutral stance on the dollar. True, the global recovery and exorbitant US trade and budget deficits are bearish for the dollar and bullish for other currencies. But the greenback’s “counter-trend bounce” is proving more formidable than many investors expected. The fundamentals of the American economy and global position remain strong. Since the outbreak of COVID-19, the US has secured its recovery with fiscal policy, maintained rule of law amid a contested election, innovated and distributed vaccines, benefited from more flexible social restrictions, refurbished global alliances, and put pressure on its geopolitical rivals. In essence, the combined effect of President Trump’s and Biden’s policies has been to make America “great again” (Chart 2). From a geopolitical perspective, the dollar is appealing. Chart 2Trump-Biden Make America Great Again?

Trump-Biden Make America Great Again?

Trump-Biden Make America Great Again?

In addition, the first two geopolitical views mentioned above – China’s headwinds and the US-Iran détente – imply a negative environment for China and the renminbi. The reason for the US to do a suboptimal deal with Iran, both in 2015 and 2021, is to reduce the risk of war and buy time to enable a strategic pivot to Asia Pacific. Three US presidents have been elected on the pledge to conclude the “forever wars” in the Middle East and South Asia. Biden is withdrawing US troops from Afghanistan in September. There can be little doubt Biden is committed to an Iran deal, which is supposed to free up the US’s hands (Chart 3). Meanwhile the US public and Congress are unified in their desire to better defend US interests against China’s economic and military rise. There has not yet been a stabilization of US-China policies. Biden is not likely to hold a summit with Chinese President Xi Jinping until late October at earliest – and that is a guess, not a confirmed summit. The Biden administration has completed its review of China policy and is maintaining the Trump administration’s hawkish posture, as predicted. The US and China may resume their strategic and economic dialogue at some point but it is impossible to go back to the status quo ante 2015. That was the year the US adopted a more confrontational stance toward China – a stance later supercharged by Trump’s election and trade tariffs. The hawkish consensus on China is one of the rare unifying factors in a deeply divided America. The Biden administration explicitly says the US-China relationship is now defined by “competition” instead of “engagement.”1 One exception to this neutral view on the dollar has been our decision to go long the Japanese yen and Swiss franc, which has not panned out so far. Our reasoning is that geopolitical risk will boost these currencies but otherwise the reduction of geopolitical risk will weigh on the dollar in the context of global growth recovery. So far geopolitical risk has remained subdued while the US dollar has outperformed. We are still sympathetic to these safe-haven currencies, however, as they are attractively valued as long as one expects geopolitical risks to materialize (Chart 4). Chart 3US Pivot To Asia Runs Through Iran

US Pivot To Asia Runs Through Iran

US Pivot To Asia Runs Through Iran

Our third key view, that EU was the real winner of the US election last year, remains on track. This is marginally positive for the euro at the expense of the dollar. Given the above points, we favor an equal-weighted basket of the euro and the dollar relative to the renminbi (Chart 5). Chart 4Safe-Haven Currencies Attractive

Safe-Haven Currencies Attractive

Safe-Haven Currencies Attractive

Chart 5Favor Euro And Dollar Over Renminbi

Favor Euro And Dollar Over Renminbi

Favor Euro And Dollar Over Renminbi

The geopolitical outlook is dollar-bullish. The macroeconomic outlook is dollar-bearish, except that China’s economy looks to slow down. We expect China to ease policy in the second half of the year but it may come late. We remain neutral dollar in the third quarter. Wait For China To Relax Policy July 1 marks the centenary of the Communist Party of China. The main thing investors should know is that the Communist Party predates China’s capitalist phase by sixty years. The party adopted capitalism to improve the economy – it never sacrificed its political or foreign policy goals. This poses a major geopolitical problem today because the Communist Party’s consolidation of power across Greater China, symbolized by Beijing’s revocation of Hong Kong’s special status in 2019, has convinced the western democracies that China is no longer compatible with the liberal world order. China launched a 13.8% of GDP monetary-and-fiscal stimulus over 2018-20 due to the trade war and COVID-19 pandemic. So the economy is stable for the hundredth anniversary celebration. The centenary goals are largely accomplished: GDP is larger, poverty is nearly extinguished, although urban incomes are still lagging (Chart 6). General Secretary Xi Jinping will mark the occasion with a speech. The speech will contribute to his governing philosophy, Xi Jinping Thought, a synthesis of communist Mao Zedong Thought and the pro-capitalist “socialism with Chinese characteristics” pioneered by General Secretary Deng Xiaoping in the 1980s-90s. The effect is to reassert Communist Party and central government primacy after the long period of decentralization that enabled China’s rapid growth phase. It is also to endorse an inward economic turn after the four-decade export-manufacturing boom. The Xi administration’s re-centralization of policy has entailed mini-cycles of tightening and loosening control over the economy. The administration leans against the country’s tendency to gorge itself on debt and grow at any cost – until it must lean the other way for fear of triggering a destabilizing slowdown. For this reason Beijing tightened policy proactively last year, producing a sharp drop in money, credit, and fiscal expansion in 2021 that now threatens to undermine the global recovery. By our measures, any further tightening will result in undershooting the regime’s money and credit targets, i.e. overtightening, and hence threaten to drag on the global recovery (Chart 7). Chart 6China's Communist Party Centenary Goals

China's Communist Party Centenary Goals

China's Communist Party Centenary Goals

Chart 7China Verges On Over-Tightening Policy

China Verges On Over-Tightening Policy

China Verges On Over-Tightening Policy

Overtightening would be a policy mistake with potentially disastrous consequences. So the base case should be that the government will relax policy rather than undermine the post-COVID recovery. However, investors cannot be confident about the timing. The 2015 financial turmoil and renminbi devaluation occurred because policymakers reacted too slowly. One reason to believe policy will be eased is that after July 1 the government will turn its attention to the twentieth national party congress in 2022, the once-in-five-years rotation of the Central Committee and Politburo. The party congress begins at the local level at the beginning of next year and culminates in the fall of 2022 with the national rotation of top party leaders. Xi Jinping was originally slated to step down in 2022. So he needs to squash any last-minute push against him by opposing factions of the party. He may have himself named chairman of the Communist Party, like Mao before him. Most importantly he will put his stamp on the “seventh generation” of China’s leaders by promoting his followers into key positions. All of this suggests that the Xi administration cannot risk triggering a recession, even if its preferences remain hawkish on economic policy. Policy easing could come as early as the end of July. As a rule of thumb, we have noticed that the Politburo’s July meeting on economic policy is often an inflection point, as was the case in 2007, 2015, 2018, and 2020 (Table 1). Some observers claim the April Politburo meeting already signaled an easing in policy, although we do not see that. If July clearly signals relaxation, global investors will cheer and emerging market assets and commodities will rise. Table 1China’s Politburo Often Hits Inflection Point On Economic Policy In July

Third Quarter Outlook 2021: The Pivot To Asia Runs Through Iran

Third Quarter Outlook 2021: The Pivot To Asia Runs Through Iran

Still we maintain a defensive posture going into the third quarter because we do not have a high level of confidence that policymakers will act preemptively. A market riot may precede and motivate the inflection point in policy. Also the negative impact of previous policy tightening will be felt in the third quarter. China plays and industrial metals are extremely vulnerable to further correction (Chart 8). Chart 8China Plays And Metals Vulnerable To Further Correction

China Plays And Metals Vulnerable To Further Correction

China Plays And Metals Vulnerable To Further Correction

The earliest occasion for a Biden-Xi summit comes at the end of October, as mentioned. While US-China talks will occur at some level, relations will remain fundamentally unstable. While a Biden-Xi summit may improve the atmosphere and lead to a new round of strategic and economic dialogue, or Phase Two trade talks, the fact is that the US is seeking to contain China’s rise and China is seeking to break out of the strictures of the US-led world order. The global elite and mainstream media will put a lot of emphasis on the post-Trump return to diplomatic “normalcy” and summits. But this is to overemphasize style at the expense of substance. Note that the positive feelings of the Biden-Putin summit on June 16 fizzled in less than a week when Russia allegedly dropped bombs in the path of a British destroyer in the Black Sea. The US and UK were training Ukraine’s military. Britain denies any bombs were dropped but Russia says next time they will hit their target. (More on this below.) This episode is instructive for US-China relations: summitry is overrated. China is building a sphere of influence and the US no longer believes dialogue alone is the answer. Tit-for-tat punitive measures and proxy battles in China’s neighboring areas, from the Korean peninsula to the Taiwan Strait to the South and East China Seas, are the new normal. Bottom Line: Tactically, stay defensive on global risk assets, especially China plays. Strategically, maintain a constructive outlook on the cycle given the global recovery and China’s need eventually to relax monetary and fiscal policy. US-Iran Deal Likely – Then The Real Trouble Starts The US will likely rejoin the 2015 Iranian nuclear deal (Joint Comprehensive Plan of Action) by August and pull out of its longest-ever war in Afghanistan in September. The US is wrapping up its “forever wars” to meet the demands of a war-weary public. Ironically, the long-term consequence is to create power vacuums that invite new geopolitical conflicts in the context of the US’s great power struggle with China and Russia. But for now a deal with Iran – once it is settled – reduces geopolitical risk by reducing the odds of military escalation in the region. The Iran talks are more significant than the Afghanistan pullout. We are confident in a deal because Biden can rejoin the 2015 deal unilaterally – it was never approved by the US Senate as a formal treaty. The Iranians will not support any militant action so aggressive as to scupper a deal that offers them the chance of reviving their economy at a critical time in the regime’s history. Reviving the deal poses a downside risk for oil prices in the third quarter though not over the long run. It is negative in the short run because investors will have to price not only Iran’s current and future production (Chart 9) but also any resulting loss of OPEC 2.0 discipline. Brent crude is trading at $76 per barrel as we go to press, above the $65-$70 per barrel average that our Commodity & Energy Strategy service expects to see over the coming five years (Chart 10). Chart 9Iran's Oil Production Will Return

Iran's Oil Production Will Return

Iran's Oil Production Will Return

Chart 10Brent Price Faces Short-Term Downside Risk From Iranian Crude

Brent Price Faces Short-Term Downside Risk From Iranian Crude

Brent Price Faces Short-Term Downside Risk From Iranian Crude