Emerging Markets

Highlights The EM equity benchmark’s concentration in the top six stocks – that in turn correlate with US FAANGM – has risen substantially. Hence, the outlook for US mega-cap stocks will continue to significantly impact the EM equity benchmark. US FAANGM stocks have been closely tracking the trajectory of – and share many other similarities with – previous bubbles. Hence, it is risky to dismiss the mania thesis. That said, it is impossible to know how long this equity mania will last, how far it will go and what will trigger its volte-face. Odds of a repeat of the 2015 boom-bust cycle in Chinese equities are low. The rally in Chinese stocks and commodities might be due for a pause. Feature Concentration Risk Chart 1EM: Mega-Caps Stocks Versus The Equal-Weighted Index

EM: Mega-Caps Stocks Versus The Equal-Weighted Index

EM: Mega-Caps Stocks Versus The Equal-Weighted Index

The EM equity index's hefty gains since the late-March lows have largely been at the hands of about six stocks: Alibaba, Tencent, TSMC, Samsung, Naspers and Meituan-Dianping (Chart 1). The latter is a Chinese web-service platform company, while Naspers derives 75% of its revenue from its equity ownership in Tencent and 25% from a Russian internet company. For ease of reference, we refer to the big four (Alibaba, Tencent, Samsung and TSMC) as EM ATST. Table 1 illustrates that the top six companies combined account for about 24.3% of the MSCI EM equity market cap. For comparison, US FAANGM (Facebook, Apple, Amazon, Netflix, Google and Microsoft) account for 25% of the S&P 500 market cap. The remainder of the EM equity universe – including all Chinese, Korean and Taiwanese stocks other than the six mega caps listed above – has rallied less (Chart 1). This is very similar to the dynamics in the US equity market, where the equally-weighted index has substantially diverged from the FAANGM index (Chart 2). Table 1Market Cap Weights & Performance Since March Lows

EM Equities: Concentration And Mania Risks

EM Equities: Concentration And Mania Risks

Chart 2US: FAANGM Versus The Equal-Weighted Index

US: FAANGM Versus The Equal-Weighted Index

US: FAANGM Versus The Equal-Weighted Index

Table 2MSCI EM Stocks: Country Weights

EM Equities: Concentration And Mania Risks

EM Equities: Concentration And Mania Risks

The EM ATST’s exponential rise has also boosted their respective country weightings in the MSCI EM equity benchmark. Table 2 demonstrates that China, Korea and Taiwan together account for 65% of the EM benchmark, India for 8% and all other 22 countries combined for 27%. Note that the market cap ($1.7 trillion) of the remaining 22 countries is almost as large as the market cap of the top six EM individual stocks. On the whole, concentration in the EM benchmark is as high as ever. Apart from global trade and Chinese growth, there are two other forces that will define the direction of EM mega-cap stocks: (1) rising geopolitical tensions between the US and China, and (2) a continuous mania or bust in “new economy” stocks. We discuss the latter in the following section. Escalating tensions between the US and China, including North Korea’s potential assault on South Korea, pose risks to Chinese, Korean and Taiwanese stocks. This is one of the critical reasons why we have been reluctant to chase these markets higher, despite upgrading our outlook on Chinese growth. If these bourses relapse, their sheer weight in the EM benchmark will pull the index down. The EM equity index’s outperformance in recent weeks has been due to the surge in both EM mega-cap stocks and Chinese share prices more broadly. Bottom Line: The EM equity benchmark concentration has risen substantially due to outsized gains in several “new economy” stocks. What’s more, the EM equity index’s outperformance in recent weeks has been due to the surge in both EM mega-cap stocks and Chinese share prices more broadly (we discuss the latter below). If the global mania in “new economy” stocks persists, EM ATST could well drive the overall EM equity index higher. Conversely, if “new economy” shares roll over for whatever reason, the EM equity benchmark’s advance will reverse. A Bubble Or Not? An assessment of the sustainability of the rally in US FAANGM stocks is critical for investors in the EM equity benchmark if for no other reason than the concentration hazard. We present the following considerations in assessing whether the FAANGM and EM ATST rally is or is not a mania: First, the exponential rally in FAANGM stocks is not a new phenomenon: It has been taking place over the past 10 years. Our FAANGM index – an equal-weighted average of six stocks (Facebook, Amazon, Apple, Netflix, Google and Microsoft) – has increased 20-fold in real (inflation-adjusted) US dollar terms since January 2010. Its rise is on par with the magnitude of the bull market in the Nasdaq 100 index in the 1990s and Walt Disney in the 1960s, and well exceeds other bubbles, as illustrated in Chart 3. All price indexes on Chart 3 are shown in real (inflation-adjusted) terms. Chart 3Each Decade = One Mania

EM Equities: Concentration And Mania Risks

EM Equities: Concentration And Mania Risks

All these manias and bubbles started with excellent fundamentals, and price gains were initially justified. Toward the end of the decade, however, their outsized gains attracted momentum chasers and speculators, catapulting share prices exponentially higher. Second, a financial mania requires: (1) solid past performance; (2) a story that can capture investors’ imaginations, and (3) plentiful liquidity. The “new economy” stocks fit all of these criteria: They have delivered super-sized performance over the past 10 years; They easily capture ordinary people’s imaginations – the average person on the street knows that FAANGM and EM ATST stocks benefit from people working from home and spending more time online; The Federal Reserve and many other central banks are injecting enormous amounts of liquidity into their respective economies. Third, there is a striking similarity between the FAANGM rally and previous bubbles: The mania-subjects of the preceding decades assumed global equity leadership early in their respective decade, rose steadily throughout, and went exponential at the very end of the decade. The latest parabolic surge in FAANGM stocks along with its duration (10 years of global equity outperformance and leadership) and magnitude (20-fold price appreciation in real inflation-adjusted terms) conspicuously resembles those of previous bubbles. Interestingly, the majority of previous bubbles peaked and tumbled around the turn of each decade, the exception being Walt Disney – the Nifty-Fifty bubble of the 1960s – which rolled over in 1973. Given FAANGM stocks have been closely tracking the trajectory of previous bubbles, it will not be surprising if 2020 ends up marking the peak for “new economy” stocks. Fourth, the last exponential upleg in the tech and telecom bubble of 1999-2000 occurred amid a one-off demand surge for tech hardware and software. The Y2K scare – worries that computers and networks around the world might malfunction on the New Year/new millennium eve – spurred many companies to order new hardware and upgrade their systems and networks. As a result, there was a one-off boom in orders in the global technology industry in the fourth quarter of 1999 and first quarter of 2000. Chart 4Orders For Computers And Electronics Have Remained Resilient

Orders For Computers And Electronics Have Remained Resilient

Orders For Computers And Electronics Have Remained Resilient

Investors extrapolated this one-off demand surge into the future, mistaking it for recurring growth. As a result, they assigned extremely high valuations to these tech stocks in the first quarter of 2000. Similarly, since March, working and shopping from home has sharply increased demand for web services, online shopping, cloud computing and tech hardware. The top panel of Chart 4 demonstrates that US manufacturing orders for computers and electronic products did not contract in the March-May period, while orders for capital goods have plunged since March. Similarly, Taiwanese exports – which are heavy on tech hardware – are holding up well despite the crash in global trade (Chart 4, bottom panel). Some of this demand strength is structural, but part of it is one-off and non-recurring. Certainly, one should not extrapolate their recent growth rates into the future. However, investors are prone to extrapolation and chasing winners. Fifth, valuations of US FAANGM and EM ATST are elevated. Trailing P/E ratios for EM ATST stocks are shown in Table 3. Table 3Price-To-Earnings For Top 6 EM Stocks

EM Equities: Concentration And Mania Risks

EM Equities: Concentration And Mania Risks

All in all, provided both US FAANGM and EM ATST consist of admirable companies with great competitive advantages and business models, it is tempting to dismiss the bubble argument. Nevertheless, there are enough similarities with previous manias to compel investors to be vigilant. Even great companies have a fair price, and substantial price overshoots will not be sustainable. We sense a growing number of investors deem US FAANGM and EM ATST stocks as invincible. When some stocks are regarded as unbeatable, their top is not far. Our major theme for the past decade – elaborated in the report, How To Play EM In The Coming Decade1 published in June 2010 – has been as follows: Sell commodities / buy health care and technology. Until 2019, we were recommending being long EM tech/short EM resource stocks. Unfortunately, since 2019, the corrections in EM “new economy” stocks have proved to be too short and fleeting, and we were unable to buy-in. Their share prices have lately gone parabolic: They are now in a full-blown mania phase. As to global equity leadership change from growth to value stocks, we maintain that major leadership rotations typically occur during or at the end of an equity selloff, as we elaborated in our October 3, 2019 report (Charts 5 and 6). Chart 5EM vs DM: Leadership Rotation Requires Market Turbulence

EM vs DM: Leadership Rotation Requires Market Turbulence

EM vs DM: Leadership Rotation Requires Market Turbulence

Chart 6Growth vs Value: Leadership Rotation Requires Market Turbulence

Growth vs Value: Leadership Rotation Requires Market Turbulence

Growth vs Value: Leadership Rotation Requires Market Turbulence

Apparently, the February-March selloff did not produce a shift in equity leadership. Barring a major selloff, “new economy” stocks will likely continue to lead. Chart 7Fed Rate Cuts Did Not Prevent The S&P 500 Bubble From Unravelling

Fed Rate Cuts Did Not Prevent The S&P 500 Bubble From Unravelling

Fed Rate Cuts Did Not Prevent The S&P 500 Bubble From Unravelling

Finally, easy money policies encourage speculation and contribute to the build-up of manias. However, when a bubble starts unravelling, low interest rates are often unable to avert the bust. For example, when the tech bubble began bursting in 2000, the Fed cut rates aggressively and US bond yields plunged. Yet, low interest rates did not prevent tech share prices from deflating further (Chart 7). Bottom Line: It is impossible to know how long this equity mania will last, how far it will go and what will trigger its volte-face. One thing is certain: there is a lot of froth – particularly in terms of valuation and positioning – in these “new economy” stocks. Yet, these excesses could last longer and get larger. A Mania In Chinese Equities? Many commentators have rushed to compare the latest surge in Chinese stocks with the exponential advance in the first half of 2015. We do not think this rally will go on without interruption for another five months like it did back then. Our rationale is as follows: The Chinese authorities are much more vigilant now, and they will try to induce periodic corrections to avoid another mania and bust similar to those that occurred five years ago. The Chinese authorities are much more vigilant now, and they will try to induce periodic corrections to avoid another mania and bust similar to those that occurred five years ago. Both China’s MSCI Investable and CSI 300 equity indexes are retesting their previous highs (Chart 8). In the past they failed to break above these levels, and this time is likely to be no different, at least for now. The latest spike is more likely to be the final hurrah before a setback. Critically, the 12-month forward P/E ratio for China’s MSCI Investible index has also risen to its previous peaks (Chart 9, top panel). This has occurred with little improvement in the 12-month forward EPS (Chart 9, bottom panel). In short, share prices have run ahead of the business cycle and are already pricing in a lot of profit recovery. Chart 8Chinese Stocks Are At Their Previous Highs

Chinese Stocks Are At Their Previous Highs

Chinese Stocks Are At Their Previous Highs

Chart 9Chinese Investable Stocks: A Rally Driven By P/E Expansion

Chinese Investable Stocks: A Rally Driven By P/E Expansion

Chinese Investable Stocks: A Rally Driven By P/E Expansion

Chart 10Chinese Onshore Stocks: A Two-Tier Market

Chinese Onshore Stocks: A Two-Tier Market

Chinese Onshore Stocks: A Two-Tier Market

Most of the rally since the March lows has been due to “new economy” stocks. Share prices of “old economy” companies did not do that well before July. Tech stocks in the onshore market have gone parabolic (Chart 10, top panel). This contrasts with lackluster performance of materials, industrials, and property stocks (Chart 10, bottom panels). Critically, in the onshore market, tech stocks are trading at the following trailing P/E ratios: the market cap-weighted P/E is 155, and the median P/E is 60. Needless to say, these valuations are outright expensive. Bottom Line: Odds of a repeat of the 2015 boom-bust cycle are low. The rally in Chinese stocks might be due for a pause. On June 18, we upgraded Chinese stocks to overweight from neutral within the EM benchmark, a recommendation that remains intact. We have a much lower conviction on the absolute performance of Chinese stocks in the near-run. China And Commodities An important question to address is whether the rally in commodities in general and copper in particular are signals of a sustainable recovery in the mainland economy. Without a doubt, economic conditions in China have been improving, and infrastructure spending has been accelerating. However, the magnitude of the upswing in copper prices is excessive relative to the strength of the Chinese economy. The spike in resource prices in general and copper in particular has been due to three forces: (1) China’s unprecedented super-strong imports; (2) global investors buying commodities; and (3) output cuts. It is highly unlikely that commodity demand in China is this strong. In our opinion, this reflects restocking. Chart 11 shows that Chinse imports of copper and copper products surged by 100% in June from a year ago, while imports of steel products increased by 100% and oil import volumes rose by 34%. It is highly unlikely that commodity demand in China is this strong. In our opinion, this reflects restocking. Provided cheap credit availability, wholesalers, intermediaries or users of commodities have rushed to buy before prices rise further. In the case of copper, it will take several months before the real economy absorbs that much of the red metal. Hence, China’s copper imports are poised to relapse in the coming months. Chart 12 illustrates that investors’ net long positions in copper have risen to their highest level since early 2019. Consistently, the July Bank of America/Meryl Lynch Global Fund Manager Survey revealed that as of early July, portfolio managers had built up their largest net long positions in commodities since July 2011. Not only oil but also copper and iron ore prices have benefitted from production declines. Due to surging COVID infections, Chile and Peru have sharply reduced copper output and Brazil has curtailed iron ore production. Chart 11Chinese Imports Of Commodities Have Surged

Chinese Imports Of Commodities Have Surged

Chinese Imports Of Commodities Have Surged

Chart 12Investors Have Gone Long Copper

Investors Have Gone Long Copper

Investors Have Gone Long Copper

Simultaneous buying of commodities by China and global investors as well as production cuts have considerably benefited resource prices as of late. Our suspicion is that commodities inventories in China have become elevated. This entails reduced purchases by China, and by extension an air pocket in commodities prices in the months ahead. Bottom Line: The rally in resources in general and copper in particular is at risk of a correction. We remain long gold/short copper. Investment Strategy In absolute terms, the risk-reward of EM share prices is not attractive. However, as we have argued in the past two months, FOMO (fear-of-missing-out) mania forces could take share prices higher. The timing of a reversal is never easy especially when a FOMO-driven mania is alive. For now, for asset allocators we reiterate a below-benchmark allocation in EM stocks within a global equity portfolio. However, a breakdown in the trade-weighted US dollar will prompt us to upgrade EM within the global equity benchmark (Chart 13). The broad trade-weighted dollar is teetering on an edge but has not yet broken down (Chart 14). In sum, global equity portfolios should be ready to upgrade their EM allocation to neutral on signs that the broad trade-weighted US dollar is breaking down. Chart 13EM vs DM: Is The Downtrend Intact?

EM vs DM: Is The Downtrend Intact?

EM vs DM: Is The Downtrend Intact?

Chart 14The Broad Trade-Weighted Dollar Is On An Edge

The Broad Trade-Weighted Dollar Is On An Edge

The Broad Trade-Weighted Dollar Is On An Edge

As we argued last week, the US dollar could weaken against DM currencies amid the next selloff in global share prices. This is why last week we switched our short positions in an EM currency basket from the US dollar to an equally-weighted basket of the euro, the Swiss franc and Japanese yen. This strategy remains valid. The US dollar is at risk versus DM currencies. However, EM exchange rates may not be out of the woods, given their poor fundamentals on the one hand and potential geopolitical risks in North Asia on the other. We are neutral on both EM local currency bonds and EM sovereign and corporate credit. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Footnotes 1 Please see Emerging Markets Strategy Special Report "How To Play EM In The Coming Decade," dated June 10, 2010. Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

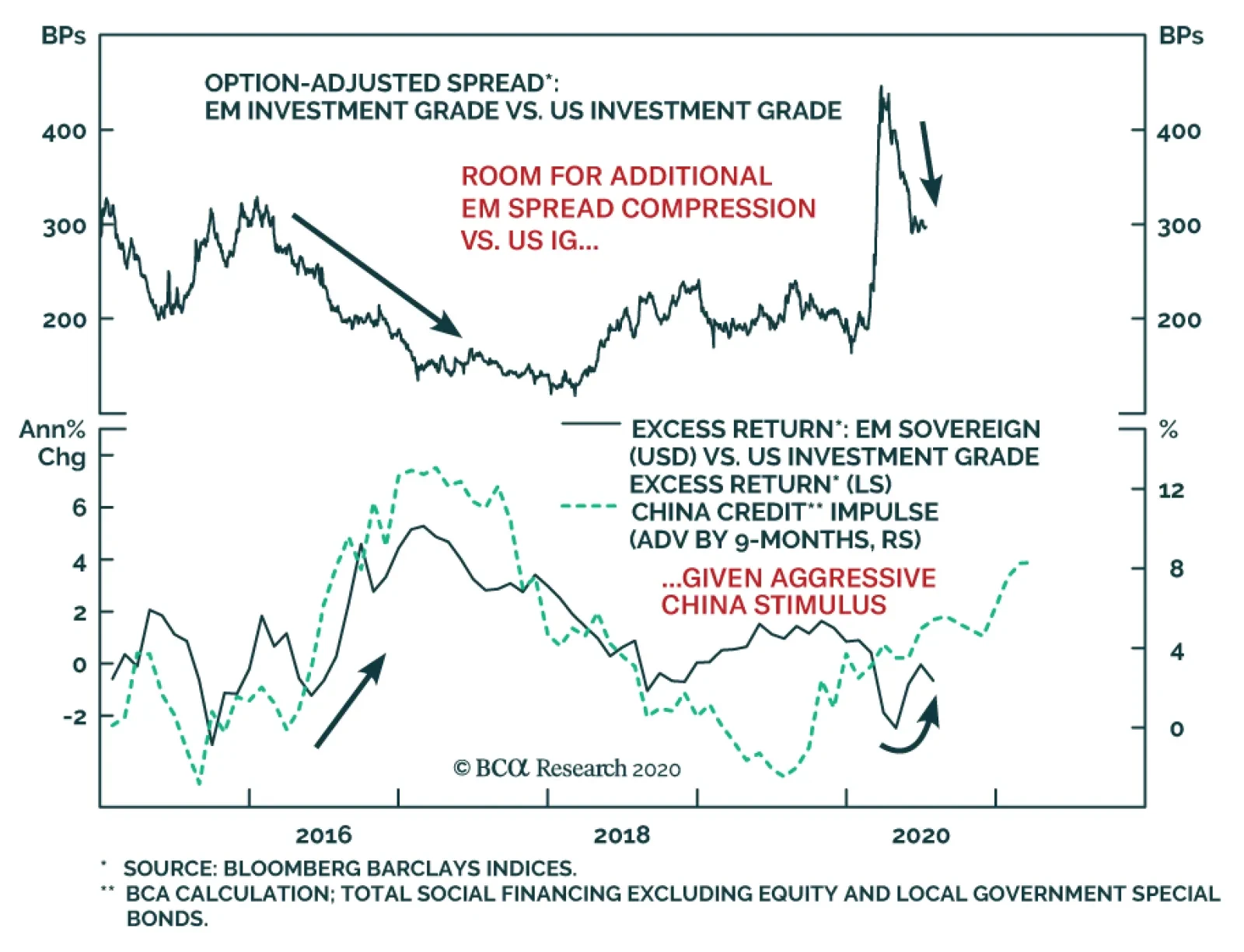

BCA Research's Global Fixed Income Strategy service is upgrading its allocation to EM USD-denominated corporates and sovereigns to neutral. A weaker USD and a clear bottom in growth are required to buy EM USD-denominated sovereign and corporate debt.…

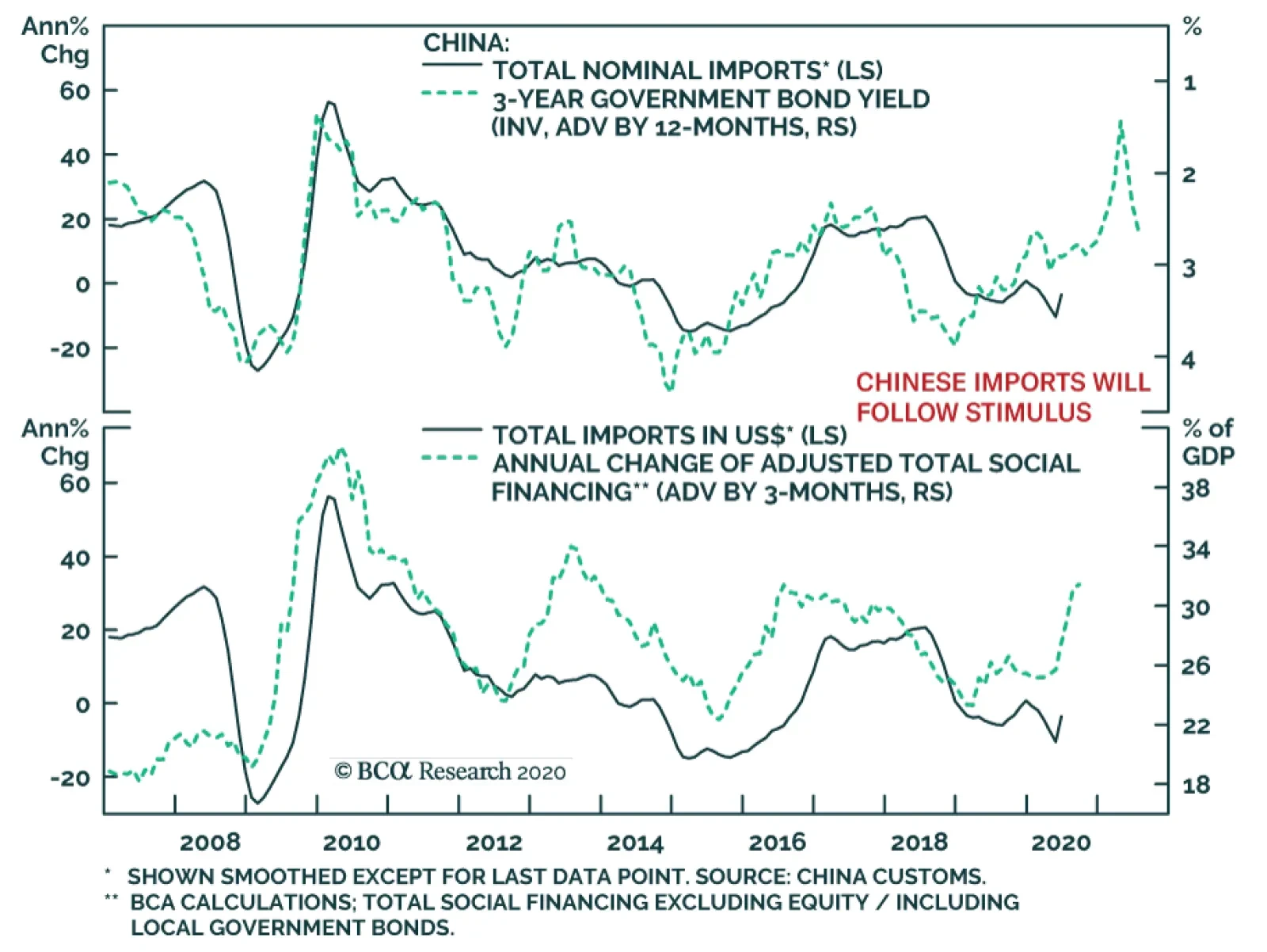

China’s June trade numbers offered some hope for the global economy. In USD terms, the annual growth rate of exports rebounded to 0.5% from -3.3% last May. Imports’ growth recovered to 2.7% from -16.7%. Shipments of masks and medical supplies supercharged…

China’s credit growth remains strong. In June, new loans hit CNY1.8 trillion, bringing new bank lending to CNY12.1 trillion for the first half of 2020, which beats the previous peak of CNY9.7 trillion recorded in H1 2019. Total social financing (which…

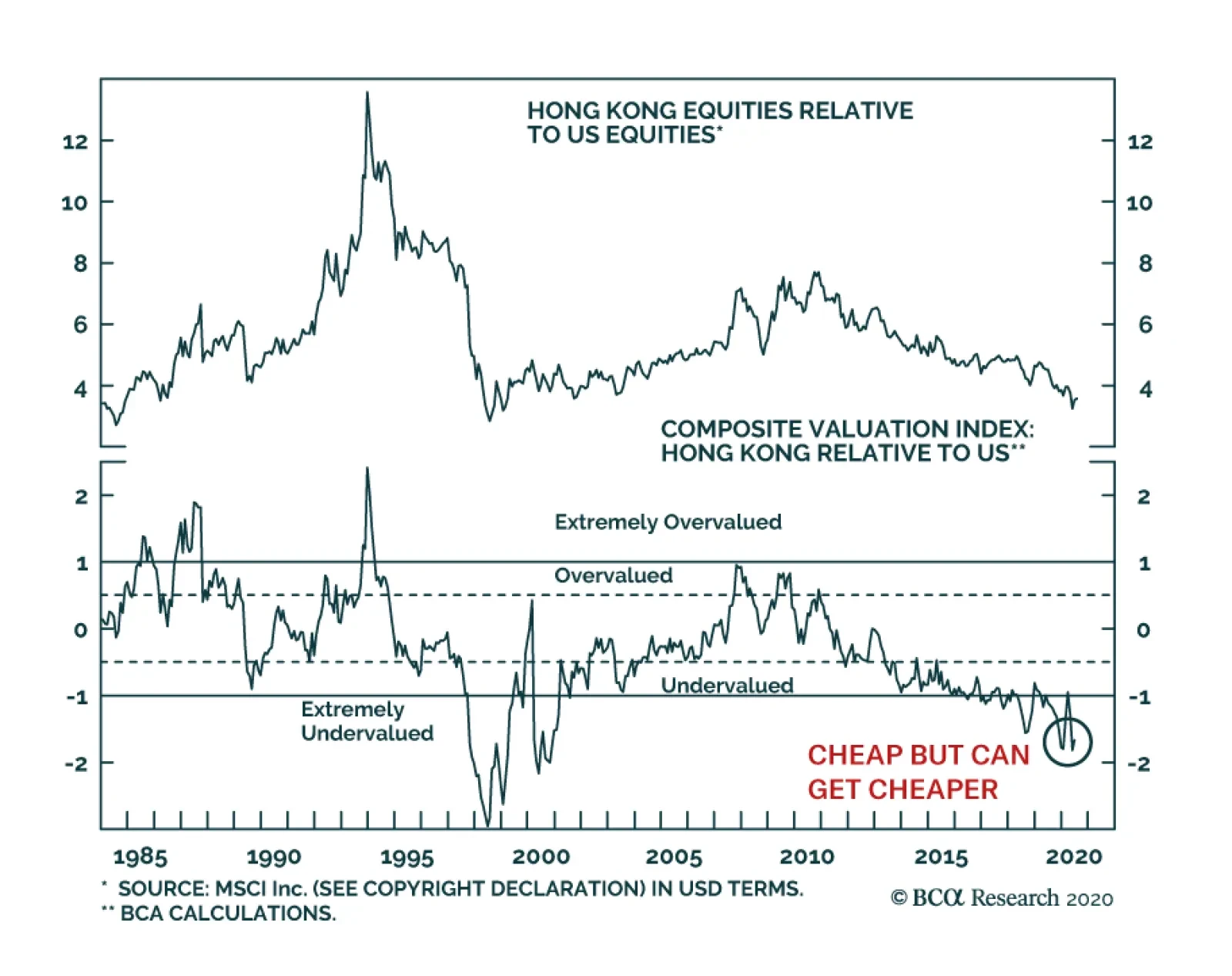

The growing incursion of Beijing into the governance of Hong Kong is accentuating the woes of a stock market already hurt by its heavy exposure to financials. As a result, investors are increasingly questioning the relevance of Hong Kong as a global financial…

Highlights The bull market in US-Iran tensions was never resolved, and now a series of suspicious explosions in Iran raises the possibility that tensions will re-escalate. Iran’s interest lies in waiting out Trump so that a Democratic victory in the US election can restore the US-Iran strategic détente agreed in 2015. However, both the Trump administration and US ally Israel are applying “maximum pressure” on Iran and could go on the offensive at a time when Trump’s odds of re-election are collapsing. Israel cannot engage in a full-fledged war with Iran alone but it would have American backing for pressure tactics through the duration of Trump’s term. A “wag the dog” scenario is not inconceivable because the US and Israel have long-term national security interests at stake while Iran is on the verge of economic collapse. Investors should prepare for near-term global equity volatility and safe-haven demand for a number of reasons but a major escalation in Iran would add to the list. Stay long Brent crude oil. Feature Since May 2018 we have argued that US-Iran tensions will remain market-relevant. We downgraded the odds of US air strikes from 40% in June 2019 to 20% in January of this year after Iran’s lackluster retaliation to the US assassination of its top military commander. Now things are heating up again due to a series of extremely suspicious explosions in Iran that may or may not be linked to Israel and the United States. The COVID-19 pandemic, oil price rout, and global recession have reinforced this bull market in US-Iran tensions by weakening and destabilizing the entire Shia Crescent, from Lebanon to Iran. They have also pushed President Trump dangerously close to “lame duck” status, which reduces the constraints on conflict with Iran for the remainder of his term. In this report we update our Iran view by looking at whether the Trump administration or Israel could attempt to “wag the dog,” i.e. provoke a conflict with Iran to boost Trump’s re-election odds or achieve some long-term strategic objectives while Trump is still in power. We have long held the view that Iran poses a market-relevant geopolitical risk and now the mysterious attacks in Iran suggest it could be materializing. Nothing is confirmed, but it is wise for investors to monitor these developments in case they escalate. Geopolitical incidents often cause buying opportunities but they can create substantial equity drawdowns first. Cyber-Rattling In The Middle East A string of mysterious explosions and fires at military and economic facilities have rocked Iran in recent days (Table 1). Table 1Iran Hit By A String Of Mysterious Attacks

Cyber-Rattling In The Middle East

Cyber-Rattling In The Middle East

The most significant of these incidents is the July 2 explosion at the Natanz nuclear facility – Iran’s main uranium enrichment facility, which houses a new centrifuge assembly center.1 The fire resulted in a significant setback to the development and production of advanced IR-6 and IR-8 centrifuges used to enrich uranium – by up to two years. Iranian officials initially downplayed the incidents as unsuspicious accidents. However the Natanz explosion was too significant to cast off. Iran’s state-run news agency IRNA declared that the Natanz incident may be the work of foreign countries, “especially the Zionist regime [Israel] and the US,” and vowed Iranian retaliation if sabotage is proven to be the case. Similarly, the New York Times reported that an anonymous Middle Eastern intelligence official – rumored to be Mossad chief Yossi Cohen – called the incident the work of Israel.2 Israel’s response to these allegations has been oblique, but the accusation is not far-fetched. Israel has a successful history of halting the advancement of nuclear programs in the region. Mossad’s Operation Opera destroyed Iraq’s only known nuclear facility in 1981, and Operation Outside the Box bombed a suspected nuclear reactor at the Kibar site in Syria in 2007. Israeli intelligence has also previously been accused of targeting Iran’s missile program – with the assassination of four Iranian nuclear scientists between 2010 and 2012. Israel is also believed to be involved, with the US, in Operation Olympic Games, the Stuxnet cyber attacks that stunted Iran’s uranium enrichment program circa 2010. Iran’s ballistic missile program and alleged nuclear weapons ambitions remain Israel’s greatest long-term strategic threat in the region. More recently, Iran and Israel have been locked in a series of cyber-attacks. Israel claims to have foiled an Iranian attack on its water facilities in April which attempted a cyber break on water control systems. A May 9 cyberattack on Iranian shipping hub Shahid Rajaae – through which half of Iran’s maritime trade traverses – is seen as Israeli retaliation. Most recently, Israel’s Mossad revealed that it thwarted Iranian attempts to attack Israeli diplomatic missions in Europe. These attacks come as the US increases pressure on UN Security Council members to support the indefinite extension of the UN arms embargo against Iran, which is scheduled to expire on October 18.3 But other signatories to the 2015 Iranian nuclear agreement – China, Russia, Germany, Britain, and France – argue that since the US withdrew from the Joint Comprehensive Plan of Action (JCPA), its threat to invoke a “snapback” provision of the deal to reimpose former UN sanctions on Iran is not legally valid. The other JCPA signatories remain committed to the deal, arguing for its necessity in order to continue IAEA inspections that prevent Iran from developing nuclear weapons. They are biding their time to see if Trump is re-elected before deciding anything. Iran has moved further from the JCPA’s requirements since announcing, on January 5, 2020, that it will no longer comply with restrictions to its nuclear program (Table 2). The risk is that unless controlled, this will eventually significantly reduce Iran’s “breakout time” – the time required to acquire enough fissile material for one bomb. The nuclear deal aimed to maintain at least a one-year breakout time, and this is generally understood to be the US’s “red line.” Table 2Iran No Longer Complying With 2015 Nuclear Deal

Cyber-Rattling In The Middle East

Cyber-Rattling In The Middle East

Despite some non-compliance, Iran is still permitting IAEA inspectors to monitor and verify its nuclear activities. Yet the IAEA Board of Governors passed a resolution, requesting Iran’s cooperation in the investigation into possible undeclared nuclear materials and sites.4 Chart 1Iran's Sphere Of Influence In Collapse

Iran's Sphere Of Influence In Collapse

Iran's Sphere Of Influence In Collapse

As tensions with US and Israel escalate, Tehran has been keen to highlight its military capabilities. Revolutionary Guard Navy Commander Rear Admiral Alireza revealed the existence of onshore and offshore underground missile sites along the Persian Gulf and Gulf of Oman, holding advanced long-range missiles and new weapons, more capable of launching attacks against enemies. Escalating tensions raise the likelihood of retaliation as Iran reconsiders its “strategic patience” policy.5 Tehran had been playing the waiting game, especially since Trump’s decision to assassinate Quds Force chief Qassem Soleimani in January. Iran has an interest in avoiding confrontation in the months ahead of the US election on November 3. Iran’s attack on Saudi Arabia in September 2019 led to a boost in Trump’s approval rating. A major conflict today would cause a patriotic rally around the president at a time when he is beset with negative opinion over the coronavirus response and poor race relations. Iran has an interest in Joe Biden winning the presidency in November. Biden would likely restore the US-Iran deal, which would remove sanctions and allow Iran to open its economy. However, neither the Trump administration nor the Israeli government share that interest. The latest attacks raise the possibility that the US and/or Israel are going on the offensive. This could force Iran to retaliate. Iranian moderates are already suffering domestically. Iran’s hardline parliamentarians were never on board with the nuclear deal and criticized President Hassan Rouhani when President Trump pulled out of it in May 2018. This past weekend Foreign Minister Javad Zarif, an ally of Rouhani whose reputation also rests on the deal, was heckled as he addressed the parliament. As of February, parliament is mostly comprised of hardliners.6 Iran is also on shaky ground in the Shia Crescent. Lebanon and Iraq – the two countries most entrenched in Iran’s sphere of influence – have been experiencing civil unrest. Protesters in both countries initially took to the streets last fall in demonstration of anger over government corruption, the sectarian based political system, and poor economic conditions. The pandemic and recession have breathed new life into these movements. The Lebanese pound collapsed on the parallel market since October, and some groups have called for the disarmament of Iran-backed Hezbollah (Chart 1). Meanwhile a June cabinet decision in Iraq to cap the amount and number of state salaries and pension payments collected – in attempt to buttress the country’s ailing finances – fueled outrage. Iraq’s Prime Minister Mustafa al-Kadhimi is also in a tussle with Iran-backed paramilitary forces as he attempts to curb their influence and bring them under state control.7 Chart 2Iran Has Little To Lose

Iran Has Little To Lose

Iran Has Little To Lose

Thus a timid stance by Iran in face of foreign attacks will not go down well. Instead, with oil production having collapsed, the economy in shambles, and its sphere of influence in turmoil, Tehran has little to lose in protecting what is left of its nuclear program and deterring American or Israeli aggression (Chart 2). With few options left, Iran is likely to move further away from its “strategic patience” in response to the uptick in “maximum pressure.” Bottom Line: Tensions are escalating between Tehran and Washington/Tel Aviv. Cyber attacks are likely to increase in the lead up to the expiration of the arms embargo on October 18 and US elections this fall. Iran may be forced to abandon its policy of “strategic patience” if its foes sabotage its nuclear capabilities. Expect the conflict to spillover to Iran’s proxies in the region – Iraq, Lebanon, and Syria. So What? Massive monetary and fiscal stimulus and continued commitment from OPEC 2.0 on the supply side will keep oil prices moving higher this year. Barring a second COVID-19 wave, our Commodity & Energy Strategists expect oil markets to rebalance beginning in 3Q2020, with Brent prices averaging $40/bbl this year and $65/bbl in 2021 (Chart 3). We remain long Brent which is up 70.55% since initiation in March. The escalation in tensions in the Persian Gulf is an upside risk to this assessment. That said, with major oil producers now operating significantly below capacity in compliance with the OPEC 2.0 production agreement, the net impact on oil prices will likely be muted and short-lived. Production can be increased to fill gaps. As demonstrated by the recent acts of sabotage in Iran and Israel, the increase in geopolitical tensions globally will manifest in cyberattacks, supporting cyber stocks. Our strategically long ISE Cyber Security Index relative to the S&P500 Info Tech sector trade is up 2% since initiation in April (Chart 4). Chart 3Oil Markets On The Way To Recovery

Oil Markets On The Way To Recovery

Oil Markets On The Way To Recovery

Chart 4Buy Cybersecurity Stocks

Buy Cybersecurity Stocks

Buy Cybersecurity Stocks

Finally, we should note that Iran is not the only geopolitical risk that could explode amid the US election cycle. China is the greater risk. But President Trump faces fewer financial and economic constraints in a conflict with Iran than he does in a conflict with China. A conflict with Iran could change the game ahead of the election at a time when Trump is beset with the coronavirus and social unrest. His opinion polling would benefit from a rally around the flag, as it did in September 2019. The risk for Trump is that this bump may not last long. Americans are less concerned about Iran than China and Russia and Trump himself has benefited from American weariness of Middle Eastern wars. All we can say for certain is that the US election is of critical strategic importance to several major and minor powers. Trump’s allies and enemies know that the next six months offer their best chance to take actions that either affect the election or exploit the current alignment of US foreign policy relative to a Democratic Party alignment. While China probably prefers Biden, it can deal with either ruling party. Whereas Israel has a unique opportunity to advance its objectives under Trump and Iran has a clear imperative to remove Trump from office. Roukaya Ibrahim Editor/Strategist Geopolitical Strategy RoukayaI@bcaresearch.com Matt Gertken Vice President Geopolitical Strategist mattg@bcaresearch.com Footnotes 1 The damaged building was constructed in 2013 to be a site for the development of advanced centrifuges. Work there was stopped in 2015 as per requirements of the JCPA, but was restarted when the US withdrew from the deal in 2018. 2 Meanwhile a group of dissidents from within Iran’s military and security forces, calling themselves Homeland Cheetahs, claimed responsibility for the Natanz attack. However, it is possible that the claim was made with the intention to mislead. Please see Jiyar Gol, "Iran blasts: What is behind mysterious fires at key sites?" BBC News, July 6, 2020. 3 The draft US resolution bans Iran from supplying, selling, or transferring weapons after the October 18 expiration of the embargo. It bans UN member states from purchasing Iranian arms or permitting citizens to train or provide financial resources or assistance to Iran without Security Council approval. 4 This resolution, introduced by France, Germany, and the UK, refers to an undeclared uranium metal disc, potential fuel-cycle-related activities such as uranium processing and conversion, and suspected storage of nuclear material. Iran’s parliament responded by issuing a statement signed by 240 out of the 290 members which called the resolution excessive and requested that Iran halt voluntary implementation of additional protocol and change inspections 5 Iran’s state-run news agency IRNA published the following commentary in response to the Natanz explosion: "The Islamic Republic of Iran has so far tried to prevent intensifying crises and the formation of unpredictable conditions and situation … the crossing of red lines of the Islamic Republic of Iran by hostile countries, especially the Zionist regime and the US, means that strategy … should be revised." 6 In addition, 120 out of the 290 parliamentarians signed and delivered a motion to the presiding board of the assembly, requesting that Rouhani be summoned for questioning. The presiding board may not issue the summons and is unlikely to result in Rouhani’s impeachment as Khamenei has requested unity amid high foreign tensions. It nonetheless reflects Rouhani’s weakened position ahead of next year’s elections. 7 Hisham al-Hashemi, an advisor to Prime Minister Mustafa al-Kadhimi who had advised the government on reducing the influence of Iran-backed militias in Iraq, was killed on July 6, days after receiving threatening telephone calls from militias.

BCA Research's Emerging Markets Strategy service was recently asked what it will take for them to go long EM risk assets and currencies in absolute terms. EM equities, credit markets, and currencies are driven by three, or more recently four, factors. We…

China’s official manufacturing PMI ticked up to 50.9 in June from 50.6 in the previous month. The Caixin manufacturing PMI came in at 51.2 in June vs. 50.7 in May and beat the market expectation of 50.5. Both readings suggest that China’s manufacturing sector…

Feature Over the last several years when I travelled to Europe, I would meet with Ms. Mea, an outspoken client of the Emerging Markets Strategy service. We have published our conversations with Ms. Mea in the past and this semi-annual series has complemented our regular reports. She has challenged our views and convictions, serving as a voice for many other clients. In addition, these conversations have highlighted nuances of our analysis, for her and to the benefit of our readers. With travel restrictions in force, this time we had to resort to an online meeting with Ms. Mea. Below are the key parts of our conversation from earlier this week. Ms. Mea: Let’s begin with your main thesis, which over the past several years has been as follows: China’s growth drives EM business cycles and financial markets overall. Indeed, as long as China’s growth dithers, EM growth and asset prices languish. However, since the pandemic started China has stimulated aggressively and there are clear signs that the economy is recovering. The latest surge in Chinese share prices confirms that a robust recovery is underway. Why do you not think China’s economy is on the upswing? Answer: True, we believe China’s business cycle is instrumental to EM economies’ growth and balance of payments. We upgraded our outlook for Chinese growth in our May 28 report as the National People’s Congress set the objective for monetary policy in 2020 to significantly accelerate the growth rate of broad money supply and total social financing relative to last year. Indeed, broad money growth as well as both private and public credit have accelerated since April and will continue to increase (Chart I-1). Domestic orders have also surged though export orders are still languishing (Chart I-2). Chart I-1China: Money And Credit Will Continue Accelerating

China: Money And Credit Will Continue Accelerating

China: Money And Credit Will Continue Accelerating

Chart I-2China: Improvement In Domestic Orders But Not In Export Ones

China: Improvement In Domestic Orders But Not In Export Ones

China: Improvement In Domestic Orders But Not In Export Ones

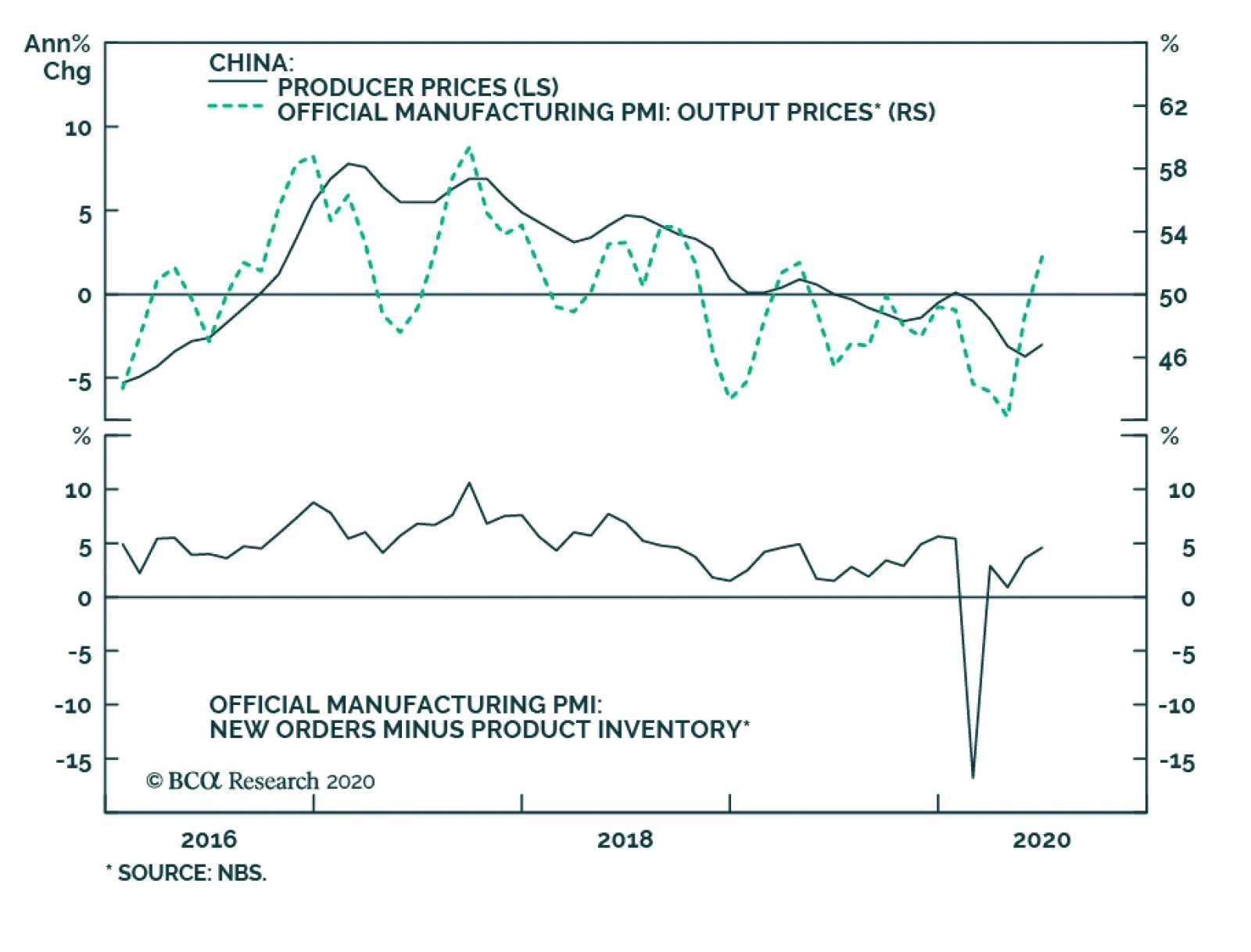

That said, financial markets, including the ones leveraged to China, have run ahead of fundamentals and a pullback is overdue. We have been waiting for such a setback to turn more positive on EM risk assets and currencies. Further, the snapback in business activity following the lockdown should not be confused with an economic expansion. As economies around the world reopened, business activity was bound to improve. Were any asset markets priced to reflect months or a whole year of closures? Even at the nadir of the global equity selloff in late March, we do not think risk assets were priced for extended lockdowns. The Chinese economy will likely eventually experience a robust expansion later this year but the nearterm outlook for global risk assets and commodities remains risky. In our view, the rally in global stocks and commodities has been much stronger than is warranted by the near-term economic conditions in a majority of economies around the world. In short, we have not been surprised at all by the economic data that has emerged since economies have reopened, but we have been perplexed by the markets’ response to these data. Even in China, which is ahead of all other countries in regards to the reopening and normalization of business activity, the level and thrust of economic activity remains worrisome. Specifically: China's manufacturing PMI new orders and the backlog of orders sub-components remain below the neutral 50 line (Chart I-3). The imports subcomponent of the manufacturing PMI has shown signs of peaking below the 50 line, portending a risk to industrial metals prices (Chart I-4). Chart I-3China Manufacturing PMI: Measures Of Orders Are Still Below 50

China Manufacturing PMI: Measures Of Orders Are Still Below 50

China Manufacturing PMI: Measures Of Orders Are Still Below 50

Chart I-4A Yellow Flag For Commodities

A Yellow Flag For Commodities

A Yellow Flag For Commodities

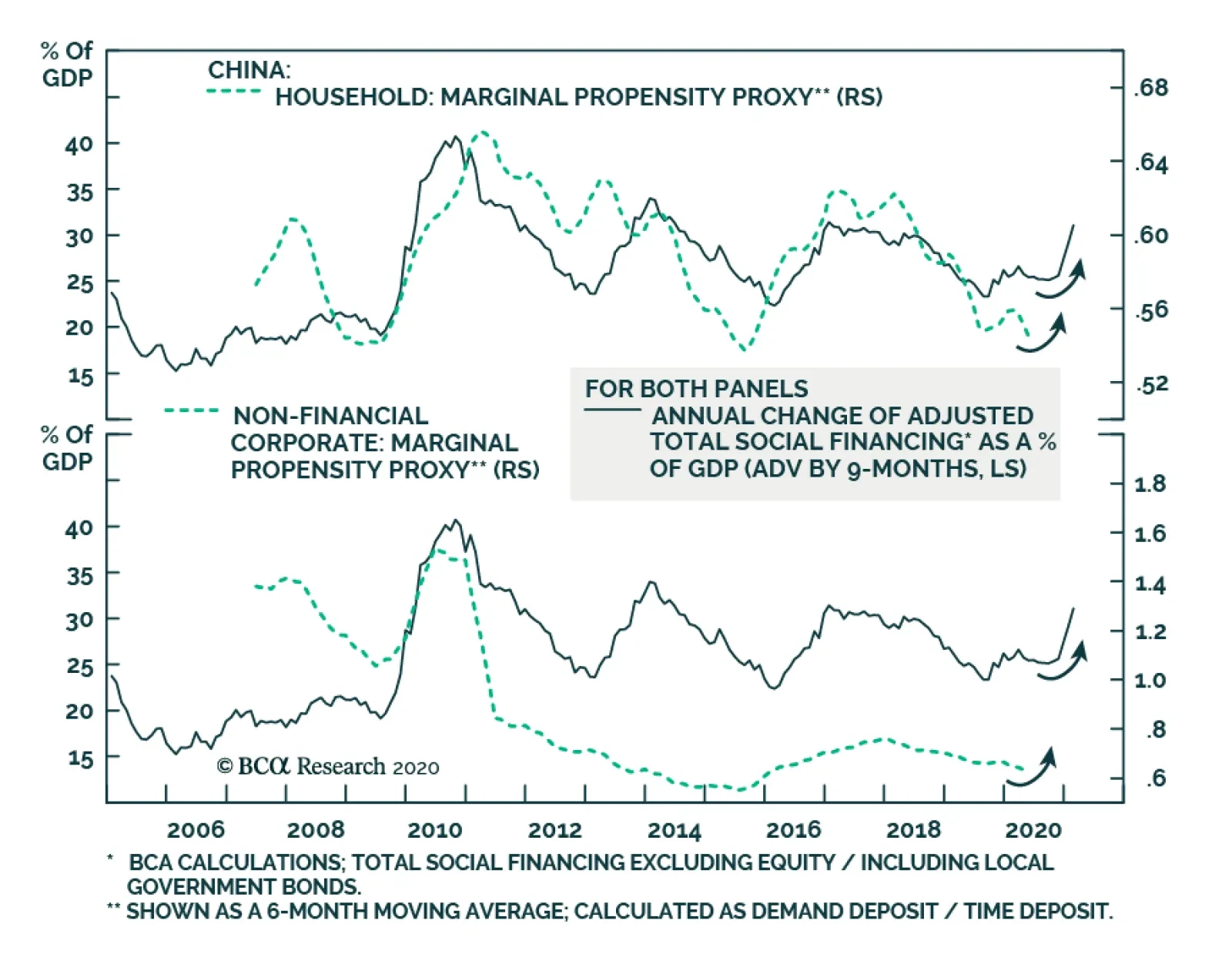

Marginal propensity to spend for both enterprises and households continues to trend lower (Chart I-5). These gauge the willingness of consumers and companies to spend and, hence, reflect the multiplier effect of the stimulus. These indicators contend that the multiplier so far remains low/weak. Finally, with the exception of new economy stocks (such as Ali-Baba and Tencent) that have been exceptionally strong worldwide, Chinese share prices leveraged to capital expenditure and consumer discretionary spending had not been particularly strong before last week, as illustrated in Chart I-6. Chart I-5Marginal Propensity To Spend Among Chinese Households And Enterprises

Marginal Propensity To Spend Among Chinese Households And Enterprises

Marginal Propensity To Spend Among Chinese Households And Enterprises

Chart I-6Chinese Stocks Had Been Languishing Till Late Outside New Economy Ones

Chinese Stocks Had Been Languishing Till Late Outside New Economy Ones

Chinese Stocks Had Been Languishing Till Late Outside New Economy Ones

In a nutshell, the Chinese economy will likely eventually experience a robust expansion later this year but the near-term outlook for global risk assets and commodities remains risky. As to EM risk assets, the key risk to our stance is a FOMO-driven rally buoyed by the “visible hand” of governments. Ms. Mea: What is your interpretation of the latest policy push in China for higher share prices? Is it also a part of the “visible hand” of government? Don’t you think this could create another strong multi-month run like it did in early 2015? Answer: Yes, this is one of many instances of the “visible hand” of governments around the world. It is not clear why Beijing is boosting investor sentiment and explicitly promoting higher share prices given how badly similar efforts in 2015 ultimately ended. At the moment, we can only speculate that one or several of the following reasons are behind this move: Beijing is preparing for an escalation in the US-China geopolitical confrontation ahead of the US presidential elections. This latter is highly probable in our opinion.1 To limit the impact of this confrontation on their economy, they want to ensure that the stock market remains in an uptrend. The same can be said for the US authorities. Apparently, the “visible hands” of both Washington and Beijing have and will continue to push share prices higher in their domestic markets. Robust equity markets will become a prominent feature of the geopolitical confrontation between the US and China. In the long run, however, this is a very negative phenomenon for the world because the two of the largest and most prominent stock markets could increasingly be driven by the “visible hand” of their governments rather than by fundamentals. As a result, equity markets could regularly send wrong price signals and will no longer serve as an efficient mechanism of capital allocation. Chart I-7Foreign Inflows Into China Have Accelerated This Year

Foreign Inflows Into China Have Accelerated This Year

Foreign Inflows Into China Have Accelerated This Year

Beijing has been luring foreign investors to buy onshore stocks and bonds and this strategy has become more vital in expectation of an escalation in the US-China confrontation. Chart I-7 shows that net inflows into onshore stocks and bonds have been surging. The more US investors buy into mainland markets, the more these investors will exercise pressure on the current and future US administrations to go soft on China. Like those US companies relying on Chinese demand, large US investment funds will have a notable exposure to Chinese financial markets and will accordingly lobby the White House and Congress to take a less adversarial stance toward China. This will reduce the maneuvering room of US politicians in this geopolitical confrontation. Finally, it is also possible that these latest media reports encouraging a bull market in China were not initiated by leaders in Beijing but were in fact spurred by mid-level bureaucrats. If that is the case, a full-blown mania akin to the one in 2015 will not be repeated and the latest frenzy surrounding Chinese stocks could end up being the final surge before a correction sets in. In brief, Chinese stocks, like other bourses worldwide, are in a FOMO-driven mania that might last for a while. Nevertheless, regardless of the direction of Chinese stocks in absolute terms, we reiterate our overweight stance on Chinese equities within the EM benchmark. Also, we have a strong conviction with respect to the merits of a long Chinese/short Korean stocks trade. Both these positions were initiated on June 18 before the latest surge in Chinese stocks. The “visible hands” of both Washington and Beijing have and will continue to push share prices higher in their domestic markets. Ms. Mea: What will it take for you to go long EM risk assets and currencies in absolute terms? Answer: EM equities, credit markets and currencies are driven by three, or more recently four, factors. We need to witness or foresee an imminent improvement in three out of four of these to go outright long. These factors include: (1) China’s business cycle and its impact on EM via global trade; (2) each individual EM country’s domestic fundamentals (inflation/deflation, balance of payments, return on capital, domestic economic cycles, monetary and fiscal policies, health of the banking system, domestic politics, etc.); (3) global risk-on and risk-off cycles that drive portfolio flows into EM. The direction of the S&P500 is an important trendsetter for these risk-on and risk-off cycles; (4) swings in geopolitical confrontation between the US and China. The first element – China’s impact on EM – is becoming positive. There could be a minor setback in mainland business cycles in the near term, but this should be used as a buying opportunity. As to structural problems in China like credit/money and property bubbles as well as the misallocation of capital, ongoing money and credit growth acceleration will fill in holes and kick the can down the road. That said, those structural problems will become even more challenging in the years to come. In short, Beijing is making credit, money and property bubbles even bigger. The second factor – domestic fundamentals in EM ex-China, Korea and Taiwan – remain downbeat. The COVID-19 outbreak has been out of control in a number of EM economies (Chart I-8). In addition, outside of China, Korea and Taiwan, EM fiscal stimulus has not been as large as in DM economies. Critically, the monetary transmission mechanism has been broken in several developing economies. In particular, central banks’ rate cuts have not translated to lower lending rates in real terms (Chart I-9). Chart I-8The COVID-19 Pandemic Has Not Peaked In Several Major EM Economies

The COVID-19 Pandemic Has Not Peaked In Several Major EM Economies

The COVID-19 Pandemic Has Not Peaked In Several Major EM Economies

Chart I-9Lending Rates Are Still High In EM ex-China, Korea And Taiwan

Lending Rates Are Still High In EM ex-China, Korea And Taiwan

Lending Rates Are Still High In EM ex-China, Korea And Taiwan

The basis is two-fold: First, banks saddled with non-performing loans are reluctant to bring down their lending rates and lend more; and second, the considerable decline in EM inflation has pushed up real lending rates (Chart I-9). The third variable driving EM financial markets – the S&P 500 – remains at risk of a material setback. If the S&P drops more than 10 or 15%, EM stocks, currencies and credit markets will also sell off markedly. Finally, there is the fourth aspect of the EM view – geopolitics – which could be critical in the coming months. The US-China confrontation will likely heighten leading up to the US elections. This will likely involve North and South Korea and Taiwan. Chart I-10EM ex-China, Korea And Taiwan: Stocks And Currencies

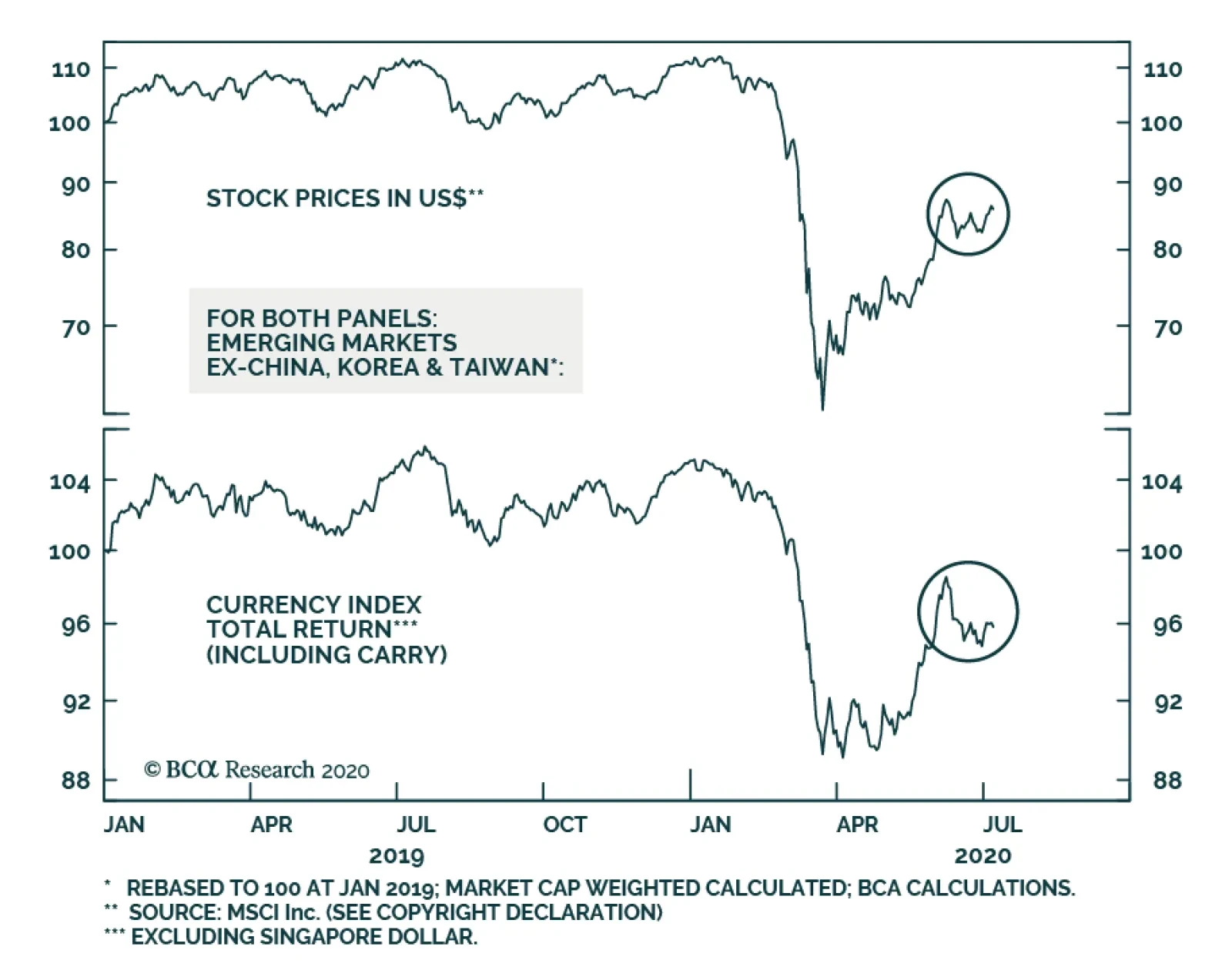

EM ex-China, Korea And Taiwan: Stocks And Currencies

EM ex-China, Korea And Taiwan: Stocks And Currencies

Chinese investable stocks as well as Korean and Taiwanese equities altogether make up 65% of the MSCI EM benchmark. Hence, a flareup in geopolitical tensions will weigh on these three bourses. Outside these markets, EM share prices and currencies have already rolled over (Chart I-10). In sum, out of the four factors listed above only the Chinese business cycle warrants an upgrade on overall EM. The other three drivers of the EM view are still negative. This keeps us on the sidelines for now. Importantly, we have been gradually moving our investment strategy from bearish to neutral on EM. Specifically, we: Took profits on the long EM currencies volatility trade on March 5. Took large profits on the long gold / short oil and copper trade on March 11. Booked gains on the short position in EM stocks on March 19. Recommended receiving long-term (10-year) swap rates (or buying local currency bonds while hedging the exchange rate risk) in many EMs on April 23. Upgraded EM sovereign credit from underweight and booked profits on our short EM corporate and sovereign credit / long US investment grade bonds strategy on June 4. The only asset class where we have not yet closed our shorts is EM currencies. In fact, we now recommend shifting our short in EM currencies (BRL, CLP, ZAR, TRY, KRW, PHP and IDR) from the US dollar to an equal-weighted basket of the Swiss franc, the euro and the Japanese yen. Unlike the March selloff, the dollar could depreciate even if the S&P 500 and global stocks drop. Ms. Mea: What is the rationale behind switching your short positions in EM currencies against the US dollar to short positions versus the Swiss franc, the euro and Japanese yen? Wouldn’t the selloff in global stocks drive the greenback higher? Answer: We have been bullish on the US dollar since 2011, consistent with our negative view on EM and commodities prices and recommendation of favoring the S&P 500 versus EM. What is making us question this strategy are the following, in order of importance: First, the Federal Reserve is monetizing US public and some private debt. The amount of US dollars is surging. Meanwhile, the pace of broad money supply growth is much more timid in the euro area, Switzerland and Japan. Broad money growth is 23% in the US, 9% in the euro area, 2.5% in Switzerland, 5% in Japan and 11% in China. This will reduce investors’ willingness to hold dollars as a store of value, incentivizing them to switch to other DM currencies. Second, the pandemic is out of control in the US and this will damage its near-term growth outlook. More fiscal stimulus and more debt monetization will be required to revive the economy. Third, the Fed will not hike interest rates even if inflation rises well above their 2% target in the next several years. This implies that the Fed will prefer to be behind the inflation curve in the years to come, which is bearish for the greenback. Finally, the yen and the euro as well as EM currencies are cheaper than the US dollar (Chart I-11 and Chart I-12). Chart I-11The US Dollar Is Expensive, The Yen Is Cheap

The US Dollar Is Expensive, The Yen Is Cheap

The US Dollar Is Expensive, The Yen Is Cheap

Chart I-12EM ex-China, Korea And Taiwan: Currencies Are Cheap

EM ex-China, Korea And Taiwan: Currencies Are Cheap

EM ex-China, Korea And Taiwan: Currencies Are Cheap

The broad trade-weighted US dollar has yet to break down as per the top panel of Chart I-13, but we are becoming nervous about it. Unlike the March selloff, the dollar could depreciate even if the S&P 500 and global stocks drop. Ms. Mea: That is interesting. Has there ever been an episode where the US dollar depreciated while the S&P 500 sold off? Answer: Yes, it occurred in late 2007 and H1 2008. The 2007-08 bear market in global stocks can be split into two periods. During the initial phase of that bear market, the US dollar depreciated substantially despite the drawdowns in global equity and credit markets (Chart I-14, top and middle panels). Chart I-13Trade-Weighted Dollar And Asian Currencies: At A Critical Juncture

Trade-Weighted Dollar And Asian Currencies: At A Critical Juncture

Trade-Weighted Dollar And Asian Currencies: At A Critical Juncture

Chart I-14In Late 2007 And H1 2008: The US Dollar Fell Amid An Equity Bear Market

In Late 2007 And H1 2008: The US Dollar Fell Amid An Equity Bear Market

In Late 2007 And H1 2008: The US Dollar Fell Amid An Equity Bear Market

EM stocks performed in line with DM ones during the first phase (Chart I-14, bottom panel). The economic backdrop was characterized by the US recession and US banks tightening credit. In fact, EM growth was still robust during that phase even though the US economy was shrinking. Remarkably, commodities prices were surging – oil reached $140 per a barrel and copper $4 per ton in June 2008. The second phase of that bear market commenced in autumn of 2008 when Lehman went bust. The orderly bear market in global stocks gave way to an acute phase – a crash in all global risk assets. Business activity collapsed worldwide and the US dollar surged. In the current cycle, the order will likely be the reverse of the 2007-08 bear market. March 2020 witnessed a crash in global risk assets and the global economy plunged similar to the second phase of the 2007-08 bear market while the US dollar surged. The second stage of this recession could resemble the first phase of the 2007-08 bear market. There will be neither worldwide lockdowns nor a crash in business activity. However, the level of activity might struggle to recover as rapidly as markets have priced in or there might be relapses in economic conditions in certain parts of the world. This is especially true for the US and other countries where the pandemic has not been effectively contained. On the whole, the second downleg in the S&P 500 and global stocks will be less dramatic but could last for a while and still be meaningful (more than 10-15%). Critically, unlike the March 2020 selloff, the greenback will likely struggle during this episode for the reasons we outlined above. Ms. Mea: What about overweighting EM equities and credit versus their DM peers? Will EM equities, credit and currencies underperform their DM peers in the potential selloff that you expect? Wouldn’t USD weakness help EM risk assets to outperform even in a broad risk selloff? Answer: Yes, we can see a scenario where EM stocks and credit markets perform in line or better than their DM peers in a potential selloff. The key is the dollar’s dynamics. If the dollar rebounds, EM stocks and credit markets will underperform their DM counterparts. If the dollar weakens during this selloff, EM stocks and credit will likely perform in line with or better than their DM peers. In sum, a technical breakdown in the broad trade-weighted dollar and a breakout in the emerging Asian currency index – both shown in Chart I-13 – would lead us to upgrade our EM allocation in both global equity and credit portfolios. For now, we are only switching our shorts in EM currencies from the US dollar to an equally-weighted basket of the Swiss franc, the euro and the Japanese yen. Ms. Mea: What are some of your other current observations on financial markets? Answer: The breadth and thrust of this global equity rally has already peaked and is weakening. It is just a matter of time before a narrowing breadth translates into lower aggregate stock indexes for both EM and DM equities as illustrated by our advance-decline lines in Chart I-15. Chart I-15EM and DM Equity Breadth Measures Have Rolled Over

EM and DM Equity Breadth Measures Have Rolled Over

EM and DM Equity Breadth Measures Have Rolled Over

Chart I-16Cyclicals And High-Beta Stocks Have Been Struggling

Cyclicals and High-Beta Stocks Have Been Struggling

Cyclicals and High-Beta Stocks Have Been Struggling

Consistently, there has already been a decoupling between various sectors and industries. The rally has been solely focused on tech and new economy stocks. Equity prices in China and Taiwan have been surging while the rest of the EM equity index has been languishing. In the DM equity space, global industrials, US high-beta stocks and micro caps have already rolled over (Chart I-16). Further, our Risk-On/Safe-Haven currency index is flashing red for EM equities (Chart I-17). Chart I-17A Red Flag For EM Equities?

A Red Flag For EM Equities?

A Red Flag For EM Equities?

Chart I-18Long Gold / Short Stocks

Long Gold / Short Stocks

Long Gold / Short Stocks

Finally, EM share prices have outperformed DM stocks since late May mostly due to the sharp rally in Chinese, Korean and Taiwanese stocks. Hence, the breadth of EM equity outperformance has been subdued. Ms. Mea: To wrap up our conversation, I want to ask you what is your strongest conviction trade for the coming months? Answer: Our strongest conviction trade is long gold / short global or EM stocks (Chart I-18). This trade will do well regardless of the direction of global share prices, the US dollar, and bond yields. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Footnotes 1 Please see Geopolitical Strategy Special Report "Watch Out For A Second Wave (Of US-China Frictions)," dated June 10, 2020, available at gps.bcaresearch.com Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

BCA Research's China Investment Strategy service concludes that although the intensity of the PBoC’s monetary easing may start to taper in H2, the central bank is likely to stay on the easing course and keep liquidity conditions ample. Bank lending to the…