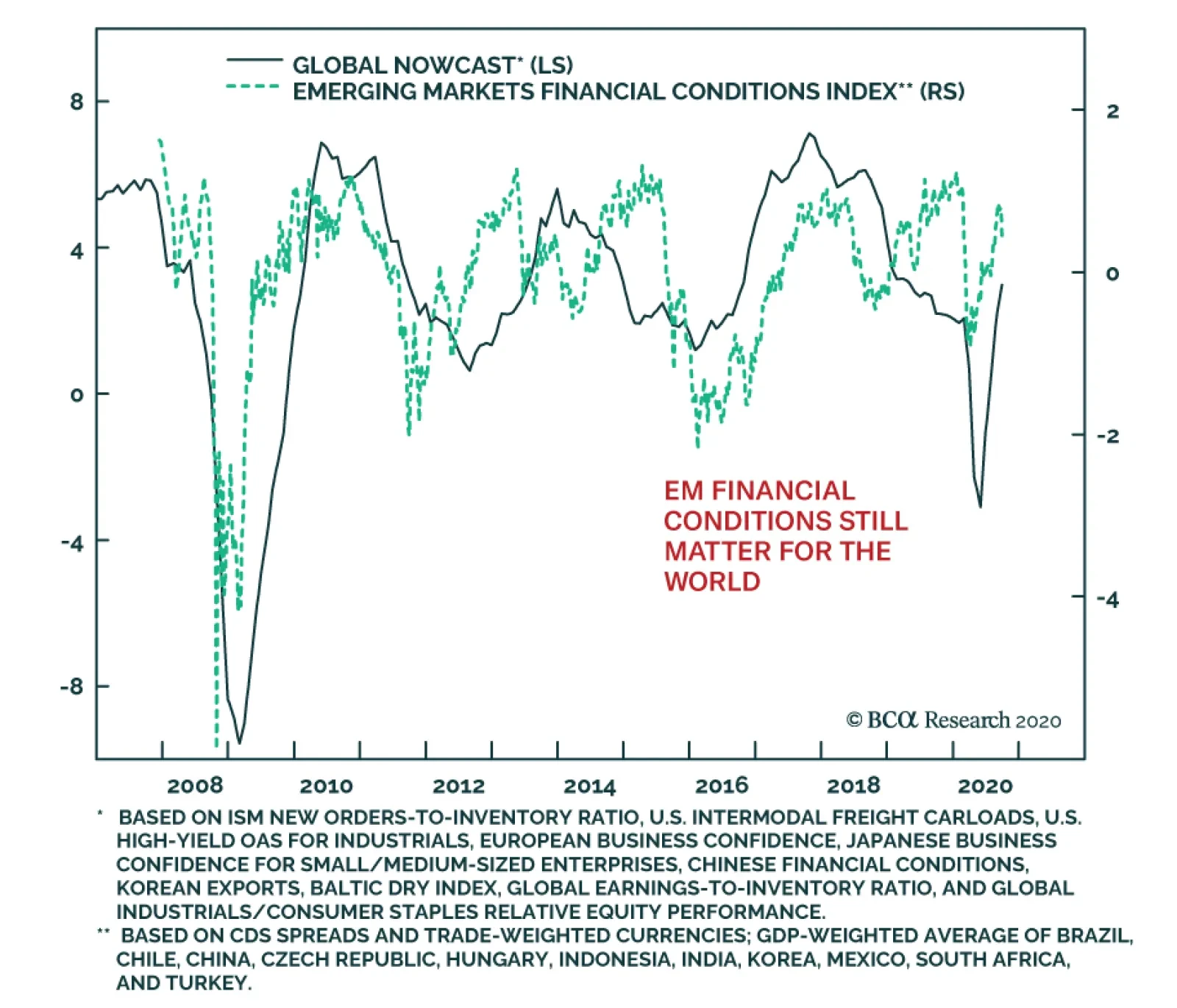

Emerging Markets

After easing for the last six months, EM financial conditions are deteriorating in response to the widening of spreads and the weakening of currencies highlighted in the Country Focus. While this deterioration in financial conditions is a reflection of the…

Highlights Near-Term Uncertainties: Investors have grown a bit more nervous in recent weeks, amid signs of a second wave of the coronavirus in Europe and with the contentious US presidential election only five weeks away. The pro-growth cyclical investment backdrop, however, remains unchanged. From a strategic perspective (6-12 months), maintain an overall neutral stance on interest rate duration, with a moderate overweight to global spread product versus government bonds while staying up in quality. EM USD-Denominated Debt: The main drivers of the emerging market hard currency debt rally since March – a weakening US dollar, improving global growth momentum, and massively accommodative global monetary policies – remain in place. Valuations, however, appear more attractive for EM USD-denominated corporates relative to USD-denominated sovereigns. Favor the former over the latter, within an overall neutral strategic allocation to EM hard currency debt. Feature Chart of the WeekMarkets Starting To Get Cautious

Markets Starting To Get Cautious

Markets Starting To Get Cautious

As the third quarter of 2020 draws to a close, investors have developed a slight case of the jitters about the near-term outlook for global financial markets. The positives that drove risk assets higher during the spring and summer - rebounding global economic activity, fueled by aggressive policy stimulus and a slowing of the spread of COVID-19, along with a weaker US dollar – have given way to some fresh uncertainties. Economic data releases have started to disappoint versus expectations, the rapid expansion of central bank balance sheets in the major developed economies has temporarily stalled, a second wave of new COVID-19 cases appears to have started in Europe and the US, and the US dollar has strengthened by 2.7% from the 2020 lows (Chart of the Week). Risk assets have pulled back in response, with the MSCI World equity index down -6.1% from the 2020 peak and US high-yield corporate credit spreads 66bps wider from recent lows. So far, these moves appear more a correction of overbought markets, rather than a change in trend. From the perspective of our strategic (6-12 months) investment recommendations, we remain generally positive on risk assets. Within global fixed income, that means maintaining a modest overall overweight stance on spread products versus government bonds, while focusing more on relative opportunities between countries and sectors to generate alpha. A Quick Assessment Of The Cyclical Backdrop The recent in increase in market volatility has started to shake out crowded positioning in popular winning trades. For example, high-flying US tech stocks have seen deeper pullbacks than the overall US equity market, while investors yanked nearly $5 billion from US junk bond funds in the week ending last Wednesday according to the Financial Times – the highest such outflow since the apex of the COVID-19 market rout in mid-March. We prefer to judge the health of a market rally by assessing the state of macroeconomic fundamentals underpinning that particular asset class Mainstream financial pundits often dub such corrections of overheated markets as a “healthy” way to ensure the continuation of medium-term bullish trends. We prefer to judge the health of a market rally by assessing the state of macroeconomic fundamentals underpinning that particular asset class – the most important of which remain positive for risk assets, in general, and global fixed income spread products, in particular. Economic Data Chart 2Economic Data Is Mostly Optimistic

Economic Data Is Mostly Optimistic

Economic Data Is Mostly Optimistic

While data surprise indices like the widely followed Citigroup series are topping out, this is more because of an improvement in beaten-up growth expectations, rather than a sharp decline in the actual data. The global ZEW economic expectations survey continues to point in an optimistic direction, while other reliable measures of business confidence like the German IFO and the US NFIB small business surveys have also continued to improve in recent months. Our own global leading economic indicator (LEI) is firming, with a majority of countries seeing a rising LEI (Chart 2). At the same time, the preliminary release of manufacturing PMI data for September showed continued improvements in the US and Europe. While the news is not 100% upbeat – the services PMI for the overall euro area fell -2.9 points in September, possibly due to the increase in new reported cases of COVID-19 in Europe – the tone of global economic data remains consistent with improving cyclical momentum. The US Dollar Chart 3Growth And Yield Differentials Signalling Dollar Weakness

Growth And Yield Differentials Signalling Dollar Weakness

Growth And Yield Differentials Signalling Dollar Weakness

The most likely medium-term path of least resistance for the US dollar remains downward. Economic growth remains stronger outside the US, based on the differential between the US and non-US manufacturing PMI data – an indicator that our currency strategists follow closely given its strong correlation to US dollar momentum (Chart 3). Relative interest rate differentials also remain less positive for the US dollar, with the decline in real US bond yields seen in 2020 pointing to additional medium-term dollar depreciation (bottom panel). US Politics The US general election is now only 35 days away, with the latest polling data showing President Trump closing the lead on the Democratic Party candidate, Joe Biden. Our colleagues at BCA Research Geopolitical Strategy remain of the view that a Biden victory is the more probable outcome, given the more difficult time Trump will have in winning all the key swing states that gave him his narrow election victory in 2016. Chart 4A "Blue Sweep" Is Bearish For Markets

A "Blue Sweep" Is Bearish For Markets

A "Blue Sweep" Is Bearish For Markets

The recent peak in US equity markets, and trough in the VIX index, coincided with improving odds of a Democratic Party sweep of the White House, House of Representatives and Senate (Chart 4). Such an outcome would give a President Biden the power, and perceived mandate, to implement many of the more progressive elements of the Democratic Party agenda – including a hike in corporate tax rates that could damage equity market sentiment. Our political strategists think that a “Blue Sweep” would only occur if the Republican Party fails to agree with the Democrats on a new fiscal stimulus bill.1 Both sides are playing hardball in the current negotiations, which is keeping investors on edge given how much of the US economy still requires fiscal support because of the pandemic. The Republicans will not want to take the blame for a failure to reach a stimulus deal, which would likely hand the Democrats the keys to the White House and Congress. Thus, a fiscal deal of sufficient size to calm jittery markets – most likely in the $2-2.5 trillion range sought by the Democrats – should be announced within the next couple of weeks before the final run up to the election. Financial/Monetary Conditions It will take more than a corrective pullback in equity and credit markets to threaten the economic recovery from the COVID-19 recession, given how highly stimulative financial conditions have become since the spring (Chart 5). In more normal times, booming equity and credit markets would eventually lead to upward pressure on government bond yields, since all would be reflecting improving economic growth and, eventually, expectations of faster inflation and tighter monetary policy. That move higher in yields would eventually act to restrain growth and depress the value of growth-sensitive risk assets. Chart 5Financial Conditions Remain Supportive For Growth

Financial Conditions Remain Supportive For Growth

Financial Conditions Remain Supportive For Growth

As we discussed in last week’s report, government bond yields are now likely to stay very low for a period measured in years, with major central banks like the US Federal Reserve leaning dovishly to support growth during the pandemic and trigger a temporary overshoot of inflation expectations.2 Thus, loose monetary settings (including more quantitative easing) will remain a critical underpinning for keeping risk assets well supported, by eliminating the typical cyclical threat from rising bond yields. Summing it all up, the fundamental economic and political backdrop remains cyclically bullish for risk assets, despite recent investor nervousness. Of course, a major wild card could be that the latest surge in new COVID-19 cases becomes large enough to trigger renewed economic restrictions in the US or Europe. Yet any such moves would likely not be as severe as those that occurred back in the spring, given the much lower mortality rates seen during the current upturn in COVID-19 cases, which is reducing the public’s willingness to accept more economy-crushing lockdowns. Bottom Line: Investors have grown a bit more nervous in recent weeks, amid signs of a second wave of the coronavirus in Europe and with the contentious US presidential election only five weeks away. The pro-growth cyclical investment backdrop, however, remains unchanged. From a strategic perspective (6-12 months), maintain an overall neutral stance on interest rate duration, with a moderate overweight to global spread product versus government bonds while staying up in quality. EM USD-Denominated Credit: Focus On Corporates Relative To Sovereigns Chart 6An Overview of USD-Denominated EM Debt

An Overview of USD-Denominated EM Debt

An Overview of USD-Denominated EM Debt

Back in July of this year, we turned more positive on emerging market (EM) USD-denominated spread product, upgrading our recommended allocation to both EM USD sovereign and corporate debt to neutral from underweight in our model bond portfolio.3 The change was motivated by signs of rebounding global economic growth after the COVID-19 lockdowns and a loss of upward momentum in the US dollar, coming at a time when EM spreads still looked relatively cheap (wide) compared to developed market corporate debt. An underweight stance was inconsistent with that backdrop. EM credit has done well since our upgrade (Chart 6). Using Bloomberg Barclays index data, the yield on the EM USD-denominated sovereign index has fallen from 5.2% to 4.4%, while the option-adjusted spread (OAS) on that same index tightened from 447bps to 368bps. It has been a similar story for EM USD-denominated corporates, with the index yield falling from 4.1% to 3.9% and the index OAS narrowing from 361bps to 344bps.4 Given the close correlations typically exhibited between EM USD sovereign and corporate yields and spreads, we have tended to change our recommended allocations to both asset classes at the same time and in the same direction. Yet the EM credit universe is quite diverse, incorporating many different issuers of highly varying credit quality and risk (Table 1). Treating the allocations to EM USD sovereign debt and USD corporate debt separately may reveal more profitable relative return opportunities. The fundamental economic and political backdrop remains cyclically bullish for risk assets, despite recent investor nervousness. Table 1Details Of The USD-Denominated EM Sovereign And EM Corporate & Quasi-Sovereign Indices

Stay The Course

Stay The Course

A first step to analyzing the EM USD sovereigns versus corporates investment decision is to develop a list of macro factors that correlate to the relative performance of EM sovereign and corporate credit. From there, we can build a list of directional indicators that can help inform that sovereign versus corporates decision. Treating the allocations to EM USD sovereign debt and USD corporate debt separately may reveal more profitable relative return opportunities. Our colleagues at BCA Research Emerging Markets Strategy have long held the view that overall EM debt performance is mostly driven by just two important macro factors: industrial commodity prices and the US dollar. Specifically, they have shown that the broad cyclical swings in EM sovereign and corporate spreads correlate strongly to the price momentum of a simple blend of industrial metal and oil prices, as well as the price momentum of a basket of EM currencies versus the US dollar (Chart 7). Chart 7EM Credit Spreads: A Commodity And Currency Story

EM Credit Spreads: A Commodity And Currency Story

EM Credit Spreads: A Commodity And Currency Story

On that basis, the recent moderate widening of EM credit spreads is justified by the corrective pullback in industrial commodity prices and a bit of US dollar strength – trends that our EM strategists believe can continue in the near-term. Although they share our view that the medium-term trend in the US dollar is still bearish, thus any near-term EM debt selloff will represent a longer-term buying opportunity.5 The demand for industrial commodities remains largely driven by economic trends in the world’s largest commodity consumer, China. Thus, our China credit impulse (the change in overall Chinese credit relative to GDP), which leads Chinese economic activity, is a good leading indicator of industrial commodity prices. We will use the China credit impulse in our list of directional indicators to forecast EM sovereign versus corporate performance. We also will include the annual rate of change of the index of EM currencies versus the US dollar (shown in Chart 7). We also believe that a global monetary policy variable should be included in our indicator list, particularly in the current environment of super-low developed market interest rates and central bank purchase of government bonds – both of which tend to drive yield-starved investors into higher-yielding EM assets and, potentially, can influence the relative performance of EM sovereigns and corporates. To capture the global monetary policy trend in our indicator list, we use the combined annual growth rate of the balance sheets of the Fed, the ECB, the Bank of Japan and the Bank of England. The message from our indicator list is that EM USD corporates should outperform EM USD sovereign debt over the next 6-12 months. In Charts 8 & 9, we show the relative total return of the Bloomberg Barclays EM USD corporate and USD sovereign indices, expressed in year-over-year percentage terms, versus our list of three potential directional indicators of the relative total return. We have broken up the overall EM universe by broad credit quality, with index data used for investment grade issuers in Chart 8 and below investment grade (high-yield) issuers in Chart 9. For all three of our directional indicators, we have pushed them forward in the charts to look for a potential leading relationship to the relative returns. Chart 8EM Investment Grade Corporates Looking Set to Outperform ...

EM Investment Grade Corporates Looking Set to Outperform ...

EM Investment Grade Corporates Looking Set to Outperform ...

Chart 9... But The High Yield Space Tells A More Mixed Story

... But The High Yield Space Tells A More Mixed Story

... But The High Yield Space Tells A More Mixed Story

The charts show that China credit impulse leads the relative total returns of EM USD corporates versus EM USD sovereigns by between 9-18 months for investment grade and high-yield EM credit. The growth of the major central bank balance sheets also leads the relative performance of EM USD corporates versus EM USD sovereigns by one full year, both for investment grade and high-yield EM credit. Finally, the annual growth of EM currencies leads the relative return of EM USD corporates versus sovereigns by around nine months, although the correlation is the weakest of the three indicators in our list. In terms of current investment strategy, the message from our indicator list is that EM USD corporates should outperform EM USD sovereign debt over the next 6-12 months, both for investment grade and high-yield, largely due to aggressive credit stimulus in China and the rapid expansion of central bank balance sheets. In terms of the attractiveness of EM USD-denominated yields in a global fixed income portfolio, however, there is a difference between higher-rated and lower-rated EM debt. In Chart 10, we present a scatter chart that plots the yields on various global fixed income sectors, all hedged into US dollars and compared to trailing yield volatility, versus the average credit rating of each sector. Investment grade EM USD corporate and sovereign issuers offer relatively more attractive yields compared to other sectors with similar credit ratings, like investment grade corporates in the US and Europe. The same cannot be said for high-yield EM USD corporates and sovereigns, which only offer a more attractive volatility-adjusted yield compared to euro area high-yield corporates among the lower-rated global credit sectors. Chart 10EM USD-Denominated High Yield Debt Not Especially Attractive On A Risk-Adjusted Basis

Stay The Course

Stay The Course

Based on this analysis, we are making the following changes in our model bond portfolio on page 14: Upgrading EM USD corporates to overweight Downgrading EM USD sovereigns to underweight Keeping the combined EM USD credit allocation at neutral. This fits with our current overall investment theme of keeping overall spread product exposure relative close to benchmark, while taking more active risks on relative allocations between fixed income sectors. Bottom Line: The main drivers of the emerging market hard currency debt rally since March – a weakening US dollar, improving global growth momentum, and massively accommodative global monetary policies – remain in place. Valuations, however, appear more attractive for EM USD-denominated corporates relative to USD-denominated sovereigns. Favor the former over the latter, within an overall neutral strategic allocation to EM hard currency debt. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 Please see BCA Research Geopolitical Strategy Weekly Report, "Stimulus Will Come … But May Not Save Trump", dated September 25, 2020, available at gps.bcaresearch.com. 2 Please see BCA Research Global Fixed Income Strategy Weekly Report, "What Would It Take To Get Bond Yields To Rise Again?", dated September 23, 2020, available at gfis.bcaresearch.com. 3 Please see BCA Global Fixed Income Strategy Weekly Report, "GFIS Model Bond Portfolio Q2/2020 Performance Review & Current Allocations: Selective Optimism", dated July 14, 2020, available at gfis.bcaraesearch.com. 4 Note that the index data we are using here includes both EM corporate and so-called “quasi-sovereign” debt, the latter being bonds issued by EM companies that are majority-owned by their local governments. 5 Please see BCA Emerging Markets Strategy Weekly Report, "A Reset In The Making", dated September 24, 2020, available at ems.bcaresearch.com. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Stay The Course

Stay The Course

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

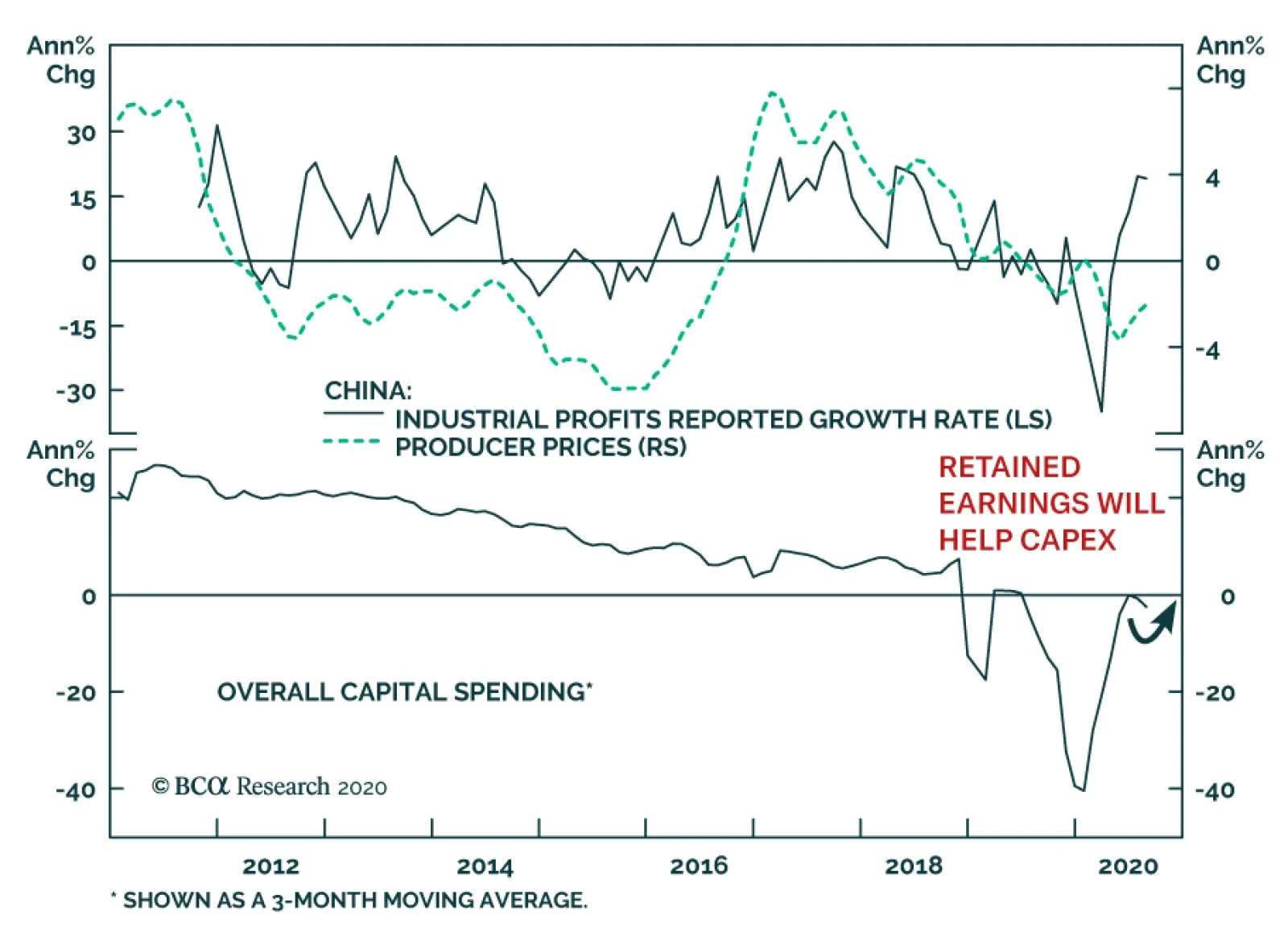

Chinese industrial profits hit the press last weekend. In August, they grew 19.1% annually, which represented the fourth straight month of profit growth. The continued industrial production rebound, the stabilization of PPI inflation, and the strengthening of…

Highlights Portfolio Strategy We recommend investors participate in the equity market rotation during the ongoing correction and position portfolios for next year’s bull market resumption by preferring unloved and undervalued deep cyclical laggards. Ultra-loose Chinese fiscal policy, rising global demand and firming domestic operating conditions, all signal that the S&P machinery recovery has legs. Vibrant emerging markets and a recuperating China, a softening US dollar rekindling the commodity complex, the nascent recovery in domestic conditions and washed out technicals, all suggest that a significant re-rating looms for severely neglected industrials equities. Recent Changes Our trailing stop got triggered and we downgraded the S&P internet retail index to neutral for a gain of 20% since the mid-April inception. This move also pushed our S&P consumer discretionary sector weighting to a benchmark allocation for a gain of 15% since inception. Table 1

Riot Point Looms

Riot Point Looms

Feature The S&P 500 broke below the important 50-day moving average last week, but managed to bounce off the early-June 3233 level – also a level where the SPX started the year – that could serve as temporary support (Chart 1). We first highlighted that investors were turning a blind eye to (geo)political risks on June 8, and failure to pass a new fiscal package before the election will continue to weigh on the economy and on stocks risking a further 10% drawdown near the SPX 3000 level. Chart 1Critical Support Levels

Riot Point Looms

Riot Point Looms

The Fed is now “out of the loop” i.e. a bystander on the sidelines, gently moving the foot off the accelerator as we illustrated last week. The FOMC’s, at the margin, less dovish monetary policy setting exerts enormous pressure on fiscal authorities to act as fiscal policy takes center stage. Our sense is that we have entered a Fiscal Policy Loop (FPL) where stalemate in Congress will cause a classic BCA riot point that in turn will force politicians’ hand to act in order to avoid a meltdown, and set in motion the next stage of the FPL (Figure 1). Keep in mind that the 2020s have ignited a paradigm shift from the Washington Consensus to the Buenos Aires Consensus1 and this is episode one of the FPL, more are sure to follow. Figure 1The Fiscal Policy Loop

Riot Point Looms

Riot Point Looms

It is no surprise that the Citi economic surprise index took off when the IRS started making direct payments to households in mid-April and leveled off toward the end of July when the stimulus money coffers ran dry (Chart 2). Chart 2In Dire Need Of Fiscal Stimulus

In Dire Need Of Fiscal Stimulus

In Dire Need Of Fiscal Stimulus

If Congress fails to pass a new fiscal package by October 16, the latest now that the Ruth Bader Ginsburg SCOTUS replacement seems to have become the number one priority, we doubt a fiscal package can pass during a contested election. Thus, realistically a fresh stimulus bill is likely only after the new president’s inauguration. Under such a backdrop, the economy will suffer a relapse despite households drawing down their replenished savings (middle panel, Chart 3). This is eerily reminiscent of the October 2008 and October 2018 fiscal policy and monetary policy mistakes, respectively, that resulted in a market riot. Similar to today, markets were down 10% and on a precipice and the policy errors pushed them off the cliff leading to another 10% gap down in a heartbeat. With regard to equity market specifics during the current FPL iteration, banks are most at risk as they are levered to the economic recovery, and commercial real estate ails remain a big headache. Absent a fiscal package bank executives will have to further provision for loan losses when they kick off Q3 earnings season in late-October as CEOs will err on the side of caution. Tack on the recent news on laundering money – including by US banks – and the Fed’s new stringent stress tests, and the risk/reward tradeoff remains poor for the banking sector (bottom panel, Chart 3). Odds are high that volatility will remain elevated heading into the election, therefore this phase represents an opportunity for investors to reshuffle portfolios and prepare for an eventual resumption of the bull market in early-2021. We continue to recommend investors avoid our “COVID-19 winners” basket and prefer our “back-to work” equity basket that we initiated on September 8. Similarly, this pullback is serving as a catalyst to shift some capital out of the fully valued tech titans and into other beaten down parts of the deep cyclical universe. Chart 3Show Me The Money

Show Me The Money

Show Me The Money

We doubt this correction is over as positioning in the NASDAQ 100 derivative markets is still lopsided; stale bulls are caught net long as NQ futures are deflating, thus a flush out looms (Chart 4). Chart 4Flush Out

Flush Out

Flush Out

The easy money has likely been made in the tech titans that near the peak on September 2, AAPL, MSFT and AMZN each commanded an almost $2tn market capitalization. Thus, booking some of these tech gains and redeploying capital in other unloved deep cyclical sectors would go a long way, especially if our thesis that the economic recovery will gain steam into 2021 pans out. Using a concrete rebalancing example to illustrate such a rotation is instructive.2 The tech titans’ (top 5 stocks) market cap weight in the SPX is 22%. Were an investor to take 10% of this weight or 220bps and redeploy it to the materials sector, which commands a 2.7% market cap weight in the SPX, would effectively double the exposure on this deep cyclical sector. The same would apply to the energy sector that comprises a mere 2.2% of the SPX, while industrials with an 8.4% market cap weight would get a sizable 26% lift (Chart 5). As a reminder our portfolio has an above benchmark allocation in all three deep cyclical sectors, and this week we reiterate our overweight stance on both the industrials sector and on a key subgroup. Chart 5Rotation Rotation Rotation

Rotation Rotation Rotation

Rotation Rotation Rotation

Buy The Machinery Breakout Were we not already overweight the S&P machinery index, would we upgrade today? The short answer is yes. Aggressive loosening in Chinese financial conditions have underpinned the economic recovery (second & third panels, Chart 6). Infrastructure projects are making a comeback and absorbing the slack in machinery demand caused by COVID-19. As a result, Chinese excavator sales have soared in the past quarter which bodes well for US machinery profit prospects (bottom panel, Chart 6). Beyond China, emerging markets demand for machinery equipment is robust as the commodity complex is recovering smartly (second panel Chart 7). The US dollar bear market is also bolstering global trade growth, despite the greenback’s recent technical bounce, and should continue to underpin machinery net export growth and therefore profit growth for US machinery manufacturers (third & bottom panels, Chart 7). Chart 6Enticing Chinese Backdrop

Enticing Chinese Backdrop

Enticing Chinese Backdrop

Chart 7Dollar The Great Reflator

Dollar The Great Reflator

Dollar The Great Reflator

The domestic machinery demand backdrop is also conducive to a renormalization of top line growth to a higher run-rate. The ISM manufacturing new orders sub-component is shooting the lights out, heralding a jump in machinery orders in the coming months (second panel, Chart 8). Simultaneously, a quick inventory check is revealing: both in the manufacturing and wholesale channels cupboards are bare which means that the risk of a liquidation phase in non-existent (third panel, Chart 8). Encouragingly, an inventory buildup phase is looming in order to satisfy firming demand. The tick up in machinery industrial production growth, the V-shaped recovery in the utilization rate and newly expanding backlog orders, all suggest that domestic demand conditions are on the mend (Chart 9). Tack on still prudent payrolls management that is keeping the machinery industry’s wage bill at bay (bottom panel, Chart 8), and a profit margin expansion phase is a high probability outcome. Chart 8What’s Not…

What’s Not…

What’s Not…

Chart 9…To Like

…To Like

…To Like

Our resurgent S&P machinery revenue growth model and climbing profit growth model do an excellent job in encapsulating all the industry’s moving parts and suggest that the path of least resistance is higher for relative share prices in the New Year (Chart 10). Finally, relative valuations have also recovered from the depth of the recession, but are only back to the neutral zone leaving enough room for a multiple expansion phase (Chart 11). Chart 10Models Say Buy

Models Say Buy

Models Say Buy

Chart 11Compelling Entry Point

Compelling Entry Point

Compelling Entry Point

In sum, ultra-loose Chinese fiscal policy, rising global demand and firming domestic operating conditions, all signal that the S&P machinery recovery has legs. Bottom Line: Stay overweight the S&P machinery index. The ticker symbols for the stocks in this index are: BLBG S5MACH– CAT, DE, PH, ITW, IR, CMI, PCAR, FTV, OTIS, SWK, DOV, XYL, WAB, IEX, SNA, PNR, FLS. Industrials Are Jumpstarting Their Engines We have been offside on the S&P industrials sector, but now is not the time to throw in the towel. In contrast we are doubling down on our overweight stance as the ongoing rotation should see some tech sector outflows find their way to under-owned capital goods producers. Industrials equities have been on the selling block and suffered a wholesale liquidation during the dark days of the COVID-19 pandemic, and have yet to regain their footing (top panel, Chart 12). The GE and Boeing sagas have dealt a big blow to this deep cyclical sector, but now this market cap weighted sector has filtered these stocks out as neither of these “fallen angels” is occupying a spot in the top 5 weight ranks. Relative valuations are washed out, and relative technicals are still deep in oversold territory (second & third panels Chart 12). Sell-side analysts are the most pessimistic they have been on record with regard to the long-term EPS growth rate that is penciled in to trail the broad market by almost 800bps (bottom panel, Chart 12)! All this bearishness is contrarily positive as a little bit of good news can go a long way. Already, relative EPS breadth is stealthily coming back, and net earnings revisions are rocketing higher (Chart 13). Chart 12Liquidation Phase…

Liquidation Phase…

Liquidation Phase…

Chart 13…Is Over

…Is Over

…Is Over

One reason behind this optimism rests with the domestic recovery. Capex intentions are firming and CEO confidence is upbeat for the coming six months. The ISM manufacturing new orders-to-inventories ratio is corroborating the budding recovery in the soft data. Green shoots are also evident in hard data releases. Durable goods orders are on the verge of expanding anew (Chart 14). Emerging markets (EM) and China represent another source of industrials sector buoyancy. The EM manufacturing PMI clocking in at 52.5 hit an all-time high. China’s PMIs are also on a similar trajectory, and the Chinese Citi economic surprise index has swung a whopping 300 points from -240 to above +60 over the past six months. The upshot is that US industrials stocks should outperform when China and the EM are vibrant (Chart 15). Chart 14Domestic And …

Domestic And …

Domestic And …

Chart 15… EM Green Shoots Are Bullish

… EM Green Shoots Are Bullish

… EM Green Shoots Are Bullish

Peering over to the currency market, the debasing of the US dollar should also underpin industrials stocks via the export relief valve (third panel, Chart 16). A depreciating greenback also lifts the commodity complex and hence industrials equities that are levered to the extraction of commodities and other derivative activities (top panel, Chart 16). Historically, an appreciating USD has been synonymous with a multiple contraction phase and vice versa. Looking ahead, the industrials sector relative 12-month forward P/E multiple should continue to expand smartly (bottom panel, Chart 16). The US Equity Strategy’s macro based EPS growth model captures all the different earnings drivers and signals that an earnings-led recovery is in the offing (Chart 17). Chart 16The Greenback Holds The Key

The Greenback Holds The Key

The Greenback Holds The Key

Chart 17Models Flashing Green

Models Flashing Green

Models Flashing Green

Adding it all up, vibrant emerging markets and a recuperating China, a softening US dollar rekindling the commodity complex, the nascent recovery in domestic conditions and washed out technicals, all suggest that a significant re-rating looms for severely neglected industrials equities. Bottom Line: We continue to recommend an above benchmark allocation in the S&P industrials sector. Anastasios Avgeriou US Equity Strategist anastasios@bcaresearch.com Footnotes 1 The Washington Consensus – a catchall term for fiscal prudence, laissez-faire economics, free trade, and unfettered capital flows – is being replaced by economic populism, by a Buenos Aires Consensus. Buenos Aires Consensus is our catchall term for everything that is opposite of the Washington Consensus: less globalization, fiscal stimulus as far as the eyes can see, erosion of central bank independence, and a dirigiste (as opposed to laissez-faire) approach to economics that seeks to protect “state champions,” stifles innovation, and ultimately curbs productivity growth. 2 Our example assumes benchmark allocation in all sectors for illustrative purposes. Current Recommendations Current Trades Strategic (10-Year) Trade Recommendations

Drilling Deeper Into Earnings

Drilling Deeper Into Earnings

Size And Style Views July 27, 2020 Overweight cyclicals over defensives April 28, 2020 Stay neutral large over small caps June 11, 2018 Long the BCA Millennial basket The ticker symbols are: (AAPL, AMZN, UBER, HD, LEN, MSFT, NFLX, SPOT, TSLA, V). January 22, 2018 Favor value over growth

Highlights Senate Republicans would be suicidal not to agree to a fiscal relief bill before the election. Democrats are still offering a $2.2 trillion package. Grassroots Republican voters will forgive Republicans for blowing out the budget deficit but they will never forgive them for throwing away control of the White House and Senate. Nevertheless financial markets face more downside until a deal is reached. We are booking gains on several of our tactical risk-off trades but will hold our strategic risk-on trades, as we are still constructive over a 12-month period. Turkey is stepping back from its foreign adventurism in the face of constraints. Our GeoRisk Indicator for Turkey has rolled over. Feature Financial markets continue to sell off in the face of a range of risks, including new threats of COVID-19 restrictions in Europe, an increase in daily new cases of the disease in the United States (Chart 1), and the US Congress’s problems passing a new round of fiscal relief. Chart 1Increase In COVID-19 Cases Among Factors Weighing On Markets

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Chart 2Congress Will Pass Stimulus ~$2-$2.5 Trillion

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Since May, when the Democrats passed the $3.4 trillion HEROES Act, we have maintained that “stimulus hiccups” would roil the market. However, we also argued that Congress would eventually pass a new package – probably in the range of $2-$2.5 trillion (Chart 2).1 The latter part of this view remains to be seen and has come under pressure from investors who fear that Congress could fail to produce a bill entirely. We are sticking with our guns. GOP senators will recognize that they face sweeping election losses; House Democrats will not be able to reverse course and deprive households of badly needed assistance. However, stock investors might sell more between now and the final deal, which must be done by around October 9 so that lawmakers can go back to their home states to campaign for the November 3 election. Moreover the fiscal deal might not come in time to save the Republicans’ re-election bid in the White House and Senate, which raises further downside risk due to the Democratic agenda of re-regulation and tax hikes. And the election’s aftershocks could also be market-negative. For example, President Trump could also escalate the conflict with China, whether as the “comeback kid” or as a lame duck. Therefore this week we are booking some gains. We will not recommend a tactical risk-on position until our fiscal view is confirmed and we can reassess. US Fiscal Stimulus Is Coming Chart 3Republicans Highly Unlikely To Win House Of Representatives

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Why would Democrats agree to a stimulus bill given that it could help President Trump and the Republicans get re-elected? Democrats are afraid to deprive households of relief amid a crisis merely to spite the president and score election points. Around 28-43 of Democrats in the House of Representatives face re-election in districts that are competitive or could become competitive. Republicans need a net gain of 20 seats to retake the House (Chart 3). If Democrats offer to cooperate yet Republican senators balk, then the latter will take the blame for any failed deal and ensuing financial turmoil. The experience of other fiscal cliffs bears this out. The debt ceiling crises of 2011 and 2013 and the government shutdowns of 2013 and 2018-19 all suggest that net presidential and congressional approval ratings suffer when partisanship prevents compromise on major fiscal issues (Charts 4A and 4B). This is a risk for the ruling GOP. All Democrats have to do is remain open to compromise. Net presidential and congressional approval ratings suffer when partisanship prevents compromise on major fiscal issues – a risk for the ruling GOP. Chart 4AFiscal Failures Pose A Risk To Ruling GOP

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Chart 4BFiscal Failures Pose A Risk To Ruling GOP

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Confirming this reasoning, Democrats joined with Republicans this week to pass a continuing resolution to maintain government spending levels through December 11, thus avoiding a government shutdown. Clearly the two parties can still cooperate despite record levels of partisanship. House Speaker Nancy Pelosi ruled out using government shutdown as a weapon to hurt the Republicans, fearing it would backfire. And just last week vulnerable House members pressured Pelosi into stating that the House will remain in session in October until a fiscal relief bill is passed. Democrats remain committed to their current plan – solidifying their grip on the House and demonstrating that they can govern, and that government can do more for households, by passing bills. This is still the strategy even if the risk is that these bills give Trump a marginal benefit. The Democratic demand is for a very large fiscal package – House Speaker Nancy Pelosi is today offering $2.2 trillion, a compromise from the initial $3.4 trillion bill (Table 1). A smaller bill is harder to negotiate because it would cut the House Democrats’ spending priorities for their constituents, including around $1 trillion in state and local government aid, while still giving Trump a bounce in opinion polls for boosting pandemic relief. This is unacceptable – and this is how a policy mistake could happen. Table 1What A Fiscal Compromise Will Look Like

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Chart 5Senate Republicans Face A Hotly Contested Election

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Chart 6Republican Senators' Hung Up On Future Deficit Concerns

Republican Senators' Hung Up On Future Deficit Concerns

Republican Senators' Hung Up On Future Deficit Concerns

Senate Republicans face a hotly contested election – with 23 of them up for re-election versus only 12 Democrats. However, 30 of them are not up for re-election this year (Chart 5). These senators fear the eventual return of deficit concerns among the Republican base so they are bargaining to limit emergency spending (Chart 6). Until they can be cajoled by their fellow senators and the White House, they pose a risk to the passage of new stimulus. But this risk is overrated. Ultimately Senate Majority Leader Mitch McConnell and the Senate Republicans will capitulate. It is political suicide if they do not. The GOP will lose control of the Senate and the White House if premature fiscal tightening sparks a bloody September-October selloff just ahead of the election (Charts 7Aand 7B). Chart 7AStocks Sell, Bonds Rally … When Congress Goes Off Fiscal Cliff

Stocks Sell, Bonds Rally... When Congress Goes Off Fiscal Cliff

Stocks Sell, Bonds Rally... When Congress Goes Off Fiscal Cliff

Chart 7BStocks Sell, Bonds Rally … When Congress Goes Off Fiscal Cliff

Stocks Sell, Bonds Rally... When Congress Goes Off Fiscal Cliff

Stocks Sell, Bonds Rally... When Congress Goes Off Fiscal Cliff

Chart 8Trump Compares Poorly To Other Presidents Re-Elected Amid Recession

Trump Compares Poorly To Other Presidents Re-Elected Amid Recession

Trump Compares Poorly To Other Presidents Re-Elected Amid Recession

Only three out of six presidents in modern times have been re-elected when a recession struck during the election year yet ended prior to the fall campaign. These were William McKinley in 1900, Teddy Roosevelt in 1904, and Calvin Coolidge in 1924.2 Trump faces the same scenario, but financial markets are signaling that Trump is not faring as well as these three predecessors (Chart 8). The Senate races are all on a knife’s edge (Chart 9). American politics are highly nationalized – partisan identification overrides regional concerns. President Trump has also personalized his political party, making the election a referendum on himself (Chart 10). These trends suggest the Senate will fall to the party that wins the White House. Chart 9The Senate Races Are All On A Knife’s Edge

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Consumer confidence is weak and bodes ill for the incumbent president and party (Chart 11). Chart 10Trump Has Personalized Partisan Politics

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Chart 11Consumer Confidence Bodes Ill For Trump And GOP

Consumer Confidence Bodes Ill For Trump And GOP

Consumer Confidence Bodes Ill For Trump And GOP

A failure to provide stimulus will ensure that sentiment worsens for the rest of the campaign and overshadows some underlying material improvements that are the Republicans’ only saving grace. Wage growth is recovering in line with the V-shape recovery in blue and purple states, including purple states that voted for Trump (Chart 12). The manufacturing rebound – and a surge in loans – is creating the conditions for the “Blue Wall” of Pennsylvania, Michigan, and Wisconsin to re-elect President Trump (Chart 13). A fiscal failure will blot out this positive news. Chart 12Fiscal Failure Would Blot Out Economic Improvements

Fiscal Failure Would Blot Out Economic Improvements

Fiscal Failure Would Blot Out Economic Improvements

Chart 13Blue Wall' Could Re-Elect Trump On Economic Improvement

Blue Wall' Could Re-Elect Trump On Economic Improvement

Blue Wall' Could Re-Elect Trump On Economic Improvement

Republicans’ standing offer is for a $1.3 trillion bill. The bipartisan “Problem Solver’s Caucus” has separately proposed a $1.5 trillion package that could be converted. McConnell has shown he can muster his troops by producing 52 Republican votes on a skinny relief bill on September 10. The Senate will go on recess on Friday, October 9 and the House is committed to staying until a bill is done. Negotiations cannot drag on much longer than that, however, because lawmakers need to go back to their home states and districts to campaign for the election. The equity selloff suggests policymakers will need to respond sooner anyway. Is there a way for Trump to bypass Congress and provide stimulus unilaterally? Chart 14Gridlock In 2020-22 Is Possible Under Trump Or Biden

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Trump is only too happy to run against a “do-nothing Congress,” which is how Harry Truman pulled off his surprise victory in 1948. He could use executive orders to redirect federal funds that have already been appropriated. However, he has already provided stimulus by decree – delaying payroll tax collections and calling on states to provide unemployment insurance – and yet the market has sold off anyway. That is because these measures are half-baked – they lack the size and the force of an act of Congress. They require coordination with states and firms, which face uncertainty over the legality of the measures and have little incentive to make sacrifices for an administration that may not last more than a few months. In short, if Trump tries to stimulate by decree, it is an election gimmick that will not satisfy market participants who need to look beyond the next 39 days to the critical question of whether US fiscal authorities understand the needs of the economy and can coordinate effectively. Congressional failure will cast a pall over the outlook given that there is still a fair chance the election could produce gridlock for the 2020-22 period, under Trump or Biden (Chart 14). Bottom Line: Financial markets face more downside until Senate Republicans capitulate to Pelosi’s demand of a bill around $2-$2.5 trillion. We think they will, but that is not an argument for getting long now – Republicans could capitulate too late to save the market from a deeper selloff. Investors should book profits now and buy when the deal is clinched. What About The Supreme Court? The Supreme Court battle over the death of Justice Ruth Bader Ginsburg may increase the risk of miscalculation in the stimulus negotiations, but not by much. Subjectively we would upgrade that risk from 25% to 33%. Republicans will fill the vacant seat before the election. So far they have the votes – even if Senator Mitt Romney changes his mind, there is still a one-seat buffer. However, a win on the high court has a mixed impact on financial markets. It may increase the odds of a Democratic Party sweep, which is initially a net negative for equities. But House Democrats will become less inclined to compromise on the size of the fiscal bill that we expect. They will say “take it or leave it” on the $2.2 trillion offer. The lowest we can see Democrats passing is $1.9 trillion. If the GOP fails to budge, the equity selloff will be aggravated by the implication that Democrats will win a clean sweep and thus gain the power to raise corporate and capital gains taxes next year. We have put 55%-60% odds on a clean sweep, but the market stands at 49%, so there is room for the market to adjust (Chart 15). As for the Supreme Court itself, a Republican nomination is legitimate regardless of the election timing, though the decision to go forward this close to the election reveals extreme levels of polarization. The Republican pick could energize the Democrats in the election, as occurred with the nomination of Justice Brett Kavanaugh just ahead of the 2018 midterms. A Democratic overreaction could mobilize conservatives, but this will be moot if the stock market collapses. If the presidential election is contested or disputed, Trump’s court nominee pick could cast the decisive vote, although, once nominated, a justice may not rule in accordance with his or her nominator’s wishes. The Supreme Court battle raises the risk of stimulus miscalculation to 33%. In a period of “peak polarization,” one should expect the Supreme Court battle to escalate further from here (Chart 16). Democrats are likely to remove the filibuster if they win the Senate. This would theoretically enable them to create four new seats on the court, which they could then fill with liberal judges. Franklin Roosevelt attempted to pack the court in 1937 when it got in the way of the New Deal and his plan only narrowly failed due to the unexpected death of a key ally in the Senate. Chart 15A Democratic Sweep Would Aggravate The Equity Selloff

A Democratic Sweep Would Aggravate The Equity Selloff

A Democratic Sweep Would Aggravate The Equity Selloff

Chart 16Supreme Court Battle Will Escalate Amid Extreme Polarization

Supreme Court Battle Will Escalate Amid Extreme Polarization

Supreme Court Battle Will Escalate Amid Extreme Polarization

Not only might the court decide the election outcome, but future controversial legislation could live or die by the court’s vote, as occurred with Obamacare in 2012 (Chart 17). In the event that Democrats achieve a clean sweep, the conservative court will be their only obstacle and they will possess the means to remove it. Chart 17Supreme Court Battle Will Prove Market Relevant In Event Of Democratic Sweep

Supreme Court Battle Will Prove Market Relevant In Event Of Democratic Sweep

Supreme Court Battle Will Prove Market Relevant In Event Of Democratic Sweep

Bottom Line: Earlier we saw a 25% chance that stimulus would fail – now we give it a 33% chance. However, the size of the stimulus is now even more likely to fall within the $2-$2.5 trillion range we have signaled in previous reports. The Supreme Court will become a major factor in domestic economic policy uncertainty if Democrats win a clean sweep of government. Turkey Hits Constraints In East Med – For Now … Turkish President Recep Tayyip Erdogan’s foreign policy assertiveness has once again put Turkey in conflict with NATO allies. Tensions escalated last month after Greece signed a maritime boundary deal with Egypt that Athens said nullified last November’s Libya-Turkey agreement (Map 1). Map 1Turkey Testing Maritime Borders In the East Med

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

In response, Turkey issued a navigational warning (which was renewed thrice) and dispatched its seismic research vessel, the Oruc Reis, to explore for hydrocarbons in disputed areas of the Eastern Mediterranean between Greece and Cyprus. In shows of force, Turkey and Greece both deployed their navies to the area last month, raising the risk of an armed confrontation.3 The motivation for Erdogan’s hard power tactics is multi-pronged. Chart 18Erdogan’s Foreign Adventurism Reflects Domestic Weakness

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

On a domestic level, Erdogan’s East Med excursions are an attempt to rally domestic support, where he and his party have lost ground (Chart 18). Given that popular opinion in Turkey indicates that the majority see the self-declared Turkish Republic of Northern Cyprus as a “kin country” and that they do not expect Turkey to be accepted into the EU, Ankara’s East Med strategy is likely to find support. On an international level, Turkey is flexing its muscles against the West. Erdogan has inserted Turkish forces into conflicts in Syria and Libya, confronting NATO allies there, and authorized the provocative purchase of the Russian S400 missile defense system at the expense of membership in the US F-35 program. The East Med gambit is another challenge to the West by testing EU unity. Specifically Erdogan is demonstrating that Turkey is willing to use military force to reject any unilateral attempts by foreign powers to impose maritime borders on Turkey – for instance through the EU’s Seville map.4 By demonstrating maritime strength, Turkey hopes to twist the EU’s arm into agreeing to a more favorable maritime partition plan in the East Med. As such the conflict is part of Turkey’s “Blue Homeland” strategy to expand its sphere of influence and secure energy supplies.5 Turkey is extremely vulnerable as a geopolitical actor because it depends on imports for three-quarters of its energy needs.6 With energy accounting for 20% of its import bill, these imports are weighing on the current account balance (Chart 19). Turkey’s exclusion from regional gas agreements has thus been a blow to its self-sufficiency goals. Meanwhile Greece, Italy, Egypt, Israel, Cyprus, and Jordan have recently formalized their cooperation through the Cairo-based East Mediterranean Gas Organization. Turkish agitation in the East Mediterranean is an attempt to prevent others from exploiting gas resources there so long as its demands remain unmet. Erdogan’s retreat demonstrates Turkey’s constraints in its challenge to the EU. While the EU has yet to impose sanctions or penalties, Erdogan has now backtracked. Oruc Reis returned to Antalya on September 13, despite official statements that it would continue its mission. Turkish and Greek military officials have been meeting at NATO headquarters. And following talks with French President Emmanuel Macron, German Chancellor Angela Merkel, and EU President Charles Michel, Erdogan’s office announced on September 22 that Turkey and Greece were prepared to resume talks. The postponement of the European Council’s special meeting to discuss Turkish sanctions to October 1-2 plays to Turkey’s favor by giving more time for talks. Chart 19Turkey's Energy Dependence A Geopolitical Vulnerability

Turkey's Energy Dependence A Geopolitical Vulnerability

Turkey's Energy Dependence A Geopolitical Vulnerability

Erdogan’s retreat demonstrates Turkey’s constraints in its challenge to the EU. The possibility of damaging sanctions was too much at a time of economic vulnerability. Given Turkey’s dependence on the EU for export earnings and FDI inflows, the impact of sanctions on Turkey’s economy cannot be overstated (Chart 20). Chart 20EU Sanctions Could Destroy Turkey's Economy

EU Sanctions Could Destroy Turkey's Economy

EU Sanctions Could Destroy Turkey's Economy

Turkey is also facing constraints diplomatically as two of its regional rivals – the United Arab Emirates (UAE) and Israel – have agreed to normalize relations and strengthen ties under the US-mediated Abraham Accords (Table 2). The UAE already dispatched F-16s to Crete to participate in joint training exercises in a show of support to Greece. Table 2The Abraham Accords Unify Turkey’s Regional Rivals

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Details about the potential sanctions have not been released. However, EU Minister of Foreign Affairs Josep Borrell has indicated that penalties could be levied not only on individuals, but also on assets, ships, and Turkish access to European ports and supplies. This could include banks financing energy exploration or even entire business sectors, such as the energy industry. Moreover, the EU could play other damaging cards such as halting EU accession talks, or limiting its customs union with Turkey, which Ankara hopes to modernize. Chart 21EU Needs Turkey’s Cooperation To Stem Flow Of Migrants

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

Stimulus Will Come … But May Not Save Trump (GeoRisk Update)

It is also in Europe’s interest to de-escalate the conflict. Sanctions on Turkey could accelerate Ankara’s re-orientation towards Russia and possibly China, expediting its transition to a hostile regional actor. In addition, Turkey has not shied away from using the 2016 migration deal, whereby Turkey has become the gatekeeper of Middle Eastern migrants fleeing to Europe, as a bargaining chip (Chart 21). Foreign Minister Mevlut Cavusoglu outright stated that Turkey will respond to EU sanctions by reneging on the deal, which could result in an influx of refugees into the EU and new challenges for Europe’s political establishment. Erdogan’s retreat is also likely a response to pressure from Washington. Secretary of State Mike Pompeo lent some support to Greece and Cyprus during his September 12 visit to Cyprus. While the US has distanced itself from recent developments in the East Med, leaving German Chancellor Angela Merkel to play the role of mediator, a deterioration in Ankara’s relations with NATO allies could accelerate Turkey’s de-coupling from the West. Some within Washington are already calling for a relocation of the US strategic Incirlik air base to Greek islands. Erdogan’s retreat from a hawkish stance is in line with similar behavior elsewhere. For instance, despite having taken delivery of all parts and completed all necessary tests, Turkey has yet to activate its Russian S-400 missile defense system. It is wary of US sanctions. Similarly, Ankara has paused its Libyan offensive toward the eastern oil crescent in face of the risk of an outright military confrontation with Egypt. In each case, Erdogan appears to be at least temporarily recognizing the limits to his foreign adventurism. Nevertheless, the recent de-escalation does not mark the end of the conflict. Rather it demonstrates that both sides have hit constraints and are pausing for a breather. Chart 22Erdogan's Tactical Retreat Will Pull Down Turkish Risk

Erdogan's Tactical Retreat Will Pull Down Turkish Risk

Erdogan's Tactical Retreat Will Pull Down Turkish Risk

The tactical retreat will provide some relief for the lira, which hit all-time lows against the dollar and euro, and thus pull down our Turkey GeoRisk indicator (Chart 22). But it does not guarantee that the Turkish risk premium will stay low. Talks between Greece and Turkey are unlikely to result in substantial breakthroughs. Instead the conflict will resurface – perhaps when Turkey is in a stronger economic position at home and the EU is distracted elsewhere, whether with internal political issues or conflicts with Russia, the UK, or any second-term Trump administration. Bottom Line: The recent de-escalation of East Med tensions does not mark the end of a bull market in Turkey-EU tensions. These tensions arise from geopolitical multipolarity – Turkey’s ability to act independently in foreign policy without facing an overwhelming, unified US-EU response. However, Turkey’s vulnerability to European economic sanctions shows that it faces real constraints. A major attempt to flout these constraints is a sell signal for the lira, as European sanctions could then become a reality. We remain negative on the lira, but will book gains on our short trade. Investment Takeaways We are booking gains on some of our tactical risk-off trades, given that we ultimately expect the US Congress to approve a new fiscal package. We are closing our long VIX December 2020 / short VIX January 2021 trade, which captured concerns about a contested election in the United States, for a gain of 4%. Volatility will still rise and a contested election is still possible, but the fiscal risk has gone up, COVID-19 cases have gone up, and Trump’s polling comeback has softened. The 4% gain does not include leverage or contract size. We were paid to put on the trade and now will be paid to exit it, so we are booking gains (Chart 23). Chart 23Book Gains On Bet On Near Term Volatility

Book Gains On Bet On Near Term Volatility

Book Gains On Bet On Near Term Volatility

We are closing our short “EM Strongman Basket” of Turkish, Brazilian, and Philippine currencies for a gain of 4.5%. The trade has performed well but Turkey is not only recognizing its constraints abroad but also recognizing constraints at home by raising interest rates to defend the lira. In Brazil, Jair Bolsonaro’s approval rating has surged and our GeoRisk indicator has topped out. The latest readings on our GeoRisk Indicators provide confirmation of our major themes, views, and trades. The charts of each country’s indicator can be found in the Appendix. Short China, Long China Plays: Geopolitical risk continues on the uptrend that began with Xi Jinping’s consolidation of power and has not abated with the Phase One trade deal. Policymakers will remain entirely accommodative on fiscal and quasi-fiscal (credit) policy in the wake of this year’s recession. New financial regulations do not herald a return of the deleveraging campaign in any way comparable to 2017-18. The October Politburo meeting on the economy could conceivably sound a hawkish note, which could conveniently undermine sentiment ahead of the US election, but if this occurs then we would not expect follow-through. China plays and commodity plays should benefit, such as the Australian dollar, iron ore prices, and Brazilian and Swedish equities. Yet we remain short the renminbi, which has recently flagged after a fierce rally. Trump is negative for the RMB and Biden will ultimately be tough on China, contrary to the market consensus. Short Taiwan: US-China strategic relations have collapsed over the course of the year but financial markets have ignored it due to COVID-19 and stimulus. The only thing keeping US-China relations on an even keel is the Trump-Xi gentleman’s agreement, which expires on November 3 regardless of the election outcome. While outright military conflict over Taiwan cannot be ruled out, Beijing is much more likely to impose economic sanctions prior to any attempt to take the island by force. This has been our base case since 2016. Our GeoRisk indicator is just starting to price this risk so it remains highly underrated from the perspective of the Taiwanese dollar and equities. We are short and there is still time to put on shorts. Long South Korea: The rise in Korean geopolitical risk since the faltering of US-North Korean diplomacy in 2019 has peaked and fallen back, as expected. Pyongyang has not substantively tested President Trump during the election year and we still do not think he will – though a showdown would mark an October surprise that could boost Trump’s approval rating. South Korean political risk should continue falling and we are long Korean equities. Short Russia: Russian geopolitical risk has exploded upward, as we expected. We have been bearish on the Russian ruble and local currency bonds, though we should note that this differs from our Emerging Markets Strategy view based on macro fundamentals. Our reasoning predates the escalation of tensions with the EU over Belarus, but Belarus highlights the negative dynamic: Vladimir Putin in his fourth term is concerned about domestic social and political stability, and this concern is especially heightened after the global pandemic and recession. Therefore he has little ability to tolerate unrest in the former Soviet sphere. Moreover, he has a window of opportunity when the US administration is distracted, and not unfriendly, whereas that will change if the Democrats take over. If Democrats win, they will not try another diplomatic “reset” with Russia; they believe engagement has failed and want revenge for Putin’s undermining the Obama administration and 2016 election interference. The Nordstream 2 pipeline and Russian local currency bonds are at risk of new sanctions. The Democrats will also increase their efforts at cyber warfare and psychological warfare to counter Russia’s use of such measures. If Trump wins, the upside for Russia is limited as Trump’s personal preferences have repeatedly lost to the US political and military establishment when it comes to Russia. The US has remained vigilant against Russian threats and has increased support for countering Russia in eastern Europe and Ukraine. Chart 24Russia Is At Risk of US Sanctions

Russia Is At Risk of US Sanctions

Russia Is At Risk of US Sanctions

In Belarus, President Lukashenko has been sworn in as president again, and he will not step down unless Russia and its allies orchestrate a replacement who is friendly toward Russian interests. Russia will not allow a pro-EU, pro-NATO government by any stretch of the imagination. The likeliest outcome is that Russia demonstrates its security and military superiority in a limited way, while the US and Europe respond with sanctions but not with military force. There is no appetite for the US or EU to engage in hot war with Russia over Belarus, which they have little hope of re-engineering in the Western image. We are short Russian currency and local bonds on the risk of sanctions stemming from either the US election cycle or the Belarus confrontation or both. We note that local currency bonds are not pricing in the risks that our geopolitical risk indicators are pricing (Chart 24). Long Europe: Our European geopolitical risk indicators show that the EU remains a haven of political stability in an unstable time. European integration is accelerating in the context of security threats from Russia, the potential for sustained economic conflict with the US (if Trump is re-elected), and economic competition with an increasingly authoritarian and mercantilist China. Europe’s latent strengths, when acting in unison, are brought out by the report on Turkey above. However, the 35% chance that the UK fails to reach a trade deal at the end of this year will still push our European risk indicators up in the near term. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Roukaya Ibrahim Editor/Strategist Geopolitical Strategy RoukayaI@bcaresearch.com We Read (And Liked) … Geopolitical Alpha: An Investment Framework For Predicting The Future What better way to revive the hallowed tradition of BCA Geopolitical Strategy book reviews than to give clients a sneak preview of our founder Marko Papic’s literary debut, Geopolitical Alpha: An Investment Framework for Predicting the Future?7 Long-time readers will know much of this book – it is the distillation of a decade of Marko’s work at BCA Research and, more recently, Clocktower Group. Here is the story of European integration – perhaps Marko’s greatest call, from back in 2011. Here is the story of multipolarity and investing. Here is the apex of globalization. Here is the decline of laissez-faire and the rise of dirigisme. Here is the end of Chimerica. Attendees of the BCA Research Academy will also recognize much in Marko’s formal exposition of his method. The categories of material constraints that bind policymakers. The practical application of the median voter theorem. The psychological lessons from Richards Heuer and Lee Ross. The occasional dash of game theory – and the workingman’s critique of it. The core teaching is the same: “Preferences are optional and subject to constraints, whereas constraints are neither optional nor subject to preferences.” There is also much that is new, notably Marko’s analysis of the COVID-19 pandemic, which is bound to generate controversy for classifying the whole episode as an example of mass hysteria comparable to the Salem witch trials, but which is as well-researched and well-argued as any section in the book. I was fortunate to learn the geopolitical method with Marko under the guidance of George Friedman, Peter Zeihan, Roger Baker, Fred Burton, Scott Stewart, and other colleagues at Stratfor (Strategic Forecasting, Inc.) in Austin, Texas from the era of the Iraq troop surge, the Russian invasion of Georgia, and the Lehman Brothers collapse. We both owe a lot to these teachers: the history of geopolitics, intelligence analysis, open source monitoring, net assessments, and, of course, forecasting. What Marko did was to take this armory of geopolitical analysis – which we both can testify is best taught in practice, not universities – and to put it to use in the financial context, where political analysis was long treated as optional and anecdotal despite the manifest and growing need for a rigorous framework. A hard-nosed analyst will never cease to be amazed by the gaps that emerge between the consensus view on Wall Street and a careful, disciplined net assessment of a nation or political movement. By the same token, the investor, trader, or economist will never cease to be amazed by the political analyst’s inability to grasp the concept of “already priced in” or “the second derivative.” What needed to be done was to master the art of macro investing and geopolitics. Marko took this upon himself. It was audacious and it provoked a lot of skepticism from the dismal scientists and the political scientists alike. But Geopolitical Alpha, the concept and the book, is the consequence – and we are now all the better for it. Marko is fundamentally a post-modern thinker. His methodological hero is Karl Marx for the development of materialist dialectic, the back-and-forth debate between economic forces that humans internalize in the form of competing ideologies. His foil is the humanist and republican, Niccolo Machiavelli – not for his amoral approach, but for prizing the virtue of the prince in the face of outrageous fortune. Human agency is Marko’s favorite punching bag – he excels at identifying the ways in which individuals will be frustrated despite their best efforts by the cold, insensitive walls of reality around them. If there is a critique of Marko’s book, then, it is that he gives short shrift to the classical liberal tradition – or as I like to think of it, the balance-of-power tradition. The idea that hegemony, or unipolarity, leads to a stable social and political environment conducive to peace and prosperity has a lot going for it. But it also partakes of an older tradition of thought that envisions a single, central political order as necessarily the most stable and predictable – a tradition that can be ascribed to Plato as well as Marx. You can see the positive implication for financial markets. But what if this tradition is only occasionally right – what if it too is subject to historical cycles? If that is the case, then the Beijing consensus is a mirage – and the US’s reversion to a blue-water strategy (not only under President Trump, but also under a future President Biden, according to his campaign agenda) does not necessarily herald the “end [of] American dominance on the world stage.” The classical tradition behind the Greco-Roman, British, and American constitutional systems, including their naval strategies, envisioned a multipolar order that was somewhat less stable but more durable, and this tradition has proven immensely beneficial for the creation of technology and wealth. Of course, Marko is very much alive to this tradition and, despite his critique of the ancients, shows himself to be highly sensitive to the interplay of virtue and fortune. Throughout the work, the analytical style can be characterized as restless energy in the service of cool, chess-playing logic. Marko is generous with his knowledge, merciless in drawing conclusions, and outrageously funny in delivery. He attacks the questions that matter most to investors and that experts too often leave shrouded in finely wrought uncertainty. He also shows himself to be a superb writer as well as strategist, interspersing his methodological training sessions with vivid anecdotes of a lifelong intellectual journey from a shattered Yugoslavia to the heights of finance. The bits of memoir are often the best, such as the intro to Chapter Six on geopolitics. To paraphrase a great author, Marko writes because he has a story to tell, not because he has to tell a story. The tale of the mysterious consulting firm Papic and Parsley will do a great public service by teaching readers precisely how skeptical of mainstream news journalism they should be. It isn’t enough to say that we read Geopolitical Alpha and liked it – the sole criterion for a review in this column. Rather, the book and its author are the reason this column exists. And Geopolitical Alpha is now the locus classicus of market-relevant geopolitical analysis. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 We favored the upper side of the range, first $2.5 trillion, and subsequently something closer to House Speaker Nancy Pelosi’s demand of $2.2 trillion. We have speculated that Republicans may get her to settle at $1.9 trillion. 2 Two of these cases were unique in that a vice president took over from a president who died and then won re-election – unlike Trump’s scenario. 3 On August 12 a Greek Navy frigate collided with a Turkish vessel guiding the Oruc Reis. Athens called the incident an accident while Ankara referred to it as a provocation. 4 The so-called Seville Map was prepared at the request of the European Union by researchers at the University of Seville, attempts to clarify the exclusive economic zones of Turkey and Greece in the Aegean Sea. The US announced on September 21 that it does not consider the Seville map to have any legal significance. 5 The Blue Homeland or Mavi Vatan doctrine announced in 2006 intends to secure Turkish control of maritime areas surrounding its coast (Mediterranean Sea, Aegean Sea, and Black Sea) in order to secure energy supplies and support Turkey’s economic growth. 6 Erdogan’s claim that gas from the recently discovered Sakarya gas field would reach consumers by 2023 is likely overly optimistic and unrealistic. The drilling costs and commercial viability of the field are yet to be determined. Thus, the find does not impact dynamics in the East Med. 7 New Jersey: Wiley, 2021. 286 pages. Section II: GeoRisk Indicators China

China: GeoRisk Indicator

China: GeoRisk Indicator

Russia

Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

UK

UK: GeoRisk Indicator

UK: GeoRisk Indicator

Germany

Germany: GeoRisk Indicator

Germany: GeoRisk Indicator

France

France: GeoRisk Indicator

France: GeoRisk Indicator

Italy

Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Canada

Canada: GeoRisk Indicator

Canada: GeoRisk Indicator

Spain

Spain: GeoRisk Indicator

Spain: GeoRisk Indicator

Taiwan

Taiwan: GeoRisk Indicator

Taiwan: GeoRisk Indicator

Korea

Korea: GeoRisk Indicator

Korea: GeoRisk Indicator

Turkey

Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

Brazil

Brazil: GeoRisk Indicator

Brazil: GeoRisk Indicator

Section III: Geopolitical Calendar

Highlights Global GDP growth estimates from the OECD point to a stronger recovery in oil demand than markets are pricing in at present (Chart of the Week). Our forecast for Brent remains at $46/bbl for 2H20 and $65/bbl on average for 2021. Global trade data – particularly EM import volumes, which are highly correlated with income (GDP) – remain supportive, as does monetary policy, particularly out of the US, EU and China. Doubt surrounds the US Congress’s determination to extend the fiscal support that underpins many households’ and firms’ budgets, but we expect a deal. Aggregate demand uncertainty remains high. COVID-19 infections are increasing globally. However, death rates appear to be trending lower, which likely will keep lockdowns localized. On the supply side, the leaders of OPEC 2.0 – Saudi Arabia (KSA) and Russia – continue to insist on full adherence to agreed production levels among member states. This carries an implicit threat the leadership may be willing to flood the market with oil to remind the laggards of the consequences of cheating, which would hit non-Gulf OPEC members particularly hard. Longer term, sharp reductions in capex point to higher prices in the mid-2020s. Feature Stronger-than-expected growth estimates, most recently the OECD’s, suggest the decline in aggregate demand to the end of this year will not be as gruesome as earlier feared. Realized oil demand continues its V-shaped recovery, in line with rising GDP in the wake of the COVID-19 pandemic. Stronger-than-expected growth estimates, most recently the OECD’s, suggest the decline in aggregate demand to the end of this year will not be as gruesome as earlier feared, and that growth could be stronger in 2021 than earlier anticipated, as seen in the Chart of the Week.1 The OECD is expecting global GDP growth to contract 4.5% this year vs. its June estimate of a 6% decline. The World Bank’s forecast of a 5.2% contraction in global GDP this year drives our oil-demand estimate, so the OECD’s estimate is more bullish for oil demand. Incoming data for EM import volumes suggest income is on track to recover by year-end or early 2021 in developing and emerging markets (Chart 2). EM import growth is driven by income growth; EM demand is the most important driver of global oil-demand growth. Chart of the WeekOECD Raises Global Growth Estimates

Fear And Loathing Attend Oil-Price Recovery

Fear And Loathing Attend Oil-Price Recovery

Chart 2EM Import Volumes Remain On Recovery Path

EM Import Volumes Remain On Recovery Path

EM Import Volumes Remain On Recovery Path

Growth estimates continue to be overshadowed by fears of another round of widespread lockdowns arising from a second wave of COVID-19 infections and deaths. For next year, the OECD expects global growth to expand at a 5% rate vs. the World Bank’s 4.2% rate. We are awaiting the Bank’s updated income (GDP) estimates before revising our oil demand estimates. We already show EM oil demand, proxied by non-OECD consumption, recovering to pre-COVID-19 levels by the middle of next year, while DM demand flattens at a lower level (Chart 3). A confirmation of better-than-expected growth – particularly from EM economies – would move our expectation of a full recovery in EM oil-demand into 1H21 and could push DM demand up slightly. Chart 3EM Oil Demand Will Surpass Pre-COVID-19 Levels In Mid-2021

EM Oil Demand Will Surpass Pre-COVID-19 Levels In Mid-2021

EM Oil Demand Will Surpass Pre-COVID-19 Levels In Mid-2021

Chart 4COVID-19 Infections Rising, But Death Rates Are Falling

Fear And Loathing Attend Oil-Price Recovery

Fear And Loathing Attend Oil-Price Recovery