Emerging Markets

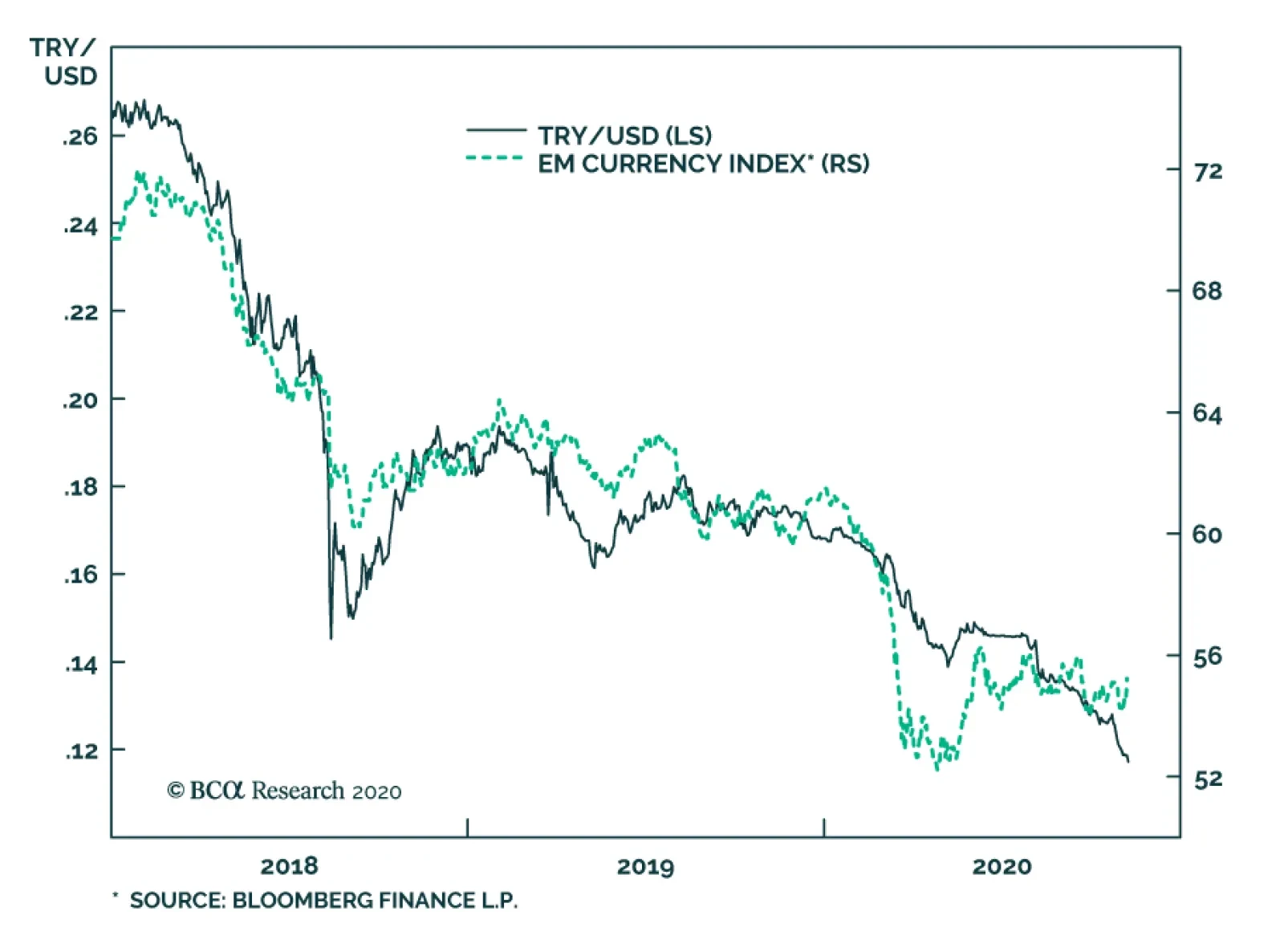

This past weekend was an eventful one in Turkey. President Recep Tayyip Erdogan fired central bank governor Murat Uysal on Saturday, replacing him with former finance minister and trusted ally Naci Agbal. The following day, finance minister Berat Albayrak…

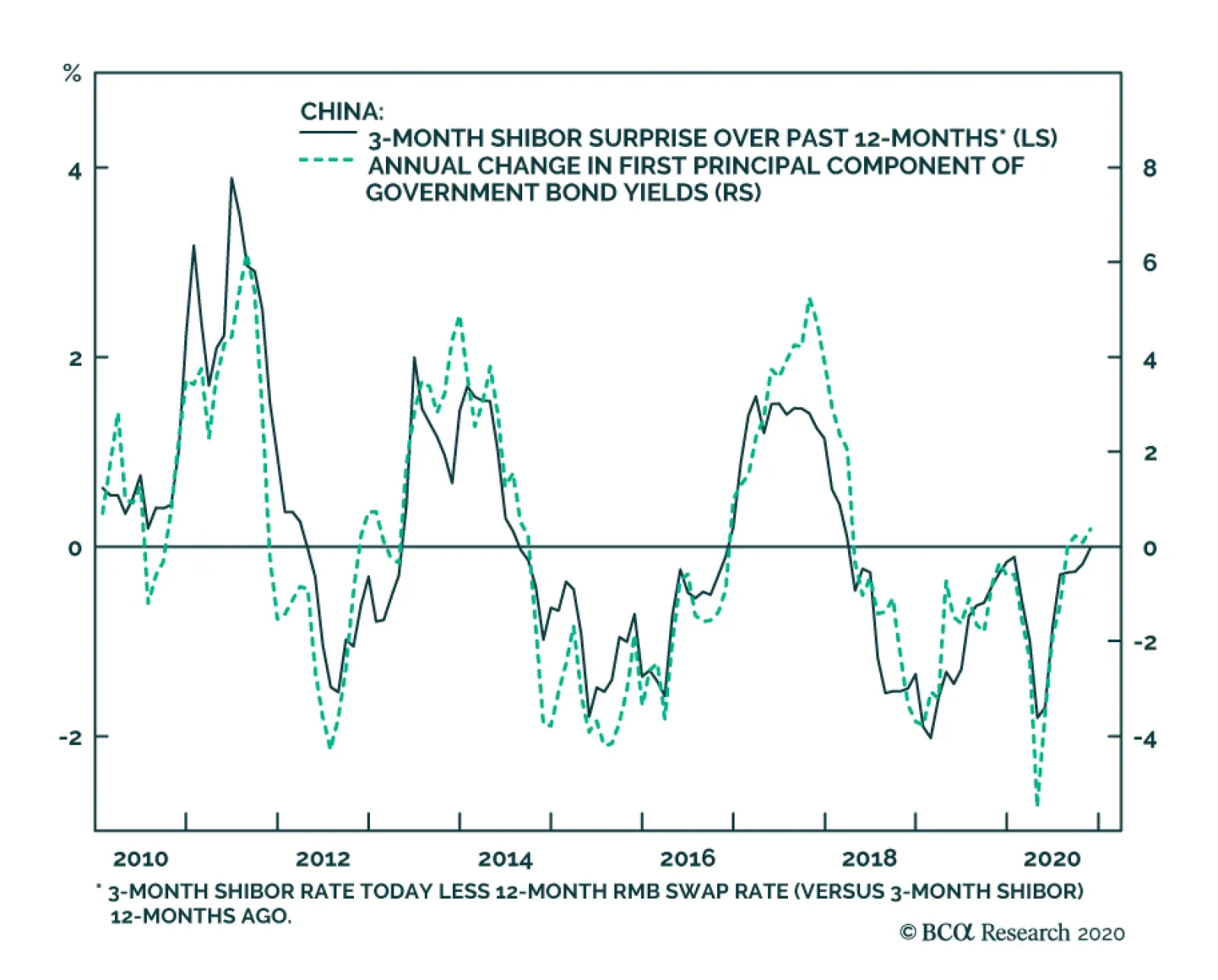

In a Special Report earlier this year, our China Investment Strategy service applied the “Golden Rule Of Bond Investing”, which links developed economy government bond returns to central bank policy rate “surprises” versus market expectations, to China. The…

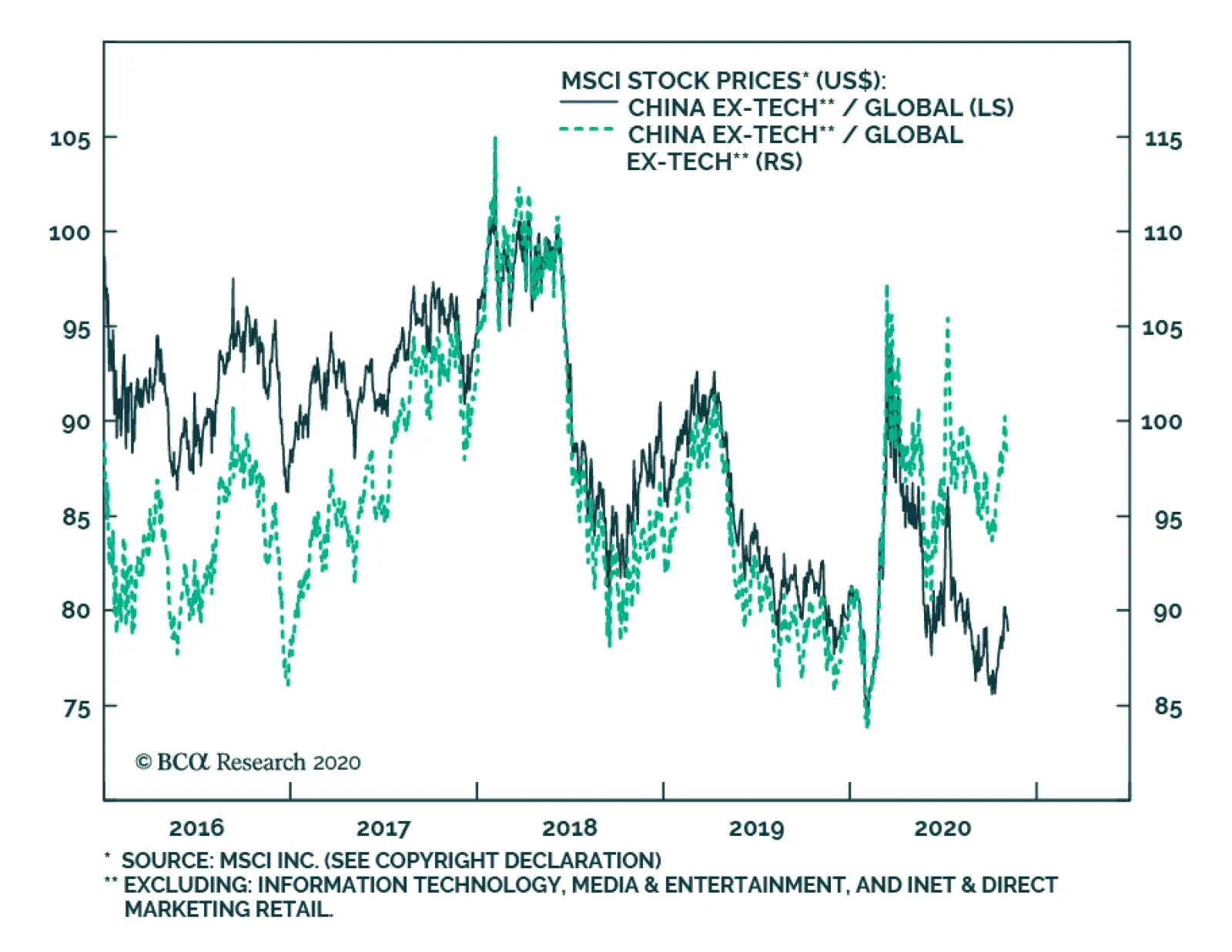

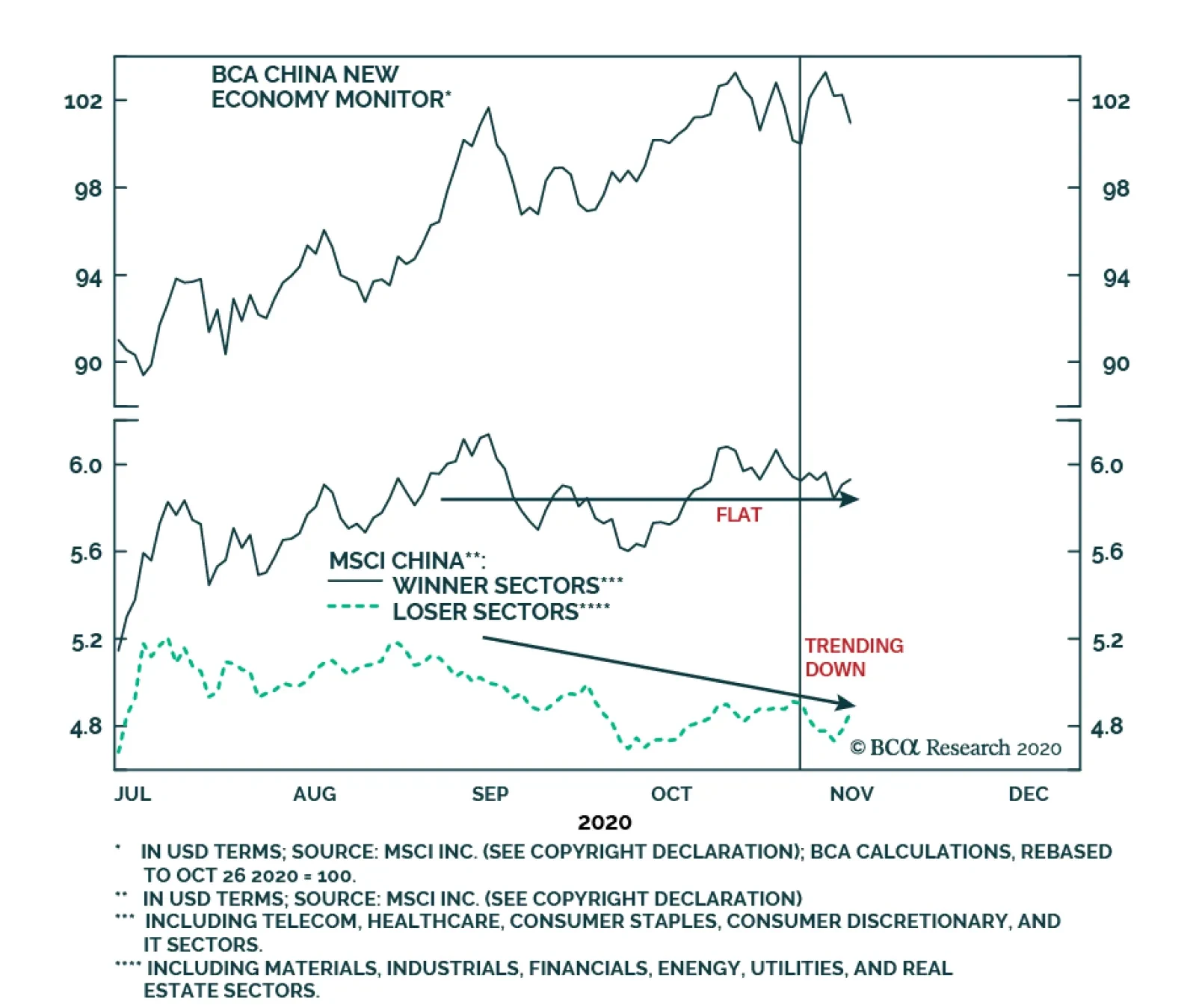

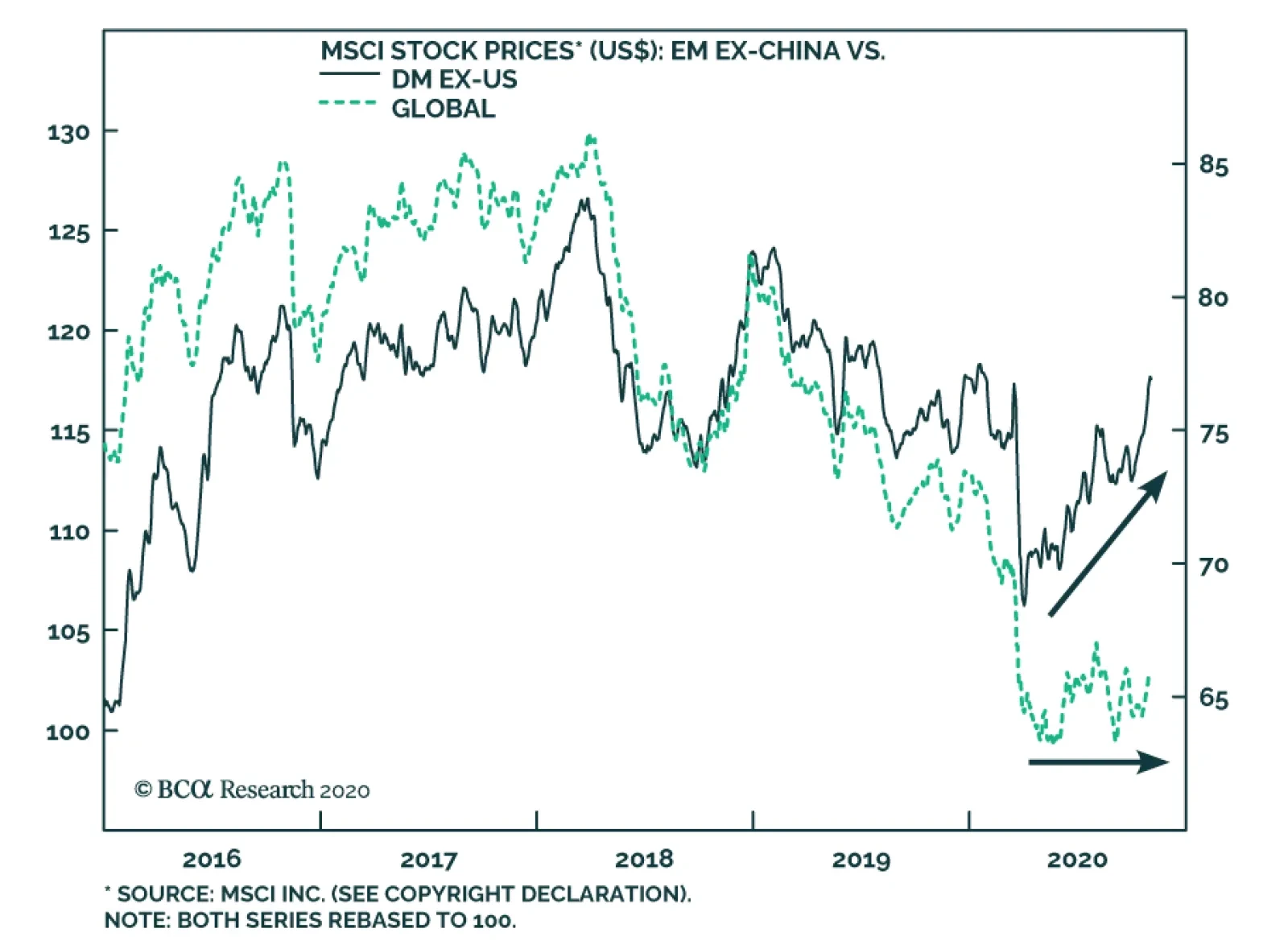

We noted in an Insight earlier this week that the recent outperformance of emerging market stocks has been almost entirely due to China's outperformance, given that the relative performance of EM ex-China versus the global benchmark has recently been flat. …

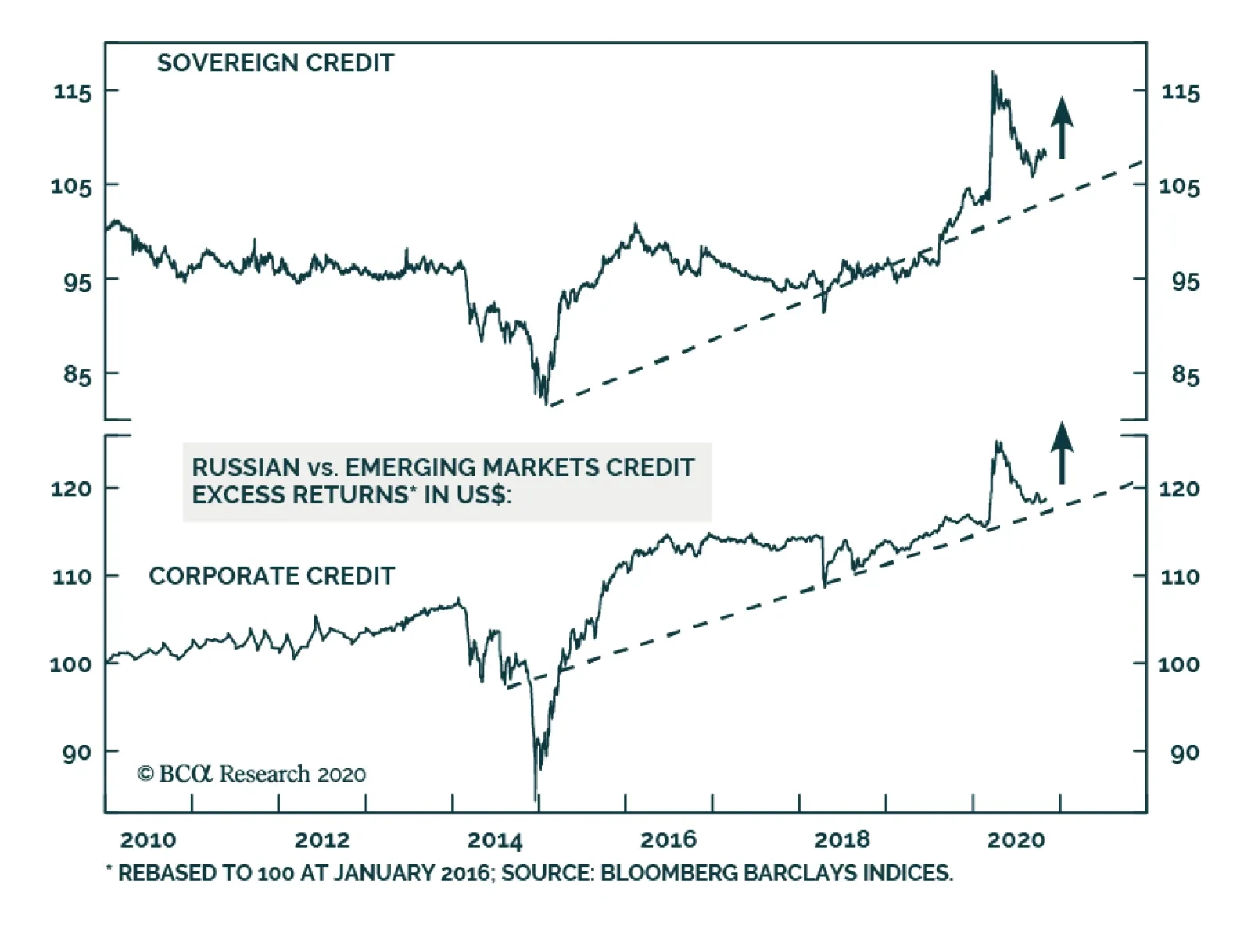

According to BCA Research's Emerging Markets Strategy service, a relapse in oil prices and forthcoming fiscal austerity in Russia will dampen the rebound in domestic demand while keeping a lid on inflation. Authorities have ample room to further ease…

BCA Research's China Investment Strategy service has argued that the Proposal from China’s 14th Five-Year Plan does not change our cyclical view on Chinese assets. The 14th Five-Year Plan has more strategic importance than in the past decade; the plan…

The 14th Five-Year Plan has more strategic importance than in the past decade. Spending on national defense, technological self-sufficiency, public welfare and green energy will likely see substantial increases under the guidelines of a strong central government. The Proposal from the Five-Year Plan does not change our cyclical view on Chinese assets. Beyond mid-2021, the differences in sectoral performance will widen. We will likely begin to trim our position in China’s “old economy” stocks in the first half of 2021.

EM stocks have rallied relative to global stocks over the past month, but this rally masks underlying dynamics. The chart above shows that this rally has been due almost entirely to the outperformance of Chinese stocks, as the relative performance of EM…

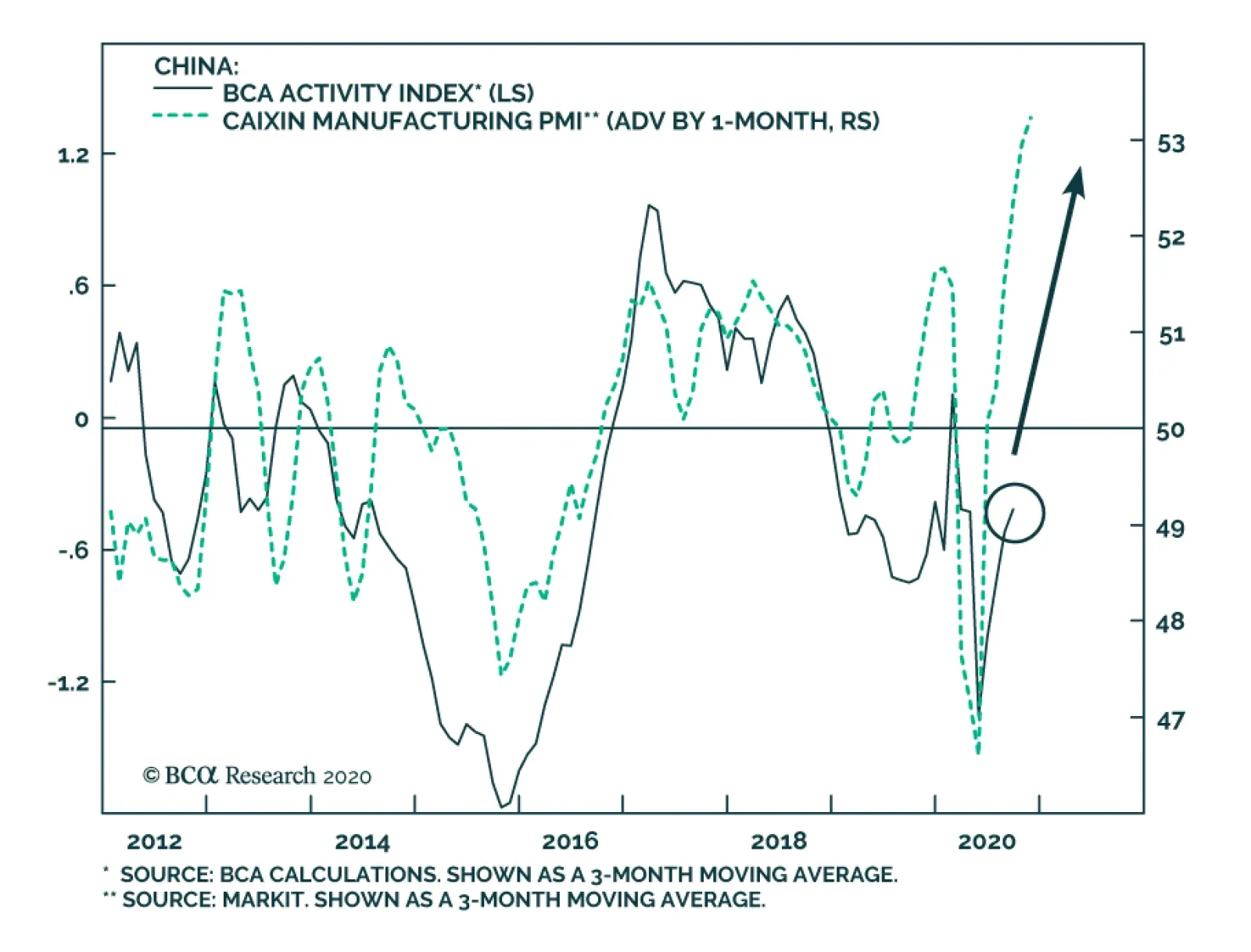

PMI indexes are coincident rather than leading indicators, but they are timely and often act as important confirming indicators. In this regard, the October update to the Caixin manufacturing PMI suggests that the uptrend in our BCA China Activity Index is…

Highlights A Biden victory with a Republican Senate (28% odds) poses the greatest risk to the global reflation trade. The US is the most susceptible to social unrest of all the developed markets. Europe is stable relative to the US, but political risks are rising as new lockdowns go into effect. Emerging markets are also susceptible to social unrest – even those that look best on paper. Chile and Thailand have more downside due to politics, despite underlying advantages. Turkey and Nigeria are among those at risk of major unrest in a post-COVID world. Book gains on EUR-GBP volatility, Indian pharma, and rare earths. Cut losses. Feature This week saw a long-awaited risk-off move in global financial markets. A new wave of COVID lockdowns plus the US failure to pass a fiscal package finally registered with investors. Over the past two months we have argued that rising COVID cases without stimulus would produce a pre-election selloff that would drive the final nail in President Trump’s re-election bid. That should still be the case (Chart 1). While we are sticking with our view that Biden will win, we have upgraded Trump’s odds from 35% to 45%. We are focused on Trump’s momentum – not alleged polling errors – in Florida and Pennsylvania, and Biden’s loss of altitude in Arizona, as these trends open a clear Electoral College path to another Trump victory (Chart 2). Nevertheless Biden is tied with Trump among men and leads by 17 percentage points among women. He is also in a statistical tie among the elderly. Chart 1COVID Rising + Stimulus Falling = Red Ink

COVID Rising + Stimulus Falling = Red Ink

COVID Rising + Stimulus Falling = Red Ink

Chart 2Trump's Momentum In Swing States

Trump's Momentum In Swing States

Trump's Momentum In Swing States

Even assuming Trump’s comeback proves too little, too late, it could produce a contested election in which Trump has constitutional advantages, or a Republican Senate. Either of these two scenarios would extend the election season volatility for one-to-three months. Our updated US election probabilities are shown in Table 1 alongside the odds from the popular online betting site PredictIt.org. Table 1There Is A 72% Chance The Post-Election Policy Setting Will Favor Reflation

Election Trades And Global Social Unrest: A GeoRisk Update

Election Trades And Global Social Unrest: A GeoRisk Update

A Biden victory with a Republican Senate (28% odds) is the only deflationary scenario in the near term, since fiscal stimulus will be reduced in size and uncertain in timing. However, assuming financial market pressure forces senators to agree, this is actually the best outcome over the full two-year Senate election period, since neither tariffs nor corporate taxes would rise. Notably Treasury yields have risen regardless of election scenario, but there is little doubt that this scenario poses the greatest risk to the global reflation trade (Chart 3). Why does this election matter? Trump’s re-election would prolong US political polarization and “maximum pressure” foreign and trade policy. Trump must win through the constitutional system, not the popular vote, so a win would push polarization up. Polarization at home, including Democratic opposition in the House of Representatives, would drive him abroad. By contrast, a Biden win would include a popular majority and might include a united Democratic Congress, which would result in a clear popular mandate and would concentrate Biden's administration on an ambitious domestic agenda. A Biden victory with a Republican Senate (28% odds) poses the greatest risk to the global reflation trade. Hence Trump’s election would bolster the USD and US equity outperformance, along with global policy uncertainty relative to the United States (Chart 4). Whereas Biden’s election, if it also brings a Democratic Senate, would bolster global equity outperformance, cyclical equities, and US policy uncertainty relative to global. Chart 3Republican Senate Less Reflationary

Republican Senate Less Reflationary

Republican Senate Less Reflationary

Chart 4Trump Would Boost US Equity Outperformance

Trump Would Boost US Equity Outperformance

Trump Would Boost US Equity Outperformance

The election will have a geopolitical fallout. First, Trump is still president through January 20 regardless of outcome and could take aggressive actions to seal his legacy and lock the Biden administration into conflict with China or Iran. Second, a contested election would create a power vacuum in which other nations could seek to take advantage of American distraction. Third, a Trump victory spells strategic conflict with Iran and China, and either could try to seize the advantage by acting first. Fourth, a Biden win spells confrontation with Russia and ultimately China, and both countries would test his resolve early in his administration. Diagram 1 summarizes these key market takeaways of the US election scenarios. This week we provide our monthly GeoRisk Update with a special focus on our COVID-19 Social Unrest Index and implications for select developed, emerging, and frontier markets. Diagram 1Scenarios For US Election Outcomes And Market Impacts

Election Trades And Global Social Unrest: A GeoRisk Update

Election Trades And Global Social Unrest: A GeoRisk Update

The United States The market can get hit by negative surprises after the US election just as easily as before.1 The US is a powder keg of social and political angst, ranking the worst among developed markets in our COVID-19 Social Unrest Index (Table 2). The lower a country ranks on the list, the less stable it is and the more susceptible to unrest. Social unrest becomes market-relevant if it weighs on consumer or business sentiment, or if it causes a major change in government or policy. Table 2The US Is The Developed Market Most Susceptible To Social Unrest

Election Trades And Global Social Unrest: A GeoRisk Update

Election Trades And Global Social Unrest: A GeoRisk Update

The first US risk is a contested election. By rallying in the swing states in the final weeks of the election, Trump has increased the likelihood of a disputed outcome. Armies of lawyers will descend upon the swing state election boards. The Supreme Court’s intervention in Florida in 2000 has incentivized political parties to seek a judicial intervention, especially if they think they are losing the popular vote narrowly. Mail-in counts, recounts, and other disputes could push up against the December 14 Electoral College voting date. Worse, if the Electoral College is hung, the House of Representatives would have to decide the outcome in January. Volatility and risk-off sentiment would predominate. Emerging markets are showing the first signs of upheaval in the wake of this year’s crisis. The second risk is resistance to the election results. If Trump wins on a constitutional technicality, the country faces widespread unrest. This would be relevant to investors if it paralyzes major cities, exacerbates the COVID outbreak, or snowballs into something big enough to suppress consumer confidence. If Biden wins on a technicality, the country faces not widespread unrest but isolated pockets of potentially armed resistance or domestic terrorist attacks. The FBI, DHS, and recent news events have confirmed the presence of armed or violent extremist groups of various ideological stripes that pose a rising threat in the current climate of pandemic, unemployment, and polarization.2 They could strike any time after the election. Europe And Brexit Chart 5European Lockdowns Push Up Political Risk

European Lockdowns Push Up Political Risk

European Lockdowns Push Up Political Risk

Europe and Canada have reinstated lockdowns in response to their rise in COVID-19 cases. The surge in political risk is evident from our GeoRisk Indicators (Chart 5). These lockdowns will not be as draconian as earlier this year as the death rate has been found to be lower than once feared. While most governments have time on the political clock to take a hardline approach today, at the start of what could be a nasty winter season, they do not have so much leeway in 2021. Greece, Spain, Italy, the UK, and France are next in line for social unrest, after the US, in our index, Table 2 above. These countries are also vulnerable because fiscal support is not as robust as elsewhere, as can be seen by our global fiscal stimulus tracker (Chart 6). France is in better shape than the others and marks the dividing line – the 2017 election was a turning point in which the political establishment unified to defeat a right-wing populist challenge. President Emmanuel Macron’s popularity is holding up decently and it will now be buttressed by his tough stance against a spate of radical Islamist terrorist attacks. Extremist incidents will continue to be a problem, given the lockdowns and economic slump. Macron will focus on economic reflation in 2021 leading up to an election for which he is clearly favored in spring of 2022. Anything that derails his political trajectory before that time is of great importance for Europe’s political future, since Macron will be the de facto leader once Angela Merkel steps down in October 2022. Italy and Spain will be ongoing sources of political risk. Italy was the first major European hotspot of the pandemic, and euroskeptic attitudes are quietly ticking back up, but the ruling coalition and especially Prime Minister Giuseppe Conte have received popular backing for their handling of the crisis. Spain, on the other hand, has seen Prime Minister Pedro Sánchez lose support, while conservative parties tick up in popular opinion. These two countries are candidates for early elections when the hens come home to roost for the pandemic and recession (Chart 7). Chart 6More Stimulus Needed In Europe

Election Trades And Global Social Unrest: A GeoRisk Update

Election Trades And Global Social Unrest: A GeoRisk Update

Chart 7Europe’s Leaders Fare Better Than Others

Election Trades And Global Social Unrest: A GeoRisk Update

Election Trades And Global Social Unrest: A GeoRisk Update

The other major countries with looming elections in 2021-22 are seeing relatively positive outcomes in popular opinion (e.g. the Netherlands, Germany). The exception is the UK, which is on the lower end of the social unrest index and is in the midst of internal disruption due to Brexit. Our assessment remains that Prime Minister Boris Johnson and the Tories will have to accept a trade deal with the EU over the next month (Chart 8). They can afford to leave on paper, but the economy would suffer and Scotland’s nationalists would be empowered to attempt secession. Our European Strategist Dhaval Joshi believes a Biden win in the US will hasten Johnson’s capitulation. We don’t expect much more upside in our GBP-EUR volatility trade after the US election result is known (Chart 9). Chart 8Go Long Sterling

Go Long Sterling

Go Long Sterling

Chart 9Close EUR-GBP Volatility Trade

Close EUR-GBP Volatility Trade

Close EUR-GBP Volatility Trade

Chart 10Trump Would Weigh On Euro

Trump Would Weigh On Euro

Trump Would Weigh On Euro

Trump’s re-election would be negative for the European Union’s economic and political stability (Chart 10). It would portend a greater trade war, Middle Eastern instability and refugees, Russian aggression, or European populism. By contrast, Biden will not use sweeping tariffs to resolve trade tensions, will seek to restore the 2015 nuclear deal with Iran, will suppress anti-establishment politics, will seek a multilateral approach to China trade tensions, and will only substantially aggravate the Europeans by being too aggressive on Russia. EM: Chile And Thailand Emerging markets are showing the first inevitable signs of upheaval in the wake of this year’s global crisis. What is critical to note about our Social Unrest Index for EM is that even if a country ranks high on the list overall, it could still face significant sociopolitical upheaval. This is manifest in the top-ranked countries of our list – Chile, Malaysia, Thailand, Russia, Indonesia – all of which have already seen some degree of social and/or political unrest in this crisis year (Table 3). Table 3Even Emerging Markets That Look Good On Paper Are Susceptible To Unrest

Election Trades And Global Social Unrest: A GeoRisk Update

Election Trades And Global Social Unrest: A GeoRisk Update

The best example is Chile, which is top-ranked in the index but ranks ninth in the “Household Grievances” column, which measures inequality, inflation, and unemployment. The latter measure helps explain how Chile erupted last fall and again this fall in mass protests. Chart 11Political Risk Weighs On Chile

Political Risk Weighs On Chile

Political Risk Weighs On Chile

Over the past week Chileans voted overwhelmingly in a referendum to revise their constitution with a constitutional convention that will be elected, i.e. not overdetermined by current members of the National Congress. The constitutional revision process is ultimately a positive way for a country with good governance to assuage its household grievances. But the process will continue through a revision process in April 2021, the November 2021 general election, and a final referendum in 2022, ensuring that political risk persists. Chilean assets have fallen short of their expected performance based on global copper prices, suggesting that they have upside in the near term (Chart 11). Positive news is driven by macro fundamentals, including Chinese stimulus, but political risk will periodically put a cap on rallies by highlighting Chile’s transition to expansive social spending, higher debts, and hence future currency risk. Thailand’s case is different, as it is not household grievances per se but rather the ongoing governance problem that is triggering mass protests. The governance problem stems from regional disparities in wealth and representative government. Modern society and pro-growth populism have repeatedly clashed with the royalist political establishment and its military backers over the past 20 years and that process is set to continue. Chart 12Thailand Not Fully Pricing New Instability Cycle

Thailand Not Fully Pricing New Instability Cycle

Thailand Not Fully Pricing New Instability Cycle

The newest round of the crisis will build for some years and ultimately culminate in some degree of bloodshed before a new political settlement is achieved. Typically, over the past 20 years, Thai political unrest creates a buying opportunity for investors. But the previous major wave of unrest, from 2006-14, occurred during the lead-up to the all-important royal succession. Now the succession is “over” and it is not clear that the new king, Vajiralongkorn, will live up to his father’s legacy as a successful arbiter of society’s conflicts. It is possible that he will overreact to domestic opposition and abuse his powers. Our Emerging Markets Strategy has downgraded Thailand in its portfolio, showing that the economy is suffering from insufficient stimulus as a negative credit impulse offsets public spending during the crisis. Thai equities do not offer relative value within the emerging market space at present (Chart 12). Most likely Thai political troubles will continue to provide a buying opportunity, but at the moment the risks are not sufficiently priced. If Chile, Malaysia, and Thailand are already experiencing significant political risk despite their high rankings on our index, then Brazil, South Africa, Turkey, and the Philippines face even greater challenges going forward. We have written about Brazil recently – we continue to see a rising political risk premium there (Chart 13). We will update our views on South Africa and the Philippines in forthcoming special reports. For now we turn to Turkey. Turkey: One Step Forward, Two Steps Back Turkey scores near the bottom of our Social Unrest Index. The regime of President Recep Tayyip Erdogan has been in power for nearly two decades, is suffering cracks in public support, is continuing to suffer the inflationary consequences of populist monetary and fiscal policy, and is embroiled in a range of international adventures and conflicts, now including Nagorno-Karabakh. After a brief pause of tensions in September, we argued that President Recep Tayyip Erdogan’s retreat would be temporary and that geopolitical tensions would re-escalate. They have done so even sooner than we thought. The lira is collapsing, as registered by our GeoRisk Indicator, which is once again on the rise (Chart 14). Chart 13Brazilian Political Risk Nearing 2018 Levels

Brazilian Political Risk Nearing 2018 Levels

Brazilian Political Risk Nearing 2018 Levels

Chart 14Turkish Political Risk Spikes Anew

Turkish Political Risk Spikes Anew

Turkish Political Risk Spikes Anew

Relations with Europe have worsened significantly. Aggressive rhetoric between Erdogan and Macron in response to France’s treatment of French Muslims and handling of recent terrorist incidents has led to a diplomatic crisis: Paris recalled its ambassador. The episode highlights both Erdogan’s increased assertiveness vis-à-vis the EU as well as his Neo-Ottoman bid to become the leader of the Muslim world. Erdogan has called for a boycott of French goods (alongside similar popular calls in various Muslim countries). The European Commission warned Turkey could face punitive action at its December summit. The feud in the eastern Mediterranean is also escalating. Turkey’s Oruc Reis seismic research vessel was once again sent out on an exploratory mission in contested waters on October 12. The mission’s duration was extended multiple times. The EU may impose sanctions as early as December. Brussels' response to Turkish provocations may include targeted anti-dumping measures, likely on steel and fish. There have also been calls to suspend the customs union, but this would require the conflict to rise above rhetoric as it would harm EU investments in Turkey. Turkey is growing even more assertive in its neighborhood with its support for Azerbaijan in the conflict with Armenia. Tensions with Russia are rising yet again. Erdogan is already overextended in Syria and Libya, and recently threatened to launch a new military operation in northern Syria if Kurdish militants do not relocate from along Turkey’s border. The warning follows a Russian airstrike on Turkey-backed Syrian rebels in Idlib earlier this week – the deadliest strike in Idlib since March. Provoking the United States, Turkey also tested its newly purchased Russian S400 missile defense system on October 16. This was swiftly followed by US warnings that Turkey faces US sanctions under the Countering America’s Adversaries Through Sanctions Act if it operationalizes the system. The risk of punitive action would rise under a Biden presidency as he is more likely to adopt a tougher stance on Erdogan than President Trump. Chart 15More Downside For Turkish Lira

More Downside For Turkish Lira

More Downside For Turkish Lira

These developments all point to a continuation in geopolitical tensions, as Erdogan flouts various risks and constraints. Turkey’s relationship with NATO allies is continuing to deteriorate meaningfully. The lira’s collapse is also in response to economic developments. After a surprise 200 basis points rate hike in September, the CBRT disappointed markets by keeping the benchmark 1 week repo rate on hold at its October 22 meeting. Investors had hoped that the September hike marked a reversal of Erdogan’s unorthodox policies. However, the October decision disconfirms this hope, as the central bank is instead opting for stealth measures to raise the cost of funding (e.g. limiting funding at the benchmark rate and thus forcing banks to borrow at higher costs; widening the interest rate corridor to give itself more room to raise the weighted average cost of funding). These decisions come amid rising inflation, debt monetization, a loss in foreign interest in Turkish equities and bonds, and deteriorating budget and current account balances. All point to further lira weakness (Chart 15). Bottom Line: The TRY faces downside pressure from the deteriorating geopolitical and economic backdrop. Although the EU has so far shown restraint in penalizing Ankara, its stance has not dissuaded Erdogan from adopting a provocative foreign policy stance. Moreover tensions with the US are at risk of escalating due to the possibility of a Biden presidency. Economic factors also point to continued weakness as monetary policy is too loose and the CBRT has not abandoned Erdoganomics. Nigeria: No Political Change Waves of protests have erupted across Nigeria in recent weeks, largely driven by the country’s youth. Protests center on calls to end the special anti-robbery squad (SARS), an arm of the national police service, which has long been accused of extrajudicial killings, torture, extortion, and corruption. Most recently, dozens of soldiers and police officers approached the scene of a major protest site in Lekki, a large district in Lagos, and opened fire, killing 12 people. The violence fueled outrage toward the government and security forces. To quell unrest, the government announced that SARS would be disbanded and promised a host of reforms. Demonstrators are skeptical of government promises without clearly specified timeframes. After all, previous incumbents have suggested police reform would be expedited. This has yet to happen, so we do not expect national policy to meet public demand. Moreover, President Buhari is a former military dictator who has maintained a hard line on security matters. He is in his final term in office and not legally required to step down until 2023. While discontent grows toward the government for social injustices, the Nigerian economy remains vulnerable and imbalanced. The local currency is facing considerable risk of major devaluation stemming from strains on its balance of payments, as BCA’s Emerging Markets Strategy pointed out in a recent report. Low oil prices and weak FDI inflows will foster various imbalances impeding the nation’s structural adjustments and its potential growth rate. The US election will act as a positive catalyst for markets in the short run as long as it produces a clear result and resolves the US fiscal stalemate. Nigeria’s current account excluding oil has been structurally wide, a sign of weak domestic productivity and an uncompetitive currency (Chart 16). Foreign currency reserves stand at $36bn, barely above foreign debt obligations at $28bn. FDI inflows have reached their second lowest point over the past decade, weighing on productivity growth, which is near 0%. A positive for Nigeria’s macro fundamentals is that public debt is low, at 23% of GDP, decreasing the likelihood of a sovereign default in the near term. Government officials refrained from large COVID fiscal relief, keeping spending in check. Coupled with low debt servicing costs, of which the foreign share only represents 2% of government revenues, a currency depreciation to improve competitiveness would not make public debt dynamics a concern. Nominal GDP is above short-term rates (Chart 17). Hence there is room for the currency to fall and government spending to pick up into next year to support the economy. Chart 16Nigeria Struggles With Economic Rebalance

Nigeria Struggles With Economic Rebalance

Nigeria Struggles With Economic Rebalance

Chart 17Nigeria Has Fiscal Firepower

Nigeria Has Fiscal Firepower

Nigeria Has Fiscal Firepower

In the post-dictatorship era, oil revenues knit the country’s predominantly Muslim north with its oil-rich and predominantly Christian south. The country has struggled to rebalance the economy in the wake of the 2014 oil shock. Crude production has fallen from over 2 million barrels per day to around 1.6 million bpd since 2010, and Nigeria struggles to meet its modest OPEC quotas. The current global crisis could have a negative long-term impact as rig counts have fallen again. We expect global oil demand to be supported in 2021, as lockdowns will be less stringent the second time and global fiscal stimulus will keep coming. And while Buhari’s age and poor health make him vulnerable, he is not without reserves of political strength. He is seen as someone who has kept up a good fight against the Islamist militant group Boko Haram. Considering that he is a northerner and a Muslim by faith, this strategy has helped ease sectarian tensions across the country, strengthening his grip. The problem is that the size of the global crisis could upset even the most stable of petro-states. Like most of sub-Saharan Africa, the youth population is large – the median age is around 18. If global oil demand relapses amid the second wave of the pandemic and a lack of domestic and global stimulus, the country will suffer yet another wave of unemployment. And if policy remains hawkish, sociopolitical troubles will be amplified. Nigeria’s impact on global oil prices is limited – it only provides 2% of global oil supply – but it could become a contributor to rising unplanned outages if instability gets out of hand. Bottom Line: The SARS protests are not likely to threaten overall government stability, but mounting economic pressures could exacerbate social unrest, and the negative feedback with security forces. This could deliver a significant blow to the aging Buhari’s government if he does not enact expansionary fiscal policy to smooth out the external shocks. Investment Takeaways Chart 18Biden Good For Global Trade Rebound

Biden Good For Global Trade Rebound

Biden Good For Global Trade Rebound

The US election will act as a positive catalyst for markets in the short run as long as it produces a clear result and resolves the US fiscal stalemate. But a contested election is not unlikely and a deflationary risk arises in the 28% chance that Biden wins while Republicans retain the Senate. Stimulus would still be agreed but its size and timing would be uncertain, prolonging the selloff. Therefore we are updating our portfolio to book some gains and cut some losses. We are booking gains on our EUR-GBP volatility trade for a return of 13%. We are closing our long Indian pharmaceuticals trade for a gain of 12%. We are throwing in the towel on our long defense and aerospace trade for a loss of 21%. And we are closing our rare earths basket trade for a gain of 5%. We are closing two pair trades and re-initiating them as absolute longs: long China Play Index relative to MSCI global stocks (0.1% return) and long ISE Cyber Security Index relative to the NASDAQ (-6.8%). Chinese reflation and global cyber-attacks will remain relevant themes. The inverse of Trump, Biden is positive for the euro, negative for the dollar, and supportive of global trade. However, a range of higher taxes and levies on corporations suggests that his administration will ultimately weigh on S&P global stocks relative to those at home. And while Biden appears softer on China, we consider this a mispricing, as he has largely coopted Trump’s and Sanders’s trade agenda (Chart 18). Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Roukaya Ibrahim Editor/Strategist Geopolitical Strategy RoukayaI@bcaresearch.com Guy Russell Research Analyst GuyR@bcaresearch.com Chart 19China: GeoRisk Indicator

China: GeoRisk Indicator

China: GeoRisk Indicator

Chart 20Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

Chart 21UK: GeoRisk Indicator

UK: GeoRisk Indicator

UK: GeoRisk Indicator

Chart 22Germany: GeoRisk Indicator

Germany: GeoRisk Indicator

Germany: GeoRisk Indicator

Chart 23France: GeoRisk Indicator

France: GeoRisk Indicator

France: GeoRisk Indicator

Chart 24Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Chart 25Canada: GeoRisk Indicator

Canada: GeoRisk Indicator

Canada: GeoRisk Indicator

Chart 26Spain: GeoRisk Indicator

Spain: GeoRisk Indicator

Spain: GeoRisk Indicator

Chart 27Taiwan: GeoRisk Indicator

Taiwan: GeoRisk Indicator

Taiwan: GeoRisk Indicator

Chart 28Korea: GeoRisk Indicator

Korea: GeoRisk Indicator

Korea: GeoRisk Indicator

Chart 29Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

Chart 30Brazil: GeoRisk Indicator

Brazil: GeoRisk Indicator

Brazil: GeoRisk Indicator

Geopolitical Calendar Footnotes 1 There have been strange warnings in recent days – an unidentified aircraft intercepted over a Trump rally in Arizona, a Saudi warning of a potential Houthi attack on Americans, and a Chinese warning of a potential US drone attack against Chinese assets in the South China Sea. None of these have amounted to anything, and the idea of a US drone attack on China is absurd, but investors should be cautious nonetheless, particularly because a range of state and non-state actors will have an incentive to take actions once the US outcome is known. 2 Please see FBI Director Christopher Wray, “Statement Before The House Homeland Security Committee,” Washington DC, September 17, 2020, fbi.gov; Department of Homeland Security, “Homeland Threat Assessment,” October 2020, dhs.gov; Tresa Baldas and Paul Egan, “More details emerge in plot to kidnap Michigan Gov. Whitmer as suspects appear in court,” USA Today, October 13, 2020, usatoday.com.

BCA Research's Emerging Markets Strategy service believes that the risk-off period in global markets will continue in the near run, i.e., there will be dusk before a sunrise. Hence, investors should maintain dry powder at the moment. Global risk assets…