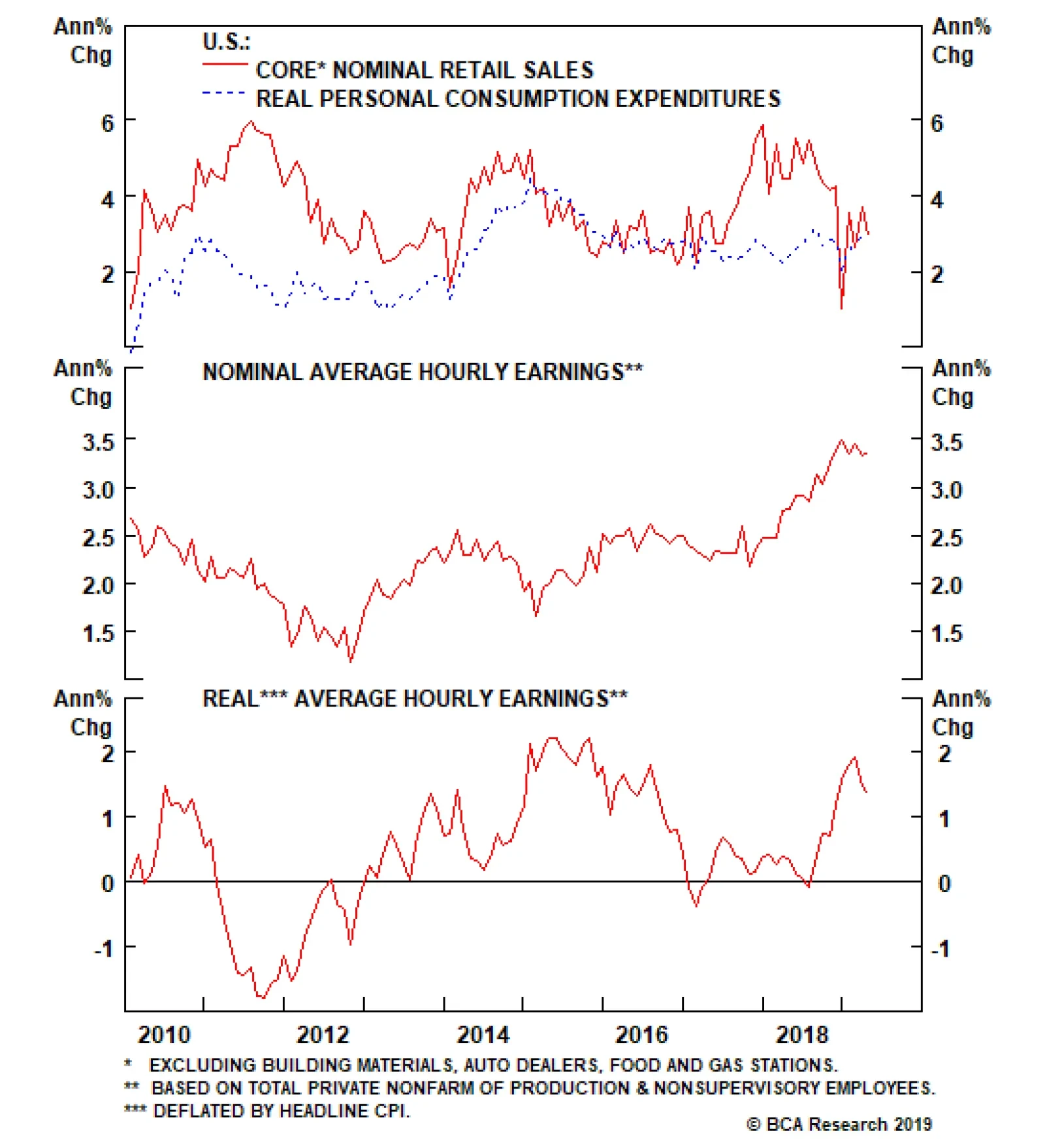

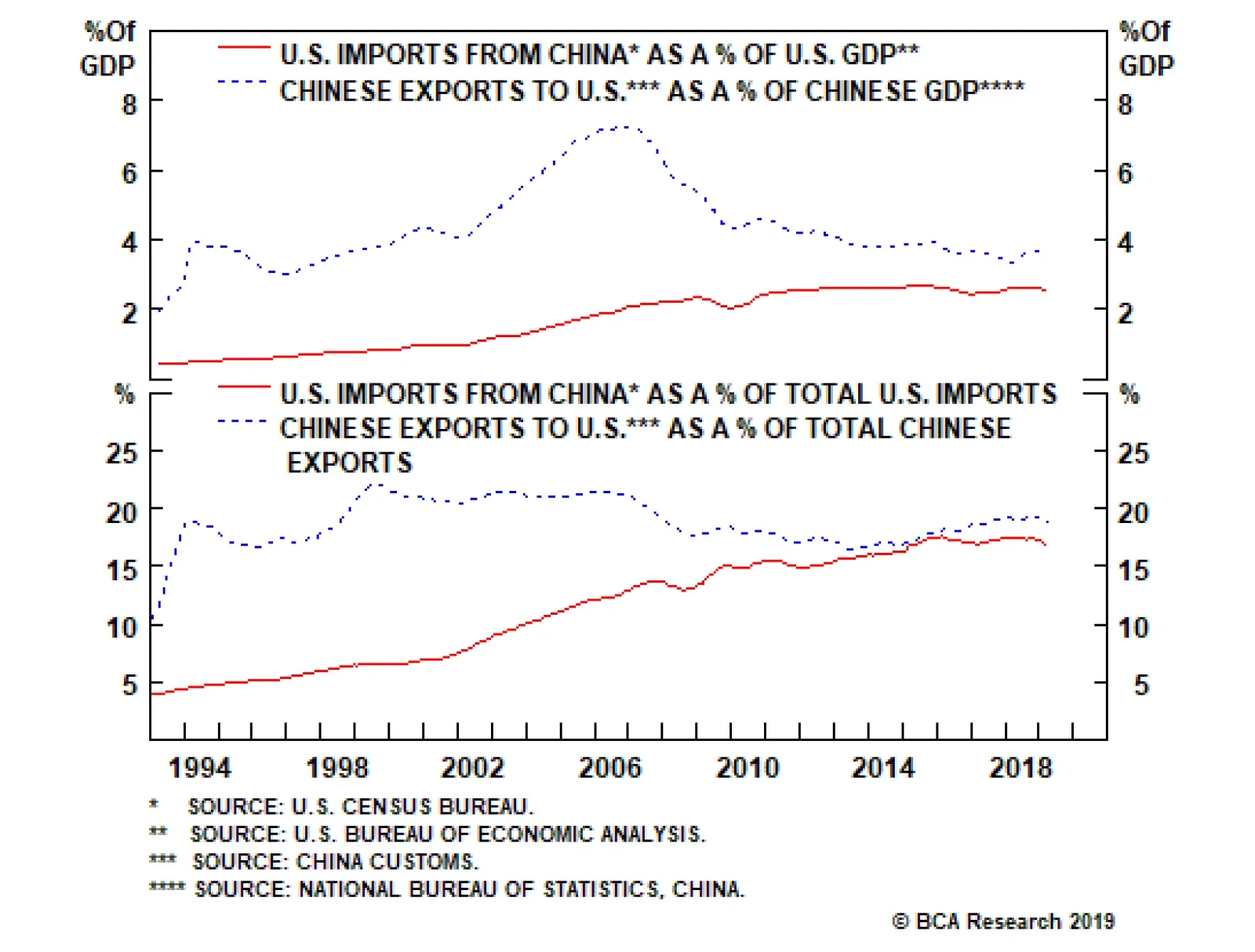

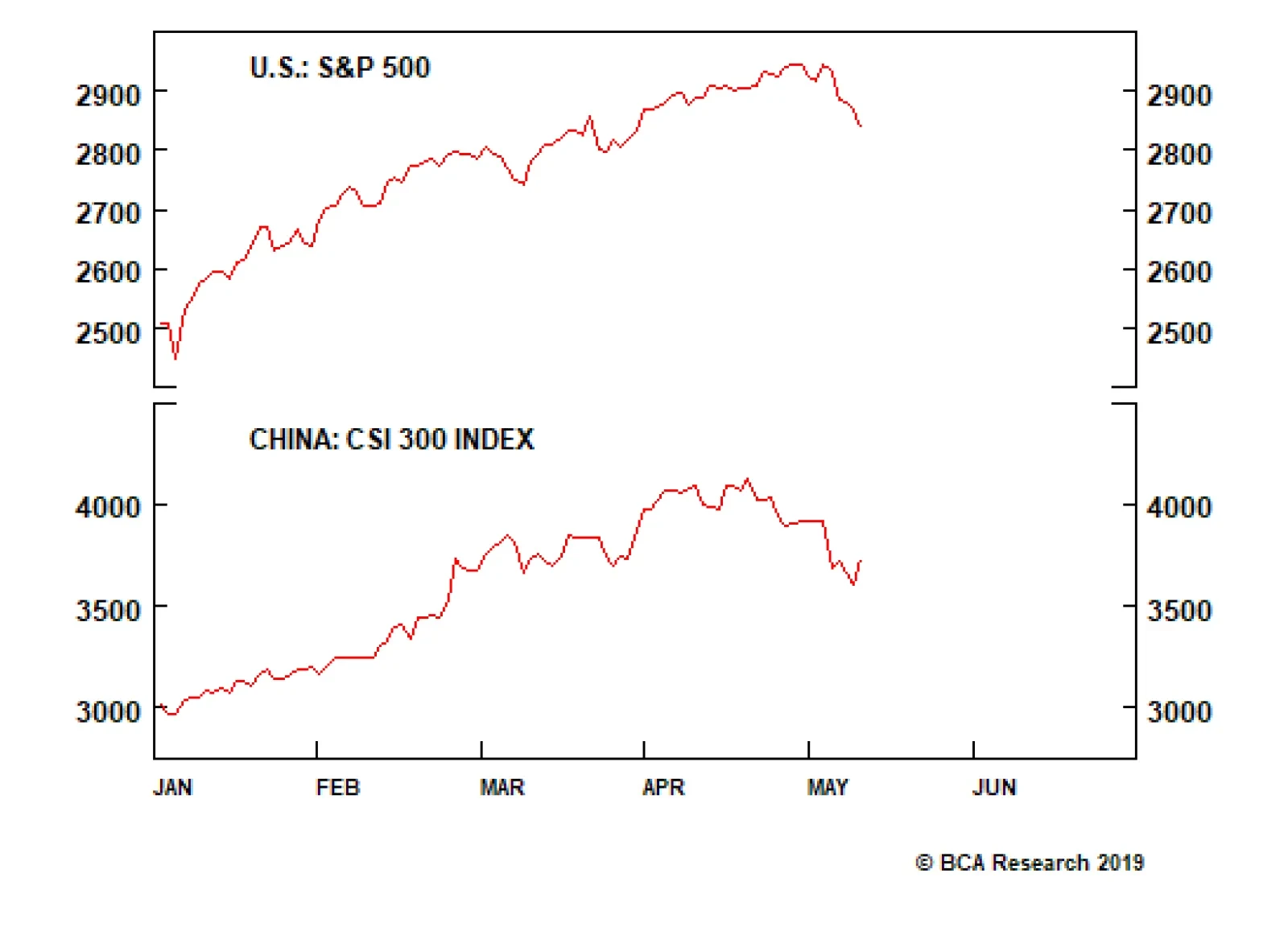

Highlights Looking past the day-to-day noise of trade-related announcements, we view the underlying odds of an actual trade agreement this year to have fallen below 50%. For the purposes of investment strategy, China-exposed investors should now simply assume that the U.S. proceeds with 25% tariffs on all imports from China. Given this, investors should stop focusing strictly on the odds of trade war, and should instead start focusing on the likely net impact of the tariff shock and China’s inevitable policy response. Simulated and empirical estimates of the impact of a 25% increase in tariffs affecting all U.S.-China trade suggest that economic conditions in China are likely to deteriorate to 2015/2016-like levels. This implies that a 2015/2016-style policy response will again be required in order for policymakers to be confident that the shock will be overcome. The preference of policymakers is to prevent another significant episode of releveraging, but the constraints facing policymakers suggest that one is unlikely to be avoided. We see a meaningful chance that this tension will be resolved by a classic market “riot” over the coming 3 months as financial markets force reluctant policymakers to capitulate. We would not recommend a long position in Chinese stocks, either in absolute terms or relative to the global benchmark, for investors with a time horizon of less than 3 months. However, over a strictly cyclical (i.e. 6-12 month) time horizon, we would recommend staying long/overweight on the basis that policymakers will ultimately respond as needed. We recommend investors hedge the inherent RMB exposure from a long US$ cyclical position in Chinese stocks by opening a long USD-CNH trade. Feature U.S. and Chinese negotiators failed last week to secure an agreement deferring the threatened increase in the second round tariff rate.1 The tariffs increased on Thursday at midnight for goods not already in transit to the U.S. (effectively doubling the existing tariffs), which was followed by the inevitable retaliation by China on Monday (scheduled to take effect on June 1). The retaliation, coupled with President Trump’s earlier warning that China should not do so, was taken by investors as a sign that 25% tariffs on all goods imported from China will soon be in place. As we go to press, the S&P 500, Hang Seng China Enterprises Index, and the CSI 300 are down 3.5%, 7%, and 6.9%, respectively, since President Trump’s May 5 tweet (Chart 1). Chart 1Investors Are Starting To Price In 25% Tariffs Affecting All U.S.-China Trade

Investors Are Starting To Price In 25% Tariffs Affecting All U.S.-China Trade

Investors Are Starting To Price In 25% Tariffs Affecting All U.S.-China Trade

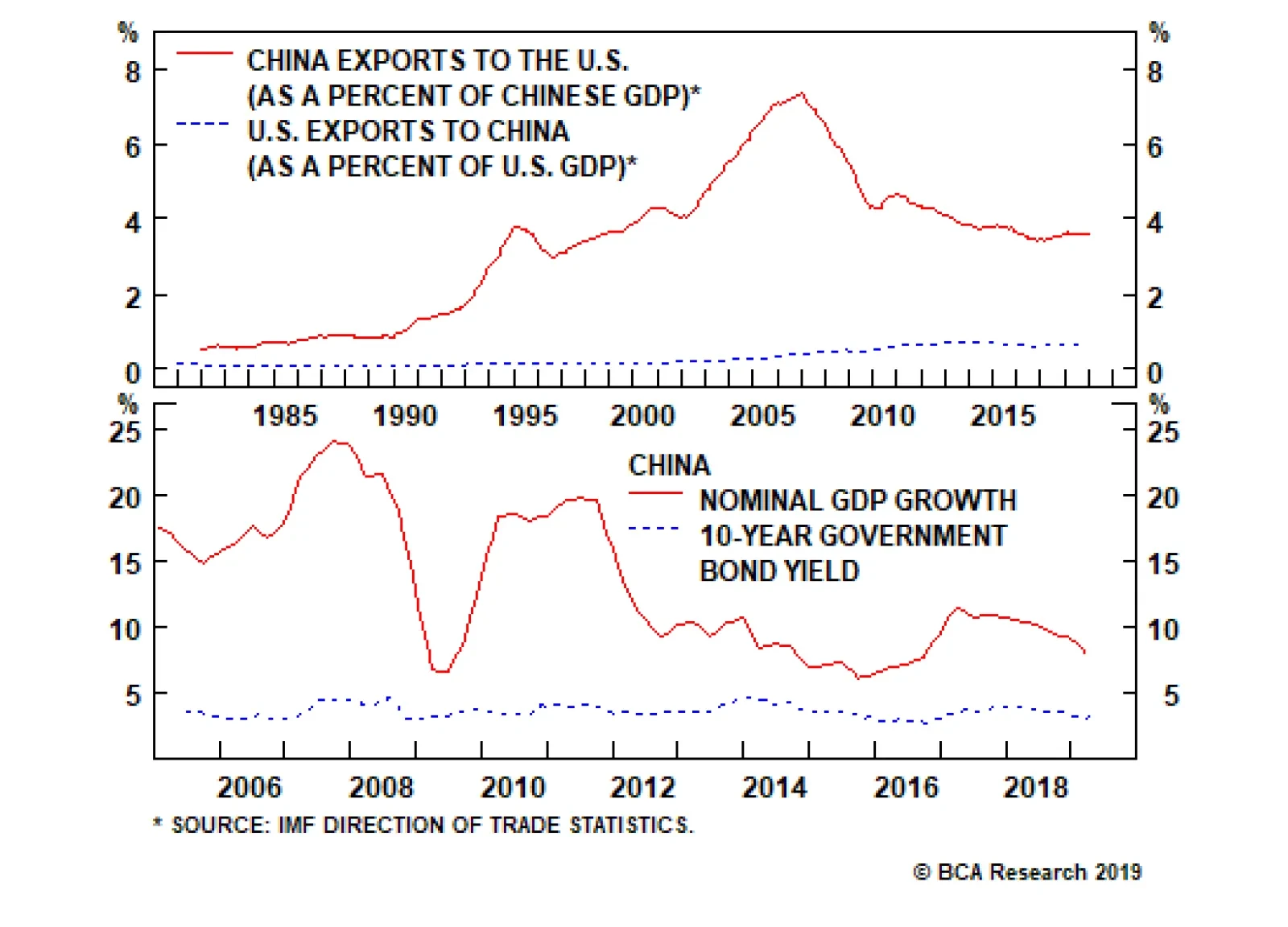

Stimulus Minus Shock Holding all else equal, the events of the past two weeks are strictly negative for Chinese economic growth and would thus justify a decisively bearish outlook for Chinese stock prices after the rally that has taken place over the past six months. However, all is not equal, because a substantial deterioration in the export outlook will invariably cause a response from Chinese policymakers. Over the coming few weeks, global investors are likely to remain highly focused on developments and announcements related to the trade conflict. But at this point, our geopolitical team believes that the conclusion of an actual trade agreement this year is now only a 40% probability. This underscores that China-exposed investors should, for the purposes of investment strategy, simply assume that the U.S. proceeds with 25% tariffs on all imports from China, and should broaden their focus to the outcome of a simple formula that describes the potential net outcome of this event. Two simple scenarios concerning this formula are outlined below: Scenario 1 (Bullish): Stimulus – Shock > 0 Scenario 2 (Bearish): Stimulus – Shock ≤ 0 In scenario 1, the impact of China’s reflationary efforts more than offsets the negative shock to aggregate demand from the sharp decline in exports to the U.S. In this scenario, investors should actually have a bullish cyclical outlook for China-related assets, even if the near-term outlook is deeply negative. Scenario 2 denotes a bearish outcome where China’s reflationary response is not larger than the magnitude of the shock, which includes a circumstance where the impacts are exactly offsetting (because of the higher uncertainty, and thus risk premium, that this would entail). “Solving” The Formula In order to “solve” this formula, investors need answers to the following three questions: What is the size and disposition of the likely shock to China’s economy in a full-tariff scenario? What kind of reflationary response is required in order to offset this shock? What are the odds that policymakers will deliver the required response? Simulated and empirical estimates of a 25% increase in tariffs affecting all U.S.-China trade suggest a sizeable economic impact. Charts 2 & 3 provide the IMF’s perspective on the first question. The charts show the simulated impact of a 25% increase in tariffs affecting all U.S.-China trade, and they estimate the near-term impact for China to be -1.25% for real GDP (-0.5% over the long-run) and -3.5% for real exports (-4.5% to -5.5% over the long run).

Chart 2

Chart 3

A recent IMF working paper came up with a more benign estimate of the first year impact, but a sizeable second year impact and a similar estimate of the long-term ramifications of tariff increases.2 Using a dataset with wide time and country coverage, the aggregate results of the study imply that Chinese output is only likely to fall about 0.2% in the year following the tariff increase. However, the cumulative shock to output increased sharply to roughly 1.6% in the second year of the tariff increase, with a negative yearly impact to output persisting for 5 years (with an average annual impact of -0.6% over the whole period, somewhat higher than the estimates shown in Charts 2 & 3). At the 90% confidence interval, the author’s estimates show that a tariff increase of this magnitude would imply a -1.7% average impact on output per year in the first two years following the increase. Chart 4The IMF's Shock Estimates Suggest A Serious Hit To China's Economy

The IMF's Shock Estimates Suggest A Serious Hit To China's Economy

The IMF's Shock Estimates Suggest A Serious Hit To China's Economy

In order to answer the second question, investors need to have some sense of the relative magnitude of the estimates noted above. Chart 4 provides some perspective and highlights that the estimates above, were they to materialize, would do two things: Taking Chinese real GDP data at face value, it would cause the largest deceleration in China’s real GDP growth rate since 2012, when the economy slowed significantly and authorities responded forcefully. Based on the most recent data for Chinese real export growth, a 3.5% deceleration in export volume would push its growth rate to its lowest level since the global financial crisis. In practice, we doubt that China’s reported real GDP growth rate accurately reflects what occurred in 2015, and it is very possible that a similar deceleration happened in that year. However, economic similarity to the 2015/2016 episode implies that a similar policy response may also be required, a proposition that is supported by our MSCI China Index earnings recession model. Table 1 shows a set of earnings recession probabilities, based on a model that we presented in two recent reports.3 The scenarios express the odds as a function of new credit to GDP and our calculation of China’s export weighted exchange rate, and assume a substantial decline in the new export orders component of the official manufacturing PMI, and flat momentum in forward earnings. Table 1Our Earnings Recession Model Suggests That A 2015/2016 Style Response Is Needed To Counter This Shock

Simple Arithmetic

Simple Arithmetic

The table clearly highlights that a significant further acceleration in new credit to GDP, coupled with a meaningful decline in the exchange rate, is needed in order to stabilize the earnings outlook. We have previously related stability in the outlook for earnings to stability in the economy itself, given the close correlation between Chinese investment-relevant economic activity and the earnings cycle (Chart 5). Given that new credit to GDP peaked at 31.5% during the 2015/2016 episode, it seems reasonable to conclude that a 2015/2016-style policy response will again be required in order for policymakers to be confident that the shock will be overcome. Policymaker Preferences Vs. Constraints This brings us to our third question: What are the odds that policymakers will deliver the stimulus required to confidently overcome the upcoming shock? It seems reasonable to conclude that a 2015/2016-style policy response will again be required in order for policymakers to be confident that the shock will be overcome. If the answer was only dependent on the preferences of policymakers, the odds would be low. China has relied heavily on credit to stimulate its economy over the past decade, and Chart 6 highlights that this has come at a high cost. The BIS’ estimate of the debt service ratio of China’s private non-financial sector is already extraordinarily high relative to other countries, and another round of meaningful re-leveraging will just make this problem even worse. Chart 5Earnings Stability = Economic ##br##Stability

Earnings Stability = Economic Stability

Earnings Stability = Economic Stability

Chart 6Further Leveraging Will Undoubtedly Make A Big Problem Even Worse

Further Leveraging Will Undoubtedly Make A Big Problem Even Worse

Further Leveraging Will Undoubtedly Make A Big Problem Even Worse

We documented in detail how this has created the risk of a debt trap for China’s state-owned enterprises in an August Special Report,4 and have presented evidence arguing that China’s policymakers appear to have good economic reasons to try and shift China’s economy away from extremely high rates of investment towards more consumption.5 This implies that restraining credit growth to avoid further leveraging has been a reasonable policy objective during periods of relative economic stability. However, policy decisions cannot be made in a vacuum, and this is true even in the case of China. As such, instead of preferences, investors should be focused on policymaker constraints in judging likely policy actions. Given the potential for second round effects, Chinese policymakers need to calibrate their policy response to ensure a positive net impact of the stimulus minus the shock. In our view, three factors point to the conclusion that Chinese policymakers face serious economic constraints in setting their policy response: Charts 2-4 highlighted that 25% tariffs on all U.S.-China trade would constitute a meaningful shock, but it is also the case that this shock would be coming at a time when Chinese economic momentum is already relatively weak. This suggests that policymakers will have to act quickly and decisively to put a floor under economic activity. Charts 7 & 8 suggest that there are meaningful second round effects on Chinese domestic investment from external sector shocks, which raises the possibility that the impact on Chinese economic activity may be larger than Charts 2-4 suggest. Chart 7 shows that while the contribution to official real GDP growth from net exports is small, Chart 8 shows that past changes in net export contribution are reasonably correlated with subsequent changes in the contribution to growth from gross capital formation. While it is possible that this relationship is not actually causal, taking it at face value implies that the IMF’s estimate of the impact on output could be exceeded if the contribution to growth from net exports declines by 0.4% or more (holding the contribution to growth from final consumption expenditure constant). Since 2018’s change in net export contribution declined by three times this amount (1.2%), the downside risks to domestic investment from effectively quadrupling U.S. import tariffs are clear. China does not have a flexible labor market, and its political system is highly sensitive to significant job losses. Chart 9 shows that the employment situation has already seriously deteriorated in lockstep with actual economic activity, further underscoring the need for policymakers to act urgently.

Chart 7

Chart 8

Chart 9The Employment Situation Is Already Deteriorating, And Will Do So Further

The Employment Situation Is Already Deteriorating, And Will Do So Further

The Employment Situation Is Already Deteriorating, And Will Do So Further

We are open to the idea that policymakers may be able to devise a stimulative response of similar reflationary magnitude to the 2015/2016 episode without resorting to a major credit overshoot, but we are currently unable to articulate what it might be. This is an area of ongoing research for BCA’s China Investment Strategy service, but for now we assume that a credit overshoot remains the ultimate line of defense for China’s policymakers that will be deployed if the pursuit of alternative strategies fail to quickly stabilize economic activity. Investment Strategy Conclusions In our view, focusing on policymaker constraints rather than their preferences is much more likely to guide investors towards the right strategy conclusions over a 6-12 month time horizon. However, in the near-term, policy mistakes can occur, and are much more likely to occur if policymakers react to the imposition of constraints rather than anticipate their arrival. Over the coming three months, we see meaningful odds that Chinese policymakers remain reluctant to allow another episode of significant releveraging in the economy. If we are correct in our assessment of the damage that the tariff shock is likely to cause, this would set up a classic market “riot”, where policymakers are forced by financial markets to capitulate and respond forcefully to the seriousness of the economic situation. Further RMB weakness is likely. Investors should hedge their exposure and go long USD-CNH. Chart 10Investors Have A Green Light To Bet On A Lower RMB

Investors Have A Green Light To Bet On A Lower RMB

Investors Have A Green Light To Bet On A Lower RMB

Given this, we would not recommend a long position in Chinese stocks, either in absolute terms or relative to the global benchmark, for investors with a time horizon of less than 3 months. However, over a cyclical (i.e. 6-12 month) time horizon, we would recommend staying long/overweight on the basis that policymakers will ultimately deliver the stimulus required to more than offset the upcoming shock to external demand. This means that our long MSCI China Index, MSCI China A onshore index, and MSCI China Growth index trades relative to the global benchmark are explicitly cyclical in orientation, and may suffer meaningful further losses over the coming few months before ultimately recovering. As a final point, Table 1 highlighted that a meaningful decline in the exchange rate is likely required in order to stabilize the earnings outlook. Chart 10 shows that currency weakness persisted well past the trough in relative Chinese investable equity performance during the 2015/2016 episode, and we would expect a similar result in the current environment given the nature of the shock. As such, we recommend investors hedge the inherent RMB exposure from a long US$ cyclical position in Chinese stocks by opening a long USD-CNH trade today, with high odds of a break above 7 in the coming weeks. Jonathan LaBerge, CFA, Vice President Special Reports jonathanl@bcaresearch.com Footnotes 1 The first, second, third “round” of tariffs reference the $50/$200/$300 billion tranches of imported goods subject to U.S. tariff announcements since last summer. 2 IMF Working Paper WP/19/9, “Macroeconomic Consequences of Tariffs”, by Davide Furceri, Swarnali A. Hannan, Jonathan D. Ostry, and Andrew K. Rose. 3 Please see China Investment Strategy Special Report “Six Questions About Chinese Stocks,” dated January 16, 2019, and Weekly Report “A Gap In The Bridge,” dated January 30, 2019 available at cis.bcaresearch.com. 3 Please see China Investment Strategy Special Report “Chinese Policymakers: Facing A Trade-Off Between Growth And Leveraging,” dated August 29, 2018, available at cis.bcaresearch.com. 4 Please see China Investment Strategy Weekly Report “Is China Making A Policy Mistake?,” dated October 31, 2018, available at cis.bcaresearch.com. Cyclical Investment Stance Equity Sector Recommendations