Emerging Markets

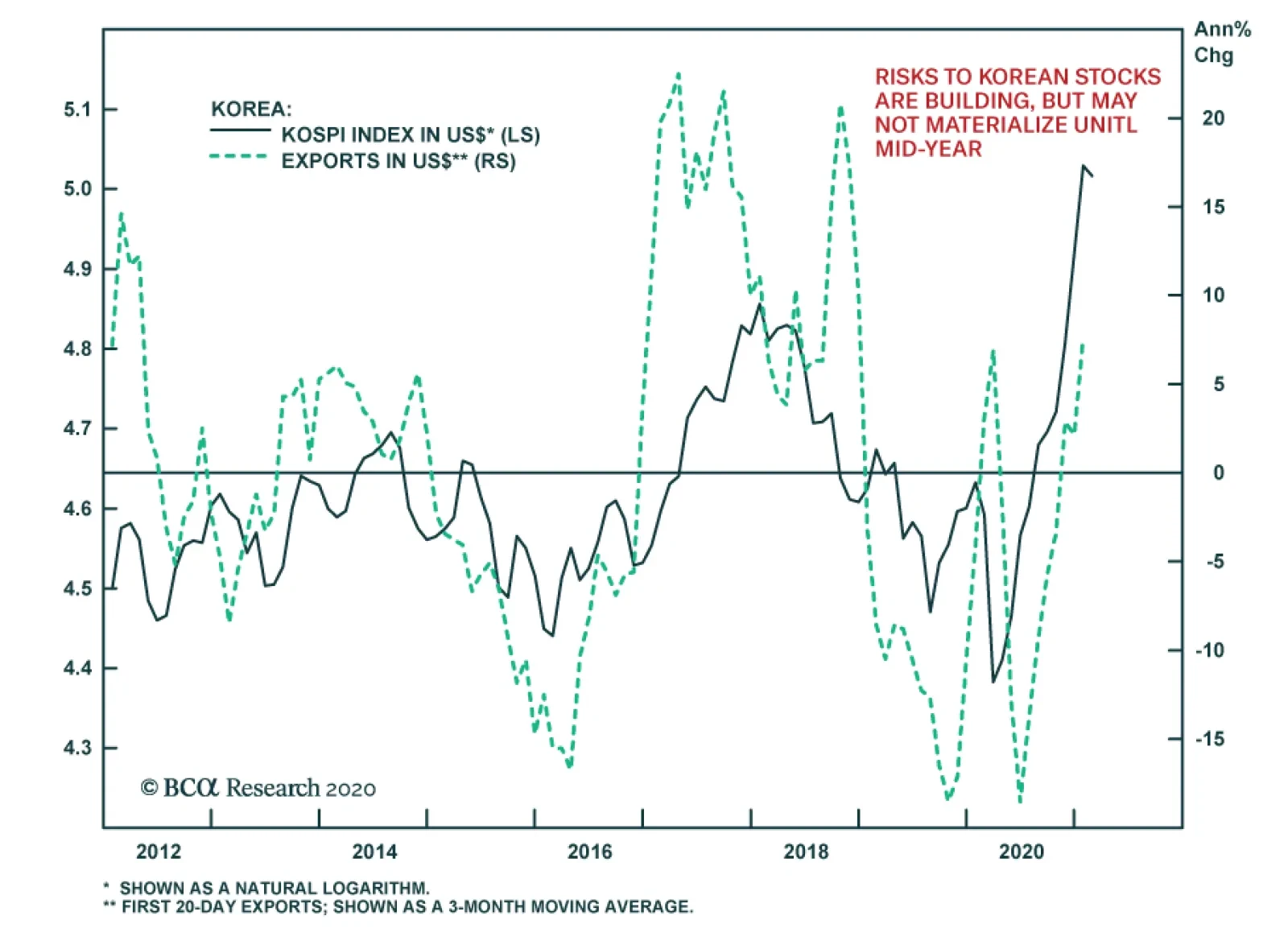

Korean equities have benefited greatly from booming retail investor demand, which has caused the KOSPI to more than double since mid-March. But the index has been trading sideways since the beginning of the year. What will the next move be? On the positive…

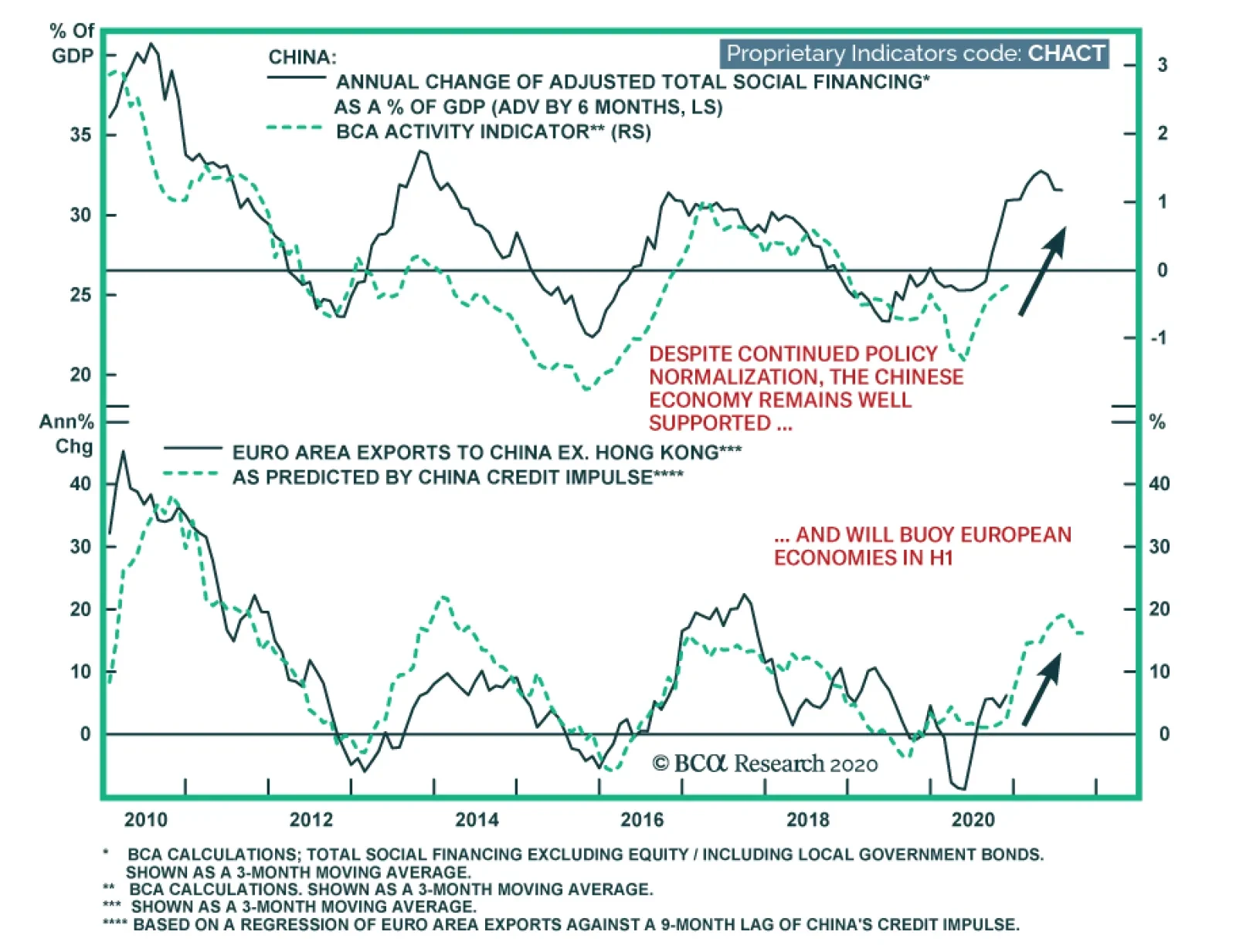

On the surface, China’s credit numbers were surprisingly strong in January. Aggregate financing was CNY 5.17 trillion from a revised CNY 1.72 trillion in December, significantly above expectations of CNY 4.60 trillion. New loans were a record CNY 3.58…

We have been worried about the deterioration in Chinese economic data amidst a rebounding dollar and over-extended prices for cyclical relative to defensive equities (see Today’s Pick). Nonetheless, we do not expect any resulting period of underperformance…

According to BCA Research’s Foreign Exchange Strategy service highlights a tactical opportunity to go short the AUD/MXN cross. Three catalysts underpin this thesis: relative economic activity, valuation, and sentiment. The Australian PMI has rebounded…

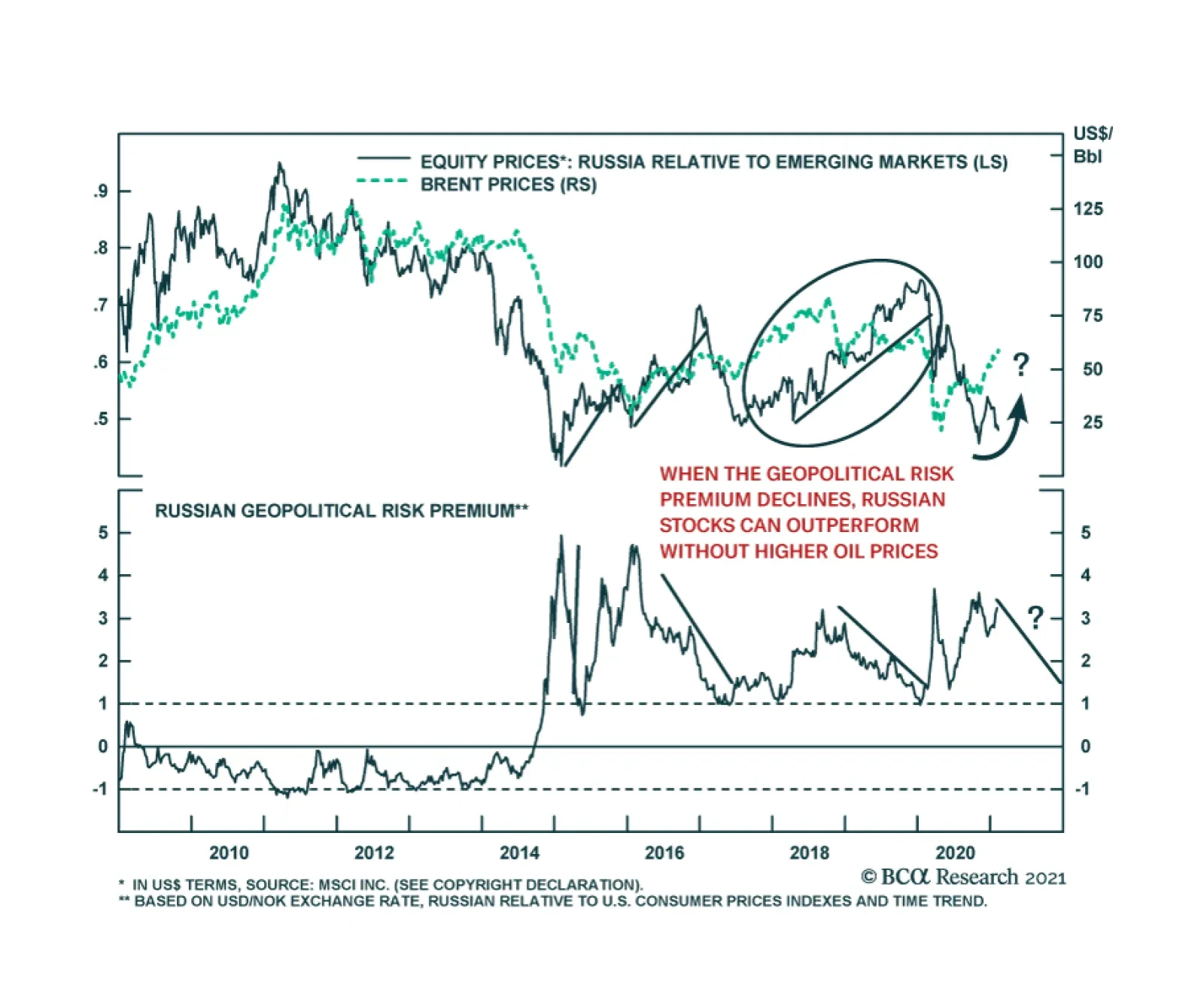

A tactical opportunity has emerged whereby investors should buy Russian stocks at the expense of the remainder of the EM benchmark. To begin with, Russian equities are cheap compared to other EM. On a relative price-to-book, price-to-sales and…

Highlights For the month of February, our trading model recommends shorting the US dollar versus the euro and Swiss franc. While we agree a barbell strategy makes sense, we would rather hold the yen and the Scandinavian currencies. In the near term, we recommend trades at the crosses, given the potential for the dollar rally to run further. An opportunity has opened up to short the AUD/MXN cross. We are tightening the stop on our short EUR/GBP position to protect profits. We believe EUR/CHF still has upside. While the US has been labelling Switzerland a currency manipulator, the real culprit is Europe. Precious metals remain a buy. We are placing a limit sell on the gold/silver ratio at 70, after our initial target of 65 was touched. Platinum should also outperform in 2021. Remain long AUD/NZD, as the key drivers (relative terms of trade and cheap valuation) remain intact. Feature Currency markets are at a crossroads. On the one hand, news on the vaccine front continues to progress, raising the specter that we might return to normalcy sometime in the second half of this year. On the other hand, the current lockdowns are slowing down economic activity across the developed world, which is bullish for the dollar. With the DXY index up 1.4% this year, it appears near-term economic weakness is dominating the currency market narrative. Our long-term trade basket is centered on a dollar-bearish theme, but we have been shifting much focus in the near term to non-US dollar opportunities. Central to this has been our conviction that the dollar is due for a countertrend bounce, in an order of magnitude of 2%-4%.1 It appears we are already halfway there (Chart I-1). For the month of January, our trade recommendations outperformed the model allocation. Notable trades were being short gold versus silver and being short EUR/GBP. Silver in particular was a big winner in January (Chart I-2). Most emerging market currencies saw weakness, especially the Korean won, Russian ruble, and Brazilian real Chart I-1The Dollar Has Been Strong In 2021

Portfolio And Model Review

Portfolio And Model Review

Chart I-2Our FX Portfolio Did Well In January

Portfolio And Model Review

Portfolio And Model Review

For the month of February, our trading model recommends shorting the US dollar, mostly versus the euro and Swiss franc (Chart I-3 and Chart I-4). The model gets its signal from three variables: Relative interest rates (both levels and rates of change), valuation, and sentiment.2 While some of these variables have moved in favor the dollar, the magnitude of these moves has not been sufficient to trigger a model shift. We agree a barbell strategy makes sense. That said, we would rather hold the yen (as the safe haven, compared to the CHF) and the Scandinavian currencies (compared to the EUR). These are our two strategic positions, and we made the case for yen long positions last week. Chart I-3Our FX Model Remains ##br##Short USD...

Our FX Model Remains Short USD...

Our FX Model Remains Short USD...

Chart I-4...Especially Versus The Euro And Swiss Franc

...Especially Versus The Euro And Swiss Franc

...Especially Versus The Euro And Swiss Franc

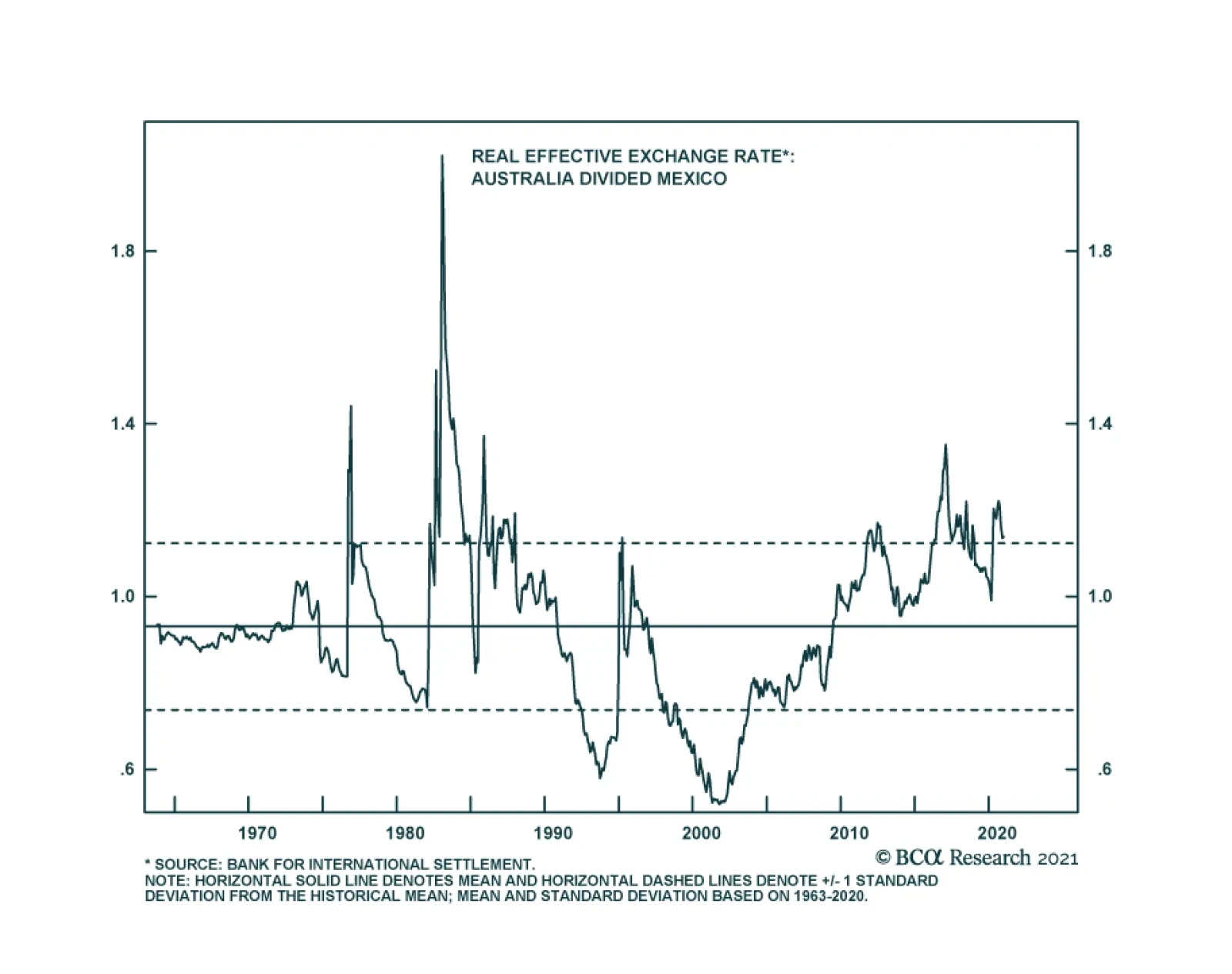

Circling back to our trades at the crosses, we maintain that they should continue to perform well in February and beyond. We revisit the rationale behind these trades, as well as introduce a new idea: Short the AUD/MXN cross. Go Short AUD/MXN A tactical opportunity has opened up to go short the AUD/MXN cross. Central to this thesis are three catalysts: relative economic activity, valuation, and sentiment. The Australian PMI has rebounded quite strongly relative to that in Mexico, driven by the performance of the Chinese economy, versus that of the US economy. Australia exports mostly to China, while Mexico is heavily tied to the US economy. With the Chinese credit impulse rolling over, the US economy has been outperforming of late. If past is prologue, this will herald a lower AUD/MXN exchange rate (Chart I-5). Correspondingly, oil prices are outperforming metals prices. China is the biggest consumer of metals, while the US is the biggest consumer of oil. A higher oil-to-metal ratio is negative for AUD/MXN. Terms of trade between Australia and Mexico have been an important driver of the exchange rate (Chart I-5). China had a massive restocking of metals last year, much more than oil and natural gas. This implies that the destocking phase (should it occur) will be most acute among metal inventories (Chart I-6), suggesting oil imports into China could fare better than metals. On a real effective exchange rate basis, the Aussie is expensive relative to the Mexican peso. Historically, this has heralded a lower exchange rate (Chart I-7). Chart I-5AUD/MXN And Terms Of Trade

Portfolio And Model Review

Portfolio And Model Review

Chart I-6Chinese Destocking: From Crude Oil To Metals?

Chinese Destocking: From Crude Oil To Metals?

Chinese Destocking: From Crude Oil To Metals?

Chart I-7AUD/MXN Is ##br##Expensive

AUD/MXN Is Expensive

AUD/MXN Is Expensive

Back in 2020, when everyone was short the Aussie and long the MXN, being a contrarian paid off handsomely. Now, speculators are roughly neutral both crosses. Should the trends we are highlighting carry on into the next few months, this will be a powerful catalyst for speculators to jump on the bandwagon. We recommend opening a short AUD/MXN trade today, with a stop loss at 16.50 and an initial target of 13. Stay Short EUR/GBP Chart I-8An Asymmetry In Pricing

An Asymmetry In Pricing

An Asymmetry In Pricing

Our short EUR/GBP position is performing well, amidst a more hawkish Bank of England this week. Technically, there remains room for much downside on the cross. Real interest rates in the UK are rising relative to those in the euro area. The Brexit discount has not been fully priced out of the EUR/GBP cross, whereas broad US dollar weakness has eroded the discount in cable (Chart I-8). From a technical perspective, speculators are still very long the EUR/GBP, even though our intermediate-term indicator is nearing bombed-out levels (Chart I-9). Chart I-9EUR/GBP Still Has Downside

EUR/GBP Still Has Downside

EUR/GBP Still Has Downside

Finally, short EUR/GBP tends to benefit from an outperformance of oil prices. We will be revisiting the fair value of the pound in upcoming reports given the fundamental shifts that are happening in the post-EU relationship. For now, we are tightening stops on our short EUR/GBP position to 0.89, in order to protect profits. Remain Long NOK And SEK Chart I-10NOK Follows Oil Prices

NOK Follows Oil Prices

NOK Follows Oil Prices

The Scandinavian currencies are extremely cheap and an attractive bet for 2021. As such, we believe the recent relapse in their performance provides an opportunity for fresh long positions. For the NOK, a rising oil price is bullish, both against the EUR and USD (Chart I-10). Meanwhile, superior handling of the pandemic has buoyed domestic economic data in Norway. Both retail sales and domestic inflation have been perking up, pushing the Norges Bank to dial forward expectations of a rate lift-off. Sweden is also holding up relatively well this year. Part of the reason for this is that over the years, the drop in the Swedish krona, both against the US dollar and euro, has made Sweden very competitive. With our models showing the Swedish krona as undervalued by 13% versus the USD, there is much room for currency appreciation before financial conditions tighten significantly. The bottom line is that both Norway and Sweden are well positioned to benefit from a global economic recovery, with much undervalued currencies that will bolster their basic balances. We expect both the SEK and NOK to remain the best performers versus the USD in the coming year. Stay Long EUR/CHF While the US has been labelling Switzerland a currency manipulator, the real culprit is the euro area. To be clear, the SNB has been actively intervening in the currency markets. However, when one looks at relative monetary policy, the expansion in the ECB’s balance sheet far outpaces that of the SNB (Chart I-11). With the correlation between balance sheet policy and the exchange rate shifting, it may embolden Switzerland to intervene even more strongly in currency markets. Historically, the Swiss franc was buffeted by the global environment (improving global trade) and rising productivity in Switzerland. As a result, the SNB had no alternative but to try to recycle those excess savings abroad by lifting its FX reserves, or see even stronger appreciation of its currency. With global trade much more muted, intervention in the FX market could be a more potent headwind for the franc. Chart I-11The SNB Is More Hawkish Than The ECB

The SNB Is More Hawkish Than The ECB

The SNB Is More Hawkish Than The ECB

Chart I-12EUR/CHF And The Global Cycle

EUR/CHF And The Global Cycle

EUR/CHF And The Global Cycle

In the near-term, the risk to this trade is that safe-haven flows reaccelerate, as investors re-price risk. However, this will be a short-term hiccup. EUR/CHF is a procyclical cross and will benefit from improvement in the Eurozone economy relative to the rest of the world (Chart I-12). Meanwhile, by many measures, the Swiss franc remains expensive versus the euro. Stay Long AUD/NZD Chart I-13RBA QE Will Hurt AUD/NZD

RBA QE Will Hurt AUD/NZD

RBA QE Will Hurt AUD/NZD

The rally in the kiwi has provided an exploitable opportunity to lean against it. We remain long the AUD/NZD cross, despite the RBA stepping up the pace of QE at its latest meeting. The rationale is as follows: The balance sheet of the RBA was already lagging that of the RBNZ, so the latest move is simply catch up (Chart I-13). It has no doubt been negative for the cross, as Australia-New Zealand rates have compressed. However, when the program expires, the AUD will be subject to external forces once again. The Australian bourse is heavy in cyclical stocks, notably banks and commodity plays, while the New Zealand stock market is the most defensive in the G10. Should value outperform growth, this will favor the AUD/NZD cross. The kiwi has benefited from rising terms of trade, as agricultural prices have catapulted higher. Should a correction ensue, as we expect, this will favor NZD short positions. Our conviction on long AUD/NZD has clearly been hit with the RBA’s latest move. As such, we are tightening stops to 1.05 for risk management purposes. Stay Long Precious Metals, Especially Silver And Platinum We are placing a limit sell on the gold/silver ratio at 70, after our initial 65 target was hit. The rationale for the trade remains intact: In a world of ample liquidity and a falling US dollar, gold and precious metals are bound to benefit. However, silver has underperformed the rise in gold. The long-term mean for the gold/silver ratio is 50, providing ample alpha for this trade (Chart I-14). Chart I-14The Case For Short Gold Versus Silver

The Case For Short Gold Versus Silver

The Case For Short Gold Versus Silver

Silver is heavily used in the electronics and renewable energy industries, which are capturing the new manufacturing landscape. Silver faced resistance near $30/oz. However, this will be a temporary hiccup. The next important level for silver will be the 2012 highs near $35/oz. After this, silver could take out its 2011 highs that were close to $50/oz, just as gold did. Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Footnotes 1 Please see our Foreign Exchange Strategy report, "Sizing A Potential Dollar Bounce," dated January 15, 2021. 2 Please see our Foreign Exchange Strategy report, "Introducing An FX Trading Model," dated April 24, 2020. Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades

BCA Research’s Emerging Markets Strategy service concludes that we are in a euphoria phase where fundamentals are less pertinent. The market can either rally or fall significantly, regardless of the profit outlook. In all likelihood, volatility will continue…

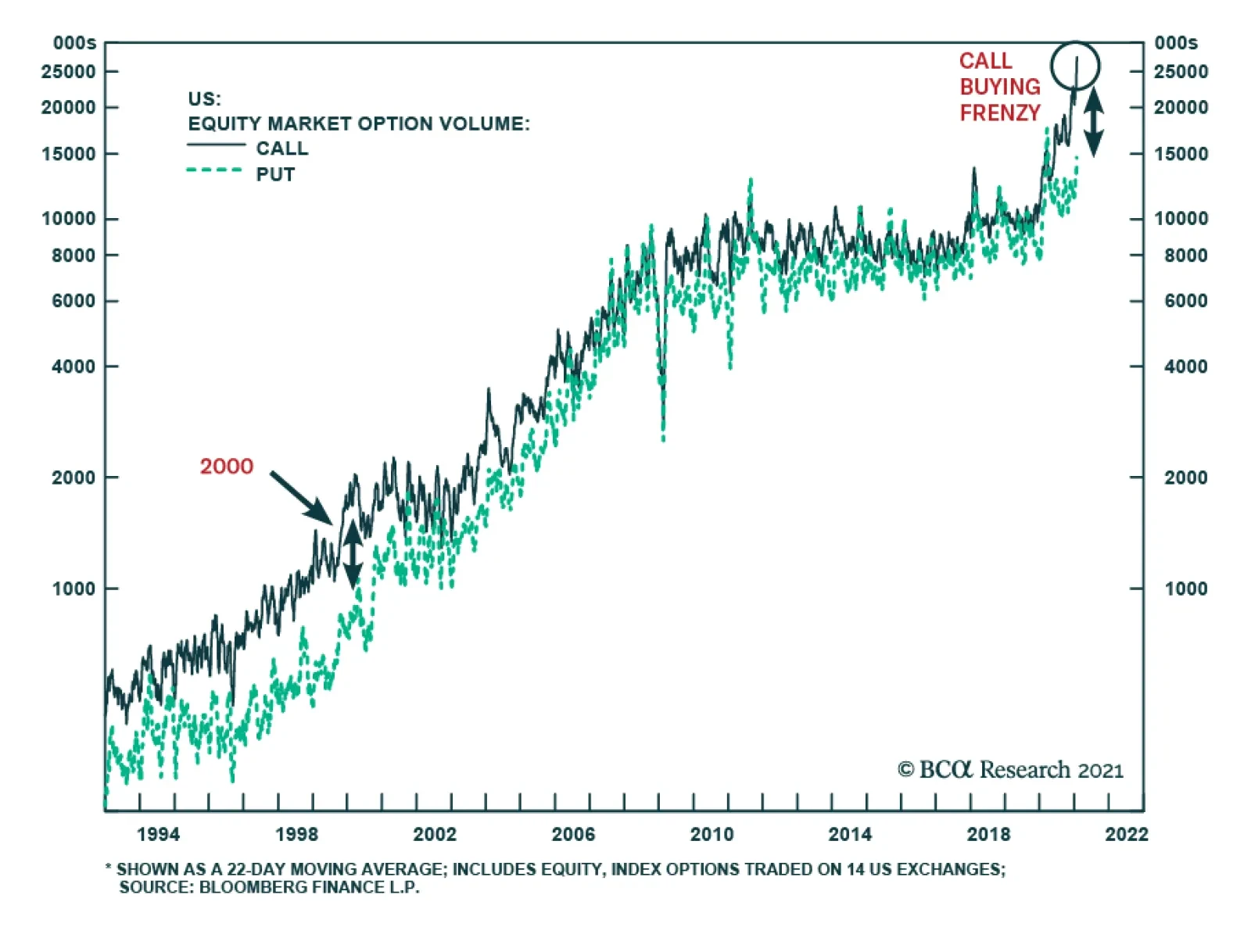

Highlights There is too much euphoria and complacency in global markets. The main distinction between the current and previous episodes of speculative equity market excesses is that classic end-of-business cycle conditions – such as economic overheating and policy tightening – are now absent. Yet, it does not mean that the bull market will continue uninterrupted. This rally might be short circuited by gravitational forces as happened with the S&P 500 in 1987 and Chinese onshore stocks in 2015. Investors should consider going long EM equity or EM currency volatility to hedge their exposure. Feature There is growing evidence that the global equity rally has turned into a frenzy. Signs of investor euphoria include: The number of traded call options in the US equity market has surged to an all-time high (Chart 1). The number of put options has spiked only in the past couple of weeks and remains well below the number of call options. Chart 1A Call Buying Frenzy Is A Symptom Of Investor Exuberance

A Call Buying Frenzy Is A Symptom Of Investor Exuberance

A Call Buying Frenzy Is A Symptom Of Investor Exuberance

Critically, there is currently too much complacency: the US put-call ratio is as low as it was in 2000 (Chart 2). The volume of stocks traded on and off all US stock exchanges has exploded since late October, reaching an all-time high (Chart 3). Chart 2A Sign Of Equity Market Complacency

A Sign Of Equity Market Complacency

A Sign Of Equity Market Complacency

Chart 3US Equity Trading Volumes Are At All-Time Highs

bca.ems_wr_2021_02_04_c3

bca.ems_wr_2021_02_04_c3

Chart 4Retail Investors Haven Been A Powerful Force In Korea And Taiwan

Retail Investors Haven Been A Powerful Force In Korea And Taiwan

Retail Investors Haven Been A Powerful Force In Korea And Taiwan

Equity fervor is prevalent not only among American individual investors but also in many parts of the world. For instance, the breathtaking rallies in the KOSPI and Taiwanese stocks has been primarily driven by local retail investors, as shown in Chart 4. The surge in Taiwanese share prices is stunning because it completely ignores the escalating geopolitical tensions over Taiwan. BCA Research’s Chief Geopolitical Strategist, Matt Gertken, recently argued that while China is unlikely to invade Taiwan immediately, a military stand-off cannot be ruled out. China and the US have yet to arrive at a mutual understanding regarding China’s access to computer chips made in Taiwan. Overall, since the lockdowns in March last year, individual investors have rushed into equities in many countries such as the US, Korea, Taiwan, Japan, India and Brazil, to name a few. Finally, US institutional investors are fully invested, as shown in Chart 5. Besides, Chart 6 reveals that US-domiciled EM equity mutual funds’ liquidity ratio (cash as a percentage of assets) is very low. Chart 5US Institutional Investors Are Long Stocks

US Institutional Investors Are Long Stocks

US Institutional Investors Are Long Stocks

Chart 6US-Domiciled EM Mutual Funds' Cash Is Low

US-Domiciled EM Mutual Funds' Cash Is Low

US-Domiciled EM Mutual Funds' Cash Is Low

There have been doubts within the global investment community about the potential for small individual investors to move the needle in the overall market. We believe that their impact has been substantial: First, there is plenty of anecdotal evidence to suggest that individual traders have been involved in options trading since the pandemic erupted. By purchasing call options, retail investors exert substantial upward pressure on share prices: dealers – who sell/write call options – typically hedge their risks by acquiring and holding the underlying stock for the duration of respective options. In short, by putting even small amounts of money at work to purchase call options, individual traders meaningfully affect share prices. Second, price formation in financial markets is influenced by the marginal investor. Everything else being equal, the entry of a new buyer into the marketplace leads to higher prices. Further, retail investors’ impact on financial markets has not been limited solely to stocks they purchase. Rather, there has been a ripple effect on the broader market. For instance, there is evidence that individual investors flocked to the market in March and April and bought en masse shares of companies most negatively affected by the pandemic, such as cruise operations, hotels, airlines and energy producers. As individual investors provided substantial bids for these stocks, institutional investors were able to offload these stocks and buy others. For instance, in Q2 last year Warren Buffett offloaded his airline stocks and allocated that capital to natural gas storage and pipelines, banks, pharma and auto stocks. If retail investors had not provided support to stocks of companies hit hard by the lockdowns and social distancing, Warren Buffett and other professional investors would not have had the opportunity to exit their positions in these stocks at acceptable prices and acquire other securities. This is the mechanism whereby the impact of new market entrants extends beyond the specific equities they purchase. Chart 7A Mini Call Option Mania Among Retail Investors

A Mini Call Option Mania Among Retail Investors

A Mini Call Option Mania Among Retail Investors

Finally, Charts 1 and 3 above clearly illustrate the surge in both the number of call options and trading volumes since last March. Among call options, transactions with a small number of options have ballooned (Chart 7). This reflects individual investors activity. Consistently, the number of brokerage accounts for retail investors has mushroomed in the US and elsewhere. Bottom Line: It is obvious that the ongoing equity market euphoria is considerable. Individual investors have been playing a vital role in fostering it. The GameStop stock saga, among others, reinforces this point. When And How Will It End? This bull market shares some similarities with previous market cycles, but it also has its distinct features. Similarities: Retail investors typically rush into financial markets toward the end of a bull market. The current US equity market rally began in 2009. After the S&P 500 showed its resilience by rebounding quickly and making new highs following the selloffs in 2015, 2018 and 2019, retail investors were reassured to jump on the bull market train when the 2020 crash occurred. In short, it took about 11 years of a US equity bull run for individual investors to feel comfortable enough to play the stock market. This is a characteristic of a late cycle/mature bull market. Speculative instruments and schemes are designed and launched. The IPO boom in SPACs1 will probably go down in history as a key feature of the speculative excesses in this cycle. Valuations overshoot during stock market euphoria but investors find reasons to justify lofty equity multiples. FAANGM stocks and other parts of the US equity market are expensive, but investors are using extremely low US bond yields – artificially suppressed by the Federal Reserve – to justify the current multiples. In such a case, the bond market will likely hold equities hostage. As bond yields rise going forward, equity valuations will be threatened. In fact, we believe rising bond yields, not the outlook for economic growth, to be the primary risk to US share prices akin to the late 1960s (Chart 8). Differences: Typically, retail investors feel comfortable investing in the stock market when the economy is strong. In this cycle, they jumped on the stock market train when the economy crashed due to the pandemic. This is a departure from previous cycles. Massive stimulus and ongoing vaccination deployment suggest the economic outlook for the US and many emerging economies is positive. In particular, EM corporate profits are set to recover (Chart 9). Chart 8The US In The 1960s: Share Prices And Treasury Yields

The US In The 1960s: Share Prices And Treasury Yields

The US In The 1960s: Share Prices And Treasury Yields

Chart 9EM EPS Is To Recover

EM EPS Is To Recover

EM EPS Is To Recover

Hence, it is hard to be bearish on stocks based on the cyclical outlook for growth, assuming vaccination campaigns will allow many major economies to fully reopen in H2 2021. Yet, a lot of this good news seem to be already priced in. Retail investors arrive to the stock market party usually in the late stage of a business cycle – when unemployment is low, inflation is rising, and policymakers are tightening policies. That combination proves lethal for the equity market and a major top in share prices ensues. Presently, due to the pandemic-induced lockdowns, we have the opposite occurring in the US and in many EM economies. Unemployment is high, inflation remains contained, and policymakers are committed to providing unlimited stimulus. In short, the main distinction between the current and previous episodes of speculative equity market excesses is that classic end-of-business cycle conditions – such as economic overheating and policy tightening – are now absent. History doesn't repeat itself, but it does rhyme. Does it mean that the bull market will continue uninterrupted? Not necessarily. This rally might be short circuited for reasons that may differ from those that terminated previous stock market frenzies. First, speculative bubbles could burst without policy tightening. An example of this is China’s equity bubble in 2015, which crashed without policy tightening due to gravitational forces reasserting themselves. Another example is the 1987 US stock market crash that occurred without an economic or fundamental financial cause. Chart 10 illustrates the cyclical trajectories of US GDP and the Fed funds rate did not change materially before and after the equity market crash. In short, the 1987 equity crash was a case when excessive speculation/overbought conditions rather than policy tightening or a recession caused an abrupt equity sell-off. Second, in the EM equity universe, leadership has been extremely narrow. Only a handful of companies have outperformed the aggregate benchmark, propelling the index to 2007 highs. These include a few Chinese new economy stocks, and Korean and Taiwanese technology stocks (Chart 11). Outside North Asian markets (China, Korea and Taiwan), every single EM bourse has underperformed both the EM and global equity benchmarks in the past year. Chart 10The 1987 S&P 500 Crash Was Not Caused By The Fed Or The Economy

The 1987 S&P 500 Crash Was Not Caused By The Fed Or The Economy

The 1987 S&P 500 Crash Was Not Caused By The Fed Or The Economy

Chart 11Euphoria In Asian TMT Stocks

Euphoria in Asian TMT Stocks

Euphoria in Asian TMT Stocks

Chart 12Global ex-TMT Stocks Have Not Broken Out Yet

bca.ems_wr_2021_02_04_c12

bca.ems_wr_2021_02_04_c12

If these global and EM TMT stocks relapse, they will inflict major damage on the EM and global indexes. The EM index has become extremely concentrated with the top five stocks accounting for 24% of the MSCI EM equity index’s market cap. Interestingly, global ex-TMT stocks have not yet broken out to new highs (Chart 12). Finally, US overall equity and global TMT valuations are vulnerable to rising US bond yields. The latter could rise without the Fed hinting at policy tightening if fixed-income investors decide that the Fed is behind the inflation curve. This could trigger a major selloff even if policymakers do not tighten policy. Investment Conclusions Chart 13Go Long EM Equity And Currency Volatility

Go Long EM Equity And Currency Volatility

Go Long EM Equity And Currency Volatility

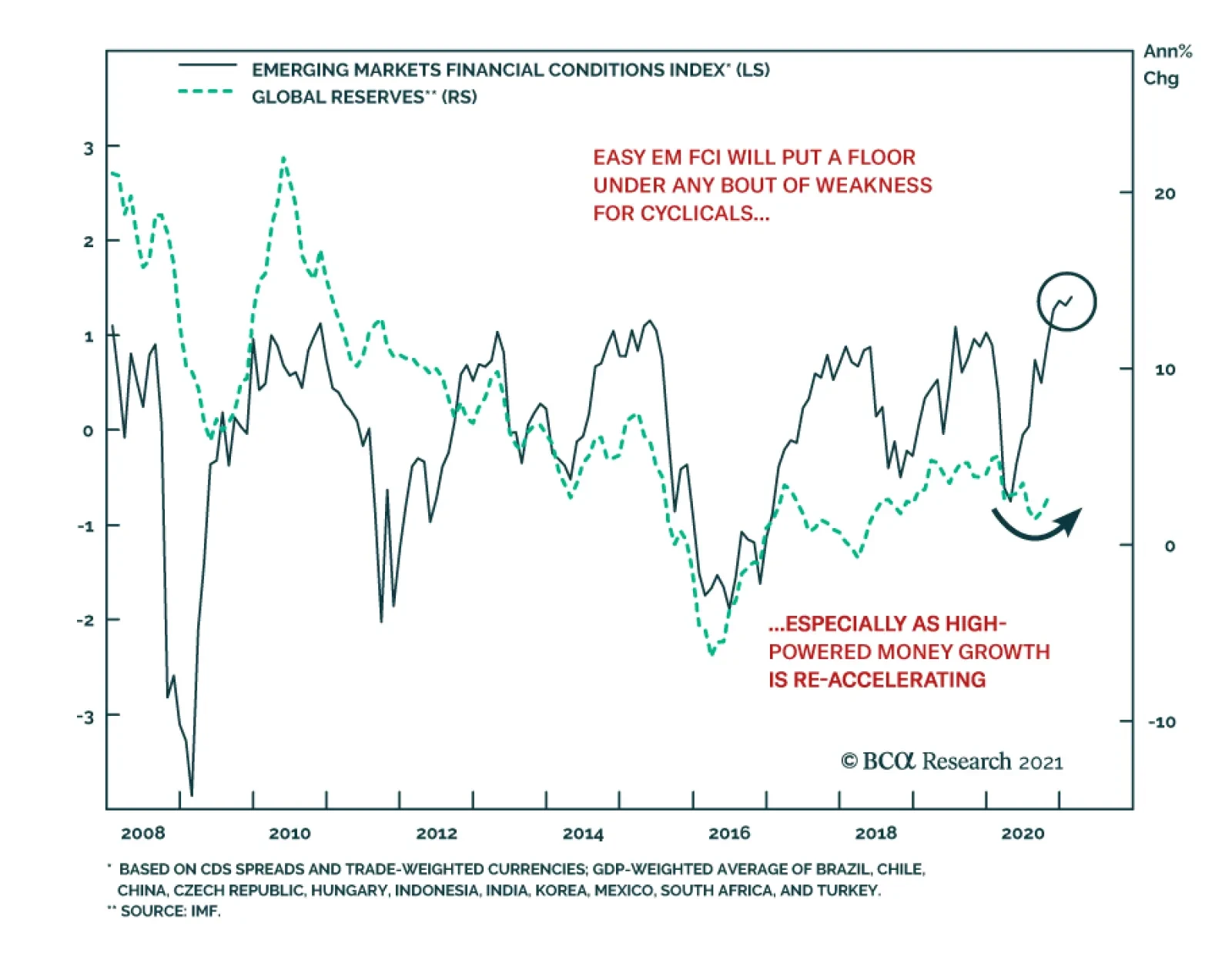

We are in a euphoria phase where fundamentals are less pertinent. The market can either rally a lot or sell off hard regardless of the profit outlook. Navigating through such markets is challenging. Going long EM equity or EM currency volatility offers a good risk-reward profile (Chart 13). Volatility will likely rise in the coming months in both scenarios: either risk assets continue rallying or they sell off. For global equity and credit portfolios, we continue recommending a neutral allocation to EM. The long-term US dollar outlook is negative, but it is oversold and odds of a near-term rebound are still high. Our currency strategy remains to short a basket of EM currencies versus an equal-weighted average of the euro, CHF and JPY. This basket of EM currencies includes the BRL, CLP, ZAR, KRW and TRY. We continue receiving 10-year swap rates in Mexico, Colombia, Russia, China, India, Indonesia and Korea. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Footnotes 1 Special Purpose Acquisition Companies (SPAC), also known as “blank check companies”, are organizations with no commercial operations that raise capital through an IPO, which is then deployed to purchase an existing company. This process is done to bypass the lengthy process of launching a traditional IPO for a young company. Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

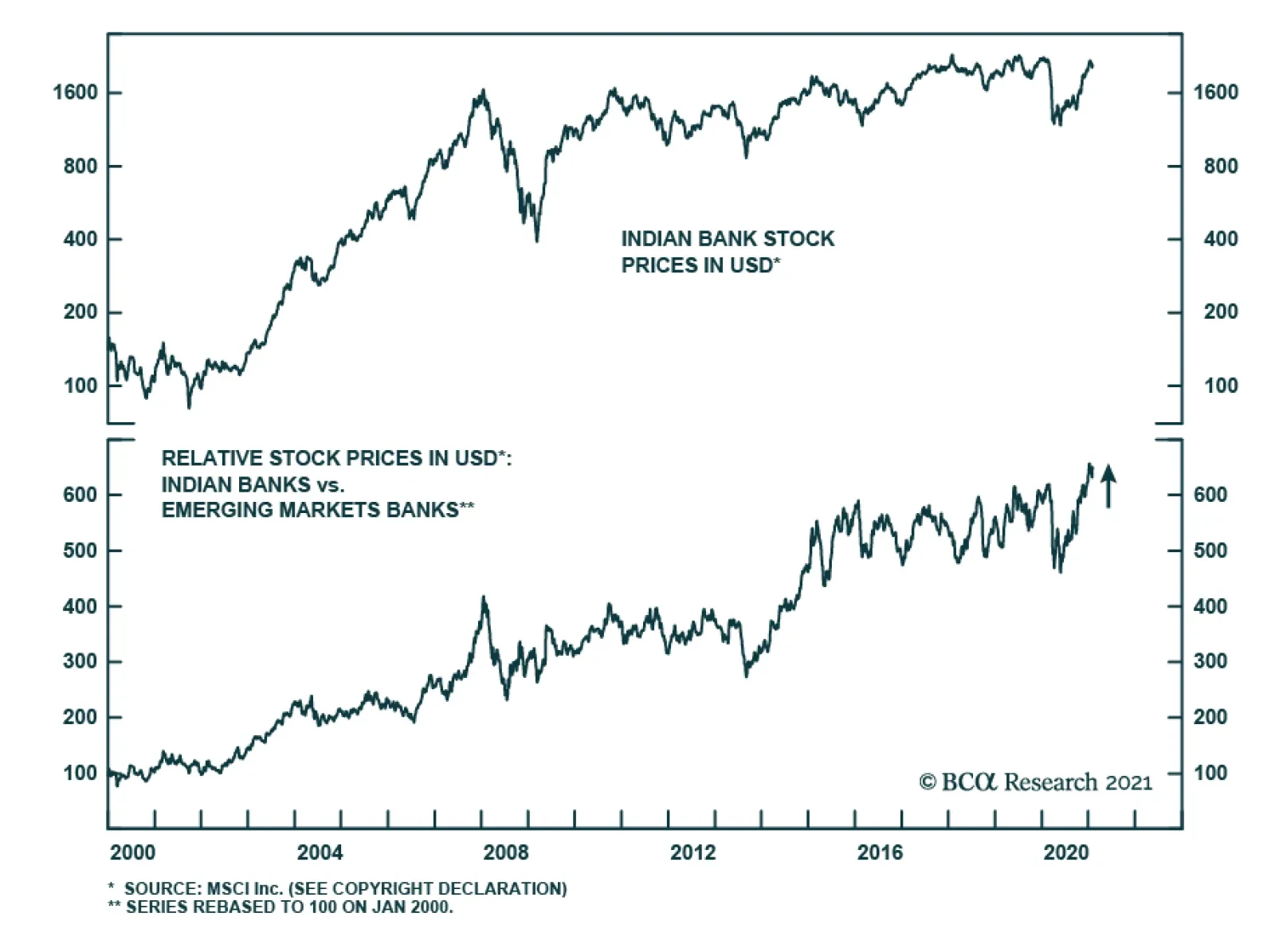

BCA Research’s Emerging Markets Strategy service recommends that investors should go long Indian banks and short EM banks. Indian bank stocks have been the star performers among emerging markets banks over the past 20 years. They have consistently…

Highlights Chart 1China's PMIs Dropped In January

China Macro And Market Review

China Macro And Market Review

January’s official PMI suggests that China’s economic recovery started the year on a weaker note. While both manufacturing and non-manufacturing PMIs remain in expansionary territory, the moderation was larger than in previous Januarys, which implies that more than seasonal factors were at play (Chart 1). The lockdowns in January due to a resurgence of COVID-19 cases in China are distorting business activities. Moreover, travel restrictions imposed for the upcoming Lunar New Year (LNY) will profoundly affect household consumption and the service sector in February and perhaps into March. Chinese stock prices, on the other hand, registered gains in January in both onshore and offshore markets. As noted in last week’s report, Chinese stocks face downside risks in the near term and we recommend that investors turn cautious. Economic and profit growth may disappoint in the first quarter, against a tightening policy backdrop. Feature Monetary Policy Normalization Remains On Track In the past three weeks, the PBoC drained short-term liquidity on a net basis from the interbank system. This action reversed market expectations in earlier January that the central bank would start to loosen monetary stance. Chart 2Chinas Monetary Policy Unlikely To Change Course When The Economy Strengthens

Chinas Monetary Policy Unlikely To Change Course When The Economy Strengthens

Chinas Monetary Policy Unlikely To Change Course When The Economy Strengthens

The soft patch in China’s first-quarter economic recovery may prompt the PBoC to temporarily slow the pace of interest rate tightening, but it is unlikely that policymakers will reverse their policy normalization over the next 6 to 12 months (Chart 2). The authorities have been increasingly concerned about asset price inflation. In our view, near-term policy shifts will be tied to asset prices rather than consumer prices. The PBoC stated that its policymaking will be data dependent, but it may not succumb to a marginally slower recovery, particularly if the weakness proves to be transitory. Moreover, the unprecedented growth contraction from Q1 last year will boost economic data in the first three months of this year due to a low base effect. This year’s monetary policy could be reminiscent of 2019 when the PBoC frequently adjusted the short-term interbank rate (i.e. 1- to 7-days) while keeping the longer rate (3-month repo rate) mostly trendless throughout the year (Chart 3). In this scenario, China's 10-year government bond yield will not rise by as much as in 2017-2018 (Chart 4). Without a substantial improvement in profit growth, however, a slower rise in bond yields will be only marginally positive for Chinese stocks (Chart 4, bottom panel). Chart 3Policy Normalization Remains On Track

Policy Normalization Remains On Track

Policy Normalization Remains On Track

Chart 4Smaller Bond Yield Hikes Are Marginally Positive For Chinese Stocks

Smaller Bond Yield Hikes Are Marginally Positive For Chinese Stocks

Smaller Bond Yield Hikes Are Marginally Positive For Chinese Stocks

Corporations May Not Deliver Strong Profit Growth In 2021 Chart 5An Impressive Profit Recovery Supported The Stock Rally In 2H20

An Impressive Profit Recovery Supported The Stock Rally In 2H20

An Impressive Profit Recovery Supported The Stock Rally In 2H20

The newly released industrial profits data showed a sharp rebound in growth this past December, with the annual profit up by 4.1% over 2019. An impressive recovery in profit growth in the second half of last year helped to drive up Chinese stock prices (Chart 5). However, the magnitude of the rally in stock prices has been much more substantial than implied by the underlying profit growth. Industrial profits have barely recovered to their 2018 levels, while A shares have jumped by 40% in the past two years (Chart 5, bottom panel). Moreover, the strong recovery in profit growth may not be sustainable in 2021. While sales revenues may pick up even more this year, operating costs will likely increase, which would compress corporate profit margins (Chart 6). Lower operating costs from last year’s cheaper financing and growth-support policies, such as tax cuts and loan payment deferrals, helped to widen corporate profit margins. China’s social security contribution exemption and reduction policy reduced the cost burden of enterprises by 1.5 trillion yuan in 2020. Moreover, cheaper global commodity and oil prices in earlier 2020 also lowered China’s industrial input prices (Chart 7). Chart 6Increasing Operation Costs May Weigh On Industrial Profit Margins

Increasing Operation Costs May Weigh On Industrial Profit Margins

Increasing Operation Costs May Weigh On Industrial Profit Margins

Chart 7Input Prices Have Risen Faster Than Output Prices

Input Prices Have Risen Faster Than Output Prices

Input Prices Have Risen Faster Than Output Prices

Chart 8Product Inventories And Account Receivables Have Not Fully Recovered

Product Inventories And Account Receivables Have Not Fully Recovered

Product Inventories And Account Receivables Have Not Fully Recovered

The normalization of policy rates and bond yields along with the rebound in commodity prices will weigh on industrial profit margins and profit growth this year. Furthermore, some cost-reduction benefits will be rolled back: policymakers have announced an end to the social security contribution waiver for corporations in 2021. However, they will extend the reduction of unemployment insurance from the end of April 2021 to April 2022. It is still unclear whether China will grant the same scale of corporate tax relief this year as it did in 2020. We note that industrial inventory turnover has not recovered to its pre-pandemic level, finished product inventories remain high, and accounts receivable payments are taking longer to reach businesses compared with 2019. All these factors highlight a lack of vigor in the industrial sector’s recovery (Chart 8). Travel Restrictions Will Dampen Q1 Economic Growth Chart 9A New Wave Of COVID-19 Cases In China

A New Wave Of COVID-19 Cases In China

A New Wave Of COVID-19 Cases In China

New travel restrictions may cause some short-term distortion in China’s aggregate economy in the first quarter. China announced inter-provincial travel constraints for the LNY, effective between January 28 and March 8, due to a resurgence of COVID-19 cases in Beijing and the northern provinces (Chart 9). Local authorities urged migrant workers to stay in their work places and not return to their hometowns. According to the Ministry of Transport, it is estimated that around 50% of migrant workers will remain in place during the LNY. Manufacturing production (secondary industry) may increase slightly because workers will take fewer vacation days during the LNY. Nevertheless, the positive effect will be more than offset by large losses from consumption and tourism (tertiary industry). Reduced consumption from holiday travel, restaurant dining, offline shopping and services will overwhelm online retail sales of goods and services. All these factors will negatively impact Q1 GDP because tertiary industry accounts for around 55% of China’s GDP, a much larger slice than secondary industry1 (Chart 10). January’s PMI shows that after narrowing in the past six months, the gap between production (supply) and new orders (demand) sub-indexes widened again in January (Chart 11). We expect the travel restrictions to exacerbate the goods oversupply in February and perhaps even into March. Chart 10New Travel Restrictions Will Have A Negative Impact On Q1 GDP

New Travel Restrictions Will Have A Negative Impact On Q1 GDP

New Travel Restrictions Will Have A Negative Impact On Q1 GDP

Chart 11Goods Oversupply May Last Through Q1

Goods Oversupply May Last Through Q1

Goods Oversupply May Last Through Q1

Lingering Deflationary Pressures While headline CPI moved back into inflationary territory in December, mainly driven by food price increases, core CPI has fallen to its lowest level since late 2010 (Chart 12). Prices for some key consumer goods and services remain firmly in deflation and they may deteriorate further in Q1 due to a high price base during last year’s LNY. Chart 12Lingering Deflationary Pressures On Consumer Prices

Lingering Deflationary Pressures On Consumer Prices

Lingering Deflationary Pressures On Consumer Prices

Chart 13PPI Will Likely Turn Positive In Q1 Due To Low Base Effect

PPI Will Likely Turn Positive In Q1 Due To Low Base Effect

PPI Will Likely Turn Positive In Q1 Due To Low Base Effect

Chart 14A Stronger RMB Will Exacerbate Deflationary Pressures

A Stronger RMB Will Exacerbate Deflationary Pressures

A Stronger RMB Will Exacerbate Deflationary Pressures

PPI deflation has eased and will probably turn positive in Q1 this year, supported by an expansionary business cycle and a low base (Chart 13). However, the risk of deflation may resurface in the second half of the year as stimulus effects subside. As such, China’s corporate profit growth will again face downward pressure, which would be exacerbated by a stronger RMB and rising real interest rate (Chart 14). Shipping Disruptions Should Be Transitory China’s export sector remains strong, benefiting from improving global demand and strength in China’s manufacturing supply chains. The drop in January’s PMI export new orders sub-index was mainly seasonal and could be due to the recent pandemic-related logistical disruptions and bottlenecks at ports (Chart 15). The recent massive jump in freight costs reflects these one-off factors and bouts of inflation this year due to disruptions in logistics, which will likely prove to be transitory (Chart 16). Chart 15Exports Should Remain Robust Through 1H21

Exports Should Remain Robust Through 1H21

Exports Should Remain Robust Through 1H21

Chart 16A Jump In Freight Costs is Probably Transitory

A Jump In Freight Costs is Probably Transitory

A Jump In Freight Costs is Probably Transitory

Real Estate Sector Under Stricter Scrutiny Housing demand and prices in top-tier cities picked up again in December despite rising mortgage rates and more restrictive bank lending to the real estate sector (Chart 17). In our view, the rebound in floor space started will be short-lived, and the gap between floor space started and completed will continue to converge (Chart 18). Real estate developers face stricter borrowing regulations and the rate of expansion of new projects will slow this year due to shrinking land transfers in 2020. Still, real estate developers will continue to finish their existing projects and promote new home sales. Therefore, on a net basis, we expect real estate investment and construction activities to remain stable in the first half of 2021. Chart 17Housing Demand In First Tier Cities Climbed Again In December

Housing Demand In First Tier Cities Climbed Again In December

Housing Demand In First Tier Cities Climbed Again In December

Chart 18A Rebound In Floor Space Started May Be Short lived

A Rebound In Floor Space Started May Be Short lived

A Rebound In Floor Space Started May Be Short lived

Table 1China Macro Data Summary

China Macro And Market Review

China Macro And Market Review

Table 2China Financial Market Performance Summary

China Macro And Market Review

China Macro And Market Review

Qingyun Xu, CFA Senior Analyst qingyunx@bcaresearch.com Jing Sima China Strategist jings@bcaresearch.com Footnotes 1China’s secondary industry is mainly comprised of mining, manufacturing, the production and supply of electricity, gas and water, and construction. The tertiary industry refers to traffic, storage and mail businesses, information transfer, computer services and software, wholesale and retail trade, accommodation and food, finance, and other services. Cyclical Investment Stance Equity Sector Recommendations