Emerging Markets

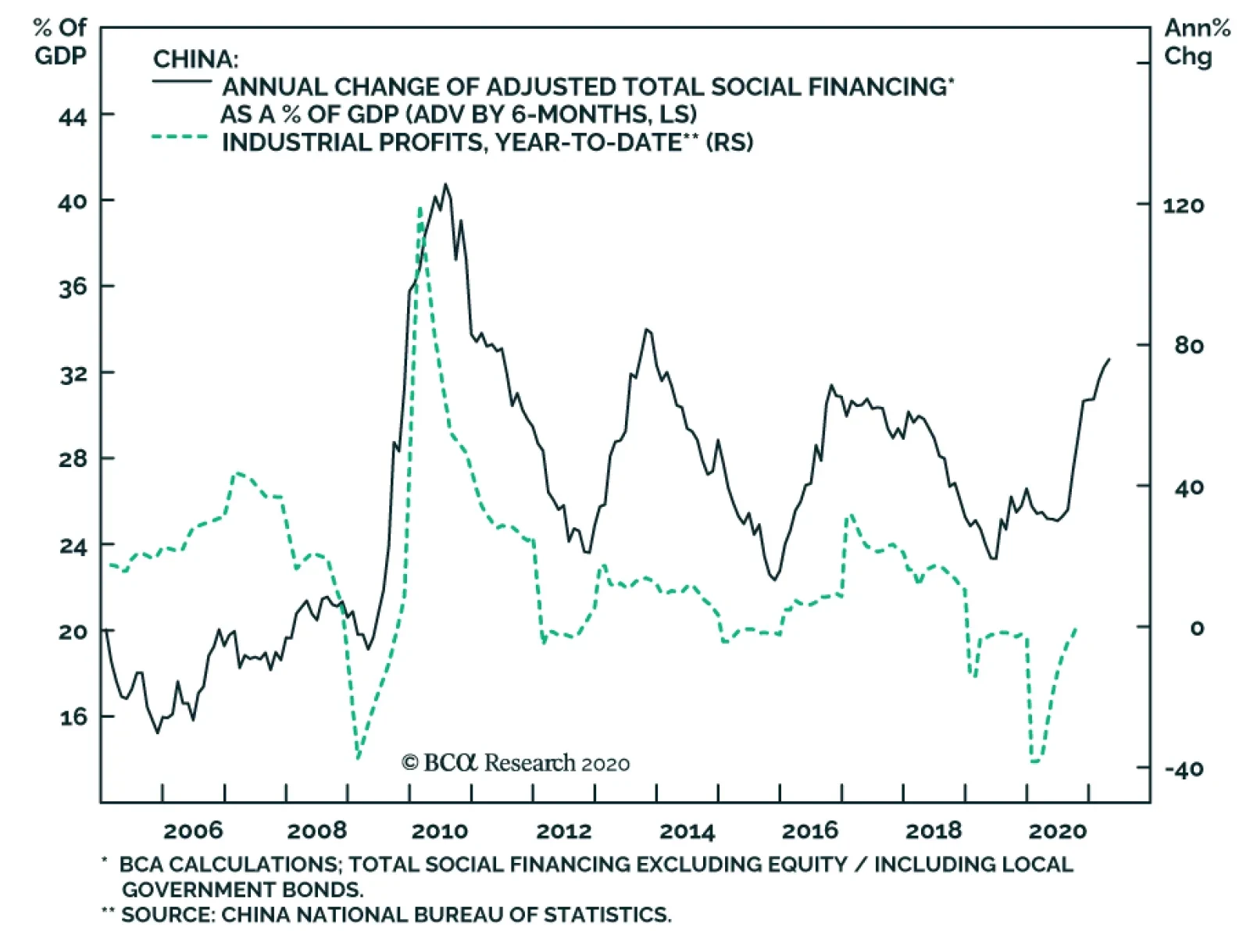

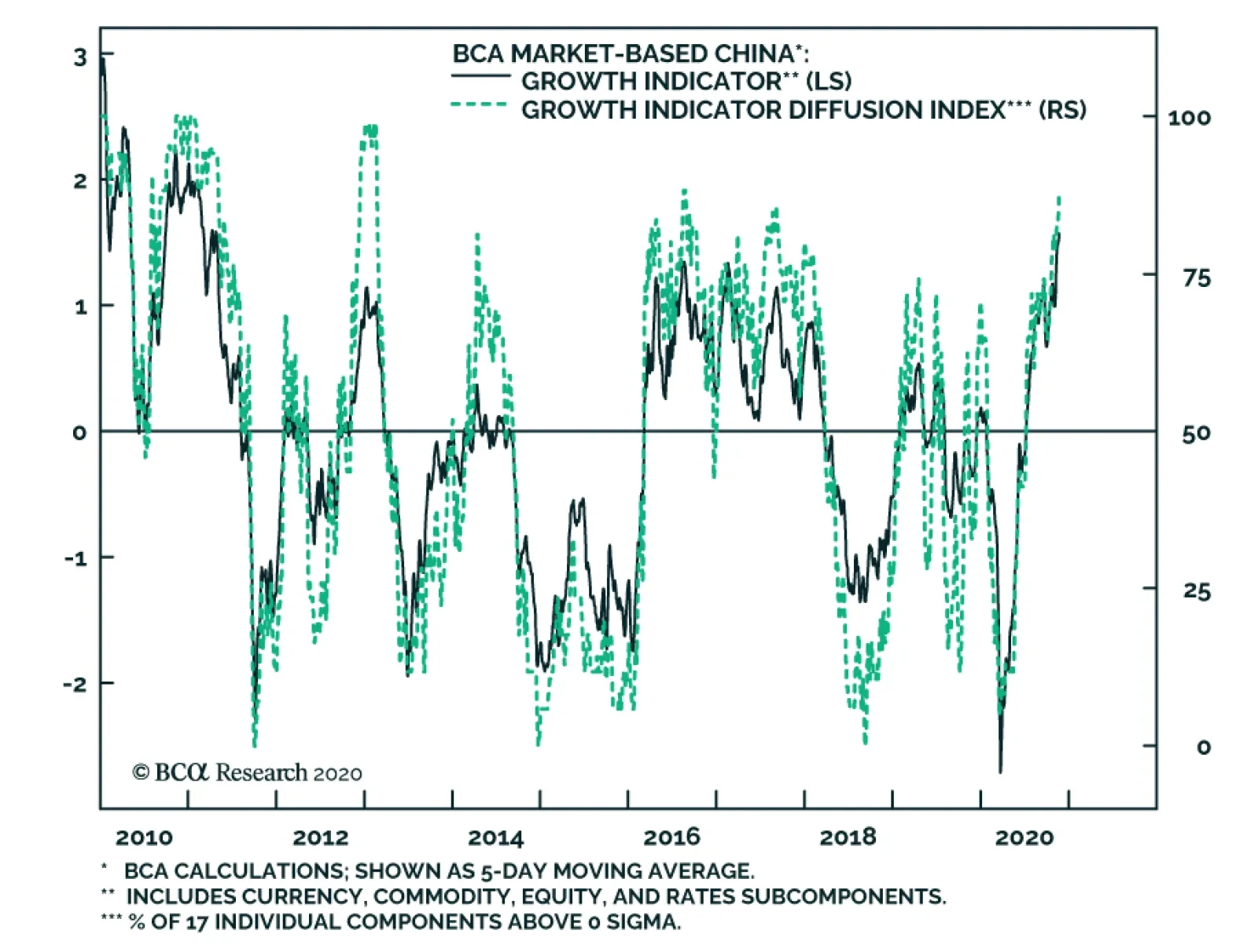

The strength in China’s post-pandemic policy support likely peaked in October. Interbank rates have normalized to their pre-pandemic levels and bond yields have risen sharply since May. The renewed emphasis on financial de-risking is evident in China’s recent anti-trust regulations against domestic leading online retail and lending providers, rising corporate bond defaults and readouts from recent PBoC meetings. In the near term, US President-elect Joe Biden will focus on reviving the economy and this may restore some balance to the Sino-US trade relationship. Additionally, China’s economic recovery is on track. The odds are rising that next year the Chinese leadership will accelerate structural reforms and the de-risking campaign, which began in 2017 but was delayed due to the US-China trade war and the COVID pandemic. These policy actions will improve China’s productivity growth and industrial competitiveness in the medium to long term, but they will create short-term headwinds to the economic recovery and the stock market’s performance. The uptrend in China’s business cycle will likely be maintained for another two quarters, propelled by the momentum from this year's massive stimulus. Historically, turning points in China’s business activities lag credit cycles by six to nine months. Given that China’s policy support apexed in Q4 this year, a peak in the country’s business cycle will probably be reached by mid-2021. Qingyun Xu, CFA Senior Analyst qingyunx@bcaresearch.com Jing Sima China Strategist jings@bcaresearch.com Below is a set of market relevant charts along with our observations: Monetary policy has tightened, but fiscal spending by local governments should pick up in the next two quarters to support the ongoing business cycle expansion into H1 2021. Fiscal spending has been constrained due to shortfalls in revenues this year, despite record sales of special-purpose bonds.1 Government expenditures will gain strength as local governments’ tax revenues start to improve and the proceeds from bond sales are distributed. Chart 1Credit Impulse Has Peaked...

Credit Impulse Has Peaked...

Credit Impulse Has Peaked...

Chart 3Business Cycle Expansion To Continue In 1H21

Business Cycle Expansion To Continue In 1H21

Business Cycle Expansion To Continue In 1H21

Chart 2...But Fiscal Spending Should Pick Up

...But Fiscal Spending Should Pick Up

...But Fiscal Spending Should Pick Up

Part of the buildup in this year’s industrial inventory is due to the solid recovery in domestic demand and proactive restocking by manufacturers. However, the pace of inventory pileup this year has been the highest since 2014, while infrastructure investment and industrial output growth have barely recovered to pre-pandemic levels. The rapid expansion in industrial inventory may be the result of cheap credit and commodity prices and could lead to a period of destocking and slower imports of raw materials in Q1 2021. Chart 4Industrial Inventory Has Run Ahead Of Economic Recovery...

Industrial Inventory Has Run Ahead Of Economic Recovery...

Industrial Inventory Has Run Ahead Of Economic Recovery...

Chart 5...Propelled By Solid Recovery And Cheap Credit

...Propelled By Solid Recovery And Cheap Credit

...Propelled By Solid Recovery And Cheap Credit

Core CPI has reached its weakest level in more than a decade, while the PPI remains in negative territory. A delayed recovery in the household consumption and services sector has been disinflationary to core CPI along with the PPI’s consumer goods price subcomponent.2 Historically, when the growth rate in the PPI outpaces that in the CPI, industrial output and profits tend to improve even if the PPI is in contraction. However, a deflationary PPI is the result of depressed demand for both industrial products and household goods. Hence, neither the widening gap between the PPI and CPI nor the improvement in industrial profits can be sustained on the back of falling consumer prices. Credit impulse tends to lead an increase in both the PPI and CPI by six to nine months. Improving service sector activities and rebounding energy and commodity prices will also be reflationary to both the CPI and the PPI. Meanwhile, the peaking credit impulse coupled with tighter domestic monetary policy and a rapidly rising RMB will limit the upside in both the consumer and producer price indexes. Chart 6Rising Deflation Risks

Rising Deflation Risks

Rising Deflation Risks

Chart 7PPI Has Been Dragged Down By Its Consumer Goods Price Component

PPI Has Been Dragged Down By Its Consumer Goods Price Component

PPI Has Been Dragged Down By Its Consumer Goods Price Component

Chart 8Improvement In Industrial Profits Is Unsustainable In A Deflationary Environment

Improvement In Industrial Profits Is Unsustainable In A Deflationary Environment

Improvement In Industrial Profits Is Unsustainable In A Deflationary Environment

Chart 9While The Economic Recovery Should Support Prices...

While The Economic Recovery Should Support Prices...

While The Economic Recovery Should Support Prices...

Chart 10...A Rapidly Rising RMB Will Limit The Upside In Producer Prices Next Year

...A Rapidly Rising RMB Will Limit The Upside In Producer Prices Next Year

...A Rapidly Rising RMB Will Limit The Upside In Producer Prices Next Year

Retail sales growth further strengthened in October. However, despite a sharp rebound in auto sales, other consumption segments, such as catering, tourism and consumer durable goods, remain sluggish. Household disposable income and employment have improved from troughs earlier this year, but both continue to lag behind the recovery in the industrial sector. The sluggish household sector has prompted Chinese leaders to take actions. In a State Council executive meeting on November 18, Primer Li Keqiang pledged to promote the consumption of home appliances, catering, and automobiles.3 Stocks of consumer goods and automakers rallied following the pro-consumption stimulus announcement. We continue to favor consumer discretionary stocks in both onshore and offshore markets. Even though the valuations in both sectors are elevated compared with the broad market, their earnings outlook also shows a notable improvement. In the next 6 months, targeted pro-consumption stimulus policies should further boost investors’ sentiment as well as profits in these sectors. Chart 11The Ex-Auto Retail Sales Remain Sluggish

The Ex-Auto Retail Sales Remain Sluggish

The Ex-Auto Retail Sales Remain Sluggish

Chart 12Improving Household Income And Employment Will Support Consumption

Improving Household Income And Employment Will Support Consumption

Improving Household Income And Employment Will Support Consumption

Chart 13Policy Support Will Continue Boosting Auto Sales...

Policy Support Will Continue Boosting Auto Sales...

Policy Support Will Continue Boosting Auto Sales...

Chart 14...And Promote NEV Sales

...And Promote NEV Sales

...And Promote NEV Sales

Chart 15Auto Sector's Outperformance Should Continue

Auto Sector's Outperformance Should Continue

Auto Sector's Outperformance Should Continue

Chart 16Consumer Discretionary Sector Will Also Benefit From More Policy Support

Consumer Discretionary Sector Will Also Benefit From More Policy Support

Consumer Discretionary Sector Will Also Benefit From More Policy Support

Chart 17Housing Demand In Second- And Third-Tier Cities Has Already Rolled Over

Housing Demand In Second- And Third-Tier Cities Has Already Rolled Over

Housing Demand In Second- And Third-Tier Cities Has Already Rolled Over

In the past four weeks, the high-frequency data show that momentum in housing demand in second- and third-tier cities has quickly abated. Moreover, bank lending to property developers has rolled over, reflecting tighter financing regulations and pressure to deleverage in the property sector. Growth has flattened in medium- and long-term consumer loans while the propensity for home purchase has ticked up slightly. This divergence may be a sign that demand for real estate has not softened, but that home buyers are waiting for more discounts from property developers. As such, the rebound in floor space started in October should be short-lived as property developers’ profit margins continue to narrow and their financing remains constrained. We expect aggregate home sales growth to decelerate slightly in 1H21 from the past six months. However, real estate developers need to complete their existing projects, which will support construction activities into H1 next year. Chart 18Home Buyers May Be Expecting More Home Price Discounts Ahead

Home Buyers May Be Expecting More Home Price Discounts Ahead

Home Buyers May Be Expecting More Home Price Discounts Ahead

Chart 19Financing Constrains Will Limit Investments In New Building Projects

Financing Constrains Will Limit Investments In New Building Projects

Financing Constrains Will Limit Investments In New Building Projects

This year’s strong outperformance in China’s offshore equity prices has been driven by the TMT sector’s stocks (Information Technology, Media & Entertainment, and Internet & Direct Marketing Retail). Since October, however, Chinese stocks excluding the TMT sector have also started to outperform the global benchmarks. Moreover, domestic cyclicals, which do not feature some of China’s leading tech companies such as Alibaba and Tencent, have outpaced onshore defensive stocks. These developments indicate that as the upswing in China’s business cycle continues to strengthen, the outperformance in China’s ex-TMT stocks will likely be sustained into early 2021. Within cyclical sectors, we continue to favor the materials and consumer discretionary sectors aimed at policy dividends and a rebound in commodity prices. Chart 20China's Ex-TMT Stocks Starting To Outperform Global

China's Ex-TMT Stocks Starting To Outperform Global

China's Ex-TMT Stocks Starting To Outperform Global

Chart 21Domestic Cyclicals Are Now Breaking Out Relative To Defensives

Domestic Cyclicals Are Now Breaking Out Relative To Defensives

Domestic Cyclicals Are Now Breaking Out Relative To Defensives

Chart 22Accelerating Economic Recovery Will Continue To Support Chinese Cyclical Stocks

Accelerating Economic Recovery Will Continue To Support Chinese Cyclical Stocks

Accelerating Economic Recovery Will Continue To Support Chinese Cyclical Stocks

Chart 23Rebounding Commodity Prices Will Bode Well For Material Stocks

Rebounding Commodity Prices Will Bode Well For Material Stocks

Rebounding Commodity Prices Will Bode Well For Material Stocks

Recent bond payment defaults by several SOEs have led to a spike in onshore corporate bond yields. Nonetheless, the ripple effect on China’s financial markets has been limited outside of the corporate bond market; onshore stocks were little changed by news of the defaults. Moreover, the PBoC’s recent liquidity injections helped to stabilize the interbank rate. Historically, corporate bond defaults and rising bond yields have not had an imminent negative impact on China’s domestic stock market performance; none of the defaults in 2015, 2016 or 2019 led to selloffs in the equity market. However, during a business cycle upswing and following a large-scale stimulus, increasing corporate defaults typically mark the onset of tightening in financial regulations and the monetary cycle. We expect the upswing in the business cycle to begin losing momentum as the tightening policy cycle gains further traction in 2021. Prices in the forward-looking equity market will likely peak sooner on the expectation that the rate of economic and corporate earnings growth will slow in 2H21. Chart 24Stress In Chinese Onshore Corporate Bond Market

Stress In Chinese Onshore Corporate Bond Market

Stress In Chinese Onshore Corporate Bond Market

Chart 25Stress In Chinese Onshore Corporate Bond Market

Stress In Chinese Onshore Corporate Bond Market

Stress In Chinese Onshore Corporate Bond Market

Chart 26But So Far Negative Impacts On The Stock Market Are Limited

But So Far Negative Impacts On The Stock Market Are Limited

But So Far Negative Impacts On The Stock Market Are Limited

Table 1China Macro Data Summary

China Macro And Market Review

China Macro And Market Review

Table 2China Financial Market Performance Summary

China Macro And Market Review

China Macro And Market Review

Footnotes 1Please see China Investment Strategy Weekly Report "China Macro And Market Review," dated October 7, 2020, available at cis.bcaresearch.com 2Headline PPI is comprised of producer and consumer goods. The weights of producer and consumer goods are roughly 75% and 25%, respectively. As for producer goods by industry, the weight of the manufacturing sector is around 50%, followed by 20% for the raw material sector; the mining sector accounts for only around 5%. 3Pro-auto consumption plans include: providing subsidies to encourage urban car owners to replace older and higher-emission models with newer environmentally friendly ones; encouraging automobile sales and upgrades in rural areas; and promoting New Energy Vehicle (NEV) sales. The plan will also loosen some existing restrictions on auto sales and increase the permits for vehicle license plates. Cyclical Investment Stance Equity Sector Recommendations

Mr. X and his daughter, Ms. X, are long-time BCA clients who visit our office toward the end of each year to discuss the economic and financial market outlook for the year ahead. This report is an edited transcript of our recent conversation, which we held remotely due to the COVID-19 pandemic. Mr. X: As always, I welcome the opportunity to discuss the economic and financial outlook with you. The past year has been truly ghastly with the wretched COVID-19 disease wreaking extraordinary economic and social havoc. I take comfort from the hope that a vaccine will allow a gradual return to more normal conditions in 2021, but my concerns about the longer-run outlook have increased. The extreme monetary and fiscal responses to the virus-related economic collapse may have been necessary but will leave most developed economies much more vulnerable down the road. Risk assets have been propped up by easy money, but I fear that simply means lower returns in the future. Ms. X: The social impact of the virus has weighed heavily on me, making me quite depressed about the outlook. I can only hope that my normal optimism will return when a vaccine ends the pandemic. Of course, I am happy that equities have done much better than might have been expected in the past year, but I share my father’s concerns about long-term returns. I look forward to discussing ideas about how to position our portfolio. BCA: The past year has indeed been grim on many levels. The economic disruption has been severe, but the social toll of the virus has been even more damaging for many people in terms of being forcibly isolated from family and friends. It is very encouraging that vaccines should start to become widely available early in the year, but the return to normality likely will take time. During the northern hemisphere winter months, the pandemic may even get worse before it gets better. As far as the longer run outlook is concerned, the policy response to the crisis will indeed have consequences. Government debt has soared in most countries and this raises the issue of how this will be dealt with in the years ahead. Meanwhile, central bank support to the markets cannot continue indefinitely, which raises the prospect of severe withdrawal pains at some point. Furthermore, both fiscal and monetary trends pose the question of whether higher inflation is inevitable. It is therefore unlikely that voters will reward politicians who impose upon them the painful deflationary pressures. Markets are forward looking and one could take the view that the strength of equity markets in the past eight months has reflected optimism about the economic outlook. However, a more plausible explanation is that hyper-stimulative monetary policies have been the main driving force behind asset prices. If that is the case, then there is some cause for optimism because central banks have made it clear that they will not be tightening policy for quite some time. While you are both right to be concerned about low returns over the long run, risk asset prices seem likely to rise further in the coming year with equities continuing to outperform bonds. We can get into that in more details later. Ms. X: Before we get into our discussion of the outlook, let’s briefly review your predictions from last year. BCA: That will be a humbling experience given that we never built a global pandemic into our forecasts! A year ago, our key conclusions were that: Global equities would enter the end game of their nearly 11-year bull market. Stocks were expensive, but bonds were even more so. As a result, if global growth could recover and the US could avoid a recession in 2020, earnings would not weaken significantly and stocks would again outperform bonds. Low rates reflected the end of the debt super cycle in the advanced economies. However, the debt super cycle was still alive in EM, particularly in China. The global economic slowdown that began more than 18 months prior to our meeting started when China tried to limit debt growth. If Beijing continued to push for more deleveraging, global growth would continue to suffer as the EM debt super cycle would end. Nonetheless, we expected China to try to mitigate domestic deflationary pressures in 2020. As a result, a small wave of Chinese reflation, coupled with the substantial easing in global monetary and liquidity conditions should have promoted a worldwide reacceleration in economic activity. Policy uncertainty would recede in 2020. Domestic constraints would force China and the US toward a trade détente. The risk of a no-deal Brexit was seen as marginal, and President Trump was still the favorite in the election. A decline in policy risk would foster a global economic rebound. That being said, some pockets of geopolitical risk remained, such as in the Middle East. Global central banks were highly unlikely to remove the punch bowl. Not only would it take some time before global deflationary forces receded, monetary authorities in the G-10 would want to avoid the Japanification of their economies. As a result, they were already announcing that they would allow inflation to overshoot their 2% target for a period of time. This would ultimately raise the need for higher rates in 2021, which would push the global economy into recession in late 2021 or early 2022. These dynamics were key to our categorization of 2020 as the end game. US growth would reaccelerate. The US consumer was in good shape thanks to healthy balance sheets as well as robust employment and wage growth prospects. Meanwhile, corporate profits and capex should have benefited from a decline in global uncertainty and a pickup in global economic activity. China would continue to stimulate its economy but would not do so as aggressively as it did over the past 10 years. Consequently, EM growth would also bottom but was unlikely to boom. Europe and Japan would reaccelerate in 2020. Bond yields would continue to grind higher in 2020. However, Treasury yields were unlikely to break above the 2.25% to 2.5% range until much later in the year. Inflationary pressures would not resurface quickly, so the Fed was unlikely to signal its intention to raise interest rates until late 2020 or later. European bonds were particularly unattractive. Corporate bonds were a mixed offering. Investment grade credit was unattractive owing to low option-adjusted spreads and high duration, especially as corporate health was deteriorating. Agency mortgage-backed securities and high-yield bonds offered better risk-adjusted value. Global stocks would enjoy their last-gasp rally in 2020. As global growth would recover, we favored the more cyclical sectors and regions which also happened to offer the best value. US stocks were the least attractive bourse; they were very expensive and loaded with defensive and tech-related exposure, two groups that would suffer from higher bond yields. We were neutral on EM equities. We recommended that investors pare exposure to equities only after inflation breakevens had moved back into their 2.3% to 2.5% normal range and the Fed fund rates had moved closer to neutral. We anticipated this to be a risk in 2021. The dollar was likely to decline because it is a countercyclical currency. Balance of payment dynamics and valuation considerations were also becoming headwinds. The pro-cyclical European currencies and the euro were expected to be the main beneficiaries of any dollar depreciation. We anticipated oil and gold to have upside. Crude would benefit from both supply-side discipline and a recovery in oil demand on the back of the improving growth outlook. Gold would strengthen as global central banks would limit the upside to real rates by allowing inflation to run a bit hot. A weaker dollar would boost both commodities. We expected a balanced portfolio to generate an average return of only 2.4% a year in real terms over the next decade. This compares to average returns of around 6.5% a year between 1982 and 2018. Obviously, our forecasts were undone by the defining event of the year: the pandemic. Nonetheless, in February we warned that asset prices did not embed enough of a risk premium to protect investors against the threat that the pandemic could terminate the global business cycle. The more deflationary risk we confront today, the more inflation we will face in the future. At the beginning of the second quarter, we were quick to recommend buying stocks back, so we participated in the rally that followed. We erred in preferring foreign to US equities, which turned out to be key winners of the pandemic thanks to their heavy exposure to growth stocks (Table 1). The economic downturn meant that bond yields fell rather than rose. They have remained exceedingly low in response to exceptionally accommodative monetary conditions, a surge in savings and deeply negative output gaps. We were right to favor peripheral bonds, which benefited from the ECB’s purchases and the European Commission’s Recovery Fund (Table 1). Finally, the market rewarded our negative stance on the dollar and our bullish view on gold. However, we were offside on oil, where the continued impact of the pandemic on global transport has left crude prices at very depressed levels. Table 12020 Asset Market Returns

OUTLOOK 2021: A Brave New World

OUTLOOK 2021: A Brave New World

A Brave New World Mr. X: You mentioned that you prefer stocks over bonds for 2021. I can accept this view; while stocks are expensive, their valuations are less demanding than that of bonds. Moreover, I agree that policymakers around the world are very afraid of the deflationary consequences of removing accommodation too early but they cannot ease monetary policy much from here. This creates an asymmetric payoff in favor of stocks versus safe-haven securities. However, my favorite asset class for the near future is cash. Granted, I enjoy the luxury of not having to track a benchmark and my core focus is capital preservation. With both stocks and bonds richly valued, I see no margin of safety and I would rather stand on the sidelines. The longer-term outlook is particularly concerning. The extraordinary accommodation implemented this year was unavoidable, but its future consequences worry me greatly. Real rates have never been so low and we are leaving unprecedented public debt loads to our children and grandchildren. Moreover, I fear further adoption of populist policies because inequalities have risen in the wake of the crisis. The worst affected families stand at the bottom of the income distribution while people like me have benefited from inflated asset prices. Therefore, I am inclined to believe that we will suffer a large inflation shock in the coming decade. The global broad money supply has exploded and it is very unlikely that central banks will normalize interest rates in due time because of the burden created by gigantic public debt loads and the spectrum of further populism. My worries extend beyond these obvious concerns. Last year I was already anxious about the incredibly large stock of global debt with negative yields. This situation has only worsened since. Moreover, the various programs implemented by the Federal Reserve, the European Central Bank and other major monetary authorities to provide liquidity directly to the private sector at the apex of the crisis have prevented the purge of unhealthy firms necessary under a capitalist system. Instead of creative destruction, zombification has become the norm. Thus, I fear that more capital is misallocated than at any point in the past 10 years. Putting it all together, my expectations are that real returns will be poor for years to come, if not outright negative. I therefore believe that gold should stand at the core of my family’s portfolio. Ms. X: I share many of my father’s concerns. It is difficult to see how monetary and fiscal authorities will normalize policy. Hence, I agree that we will face the painful legacy of a large debt overhang and poor long-term returns. Moreover, the poor demographic profile in most advanced economies as well as China bodes ill for trend growth. I do see opportunities within this bleak picture. Healthcare stocks should benefit from an aging of the world’s population and tech equities will remain a source of disruption, innovation and profit growth in the coming decades. Thus, an equity portfolio built around these themes should generate positive real returns. In light of the positive vaccine news, next year will offer investors with both rapidly expanding profits and low discount rates and it is hard to imagine equities performing poorly. BCA: Clearly, we have many things to discuss. We should start with the COVID-19 pandemic. The news that vaccines developed by Pfizer/BioNTech and Moderna are around 95% effective is very encouraging. The Oxford/AstraZeneca announcement also is a source of optimism, even if the trial results have been less clear-cut. Moreover, other vaccines are currently in the mass-testing stage. By next winter, approximately 1.5 billion people globally should have been vaccinated. These positives hide many issues. First, transporting the Pfizer and Moderna vaccines (particularly the one produced by Pfizer, which needs to be kept at -70°C) will be challenging, especially for poorer countries. Second, the mRNA technology used in these vaccines is new and its long-term impact is unknown. Hence, many people will be reluctant to take this shot, especially as the confidence in the safety of vaccines has declined among the general public. Only 58% of Americans said they would probably take a COVID-19 vaccine, a number that will rise once the vaccine is demonstrated but which still highlights the challenge (Chart 1). Third, the virus could mutate and render the current generation of vaccines ineffective. The recent news of such mutations in mink farms in Denmark is worrisome, especially as the new strain of the virus has already jumped back into the human population. Chart 1The Vaccine Blues

OUTLOOK 2021: A Brave New World

OUTLOOK 2021: A Brave New World

Our base case is that the vaccines will allow a progressive reopening of the economic sectors currently still under lockdown. They will lead to a further improvement in employment, consumer and business sentiment, and aggregate demand. With less fear of getting infected, consumers will return to shops, restaurants, hotels, etc. This will have a very beneficial impact on capex and profit growth. It will result in higher stock prices, especially for value stocks, cyclical stocks, as well as higher yields and commodity prices. Despite this optimistic base case, investors must have contingencies ready. The three aforementioned risks around the vaccines suggest that additional waves of infections cannot be entirely ruled out and that lockdowns may continue in 2021. Thus, we could still face periods of downward pressure on activity, yields, and value stocks. For now it remains prudent not to tilt portfolios fully toward a post-COVID bias. In contrast to the past 40 years, a 60/40 portfolio will fare poorly once we account for higher inflation. Even if the vaccines enjoy widespread adoption, near-term threats to economic activity remain. The realization that the end of the pandemic is close may prompt a temporary period where households hunker down and behave in a very conservative fashion. After all, few consumers will want to contract the virus just before a vaccine becomes available. Moreover, the sight of the end of the lockdowns reduces the fiscal authorities’ urgency to provide additional support to the population and small businesses. These two dynamics could prompt a deep contraction in spending in the first quarter of 2021, which would hurt stock prices. Mr. X: Thank you. While these near-term dynamics are crucial, the emergence of the vaccine increases the importance of discussing the long-term implications of the extreme policy conducted in recent months. BCA: The long-term implications of aggressive policy stimulus tie into the evolution of the debt super cycle. As a share of US GDP, total private debt has spiked near a record high and total nonfinancial debt has surged to new all-time highs (Chart 2). This reflects two phenomena. First, the denominator of the ratio – GDP – has collapsed. Second, total nonfinancial debt also highlights the rapid increase in government deficits. Hence, climbing leverage was a consequence of the necessary dissaving by the public sector to alleviate the deflationary forces created by the crisis. This problem is repeated around the world. As Chart 3 demonstrates, nonfinancial debt levels across the G10 are rapidly rising. Moreover, debt loads in emerging markets are also extremely elevated. Chart 2COVID-19 Boosted Debt Ratios

COVID-19 Boosted Debt Ratios

COVID-19 Boosted Debt Ratios

Chart 3Elevated Debt Everywhere

Elevated Debt Everywhere

Elevated Debt Everywhere

Going forward, either rising savings or faster nominal GDP growth will cause the debt ratios to decline. The first option is difficult; increasing savings is deflationary and it could worsen the debt arithmetic by keeping real interest rates stubbornly high. Moreover, it is politically unpopular, especially when the public sector has been the borrower. Here, we echo the words of Keynes from his 1923 Tract On Monetary Reform: "The progressive deterioration in the value of money through history is not an accident, and has had behind it two great driving forces – the impecuniosity of governments and the superior political influence of the debtor class (…). No state or government is likely to decree its own bankruptcy or its own downfall so long as the instrument of taxation by currency depreciation through the creation of legal tender (money) still lies at hand… The active and working elements (i.e., debtors) in no community, ancient or modern will consent to hand over to the rentier or bond holding class more than a certain proportion of the fruits of their work. When the piled up debt demands more than a tolerable proportion, relief has usually been sought in (…) repudiation (…) and currency depreciation." Nominal rates cannot fall further, while large inequalities and social immobility are fomenting populism (Chart 4). Moreover, the recent COVID-19 crisis has deepened the angst of the general population and its dissatisfaction with policymakers. It is therefore unlikely that voters will reward politicians who impose upon them the painful deflationary pressures that result from the high savings necessary to reduce public sector debt loads. Even a Republican-controlled US Senate will have to allow larger deficits than usual in today’s climate. Chart 4Inequalities And Immobility Are The Roots Of Populism

OUTLOOK 2021: A Brave New World

OUTLOOK 2021: A Brave New World

Instead, we expect fiscal and monetary policy to work in tandem to lift inflation and deflate the global debt load. The rising popularity of Modern Monetary Theory fits within this paradigm shift. MMT posits that as long as governments issue debt in their own currency, central bank money printing can finance the deficit. The only constraint on policymakers becomes the level of inflation that society tolerates. Society is likely to tolerate a rise in inflation. MMT is unpalatable to savers, but the majority of citizens are debtors, not lenders. In an MMT framework where the median voter is a borrower, the tolerance for inflation will likely be high, which will hurt the value of financial assets. Moreover, the corporate sector is unlikely to fight strongly against large deficits funded by central banks. If we accept the Kalecki Equation of Profits, which can be simplified as: Profits = Investment – Household Savings – Government Savings – Foreign Savings + Dividends then business profits will suffer if deleveraging takes hold, whether in the public or private sector. Instead, MMT-like policies, which will keep savings at low levels and prevent deleveraging, offers a way to keep nominal profits afloat. For businesses too, the path of least resistance steers toward higher inflation. Different countries will vary in their ability to pass MMT-like policies, but the policy shift toward inflationary policies is clear. The specter of rising populism should result in heavier regulation, at least in the EU and the US under the incoming Biden administration. Regulation further hurts the growth rate of the supply-side of the economy. It limits competition, it protects workers and it increases the cost of doing business. We expect additional fiscal stimulus will come through in the coming months. Beyond political forces, the demographic deterioration highlighted by Ms. X points in the same direction. An aging population means that the dependency ratio (the number of dependents per worker) is increasing. Moreover, analysis by the UN underscores that in old age, consumption increases due to rising spending on healthcare (Chart 5). We are therefore likely to witness a slowing expansion of the supply side relative to the demand side of the economy. By definition, this process is inflationary. In the second half of the decade, inflation could average as high as between 3% and 5%. Keep in mind that inflation is not a linear process. Once it starts to rise, it becomes very hard to control. In this regard, the experience of the late 1960s is extremely instructive. Through the 1960s boom, inflation was well behaved, contained between 0.7% and 1.2%. Then it started to rise in 1966, and quickly hit 6.1% by 1970 (Chart 6). While the average-inflation target the Fed recently adopted is well intentioned, in an environment where governments are unlikely to curtail deficits as fast as the private sector cuts its savings, it could easily unleash a long-term inflationary trend. Chart 5Aging Doesn't Spell Less Spending

Aging Doesn't Spell Less Spensing

Aging Doesn't Spell Less Spensing

Chart 6Inflation Is Stable Until It Is Not

Inflation Is Stable Until It Is Not

Inflation Is Stable Until It Is Not

Ms. X: Why won’t technological advancements such as AI and automation cause low inflation to prevail for the rest of the decade? Chart 7Low Productivity

Low Productivity

Low Productivity

BCA: The great paradox of this crisis is that the more deflationary risk we confront today, the more inflation we will face in the future. This relationship is the consequence of financial repression. Debt arithmetic will only stay manageable as long as real interest rates remain low; consequently, central banks will only be able to increase interest rates if nominal growth rises significantly from its low average of the past decade. Both workforce and productivity growth are low, thus quicker inflation is the only solution. As you hinted, technology is a risk to our long-term inflation view. However, technology has most often been a deflationary force. The key question is whether we are experiencing a greater impact than normal on productivity from current technological developments. So far, the answer seems to be no. Even if the statistical estimation methods for GDP overestimate inflation and thus underestimate productivity, we are still nowhere near the kind of productivity gains registered in the post-WWII period or at the turn of the millennium. We remain much closer to the productivity recorded in the 1970s or early 1980s (Chart 7). As a result, we expect technology not to be enough of a game changer to undo the inflationary effect of the shift away from the pro-capital, deregulatory, pro-global-trade consensus that prevailed for the past forty years. Ms. X: Your view rests on an assessment that political forces are structurally moving toward populism. Doesn’t the most recent US election counter this argument? Was it not a victory of centrism over populism? Chart 8AValuations Point To Poor Long-Term Returns

Valuations Point To Poor Long-Term Returns

Valuations Point To Poor Long-Term Returns

Chart 8BValuations Point To Poor Long-Term Returns

Valuations Point To Poor Long-Term Returns

Valuations Point To Poor Long-Term Returns

Chart 8CValuations Point To Poor Long-Term Returns

Valuations Point To Poor Long-Term Returns

Valuations Point To Poor Long-Term Returns

Chart 8DValuations Point To Poor Long-Term Returns

Valuations Point To Poor Long-Term Returns

Valuations Point To Poor Long-Term Returns

BCA: It was a victory of moderation over populism, but it was a narrow victory that reveals powerful populist undercurrents, particularly the strong demand for economic reflation. Despite a pandemic and recession in the election year, President Trump narrowly lost in the key swing states, and managed to garner roughly 74 million votes, the second highest tally in history. Moreover he led the Republican Party to gain seats in the House of Representatives and (likely) to retain control of the Senate. Exit polls reveal that the economy was still the number one issue on voters’ minds – they rejected Donald Trump’s personality but embraced his “growth at any cost” approach. By the same token, the Democratic Party lost elections down the ballot because they became associated with lockdowns and revolutionary social causes. President-Elect Joe Biden won the election, first, by not being Donald Trump, and second, by campaigning on a larger government spending program, a moderately liberal social stance, and a less belligerent protectionism on trade and China. The fact that both candidates wanted large stimulus packages and infrastructure programs tells us something about the median voter’s stance on economic policy: it is reflationary. Going forward, if Republicans control the Senate then the Biden administration will have to appeal to moderate Republican senators to get enough votes for COVID relief and economic recovery. If Democrats gain control of the Senate on January 5, they will have a one-vote majority and their legislative agenda will depend on winning over moderate Democratic senators. The Republican scenario is less reflationary but more likely, while the Democratic scenario is more reflationary but less likely. What investors can count on in 2021 is that the US government will not enact the mammoth splurge of government spending but that Republican senators will also be cognizant of the need for some fiscal support. Mr. X: If you expect inflation to rise structurally, how should we position our portfolio on a long-term basis? Bonds will obviously suffer, but so will an extremely expensive equity market that requires low bond yields to justify current prices. It seems like there is nowhere to hide but gold. BCA: The next one to two decades will not look like the past four, which were extraordinarily rewarding for investors. The taming of inflation, the broadening of globalization and far-reaching deregulation both cut interest rates and boosted profit margins. These trends stimulated demand and lifted asset valuations. These dynamics fed exceptional returns for all financial assets. However, these tailwinds have dissipated. The Fed will look through next year’s temporary inflation rebound. This change has many important implications for portfolio construction. You are correct that it will be hard for equities to generate decent real returns in the coming decade. Valuations may be a poor gauge of immediate stock returns, but they are clearly correlated with long-term returns (Chart 8). The odds of higher inflation in the second half of the decade will eventually cause policymakers to raise interest rates and force a normalization of equities multiples. Moreover, greater regulation and rising populism will raise the share of GDP absorbed by wages. Profit margins are likely to decline from here (Chart 9). Chart 9Profit Margins Under Threat?

Profit Margins Under Threat?

Profit Margins Under Threat?

Despite the poor long-term outlook for real stock returns, equities should still outperform bonds. Over the past 150 years, shares beat bonds in each episode of cyclically rising inflation, even if stocks generate paltry inflation-adjusted returns (Table 2). This time will not be different. Equities are significantly cheaper than bonds. Based on the current level of bond and dividend yields, US, Eurozone, UK and Japan bourses need to fall in real terms 23%, 32% 50% and 20%, respectively, over the next 10-year to underperform local government bonds (Chart 10). Additionally, the duration of bonds is very high due to their extremely low yields, which means that bond prices are exceptionally sensitive to rising rates. Table 2Stocks Beat Bonds, Part I

OUTLOOK 2021: A Brave New World

OUTLOOK 2021: A Brave New World

In contrast to the past 40 years, a 60/40 portfolio will fare poorly once we account for higher inflation. During the period from 1965 to 1982, when US core CPI inflation rose from 1.2% to 13.6%, the 60/40 portfolio lost 30% of its value in real terms (Chart 11). Moreover, the portfolio started to suffer poor inflation-adjusted returns well before inflation moved into double digits. As soon as CPI accelerated in 1966, the standard portfolio began to lose value. This time, inflation will not reach the dizzying height of the late 70s, but equities are trading at price-to-sales, price-to-book or Shiller P/E 33% above that of 1965 and Treasury yields stand at 0.88%, not 4.65%. Chart 10Stocks Beat Bonds, Part II

Stocks Beat Bonds, Part II

Stocks Beat Bonds, Part II

Chart 11The 60/40 Portfolio Doesn't Like Inflation

The 60/40 Portfolio Doesn't Like Inflation

The 60/40 Portfolio Doesn't Like Inflation

The problematic long-term outlook for the 60/40 portfolio will demand greater creativity from investors than over the past 40 years. We like assets such as farmland, timberland, and natural resources as inflation hedges. We also like precious metals. Silver is particularly attractive; like gold it thrives from rising inflation, but unlike its yellow counterpart, silver trades at a discount to its fair value implied by the long-term trend in consumer prices (Chart 12). Industrial metals are also interesting; the effort to reduce carbon emissions will hurt fossil fuel prices but will require greater reliance on electricity. Hence, the demand for copper will stay robust while investments in extraction capacity have been poor for the last decade. Silver, a great electricity and heat conductor, will also benefit from this trend. Chart 12Silver Is Cheaper Than Gold

Silver Is Cheaper Than Gold

Silver Is Cheaper Than Gold

Within equity portfolios, winners and losers will also change. Empirically, technology, utilities and telecom services underperform when inflation rises durably. On the other hand, healthcare, materials and real estate outperform. The first group does not possess much pricing power in an accelerating CPI environment while the second does, justifying the bifurcated relative performances. We recommend tilting long-term equity exposure this way. Finally, this sectoral view implies a structural overweight in Europe and Japan at the expense of the US and emerging markets. Mr X: Thank you. This discussion about long-term risks and portfolio construction was very useful. That being said, the thought of MMT becoming more mainstream leaves me extremely uncomfortable. The Economic Outlook Ms. X: From your observations on the vaccine rollout, I presume you expect the recovery to remain robust next year. Aren’t you concerned that a big part of the G-10 could experience a double dip recession in the first half of the year? BCA: Near-term risks are very elevated and it is likely that Europe is experiencing a renewed slump in activity as we speak. In response to the recent violent second wave of infections, consumers have avoided public spaces and governments across the continent and in the UK have implemented increasingly stringent lockdowns. Various high-frequency indicators and live trackers for the regions already indicate that another contraction in activity is taking place (Chart 13). The US is not immune to a slowdown. The country is in the thrall of its third wave of infections and local governments are increasingly imposing lockdowns. Just look at New York City, which is somewhat of a canary in the coalmine for the nation, where schools have closed. This development is happening as the economy was already slowing down after a blistering recovery in the third quarter. Naturally, the US economic surprise index is quickly declining, which indicates that economic data is falling short of expectations (Chart 14). Chart 13The European Economy Is Slowing Right Now

The European Economy Is Slowing Right Now

The European Economy Is Slowing Right Now

Chart 14The US Economy Is Decelerating

The US Economy Is Decelerating

The US Economy Is Decelerating

Growth is slowing but the level of US GDP is not doomed to contract. First, inventory restocking could add as much as 3.5% to current quarter GDP. Second, consumer spending is still robust. This summer, household savings jumped massively in response to both the large transfers created by the CARES act as well as the low marginal propensity to spend caused by depressed consumer confidence. Now, consumers are deploying this large pool of funds, which is buttressing expenditures. Despite these short-term headwinds, growth in 2021 should be well above trend in the US and in Europe. The ECB Target II balance permanently attaches Germany to its weaker neighbors. Mr. X: What about the risk that a lack of fiscal stimulus could scuttle the recovery? BCA: We are not overly concerned about that as we expect additional fiscal stimulus will come through in the coming months. Chart 15Borrowing Costs Are Not A Constraint To Spending

OUTLOOK 2021: A Brave New World

OUTLOOK 2021: A Brave New World

In Europe, the case for additional fiscal support is clear. All the major euro area countries, including Greece, can borrow at negative interest rates, depending on the maturity (Chart 15). This too is true for Sweden, Switzerland and even the UK. Within the Eurozone, the issuance linked to the European Commission’s Recovery Fund represents the first wave of common-debt issuance. It is an embryonic tool for fiscal risk sharing, one that goes further than the European Stability Mechanism, and it is an important driver of the spread compression in the European bond market. European governments are under little pressure to apply any fiscal brake because of these low borrowing costs. Moreover, the various European central banks are buttressing government bond markets. Thus, fiscal authorities have a free hand to provide additional support if they choose to do so while lockdowns remain in place. The loose fiscal setting will allow activity to recover quickly. In the US, the situation is more complex, but we expect at least a minimal level of support. The gridlock in Washington prevents the large stimulus that would have passed under a unified Democratic control of Congress. However, a Biden administration faced with a Senate controlled by the GOP also cannot increase taxes significantly. Meanwhile the Republicans are willing to provide additional help as long as it targets households and small businesses. Netting these forces out, we expect a stimulus package of $500 billion to $1 trillion. This is smaller than the various offers on the table prior to the election, but the more concrete eventuality of a vaccine deployment in the first half of 2021 also means that the economy needs help for a shorter period. While the risk to the forecast is that the Democrats and the Republican reach a larger compromise, investors may have to wait months for a deal. This delay could magnify the underlying weakness in the US economy. Chart 16The Chinese Locomotive Is Intact

The Chinese Locomotive Is Intact

The Chinese Locomotive Is Intact

In Japan, the law prescribes a negative fiscal thrust of –7.1% of GDP. We doubt this will transpire. Prime Minister Suga does not want to kill a nascent recovery and feed powerful deflationary pressures. Hence, supplementary budgets will provide more support to growth. Ms. X: Last year, we spoke a lot about China as an important driver of the global manufacturing cycle and growth. Is this still the case? BCA: China remains an important factor supporting our positive stance on global growth in 2021. Thanks to the aggressive use of testing and tracing, China has contained the virus, which is letting the economy heal and respond normally to monetary policy. On this front, the lagged impact of the easing enacted since 2019 will continue. Total social financing flows have rebounded to 33% of GDP and are consistent with a further improvement in our China Activity Indicator (Chart 16). Strengthening Chinese cyclical spending will lift imports of raw materials and machinery. The uptick in the Chinese credit and fiscal impulse suggests that China will remain a positive force for the rest of the world until the second half of 2021. After the summer, the positive impact of China on global growth will ebb. The PBoC is already allowing market interest rates to increase, which suggests that the apex of the credit easing was reached in Q4. Nonetheless, President Xi Jinping cannot tolerate any kind of instability ahead of the 100th anniversary of the CCP in October 2021. Thus, the fiscal and monetary policy tightening will be calibrated before that date and will only become a major risk afterwards. As a result, global growth will enjoy its maximum contribution from Chinese demand around Q2 2021. After that, Chinese activity will still be high enough to keep global industrial production elevated, but not enough to cause a further acceleration. Chart 17China's Marginal Propensity To Consume Augurs Well

China's Marginal Propensity To Consume Augurs Well

China's Marginal Propensity To Consume Augurs Well

Another good news for the Chinese and global economies is the recent pickup in China’s marginal propensity to consume (MPC), as approximated by the gap between the growth rate of M1 and M2 money supply (Chart 17). When M1 accelerates faster than M2, demand deposits are growing quicker than savings deposits, which highlights that economic agents are positioning their liquidity for increased spending. The MPC’s uptick will reinforce the positive signal for global economic activity from China’s credit trend. It also creates upside risk for China’s economy in the second half of the year compared to what policy dynamics imply. Ms. X: Beyond China and fiscal policy, do you foresee any other tailwinds for the global business cycle? BCA: Yes, there are plenty. As we already mentioned, the vaccine should allow the service sector to normalize progressively over the course of the year. Households’ healthy balance sheets will underpin US consumer spending next year. At the end of 2019, debt to disposable income stood at an 18-year low and the debt servicing-costs ratio was near generational troughs. In addition, both of these measures of financial health only improved during the crisis. Collapsing interest rates allowed households to refinance their mortgages and government transfers boosted disposable income. Likewise, after a very negative shock in Q1, household net worth quickly rebounded in Q2 when asset prices surged and household savings grew (Chart 18). The wealth effect will therefore help consumption, especially because employment continues to improve. The odds of higher yields are most pronounced for longer maturities. The outlook for capex is also bright. Capex intentions have been surprisingly robust in recent months and core durable goods shipments have reached all-time highs (Chart 19). Admittedly, capex is a lagging economic variable – companies take their cues from the behavior of households. But, this means that, as household spending continues to recover, so will capital investment. Another way to approach this topic is to think about the link between capex and corporate profitability. In capital budgeting, the pecking order theory argues that retained earnings are the preferred source of financing for corporate investments. This theory is echoed by empirical evidence. Business capital formation follows operating profits by roughly six months (Chart 20). The positive outlook for profits therefore bodes well for capex. Chart 18Solid Household Balance Sheets In The US

Solid Household Balance Sheets In The US

Solid Household Balance Sheets In The US

Chart 19Surprising Capex Rebound

Surprising Capex Rebound

Surprising Capex Rebound

Chart 20Earnings Drive Capex

Earnings Drive Capex

Earnings Drive Capex

A major concern for the US economy is commercial real estate. This sector’s losses will likely be very large because many buildings are now uneconomical. Even if vaccines normalize daily activities, post-pandemic life has in some ways been reshaped. Workers are likely to conduct more of their job from home and shoppers have become used to the convenience of E-commerce. As a result, the need for office and retail space will decrease, which falling rents are already reflecting. The hit to the US banking system is still unknown. While CRE accounts for 13% of bank assets, this exposure is concentrated within smaller regional banks, which are much frailer than their SIFI counterparts (Chart 21). We could therefore see some localized troubles within a banking system that is tightening credit standards already (Chart 22). This danger warrants close monitoring. Chart 21CRE Is A Threat For Small Banks

CRE Is A Threat For Small Banks

CRE Is A Threat For Small Banks

Chart 22Another Tightening In Standards Would Be Dangerous

Another Tightening In Standards Would Be Dangerous

Another Tightening In Standards Would Be Dangerous

Chart 23Europe Is More Exposed To Chinese Demand

Europe Is More Exposed To Chinese Demand

Europe Is More Exposed To Chinese Demand

It is not clear whether the US or the euro area will enjoy the sharpest growth improvement in 2021. Normally, Europe benefits the most during a manufacturing upswing, especially when China’s marginal propensity to consume is expanding (Chart 23). The European economy is more cyclical than that of the US because exports and manufacturing constitute a larger share of employment and gross value added (Chart 23, bottom panel). Moreover, the fiscal drag in Europe is likely to subtract roughly 3% from GDP next year while it could subtract 5% to 7% from the US GDP. However, an important handicap will counterbalance these advantages for Europe; the biggest source of economic delta next year should be the service sector because spending on goods began to recover in earnest in 2020. There is simply more pent-up demand left in services than goods and the service sector accounts for a larger share of output in the US than in Europe. Three additional factors could also favor the US against both Europe and Japan. First, residential activity is rebounding more quickly in North America. Historically, residential investment makes a large contribution to cyclical expenditures and it galvanizes additional spending on durable goods. Second, the Fed was able to engineer deeper declines in real interest rates than the ECB or the BoJ while Washington expanded the deficit faster than Tokyo or most European capitals. Finally, the weak dollar is creating another relief valve unavailable to Japan and Europe. In fact, the euro’s strength is potentially the greatest dampener of the European recovery in the coming quarter. Finally, emerging economies face important domestic hurdles that will handicap them significantly versus advanced economies in the first half of the year. EM banking systems remain fragile after the violent capital outflows witnessed in the first half of 2020. Thus, their ability to expand credit is comparatively limited. Moreover, EM economies have yet to withstand the inevitable second wave of infections, and their healthcare systems are even weaker than in advanced economies. The logistical complications associated with the rollouts of the vaccine will be most acute in poorer countries. Mr. X: I share your worries about long-term inflation, but where do you stand regarding near-term dynamics? A faster inflation recovery would amount to the kiss of death for asset markets. BCA: You are correct that faster inflation would threaten asset markets. It would force a rapid re-pricing of the Fed’s policy path and lift yields higher. Expensive stocks would buckle under this impulse. However, while it is a risk we monitor closely, it is far from our base case. We particularly like real yield curve steepeners. To begin with, both the output gap and the unemployment gap will remain meaningful in 2021. Our US Composite Capacity Utilization Indicator is not consistent with higher inflation (Chart 24). Additionally, at 6.9%, the US unemployment rate understates the amount of slack in the labor market. The employment-to-population ratio for prime-age workers offers a more accurate read of the labor market because it accounts for discouraged workers. This labor market indicator points toward limited inflation in the Employment Cost Index (Chart 25). Chart 24Limited Immediate Inflationary Pressures

Limited Immediate Inflationary Pressures

Limited Immediate Inflationary Pressures

Chart 25The Labor Market Is Replete With Slack

OUTLOOK 2021: A Brave New World

OUTLOOK 2021: A Brave New World

Inflation is still likely to spike in the first half of the year, but this jump will prove temporary. In the second quarter, both the core CPI and the core PCE inflation will incorporate a strong base effect when annual comparisons include the extremely depressed numbers that prevailed at the nadir of the recession. Moreover, once the service sector reopens in response to broadening vaccination programs, service sector inflation could pop higher, as goods prices did once the goods sector reopened last summer. The base effect will quickly ebb and the initial surge in service inflation should also dissipate because shelter inflation will remain dampened by stubborn permanent unemployment (Chart 26). The Fed will look through next year’s temporary inflation rebound. Its new average inflation target officialized last September is designed to avoid this kind of premature response and Fed officials are currently more afraid of committing deflationary errors than inflationary ones. Markets understand this well. Hence, as long as inflation breakeven rates remain below the 2.3% to 2.5% band consistent with market participants believing in the Fed’s ability to achieve 2% inflation durably (Chart 27), market wobbles caused by higher inflation will create buying opportunities. Chart 26Shelter Inflation Will Remain Downbeat

Shelter Inflation Will Remain Downbeat

Shelter Inflation Will Remain Downbeat

Chart 27The Fed Monitors Inflation Expectations

The Fed Monitors Inflation Expectations

The Fed Monitors Inflation Expectations

One factor could cause inflation to start moving durably higher than our base case anticipates. So far, money supply is behaving very differently than in the wake of the GFC. Back then, the Fed aggressively expanded its balance sheet, but the private sector’s deleveraging compressed money demand. Consequently, the Fed’s money injections stayed trapped in the banking system where excess reserves swelled. Broad money growth was tepid and the money multiplier collapsed. Today, the private sector is not deleveraging and M2 has surged at its fastest pace since 1944. Thanks to this lack of monetary bottlenecks, real interest rates fell much faster than in 2008/9 even if the nominal Fed Funds rate dropped to zero in both instances (Chart 28). Monetary conditions are therefore much more accommodative than they were 12 years ago. Another consequence of a functioning monetary system is that the broad money supply’s advance is outstripping the Treasury’s issuance. Historically, when money supply grows quicker than government debt, inflation emerges (Chart 29). We are tracking the velocity of money closely to gauge whether this risk is morphing into reality. Chart 28Policy Is More Accommodative Than During the GFC

bca.ems_ctm_2024_04_29_c6

Policy Is More Accommodative Than During the GFC

Policy Is More Accommodative Than During the GFC

Chart 29An Inflationary Risk

An Inflationary Risk

An Inflationary Risk

Ms. X: Before we move on to asset market forecasts for 2021, I would like to hear your thoughts on Brexit and the extraordinary showing of European unity last summer. BCA: We came very close to ending the Brexit transition period without a free-trade agreement between the UK and the EU. First, PM Boris Johnson had been under attack from the right wing of the Conservative party. In response, his government ramped up the hard rhetoric in recent months. However, the negative impact on the British economy in the absence of a free trade agreement with the EU was always a binding constraint on the PM. Hence, the tough rhetoric was mostly bluster and negotiation tactic with Brussels. Second, the electoral defeat of President Donald Trump in the US means that the UK is unlikely to receive preferential treatment from the US if it cannot reach a trade deal with the EU. The UK would be on its own, especially because President-Elect Joe Biden is likely to side with the EU, with whom he wants to rebuild a relationship. On the EU side, it is highly unlikely that Berlin will let French demands on fishing rights threaten its capacity to sell to its 5th export market. Thus, we expect a deal to come to fruition imminently. The move toward fiscal integration in Europe is also crucial beyond its near-term bullish impact on Italian, Spanish or Portuguese bonds. Jean Monnet, one of the architects of the 1951 Treaty of Paris that created the European Coal and Steel Community (the EU’s embryo), famously wrote in his memoirs that: “Europe will be forged in crises, and will be the sum of the solutions adopted for those crises.” We witnessed these dynamics last summer. The EUR750 billion Recovery Fund created by the European Commission to help economies struggling with the pandemic will issue its own bonds. It is the first step toward a permanent common bond issuance mechanism and fiscal risk sharing in the euro area. As expensive as stocks may be in absolute terms, the monetary and yield backdrop creates a large enough buffer for now. The experience of last decade’s euro crisis shows that temporary solutions often become permanent features of the EU, even if its treaties originally forbade them. The latest move will be no exception. The euro is popular; it is supported by 83%, 60%, 72%, 76% and 82% of the Spanish, Italian French, Dutch and German populations, respectively (Chart 30). Moreover, German support for the euro is particularly important. Germany’s current account surplus equals 7% of GDP because of the euro. The euro is a lot weaker than the Deutsche mark would be, which boosts German exporters’ competitiveness in international markets and within the euro area. Without the common currency, German cars would be much more expensive in France, Italy or China than they are today. Chart 30The Glue That Binds Europe Together

The Glue That Binds Europe Together

The Glue That Binds Europe Together

Likewise, the ECB Target II balance permanently attaches Germany to its weaker neighbors. Italy and Spain owe EUR 1 trillion to this settlement system while Germany is owed EUR915 billion. If Italy or Spain were to go bankrupt or to leave the euro and redenominate their debt in lira or pesetas, the resulting hit would threaten the viability of the German banking system (Chart 30, bottom panel). Chart 31Competitiveness Convergence

Competitiveness Convergence

Competitiveness Convergence

The past competitiveness problems of the European periphery are also steadily diminishing. Compared to Germany, harmonized unit labor costs in Italy or Spain have fallen 15% since 2009 and are not far from the levels prevailing at the introduction of the euro in 1999 (Chart 31). Consequently, current account deficits in Spain and Italy are narrowing considerably. Germany’s euro benefits, the tie created by the Target II imbalances and the periphery's improved competitiveness only bring Europe together and they allow the COVID-19 crisis to force a closer union. While these developments have little implication for Europe’s growth next year, they constitute a major long-term positive because they will curtail the cost of capital in the periphery and permit the sharing of funds necessary to build a lasting monetary union. Ms. X: To summarize; at the beginning of 2021, global growth should remain volatile. However, the recovery will ultimately strengthen over the remainder of the year thanks to the rollout of vaccines, the sustained fiscal support across major economies, the continued positive impact of China’s economic healing, and the strength of household balance sheets. Capex will remain robust as well, even if commercial real estate is a dangerous spot that we must monitor. Moreover, it is too early to ascertain whether the US or the EU will experience the strongest recovery in 2021, but emerging economies should lag behind. In addition, while you are concerned about the long-term inflation risk, consumer prices should not experience a durable pickup this year. Likewise, you foresee a benign outcome to the UK-EU trade negotiations and are positive on European integration. BCA: Yes, you summed it up nicely. Bond Market Prospects Ms. X: I find the Treasury market very puzzling right now. On the one hand, demanding valuations of US government bonds worry me, particularly in light of the upbeat economic outlook for 2021. On the other hand, if inflation remains low and the Fed is unlikely to push up rates until 2022 at the earliest, the upside for yields should be limited. BCA: We recommend a below-benchmark duration for fixed-income portfolios with an investment horizon of 12 months or so. Valuations partially underpin this recommendation. Our Global and US Bond Valuation Indices highlight that government bonds are at the level of overvaluation that, over the past 30 years, often produce a negative return in the following 12 months (Chart 32). However, valuations only indicate the degree of vulnerability of an asset but they rarely trigger price moves. Instead, timing most often relies on cyclical and technical factors. Favor cyclical equities relative to defensive ones. Cyclical forces are increasingly negative for bonds. In the US, our BCA Pipeline Inflation Indicator has perked up. It is not pointing toward an imminent rise in inflation but it suggests that deflationary risks are ebbing, something BCA’s Corporate Pricing Power Proxy also captures (Chart 33). A removal of the left-tail risk in CPI should push up yields, especially as our BCA Nominal Cyclical Spending Proxy is also firming, which normally happens ahead of meaningful yield pickups (Chart 33, bottom panel). Chart 32Pricey Bonds

Pricey Bonds

Pricey Bonds

Chart 33Cyclical Risks For Bond Prices

Cyclical Risks For Bond Prices

Cyclical Risks For Bond Prices

Chart 34Investors Will Want Protection Against Inflation Uncertainty

Investors Will Want Protection Against Inflation Uncertainty

Investors Will Want Protection Against Inflation Uncertainty

The odds of higher yields are most pronounced for longer maturities. First, our central forecast expects a significant rise in inflation in the latter part of the decade. Second, monetary and fiscal policy will remain very accommodative over the coming years even as private demand increases, which will lift medium- to long-term inflation uncertainty. Rising inflation uncertainty usually facilitates a steepening of the yield curve (Chart 34). Despite these forces, the upside to yields will prove limited in 2021. The Fed’s new inflation target means that it will be patient, and waiting for core PCE inflation to move sustainably above 2% could take time. The US central bank is therefore unlikely to increase interest rates for many years. This inertia limits the immediate upside in Treasury yields, but does not preclude it. While the Fed will not be quick to lift off, its forward interest rate guidance is not going to get any more dovish and the bond market is already pricing-in the first rate hike for late 2023. This expected liftoff date will be brought forward as the economy recovers, meaning that long-maturity nominal yields, real yields and inflation breakeven rates all have moderate upside. The recent equity market leadership of growth stocks is another limiting factor for higher yields. Growth stocks are extremely sensitive to long bond yields. If the latter back up too fast, it will scuttle bourses and unleash risk aversion and deflationary pressures. This creates an upper bound on the speed at which yields can move up. Mr. X: Even with their limited room to fall in the near term, the meaningful long-term and valuation risks of bonds make them so unappealing to me that I refrain from using them as near-term portfolio hedges. How can I protect my equity holdings right now? BCA: Hedging near-term risks to stocks has become one of the most hotly discussed topic with our clients because investors are witnessing the increasingly asymmetric payoffs of bonds. When equity prices rise, bond prices typically decline, but when stocks correct, bond prices barely rally. This newfound behavior of safe-haven bonds is a consequence of global policy rates having moved to or near their lower bound. We increasingly like small-cap firms relative to large-cap ones. For non-US based investors, there is a simple solution to this problem: parking some funds in US cash because the USD still acts as an effective hedge against market corrections. For US-based investors, finding adequate protection is more challenging. Those who can short and use leverage should sell currency pairs with an elevated sensitivity to changes in risk aversion, such as the EUR/CHF, AUD/JPY or MXN/JPY, to achieve some protection. Otherwise, holding cash to buy back stocks at lower levels remains an appropriate strategy. Mr. X: Which government bond market do you like most, or more accurately, which one should I avoid most right now? BCA: At the moment, we prefer the European periphery. The valuation ranking we often use when we see you is clear: Portuguese, Greek, Italian or Spanish bonds are the cheapest while German Bunds and US T-Notes are exceptionally expensive (Chart 35). Real bond yields confirm this estimation. Additionally, the nascent fiscal risk-sharing created by the European Commission’s Recovery Fund should result in declining breakup risk premia embedded in peripheral bonds. Furthermore, the ECB’s asset purchases are set to rise in response to Frankfurt’s efforts to fight off the deflationary effect of both the euro’s appreciation and the second wave’s lockdowns. Chart 35The Value Is In Europe’s Periphery

OUTLOOK 2021: A Brave New World

OUTLOOK 2021: A Brave New World

We are more negative on US Treasuries than Bunds. The valuation difference between the two safe havens is minimal. However, in 2020 the US has been more reflationary than Europe and the recent decline in the USD should lift US inflation relative to Germany’s, which will widen yield differentials in favor of Bund prices (Chart 36). Besides, the US economy has a higher potential GDP growth than Europe, which warrants a superior neutral rate of interest. Consequently, investors should expect US real yields to rise relative to the euro area’s benchmark. Outside of these markets, dedicated fixed-income investors should also overweight JGBs within their portfolio. JGBs have a low yield beta, which will limit their price declines if global yields move up. If the global recovery peters off, this feature will not create a major handicap because global yields have limited room to fall from here. Moreover, Japanese bonds are the cheapest safe haven (Chart 37). Chart 36Bunds vs Treasuries: Follow The Inflation Gap

Bunds vs Treasuries: Follow The Inflation Gap

Bunds vs Treasuries: Follow The Inflation Gap

Chart 37JGBs Are The More Attractive Safe Haven

OUTLOOK 2021: A Brave New World

OUTLOOK 2021: A Brave New World

We are neutral Canadian and Australian bonds. Historically, Canadian and Australian yields tend to have high betas to US T-Note yields. However, the BoC and the RBA are very active purchasers in their domestic markets, which will dampen the volatility of Canadian and Australian bonds. Ms. X: Considering the limited scope for major interest rate moves next year, what are your high-conviction trades for fixed-income portfolios? BCA: Within US government bond markets, we like curve steepeners. We also recommend positioning for rising inflation expectations by going overweight TIPS relative to nominal Treasuries. We particularly like real yield curve steepeners (within the TIPS curve). The cost of short-maturity inflation protection is below that of long-maturity protection, which means that short-term inflation breakeven rates have more upside as core PCE returns to the Fed’s target. A TIPS-curve steepener benefits from both a flattening of the inflation breakeven curve and a steepening of the nominal Treasury curve. It is therefore a high-octane play on both our favored strategies. We like both Europe and Japan. Within US corporate credit, we are currently overweight investment grade and Ba-rated high-yield bonds. However, valuation at the upper-end of the credit spectrum heavily favors tax-exempt municipal bonds over corporates. Investors that can take advantage of the tax exemption should prefer munis over investment grade corporates. Elsewhere, we are underweight MBS as pre-payment risk is elevated, but we like consumer ABS due to the strong position of household balance sheets. Ms. X: Before we moved on to equities, where do you stand on EM credit? Do you expect any global search for yield to push EM bond prices higher? BCA: With a few exceptions like Mexico and Russia, we prefer US corporate bonds to dollar denominated EM bonds of similar credit quality. EM bonds offer poorer value, but EM spreads will continue to evolve in line with US corporate spreads. Because of this directional correlation, our preference for US investment grade bonds translates to EM bonds as well. Our more circumspect attitude toward EM high-yield bonds also reflects our more conservative stance on US high-yield bonds. For local-currency rates, we are receivers in the swap market because the near-term outlook for EM currencies is difficult. Most EM countries have a deflation problem, not inflation troubles. Hence, real and nominal rates in emerging economies will fall as central banks try to stimulate their economies. These declines will be positive for the local-currency performance of EM bonds but it will hurt their currencies. Over the next twelve months, this challenge will be most pronounced against non-US DM currencies. In the short-term, this hindrance will also exist against the USD because the Greenback should rebound temporarily, something we can discuss in more detail in our chat about the currency and commodity markets. Our favorite bets are to receive Mexican, Colombian, Russian, Indian, Chinese and Korean swap rates. Mr. X: I agree that the case to make a major duration bet next year is limited, but risks are slightly skewed toward upside for yields. I am a little surprised that you like European peripheral bonds so much and yet prefer Bunds to Treasuries. I will have to digest your view on EM bonds because I would have bought EM currencies outright. Finally, I find your real yield curve steepener idea extremely intriguing. Thank you for giving me ideas to ponder. Now, shall we move to next year’s equity outlook? Equity Market Outlook Chart 38The Bubble Can Grow

The Bubble Can Grow

The Bubble Can Grow