Emerging Markets

Highlights Continued upgrades to global economic growth – most recently by the IMF this week –will support higher natgas prices. In our estimation, gas for delivery at Henry Hub, LA, in the coming withdrawal season (November – March) is undervalued at current levels at ~ $2.90/MMBtu. Inventory demand will remain strong during the current April-October injection season, following the blast of colder-than-normal weather in 1Q21 that pulled inventories lower in the US, Europe and Northeast Asia. The odds the US will succeed in halting completion of the final leg of the Russian Nord Stream 2 natural gas pipeline into Germany are higher than the consensus expectation. Our odds the pipeline will not be completed this year stand at 50%, which translates into higher upside risk for natural gas prices. We are getting long 1Q22 calls on CME/NYMEX Henry Hub-delivered natgas futures struck at $3.50/MMBtu vs. short 1Q22 $3.75/MMBtu calls at tonight's close. The probability of Nord Stream 2 cancellation is underpriced, which means European TTF and Asian JKM prices will have to move higher to attract LNG cargoes next winter from the US, if the pipeline is cancelled (Chart of the Week). Feature As major forecasting agencies continue to upgrade global growth prospects, expectations for industrial-commodity demand – energy, bulks, and base metals – also are moving higher. This week, the IMF raised its growth expectations for this year and next to 6% and 4.4%, respectively, nearly a full percentage-point increase versus its January forecast update for 2021.1 This upgrade follows a similar move by the OECD last month.2 In the US, the EIA is expecting industrial demand for natural gas to rise 1.35 Bcf/d this year to 23.9 Bcf/d; versus 2019 levels, industrial demand will be 0.84 Bcf/d higher in 2021. For 2022, industrial demand is expected to be 24.2 Bcf/d. US industrial demand likely will recover faster than the EU's, given the expectation of a stronger recovery on the back of massive fiscal and monetary stimulus. Overall natgas demand in the US likely will move lower this year, given higher natgas prices expected this year and next will incentivize electricity generators to switch to coal at the margin, according to the EIA. Total demand is expected to be 82.9 Bcf/d in the US this year vs. 83.3 Bcf/d last year, owing to lower generator demand. Pipeline-quality gas output in the US – known as dry gas, since its liquids have been removed for other uses – is expected to average 91.4 Bcf/d this year, essentially unchanged. Lower consumption by the generators and flat production will allow US gas inventories to return to their five-year average levels of 3.7 Tcf by the end of October, in the EIA's estimation (Chart 2). Chart of the WeekUS-Russia Geopolitical Risk Underpriced

US-Russia Pipeline Standoff Could Push LNG Prices Higher

US-Russia Pipeline Standoff Could Push LNG Prices Higher

Chart 2US Natgas Inventories Return To Five-Year Average

US-Russia Pipeline Standoff Could Push LNG Prices Higher

US-Russia Pipeline Standoff Could Push LNG Prices Higher

US Liquified Natural Gas (LNG) exports are likely to expand, as Asian and European demand grows (Chart 3). Prior to the boost in US LNG demand from colder weather, exports set monthly records of 9.4 Bcf/d and 9.8 Bcf/d in November and December of last year, respectively, with Asia accounting for the largest share of exports (Chart 4). This also marked the first time LNG exports exceeded US pipeline exports to Mexico and Canada. The EIA is forecasting US LNG exports will be 8.5 bcf/d and 9.2 Bcf/d this year and next, versus pipeline exports of 8.8 Bcf/d and 8.9 Bcf/d in 2021 and 2022, respectively. Chart 3US LNG Exports Continue Growing

US-Russia Pipeline Standoff Could Push LNG Prices Higher

US-Russia Pipeline Standoff Could Push LNG Prices Higher

Chart 4US LNG Exports Set Records In November And December 2020

US-Russia Pipeline Standoff Could Push LNG Prices Higher

US-Russia Pipeline Standoff Could Push LNG Prices Higher

US LNG exports – and export potential given the size of the resource base at just over 500 Tcf – now are of a sufficient magnitude to be a formidable force in global markets, particularly in Europe. This puts it in direct conflict with Russia, which has targeted Europe as a key market for its pipeline natural gas exports. US-Russia Standoff Looming Over Nord Stream 2 Given the size and distribution of global oil and gas production and consumption, it comes as no surprise national interests can, at times, become as important to pricing these commodities as supply-demand fundamentals. This is particularly true in oil, and increasingly is becoming the case in natural gas. That the same dramatis personae – the US and Russia – should feature in geopolitical contests in oil and gas markets also should not come as a surprise. In an attempt to circumvent transporting its natural gas through Ukraine, Russia is building a 1,230 km underwater pipeline from Narva Bay in the Kingisepp district of the Leningrad region of Russia to Lubmin, near Greifswald, in Germany (Map 1). The Biden administration, like the Trump administration and US Congress, is officially attempting to halt the final leg of the pipeline from being built, although Biden has not yet put America’s full weight into stopping it. Biden claims it will be up to the Europeans to decide what to do. At the same time, any major Russian or Russian-backed military operation in Ukraine could trigger an American action to halt the pipeline in retaliation. Map 1Nord Stream 2 Route

US-Russia Pipeline Standoff Could Push LNG Prices Higher

US-Russia Pipeline Standoff Could Push LNG Prices Higher

In our estimation, there is a 50% chance that the Nord Stream 2 natural gas pipeline will not be completed this year or go into operation as planned given substantial geopolitical risks. The $11 billion pipeline would connect Russia directly to Germany with a capacity of about 55 billion cubic meters, which, combined with the existing Nord Stream One pipeline, would equal 110 BCM in offshore capacity, or 55% of Russia's natural gas exports to Europe in 2019. The pipeline’s construction is 94% complete, with the Russian ship Akademik Cherskiy entering Danish waters in late March to begin laying pipes to finish the final 138-kilometer stretch, according to Reuters. The pipeline could be finished in early August at the pace of 1 kilometer per day.3 The Russian and German governments are speeding up the project to finish it before US-Russia tensions, or the German elections in September, interrupt the construction process again. It is not too late for the US to try to halt the pipeline through sanctions. But for the Americans to succeed, the Biden administration would have to make an aggressive effort. Notably the Biden administration took office with a desire to sharpen US policy toward Russia.4 While Biden seeks Russian engagement on arms reduction treaties and the Iranian nuclear negotiations, he mainly aims to counter Russia, expand sanctions, provide weapons to Ukraine, and promote democracy in Russia’s sphere of influence. The result will almost inevitably be a new US-Russia confrontation, which is already taking shape over Russia’s buildup of troops on the border with Ukraine, where US and Russian meddling could cause civil war to reignite (Map 2). Map 2Russia’s Military Tensions With The West Escalate In Wake Of Biden’s Election And Ukraine’s Renewed Bid To Join NATO

US-Russia Pipeline Standoff Could Push LNG Prices Higher

US-Russia Pipeline Standoff Could Push LNG Prices Higher

Tensions in Ukraine are directly tied to US military cooperation with Ukraine and any possibility that Ukraine will join the NATO military alliance, a red line for Putin. Nord Stream 2 is Russia’s way of bypassing Ukraine but a new US-Russia conflict, especially a Russian attack on Ukraine, would halt the pipeline. The pipeline’s completion would improve Russo-German strategic relations, undercut US liquefied natural gas exports to Germany and the EU, and reduce the US’s and eastern Europe’s leverage over Russia (and Germany). Biden says his administration is planning to impose new sanctions on firms that oversee, construct, or insure the pipeline, and such sanctions are required under American law.5 Yet Biden also wants a strong alliance with Germany, which favors the pipeline and does not want to escalate the conflict with Russia. The American laws against Nord Stream have big loopholes and give the president discretion regarding the use of sanctions, which means Biden would have to make a deliberate decision to override Germany and impose maximum sanctions if he truly wanted to halt construction.6 This would most likely occur if Russia committed a major new act of aggression in Ukraine or against other European democracies. The German policy, under the current ruling coalition led by Chancellor Angela Merkel’s Christian Democratic Union, is to finish the pipeline despite Russia’s conflicts with the West and political repression at home. Russia provides more than a third of Germany’s natural gas imports and this pipeline would bypass eastern Europe’s pipeline network and thus secure Germany’s (and Austria’s and the EU’s) natural gas supply whenever Russia cuts off the flow to Ukraine (through which roughly 40% of Russian natural gas still must pass to reach Europe). Germany's Election And Natgas Politics Germany wants to use natural gas as a bridge while it phases out nuclear energy and coal. Natural gas has grown 2.2 percentage points as a share of Germany’s total energy mix since the Fukushima disaster of 2011, and renewable energy has grown 7.7ppt, while coal has fallen 7.3ppt and nuclear has fallen 2.5ppt (Chart 5). The German federal election on September 26 complicates matters because Merkel and the Christian Democrats are likely to underperform their opinion polls and could even fall from power. They do not want to suffer a major foreign policy humiliation at the hands of the Americans or a strategic crisis with Russia right before the election. They will insist that Biden leave the pipeline alone and will offer other forms of cooperation against Russia in compensation. Therefore, the current German government could push through the pipeline and complete the project even in the face of US objections. But this outcome is not guaranteed. The German Greens are likely to gain influence in the Bundestag after the elections and could even lead the German government for the first time – and they are opposed to a new fossil fuel pipeline that increases Russia’s influence. Chart 5Germany Sees Nord Stream 2 Gas As Bridge To Low-Carbon Economy

US-Russia Pipeline Standoff Could Push LNG Prices Higher

US-Russia Pipeline Standoff Could Push LNG Prices Higher

Hence there is a fair chance that the pipeline does not become operational: either Americans halt it out of strategic interest, or the German Greens halt it out of environmental and strategic interest, or both. True, there is a roughly equal chance that Merkel’s policy status quo survives in Germany, which would result in an operational pipeline. The best case for Germany might be that the current government completes the pipeline physically but the next government has optionality on whether to make it operational. But 50/50 odds of cancellation is a much higher risk than the consensus holds. The Russian policy is to finish Nord Stream 2 while also making an aggressive military stance against the West’s and NATO’s influence in Ukraine. This would expand Russian commodity and energy exports and undercut Ukraine’s natgas transit income. It would also increase Russian leverage over Germany – and it would divide Germany from the eastern Europeans and Americans. A preemptive American intervention would elicit Russian retaliation. The Russians could respond in the strategic sphere or the economic sphere. Economically they could react by cutting off natural gas to Europe, but that would undermine their diplomatic goals, so they would more likely respond by increasing production of natural gas or crude oil to steal American market share. In any scenario Russian retaliation would likely cause global price volatility in one or more energy markets, in addition to whatever volatility is induced by the cancellation of Nord Stream 2 itself. US-Russia tensions are likely to escalate but only Ukraine and Nord Stream 2, or the separate Iranian negotiations, have a direct impact on global energy supply. If Germany goes forward with the pipeline, then Russia would need to be countered by other means. The Americans, not the Germans, would provide these “other means,” such as military support to ensure the integrity of Ukraine and other nations’ borders. The Russians may gain a victory for their energy export strategy but they will never compromise on Ukraine and they will still need to focus on the broader global shift to renewable energy, which threatens their economic model and hence ultimately their regime stability. So, the risk of a market-moving US-Russia conflict can be delayed but probably not prevented (Chart 6). Chart 6US-Russia Conflit Likely

US-Russia Conflit Likely

US-Russia Conflit Likely

Bottom Line: The Nord Stream 2 pipeline is not guaranteed to be completed this year as planned. The US is more likely to force a halt to the Nord Stream 2 pipeline than the consensus holds, especially if Russia attacks Ukraine. If the US fails to do so, then the German election will become the next signpost for whether the pipeline will become operational. If the Americans halt the pipeline, then US-Russian conflict either already erupted or will occur sooner rather than later and will likely impact global oil or natural gas prices. Investment Implications Our subjective assessment of 50% odds the US will succeed in halting completion of the final leg of Nord Stream 2 are higher than the consensus expectation. This translates directly into higher upside risk for natural gas prices in the US and Europe later this year and next. Given our view, we are getting long 1Q22 calls on CME/NYMEX Henry Hub-delivered natgas futures struck at $3.50/MMBtu vs. short 1Q22 $3.75/MMBtu calls at tonight's close. The probability of Nord Stream 2 cancellation is underpriced, which means the odds of higher prices in the LNG market are underpriced (Chart 7). The immediate implication of our view is European TTF prices will have to move higher to attract LNG cargoes next winter from the US, if the Nord Stream 2 pipeline's final leg is cancelled. This also would tighten the Asian markets, causing the JKM to move higher as well (Chart 8). Any indication of colder-than-normal weather in the US, Europe or Asian markets would mean a sharper move higher. Chart 7Natgas Tails Are Too Narrow For Next Winter

US-Russia Pipeline Standoff Could Push LNG Prices Higher

US-Russia Pipeline Standoff Could Push LNG Prices Higher

Chart 8Nord Stream 2 Cancellation Would Boost JKM Prices

Nord Stream 2 Cancellation Would Boost JKM Prices

Nord Stream 2 Cancellation Would Boost JKM Prices

Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Commodities Round-Up Energy: Bullish The US and Iran began indirect talks earlier this week in Vienna aimed at restoring the Joint Comprehensive Plan of Action (JCPOA), otherwise known as the "Iran nuclear deal." All of the other parties of the deal – Britain, China, France, Germany and Russia – are in favor of restoring the deal. BCA Research believes this is most likely to occur prior to the inauguration of a new president who is expected to be a hardliner willing to escalate Iran’s demands. US President Biden can unilaterally ease sanctions and bring the US into compliance with the deal, and Iran could then reciprocate. If a deal is not reached by August it could take years to resolve US-Iran tensions. China could offer to cooperate on sanctions and help to broker negotiations following the signing of its 25-year trade deal with Iran last week. Russia likely would demand the US not pressure its allies to cancel the Nord Stream 2 deal, in return for its assistance in brokering a deal. Base Metals: Bullish Iron ore prices continue to be supported by record steel prices in China, trading at more than $173/MT earlier this week. Even though steel production reportedly is falling in the top steel-producer in China, Tangshan, as a result of anti-pollution measures, for iron ore remains stout. As we have previously noted, we use steel prices as a leading indicator for copper prices. We remain long Dec21 copper and will be looking for a sell-off to get long Sep21 copper vs. short Sep21 copper if the market trades below $4/lb on the CME/COMEX futures market (Chart 9). Precious Metals: Bullish Gold held support ~ $1,680/oz at the end of March, following an earlier test in the month. We remain long the yellow metal, despite coming close to being stopped out last week (Chart 10). The earlier sell-off appeared to be caused by a need to raise liquidity to us. We continue to expect the Fed to hold firm to its stated intent to wait for actual inflation to become manifest before raising rates, and, therefore, continue to expect real rates to weaken. This will be supportive of gold and commodities generally (Chart 10). Ags/Softs: Neutral Corn continues to be well supported above $5.50/bu, following last week's USDA report showing farmers intend to increase acreage planted to just over 91mm acres, which is less than 1% above last year's level. Chart 9

Copper Prices Surge As Global Storage Draws

Copper Prices Surge As Global Storage Draws

Chart 10

Gold Disconnected From US Dollar And Rates

Gold Disconnected From US Dollar And Rates

Footnotes 1 Please see the Fund's April 2021 forecast Managing Divergent Recoveries. 2 We noted last week these higher growth expectations generally are bullish for industrial commodities – energy, metals, and bulks. Please see Fundamentals Support Oil, Bulks, And Metals, which we published 1 April 2021. It is available at ces.bcaresearch.com. 3 For the rate of construction see Margarita Assenova, “Clouds Darkening Over Nord Stream Two Pipeline,” Eurasia Daily Monitor 18: 17 (February 1, 2021), Jamestown Foundation, jamestown.org. For the current status, see Robin Emmott, “At NATO, Blinken warns Germany over Nord Stream 2 pipeline,” Reuters, March 23, 2021, reuters.com. 4 The Democratic Party blames Russia for what it sees as a campaign to undermine the democratic West and recreate the Soviet sphere of influence. See for example the 2008 invasion of Georgia, the failure of the Obama administration’s 2009-11 diplomatic “reset,” the Edward Snowden affair, the seizure of Crimea and civil war in Ukraine, the survival of Syria’s dictator, and Russian interference in US elections in 2016 and 2020. 5 The Countering Russian Influence in Europe and Eurasia Act of 2017, and the Protecting Europe’s Energy Security Act of 2019/2020, contain provisions requiring sanctions on firms that have contributed in any way a minimum of $1 million to the project, or provide pipe-laying services or insurance. There are exceptions for services provided by the governments of the EU member states, Norway, Switzerland, or the UK. The president has discretion over the implementation of sanctions as usual. 6 The German state of Mecklenburg-Vorpommern is creating a shell foundation to enable the completion of the pipeline. It can shield companies from American sanctions aimed at private companies, not sovereigns. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades Commodity Prices and Plays Reference Table Summary of Closed Trades

Higher Inflation On The Way

Higher Inflation On The Way

We calculate sector and country effects for an Emerging Market portfolio. We then use our results to make conclusions on EM equity allocations. Although sector effects increased significantly over the past three years in EM, country effects continue to play a larger role. This means that EM equity investors should continue incorporating country macro views into their portfolio construction. Sector composition is more important for countries like Colombia, Mexico, and Russia whose composition is substantially different from the EM benchmark.

As expected, the Reserve Bank of India kept the benchmark repurchase rate unchanged at 4% at its Wednesday meeting. Nonetheless, the RBI managed to surprise investors by announcing plans to purchase up to one trillion rupees ($14 billion) of bonds this…

Feature The selloff in Chinese stocks since mid-February reflects a rollover in earnings growth and multiples. Lofty valuations in Chinese equities driven by last year’s massive stimulus means that stock prices are vulnerable to any pullback in policy supports (Chart 1A and 1B). Chart 1AGrowth In Chinese Investable Earnings And Multiple Expansions Has Rolled Over

Growth In Chinese Investable Earnings And Multiple Expansions Has Rolled Over

Growth In Chinese Investable Earnings And Multiple Expansions Has Rolled Over

Chart 1BEarnings Outlook Still Looks Promising In The Onshore Market, But May Soon Peak

Earnings Outlook Still Looks Promising In The Onshore Market, But May Soon Peak

Earnings Outlook Still Looks Promising In The Onshore Market, But May Soon Peak

After diverging in the past seven to eight months, Chinese stocks have started to gravitate towards deteriorating monetary conditions index. The market may be beginning to price in a peak in economic as well as corporate profit growth (Chart 2). Defensive stocks in China’s onshore and offshore equity markets have also outperformed cyclicals since February, which confirms that investors expect earnings growth will slow in the coming months (Chart 3). A tighter monetary policy stance, coupled with increased regulations targeting the real estate, banking, and tech sectors have further dampened investors’ appetite for Chinese stocks. Chart 2A-Share Prices Start To Gravitate Towards Tightening Monetary Conditions

A-Share Prices Start To Gravitate Towards Tightening Monetary Conditions

A-Share Prices Start To Gravitate Towards Tightening Monetary Conditions

Chart 3Defensives Have Prevailed Over Cyclicals In Both Onshore And Offshore Markets

Defensives Have Prevailed Over Cyclicals In Both Onshore And Offshore Markets

Defensives Have Prevailed Over Cyclicals In Both Onshore And Offshore Markets

The official PMIs bounced back smartly in March following three consecutive months of decline. However, the strong PMI readings do not change our view that the speed of China’s economic recovery is near its zenith. PMIs in the first two months of the year are typically lower due to the Lunar New Year (LNY), and the improvement in March’s PMI did not exceed seasonal rebounds experienced in previous years. Weakening fixed-asset investments also indicate that economic activity is moderating. We remain cautious on the 6 to 12-month outlook for Chinese stocks, in both absolute and relative terms. Qingyun Xu, CFA Associate Editor qingyunx@bcaresearch.com Jing Sima China Strategist jings@bcaresearch.com China’s NBS manufacturing and non-manufacturing PMIs in March beat market expectations with sharp rebounds after moderating in the previous three months. The improvement in the PMIs will likely provide authorities with confidence to stay the course on policy normalization. The methodology calculating PMI indexes reflects the net reported improvement in business activities relative to the previous month and there was a notable decline in PMIs in February, due to the LNY holiday and travel restrictions related to the spread of COVID-19. Additionally, the average reading of China’s official composite PMI in Q1 this year was 2.2 percentage points lower than in Q4 last year and weaker than the Q1 PMI figures in most of the pre-pandemic years. Moreover, Chinese Caixin manufacturing PMI, which focuses on smaller and private corporates, declined further in March as it continued its downward trend started in December 2020. Chart 4Q1 PMIs Slowed By More Than Seasonal Factors

Q1 PMIs Slowed By More Than Seasonal Factors

Q1 PMIs Slowed By More Than Seasonal Factors

Chart 5Caixin PMI Shows Further Deterioration Among Private-Sector Manufacturers

Caixin PMI Shows Further Deterioration Among Private-Sector Manufacturers

Caixin PMI Shows Further Deterioration Among Private-Sector Manufacturers

Growth in credit expansions in February was better than expected, supported by a substantial increase in corporates’ demand for medium- and long-term loans. Travel restrictions during this year’s LNY led to a shorter holiday, a faster resumption in manufacturing activity after the break and stronger credit demand in February. China’s Monetary Policy Committee meeting last week reiterated the authorities’ hawkish policy tone and removed dovish language prevalent in last month’s National People’s Congress, such as “maintaining the consistency, stability, and sustainability in monetary policy” and “not making a sudden turn in policymaking.” Given the strong headline economic and credit data in January and February, the authorities will be unlikely to slow normalizing monetary policy. Therefore, the risk of a policy-tightening overshoot remains high. The PBoC has continued to drain net liquidity in the interbank system since early this year, evidenced by falling excess reserves at the central bank. Excess reserves normally lead the credit impulse by about six months, signaling that the latter will continue to decelerate in the months ahead. In turn, the credit impulse normally leads the business cycle by six to nine months, meaning that China’s cyclical economic recovery will likely peak in the first half of 2021. Chart 6Corporates Demand For Longer-Term Bank Loans Resumed Their Upward Trend Early This Year

Corporates Demand For Longer-Term Bank Loans Resumed Their Upward Trend Early This Year

Corporates Demand For Longer-Term Bank Loans Resumed Their Upward Trend Early This Year

Chart 7Falling Excess Reserves Leads To A Deceleration In Credit And Economic Growth

Falling Excess Reserves Leads To A Deceleration In Credit And Economic Growth

Falling Excess Reserves Leads To A Deceleration In Credit And Economic Growth

Robust industrial activities and improving profitability helped to boost profit growth in January and February. The bounce in producer prices also drove up returns in industrial output, particularly in upstream industries loaded with commodity producers. Nevertheless, weak final demand is limiting the ability of Chinese producers to pass on higher prices to domestic consumers, highlighted in the divergence between Chinese PPI and CPI. In addition, China’s domestic demand for commodities and industrial metals may reach its cyclical peak in mid-2021, following ongoing credit tightening and reduced economic activity. Commodity inventories have surged to historical highs due to soaring imports (which far exceeded consumption) during 2H20. Inventory destocking pressures will weigh on commodity prices with China’s domestic demand reaching its cyclical peak. Disinflation/deflation pressures may re-emerge in 2H21, which will pose downside risks to China’s industrial profits. Chart 8Industrials Posted A Strong Rebound In The First Two Months of 2021

Industrials Posted A Strong Rebound In The First Two Months of 2021

Industrials Posted A Strong Rebound In The First Two Months of 2021

Chart 9Surging Commodity Prices Helped To Boost Upstream Industry Profits

Surging Commodity Prices Helped To Boost Upstream Industry Profits

Surging Commodity Prices Helped To Boost Upstream Industry Profits

Chart 10Domestic Final Demand Remains Sluggish

Domestic Final Demand Remains Sluggish

Domestic Final Demand Remains Sluggish

Chart 11Decelerating Chinese Credit Growth Poses Downside Risks To Global Commodity Prices

Decelerating Chinese Credit Growth Poses Downside Risks To Global Commodity Prices

Decelerating Chinese Credit Growth Poses Downside Risks To Global Commodity Prices

Chart 12Chinas Raw Material Inventory Restocking Cycle May Be Near A Cyclical Peak

Chinas Raw Material Inventory Restocking Cycle May Be Near A Cyclical Peak

Chinas Raw Material Inventory Restocking Cycle May Be Near A Cyclical Peak

Chart 13Real Estate And Infrastructure Investment Losing Steam In 2021

Real Estate And Infrastructure Investment Losing Steam In 2021

Real Estate And Infrastructure Investment Losing Steam In 2021

Investments in infrastructure and real estate drove China’s economic recovery in the second half of 2020. However, growth momentum in both sectors has slowed because of retreating government spending in infrastructure and tightening regulations in the property sector. Both home sales and housing prices, especially in tier-one cities, rose significantly in January-February this year, deepening authorities’ concerns over bubble risks in the property market. The share of mortgages, deposits and advanced payments as a source of funds for property developers reached an all-time high in February. Following the LNY, the authorities introduced a slew of new restrictions on the housing market to curb excessive demand. These were in addition to placing limits on bank lending to both property developers and household mortgages. All of these measures will weigh on housing supply and demand, and the impact is already evident in falling land purchases and housing starts. At the same time, property developers are rushing to complete existing projects. The tighter regulations on real estate financing will likely weaken growth in real estate investment and construction activities in the second half of this year. Chart 14Housing Prices In Top-Tier Cities Have Been On A Tear …

Housing Prices In Top-Tier Cities Have Been On A Tear

Housing Prices In Top-Tier Cities Have Been On A Tear

Chart 15… But Bank Lending To Developers And Mortgage Loans Continue Downward Trend

But Bank Lending To Developers And Mortgage Loans Continue Downward Trend

But Bank Lending To Developers And Mortgage Loans Continue Downward Trend

Chart 16Property Developers Are Rushing To Sell And Complete Existing Projects

Property Developers Are Rushing To Sell And Complete Existing Projects

Property Developers Are Rushing To Sell And Complete Existing Projects

Chart 17Forward-Looking Indicators Suggest A Slowdown In Housing And Construction Activities

Forward-Looking Indicators Suggest A Slowdown In Housing And Construction Activities

Forward-Looking Indicators Suggest A Slowdown In Housing And Construction Activities

Table 1China Macro Data Summary

China Macro And Market Review

China Macro And Market Review

Table 2China Financial Market Performance Summary

China Macro And Market Review

China Macro And Market Review

Footnotes Cyclical Investment Stance Equity Sector Recommendations

China’s Caixin PMI showed an expansion in economic activity in March, in line with the message from the official PMI released last week. The Caixin Services PMI rebounded to 54.3 from 51.5, exceeding expectations of a 52.1 print. This offset the impact of the…

Our long Russian equities / short EM tactical recommendation is up 6.28% since initiation on February 5. However, risks to this trade are now rising. On Monday, President Putin signed a law allowing him to run for two more six-year terms, raising the…

Highlights Global manufacturing activity will soon peak due to growing costs and China’s policy tightening. This process will allow the dollar’s rebound to continue. EUR/USD’s correction will run further. This pullback in the euro is creating an attractive buying opportunity for investors with a 12- to 24-month investment horizon. Eurozone banks will continue to trade in unison with the euro. Feature The correction in the euro has further to run. The dollar currently benefits from widening real interest differentials, but a growing list of headwinds will cause a temporary setback for the global manufacturing sector, which will fuel the greenback rally further. Nonetheless, EUR/USD will stabilize between 1.15 and 1.12, after which it will begin a new major up-leg. Consequently, investors with a 12- to 24-month investment horizon should use the current softness to allocate more funds to the common currency. A Hiccup In Global Industrial Activity Global manufacturing activity is set to decelerate on a sequential basis and the Global Manufacturing PMI will soon peak. The first problem for the global manufacturing sector is the emergence of financial headwinds. The sharp rebound in growth in the second half of 2020 and the optimism created by last year’s vaccine breakthrough as well as the rising tide of US fiscal stimulus have pushed US bond yields and oil prices up sharply. These financial market moves are creating a “growth tax” that will bite soon. Mounting US interest rates have lifted global borrowing costs while the doubling in Brent prices has increased the costs of production and created a small squeeze on oil consumers. Thus, even if the dollar remains well below its March 2020 peak, our Growth Tax Indicator (which incorporates yields, oil prices and the US dollar) warns of an imminent top in the US ISM Manufacturing and the Global Manufacturing PMI (Chart 1). Already, the BCA Global Leading Economic Indicator diffusion index has dipped below the 50% line, which usually ushers in downshifts in global growth. A deceleration in China’s economy constitutes another problem for the global manufacturing cycle. Last year’s reflation-fueled rebound in Chinese economic activity was an important catalyst to the global trade and manufacturing recovery. However, according to BCA Research’s Emerging Market Strategy service, Beijing is now tightening policy, concerned by a build-up in debt and excesses in the real estate sector. Already, the PBoC’s liquidity withdrawals are resulting in a decline of commercial bank excess reserves, which foreshadows a slowing of China’s credit impulse (Chart 2). Chart 1The Global Growth Tax Will Bite

The Global Growth Tax Will Bite

The Global Growth Tax Will Bite

Chart 2Chinese Credit Will Slow

Chinese Credit Will Slow

Chinese Credit Will Slow

In addition to liquidity withdrawals, Chinese policymakers are also tightening the regulatory environment to tackle excessive debt buildups and real estate speculation. The crackdown on property developers and house purchases will cause construction activity to shrink in the second half of 2021. Meanwhile, tougher rules for both non-bank lenders and the asset management divisions of banks will further harm credit creation. BCA’s Chief EM strategist, Arthur Budaghyan, notes that consumer credit is already slowing. Chinese fiscal policy is unlikely to create a counterweight to the deteriorating credit impulse. China’s fiscal impulse will be slightly negative next year. Chinese financial markets are factoring in these headwinds, and on-shore small cap equities are trying to break down while Chinese equities are significantly underperforming global benchmarks. Chart 3Deteriorating Surprises

Deteriorating Surprises

Deteriorating Surprises

Bottom Line: The combined assault from the rising “growth tax” and China’s policy tightening is leaving its mark. Economic surprises in the US, the Eurozone, EM and China have all decelerated markedly (Chart 3), which the currency market echoes. Some of the most pro-cyclical currencies in the G-10 are suffering, with the SEK falling relative to the EUR and the NZD and AUD both experiencing varying degrees of weakness. The Euro Correction Will Run Further… Until now, the euro’s decline mostly reflects the rise in US interest rate differentials; however, the coming hiccup in the global manufacturing cycle is causing a second down leg for the euro. First, the global economic environment remains consistent with more near-term dollar upside, due to: Chart 4Commodities Are Vulnerable

Commodities Are Vulnerable

Commodities Are Vulnerable

A commodity correction that will feed the dollar’s rebound. Aggregate speculator positioning and our Composite Technical Indicator show that commodity prices are technically overextended (Chart 4). With this backdrop, the coming deceleration in Chinese economic activity is likely to catalyze a significant pullback in natural resources, which will hurt rates of returns outside the US and therefore, flatter the dollar. The dollar’s counter-cyclicality. The expected pullback in the Global Manufacturing PMI is consistent with a stronger greenback (Chart 5). The dollar’s momentum behavior. Among G-10 FX, the dollar responds most strongly to the momentum factor (Chart 6). Thus, the likelihood is high that the dollar’s recent rebound will persist, especially because our FX team’s Dollar Capitulation Index has only recovered to neutral from oversold levels and normally peaks in overbought territory. Chart 5The Greenback's Counter-Cyclicality

The Greenback's Counter-Cyclicality

The Greenback's Counter-Cyclicality

Chart 6The Dollar Is A High Momentum Currency

The Euro Dance: One Step Back, Two Steps Forward

The Euro Dance: One Step Back, Two Steps Forward

Second, the euro’s specific dynamics remain negative for now. Based on our short-term valuation model, the fair value of EUR/USD has downshifted back to 1.1, which leaves the euro 7% overvalued (Chart 7). Until now, real interest rate differentials and the steepening of the US yield curve relative to Germany’s have driven the decline in the fair value estimate. However, the deceleration in global growth also hurts the euro’s fair value because the US is less exposed than the Eurozone to the global manufacturing cycle. Chart 7The Euro's Short-Term Fair Value Is At 1.1

The Euro's Short-Term Fair Value Is At 1.1

The Euro's Short-Term Fair Value Is At 1.1

Chart 8Speculators Have Not Capitulated

Speculators Have Not Capitulated

Speculators Have Not Capitulated

The euro is also technically vulnerable, similar to commodities. Speculators are still massively net long EUR/USD and the large pool of long bets in the euro suggests that a capitulation has yet to take place (Chart 8). The euro responds very negatively to a weak Chinese economy. The Eurozone has deeper economic ties with China than the US. Exports to China account for 1.7% of the euro area’s GDP, and 2.8% of Germany’s compared to US exports to China at 0.5% of GDP. Indirect financial links are also larger. Credit to EM accounts for 45% of the Eurozone’s GDP compared to 5% for the US. Thus, the negative impact of a Chinese slowdown on EM growth has greater spillovers on European than on US ones rates of returns. A weak CNY and sagging Chinese capital markets harm the euro. The euro’s rebound from 1.064 on March 23 2020 to 1.178 did not reflect sudden inflows into European fixed-income markets. Instead, the money that previously sought higher interest rates in the US left that country for EM bonds and China’s on-shore fixed-income markets, the last major economies with attractive yields. These outflows from the US to China and EM pushed the dollar down, which arithmetically helped the euro. Thus, the recent EUR/USD correlates closely with Sino/US interest rate and with the yuan because the euro’s strength reflects the dollar demise (Chart 9). Consequently, a decelerating Chinese economy will also hurt EUR/USD via fixed-income market linkages. Finally, the euro will depreciate further if global cyclical stocks correct relative to defensive equities. Deep cyclicals (financials, consumer discretionary, energy, materials and industrials) represent 59% of the Eurozone MSCI benchmark versus 36% of the US index. Cyclical equities are exceptionally overbought and expensive relative to defensive names. They are also very levered to the global business cycle and Chinese imports. In this context, the expected deterioration in both China’s economic activity and the Global Manufacturing PMI could cause a temporary but meaningful pullback in the cyclicals-to-defensives ratio and precipitate equity outflows from Europe into the US (Chart 10). Chart 9EUR/USD And Chinese Rates

EUR/USD And Chinese Rates

EUR/USD And Chinese Rates

Chart 10EUR/USD Will Follow Cyclicals/Defensives

EUR/USD Will Follow Cyclicals/Defensives

EUR/USD Will Follow Cyclicals/Defensives

Bottom Line: A peak in the global manufacturing PMI will hurt the euro, especially because China will meaningfully contribute to this deceleration in global industrial activity. Thus, the euro’s pullback has further to run. An important resistance stands at 1.15. A failure to hold will invite a rapid decline to EUR/USD 1.12. Nonetheless, the euro’s depreciation constitutes nothing more than a temporary pullback. … But The Long-Term Bull Market Is Intact We recommend buying EUR/USD on its current dip because the underpinnings of its cyclical bull market are intact. Chart 11Investors Structurally Underweight Europe

Investors Structurally Underweight Europe

Investors Structurally Underweight Europe

First, investors are positioned for a long-term economic underperformance of the euro area relative to the US. The depressed level of portfolio inflows into Europe relative to the US indicates that investors already underweight European assets (Chart 11). This pre-existing positioning limits the negative impact on the euro of the current decrease in European growth expectations (Chart 11, bottom panel). Second, as we wrote last week, European growth is set to accelerate significantly this summer. Considering the absence of ebullient investor expectations toward the euro, this process can easily create upside economic surprises later this year, especially when compared to the US. Moreover, the deceleration in Chinese and global growth will most likely be temporary, which will limit the duration of their negative impact on Europe. Third, the US stimulus measure will create negative distortions for the US dollar. The addition of another long-term stimulus package of $2 trillion to $4 trillion to the $7 trillion already spent by Washington during the crisis implies that the US government deficit will not narrow as quickly as US private savings will decline. Therefore, the US current account deficit will widen from its current level of 3.5% of GDP. As a corollary, the US twin deficit will remain large. Meanwhile, the Fed is unlikely to increase real interest rates meaningfully in the coming two years because it believes any surge in inflation this year will be temporary. Furthermore, the FOMC aims to achieve inclusive growth (i.e. an overheated labor market). This policy combination forcefully points toward greater dollar weakness. The US policy mix looks particularly dollar bearish when compared to that of the Eurozone. To begin with, the balance of payment dynamics make the euro more resilient. The euro area benefits from the underpinning of a current account surplus of 1.9% of GDP. Moreover, the European basic balance of payments stands at 1.5% of GDP compared to a 3.6% deficit for the US. Additionally, FDI into Europe are rising relative to the US. The divergence in the FDI trends will continue due to the high probability that the Biden administration will soon increase corporate taxes. Chart 12The DEM In The 70s

The DEM In The 70s

The DEM In The 70s

The combination of faster vaccine penetration and much larger fiscal stimulus means that the US economy will overheat faster than Europe’s. Because the Fed seems willing to tolerate higher inflation readings, US CPI will rise relative to the Eurozone. In the 1970s, too-easy policy in Washington meant that the gap between US and German inflation rose. Despite the widening of interest rate and growth differentials in favor of the USD or the rise in German relative unemployment, the higher US inflation dominated currency fluctuations and the deutschemark appreciated (Chart 12). A similar scenario is afoot in the coming years, especially in light of the euro bullish relative balance of payments. Fourth, valuations constitute an additional buttress behind the long-term performance of the euro. Our FX strategy team Purchasing Power Parity model adjusts for the different composition of price indices in the US and the euro area. Based on this metric, the euro is trading at a significant 13% discount from its long-term fair value, with the latter being on an upward trend (Chart 13). Furthermore, BCA’s Behavioral Exchange Rate Model for the trade-weighted euro is also pointing up, which historically augurs well for the common currency. Lastly, even if the ECB’s broad trade-weighted index stands near an all-time high, European financial conditions remain very easy. This bifurcation suggests that the euro is not yet a major hurdle for the continent and can enjoy more upside (Chart 14). Chart 13EUR/USD Trades Well Below Long-Term Fair Value

EUR/USD Trades Well Below Long-Term Fair Value

EUR/USD Trades Well Below Long-Term Fair Value

Chart 14Easy European Financial ##br##Conditions

Easy European Financial Conditions

Easy European Financial Conditions

Chart 15Make Room For the Euro!

Make Room For the Euro!

Make Room For the Euro!

Finally, the euro will remain a beneficiary from reserve diversification away from the USD. The dollar’s status as the premier reserve currency is unchallenged. However, its share of global reserves has scope to decline while the euro’s proportion could move back to the levels enjoyed by legacy European currencies in the early 1990s (Chart 15). Large reserve holders will continue to move away from the dollar. BCA Research’s Geopolitical Strategy team argues that US tensions with China transcend the Trump presidency. Meanwhile, the current administration’s relationship with Russia and Saudi Arabia will be cold. For now, their main alternative to the dollar is the euro because of its liquidity. Moreover, the NGEU stimulus program creates an embryonic mechanism to share fiscal risk within the euro area. The Eurozone is therefore finally trying to evolve away from a monetary union bereft of a fiscal union. This process points toward a lower probability of a break up, which makes the euro more attractive to reserve managers. Bottom Line: Despite potent near-term headwinds, the euro’s long-term outlook remains bright. Global investors already underweight European assets, yet balance of payment and policy dynamics point toward a higher euro. Moreover, valuations and geopolitical developments reinforce the cyclical tailwinds behind EUR/USD. Thus, investors with a 12- to 24-month investment horizon should use the current euro correction to gain exposure to the European currencies. Any move in EUR/USD below 1.15 will generate a strong buy signal. Sector Focus: European Banks And The Istanbul Shake The recent decline in euro area bank stocks coincides with the 14% increase in USD/TRY and the 17% decline in the TUR Turkish equities ETF following the sacking of Naci Ağbal, the CBRT governor. President Erdogan is prioritizing growth over economic stability because his AKP party is polling poorly ahead of the 2023 election. The Turkish economy is already overheating, and the lack of independence of the CBRT under the leadership of Şahap Kavcıoğlu promises a substantial increase in Turkish inflation, which already stands at 16%. Hence, foreign investors will flee this market, creating further downward pressures on the lira and Turkish assets. European banks have a meaningful exposure to Turkey. Turkish assets account for 3% of Spanish bank assets or 28% of Tier-1 capital. For France, this exposure amounts to 0.7% and 5% respectively, and for the UK, it reaches 0.3% and 2%. As a comparison, claims on Turkey only represent 0.3% and 0.5% of the assets and Tier-1 capital of US banks. Unsurprisingly, fluctuations in the Turkish lira have had a significant impact one the share prices of European banks in recent years, even after controlling for EPS and domestic yield fluctuations (Table 1). Table 1TRY Is Important To European Banks…

The Euro Dance: One Step Back, Two Steps Forward

The Euro Dance: One Step Back, Two Steps Forward

Nonetheless, today’s TRY fluctuations are unlikely to have the same lasting impact on European banks share prices as they did from 2017 to 2019 because European banks have already shed significant amounts of Turkish assets (Chart 16). This does not mean that European banks are out of the woods yet. The level of European yields remains a key determinant of the profitability of Eurozone’s banks, and thus, of their share prices (Chart 17, top panel). Moreover, the euro still tightly correlates with European bank stocks as well (Chart 17, bottom panel). As a result, our view that the global manufacturing cycle will experience a temporary downshift and the consequent downside in EUR/USD both warn of further underperformance of European banks. Chart 16… But Less Than It ##br##Once Was

The Euro Dance: One Step Back, Two Steps Forward

The Euro Dance: One Step Back, Two Steps Forward

Chart 17Higher Yields And A stronger Euro, These Are Few Of My Favorite Things

Higher Yields And A stronger Euro, These Are Few Of My Favorite Things

Higher Yields And A stronger Euro, These Are Few Of My Favorite Things

These same views also suggest that this decline in bank prices is creating a buying opportunity. Ultimately, we remain cyclically bullish on the euro and the transitory nature of the manufacturing slowdown implies that global yields will resume their ascent. The cheap valuations of European banks, which trade at 0.6-times book value, make them option-like vehicles to bet on these trends, even if the banking sectors long-term prospects are murky. Moreover, they are a play on Europe’s domestic recovery this summer. We will explore banks in greater detail in future reports. Mathieu Savary, Chief European Investment Strategist Mathieu@bcaresearch.com

Highlights The Biden administration is combining Trumpian nationalism with a renewed push for US innovation in a major infrastructure bill that is highly likely to become law. Populism and Great Power struggle with China and Russia are structural forces that give enormous momentum to this effort. Don’t bet against it. President Biden’s $2.4 trillion infrastructure and green energy plan has a subjective 80% chance of passing into law by the end of the year, as infrastructure is popular and Democrats control Congress. The net deficit increase will range from $700 billion to $1.3 trillion depending on the size of corporate tax hikes in the final bill. The second part of Biden’s plan, the roughly $2 trillion American Families Plan, has a much lower chance of passage – at best 50/50 – as the 2022 midterm elections will loom and fiscal fatigue will set in. While the US infrastructure package is a positive cyclical catalyst, it was largely expected, and the Biden administration still faces early stress-tests on China/Taiwan, Russia, Iran, and even North Korea. Game theory helps explain why financial markets cannot ignore the 60% chance of a crisis in the Taiwan Strait. A full-fledged war is still low-probability but Taiwan remains the world’s preeminent geopolitical risk. In emerging markets, stay short Russian and Brazilian currency and assets – and continue favoring Indian stocks over Chinese. Feature The “arsenal of democracy” is a phrase that President Franklin Delano Roosevelt used to describe the full might of US government, industry, and labor in assisting the western allies in World War II. The US is reviving this combination of productive forces today, with President Joe Biden’s $4 trillion-plus American Jobs and Families Plan unveiled in Pittsburgh on March 31. The context is once again a global struggle among the Great Powers, albeit not world war (at least not yet … more on that below). The US is reviving its post-WWII pursuit of global liberal hegemony – symbolized by its role, growing once again, as the world’s chief consumer and chief warrior (Chart 1). Biden promoted his plan to build up the US’s infrastructure and social safety net explicitly as a historic and strategic investment – “in 50 years, people are going to look back and say this was the moment that American won the future.”1 It is critical for investors to realize that they are not witnessing another round of COVID-19 fiscal relief. That task is already completed with the Republican spending of 2020 and Biden’s own $1.9 trillion American Rescue Plan Act (ARPA), which together with the vaccine rollout are delivering a jolt to growth (Chart 2). Chart 1America Pursues Hegemony Anew

America Pursues Hegemony Anew

America Pursues Hegemony Anew

Chart 2Consensus Expects 6.5% US GDP Growth After American Rescue Plan

Consensus Expects 6.5% US GDP Growth After American Rescue Plan

Consensus Expects 6.5% US GDP Growth After American Rescue Plan

Our own back-of-the-envelope estimates of growth suggest that there is considerable upside risk even under current law (Chart 3). The output gap is also guesstimated here, and it will tighten faster than expected, especially as the service sector revives on economic reopening. Chart 3Back-Of-Envelope: US GDP And Output Gap Show Upside Risk After American Rescue Plan Act (ARPA)

The Arsenal Of Democracy

The Arsenal Of Democracy

A growth overshoot is even more likely considering that the first part of Biden’s proposal, the $2.4 trillion American Jobs Plan consisting mostly of infrastructure and green energy, is highly likely to pass Congress (by July at earliest and December at latest, most likely late fall). Our revised estimates for the US budget deficit show that this bill will add considerably to the deficit in the coming years, peaking in three or four years, thus averting the “fiscal cliff” in 2022-23 and adding to aggregate demand in the years after the short-term COVID-era cash handouts dry up (Chart 4). The net deficit increase will be $700 billion if Biden gets all of his tax hikes and $1.3 trillion if he only gets half of them, according to our sister US Political Strategy. Chart 4US Budget Deficit Will Remain Fat In Coming Years

The Arsenal Of Democracy

The Arsenal Of Democracy

We give Biden’s $2.4 trillion American Jobs Plan an 80% chance of passing through Congress by the end of the year. Infrastructure is broadly popular – as President Trump’s own $2 trillion infrastructure campaign proposal revealed – and Democrats have just enough votes to push it through the Senate via budget reconciliation, which requires zero votes from Republicans. Biden’s political capital is still strong given that his approval rating will stay above 50% as long as Trump is the obvious alternative and the Republicans are deeply divided over their own future (Chart 5).2 The second part of his plan, the $1.95 trillion American Families Plan, is much less likely to pass before the 2022 midterm elections – we would say 50/50 odds at best, if the infrastructure deal passes quickly. Chart 5Biden’s Political Capital Is Sufficient To Pass Another Major Law

The Arsenal Of Democracy

The Arsenal Of Democracy

Of course there are very important differences between Biden’s $2.4 trillion infrastructure plan and the similarly sized proposal that Trump would have unveiled this month had he been re-elected: Biden’s proposal is probably heavier on innovation and research and development, and certainly heavier on unionization and labor regulation, than Trump’s would have been. Biden’s plan integrates infrastructure with sustainability, renewable energy, and climate change initiatives that will help the US catch up with Europe and China on the green front. The plan will consist of direct government spending – rather than government seed money to promote private investment. It will be partially offset by repealing the corporate tax cuts in Trump’s signature Tax Cuts and Jobs Act. Most importantly – from a geopolitical point of view – Biden is making a bid for the US to resume its post-WWII quest for global liberal hegemony. He argued that the US stands at the crossroads of a global choice between “democracies and autocracies” and that rebuilding US infrastructure is ultimately about proving that democracies can create consensus and “deliver for their people.” Autocratic regimes, fairly or not, routinely call attention to the divisiveness of modern party politics in the West and the resulting policy gridlock which produces bad outcomes for many citizens, resulting in greater domestic dysfunction and “chaos.” It is important to note that this bid for hegemony will be more, not less, destabilizing for global politics as it will make the US economy more self-sufficient and insulated from the world. It will intensify the US-China and US-Russia strategic competition while making it more difficult for Biden to conduct bilateral diplomacy with these states given their differences in moral values and frequent human rights violations. What is happening now is the culmination of political shifts that pre-date the pandemic, but were galvanized by the pandemic, and it is of global, geopolitical significance for the coming decade and beyond.3 Biden and the establishment Democrats – embattled by populism on their right and left flanks – are shamelessly coopting President Trump’s “Make America Great Again” nationalism with a larger-than-life, infrastructure-and-manufacturing initiative that emphasizes productivity as well as “Buy American” protectionism. Biden explicitly argued that Americans need to boost innovation to “put us in a position to win the global competition with China in the upcoming years.” At Biden’s first press conference on March 25, he made a similar point about China: So I see stiff competition with China. China has an overall goal, and I don’t criticize them for the goal, but they have an overall goal to become the leading country in the world, the wealthiest country in the world, and the most powerful country in the world. That’s not going to happen on my watch because the United States are going to continue to grow and expand.4 The US trade deficit is set to widen a lot further under this massive domestic buildout. It aims to be the largest government investment program since Dwight Eisenhower’s building of the highways or the Kennedy-Johnson-Nixon space race. But it explicitly aims to diminish China’s role as a supplier of US goods and materials and the US trade deficit already shows evidence of economic divorce (Chart 6). The US is bound to have a larger trade deficit due to its own savings-and-investment imbalances but it has a powerful interest in redistributing this trade deficit to its allies and reducing over-dependency on China, which is itself pursuing strategic self-sufficiency and military modernization in anticipation of an ongoing rivalry this century. Chart 6Biden's Coopts Trump's Trade And Manufacturing Agenda

Biden's Coopts Trump's Trade And Manufacturing Agenda

Biden's Coopts Trump's Trade And Manufacturing Agenda

Bottom Line: Biden’s $2.4 trillion American Jobs Plan has an 80% chance of passing Congress later this year with a net increase to the fiscal thrust of between $700 billion and $1.3 trillion, depending on how many and how high the corporate tax hikes. The other $2 trillion social spending part of Biden’s plan has only a 50/50 chance of passage. The infrastructure and green energy rebuild should be understood as a return of Big Government motivated by populism and Great Power competition – it is a geopolitical theme with enormous momentum. The result will be faster US growth and higher inflation expectations, with the upside risk of a productivity boom (or boomlet) from the combination of public and private sector innovation. Investors should not bet against the cyclical bull market even though any increase in long-term potential GDP is speculative. A Fourth Taiwan Strait Crisis And The Cuban Missile Crisis Biden’s American Jobs Plan reserves $50 billion for US semiconductor manufacturing, a vast sum, larger than expectations and far larger than the relatively small public investments that helped revolutionize the US chip industry in the 1980s. But it will take a long time for these investments to pay off in the form of secure and redundant supply chains, while a semiconductor shortage is raging today that is already entangled with the US-China rivalry and tensions over the Taiwan Strait. The risk of a diplomatic or military incident is urgent because the chip shortage exacerbates China’s vulnerabilities at a time when the Biden administration is about to make critical decisions regarding the tightness of new export controls that cut off China’s access to US semiconductor chips, equipment, and parts. If the Biden administration appears to pursue a full-fledged tech blockade, as the Trump administration seemed bent on doing, then China will retaliate economically or militarily. Before going further we should point out that there are still areas of potential US-China cooperation under the Biden administration that could reduce tensions this year (though not over the long run). Biden and Xi Jinping might meet virtually as early as this month to discuss carbon emission reduction targets. Meanwhile China is positioning itself to serve as power-broker on two major foreign policy challenges – Iran and North Korea. Biden expressly seeks Chinese and Russian assistance based on the mutual interest in nuclear non-proliferation. Notably, Beijing’s renewed strategic dealings with Iran over the past month highlight its confidence that Biden does not have the appetite to stick with Trump’s “maximum pressure” but rather will seek to reduce sanctions and restore the 2015 nuclear deal. Hence China will seek to parlay influence over Tehran in exchange for reduced US pressure on its trade and economy (Chart 7). Beijing is making a similar offer on North Korea. Chart 7China Holds The Key To Iran, As With North Korea?

China Holds The Key To Iran, As With North Korea?

China Holds The Key To Iran, As With North Korea?

Ironically both Iranian and North Korean geopolitical tensions should skyrocket in the short term since high-stakes negotiations are beginning, even though they are ultimately more manageable risks than the mega-risk of US-China conflict over Taiwan. China cannot gain the advanced technology it needs to achieve a strategic breakthrough if the US should impose a total tech blockade, e.g. draconian export controls enforced on US allies. Yet it is highly unlikely to gain the tech by seizing Taiwan, since war would likely destroy the computer chip fabrication plants and provoke global sanctions that would crush its economy. The result is that China is launching a massive campaign of domestic production and indigenous innovation while circumventing US restrictions through cyber and other means. Still, a dangerous strategic asymmetry is looming because the US will retain access to the most advanced computer chips via its alliances and on-shoring, whereas China will remain vulnerable to a tech blockade via Taiwan. This brings us to our chief global geopolitical risk: a US-China showdown in the Taiwan Strait. Highlighting the urgency of the risk, Admiral John Aquilino, the nominee for Commander of the US Indo-Pacific Command, told the Senate Armed Services Committee that China might not wait six years to attack Taiwan: “My opinion is that this problem is much closer to us than most think and we have to take this on.”5 To illustrate the calculus of such a showdown – and our reasons for maintaining an alarmist tone and building up market hedges and safe-haven investments – we turn to game theory. Game theory is not a substitute for empirical analysis but a tool to formalize complex international systems with multiple decision-makers. An obvious yet fair analogy to a US-China-Taiwan crisis is the Cuban missile crisis of 1962.6 The standard construction of the Cuban missile crisis in game theory goes as follows: if the US maintains a blockade and the Soviets withdraw their missiles a compromise is achieved and war is averted; if the US conducts air strikes and the Soviets maintain or use their missiles then war ensues. The payouts to each player are shown in the matrix in Diagram 1. Diagram 1Cuban Missile Crisis, 1962

The Arsenal Of Democracy

The Arsenal Of Democracy

One concern about this construction is that the payouts may underestimate the costs of war since nuclear arms could be used. We insert a comment into the diagram highlighting that the payouts could be altered to account for nuclear war. Note that this alteration does not change the final outcome: the equilibrium scenario is still US blockade and Soviet withdrawal, which is what happened in reality. If we model a US-China-Taiwan conflict along similar lines, the US takes the role of the Soviet Union while China stands where the US stood in 1962 (Diagram 2). This is a theoretical scenario in which the US offers Taiwan a decisive improvement in its security or offensive military capabilities. However, because of the unique circumstances of the Chinese civil war, in which the victors established the People’s Republic of China in Beijing in 1949 and the defeated forces retreated to Taiwan, China’s regime legitimacy is at stake in any showdown over Taiwan. If Beijing suffered a defeat that secured Taiwan’s independence while degrading Beijing’s regime legitimacy and security, the Chinese regime might not survive the domestic blowback.7 Diagram 2Fourth Taiwan Strait Crisis – What Happens If The US Offers Game-Changing Military Support To Taiwan?

The Arsenal Of Democracy

The Arsenal Of Democracy

Thus we reduce the Chinese payout in the case of American victory. In the top right cell of Diagram 2, the row player’s payout falls from two points (2ppt) in the first diagram to one point (1ppt) in this diagram. This seemingly slight change entirely alters the outcome of the game. Beijing now faces equally bad outcomes in the event of defeat, whereas victory remains preferable to a tie. Therefore as long as China believes that the US will not resort to nuclear weapons to defend Taiwan (a reasonable assessment) then it may make the mistake of opting for military force to ensure victory. Fortunately for global investors the US is not providing Taiwan with game-changing military capabilities, although it is ultimately up to China to decide what threatens its security and the US is in the process of upgrading Taiwan’s defense in an effort to deter Beijing from forceful reunification. Thus the exercise demonstrates why we do not expect immediate war – no game-changer yet – but at the same time it shows why war is much likelier than the consensus holds if the military or political status quo changes in a way that China deems strategically unacceptable. A lower-degree Taiwan crisis should be expected – i.e. one in which the US maintains tech restrictions, offers arms sales or military training that do not upend the military balance, or signs free trade agreements or other significant upgrades to the US-Taiwan relationship.8 We would give a 60% probability to some kind of crisis over the next 12-24 months. The global equity market could at least suffer a 10% correction in a standard geopolitical crisis and it could easily fall 20% if US-China war appears more likely. What would trigger a full-fledged Taiwan war? We would grow even more alarmed if we saw one of three major developments: Chinese internal instability giving rise to a still more aggressive regime; the US providing Taiwan with offensive military capabilities; or Taiwan seeking formal political independence. The first is fairly likely, the second lends itself to miscalculation, and the third is unlikely. But it would only take one or two of these to increase the war risk dramatically. Bottom Line: The Taiwan Strait is still the critical geopolitical risk and Biden’s policy on China is still unclear. Iranian and North Korean tensions will escalate in the short run but the fundamental crisis lies in Taiwan. Since some kind of showdown is likely and war cannot be ruled out we advise clients to accumulate safe-haven assets like the Japanese yen and otherwise not to bet headlong against the US dollar until it loses momentum. Emerging Markets Round-Up In this section we will briefly update some important emerging market themes and views: Chart 8Favor USMCA Over Putin's Russia

Favor USMCA Over Putin's Russia

Favor USMCA Over Putin's Russia

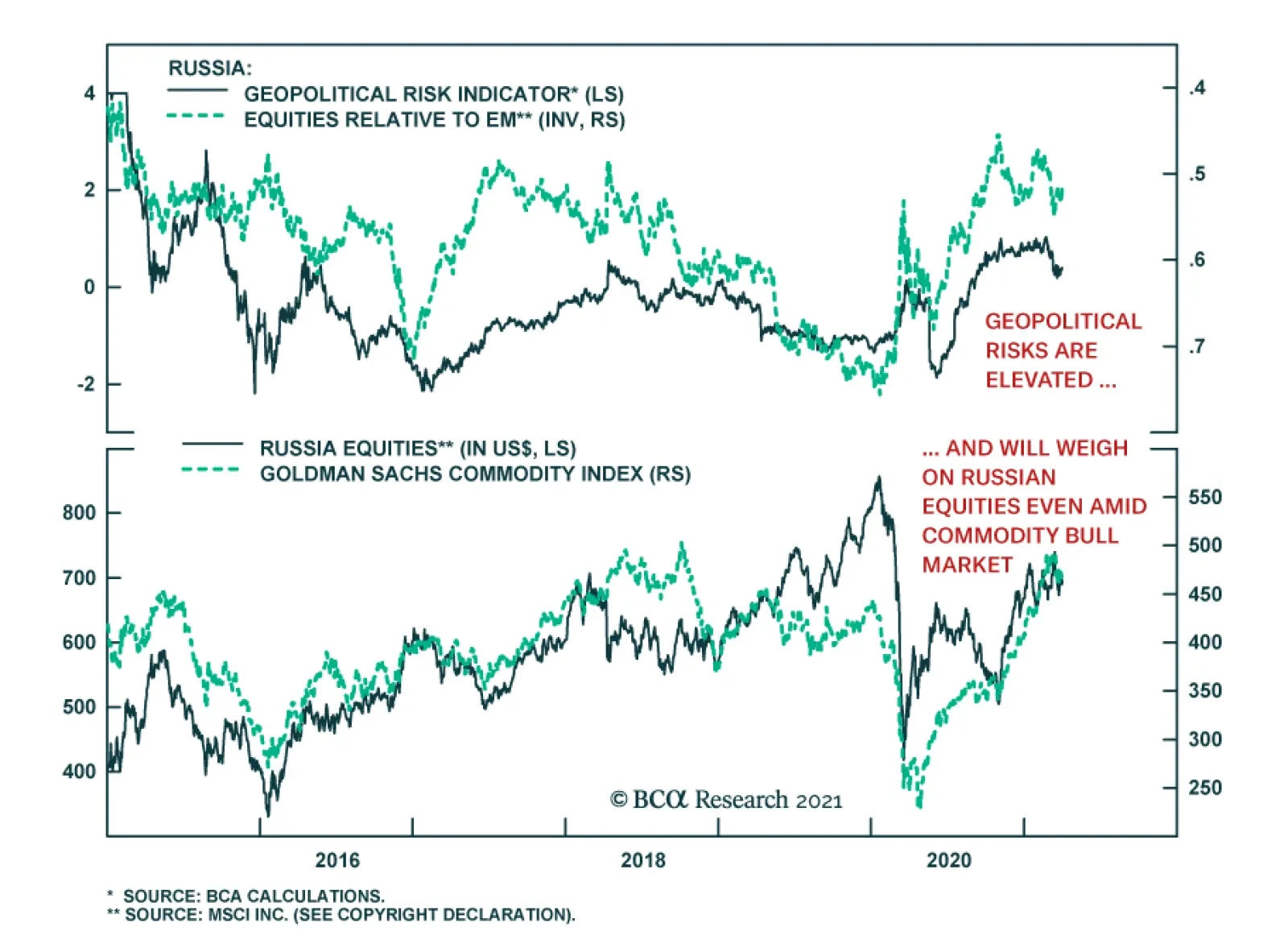

Russia: US-Russia tensions are escalating in the face of Biden’s reassertion of the US bid for liberal hegemony, which poses a direct threat to Russia’s influence in eastern Europe and the former Soviet Union. Ukraine is expected to see a renewed conflict this spring. The top US and Russian military commanders spoke on the phone for the second time this year after Ukrainian military reports indicated that Russia is amassing forces on the border. We also assign a 50/50 chance that the US will use sanctions to prevent the completion of the NordStream II pipeline from Russia to Germany, an event that would shake up the German election as well as provoke a Russian backlash. The Russian ruble has suffered a long slide since Putin’s invasion of Georgia in 2008 and Crimea in 2014 and the country’s currency and equities have not staged much of a comeback amid the global cyclical upswing and commodity price rally post-COVID. We recommend investors favor the Canadian dollar and Mexican peso as oil plays in the context of American stimulus and persistent Russian geopolitical risk (Chart 8). We also favor developed market European stocks over emerging Europe, which will suffer from renewed US-Russia tensions. Brazil: Brazilian President Jair Bolsonaro’s domestic political troubles are metastasizing as expected – the rally-around-the-flag effect in the face of COVID-19 has faded and his popular approval rating now looks dangerously like President Trump’s did, relative to previous presidents, which is an ominous warning for the “Trump of the South,” who faces an election in October 2022 (Chart 9). The COVID-19 deaths are skyrocketing, with intensive care units reaching critical levels across the country. The president has reshuffling his cabinet, including all three heads of the military in an unprecedented disruption that compounds fears about his willingness to politicize the military.9 Meanwhile the judicial system looks likely (but not certain) to clear former President Luiz Inácio Lula da Silva to run against Bolsonaro for the presidency, a potent threat (Chart 10). Bolsonaro’s three pillars of political viability have cracked under the pandemic: the country remains disorderly, the systemic corruption and the “Car Wash” scandal under the former ruling party are no longer at the center of public focus, and fiscal stimulus has replaced structural reform. Chart 9Brazil: Will ‘Trump Of The South’ Face Trump’s Fate?

The Arsenal Of Democracy

The Arsenal Of Democracy

Our Brazilian GeoRisk Indicator has reached a peak with Bolsonaro’s crisis – and likely breaking of the fiscal spending growth cap put in place at the height of the political crisis in 2016 – while Brazilian equities relative to emerging markets have hit a triple bottom (Chart 11). It is too soon for investors to buy into Brazil given that the political upheaval can get worse before it gets better and a Lula administration is no cure for Brazil’s public debt crisis, though a short-term technical rally is at hand. Chart 10Brazil’s Lula Looks To Be A Contender In 2022?

The Arsenal Of Democracy

The Arsenal Of Democracy

Chart 11Brazil: Policy Risk Peaks, Equities Hit Triple-Bottom Versus EM

Brazil: Policy Risk Peaks, Equities Hit Triple-Bottom Versus EM

Brazil: Policy Risk Peaks, Equities Hit Triple-Bottom Versus EM

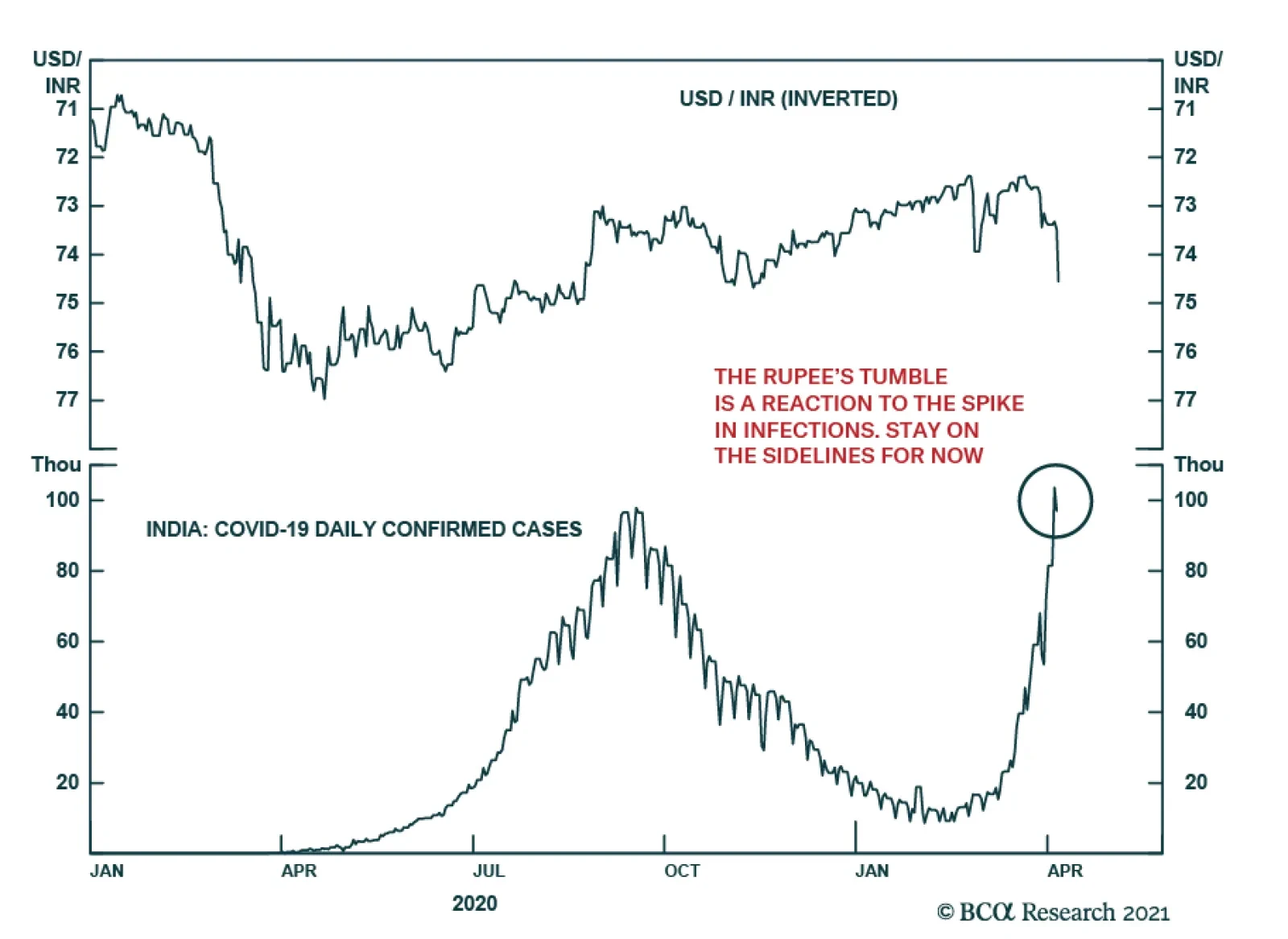

India: A lot has happened since we last updated our views on India, South Asia, and the broader Indian Ocean basin. Farmer protests broke out in India, forcing Prime Minister Narendra Modi to temporarily suspend his much-needed structural reforms to the agricultural sector, while China-backed military coup broke out in Myanmar, and the US election set up a return to negotiations with Iran and the Taliban in Afghanistan. Perhaps the biggest surprise was the Indo-Pakistani ceasefire, despite boiling tensions over India’s decision to make Jammu and Kashmir a federal union territory. The ceasefire is temporary but it does highlight a changing geopolitical dynamic in the region. India and Pakistan ceased fire along the Line of Control where they have fought many times. The ceasefire does not resolve core problems – Pakistan will not stop supporting militant proxies and India will not grant Kashmir autonomy – but it does show their continued ability to manage the intensity of disputes while dealing with the global pandemic. An earlier sign of coordination occurred after the exchange of air strikes in early 2019, which preceded the Indian election and suggested that India and Pakistan had the ability to control their military encounters. India’s move to revoke the autonomy of Jammu and Kashmir in August 2019, along with various militant operations, created the basis for another major conflict this year. After all, the Kargil war in 1999 followed nuclear weaponization, while the 2008 conflict followed the Mumbai attack. But instead India and Pakistan have agreed to a temporary truce. A major India-Pakistan conflict would be a “black swan” as nobody is expecting it at this point. Not coincidentally, India and China also reduced tensions after the flare-up in their Himalayan territorial disputes in 2020. China may be reducing tensions now that it no longer has to distract its population from Trump and the US election. China is shifting its focus to the Myanmar coup, another area where it hopes to parlay its influence with a Biden administration preoccupied with democracy and human rights. Sino-Indian tensions will resume later, especially as China continues its infrastructure construction at the farthest reaches of its territory for the sake of economic stimulus, internal control, and military logistics. The Biden administration is adopting the Trump administration’s efforts to draw India into a democratic alliance. But more urgently it is trying to withdraw from Afghanistan and cut a deal with Iran, which means it will need Indian and Pakistani cooperation and will want India to play a supportive role. Typically India eschews alliances and it will disapprove of Biden’s paternalism. For both China and Pakistan, making a temporary truce with India discourages it from synching up relations with the US immediately. Still, we expect India to cooperate more closely with the US over time, both on economic and security matters. This includes a beefed up “Quad” (Quadrilateral Security Dialogue) with Japan and Australia, which already have strong economic ties with India. Biden’s attempt to frame US foreign policy as a global restoration of democracy and liberalism will not go very far if he alienates the largest democracy in the world and in Asia. Nor will his attempt to diversify the US economy away from China or counter China’s regional assertiveness. Therefore Biden will have to take a supportive role on US-India ties. We are sticking with our contrarian long India / short China equity trade (Chart 12). India cannot achieve its geopolitical goals without reforming its economy and for that very reason it will redouble its structural reform drive, which is supported by changing voting patterns in favor of accelerating nationwide economic development. India will also receive a tailwind from the US and its allies as they seek to diversify production sources and reduce supply chain dependency on China, at least for health, defense, and tech. Meanwhile China’s government is pursing import substitution, deleveraging, and conflict with its neighbors and the United States. While Chinese equities are much cheaper than Indian equities on a P/E basis, they are not as pricey on a P/B and P/S basis (Chart 13) – and valuation trends can continue under the current macro and geopolitical backdrop. Indian equities are more volatile but from a long-term and geopolitical point of view, India’s moment has arrived. Chart 12Contrarian Trade: Stick To Long India / Short China

Contrarian Trade: Stick To Long India / Short China

Contrarian Trade: Stick To Long India / Short China

Bottom Line: Stay long Indian equities relative to Chinese and stay short Russian and Brazilian currencies and assets. These views are based on political and geopolitical themes that will remain relevant over the long run but are also seeing short-term confirmation. Chart 13Indian Stocks Not As Over-Priced On Price-To-Book, Price-To-Sales

Indian Stocks Not As Over-Priced On Price-To-Book, Price-To-Sales

Indian Stocks Not As Over-Priced On Price-To-Book, Price-To-Sales

Investment Takeaways To conclude we want to highlight two investment takeaways. First, while the market has rallied in expectation of the US stimulus package, Biden must now get the package passed. This roller coaster process, combined with the inevitable European recovery once the vaccine rollout gets on its feet (Chart 14), will power an additional rally in cyclicals, value stocks, and commodities. This is true as long as China does not tighten monetary and fiscal policy too abruptly, a risk we have highlighted in previous reports. Chart 14Europe's Vaccination Problem

Europe's Vaccination Problem

Europe's Vaccination Problem

While the US is pursuing “Buy American” provisions within its stimulus package, its growing trade deficit shows that it will be forced to import goods and services to meet its surging demand. This is beneficial for its nearest trade partners, Canada and Mexico, and Europe – as well as China substitutes further afield in some cases. Our European Investment Strategist Mathieu Savary has pointed out the opportunities lurking in Europe at a time when vaccine troubles and lockdowns are clouding the medium-term economic view, which is brightening. He recommends going long the “laggard” sectors and sub-sectors that have not benefited much relative to “leaders” that rallied sharply in the wake of last year’s stimulus, vaccine discovery, and defeat of President Trump (Chart 15). The laggard sectors are primed to outperform on rising US interest rates and decelerating Chinese economy as well (Chart 16). Therefore we recommend going long his basket of Euro Area laggards and short the leaders. Chart 15Europe’s Laggards And Leaders

The Arsenal Of Democracy

The Arsenal Of Democracy

Chart 16Macro Forces Favor The Laggards over the Leaders

Macro Forces Favor The Laggards over the Leaders