Emerging Markets

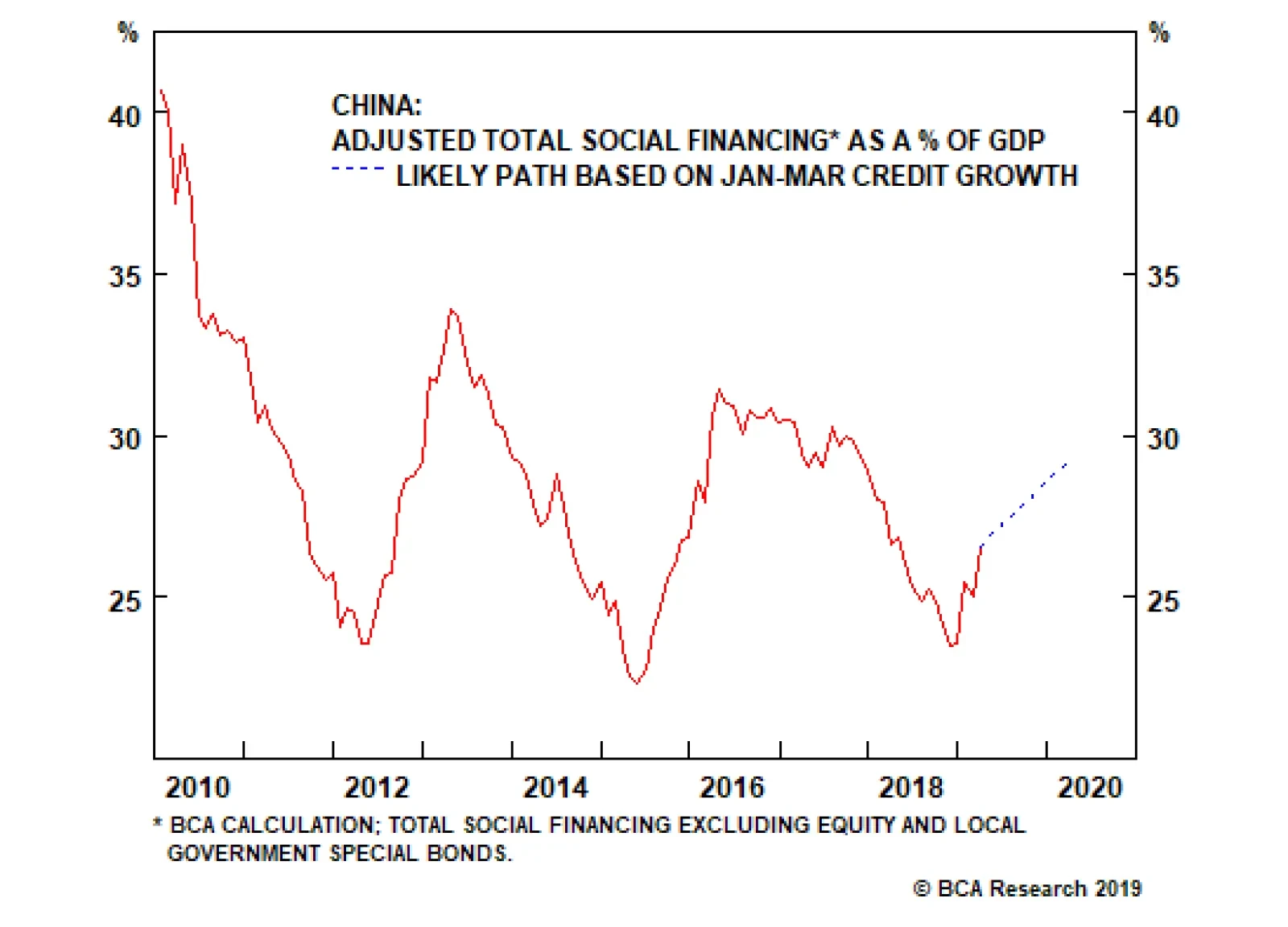

Highlights Chinese credit origination surpassed expectations in March. Credit growth is now clearly trending higher, and the latest data suggest that economic activity is rebounding. This bodes well for global growth. The conventional wisdom is that China’s releveraging efforts represent “short-term gain for long-term pain.” We disagree. For the most part, Chinese releveraging is inevitable, desirable, and sustainable. Credit growth is inevitable because rising debt is necessary for transforming the country’s copious savings into fixed-asset investment. It is desirable for ensuring that GDP growth stays close to trend. It is broadly sustainable because the interest rate at which the government and much of the private sector are able to borrow is well below the economy’s growth rate. In fact, under a plausible set of assumptions, faster credit growth in China could lead to a lower debt-to-GDP ratio. Stronger global growth later this year should weaken the U.S. dollar. We are closing our long DXY trade for a carry-adjusted gain of 16.4% and exiting our long USD/CNY trade for a loss of 3.1%. We are also taking profits on our short AUD/CAD, short EUR/CAD, and short EUR/RUB trades of 1.6%, 3.9%, and 8.6%, respectively, and initiating two new currency trades: short USD/RUB and long EUR/JPY. The combination of a weaker dollar and faster Chinese growth should benefit EM and European stocks. Gold hit our limit buy order of $1275/ounce and we are now long the yellow metal. Feature A Blockbuster Month For Chinese Credit Growth After turning cautious for about six months, we moved back to being bullish on global equities in late December. We also sold our put on the EEM ETF on January 3rd for a gain of 104% in anticipation of a wave of Chinese credit stimulus. Credit growth blew past expectations in January, but surprised on the downside in February. This made the March release particularly important. In the end, the March data did not disappoint those who were hoping for a solid reading. New CNY loans rose by RMB 1690 billion, above Bloomberg consensus estimates of RMB 1250 billion. Our adjusted aggregate financing measure, which excludes a number of items such as equity financing but includes local government bond issuance, rose by 12.3% year-over-year, up from 11.6% in February (Chart 1). China’s credit impulse leads the import component of its manufacturing PMI (Chart 2). The credit impulse bottomed in November 2018, which should feed into higher imports over the coming months. This week’s release of better-than-expected data on industrial production, retail sales, and housing activity all suggest that the rebound in Chinese growth is already afoot. Chart 1Chinese Credit Growth Is Rebounding...

Chinese Credit Growth Is Rebounding...

Chinese Credit Growth Is Rebounding...

Chart 2...Which Should Bode Well For Global Exports To China

...Which Should Bode Well For Global Exports To China

...Which Should Bode Well For Global Exports To China

Short-Term Gain For Long-Term Pain? At times like these, the bears are always ready with their standby argument: Sure, China may be stimulating, but all that credit growth will just make the debt bubble even bigger. Once the bubble bursts, there will be hell to pay. Long-term investors should steer clear of any growth-sensitive assets. It is a seductive argument. But it is wrong. Chinese releveraging is: 1) inevitable; 2) desirable; and 3) sustainable. The fundamental macroeconomic problem that China faces is that it consumes too little of what it produces. 1. Chinese Debt Growth Is Inevitable The fundamental macroeconomic problem that China faces is that it consumes too little of what it produces. The result is a national savings rate of 45%, by far the highest of any major economy (Chart 3). Chart 3China Still Saving A Lot

China Still Saving A Lot

China Still Saving A Lot

Chart 4From Exporting Savings To Investing Domestically And Building Up Debt

From Exporting Savings To Investing Domestically And Building Up Debt

From Exporting Savings To Investing Domestically And Building Up Debt

There was a time when China was able to export a large part of its excess production. Its current account surplus reached nearly 10% of GDP in 2007. As its economy has grown in relation to the rest of the world, running massive trade surpluses has become more difficult. This is especially true today, when the country is being targeted by the Trump administration and much of the international community for alleged unfair trade practices. As China’s ability to churn out large current account surpluses declined, the government moved to Plan B: propping up growth by recycling the country’s copious savings into fixed-asset investment. This process saw households park their savings in banks and other financial institutions which, in turn, lent the money out to companies and local governments in order to finance various investment projects. Not surprisingly, debt levels exploded higher (Chart 4). As China’s population ages and more workers leave the labor force, savings will decline. However, this is likely to be a slow process. In the meantime, further debt growth is inevitable. 2. Chinese Debt Growth Is Desirable In an ideal world, Chinese households would consume more of their incomes, leaving only enough savings to finance high-quality private and public investment projects. That is not the world we are living in. In a far-from-ideal world, we need to think about second-best solutions. Yes, a sizable share of Chinese investment spending goes towards projects of dubious value. Yet, the same could have been said about Japan’s fabled “bridges to nowhere.” One may regard the construction of a seldom-used bridge as a misallocation of capital. But what is the counterfactual? If the bridge had not been built, would the workers have found productive work? If not, then there also would have been a misallocation of capital – human capital – which is arguably a much more serious problem. In any case, keep in mind that the rate of return on private investment depends on the state of the economy. If an economy is suffering from chronic lack of demand, only the most worthwhile projects will be undertaken. As the economic outlook improves, the set of viable projects will expand. It is only when all excess private-sector savings have been depleted, and interest rates are rising, that public spending starts to crowd out private investment. 3. Chinese Debt Growth Is Sustainable Even if one accepts the proposition that China needs continued debt growth to maintain full employment, is it still possible that all this additional debt will push the economy into a full-blown debt crisis? Most self-professed “serious-minded” observers would say yes. But then again, many of these same observers were predicting that Japan was heading for a debt crisis when government debt reached 100% of GDP in the late 1990s. Today, Japan’s government debt-to-GDP ratio stands at about 240% of GDP, and yet interest rates remain at rock-bottom levels. China will avoid a debt crisis for the same reason Japan has been able to avoid one. Much of China’s debt stock is composed of state-owned enterprise, local government, and other forms of quasi-public sector debt. Credit policy in China is often indistinguishable from fiscal policy. Given the abundant supply of savings in the economy, most of this debt can be internally financed at fairly low interest rates. The standard equation for government debt dynamics says that the change in the debt-to-GDP ratio, D/Y, can be expressed as:1

Image

G - T is the primary budget deficit, r is the borrowing rate, and g is the growth rate of the economy (it is irrelevant whether r and g are defined in nominal or real terms, as long as they are both expressed the same way). China will avoid a debt crisis for the same reason Japan has been able to avoid one. The Chinese 10-year government bond yield is currently four percentage points below projected GDP growth over the next decade, which is one of the biggest gaps among the major economies (Chart 5). Arithmetically, this means that China can have as large a primary fiscal deficit as it wants. As long as r remains below g, the debt-to-GDP ratio will converge to a stable level. Chart 6 shows this point analytically.

Chart 5

Chart 6

In fact, it is possible that a permanently larger budget deficit could lead to a decline in the equilibrium debt-to-GDP ratio. How could that be? The answer is revealed by the equation above. If the debt-to-GDP ratio is fairly high to begin with and an increase in the primary budget deficit leads to higher inflation (and hence, lower real rates and/or faster nominal GDP growth), this could more than fully counteract the increase in the deficit. Chart 7Stronger Growth Coincided With Accelerating Inflation And Lower Real Rates

Stronger Growth Coincided With Accelerating Inflation And Lower Real Rates

Stronger Growth Coincided With Accelerating Inflation And Lower Real Rates

This is not just a theoretical curiosity. Historically, Chinese inflation has risen while real rates have fallen whenever GDP growth has accelerated (Chart 7). Given China’s high debt levels, even a modest amount of additional inflation could put significant downward pressure on the debt-to-GDP ratio.2 Of course, all this is predicated on the assumption that faster credit growth will not cause interest rates to rise above the growth rate of the economy. For the portion of China’s debt stock that is either directly or indirectly backstopped by the central government, this seems like a safe assumption. After all, if credit/fiscal stimulus is simply being undertaken in response to inadequate demand, there is no need for policymakers to hike rates. Things get trickier when we look at private debt. In the past, the government has encouraged state-owned banks to roll over souring loans for fear that a wave of defaults would undermine the economy and endanger social stability. More recently, however, policymakers have been backing away from this strategy due to the well-founded view that it encourages moral hazard. Faster growth in China in the second half of this year will lift Chinese imports. This will be welcome news for the rest of the world. We expect the authorities to continue taking steps to instill market discipline by allowing failing firms to, well, fail. Realistically, however, the transition to a full market-based economy will take quite a bit of time. In the interim, the government will keep cutting taxes and increasing on-budget spending in order to ensure that any decline in employment among failing firms is offset by employment growth elsewhere. In such an environment, neither a debt crisis nor a deep economic slowdown appear likely. Investment Conclusions Faster growth in China in the second half of this year will lift Chinese imports. This will be welcome news for the rest of the world.

Chart 8

Chart 9Germany Welcomes The Upturn In Chinese Credit Growth

Germany Welcomes The Upturn In Chinese Credit Growth

Germany Welcomes The Upturn In Chinese Credit Growth

While the U.S. will benefit from a revival in Chinese growth, Europe will gain even more (Chart 8). Germany, in particular, should see a pronounced acceleration in growth. China’s credit impulse leads Chinese automobile spending which, in turn, reliably leads euro area automobile exports, as well as overall exports (Chart 9). The recent rebound in the expectations component of the German ZEW index, as well as in the manufacturing output component of the April flash PMI, suggests that green shoots are starting to sprout (Chart 10). Italy should also benefit from the steep drop in bond yields since last October (Chart 11). Italian industrial production strongly surprised to the upside in February, suggesting that the euro area’s third biggest economy may have finally turned the corner. Chart 10Tentative Green Shoots Out Of Germany

Tentative Green Shoots Out Of Germany

Tentative Green Shoots Out Of Germany

Chart 11Italy: The Drop In Bond Yields Should Boost The Economy

Italy: The Drop In Bond Yields Should Boost The Economy

Italy: The Drop In Bond Yields Should Boost The Economy

The ECB will not hike rates this year even if growth shifts into higher gear, but the market will probably price in a bit more monetary tightening in 2020 and 2021. This should help lift the euro. We recommend that investors position themselves for this by going long EUR/JPY. Relatedly, we are closing our short EUR/CAD trade for a gain of 3.9%. The U.S. dollar tends to be a countercyclical currency, meaning that it moves in the opposite direction of the global business cycle (Chart 12). This countercyclicality stems from the fact that the U.S. is more geared towards services than manufacturing compared with most other economies (Chart 13). As such, when global growth accelerates, capital tends to flow from the U.S. to the rest of the world, translating into more demand for foreign currency and less demand for dollars. Chart 12The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

Chart 13The U.S. Is A Low-Beta Play On Global Growth

The U.S. Is A Low-Beta Play On Global Growth

The U.S. Is A Low-Beta Play On Global Growth

A “patient” Fed and the prospect of stronger global growth in the second half of this year are bearish for the dollar. As such, we are closing our long DXY trade for a carry-adjusted gain of 16.4% and exiting our long USD/CNY trade for a loss of 3.1%. We are also closing our short AUD/CAD trade for a gain of 1.6%. Faster Chinese growth will boost metal prices, which is bullish for the Aussie dollar. Lastly, we are switching our short EUR/RUB trade (which is currently up 8.6%) into a short USD/RUB trade. A weaker greenback and stronger global growth will be manna from heaven for international stocks, especially when priced in U.S. dollars. Investors should prepare to move European and EM equities to overweight within a global equity portfolio during the coming weeks. A “patient” Fed and the prospect of stronger global growth in the second half of this year are bearish for the dollar. We are less keen on upgrading Japanese equities. While Japanese exporters will benefit from stronger Chinese growth, the domestic economy will be weighed down by the upcoming hike in the sales tax, which is slated to take place in October. Moreover, the yen is likely to experience headwinds as global bond yields rise in relation to JGB yields. Investors contemplating buying Japanese stocks should hedge any currency risk. Finally, the price of gold fell to $1275/ounce earlier this week, triggering our buy order. With the Fed on pause, the U.S. economy starting to overheat, and the dollar likely to trend lower, bullion could shine over the coming months. Peter Berezin, Chief Global Strategist Global Investment Strategy peterb@bcaresearch.com Footnotes 1 Please see Global Investment Strategy Weekly Report, “Is There Really Too Much Government Debt In The World?” dated February 22, 2019, for a fuller discussion of this debt sustainability equation.

Image

Strategy & Market Trends MacroQuant Model And Current Subjective Scores

Chart 14

Tactical Trades Strategic Recommendations Closed Trades

Highlights The political economy of oil will become even more complicated, following remarks by Russian Finance Minister Anton Siluanov over the weekend, which suggested policymakers there are considering another market-share war to crash prices to limit the growth of U.S. shales. The logic appears to be that by abandoning OPEC 2.0’s production-cutting deal and pushing Brent prices below $40/bbl once again for a year or so, Russia will severely reduce investment flow to the U.S. shale-oil patch, allowing it to retake global market share ceded mostly to Texas oil producers.1 The threat of a market-share war was proffered on top of stepped-up rhetoric by senior government officials – ranging from Igor Sechin, head of state-owned Rosneft Oil, to Kirill Dmitriev, CEO of the Russian Direct Investment Fund (RDIF) – indicating Russia will be pushing for higher production by OPEC 2.0 in 2H19 at the coalition’s upcoming June meeting. We agree with this assessment: The market will require OPEC 2.0 to lift production in 2H19, given our assessment of supply-demand balances. In our estimation, OPEC 2.0’s position has been strengthened considerably by policy-induced disruptions to the oil market.2 As such, we believe Russia’s threat of a market-share war is a feint, particularly since Russia has benefited greatly from higher prices (see below). Our balances and price forecasts this month are largely unchanged (Chart of the Week). We continue to expect Brent to average $75/bbl this year. For 2020, we expect Brent to average $80/bbl. WTI will trade $7 and $5/bbl lower (Chart 2). The balance of price risk has shifted slightly to the left side of the distribution, driven by policy risk and potential miscalculation by the dramatis personae on the international stage, chiefly leaders in the U.S., Russia and China. Chart of the WeekMarkets Continue To Track BCA Balances...

Markets Continue To Track BCA Balances...

Markets Continue To Track BCA Balances...

Chart 2...While Prices Continue Tracking BCA Forecasts

...While Prices Continue Tracking BCA Forecasts

...While Prices Continue Tracking BCA Forecasts

Highlights Energy: Overweight. Tensions in Libya could keep ~ 300k b/d of supply from reaching global markets via its Zawiya port near Tripoli. We closed our long June 2019 $70/bbl vs. short $75/bbl call spread last Thursday with a gain of 87.7%.3 Base Metals: Neutral. China’s latest credit data confirms our view the country’s credit cycle bottomed earlier this year: March Total Social Financing (TSF) increased CNY 2.8 trillion month-on-month vs. consensus expectation of CNY 1.7 trillion. This will support base metals in the coming months. We continue to expect Chinese authorities to expand credit in 2H19.Our long copper trade is up 0.7% since inception on March 7, 2019. We are closing out our tactical iron-ore trade – long 65% Fe vs. short 62% Fe at tonight’s close; it was up 22.9% at Monday’s close. Precious Metals: Neutral. Gold fell 4% from its February high on easing inflation concerns and as fears of an equity correction subsided. March U.S. PCE ex-food and -energy dropped to 1.79% yoy from 1.95% in February, while global equities rose 14% YTD. Our long gold recommendation is down 2.4% since last week, but is still up 3.6% since inception on May 4, 2017. Agriculture: Underweight. U.S. corn and wheat farmers are behind schedule in their spring planting, according to USDA data. The top four American corn-producing states had not started planting by last week, while spring and winter wheat producing states are 11% and 3% behind schedule, mostly due to weather conditions. While delays in planting are always cause for concern, we are still early in the planting season, which gives farmers time to catch up. Feature Policy uncertainty vis-à-vis global oil supply was elevated by Russian Finance Minister Anton Siluanov’s comments indicating policymakers are considering reviving an oil market-share war directed at U.S. shale-oil producers. Siluanov said prices could fall to $40/bbl or less, in the event. Russian President Vladimir Putin, who, among the policy elites of Russia, remains primus inter pares, has indicated he is satisfied with prices where they are now His remarks come on the back of statements from Russian government and oil company officials lobbying for higher output. These comments suggest there is a heavyweight Russian contingent fully supporting these demands for OPEC 2.0 to increase production in 2H19 when it meets in June. Otherwise, the threat implies, Russia will seriously consider leaving OPEC 2.0, and will launch its own market-share war against U.S. shale-oil production, led by the fast-growing Permian Basin in Texas. Thus far, Russian President Vladimir Putin, who, among the policy elites of Russia, remains primus inter pares, has indicated he is satisfied with prices where they are now – nicely above $70/bbl in the Brent market. He also wants to maintain cooperation with OPEC 2.0, particularly its other putative leader, KSA. We continue to believe, however, KSA and Russia become less comfortable with Brent prices moving sharply above $80/bbl.4 Nonetheless, the threat posed by the U.S. shales is non-trivial: In our latest balances estimates, we raised our 2H19 U.S. output estimates to 12.53mm b/d, and slightly decreased our 2020 estimates to 13.35mm b/d”, led by a 1.17mm b/d and 0.84mm b/d increase in shale output this year and next (Chart 3). Chart 3U.S. Oil Production Estimate Higher For Shales

U.S. Oil Production Estimate Higher For Shales And GOM

U.S. Oil Production Estimate Higher For Shales And GOM

However, Russia – and OPEC 2.0 generally – may be overestimating the rate of growth from U.S. shales going forward: In future research, we will be exploring the extent to which capital markets will restrain growth in the U.S. shales, as investors continue to demand higher returns. The days of growing shale production at any cost may be coming to an end. Russia’s Threat Is A Feint We believe Russia’s threat of a market-share war is a feint: A market-share war would damage the Rodina’s economy more than the balance sheets of U.S. shale producers, particularly those that hedge the first year or two of their production. The threat needs to be understood in the context of the deterioration of Russia’s position in Venezuela; the increasing tempo of U.S. military operations in its near abroad; and rapidly evolving global oil and gas trade flows, all of which are working against Russian interests and investments.5 The threat appears to be a not-too-subtle reminder of the havoc Russia still can create globally, should it choose to do so, as Vladimir Rouvinski noted recently re Russia’s Venezuela policy.6 Russia almost surely is better off under the production-cutting regime launched by OPEC 2.0 than it would be in another price war. Russia’s GDP elasticity to oil prices is more than twice that of KSA’s, which we demonstrated last week.7 This means, from an economic standpoint, it benefits more from higher prices than the Kingdom, based on our modeling. Russia’s oil is exported to refiners and trading companies who pay whatever price is clearing the market, versus KSA, which relies more on direct investments in end-use markets to serve captive demand, and whose GDP has a higher sensitivity to EM economic growth. Russia almost surely is better off under the production-cutting regime launched by OPEC 2.0 than it would be in another price war. The coalition’s production-cutting deal this year has reduced global supplies by 1.0mm b/d since the beginning of the year, lifting price from below $50/bbl to more than $70/bbl, in line with our forecast. These production cuts have been supported by strong global demand this year this, which, we expect, will persist in 2020. Of course, Russia could abandon the production-cutting deal with KSA, in the hope of severely reducing investment in U.S. shale-oil production. However, it also would accelerate the loss of foreign direct investment (FDI) in its own hydrocarbons sector, along with those of other OPEC 2.0 member states (Chart 4). Bottom Line: A Russian market-share war aimed at U.S. shale producers would run the very real risk of tanking Russia’s GDP and those of the rest of OPEC 2.0’s member states, as these economies lack the resilience and diversification of the U.S.’s GDP, particularly Texas’s. Even if its fiscal balances are in better shape now, Russia’s economy remains highly sensitive to Brent crude oil prices – moreso than KSA’s, and far moreso the U.S.’s (Chart 5).8 Chart 4Another Oil Market-Share War Would Crush OPEC 2.0 In-Bound FDI

Another Oil Market-Share War Would Crush OPEC 2.0 In-Bound FDI

Another Oil Market-Share War Would Crush OPEC 2.0 In-Bound FDI

Chart 5Russia Benefits More Than KSA From Higher Oil Prices

Russia Benefits More Than KSA From Higher Oil Prices

Russia Benefits More Than KSA From Higher Oil Prices

BCA’s Balances Mostly Unchanged Our updated balances reflect the lower Venezuelan and Iranian output reported by OPEC’s survey of secondary sources (Table 1). As we have noted previously, we believe OPEC 2.0’s spare capacity is sufficient to cover the loss of Venezuelan output, and the limited losses on Iranian exports imposed by U.S. sanctions (Chart 6). Beyond that, however, the market will be severely stretched if an unplanned outage removes significant production from global supply. Table 1BCA Global Oil Supply - Demand Balances (MMb/d, Base Case Balances)

Russia Posits Oil Market-Share War: Red Herring Or Real Threat?

Russia Posits Oil Market-Share War: Red Herring Or Real Threat?

On the supply side, we continue to expect OPEC and Russia to lift supply in 2H19, following the successful draining of global inventories (Chart 7). We expect OPEC ex-Iran, Libya and Venezuela, led by KSA, will lift 2H19 supply by ~ 400k b/d vs. 1H19 levels, while we expect Russia’s output to rise 200k b/d.

Chart 6

Chart 7Lower Inventories Require OPEC 2.0 Supply Increase In 2H19

Lower Inventories Require OPEC 2.0 Supply Increase In 2H19

Lower Inventories Require OPEC 2.0 Supply Increase In 2H19

We continue to expect oil demand to be supported by the renewed easing of monetary policy globally, which will redound to the benefit of EM demand, which also will benefit from the bottoming of China’s credit cycle. Indeed, the EIA added 130k b/d to its estimate of non-OECD demand for this year, on the back of stronger expected growth. We expect demand growth of 1.5mm b/d this year and 1.6mm b/d next year, with EM growth accounting for 1.1mm b/d of growth this year and 1.3mm b/d next year. In levels, global demand will average 101.8mm b/d and 103.4mm b/d in 2019 and 2020. Waivers On U.S. Iran Sanctions Will Be Extended We continue to expect waivers on U.S. sanctions of Iranian oil imports will be extended on May 2, owing to the still-tight supply conditions globally with Venezuela output collapsing and ~ 1mm b/d of Iranian oil already forced off the market. This has, as we’ve noted in our discussions of the New Political Economy of oil, strengthened OPEC 2.0’s hand. This will become apparent when the coalition meets in June to consider whether to increase production in 2H19, in line with our expectation. KSA, Russia and OPEC 2.0 member states will have sufficient data on hand to determine whether and by how much to lift output, in a manner that supports their GDPs. Indeed, on Wednesday, Russian Energy Minister Alexander Novak said, “We should do what is more expedient for us.”9 KSA and Russia appear to be managing production in a manner consistent with our forecasts of $75 and $80/bbl for Brent this year and next than not. We also expect U.S. President Donald Trump to try to jawbone OPEC 2.0 into increasing production again, as he did in 2H18. However, we expect those demands to fall on deaf ears, unless fundamental supply dislocations warrant such action. Bottom Line: OPEC 2.0’s strategy is working – it will have maximum flexibility re how it handles its production in 2H19, following the U.S. decision on waivers to its Iran oil-export sanctions on May 2. As we noted last month, KSA and Russia appear to be managing production in a manner consistent with our forecasts of $75 and $80/bbl for Brent this year and next than not. Robert P. Ryan, Chief Commodity & Energy Strategist rryan@bcaresearch.com Hugo Bélanger, Senior Analyst Commodity & Energy Strategy HugoB@bcaresearch.com Footnotes 1 OPEC 2.0 is the name we coined for the OPEC/Non-OPEC oil-producer coalition led by the Kingdom of Saudi Arabia (KSA) and Russia. It agreed in November to remove 1.2mm b/d off the market, in order to balance global supply and demand and reduce inventories. Please see “Russia, OPEC may ditch oil deal to fight for market share: Russian minister,” published April 13, 2019, for a re-cap of Siluanov’s remarks. 2 Please see “The New Political Economy of Oil,” published by BCA Research’s Commodity & Energy Strategy February 21, 2019; and “OPEC 2.0: Oil’s Price Fulcrum,” published March 21, 2019. It is available at ces.bcaresearch.com. 3 Please see “Oil steadies as market focuses on supply risks,” published April 15 2019 by reuters.com 4 Please see “Putin Says No Imminent Decision on Oil Output Cuts,” published April 10, 2019, by The Moscow Times. 5 Please see for example, “Pentagon developing military options to deter Russian, Chinese influence in Venezuela,” published by cnn.com April 15, 2019; “Destroyer USS Ross Enters Black Sea, Fourth U.S. Warship Since 2019,” published by news.usni.org April 15, 2019; and “U.S. LNG exports pick up, with Europe a major buyer,” published by reuters.com March 7, 2019. 6 Please see “Russian-Venezuelan Relations at a Crossroads” by Vladimir Rouvinski, published by the Wilson Center’s Kennan Institute in its February Latin American digest. 7 Please see “Sussing Out OPEC 2.0’s Production Cuts, U.S. Waivers On Iran Sanctions,” published by BCA Research’s Commodity & Energy Strategy April 11, 2019. It is available at ces.bcaresearch.com. 8 We discuss the impact of higher oil prices on Russia’s economy in last week’s report, which is cited in footnote 6 above. Russia’s GDP in 2017 was ~ U.S. $1.6 trillion, according to the World Bank, while the GDP of Texas was ~ $1.7 trillion, American Enterprise Institute. 9 Please see “Russia’s Novak: early to speak about options for oil output deal,” published reuters.com April 17, 2019. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades TRADE RECOMMENDATION PERFORMANCE IN 2019 Q1

Image

Commodity Prices and Plays Reference Table Trades Closed in 2019 Summary of Closed Trades

Image

Highlights In China, “helicopter” money and the socialist put are positive for growth in the medium term but will prove harmful for the economy over the long run. In the socialist put scenario, a buy-and-hold strategy is inappropriate for Chinese stocks. The enormous amount of money supply in China is “the sword of Damocles” on the yuan’s exchange rate. A new equity trade: Short Chinese banks / long U.S. banks. Take profits on our short Chinese property developers / long U.S. homebuilders equity position. Feature Last week’s China credit and money data affirmed that Chinese banks have engaged in another round of massive credit and money injection into the economy. In the first quarter alone, aggregate credit rose by RMB 8.5 trillion (US$1.3 trillion). Aggregate credit growth accelerated to 11.6%, well above first-quarter nominal GDP growth of 8% (Chart I-1). This is in spite of numerous pledges by many of China’s top policymakers that they have no plans to resort to “floodgate irrigation” style stimulus, and that credit/money growth will be kept on par with nominal GDP growth. Our credit and fiscal spending impulse has spiked up, pointing to a potential improvement in economic data in the months ahead (Chart I-2). Chart I-1China: No Deleveraging At All

China: No Deleveraging At All

China: No Deleveraging At All

What’s more, there is anecdotal evidence of a revival of housing demand in March, and that property developers have once again commenced bidding up land prices in certain parts of the country. Chart I-2China: Leading Economic Indicators

China: Leading Economic Indicators

China: Leading Economic Indicators

Regarding investment strategy, two weeks ago we put a stop-buy limit on the MSCI EM stock index at 1125. If this index breaks above this level we will turn tactically positive on EM risk assets. There is anecdotal evidence of a revival of housing demand in March, and that property developers have once again commenced bidding up land prices in certain parts of the country. Below are the pros and cons of upgrading the EM outlook at the current juncture. Pros The credit impulse in China leads both the mainland’s business cycle and the global manufacturing cycle by an average of nine months. Given its bottom was in December 2018, the trough in the mainland business and global industrial cycles should have been around August 2019 (Chart I-3). Chart I-3Global Manufacturing PMI Has Not Led Global Stocks

Global Manufacturing PMI Has Not Led Global Stocks

Global Manufacturing PMI Has Not Led Global Stocks

Our assessment has been that the bottom in EM equities that occurred in late December 2018 was too early. Our basis has been that the Chinese and global manufacturing cycles were not likely to bottom before August 2019, according to their previous relationship with China’s credit and fiscal spending impulse. Consequently, we have been expecting China-related plays in financial markets to experience a setback before a more sustainable buying opportunity emerged. However, as China’s credit recovery is now gaining momentum and infrastructure spending financed by local government special bonds is accelerating, the window of downside risk for share prices is narrowing. There have been no recent major stimulus measures directed at China’s property market, but it appears banks have substantially boosted mortgage loan origination and their financing of property developers by loosening lending standards. Easy financing for both homebuyers and property developers makes a revival in real estate more likely. The property market and construction activity are critical to the mainland’s business cycle. If green shoots in the property market multiply, the odds of an overall growth recovery will rise substantially. Finally, if the EM equity index breaks above our stop-buy limit, it would clear an important technical resistance level, confirming the sustainability of this rally (Chart I-4). Cons EM corporate profit growth is contracting in U.S. dollar terms, and the pace of contraction will deepen into the end of this year. This assessment is based on the previous decline in China’s credit impulse. The latter suggests a bottom in EM EPS in December 2019 (Chart I-5). It is still unclear whether EM share prices can ignore this profit contraction and advance through the entire year without major bumps. Chart I-4EM Stocks Are Facing Technical Resistance

EM Stocks Are Facing Technical Resistance

EM Stocks Are Facing Technical Resistance

Chart I-5EM Profits Will Continue Contracting

EM Profits Will Continue Contracting

EM Profits Will Continue Contracting

As of March, Chinese domestic smartphone sales (Chart I-6), as well as Korean, Japanese, Singaporean and Taiwanese exports to the mainland, are all still shrinking at double-digit rates from a year ago (Chart I-7). Chart I-6China: Consumer Spending In March Was Still Weak

China: Consumer Spending In March Was Still Weak

China: Consumer Spending In March Was Still Weak

Chart I-7Exports To China Contracted At A Double-Digit Rate In March

Exports To China Contracted At A Double-Digit Rate In March

Exports To China Contracted At A Double-Digit Rate In March

Our indicators for marginal propensity to consume for Chinese households and companies remain in a downtrend as of March (Chart I-8). An upturn in these indicators is needed to validate that the fiscal and credit stimulus is accompanied by a greater multiplier effect. Chart I-8China: Marginal Propensity To Spend By Consumers And Enterprises

China: Marginal Propensity To Spend By Consumers And Enterprises

China: Marginal Propensity To Spend By Consumers And Enterprises

Chart I-9Low Vol Precedes A ##br##Regime Shift

Low Vol Precedes A Regime Shift

Low Vol Precedes A Regime Shift

Finally, financial markets’ aggregate volatility is extremely low (Chart I-9). This is especially true for the currency markets (Chart I-10, top panel). Typically, this is a sign of both complacency and a forthcoming major regime shift in financial markets. Chart I-10The Dollar Is Poised To Break Out Or Break Down

The Dollar Is Poised To Break Out Or Break Down

The Dollar Is Poised To Break Out Or Break Down

We would be much more comfortable upgrading the EM outlook if the broad trade-weighted U.S. dollar broke down, corroborating the improvement in global/EM growth. So far, the greenback has been moving sideways along its 200-day moving average (Chart I-10, bottom panel). If the dollar breaks out, it would confirm the negative outlook for EM. Investors should closely watch foreign exchange markets and adjust their investment strategy accordingly. “Helicopter” Money Forever = A Socialist Put China’s forthcoming recovery is good news for financial markets. Nonetheless, the long-term outlook for the Chinese economy is deteriorating because the credit and money, as well as property bubbles, will keep expanding. First, China holds the world record with respect to corporate sector leverage (Chart I-11). Second, households in China are more leveraged than those in the U.S. (Chart I-12). Given that borrowing costs for households are higher in China than in the U.S., interest payments take up a larger share of Chinese households’ disposable income. Chart I-11Corporate Sector Leverage: China Holds The World Record

Corporate Sector Leverage: China Holds The World Record

Corporate Sector Leverage: China Holds The World Record

Chart I-12Chinese Households Are More Leveraged Than Americans

Chinese Households Are More Leveraged Than Americans

Chinese Households Are More Leveraged Than Americans

Third, contrary to popular belief, banks do not channel savings/deposits into credit. They create deposits/money supply when they lend to or buy assets from non-banks. Money supply is the sum of deposits and cash in circulation. Financial markets’ aggregate volatility is extremely low. This is especially true for the currency markets. In a nutshell, credit and money excesses in China are not natural outcomes of the nation’s high savings rate but are the result of reckless credit origination by China’s commercial banks. We have elaborated on this point in a series of reports we have written on credit, money and savings.1 When commercial banks originate a loan, they create new money and new purchasing power “out of thin air.” Nobody needs to save for a bank to make a loan or buy assets. Consequently, new purchasing power for goods and services boosts demand in the real economy and inflates asset prices. Chinese banks have literally been dropping “helicopter” money over the past 10 years. Since January 2009 – the onset of the country’s massive credit binge – banks have created 165 trillion yuan ($25 trillion) of new broad money, based on our measure of M3 broad money. This is triple of the $8.3 trillion broad money supply created in the U.S., the euro area and Japan combined during the same period (Chart I-13, top panel). Chart I-13Helicopter Money In China

Helicopter Money In China

Helicopter Money In China

China’s broad (M3) money supply now stands at 220 trillion yuan, equivalent to $32.5 trillion. What’s astonishing is that Chinese broad money is larger than the sum of broad money in both the U.S. and the euro area (i.e. all outstanding U.S. dollars and euros in the world combined) (Chart I-13, bottom panel). Yet China’s nominal GDP is only 38% of U.S. and euro area’s GDP combined. Credit and money excesses in China are not natural outcomes of the nation’s high savings rate but are the result of reckless credit origination by China’s commercial banks. In a market-based economy, the constraints on banks doing “helicopter” money are bank shareholders, regulators and central banks. Bank shareholders are the primary and largest losers from credit booms because they are highly exposed to non-performing loans. That is why they should be the first to cut credit flows to the economy when they sense non-payments on loans could rise. In China, neither bank shareholders nor bank regulators or the People’s Bank of China have prevented banks from expanding credit/money. Moreover, the authorities have not forced banks to acknowledge non-performing loans. This scenario – whereby banks expand credit without taking responsibility for collecting the loans – only occurs in a socialist system. This is the ultimate socialist put. China’s Potential Growth Roadmaps We have been arguing for several years that China is facing a historic choice between: (1) Moving toward a more market-based economic system that entails making creditors and borrowers take responsibility for their lending/borrowing and investment decisions. If lenders and borrowers are made explicitly accountable for their business/financial decisions, then credit flows will decelerate considerably, bankruptcies will mushroom and a period of deleveraging will be inevitable. However, the quality of capital allocation will improve, enhancing the country’s productivity and potential growth in the long run (Chart I-14).

Chart I-14

This is a scenario of medium-term pain, long-term gain. The recent ramp-up in credit growth does not suggest the authorities are willing to embrace this option. Chart I-15China: Structural Growth Tailwinds Have Dissipated

China: Structural Growth Tailwinds Have Dissipated

China: Structural Growth Tailwinds Have Dissipated

(2) “Helicopter money” and a socialist put scenario entails lower potential GDP growth and rising inflation. If China continues opting to keep the socialist put in place, its potential growth rate – which is equivalent to the sum of growth rates in productivity and the labor force – will drop significantly. In the long run, this socialist put discourages innovation and breeds capital misallocation, reducing productivity growth. In fact, the industrialization ratio is 85% – not 60% as many contend(Chart I-15, top panel). Further, China’s labor force growth has stalled and will be mildly negative in the years to come (Chart I-15, bottom panel). Together, these circumstances point to a slower potential growth rate. Meanwhile, recurring stimulus via “helicopter” money will create mini-cycles around a falling potential growth rate (Chart I-16). Below we discuss the investment strategy this scenario entails.

Chart I-16

Implications Of The Socialist Put For The Currency… Slowing productivity and rampant money/purchasing power creation ultimately lead to rising inflation. Higher inflation and low interest rates - required to sustain an ever-rising debt burden - are a recipe for currency depreciation. Chinese households and businesses are eager to diversify their copious and mushrooming renminbi deposits into foreign currencies and assets. The PBoC’s foreign exchange reserves of $3 trillion are equal to only 10% of the amount of yuan deposits and cash in circulation. Foreign exchange reserves’ coverage of local currency money supply is much higher in many other EM countries, including Brazil and Russia (Chart I-17). Chart I-17China's FX Reserves Cover Less Local Currency Deposits Than Peers

China's FX Reserves Cover Less Local Currency Deposits Than Peers

China's FX Reserves Cover Less Local Currency Deposits Than Peers

The enormous amount of money supply/deposits in China is “the sword of Damocles” on the yuan’s exchange rate in the long run. It is therefore inconceivable that China can fully open its capital account in the foreseeable future. On the contrary, capital account restrictions will be further tightened. Plus, the current account will become much more regulated so that there is no leakage of capital via trade transactions – such as over-invoicing of imports or under-invoicing of exports. The inability to repatriate capital when needed and structural RMB depreciation are the key risks to long-term investors in China’s onshore capital markets. …And Chinese Stocks In the socialist put scenario, a buy-and-hold strategy is inappropriate for Chinese stocks: Investors should attempt to play the resultant mini-cycles (Chart I-16). In reality, however, economic and especially financial market mini-cycles are not symmetric, and investors can make money only if they time them properly. In fact, this decade Chinese share prices – both in absolute terms and relative to global stocks – have experience wild swings (Chart I-18). Chart I-18Chinese Stocks Are Following Mini-Cycles

Chinese Stocks Are Following Mini-Cycles

Chinese Stocks Are Following Mini-Cycles

Concerning the current outlook for Chinese investable stocks, our take is as follows: On absolute performance, we will turn positive on Chinese share prices if our stop-buy on EM equities is triggered, as per our discussion above. As for their relative performance within EM and global equity portfolios, simply because the stimulus originates in China does not warrant an overweight position in Chinese stocks. The primary losers from credit bubbles are banks and other financial companies. The basis is that they will carry the burden of potential rising non-performing loans unless the government bails them out by purchasing bad assets at par. The latter has not been the case so far this decade. Hence, an underweight position in Chinese banks/financials is currently warranted. Furthermore, the large debtors in the non-financial corporate sector should also be underweighted. When a company increases its debt but its new investments produce little net new cash flow, its equity value declines. It is difficult to find so many high-return investment projects, especially in a slowing economy. Therefore, another round of considerable capital misallocation is currently underway, and shareholders of the companies that are undertaking these investments will end up losing. In a socialist system, shareholders typically do not make money. They lose money. This is the rationale to underweight Chinese stocks within both EM and global equity portfolios. Yet, there is a caveat: This framework may not be pertinent to the two largest companies in the Chinese investable equity index Ali-Baba and Tencent - each of which accounts for 13% of the index. These two companies score well on the above issues but face different non-macro hazards including regulatory, business model and other risks. Weighing the pros and cons, we recommend maintaining a market weight allocation in Chinese equities within an EM equity portfolio. This is the view of BCA’s Emerging Markets Strategy team, which differs from the recommendations of other BCA services that are currently advocating an overweight position in Chinese stocks within a global equity portfolio. A New Trade: Short Chinese Bank / Long U.S. Bank Stocks Chinese banks’ equity value will erode as they once again expand their balance sheets aggressively, as per our discussion above. Chinese banks’ EPS have been and will continue to be diluted by the need to raise more capital. U.S. banks are better capitalized, and their asset quality is much better. Since the 2007-08 credit crisis, they have been much more prudent in expanding their balance sheets. U.S. bank stocks have underperformed the S&P 500 index since August 2018 because of falling U.S. interest rate expectations. The odds are high that U.S. bond yields are bottoming and will rise considerably – because the drag from China’s slowdown on the global economy is diminishing. This will help U.S. bank stocks. Although Chinese bank stocks optically appear undervalued, they are “cheap” for a reason. The fact that they have been “cheap” since 2011 and have failed to re-rate confirms that they suffer from chronic problems that have not been addressed yet (Chart I-19). Finally, their relative performance is facing a major resistance level, and will likely relapse (Chart I-20). Chart I-19Chinese Banks Are Cheap##br## For A Reason

Chinese Banks Are Cheap For A Reason

Chinese Banks Are Cheap For A Reason

Chart I-20A New Trade: Short Chinese Banks / Long U.S. Banks

A New Trade: Short Chinese Banks / Long U.S. Banks

A New Trade: Short Chinese Banks / Long U.S. Banks

Take Profits On Short Chinese Property Developers / Long U.S. Homebuilders Position “Helicopter” money might be temporary positive for mainland property developers. In the meantime, share prices of U.S. homebuilders will be hurt due to rising U.S. bond yields. We are closing this position to protect profits. This recommendation has produced a 90% gain since its initiation on March 6, 2012. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Footnotes 1 Please see Emerging Markets Strategy Special Report "Misconceptions About China's Credit Excesses," dated October 26, 2016 and Emerging Markets Strategy Special Report "The True Meaning Of China's Great 'Savings' Wall," dated December 20, 2017, available at ems.bcaresearch.com Equity Recommendations Fixed-Income, Credit And Currency Recommendations

There are four non-trivial risks to a bullish relative stance towards Chinese stocks over the coming year. The trade deal between the U.S. and China falls through or substantially underwhelms. A full resumption of the trade war would definitely cause…

In an optimistic scenario, Chinese investable and domestic stocks have the potential to earn double-digit returns (12-15%) in US$ terms relative to global stocks over the coming year. Conservatively, our China Investment Strategy team expects high…

Our China Investment Strategy team uses monetary conditions, money, and credit growth to reliably predict Chinese “investment-relevant economic activity”. Chinese activity, in turn, has reliably led investable equity earnings growth, and we have therefore…

Dear Client, This Special Report is the full transcript and slides of a keynote presentation I recently gave to the Sovereign Investor Institute in London titled: 'The Biggest Risks To The Global Economy Are…' The short presentation pulls together several concepts and observations which identify the ‘weak links’ in the global economy. Therefore, the presentation should serve as a useful summary of the global economy’s current vulnerabilities. The report then explains how each of the risks translates into a European investment context. I hope you find it insightful. Best regards, Dhaval Joshi, Chief European Investment Strategist

Image

Feature Full Transcript And Slides

Image

Good morning Thank you for inviting me to give today’s keynote presentation under the title: ‘The Biggest Risks To The Global Economy Are…’ (Slide 1). I will not discuss all the risks out there, but the four risks that I will present are the ones that I think are the most significant. And the biggest of these four risks I will leave to the end. So let’s begin. Risk 1 is China’s Credit Cycle (Slide 2). You can see this very clearly in this slide (Slide 3) which shows the short-term accelerations and decelerations in credit within the world’s three largest economies – Europe, the United States, and China. In essence, it is showing how much new credit was created in the last six months compared with the preceding six months. Was it more credit creation or was it less, and how much more or less? Everything is in dollars to allow a fair comparison.

Image

Image

Now look at the red line. The red line is China. Just ten years ago, China’s credit cycle was irrelevant. It simply didn’t matter. But after the GFC, China’s short-term credit expansions and contractions suddenly became as large as those in Europe and the U.S. More recently, China’s cycle is dwarfing the others, so now it is the European and the U.S. credit cycles that are irrelevant! This means that whenever China’s short-term credit cycle turns down, as it did in late 2015, early 2017, and 2018, the global economy feels a chill. The point is that this short-term cycle is a near-perfect oscillator. Down-oscillations will occur every eighteen months or so, and any of them has the potential to turn nasty. Though we are currently in an up-oscillation, the next down-oscillation is due later this year. And I predict that it will pose a big risk to the global economy. Risk 2 is Trade Imbalances (Slide 4). This slide (Slide 5) has a mischievous title ‘Where President Trump Is Right About Europe’. The red line shows where the president is absolutely right: Europe is running a massive – a record-high – trade surplus with the United States. It is an undeniable fact. But the president is wrong about the underlying cause. The underlying cause is not unfair trade practices or tariffs, the underlying cause is the other line, the blue line, which shows the divergent monetary policies of the ECB and the Fed.

Image

Image

The trade imbalance and monetary policy divergence are moving together tick for tick, and the transmission mechanism is of course the exchange rate. The divergent monetary policies have depressed the euro, and a depressed euro obviously makes German cars cheaper for American consumers. That is the reason that the president is seeing so many BMWs driving down Fifth Avenue! My point is that these record-high imbalances are being used to justify economic nationalism – retaliatory tariffs, restricted trade, and potentially all-out trade wars. Alternatively, this chart suggests that the imbalances would correct with large-scale movements of exchange rates. But to me, either of these options poses a big risk to the global economy. Risk 3 Is Technological Disruption (Slide 6). To understand why, I want to introduce you to a concept known as Moravec’s Paradox (Slide 7). A professor of robotics, Hans Moravec, noticed something odd. He realized that things that we find very hard are actually very easy for AI. Things like complex mathematics, speaking multiple languages, or advance pattern recognition. Typically, as few people have these skills, they are well-paid skills.

Image

Image

Whereas things that we find very easy are incredibly difficult for AI. Things like human movement and recognizing, and responding to, emotional signals. Typically, as everybody has these skills, they are low-paid skills. Moravec’s Paradox means that the current wave of technological progress is much more disruptive than previous waves. The steam engine destroyed low-paid jobs, forcing workers up the income ladder. But the current wave of technology, led by AI, is destroying well-paid jobs forcing workers down the income ladder.

Image

You can see it in the data. While job creation in most major economies is on the face of it very strong, just look at what type of jobs are being created (Slide 8). Food delivery, bar work, care work and social work. Now you’ll agree that this is not highly paid work with career prospects! In essence, the current wave of technology is revealing a huge misallocation of capital. You might have invested huge amounts of time and money in say, becoming a linguist. Only to find that AI can translate languages much better than you – and your employment opportunities are limited to lower-income work. Well that misallocation of capital is very disruptive. In my opinion, it’s one of the main reasons why even though economies are growing and unemployment is very low, people don’t feel good. Making them susceptible to simplistic fixes such as ‘take back control’ and economic nationalism. My point is that the current wave of AI-led job disruption has much further to run, and the populist backlash will remain a big risk to the global economy. But now I want to turn to what I believe is the biggest risk of all. Risk 4 Is Higher Bond Yields (Slide 9). Most people believe that economic downturns cause financial market downturns. But the truth is the complete opposite: the causality almost always runs the other way! In the vast majority of cases, it is financial market imbalances and mispricing that cause economic downturns and crises. Take the last three economic downturns – in 2001, in 2008 and in 2011. They all had their roots in financial mispricing – the dot com bubble, the U.S. mortgage market, and euro area sovereign debt. Likewise for the Great Depression in the 30s, Japan’s recession in the early 90s. I could go on. You get the point… What is the financial vulnerability today that could cause an economic downturn? (Slide 10) The answer is that the very rich valuation of equities and other risk-assets is highly sensitive to bond yields. Which means that substantially higher bond yields pose a very big risk to the global economy.

Image

Image

You see, at very low bond yields, the bond price can no longer go up much but it can go down massively (Slide 11). The latest advances in financial theory now conclusively show that this unattractive ‘negative’ asymmetry is what defines ‘risk’ for investors. The crucial point is that at low bond yields, bonds become as risky, or more risky, than equities (Slide 12). And this necessarily means that equities no longer need to deliver a superior return, a risk-premium, over the low bond yield (Slide 13). As bond yields decline this means equity valuations get an exponential boost because both components of the equity’s required return – the risk-free component and the risk-premium component – are collapsing simultaneously (Slide 14).

Image

Image

Image

Image

But if bond yields rise substantially, the process would go into vicious reverse and equity valuations would fall off a cliff. Other risk-assets too, and bear in mind that if we include real estate – as we should – global risk-assets are worth $400 trillion, five times the size of the global economy! Our research shows that the point of vulnerability is if the global 10-year bond yield approaches 2 percent, which is about 50 basis points above where it stands right now. And that, to me, is by far the biggest risk to the global economy.

Image

So to summarise, the biggest risks to the global economy are: China’s credit cycle; trade imbalances and technological disruption and their associated populist backlash; and the biggest risk is higher bond yields (Slide 15). In the near future I think alarm bells should start to ring if China’s credit cycle has tipped into a down-oscillation and/or the global 10-year bond yield is 50 bps higher. Don’t worry, the alarm bells are not ringing right now but they might be later this year. Finally, given the title you gave me, this presentation has necessarily focussed on the key risks. But I don’t want you to get too negative. I also have another presentation called ‘The Biggest Positives For The Global Economy Are…’ And for balance, I hope you invite me to present that next time! Thank you. How Do The Risks Translate Into A European Investment Context? Risk 1: China’s Credit Cycle, is highly relevant to European investors, for two reasons. First, the European economy is very open, meaning that exports make a substantial contribution to GDP growth. This is especially true in Europe’s engine economy, Germany, but it is also important for other major economies like Sweden. And it is evidenced in large trade surpluses as, for example, illustrated in Slide 5. Therefore, whenever China’s credit cycle enters a down-oscillation, as it did last year, Germany cannot escape the nasty chill coming through its all-important net export channel. Second, the European equity market is over-exposed to global growth sensitive sectors and companies – specifically, Industrials, Materials, and Financials. These sectors tend to have a very high operational gearing to global growth. Meaning that a small change in global growth has a disproportionate effect on these companies’ profits and share price performance. The upshot is that in a credit cycle up-oscillation, Europe’s global-growth sensitive stock markets and sectors benefit from a sharp burst of outperformance. The opposite applies in a credit cycle down-oscillation. It follows that if China’s credit cycle is due to tip into a down-oscillation later this year, it would be time to close our successful relative overweighting to European equities and to the global growth sensitive cyclical sectors. Risk 2: Trade Imbalances, is also highly relevant to European investors, for the obvious reason that European economies – especially Germany – are running huge trade surpluses. This puts these economies squarely in the cross-hairs of a retaliatory salvo involving tariffs, trade barriers, or worse, an all-out trade war. Clearly, Europe’s ‘exporting champions’ are the most vulnerable to this risk. The issue is important for the exchange rate too. We showed conclusively that Europe’s trade imbalance is the consequence of the depressed euro. It follows that another way to correct this imbalance is via a stronger euro. In this sense, the fundamentals imply euro upside from here. Risk 3: Technological Disruption, manifests through disruption in the jobs market, the lack of feel good, and the ensuing backlash leading to populism and nationalism. This is particularly relevant to Europe because its collection of nations, each with its own political processes, provides more scope for a political tail-event. A lull in the major political-event cycle is a good thing for Europe. In this regard, the upcoming EU parliamentary elections is not a big risk given the EU parliament’s inability, by itself, to drive policy. The risk increases approaching a meaningful political event, and this includes the date of Brexit. Therefore, this risk is likely to rise somewhat towards the end of the year. Risk 4: Higher Bond Yields, is clearly very relevant to Europe because many of the core euro area bond yields are at their lower bound. This means that the negative asymmetry of returns has its maximum impact on, for example, German bunds. It follows that German bunds are a sell in the near-term. Nevertheless, the upside to yields is ultimately limited given the aforementioned vulnerability of risk-asset valuations to higher bond yields. Therefore, the better long-term strategy is to short German bunds relative to U.S. T-bonds. Finally, a 50 basis points rise in 10-year yields from current levels would be a trigger to flip to underweight European equities. Fractal Trading System* Crude oil is at a technical reversal level. The best way to play this is on a hedged basis versus metals: short WTI, long LMEX. Set the profit target at 5 percent with a symmetrical stop-loss. In other trades, we are pleased to report long AUD/CNY achieved its profit target at which it was closed. This leaves five open positions. For any investment, excessive trend following and groupthink can reach a natural point of instability, at which point the established trend is highly likely to break down with or without an external catalyst. An early warning sign is the investment’s fractal dimension approaching its natural lower bound. Encouragingly, this trigger has consistently identified countertrend moves of various magnitudes across all asset classes.

Short WTI / Long LMEX

Short WTI / Long LMEX

The post-June 9, 2016 fractal trading model rules are: When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. Use the position size multiple to control risk. The position size will be smaller for more risky positions. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com Dhaval Joshi, Chief European Investment Strategist dhaval@bcaresearch.com Fractal Trading Model Recommendations Asset Allocation Equity Regional and Country Allocation Equity Sector Allocation Bond and Interest Rate Allocation Currency and Other Allocation Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart I-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights BCA’s China Investment Strategy team recommended that investors upgrade Chinese stocks to overweight (both investable and domestic) in a Special Alert last week. Investors had a legitimate macro fundamental basis to go overweight Chinese stocks as of February 15, but we hesitated to shift our stance due to several still-present risks and out of concern that the sheer magnitude of the spike in credit could cause a regulatory response that would constrain credit growth in future months. The March credit data has confirmed that Chinese policymakers have chosen to prioritize growth for now, but we are unconvinced that a shift back to controlling leverage is out of the question over the coming year. Investors should continue to monitor this and several other risks noted below. Despite having already rallied significantly this year, Chinese investable and domestic stocks have the potential to earn double-digit relative returns (12-15%) in an optimistic scenario in US$ terms versus global stocks over the coming year. Conservatively, we expect high single-digit relative returns (6-8%). Feature BCA’s China Investment Strategy team recommended that investors upgrade Chinese stocks to overweight (both investable and domestic) in a Special Alert last week.1 In this week’s report we address several issues concerning the outlook for the economy and for Chinese stocks in a Q&A format where we answer the questions of a hypothetical, representative investor. In particular, we will discuss how much relative equity upside investors can expect over the coming year, whether the recent pace of credit growth significantly increases the chance of another credit overshoot, and when investors should expect to see a pickup in actual economic activity. Q: First, a question about timing. Why did it take so long to recommend upgrading Chinese stocks? Haven’t Chinese equities been forecasting an economic recovery for several months? A: Prior to the release of the January total social financing data on February 15, investors had no legitimate macro fundamental basis to go overweight Chinese stocks and were instead responding to a relatively less important factor for the economy – the Sino/U.S. trade war. We placed Chinese stocks on upgrade watch in late-February, and waited for confirmation that the spike in credit was not a one-off surge to be reversed by policymakers dead set against “flood irrigation-style” stimulus. As investors are surely aware, no two economic or financial market cycles are exactly alike. This is particularly true in the case of China; its economy experienced a major structural shift a decade ago, and economic and financial market oscillations since then have been highly disparate. As part of our ongoing search to identify tools that reliably predict the Chinese economy, we presented detailed evidence in a November 2017 Special Report2 that suggested monetary conditions, money, and credit growth have been among the most reliable predictors of Chinese “investment-relevant economic activity” (Chart 1). Chinese activity, in turn, has reliably led investable equity earnings growth, and we have therefore followed this framework closely when judging the economic outlook and the attendant implications for investment strategy. Chart 1Monetary Conditions, Money, And Credit Growth Reliably Lead Chinese Economic Activity

Monetary Conditions, Money, And Credit Growth Reliably Lead Chinese Economic Activity

Monetary Conditions, Money, And Credit Growth Reliably Lead Chinese Economic Activity

Given that financial markets typically lead turning points in economic activity, many market participants have incorrectly suggested that the bottom in Chinese stocks in late-October reflected prescient expectations of a durable re-acceleration in Chinese credit growth. Rather, a detailed examination of the events of the past year highlights that the opposite is true: global investors, the most influential “buyer” of Chinese investable stocks, materially lagged or ignored important developments in leading economic indicators and focused instead on a relatively less important factor for the economy – the Sino/U.S. trade war. Two important pieces of evidence support this point: We prominently discussed the risk that a trade war would pose to China’s economy in the first-half of 2018,3 but we underscored numerous times that this risk was on top of an ongoing and much more concerning slowdown in leading indicators for China’s industrial sector. By June of last year our leading indicator for the Li Keqiang index had been in a downtrend for 16 months straight (Chart 2), and yet investors only sold Chinese investable stocks once President Trump began imposing tariffs against Chinese exports to the U.S. We placed Chinese stocks on downgrade watch at the end of March 2018,4 well in advance of the selloff versus global stocks, and deftly triggered the downgrade on June 20.5 Relative to the global benchmark, November 2018 represented the largest month of relative performance for Chinese investable stocks. At that time, there was zero credible evidence to suggest that a credit upturn was underway; in fact, money and credit growth weakened on a sequential basis for most of Q4. It is true that monetary policy eased significantly following the imposition of U.S. tariffs in June, but given the extent of the decline in interbank rates, this would have led to a bottom in relative performance in July or August if investors were willing to assume that China’s monetary transmission mechanism would work without impairment. November 2nd marks the clear inflection point for Chinese investable stocks and our BCA Market-Based China Growth Indicator (Chart 3), and in our view this proves beyond a doubt that investors have been solely focused on trade: on that day, news broke that President Trump wanted to make a deal with Xi Jinping at the G20 meeting in Argentina later that month, and had instructed aides to begin “drafting terms”.6 Chart 2Until Tariffs Arrived, Investors Completely Ignored The Decline In Leading Indicators

Until Tariffs Arrived, Investors Completely Ignored The Decline In Leading Indicators

Until Tariffs Arrived, Investors Completely Ignored The Decline In Leading Indicators

Chart 3It Was News Of A Trade Deal That Caused A Bottom In China-Related Assets

It Was News Of A Trade Deal That Caused A Bottom In China-Related Assets

It Was News Of A Trade Deal That Caused A Bottom In China-Related Assets

Besides recommending a tactical overweight stance on December 5,7 we generally failed to forecast and position for a meaningful détante in the trade war, and we acknowledge that this contributed to a period of missed potential outperformance. But our research suggests that a trade deal would have been irrelevant had the drivers of China’s relevant economic activity continued to deteriorate, and investors had no concrete signs to suggest otherwise prior to the release of the January total social financing data on February 15 (Chart 4). We conservatively forecast high single-digit relative returns versus global stocks, on the order of 6-8%. There is even more upside potential in an optimistic scenario. Chart 4Before February 15, There was No Basis To Confidently Project An Upturn In Credit

Before February 15, There was No Basis To Confidently Project An Upturn In Credit

Before February 15, There was No Basis To Confidently Project An Upturn In Credit

Starting on February 15, investors did have a legitimate macro fundamental basis to go overweight Chinese stocks. We responded to the January data by placing Chinese stocks on upgrade watch,8 but we hesitated to move to an outright cyclical overweight at that time due to several still-present risks (discussed below) and out of concern that the sheer magnitude of the spike in credit could cause a regulatory response, discreet or otherwise, that would constrain credit growth in future months. The public spat between Premier Li Keqiang and the PBOC over whether the January credit spike represented “flood irrigation-style” stimulus and the disappointing February credit data were both emblematic of these concerns, but ultimately the March credit data has confirmed that a significant credit expansion is underway. This has indeed raised the odds of a major credit overshoot, although we reiterate below why policymakers are likely to remain reluctant to allow one to occur. Q: Chinese investable stocks have already rallied 22% year-to-date in US$ terms; domestic stocks are up 37%. How much further upside can investors realistically expect? A: In an optimistic scenario, Chinese investable and domestic stocks have the potential to earn double-digit relative returns (12-15%) in US$ terms versus global stocks over the coming year. Conservatively, we expect high single-digit relative returns (6-8%). Chart 5 presents our earnings recession model for the MSCI China index. The recent improvement in credit, forward earnings momentum, and the new export orders component of the official manufacturing PMI have already caused the model probability to peak. The dotted line shows that the odds of a contraction in earnings over the coming year are set to fall very sharply if credit even just continues on a moderate expansion path, and assuming that the current values of the remaining model predictors stay constant. Chart 6 shows that while there has been an earnings “response” to the ongoing economic slowdown in China, the response has so far been less intense than what might be expected. While this raises a near-term risk for Chinese stocks if Q1 & Q2 earnings disappoint (see below), it also implies that the level of 12-month trailing earnings may not trend lower over the coming year. Chart 5The Odds Of An Earnings Decline Over The Next Year Have Peaked And Will Fall Further

The Odds Of An Earnings Decline Over The Next Year Have Peaked And Will Fall Further

The Odds Of An Earnings Decline Over The Next Year Have Peaked And Will Fall Further

Chart 6The 'Response' Of Earnings To A Slowing Economy Has Been Less Intense Than Expected

The 'Response' Of Earnings To A Slowing Economy Has Been Less Intense Than Expected

The 'Response' Of Earnings To A Slowing Economy Has Been Less Intense Than Expected

If Chinese earnings are largely stable over the next year, we think it is reasonable to expect that investable Chinese stock prices will re-approach or fully return to their early-2018 high. We noted in our March 27 Weekly Report that China’s potential to command a higher multiple than global stocks is probably capped barring a major structural improvement in earnings growth,9 but Chart 7 highlights that Chinese stocks were still cheaper than their global counterparts at their peak early last year. Chart 7Even At Their 2018 High, Chinese Stocks Were Cheaper Than Global Stocks

Even At Their 2018 High, Chinese Stocks Were Cheaper Than Global Stocks

Even At Their 2018 High, Chinese Stocks Were Cheaper Than Global Stocks

It is true that the multiple expansion that occurred for Chinese stocks in 2016 and 2017 was quite large, but in our view this was due to the index addition and growth of technology companies with potential structural growth stories (such as the “BAT” stocks) rather than due to a significant decline in the risk premium assigned to Chinese stocks. These firms are still present in the investable index, and we have no reason to believe that investors over the coming year will perceive their structural earnings potential to be any different than was the case early last year, which suggests that a forward P/E ratio of 14 to 14½ is again achievable. Domestic equities do not directly benefit from the “BAT effect”, but their realized earnings growth has been somewhat superior than the investable index over the past few years. In effect, we have no strong reasons to argue against a return of both domestic and investable forward multiples back to levels seen in early-2018. Chart 8 highlights that a return to these levels would imply a relative price return of about 12% for investable stocks and 14-15% for domestic stocks, in US$ terms. Several risks (highlighted below) underscore the possibility that Chinese stocks will trend higher but not fully return to their early-2018 levels over the coming year. Given this, we conservatively forecast high single-digit relative returns versus global stocks, on the order of 6-8%. As a final point, for investors focused on A-shares, we should note that our domestic equity call is based on the MSCI China A Onshore index, not the CSI 300 or the FTSE/Xinhua A50 index. While the former very closely tracks the latter two, Chart 9 highlights that the CSI 300 and the A50 have rebounded closer to their early-2018 highs than the MSCI China A Onshore index, suggesting that there is somewhat less upside potential for the former than the latter. Chart 8There Is Meaningful Further Upside Potential For Chinese Stocks Vs. Global

There Is Meaningful Further Upside Potential For Chinese Stocks Vs. Global

There Is Meaningful Further Upside Potential For Chinese Stocks Vs. Global

Chart 9A-Shares: Favor MSCI Indexes Over The CSI300 And The A50

A-Shares: Favor MSCI Indexes Over The CSI300 And The A50

A-Shares: Favor MSCI Indexes Over The CSI300 And The A50