Emerging Markets

Highlights The ongoing transition to a post-pandemic state and fiscal policy are either positive or net-neutral for risky asset prices. Fiscal thrust will turn to fiscal drag over the coming year, but the negative impact this will have on goods spending will likely be offset by a significant improvement in services spending, and thus is not likely to cause a concerning slowdown in overall economic activity. A modestly hawkish shift in the outlook for monetary policy is likely over the coming year, potentially occurring over the late summer or early fall in response to outsized jobs growth. However, such a shift is not likely to become a negative driver for risky asset prices over the coming 6-12 months, barring a major rise in market expectations for the neutral rate of interest. This may very well occur once the Fed begins to raise interest rates, but not likely before. Investors should overweight risky assets within a multi-asset portfolio, and fixed-income investors should maintain a below-benchmark duration position. We continue to favor value over growth on a 6-12 month time horizon, although growth may outperform in the near term. A bias toward value over the coming year supports an overweight stance toward global ex-US equities, and an overall pro-risk stance favors bearish US dollar bets. Feature Three factors continue to drive our global macroeconomic outlook and our cyclical investment recommendations. The first factor is our assessment of the global progress that is being made on the path to a post-pandemic state, and the return to pre-COVID economic conditions; the second is the likely contribution to growth from fiscal policy over the coming year; and the third is the outlook for monetary policy and whether or not monetary conditions will remain stimulative for both economic activity and financial markets. If the world continues to progress meaningfully on the path to a post-pandemic state, and if the impact of fiscal and monetary policy remains in line with market expectations, then we see no reason to alter our recommended investment stance. Equity market returns will be modest over the coming 6 to 12 months in this scenario given how significantly stocks have rebounded from their low last year, but we would still expect stocks to outperform bonds and would generally be pro-cyclically positioned. We present below our assessment of these three factors and their potential to deviate from consensus expectations over the coming year, to determine their likely impact on economic activity and financial markets. The Ongoing Transition To A Post-Pandemic World Chart I-1Enormous Progress Has Been Made In The Fight Against COVID-19

Enormous Progress Has Been Made In The Fight Against COVID-19

Enormous Progress Has Been Made In The Fight Against COVID-19

Chart I-1 highlights that meaningful progress continues to be made in vaccinating the world's population against COVID-19. North America and Europe continue to lead the rest of the world based on the share of people who have received at least one dose, but South America continues to make significant gains, and recent data updates highlight that Asia and Oceania are also making meaningful progress. Africa is the clear laggard in the war against SARS-COV-2 and its variants, but progress there has been delayed, at least in part, by India’s export restrictions of the Oxford-AstraZeneca/COVISHIELD vaccine. This suggests that, while Africa will continue to lag, the share of Africans provided with a first dose of vaccine will begin to rise once India resumes its exports and deliveries to African countries under the COVAX program continue. If variants of the disease were not a source of concern, Chart I-1 would highlight that the full transition to a post-pandemic economy over the next several months would be near certain. However, as evidenced by the recent decision in the UK to postpone the lifting of COVID-19 restrictions by 4 weeks due to the spreading of the Delta variant, the global economy is not entirely out of the woods yet. Encouragingly, the delay in the UK genuinely appears to be temporary. Chart I-2 highlights that while the number of confirmed UK COVID-19 cases has been rising over the past month, the uptick in hospitalizations and fatalities has so far been quite muted. Importantly, the rise in hospitalizations appears to be occurring among those who have not yet been fully vaccinated, underscoring that variants of the disease are only truly concerning if they are vaccine-resistant. The evidence so far is that the Delta variant is more transmissible and may increase the risk of hospitalization, but that two doses of COVID-19 vaccine offer high protection. Of course, vaccines only offer protection if you get them, and evidence of vaccination hesitancy in the US is thus a somewhat worrying sign. Chart I-3 shows that the daily pace of vaccinations in the US has slowed significantly from mid-April levels, resulting in a slower rise in the share of the population that has received at least one dose (second panel). On this metric, the US has recently been outpaced by Canada, and the gap between the UK and the US is now widening. Germany and France are close behind the US and may surpass it soon. Chart I-2The UK Delay In Removing Restrictions Seems Genuinely Temporary

The UK Delay In Removing Restrictions Seems Genuinely Temporary

The UK Delay In Removing Restrictions Seems Genuinely Temporary

Chart I-3Recent Vaccination Progress In The US Has Been Underwhelming

Recent Vaccination Progress In The US Has Been Underwhelming

Recent Vaccination Progress In The US Has Been Underwhelming

Sadly, Chart I-4 highlights that there is a political dimension to vaccine hesitancy in the US. The chart shows that state by state vaccination rates as a share of the population are strongly predicted by the share of the popular vote for Donald Trump in the 2020 US presidential election. Admittedly, part of this relationship may also be capturing an urban/rural divide, with residents in less-dense rural areas (which typically support Republican presidential candidates) perhaps feeling a lower sense of urgency to become vaccinated against the disease. Chart I-4The US Politicization Of Vaccines Raises The Risk From COVID-19 Variants

July 2021

July 2021

But given the clear politicization that has already occurred over some pandemic control measures, such as the wearing of masks, Chart I-4 makes it difficult to avoid the conclusion that the same thing has occurred for vaccines. This is unfortunate, and seemingly raises the risk that the Delta variant may spread widely in red states over the coming several months, potentially delaying economic reopening, or risking the reintroduction of pandemic control measures. However, there are two counterarguments to this concern. First, non-vaccine immunity is probably higher in red than blue states, and CDC data suggest that this effect could be large. While this figure is still preliminary and subject to change (and likely will), the CDC estimates that only 1 out of 4.3 cases of COVID-19 were reported from February 2020 to March 2021. Taken at face value, this implies that there were approximately 115 million infections during that period, compared with under 30 million reported cases. That gap accounts for 25% of the US population, and given that red states were slower to implement pandemic control measures last year and their residents often more resistant to the measures, it stands to reason that a disproportionate share of unreported cases occurred in these states. Second, as noted above, the evidence thus far suggests that the Delta variant is not vaccine resistant, at least for those who are fully vaccinated. This is significant because if Delta were to spread widely in red states over the coming several months, the resulting increase in hospitalizations would likely convince many vaccine hesitant Americans to become vaccinated out of fear and self-interest – two powerfully motivating factors. Thus, the Delta variant may become a problem for the US in the fall, but if that occurs a solution is not far from sight. And, in other developed countries where vaccine hesitancy rates appear to be lower, it would seem that a new, vaccine-resistant variant of the disease would likely be required in order to cause a major disruption in the transition to a post-pandemic state. Such a variant could emerge, but we have seen no evidence thus far that one will before vaccination rates reach levels that would slash the odds of further widespread mutation. Fiscal Policy: Passing The Baton To Services Spending Chart I-5 highlights that US fiscal policy is set to detract from growth over the coming 6-12 months, reflecting the one-off nature of some of the fiscal response to the pandemic. This is true outside of the US as well, as Chart I-6 highlights that the IMF is forecasting a two percentage point increase in the Euro Area’s cyclically-adjusted primary budget balance, representing a significant amount of fiscal drag relative to the past two decades. Chart I-5Fiscal Thrust Will Eventually Turn To Fiscal Drag In The US…

July 2021

July 2021

Should investors be concerned about the impact of fiscal drag on advanced economies over the coming year? In our view, the answer is no. The reason is that much of the fiscal response in the US and Europe has been aimed at supporting income that has been lost due to a drastic reduction in services spending, which will continue to recover over the coming months as the effect of the pandemic continues to ebb. Chart I-7 underscores this point by highlighting the “gap” in US consumer goods and services spending relative to its pre-pandemic trend. The chart highlights that US goods spending is running well above what would be expected, whereas there is a sizeable gap in services spending (which accounts for approximately 70% of US personal consumption expenditures). Goods spending will likely slow as fiscal thrust turns to fiscal drag, but services spending will improve meaningfully – aided not just by a post-pandemic normalization in economic activity, but also by the sizeable amount of excess savings that US households have accumulated over the past year (Chart I-7, panel 2). Chart I-6... And In Europe

... And In Europe

... And In Europe

Chart I-7But Reduced Transfers Will Only Impact Spending On Goods, Not Services

But Reduced Transfers Will Only Impact Spending On Goods, Not Services

But Reduced Transfers Will Only Impact Spending On Goods, Not Services

While some of these savings have already been deployed to pay down debt and some may be permanently saved in anticipation of higher future taxes, the key point for investors is that the negative impact on goods spending from reduced fiscal thrust will be offset by a significant improvement in services spending, and thus is not likely to cause a concerning slowdown in overall economic activity. Monetary Policy: A Modestly Hawkish Shift Is Likely This leaves us with the question of whether or not monetary policy will become a negative driver for risky asset prices over the coming 6-12 months, which is especially relevant following last week’s FOMC meeting. The updated “dot plot” following the meeting shows that 7 of the 18 FOMC participants anticipate a rate hike in 2022, and the majority (13 members) expect at least one rate hike before the end of 2023, raising the median forecast for the Fed funds rate to 0.6% by the end of that year. Chart I-8 highlights that while 10-year Treasury yields remains mostly unchanged following the meeting, yields moved higher at the short-end and middle of the curve. Chart I-8The FOMC Meeting Resulted In Higher Short- And Mid-Term Yields

The FOMC Meeting Resulted In Higher Short- And Mid-Term Yields

The FOMC Meeting Resulted In Higher Short- And Mid-Term Yields

Investor fears that the Fed may shift in a significantly hawkish direction at some point over the next year have been far too focused on inflation, and far too little focused on employment. It is not a coincidence that the Fed’s guidance was updated following the May jobs report, which saw a stronger pace of jobs growth relative to April. Table I-1 updates our US Bond Strategy service’s calculations showing the average monthly nonfarm payroll growth that will be required for the unemployment rate to reach 3.5-4.5% assuming a full recovery in the participation rate, which is the range of the Fed’s NAIRU estimates. May’s payroll growth number of 560k implies that the Fed’s maximum employment criterion will be met sometime between June and September next year, if monthly payroll growth continues at that pace. Table I-1Calculating The Distance To Maximum Employment

July 2021

July 2021

Chart I-9Lighter Restrictions In Blue States Will Push Down The Unemployment Rate

Lighter Restrictions In Blue States Will Push Down The Unemployment Rate

Lighter Restrictions In Blue States Will Push Down The Unemployment Rate

It is currently difficult to assess with great confidence what average payroll growth will prevail over the coming year, but we noted in last month’s report that there were compelling arguments in favor of outsized jobs growth this fall.1 In addition to those points, we note the following: Blue states have generally been slower to reopen their economies, and Chart I-9 highlights that these states have consequently been slower to return to their pre-pandemic unemployment rate. Among blue states, California and New York are the largest by population, and it is notable that both states only lifted most COVID-19 restrictions on June 15 – including the wearing of masks in most settings. This implies that services jobs are likely to grow significantly in these states over the coming few months. Both consensus private forecasts as well as the Fed’s expectation for real GDP growth imply that the output gap will be closed by Q4 of this year (Chart I-10). These expectations appear to be reasonable, given the substantial amount of excess savings that have been accumulated by US households and the fact that monetary policy remains extremely stimulative. When the output gap turned positive during the last economic cycle, the unemployment rate was approximately 4% – well within the Fed’s NAIRU range. Chart I-10 also shows that the Fed’s 7% real GDP growth forecast for this year would put the output gap above its pre-pandemic level, when the unemployment rate stood at 3.5%. In fact, it is possible that annualized Q2 real GDP growth will disappoint current consensus expectations of 10%, due to the scarcity of labor supply (scarcity that will be eased by labor day when supplemental unemployment insurance benefit programs end). Were Q2 GDP to disappoint due to supply-side limitations, it would strengthen the view that job gains will be very strong this fall ceteris paribus, as it would highlight that real output per worker cannot rise meaningfully further in the short-term and that stronger growth later in the year will necessitate very large job gains. Chart I-11 highlights that US air travel and New York City subway ridership have already returned close to 75% and 50% of their pre-pandemic levels, respectively. Based on the trend over the past three months, the chart implies that air travel will return to its pre-pandemic levels by mid-October of this year, and New York City subway ridership by June 2022. This underscores that travel-related services employment will recover significantly in the fall, and that jobs in downtown cores will rebound as office workers progressively return to work. Chart I-10Expectations For Growth This Year Suggest A Rapid Decline In The Unemployment Rate

Expectations For Growth This Year Suggest A Rapid Decline In The Unemployment Rate

Expectations For Growth This Year Suggest A Rapid Decline In The Unemployment Rate

Chart I-11Services Employment Will Recover In The Fall

Services Employment Will Recover In The Fall

Services Employment Will Recover In The Fall

On the latter point, one major outstanding question affecting the outlook for monetary policy is the magnitude of the likely permanent impact of work from home policies on employment in central business districts. Fewer office workers commuting to downtown office locations suggests that some jobs in the leisure & hospitality, retail trade, professional & business services, and other services industries will never return or will be very slow to do so, arguing for a longer return to maximum employment (and the Fed’s liftoff date). We examine this question in depth in Section 2 of this month’s report, and find that the “stickiness” of work from home policies will likely cause permanent central business job losses on the order of 575k (or 0.35% of the February 2020 labor force). While this would be non-trivial, when compared with a pre-pandemic unemployment rate of 3.5%, WFH policies alone are not likely to cause a long-term deviation from the Fed’s maximum employment objective. Outsized jobs growth this fall, at a pace that quickly reduces the unemployment rate, argues for a first Fed rate hike that is even earlier than the market expects. Chart I-12 presents The Bank Credit Analyst service’s current assessment of the cumulative odds of the Fed’s liftoff date by quarter; we believe that it is likely that the Fed will have raised rates by Q3 of next year, and that a rate hike in the first half of 2022 is a possibility. These odds are slightly more aggressive than those presented by our fixed-income strategists in a recent Special Report,2 but are consistent with their view that the Fed will raise interest rates by the end of next year. Chart I-12The Bank Credit Analyst’s Assessment Of The Odds Of The First Rate Hike

July 2021

July 2021

The odds presented in Chart I-12 are also more hawkish than the Fed funds rate path currently implied by the OIS curve, meaning that we expect investors to be somewhat surprised by a shifting monetary policy outlook at some point over the coming year, potentially over the next 3-6 months. Payroll growth during the late summer and early fall will be a major test for the employment outlook, and is the most likely point for a hawkish shift in the market’s view of monetary policy. Is this likely to become a negative driver for risky asset prices over the coming 6-12 months? In our view, the answer is “probably not.” While investors tend to focus heavily on the timing of the first rate hike as monetary policy begins to tighten, the reality is that it is the least relevant factor driving the fair value of 10-year Treasury yields. Investor expectations for the pace of tightening and especially for the terminal Fed funds rate are far more important, and, while it is quite possible that expectations for the neutral rate of interest will eventually rise, it seems unlikely that this will occur before the Fed actually begins to raise interest rates given that most investors accept the secular stagnation narrative and the view that “R-star” is well below trend rates of growth (we disagree).3 Chart I-13 highlights the fair value path of 10-year Treasury yields until the end of next year, assuming a 2.5% terminal Fed funds rate, no term premium, and a rate hike pace of 1% per year. The chart highlights that while government bond yields are set to move higher over the coming 6-12 months, they are likely to remain between 2-2.5%. This would drop the equity risk premium to a post-2008 low (Chart I-14), which would further reduce the attractiveness of stocks relative to bonds. But we doubt that this would be enough of a decline to cause a selloff, and it would still imply a stimulative level of interest rates for households and firms. Chart I-1310-Year Yields Will Rise Over The Coming Year, But Not Sharply

10-Year Yields Will Rise Over The Coming Year, But Not Sharply

10-Year Yields Will Rise Over The Coming Year, But Not Sharply

Chart I-14Rising Yields Will Cause An Unwelcome But Contained Decline In The ERP

Rising Yields Will Cause An Unwelcome But Contained Decline In The ERP

Rising Yields Will Cause An Unwelcome But Contained Decline In The ERP

Investment Conclusions Among the three factors driving our global macroeconomic outlook and our cyclical investment recommendations, continued progress on the path toward a post-pandemic state and fiscal policy remain either positive or mostly neutral for risky assets. A potentially hawkish shift in the outlook for monetary policy this fall remains the chief risk, but we expect the rise in bond yields over the coming year to remain well-contained barring a sea change in investor expectations for the terminal Fed funds rate – which we believe is unlikely to occur before the Fed begins to raise interest rates. Consequently, we continue to recommend that investors should overweight risky assets within a multi-asset portfolio, and that fixed-income investors should maintain a below-benchmark duration position. We expect modest absolute returns from global equities, but even mid-single digit returns are likely to beat those from long-dated government bonds and cash positions. While value stocks may underperform growth stocks over the coming 3-4 months,4 rising bond yields over the coming year will ultimately favor value stocks and will likely weigh on elevated tech sector (and therefore growth stock) valuations (Chart I-15). Chart I-16 highlights that the attractiveness of US value versus growth is meaningfully less compelling for the S&P 500 Citigroup indexes, suggesting that investors should continue to favor MSCI-benchmarked value over growth positions over a 6-12 month time horizon.5 Chart I-15Value Is Extremely Cheap

Value Is Extremely Cheap

Value Is Extremely Cheap

Chart I-16Value Vs. Growth: The Benchmark Matters

Value Vs. Growth: The Benchmark Matters

Value Vs. Growth: The Benchmark Matters

The likely outperformance of value versus growth also has implications for regional allocation within a global equity portfolio. The US is significantly overweight broadly-defined technology relative to global ex-US stocks, and financials – which are overrepresented in value indexes – have already meaningfully outperformed in the US this year compared with their global peers and are now rolling over (Chart I-17). This underscores that investors should favor ex-US stocks over the coming year, skewed in favor of DM ex-US given that China’s credit impulse continues to slow (Chart I-18). Chart I-17Favor Global Ex-US Stocks Over The Coming Year

Favor Global Ex-US Stocks Over The Coming Year

Favor Global Ex-US Stocks Over The Coming Year

Chart I-18Concentrate Global Ex-US Exposure In Developed Markets

Concentrate Global Ex-US Exposure In Developed Markets

Concentrate Global Ex-US Exposure In Developed Markets

Finally, global ex-US stocks also tend to outperform when the US dollar is falling, and we would recommend that investors maintain a short dollar position on a 6-12 month time horizon despite the recent bounce in the greenback. Chart I-19 highlights that the dollar remains strongly negatively correlated with global equity returns, and that the dollar’s performance over the past year has been almost exactly in line with what one would have expected given this relationship. Thus, a bullish view toward global stocks implies both US dollar weakness and global ex-US outperformance over the coming year. Chart I-19A Bullish View Towards Global Stocks Implies A Dollar Bear Market

A Bullish View Towards Global Stocks Implies A Dollar Bear Market

A Bullish View Towards Global Stocks Implies A Dollar Bear Market

Jonathan LaBerge, CFA Vice President The Bank Credit Analyst June 24, 2021 Next Report: July 29, 2021 II. Work From Home “Stickiness” And The Outlook For Monetary Policy Work from home policies, originally designed as emergency measures in the early phase of the COVID-19 pandemic, are likely to be “sticky” in a post-pandemic world. This will negatively impact the labor market in central business districts, via reduced spending on services by office workers. The potential impact of working from home is often cited as an example of what is likely to be a lasting and negative effect on jobs growth, but we find that it is not likely to be a barrier to the labor market returning to the Fed’s assessment of “maximum employment.” The size of the impact depends importantly on whether employee preferences or employer plans for WFH prevail, but our sense is that the latter is more likely. A weaker pace of structures investment in response to elevated office vacancy rates will likely have an even smaller impact on growth than the effect of reduced central business district services employment. The contribution to growth from structures investment has been small over the past few decades, office building construction is a small portion of overall nonresidential structures, and there are compelling arguments that the net stock of office structures will stay flat, rather than decline. Our analysis suggests that job growth over the coming year could be even stronger than the Fed and investors expect, possibly resulting in a first rate hike by the middle of next year. This would be earlier than we currently anticipate, but it underscores that fixed-income investors should remain short duration on a 6-12 month time horizon, and that equity investors should favor value over growth positions beyond the coming 3-4 months. The outlook for US monetary policy over the next 12 to 18 months depends almost entirely on the outlook for employment. Many investors are focused on the potential for elevated inflation to force the Fed to raise interest rates earlier than it currently anticipates, but it is the progress in returning to “maximum employment” that will determine the timing of the first Fed rate hike – and potentially the speed at which interest rates rise once policy begins to tighten. In this report, we estimate the extent to which the “stickiness” of working from home (WFH) policies and practices could leave a lasting negative impact on the US labor market. We noted in last month's report that a large portion of the employment gap relative to pre-pandemic levels can be traced to the leisure & hospitality and professional and business services industries, both of which – along with retail employment – stand to be permanently impaired if the office worker footprint is much lower in a post-COVID world.6 Using employee surveys and a Monte Carlo approach, we present a range of estimates for the permanent impact of WFH policies on the unemployment rate, and separately examine the potential for lower construction of office properties to weigh on growth. We find that the impact of reduced office building construction is likely to be minimal, and that WFH policies may structurally raise the unemployment rate by 0.3 to 0.4%. While non-trivial, when compared with a pre-pandemic unemployment rate of 3.5%, WFH policies alone are not likely to cause a long-term deviation from the Fed’s maximum employment objective. Relative to the Fed’s expectations of a strong, lasting impact on the labor market from the pandemic, this suggests that job growth over the coming year could be even stronger than the Fed and investors expect, possibly resulting in a first rate hike by the middle of next year. This would be earlier than we currently anticipate, but it underscores that fixed-income investors should remain short duration on a 6-12 month time horizon, and that equity investors should favor value over growth positions beyond the coming 3-4 months (a period that may see outperformance of the latter). Quantifying The Labor Market Impact Of The New Normal For Work In a January paper, Barrero, Bloom, and Davis (“BBD”) presented evidence arguing why working from home will “stick.” The authors surveyed 22,500 working-age Americans across several survey “waves” between May and December 2020, and asked about both their preferences and their employer’s plans about working from home after the pandemic. Chart II-1 highlights that the desired amount of paid work from home days (among workers who can work from home) reported by the survey respondents is to approximately 55% of a work week, suggesting that a dramatic reduction in office presence would likely occur if post-pandemic WFH policies were set fully in accordance with worker preferences. Chart II-1Employee Preferences Imply A Dramatic Reduction In Post-COVID Office Presence

July 2021

July 2021

However, Table II-1 highlights that employer plans for work from home policies are meaningfully different than those of employees. The table highlights that employers plan for employees to work from home for roughly 22% of paid days post-pandemic, which essentially translates to one day per week on average.7 BBD noted that CEOs and managers have cited the need to support innovation, employee motivation, and company culture as reasons for employees’ physical presence. Managers believe physical interactions are important for these reasons, but employees need only be on premises for about three to four days a week to achieve this. Table II-1 also shows that employers plan to allow higher-income employees more flexibility in terms of working from home, and less flexibility to employees whose earnings are between $20-50k per year. Table II-1Employer Plans, However, Imply Less Working From Home Than Employees Prefer

July 2021

July 2021

Based on the survey results, BBD forecast that expenditure in major cities such as Manhattan and San Francisco will fall on the order of 5 to 10%. In order to understand the national labor market impact of work from home policies and what implications this may have on monetary policy, we scale up BBD’s calculations using a Monte Carlo approach that incorporates estimate ranges for several factors: The percent of paid days now working from home for office workers The amount of money spent per week by office workers in central business districts (“CBDs”) The number of total jobs in CBDs The percent of CBD jobs in industries likely to be negatively impacted by reduced office worker expenditure The average weekly earnings of affected CBD workers The average share of business revenue not attributable to strictly variable expenses The percent of affected jobs likely to be recovered outside of CBDs Our approach is as follows. First, we calculate the likely reduction in nationwide CBD spending from reduced office worker presence by multiplying the likely percent of paid days now permanently working from home by the number of total jobs in CBDs and the average weekly spending of office workers. This figure is then increased due to the estimated acceleration in net move outs from principal urban centers in 2020 (Chart II-2); we assume a 5% savings rate and an average annual salary of $50k for these resident workers, and assume that all of their spending occurred within CBDs. We also assume that roughly 50% of jobs connected to this spending are recovered. Chart II-2Fewer Residents Will Also Lower Spending In Central Business Districts

July 2021

July 2021

Then, we calculate the gross number of jobs lost in leisure & hospitality, retail trade, and other services by multiplying this estimate of lost spending by an estimate of non-variable costs as a share of revenue for affected industries, and dividing the result by average weekly earnings of affected employees. For affected CBD employees in the administrative and waste services industry, we simply assume that the share of jobs lost matches the percent of paid days now permanently working from home. Finally, we adjust the number of jobs lost by multiplying by 1 minus an assumed “recovery” rate, given that some of the reduction in spending in CBDs will simply be shifted to areas near remote workers’ residences. We assume a slightly lower recovery rate for lost jobs in the administrative and waste services industry. Table II-2 highlights the range of outcomes for each variable used in our simulation, and Charts II-3 and II-4 present the results. The charts highlight that the distribution of outcomes based on employer WFH intensions suggest high odds that nationwide job losses in CBDs due to reduced office worker presence will not exceed 400k. Based on average employee preferences, that number rises to roughly 800-900k. Table II-2The Factors Affecting Permanent Central Business District Job Losses

July 2021

July 2021

Chart II-3The Probability Distribution Of CBD Jobs Lost…

July 2021

July 2021

Chart II-4…Based On Our Monte Carlo Approach

July 2021

July 2021

This raises the question of whether employer plans or employee preferences for WFH arrangements will prevail. Our sense is that it will be closer to the former, given that we noted above that employer WFH plans are the least flexible for employees whose earnings are between $20-50k per year (who are presumably employees who have less ability to influence the policy of firms). Chart II-5 re-presents the projected job losses shown in Chart II-4 as a share of the February 2020 labor force, along with a probability-weighted path that assumes a 75% chance that employer WFH plans will prevail. The chart highlights that WFH arrangements would have the effect of raising the unemployment rate by approximately 0.35%. However, relative to a pre-pandemic starting point of 3.5%, this would raise the unemployment rate to a level that would still be within the Fed’s NAIRU estimates (Chart II-6). Therefore, the “stickiness” of WFH arrangements alone do not seem to be a barrier to the labor market returning to the Fed’s assessment of “maximum employment,” suggesting that the conditions for liftoff may be met earlier than currently anticipated by investors. Chart II-5CBD Job Losses Will Not Be Trivial, But They Will Not Be Enormous

July 2021

July 2021

Chart II-6Sticky WFH Policies Will Not Prevent A Return To Maximum Employment

Sticky WFH Policies Will Not Prevent A Return To Maximum Employment

Sticky WFH Policies Will Not Prevent A Return To Maximum Employment

The Impact Of Lower Office Building Construction A permanently reduced office footprint could also conceivably impact the US economy through reduced nonresidential structures investment, as builders of commercial real estate cease to construct new office towers in response to expectations of a long-lasting glut. However, several points highlight that the negative impact on growth from US office tower construction will be even smaller than the CBD employment impact of reduced office worker presence that we noted above. First, Chart II-7 highlights the overall muted impact that nonresidential building investment has had on real GDP growth by removing the contribution to growth from nonresidential structures and for overall nonresidential investment. The chart clearly highlights that the historically positive contribution to real US output from capital expenditures over the past four decades has come from investment in equipment and intellectual property products, not from structures. Chart II-8 echoes this point, by highlighting that US real investment in nonresidential structures has in fact been flat since the early-1980s, contributing positively and negatively to growth only on a cyclical basis (not on a structural basis). Chart II-7Structures Have Not Contributed Significantly To US Growth For Some Time

Structures Have Not Contributed Significantly To US Growth For Some Time

Structures Have Not Contributed Significantly To US Growth For Some Time

Chart II-8Nonresidential Structures Investment Has Been Flat For Four Decades

Nonresidential Structures Investment Has Been Flat For Four Decades

Nonresidential Structures Investment Has Been Flat For Four Decades

Second, Table II-3 highlights that office properties make up a small portion of investment in private nonresidential structures. In 2019, nominal investment in office structures amounted to $85 billion, compared with $630 billion in overall structures investment, meaning that office properties amounted to just 13% of structures investment. Table II-3Office Structures Investment Is A Small Share Of Total Structures Investment

July 2021

July 2021

Table II-4Conceivably, Vacant Office Properties Could Be Converted To Luxury Residential Units

July 2021

July 2021

Third, it is true that investment is a flow and not a stock variable, meaning that, if the net stock of office buildings were to fall as a result from WFH policies, then the US economy would see a potentially persistently negative rate of growth from nonresidential structures (which would constitute a drag on growth). But if the net stock were instead to remain flat, then gross office property investment should equal the depreciation of those structures. The second column of Table II-3 highlights that current-cost depreciation of office structures was $53 billion in 2019 (versus nominal gross investment of $85 billion). Had office property investment been ~$30 billion lower in 2019, it would have reduced nominal GDP by a mere 14 basis points (resulting in an annual growth rate of 3.84%, rather than 3.98%). Fourth, there is good reason to believe that the net stock of office properties will stay flat, as the economics of converting offices to luxury housing units (whose demand is not substantially affected by factors such as commuting) – either fully or partially into mixed-use buildings – appear to be plausible. Table II-4 highlights that the average annual asking rent for office space per square foot in Manhattan was $73.23 in Q1 2021, and that the recent median listing home price per square foot is roughly $1,400. In a frictionless world where office space could be instantly and effortlessly sold as residential property, existing prices would imply a healthy (gross) rental yield of 5.2%. Thoughts On The Future Of Office Properties Of course, reality is far from frictionless. There are several barriers that will slow office-to-residential conversion as well as construction costs, which will meaningfully lower the net value of existing office real estate in large central business districts such as Manhattan. In a recent article in the Washington Post, Roger K. Lewis, retired architect and Professor Emeritus of Architecture at the University of Maryland, College Park, detailed several of these technical barriers (which we summarize below).8 Office buildings are typically much wider than residential buildings, the latter usually being 60 to 65 feet in width in order to enable windows and natural light in living/dining rooms and bedrooms. This suggests that office-to-residential conversion might require modifying the basic structure of office buildings, including cutting open parts of roof and floor plates on upper building levels to bring natural light into habitable and interior rooms, and other costly structural modifications to address the additional plumbing and infrastructure that will be needed. Lewis noted that floor-to-floor dimensions are typically larger in office buildings, which is beneficial for office-to-residential conversion because increased room heights augments the sense of space and openness, while allowing natural light to penetrate farther into the apartment. It also allows for extra space to place needed additional building infrastructure, such as sprinkler pipes, electrical conduits, light fixtures, and air ducts. But unique apartment layouts are often needed to use available floor space effectively in an office-to-residential conversion, which will increase design costs and raise the risk that nonstandard layouts may result in unforeseen quality-of-living problems that will necessitate additional future construction to correct. Zoning regulations and building code constraints will likely add another layer of costs to office-to-housing conversions, as these rules are written for conventional buildings, meaning that special exceptions or even regulatory changes are likely to be required. So it is clear that the process of converting office space to residential property will be a costly endeavor for office tower owners, which will likely reduce the net present value of these properties relative to pre-pandemic levels. But; this process appears to be feasible and, when faced with the alternative of persistently high vacancy rates and lost revenue, our sense is that office tower owners will choose this route – thus significantly reducing the likelihood that the growth in national gross investment in office properties will fall below the rate of depreciation. In addition, the trend in suburban and CBD office property prices suggests that there are two other possible alternatives to widespread office-to-residential conversion that would also argue against a significant and long-lasting decline in office structures investment. Chart II-9 highlights that the average asking rent has already fallen significantly in most Manhattan submarkets, and Chart II-10 highlights that suburban office prices are accelerating and rising at the strongest pace relative to CBD office prices over the past two decades, possibly in response to increased demand for workspace that is closer to home for many workers who previously commuted to CBDs. Chart II-9Working From The Office Is Getting Cheaper

July 2021

July 2021

Chart II-10Suburban Offices Are Getting More Expensive

Suburban Offices Are Getting More Expensive

Suburban Offices Are Getting More Expensive

Thus, the first alternative outcome to CBD office-to-residential conversion is that an increase in suburban office construction offsets the negative impact of outright reductions in CBD office investment if residential conversions prove to be too costly or too technically challenging. The second alternative is that owners of CBD office properties “clear the market” by dramatically cutting rental rates even further, to alter the cost/benefit calculation for firms planning permissive WFH policies. We doubt that existing rents reflect the extent of vacancies in large cities such as Manhattan, so we would expect further CBD office price declines in this scenario. But if owners of centrally-located office properties face significant conversion costs and a decline in the net present value of these buildings is unavoidable and its magnitude uncertain, owners may choose to cut prices drastically as the simpler solution. Investment Conclusions Holding all else equal, the fact that owners of CBD office properties are likely to experience some permanent decline in the value of these real estate assets is not a positive development for economic activity. But these losses will be experienced by firms, investors, and ultra-high net worth individuals with strong marginal propensities to save, suggesting that the economic impact from this shock will be minimal. And as we highlighted above, a decline in the pace of gross office building investment to the depreciation rate will have a minimal impact on the overall economy. This leaves the likely impact on CBD employment as the main channel by which WFH policies are likely to affect monetary policy. As we noted above and as discussed in Section 1 of our report, the Fed is now focused entirely on the return of the labor market to maximum employment, which we interpret as an unemployment rate within the range of the Fed’s NAIRU estimates (3.5% - 4.5%) and a return to a pre-pandemic labor force participation rate. Chart II-11On A One-Year Time Horizon, Favor Value Over Growth

On A One-Year Time Horizon, Favor Value Over Growth

On A One-Year Time Horizon, Favor Value Over Growth

Our analysis indicates that WFH policies may structurally raise the unemployment rate by 0.3 to 0.4%. While non-trivial, when compared with a pre-pandemic unemployment rate of 3.5%, this suggests that WFH policies alone are not likely to cause a long-term deviation from the Fed’s maximum employment objective. The implication is that job growth over the coming year could be even stronger than the Fed and investors expect, which could mean that the Fed may begin lifting rates by the middle of next year barring a major disruption in the ongoing transition to a post-pandemic world. This is earlier than we currently expect, but the fact that it would also be earlier than what is currently priced into the OIS curve underscores that fixed-income investors should remain short duration on a 6-12 month time horizon. In addition, as noted in Section 1 of our report, while value stocks may underperform growth stocks over the coming 3-4 months,9 rising bond yields over the coming year will ultimately favor value stocks and will likely weigh on elevated tech sector valuations. Chart II-11 highlights that the relative valuation of growth stocks remains above its pre-pandemic starting point (Chart II-11), suggesting that investors should continue to favor MSCI-benchmarked value over growth positions over a 6-12 month time horizon. Finally, as also noted in Section 1 of our report, we do not expect rising bond yields to prevent stock prices from grinding higher over the coming year, unless investor expectations for the terminal fed funds rate move sharply higher – an event that seems unlikely, although not impossible, before monetary policy actually begins to tighten. Jonathan LaBerge, CFA Vice President The Bank Credit Analyst III. Indicators And Reference Charts BCA’s equity indicators highlight that the “easy” money from expectations of an eventual end to the pandemic have already been made. Our technical, valuation, and sentiment indicators are very extended, highlighting that investors should expect positive but more modest returns from stocks over the coming 6-12 months. Our monetary indicator has aggressively retreated from its high last year, reflecting a meaningful recovery in government bond yields since last August. The indicator still remains above the boom/bust line, however, highlighting that monetary policy remains supportive for risky asset prices. Forward equity earnings already price in a complete earnings recovery, but for now there is no meaningful sign of waning forward earnings momentum. Net revisions remain very strong, and positive earnings surprises have risen to their highest levels on record. Within a global equity portfolio, there has been a modest tick down in global ex-US equity performance, driven by a rally in growth stocks (which may persist for a few months). EM stocks had previously dragged down global ex-US performance, and they continue to languish. A bias towards value stocks on a 1-year time horizon means that investors should still favor ex-US stocks over the coming year, skewed in favor of DM ex-US given that China’s credit impulse continues to slow. The US 10-Year Treasury yield has trended modestly lower since mid-March, after having risen to levels that were extremely technically stretched. Despite this pause, our valuation index highlights that bonds are still expensive, and we expect that yields will move higher over the cyclical investment horizon if employment growth in Q3/Q4 implies a faster return to maximum employment than currently projected by the Fed. We expect the rise to be more modest than our valuation index would imply, but we would still recommend a short duration stance within a fixed-income portfolio. The extreme rise in some commodity prices over the past several months is beginning to ease. Lumber prices have fallen close to 50% from their recent high, whereas industrial metals and agricultural prices are down roughly 5% and 17%, respectively. We had previously argued that a breather in commodity prices was likely at some point over the coming several months, and we would expect further declines as supply chains normalize, labor supply recovers, and Chinese demand for metals slows. US and global LEIs remain in a solid uptrend, and global manufacturing PMIs are strong. Our global LEI diffusion index has declined significantly, but this likely reflects the outsized impact of a few emerging market countries (whose vaccination progress is still lagging). Strong leading and coincident indicators underscore that the global demand for goods is robust, and that output is below pre-pandemic levels in most economies because of very weak services spending. The latter will recover significantly later this year, as social distancing and other pandemic control measures disappear. EQUITIES: Chart III-1US Equity Indicators

US Equity Indicators

US Equity Indicators

Chart III-2Willingness To Pay For Risk

Willingness To Pay For Risk

Willingness To Pay For Risk

Chart III-3US Equity Sentiment Indicators

US Equity Sentiment Indicators

US Equity Sentiment Indicators

Chart III-4US Stock Market Breadth

US Stock Market Breadth

US Stock Market Breadth

Chart III-5US Stock Market Valuation

US Stock Market Valuation

US Stock Market Valuation

Chart III-6US Earnings

US Earnings

US Earnings

Chart III-7Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

Chart III-8Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

Global Stock Market And Earnings: Relative Performance

FIXED INCOME: Chart III-9US Treasurys And Valuations

US Treasurys And Valuations

US Treasurys And Valuations

Chart III-10Yield Curve Slopes

Yield Curve Slopes

Yield Curve Slopes

Chart III-11Selected US Bond Yields

Selected US Bond Yields

Selected US Bond Yields

Chart III-1210-Year Treasury Yield Components

10-Year Treasury Yield Components

10-Year Treasury Yield Components

Chart III-13US Corporate Bonds And Health Monitor

US Corporate Bonds And Health Monitor

US Corporate Bonds And Health Monitor

Chart III-14Global Bonds: Developed Markets

Global Bonds: Developed Markets

Global Bonds: Developed Markets

Chart III-15Global Bonds: Emerging Markets

Global Bonds: Emerging Markets

Global Bonds: Emerging Markets

CURRENCIES: Chart III-16US Dollar And PPP

US Dollar And PPP

US Dollar And PPP

Chart III-17US Dollar And Indicator

US Dollar And Indicator

US Dollar And Indicator

Chart III-18US Dollar Fundamentals

US Dollar Fundamentals

US Dollar Fundamentals

Chart III-19Japanese Yen Technicals

Japanese Yen Technicals

Japanese Yen Technicals

Chart III-20Euro Technicals

Euro Technicals

Euro Technicals

Chart III-21Euro/Yen Technicals

Euro/Yen Technicals

Euro/Yen Technicals

Chart III-22Euro/Pound Technicals

Euro/Pound Technicals

Euro/Pound Technicals

COMMODITIES: Chart III-23Broad Commodity Indicators

Broad Commodity Indicators

Broad Commodity Indicators

Chart III-24Commodity Prices

Commodity Prices

Commodity Prices

Chart III-25Commodity Prices

Commodity Prices

Commodity Prices

Chart III-26Commodity Sentiment

Commodity Sentiment

Commodity Sentiment

Chart III-27Speculative Positioning

Speculative Positioning

Speculative Positioning

ECONOMY: Chart III-28US And Global Macro Backdrop

US And Global Macro Backdrop

US And Global Macro Backdrop

Chart III-29US Macro Snapshot

US Macro Snapshot

US Macro Snapshot

Chart III-30US Growth Outlook

US Growth Outlook

US Growth Outlook

Chart III-31US Cyclical Spending

US Cyclical Spending

US Cyclical Spending

Chart III-32US Labor Market

US Labor Market

US Labor Market

Chart III-33US Consumption

US Consumption

US Consumption

Chart III-34US Housing

US Housing

US Housing

Chart III-35US Debt And Deleveraging

US Debt And Deleveraging

US Debt And Deleveraging

Chart III-36US Financial Conditions

US Financial Conditions

US Financial Conditions

Chart III-37Global Economic Snapshot: Europe

Global Economic Snapshot: Europe

Global Economic Snapshot: Europe

Chart III-38Global Economic Snapshot: China

Global Economic Snapshot: China

Global Economic Snapshot: China

Jonathan LaBerge, CFA Vice President The Bank Credit Analyst Footnotes 1 Please see The Bank Credit Analyst "June 2021," dated May 27, 2021, available at bca.bcaresearch.com 2 Please see US Bond Strategy/Global Fixed Income Strategy Special Report "A Central Bank Timeline For The Next Two Years," dated June 1, 2021, available at usbs.bcaresearch.com 3 Please see The Bank Credit Analyst Special Report "R-star, And The Structural Risk To Stocks," dated March 31, 2021, available at bca.bcaresearch.com 4 Please see US Equity Strategy "Rotate Into Growth Stocks, Be Granular In The Selection Of Cyclicals," dated June 14, 2021, available at uses.bcaresearch.com 5 For a discussion of the differences in value and growth benchmarks, please see Global Asset Allocation Special Report “Value? Growth? It Really Depends!” dated September 19, 2019, available at gaa.bcaresearch.com 6 Please see The Bank Credit Analyst "June 2021," dated May 27, 2021, available at bca.bcaresearch.com 7 Readers should note that the desired share of paid work from home days post-COVID among employees is shown to be lower in Table II-1 than what is implied by Chart II-1 on a weighted-average basis. This is due to the fact that Table II-1 excludes responses from the May 2020 survey wave, because the authors did not ask about employer intensions during that wave. This underscores that the average desired number of paid days working from home declined somewhat over time, and thus argues for the value shown in Table II-1 as the best estimate for employee preferences. 8 Roger K. Lewis, “Following pandemic, converting office buildings into housing may become new ‘normal,’ Washington Post, April 3, 2021. 9 Please see US Equity Strategy "Rotate Into Growth Stocks, Be Granular In The Selection Of Cyclicals," dated June 14, 2021, available at uses.bcaresearch.com

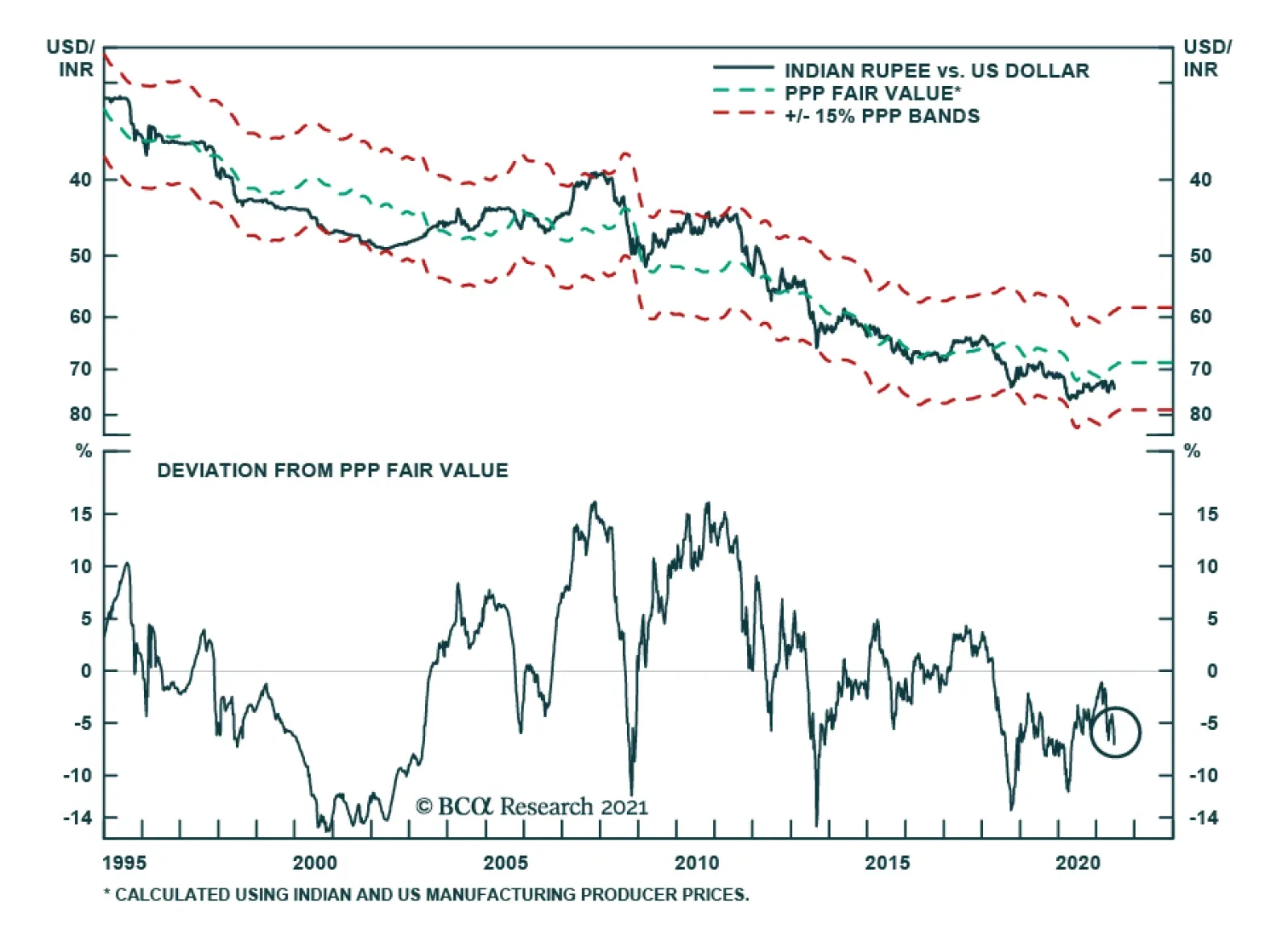

According to BCA Research’s Emerging Markets Strategy service, the Indian rupee is about 7% cheaper than its fair value versus the US dollar. The concept of purchasing power parity (PPP) theorizes that the currency of an economy with higher inflation will…

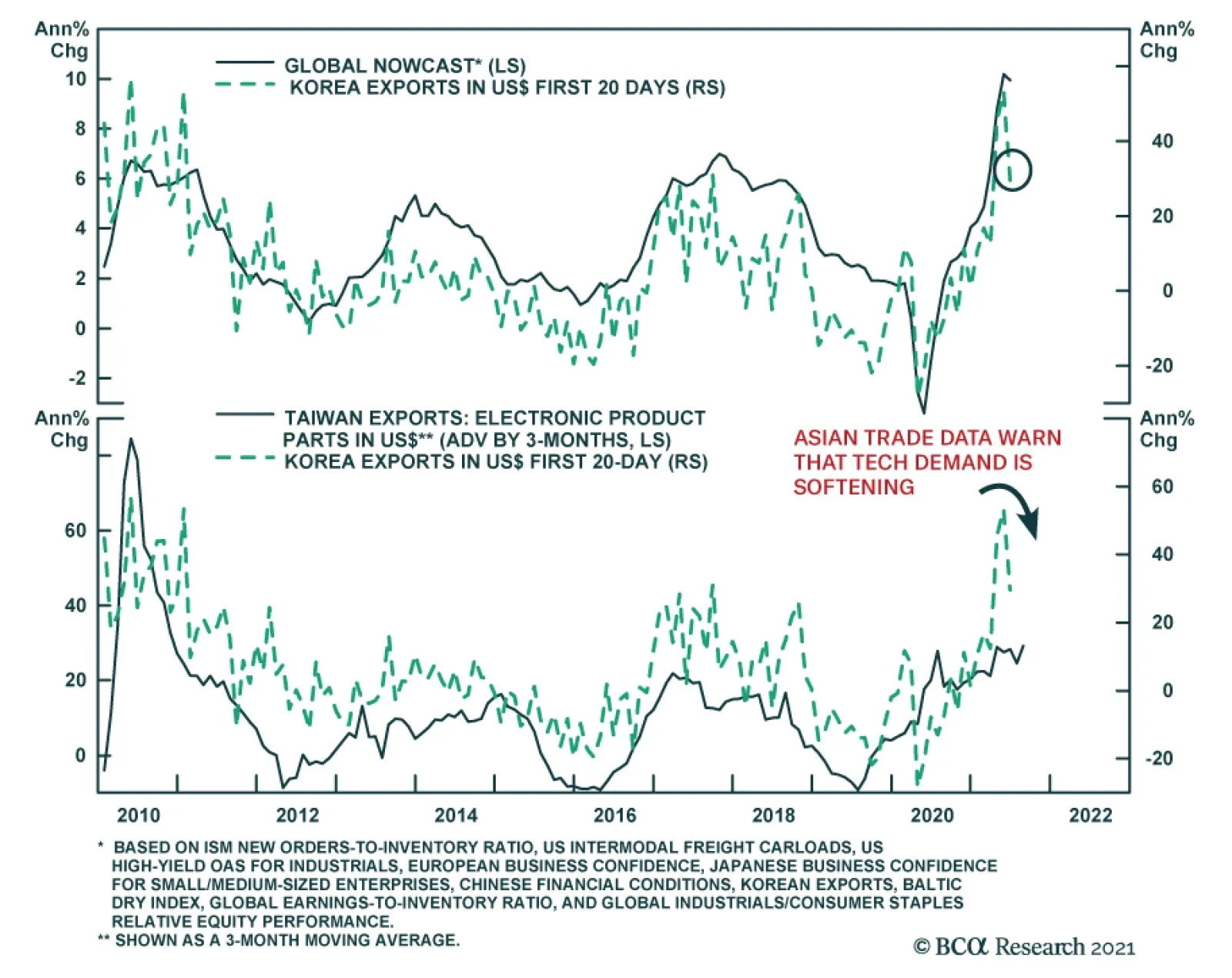

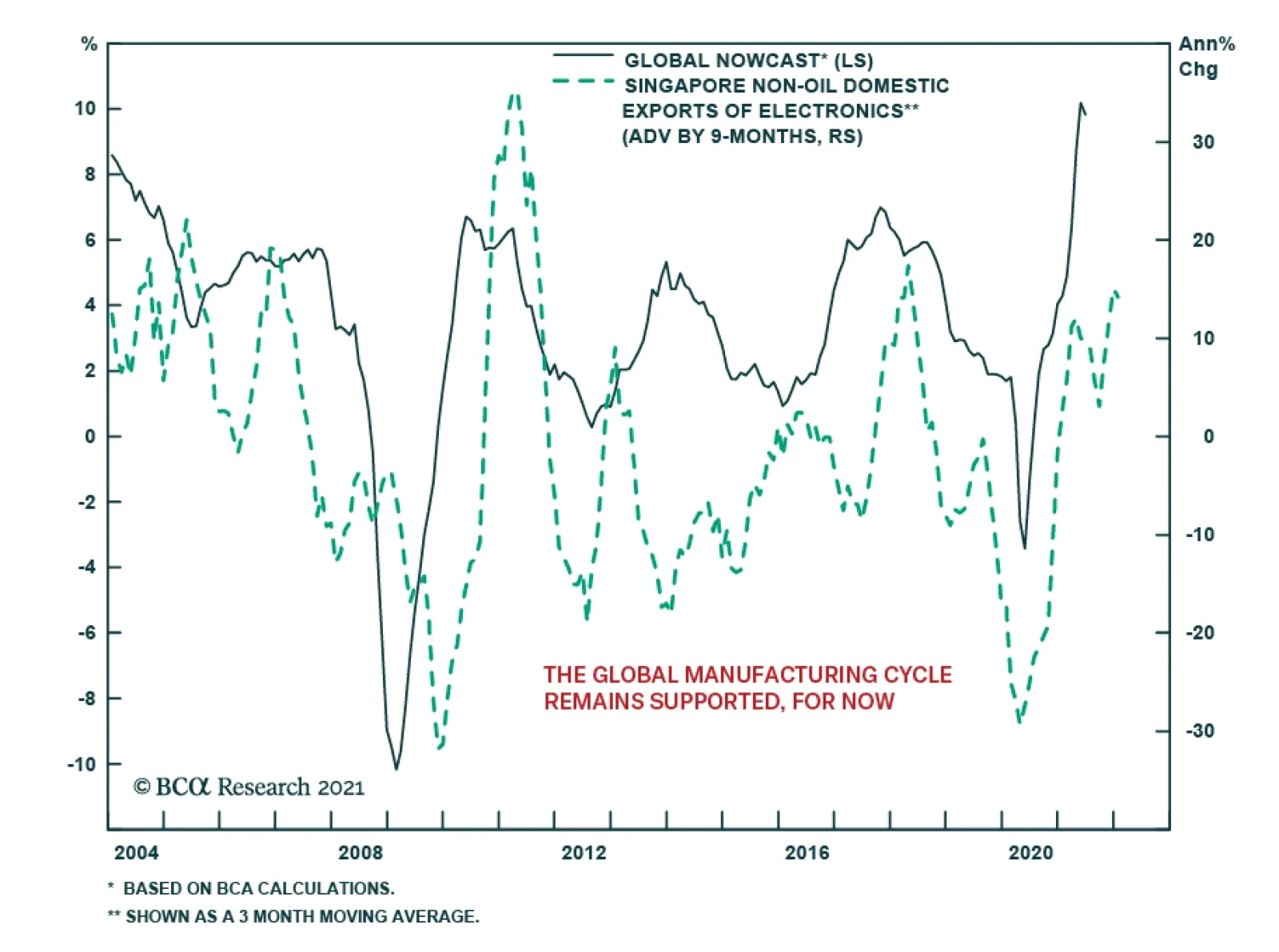

Taiwanese export orders and South Korean exports are sending a warning about the state of Asia’s manufacturing cycle. Korean exports in the first 20 days of June slowed to 29.5% y/y from 53.3%. Similarly, Taiwan’s export orders slowed to 34.5% y/y,…

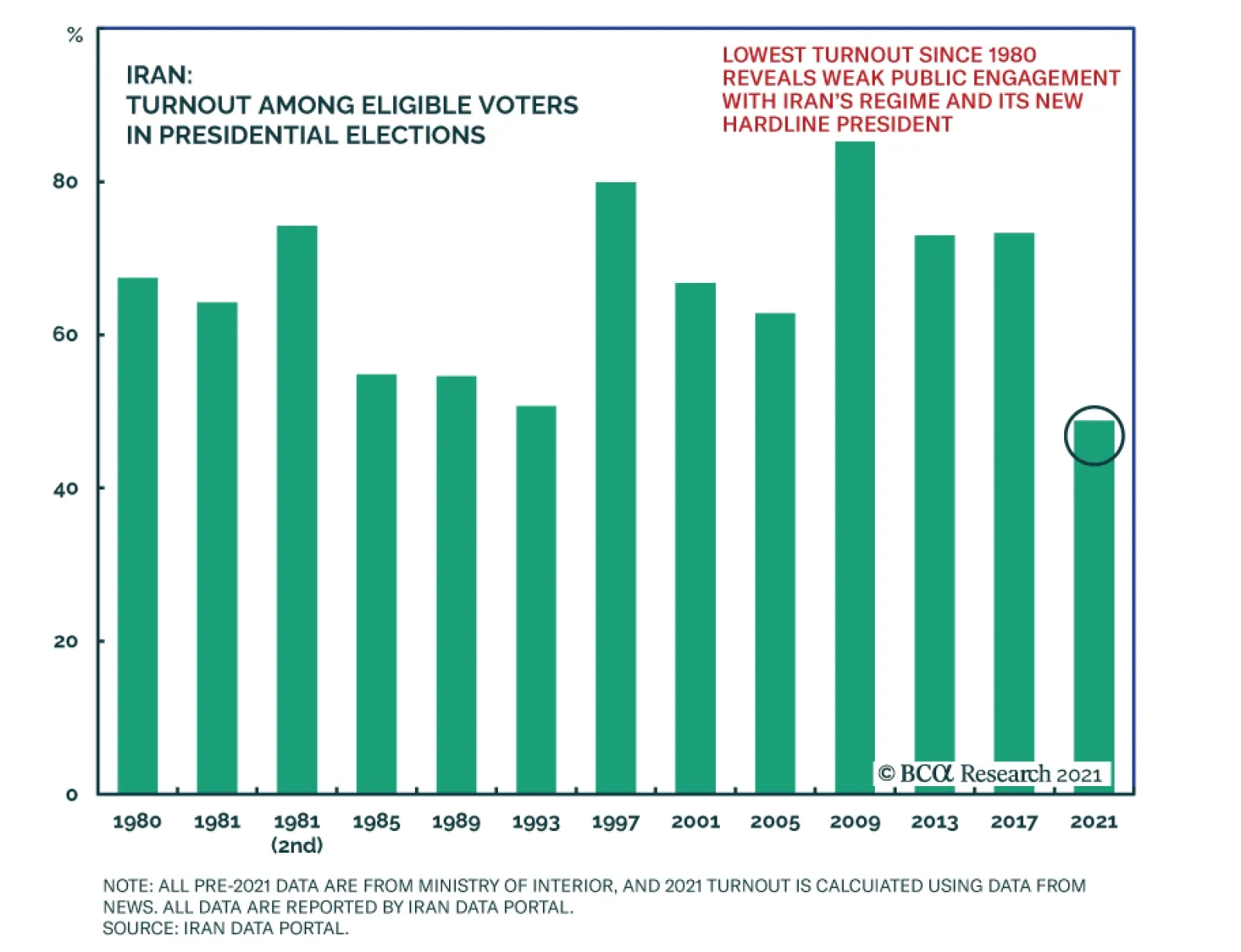

Iran held its presidential election on June 20. Islamic cleric and regime hardliner Ebrahim Raisi won the election as expected, with 62% of the vote. Voter turnout fell from 70% in 2017 to 49% this year, as Iranian liberals, reformists, and opposition…

According to BCA Research’s Geopolitical Strategy service, the macro and geopolitical outlook is darkening for China’s communist party. The “East Asian miracle” phase of Chinese growth has ended. Potential GDP growth is slowing and it will be harder for…

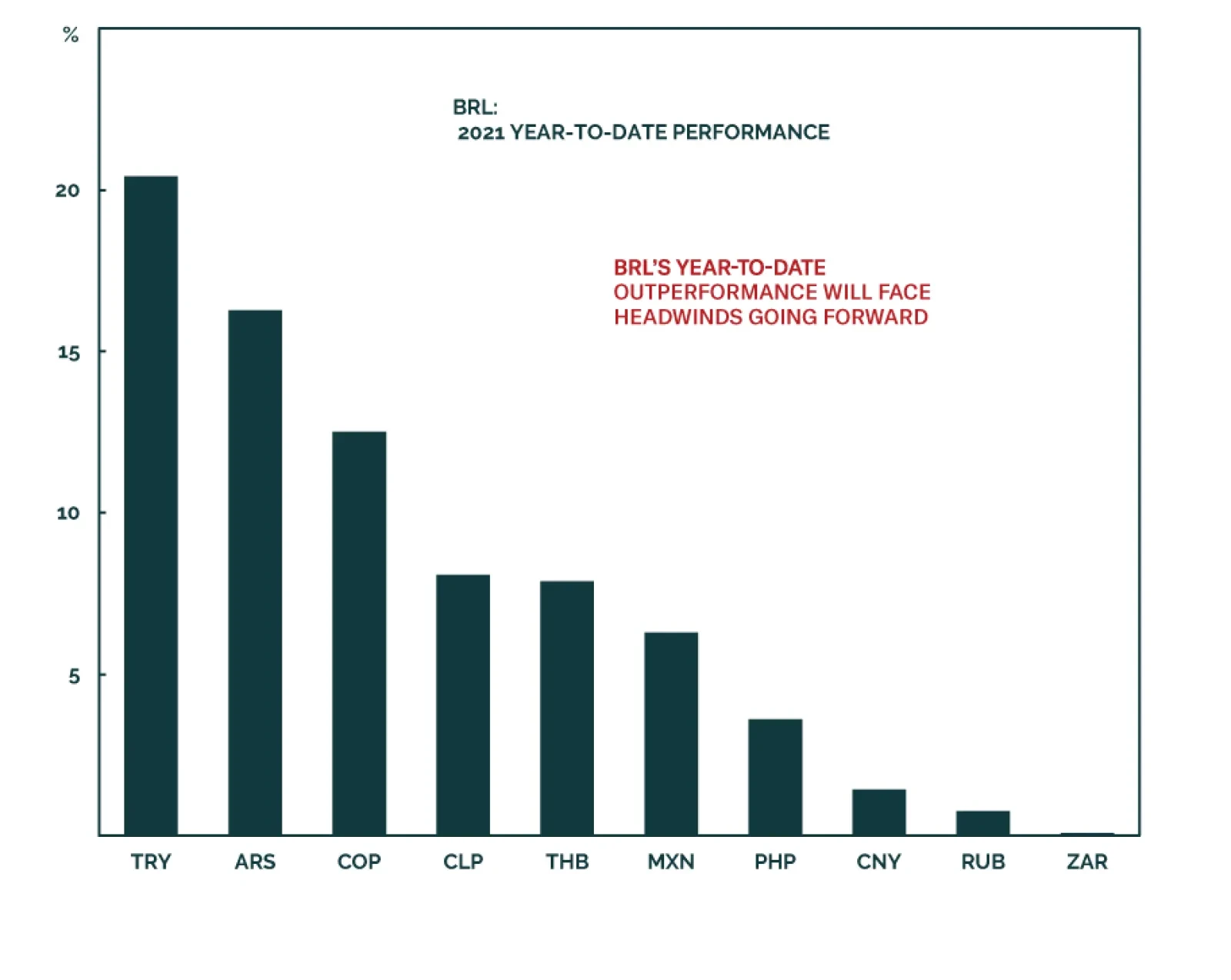

The Brazilian real was up 1.4% versus the dollar on Thursday – a day of broad dollar strength. The gain comes on the back of the Central Bank of Brazil’s decision to hike rates by 75 bps for the third consecutive time, bringing the benchmark Selic rate to…

Highlights China’s Communist Party has overcome a range of challenges over the past 100 years, performed especially well over the past 42 years, but the macro and geopolitical outlook is darkening. The “East Asian miracle” phase of Chinese growth has ended. Potential GDP growth is slowing and it will be harder for Beijing to maintain financial and sociopolitical stability. The Communist Party has shifted the basis of its legitimacy from rapid growth to quality of life and nationalist foreign policy. The latter, however, will undermine the former by stirring up foreign protectionism. In the near term, global investors should favor developed market equities over China/EM equities. But they should favor China and Hong Kong stocks over Taiwanese stocks given significant geopolitical risk over the Taiwan Strait. Structurally, favor the US dollar and euro over the renminbi. Feature Ten years ago, in the lead up to the Communist Party’s 90th anniversary, I wrote a report called “China and the End of the Deng Dynasty,” referring to Deng Xiaoping, the Chinese Communist Party’s great pro-market reformer.1 The argument rested on three points: the end of the export-manufacturing economic model, an increasingly assertive foreign policy, and the revival of Maoist nationalism. After ten years the report holds up reasonably well but it did not venture to forecast what precisely would come next. In reality it is the rule of the Communist Party, and not the leader of any one man, that fits into China’s history of dynastic cycles. As the party celebrates a hundred years since its founding on July 23, 1921, it is necessary to pause and reflect on what the party has achieved over the past century and what the current Xi Jinping era implies for the country’s next 100 years. Single-Party Rule Can Bring Economic Success. Communism Cannot. Regime type does not preclude wealth. Countries can prosper regardless of whether they are ruled by one person, one party, or many parties. The richest countries in the world grew rich over centuries in which their governments evolved from monarchy to democracy and sometimes back again. Even today several of the world’s wealthy democracies are better described as republics or oligarchies. Chart 1China Outperformed Communism But Not Liberal Democracy

China’s Communist Party Turns 100: So What?

China’s Communist Party Turns 100: So What?

The rule of one person, or autocracy, is not necessarily bad for economic growth. For every Kim Il Sung of North Korea there is a Lee Kuan Yew of Singapore. But authority based on a single person often expires with that person and rarely survives his grandchild. In China, Chairman Mao Zedong’s death occasioned a power struggle. Deng Xiaoping’s attempts to step down led to popular unrest that threatened the Communist Party’s rule on two separate occasions in the 1980s. The rule of a single party is thought to be more sustainable. Japan and Singapore are effectively single-party states and the wealthiest countries in Asia. They are democracies with leadership rotation and a popular voice in national affairs. And yet South Korea’s boom times occurred under single-party military rule. The same goes for the renegade province of Taiwan. Only around the time these two reached about $11,000-$14,000 GDP per capita did they evolve into multi-party democracies – though their wealth grew rapidly in the wake of that transition. China and soon Vietnam will test whether non-democratic, single-party rule can persist beyond the middle-income economic status that brought about democratic transition in Taiwan (Chart 1). Vietnam and Taiwan are the closest communist and non-communist governing systems, respectively, to mainland China. Insofar as China and Vietnam succeed at catching up with Taiwan it will be for reasons other than Marxist-Leninist ideology. Most communist systems have failed. At the height of international communism in the twentieth century there were 44 states ruled by communist parties; today there are five. China and Vietnam are the rare examples of communist states that not only survived the Soviet Union’s fall but also unleashed market forces and prospered (Chart 2). North Korea survived in squalor; Cuba’s experience is mixed. States that close off their economies do not have a good record of generating wealth. Closed economies lack competition and investment, struggle with stagflation, and often succumb to corruption and political strife. Openness seems to be a more diagnostic variable than government type or ideology, given the prosperity of democratic Japan and non-democratic China. Has the CPC performed better than other communist regimes? Arguably. It performs better than Vietnam but worse than Cuba on critical measures like infant mortality rates and life expectancy. Has it performed better than comparable non-communist regimes? Not really, though it is fast approaching Taiwan in all of these measures (Chart 3). Chart 2Communist States Get Rich By Compromising Their Communism

China’s Communist Party Turns 100: So What?

China’s Communist Party Turns 100: So What?

Chart 3China Catching Up To Cuba On Basic Wellbeing

China’s Communist Party Turns 100: So What?

China’s Communist Party Turns 100: So What?

What can be said for certain is that, since China’s 1979 reform and opening up, the CPC has avoided many errors and catastrophes. It survived the 1980s, 1990s, and 2000s without succumbing to international isolation, internal divisions, or economic crisis. It has drastically increased its share of global power (Table 1). Contrast this global ascent with the litany of mistakes and crises in the US since the year 2000. The CPC also managed the past decade relatively well despite the Chinese financial turmoil of 2015-16, the US trade war of 2018-19, and the COVID-19 pandemic. However, these events hint at greater challenges to come. China’s transition to a consumer-oriented economy has hardly begun. The struggle to manage systemic financial risk is intensifying today at risk to growth and stability (Chart 4). The trade war is simmering despite the Phase One trade deal and the change of party in the White House. And it is too soon to draw conclusions about the impact of the global pandemic, though China suppressed the virus more rapidly than other countries and led the world into recovery. Table 1China’s Global Rise After ‘Reform And Opening Up’

China’s Communist Party Turns 100: So What?

China’s Communist Party Turns 100: So What?

Chart 4China To Keep Struggling With Financial Instability

China To Keep Struggling With Financial Instability

China To Keep Struggling With Financial Instability

Judging by the points above, there are two significant risks on the horizon. First, the CPC’s revival of neo-Maoist ideology, particularly the new economic mantra of self-reliance and “dual circulation” (import substitution), poses the risk of closing the economy and undermining productivity.2 Second, China’s sliding back into the rule of a single person – after the “consensus rule” that prevailed after Deng Xiaoping – increases the risk of unpredictable decision-making and a succession crisis whenever General Secretary Xi Jinping steps down. The party’s internal logic holds that China’s economic and geopolitical challenges are so enormous as to require a strongman leader at the helm of a single-party and centralized state. But because of the traditional problems with one-man rule, there is no guarantee that the country will remain as stable as it has been over the past 42 years. Slowing Growth Drives Clash With Foreign Powers Every major East Asian economy has enjoyed a “miracle” phase of growth – and every one of them has seen this phase come to an end. Now it is China’s turn. The country’s potential GDP growth is slowing as the population peaks, the labor force shrinks, wages rise, and companies outsource production to cheaper neighbors (Charts 5A & 5B). The Communist Party is attempting to reverse the collapse in the fertility rate by shifting from its historic “one Child policy,” which sharply reduced births. It shifted to a two-child policy in 2016 and a three-child policy in 2021 but the results have not been encouraging over the past five years. Chart 5AChina’s Demographic Decline Accelerating

China’s Communist Party Turns 100: So What?

China’s Communist Party Turns 100: So What?

Chart 5BChina’s Demographic Decline Accelerating

China’s Communist Party Turns 100: So What?

China’s Communist Party Turns 100: So What?

In the best case China’s growth will follow the trajectory of Taiwan and South Korea, which implies at most a 6% yearly growth rate over the next decade (Chart 6). This is not too slow but it will induce financial instability as well as hardship for overly indebted households, firms, and local governments. Chart 6China's Growth Rates Will Converge With Taiwan, South Korea

China's Growth Rates Will Converge With Taiwan, South Korea

China's Growth Rates Will Converge With Taiwan, South Korea

The Communist Party’s legitimacy was not originally based on rapid economic growth but it came to be seen that way over the roaring decades of the 1980s through the 2000s. Thus when the Great Recession struck the party had to shift the party’s base of legitimacy. The new focus became quality of life, as marked by the Xi administration’s ongoing initiatives to cut back on corruption, pollution, poverty, credit excesses, and industrial overcapacity while increasing spending on health, education, and society (Chart 7). Chart 7China’s Fiscal Burdens Will Rise On Social Welfare Needs

China’s Communist Party Turns 100: So What?

China’s Communist Party Turns 100: So What?

The party’s efforts to improve standards of living and consumer safety also coincided with an increase in propaganda, censorship, and repression to foreclose political dissent. The country falls far short in global governance indicators (Chart 8). Chart 8China Lags In Governance, Rule Of Law

China’s Communist Party Turns 100: So What?

China’s Communist Party Turns 100: So What?

A second major new source of party legitimacy is nationalist foreign policy. China adopted a “more assertive” foreign and trade policy in the mid-2000s as its import dependencies ballooned. It helped that the US was distracted with wars of choice and financial crises. After the Great Recession the CPC’s foreign policy nationalism became a tool of generating domestic popular support amid slower economic growth. This was apparent in the clashes with Japan and other countries in the East and South China Seas in the early 2010s, in territorial disputes with India throughout the past decade, in political spats with Norway and most recently Australia, and in military showdowns over the Korean peninsula (2015-16) and today the Taiwan Strait (Chart 9). Chart 9Proxy Wars A Real Risk In China’s Periphery

China’s Communist Party Turns 100: So What?

China’s Communist Party Turns 100: So What?

If China were primarily focused on foreign policy and global strategy then it would not provoke multiple neighbors on opposite sides of its territory at the same time. This is a good way to motivate the formation of a global balance-of-power coalition that can constrain China in the coming years. But China’s outward assertiveness is not driven primarily by foreign policy considerations. It is driven by the secular economic slowdown at home and the need to use nationalism to drum up domestic support. This is why China seems indifferent to offending multiple countries at once (like India and Australia) as well as more distant trade partners whom it “should be” courting rather than offending (like Europe). Such assertive foreign policy threatens to undermine quality of life, namely by provoking international protectionism and sanctions on trade and investment. The US is galvanizing a coalition of democracies to put pressure on China over its trade practices and human rights. The Asian allies are mostly in step with the US because they fear China’s growing clout. The European states do not have as much to fear from China’s military but they do fear China’s state-backed industry and technological rise. Europe’s elites also worry about anti-establishment political movements just like American elites and therefore are trying to win back the hearts and minds of the working class through a more proactive use of fiscal and industrial policy. This entails a more assertive trade policy. China has so far not adapted to the potential for a unified front among the democracies, other than through rhetoric. Thus the international horizon is darkening even as China’s growth rates shift downward. China’s Geopolitical Outlook Is Dimming China’s government has overcome a range of challenges and crises. The country takes an ever larger role in global trade despite its falling share of global population because of its productivity and competitiveness. The drop in China’s outward direct investment is tied to the global pandemic and may not mark a top, given that the country will still run substantial current account surpluses for the foreseeable future and will need to recycle these into natural resources and foreign production (Chart 10). However, the limited adoption of the renminbi as a reserve currency in the face of this formidable commercial power reveals the world’s reservations about Beijing’s ability to maintain macroeconomic stability, good governance, and peaceful foreign relations. Chart 10China's Rise Continues

China's Rise Continues

China's Rise Continues

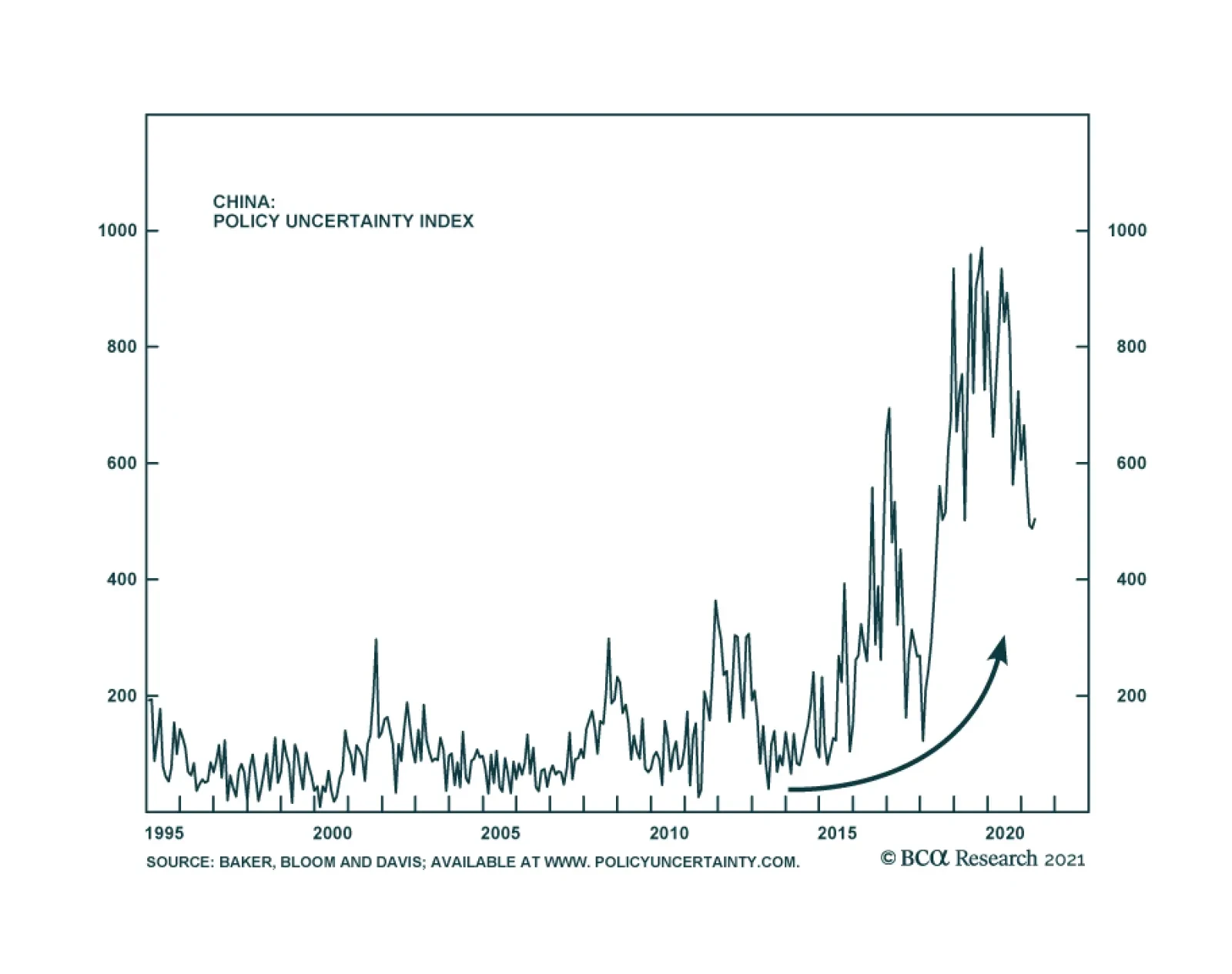

Chart 11China's Policy Uncertainty: A Structural Uptrend

China's Policy Uncertainty: A Structural Uptrend

China's Policy Uncertainty: A Structural Uptrend

China is not in a position to alter the course of national policy dramatically prior to the Communist Party’s twentieth national congress in 2022. The Xi administration is focused on normalizing monetary and fiscal policy and heading off any sociopolitical disturbances prior to that critical event, in which General Secretary Xi Jinping, who was originally slated to step down at this time according to the old rules, may be anointed the overarching “chairman” position that Mao Zedong once held. The seventh generation of Chinese leaders will be promoted at this five-year rotation of the Central Committee and will further consolidate the Xi administration’s grip. It will also cement the party’s rotation back to leaders who have ideological educations, as opposed to the norm in the 1990s and early 2000s of promoting leaders with technocratic skills and scientific educations.3 This does not mean that President Xi will refuse to hold a summit with US President Biden in the coming months nor does it mean that US-China strategic and economic dialogue will remain defunct. But it does mean that Beijing is unlikely to make any major course correction until after the 2022 reshuffle – and even then a course correction is unlikely. China has taken its current path because the Communist Party fears the sociopolitical consequences of relinquishing economic control just as potential growth slows. The new ruling philosophy holds that the Soviet Union fell because of Mikhail Gorbachev’s glasnost and perestroika, not because openness and restructuring came too late. Moreover it is far from clear that the US, Europe, and other democratic allies will apply such significant and sustained pressure as to force China to change its overall strategy. America is still internally divided and its foreign policy incoherent; the EU remains reactive and risk-averse. China has a well-established set of strategic goals for 2035 and 2049, the 100th anniversary of the People’s Republic, and the broad outlines will not be abandoned. The implication is that tensions with the US and China’s Asian neighbors will persist. Rising policy uncertainty is a secular trend that will pick back up sooner rather than later (Chart 11), to the detriment of a stable and predictable investment environment. Chart 12Chinese Government’s Net Worth High But Hidden Liabilities Pose Risks

China’s Communist Party Turns 100: So What?

China’s Communist Party Turns 100: So What?

Monetary and fiscal dovishness and a continued debt buildup are the obvious and necessary solutions to China’s combination of falling growth potential, rising social liabilities, the need to maintain the rapid military buildup in the face of geopolitical challenges. Sovereign countries can amass vast debts if they own their own debt and keep nominal growth above average bond yields. China’s government has a very favorable balance sheet when national assets are taken into consideration as well as liabilities, according to the IMF (Chart 12). On the other hand, China’s government is having to assume a lot of hidden liabilities from inefficient state-owned companies and local governments. In the short run there are major systemic financial risks even though in the long run Beijing will be able to increase its borrowing and bail out failing entities in order to maintain stability, just like Japan, the US, and Europe have had to do. The question for China is whether the social and political system will be able to handle major crises as well as the US and Europe have done, which is not that well. Investment Takeaways The rule of a single party is not a bar to economic success – but the rule of a single person is a liability due to the problem of succession. Marxism-Leninism is terrible for productivity unless it is compromised to allow for markets to operate, as in China and Vietnam. States that close their economies to the outside world usually atrophy. There is no compelling evidence that China’s Communist Party has performed better than a non-communist alternative would have done, given the province of Taiwan’s superior performance on most economic indicators. Since 1979, the Communist Party has avoided catastrophic errors. It has capitalized on domestic economic potential and a favorable international environment. Now, in the 2020s, both of these factors are changing for the worse. China’s “miracle” phase of growth has expired, as it did for other East Asian states before it. The maturation of the economy and slowdown of potential GDP have forced the Communist Party to shift the base of its political legitimacy to something other than rapid income growth: namely, quality of life and nationalist foreign policy. An aggressive foreign policy works against quality of life by provoking protectionism from foreign powers, particularly the United States, which is capable of leading a coalition of states to pressure China. The Communist Party’s policy trajectory is unlikely to change much through the twentieth national party congress in 2022. After that, a major course correction to improve relations with the West is conceivable, though we would not bet on it. Between 2021 and China’s 2035 and 2049 milestones, the Communist Party must navigate between rising socioeconomic pressures at home and rising geopolitical pressures abroad. An economic or political breakdown at home, or a total breakdown in relations with the US, could lead to proxy wars in China’s periphery, including but not limited to the Taiwan Strait. For now, global investors should favor the euro and US dollar over the renminbi (Chart 13). Chart 13Prefer The Dollar And Euro To The Renminbi

Prefer The Dollar And Euro To The Renminbi

Prefer The Dollar And Euro To The Renminbi

Mainland investors should favor government bonds relative to stocks. Chinese stocks hit a major peak earlier this year and the government’s seizure of control over the tech sector is taking a toll. Investors should prefer developed market equities relative to Chinese equities until China’s current phase of policy tightening ends and there is at least a temporary improvement in relations with the United States. But investors should also prefer Chinese and Hong Kong stocks relative to Taiwanese due to the high risk of a diplomatic crisis and the tail risk of a war. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 The report concluded, “the emerging trends suggest a likely break from Deng's position toward heavier state intervention in the economy, more contentious relationships with neighbors, and a Party that rules primarily through ideology and social control.” Co-written with Jennifer Richmond, "China and the End of the Deng Dynasty," Stratfor, April 19, 2011, worldview.stratfor.com. 2 The Xi administration’s new concept of “dual circulation” entails that state policy will encourage the domestic economy whereas the international economy will play a secondary role. This is a reversal of the outward and trade-oriented economic model under Deng Xiaoping. See “Xi: China’s economy has potential to maintain long-term stable development,” November 4, 2020, news.cgtn.com. 3 See Willy Wo-Lap Lam, "China’s Seventh-Generation Leadership Emerges onto the Stage," Jamestown Foundation, China Brief 19:7, April 9, 2019, Jamestown.org.

Singapore trade data is flagging a small warning about the state of the global manufacturing cycle. The country’s non-oil domestic exports (NODX) declined 0.1% m/m in May, disappointing expectations of a 4.5% m/m increase. On a year-over-year basis, NODX is…

Emerging Markets Strategy has been recommending that investors position for a dollar rebound and believes the dollar’s move will be playable: it will be meaningful and last a few months. US dollar strength will be driven by both repricing of the Fed’s…