Emerging Markets

Highlights Global equities and other risk assets will trade sideways with elevated volatility over the coming weeks before grinding higher for the remainder of the year, as global growth finally accelerates after a series of false starts. We now see the Fed raising rates more slowly than we had previously envisioned, but ultimately having to scramble to hike rates in order to quell inflation. The fed funds rate will probably plateau at 4% in 2021, implying nine quarter-point hikes more than the market is currently discounting. Over a 12-month horizon, investors should overweight global equities, underweight government bonds, and maintain a neutral allocation to cash. The dollar will peak in the second quarter and then weaken over the remainder of the year and into 2020, before starting to strengthen again late next year. Investors should prepare to temporarily upgrade EM and European stocks over the coming weeks, while increasing exposure to cyclical equity sectors. Industrial metals and oil will strengthen over the course of the year. Gold should be bought on any dip. Investors should begin to de-risk their portfolios in late-2020 in anticipation of a recession in 2021.

Chart 001

Feature Here We Go Again? After having become more defensive last June, we turned bullish on stocks following the December post-FOMC meeting plunge. As stocks continued to rebound, we tempered our optimism. In the beginning of March, we wrote that “having rallied since the start of the year, global stocks will likely enter a ‘dead zone’ over the next six-to-eight weeks as investors nervously await the proverbial green shoots to sprout.”1 Last Friday’s release of disappointing European PMI data poured some herbicide on the green shoots thesis. Germany’s manufacturing PMI hit a six-year low, with the new orders component registering the weakest reading since the Great Recession. This took the 10-year German bund yield into negative territory for the first time since 2016. The U.S. 10-year Treasury yield also fell to a 15-month low, causing the 3-month/10-year curve to invert. Historically, an inverted yield curve has been a reliable predictor of U.S. recessions (Chart 1). Chart 1Yield Curve Inversions, Recessions, And The Term Premium

Yield Curve Inversions, Recessions, And The Term Premium

Yield Curve Inversions, Recessions, And The Term Premium

President Trump’s decision to appoint TV commentator Stephen Moore to the Fed’s Board of Governors did not help matters. Recommended by fellow supply-side “economist” Larry Kudlow, Moore is best known for dismissing concerns over the state of the housing market in 2007, his spot-on 2010 prediction that QE would cause hyperinflation, and his belief that the Trump tax cuts would lead to a smaller budget deficit. Global Growth Will Accelerate In The Second Half Of The Year Given all these worrisome developments, is it time to turn cyclically bearish on the economic outlook and risk assets again? We do not think so. While the next few weeks could be challenging for equities – a risk that our MacroQuant model is currently flagging – sentiment should improve as global growth finally accelerates after a series of false starts. Indeed, some positive signs are already visible: The diffusion index of our global leading economic indicator, which tracks the share of countries with rising LEIs, has moved higher (Chart 2). It leads the global LEI. Service sector PMIs have also generally improved, suggesting that the weakness in global growth remains concentrated in trade and manufacturing. And even on the trade front, a few forward-looking indicators such as the Baltic Dry Index and the weekly Harpex shipping index, which measures global container shipping activity, have bounced off their lows. We would downplay the signal from the yield curve, as it currently is severely distorted by a negative term premium. If the 10-year Treasury term premium were back to where it was in 2004, the 3-month/10-year slope would be more than 200 bps steeper, and nobody would be talking about this issue. In fact, given today’s term premium, the curve would have almost certainly inverted in 1995. Anyone who got out of stocks back then would have missed out on one of the greatest bull markets in history. It should also go without saying that some of the decline in the U.S. 10-year yield reflects a positive development: The Fed has turned more dovish! If one looks at the 10-year/30-year portion of the yield curve, it has actually steepened. This is a sign that the market is seeing the Fed’s actions as being reflationary in nature. There is no clear causal mechanism by which an inverted yield curve slows economic activity, apart from it potentially becoming a self-fulfilling prophecy where the yield-curve inversion scares investors, thereby leading to a tightening in financial conditions (Chart 3). Such “doom loops” are conceptually possible, but as we discussed earlier this year, they are unlikely to occur in the current environment.2 At any rate, financial conditions have eased since the start of the year. This should boost growth in the coming months. Chart 2Global Growth May Be ##br##Starting To Stabilize

Global Growth May Be Starting To Stabilize

Global Growth May Be Starting To Stabilize

Chart 3Easier Financial Conditions Since The Start Of The Year Bode Well For Global Growth

Easier Financial Conditions Since The Start Of The Year Bode Well For Global Growth

Easier Financial Conditions Since The Start Of The Year Bode Well For Global Growth

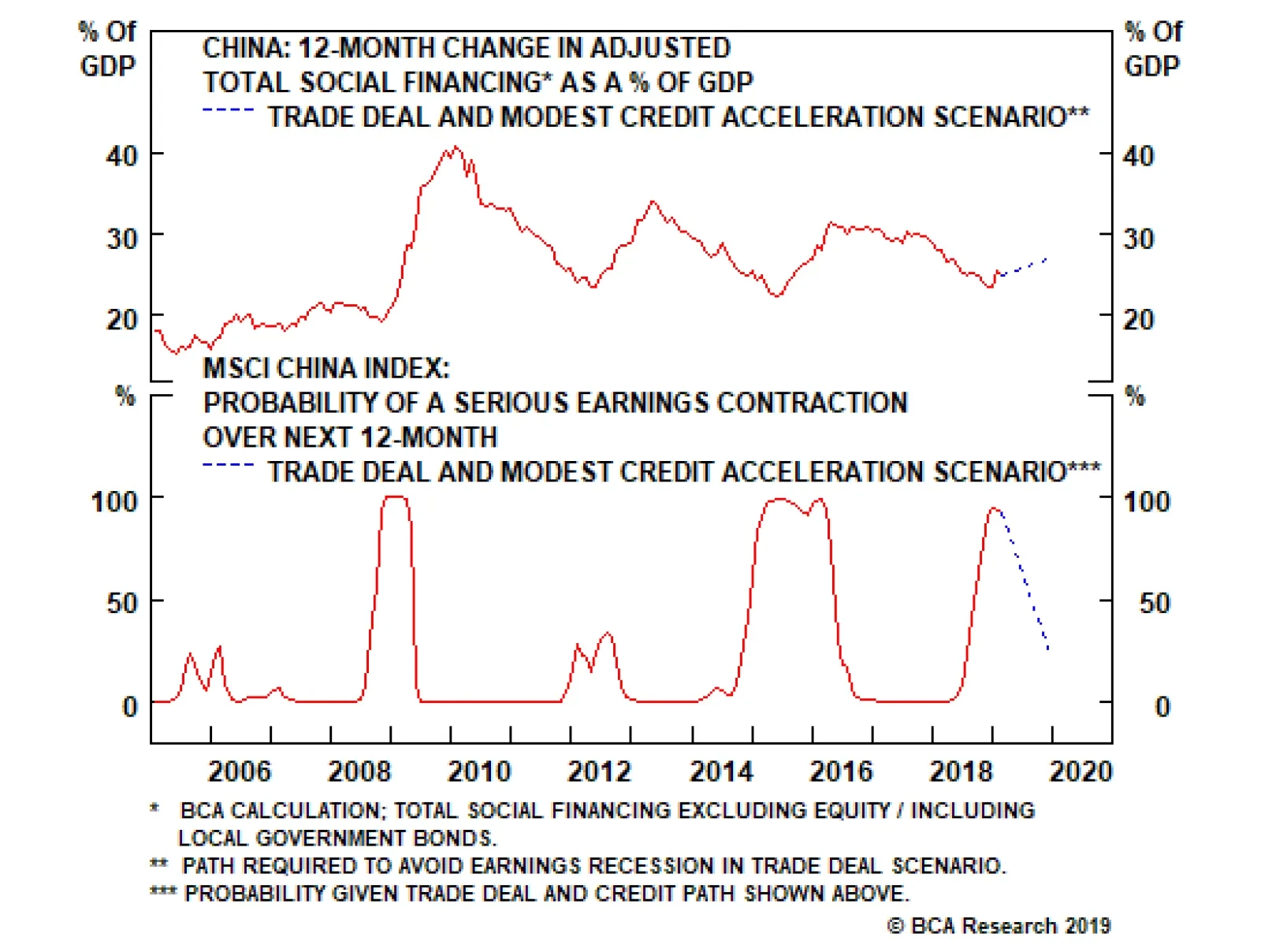

Chinese Credit Growth Set To Rise Global growth has been weighed down by a slowing Chinese economy. Last year’s deleveraging campaign led to a significant deceleration in investment spending, which had negative repercussions for capital equipment and commodity producers all over the world (Chart 4). Historically, China has loosened the reins on the financial sector whenever credit growth has fallen towards nominal GDP growth (Chart 5). It appears we have reached this point. Despite a weak seasonally-distorted February print, credit growth has finally accelerated on a year-over-year basis. Chart 4China: The Deleveraging Campaign Had Adverse Effects On Investment Spending

China: The Deleveraging Campaign Had Adverse Effects On Investment Spending

China: The Deleveraging Campaign Had Adverse Effects On Investment Spending

Chart 5Historically, China Has Scaled Back On Deleveraging When Credit Growth Has Fallen Close To Nominal GDP Growth

Historically, China Has Scaled Back On Deleveraging When Credit Growth Has Fallen Close To Nominal GDP Growth

Historically, China Has Scaled Back On Deleveraging When Credit Growth Has Fallen Close To Nominal GDP Growth

We do not expect Chinese credit growth to rise as much as in past releveraging cycles. However, this is because the economy is in better shape, not because there is some intrinsic constraint to increasing debt from current levels. China’s elevated savings rate has kept interest rates well below trend nominal GDP growth, which is the key determinant of debt sustainability (Chart 6).3 As long as the central government maintains an implicit guarantee on most local and corporate debt, as it is currently doing, default risk will remain minimal. In any case, given that total debt stands at 240% of GDP, even a one percentage-point increase in credit growth would generate a hefty 2.4% of GDP in credit stimulus. The Chinese credit impulse leads imports by about six-to-nine months (Chart 7). This bodes well for global trade in the second half of the year. Chart 6China's High Savings Rate Has Kept Interest Rates Well Below Trend Nominal GDP Growth

China's High Savings Rate Has Kept Interest Rates Well Below Trend Nominal GDP Growth

China's High Savings Rate Has Kept Interest Rates Well Below Trend Nominal GDP Growth

Chart 7Global Trade Will Benefit From A Chinese Reflationary Impulse

Global Trade Will Benefit From A Chinese Reflationary Impulse

Global Trade Will Benefit From A Chinese Reflationary Impulse

A Lull In The Trade War? A de-escalation in the trade war would help matters. As a self-professed master negotiator, Donald Trump needs to secure a deal with China before next year‘s presidential election, while also convincing American voters that the agreement was concluded on favorable terms for the United States. Reaching a deal with China early on in his term would have been risky for Trump if it had failed to bring down the bilateral trade deficit – an entirely likely outcome given how pro-cyclical U.S. fiscal policy is. At this point, however, Trump could crow about making a great deal with China while reassuring voters that the product of his brilliance will be realized only after he has been re-elected. Thus, the likelihood that Trump will seek to strike a deal has risen. For their part, the Chinese want as much negotiating leverage as they can muster. This means being able to convincingly demonstrate that their economy is strong enough to handle the repercussions from turning down a trade deal that fails to serve their interests. Since the credit cycle is the dominant driver of Chinese growth, this requires putting the deleveraging campaign on the backburner. Faster Global Growth And Stronger Domestic Demand Will Benefit Europe Stronger Chinese growth will help the European export sector later this year. The export component of the Chinese Caixin PMI has moved up from its lows. It leads the euro area PMI by about three months. Meanwhile, euro area domestic demand will benefit from a more accommodative fiscal policy and lower bond yields. The decline in bond yields will be especially helpful to Italy. The spike in yields and loss of business confidence following the election of a populist government last March plunged the economy into recession (Chart 8). Now that the 10-year BTP yield has fallen more than 100 bps from its highs, the Italian economy should start to perk up. The ECB will not raise rates this year even if domestic growth speeds up, but the market will probably price in a few rate hikes in 2020 and beyond. This will allow for a modest re-steepening of yield curves in core European bond markets, which should be positive for long-suffering bank profits. Brexit remains a concern. The ongoing saga has reached the farcical stage where: 1) The U.K. has voted to leave the EU; but 2) Parliament has voted to stay in the EU unless it reaches a satisfactory deal with Brussels; while 3) rejecting the only deal with Brussels that was on offer. Given that most British voters no longer want Brexit (Chart 9), we think that the government will kick the proverbial can down the road until a second referendum is announced or a “soft Brexit” deal is formulated. Either outcome would be welcomed by markets. Chart 8Italian Bond Yields Are A Headwind No More

Italian Bond Yields Are A Headwind No More

Italian Bond Yields Are A Headwind No More

Chart 9U.K.: In The Case Of A Do-Over, The Remain Side Would Likely Win

U.K.: In The Case Of A Do-Over, The Remain Side Would Likely Win

U.K.: In The Case Of A Do-Over, The Remain Side Would Likely Win

What Will The Fed Do?

Chart 10

Last year’s “Christmas Crash” clearly shifted the Fed’s reaction function in a more dovish direction. We do not expect Jay Powell to raise rates over the next few months, but a reacceleration in global growth is likely to prompt the Fed to tighten anew in December. The Fed will continue raising rates once per quarter in 2020, before accelerating the pace of tightening in 2021 in response to rising inflation. In all, we see the fed funds rate increasing to around 4% by the end of this cycle. This represents nine quarter-point hikes more than the market is currently discounting (Chart 10). We were stopped out of our short fed funds futures trade, but we recommend that clients short the June-2021 fed funds futures or a similar instrument. The U.S. Economy: Great Again Fundamentally, the U.S. economy is on solid ground and can handle higher interest rates. Unlike a decade ago, the housing market is in good shape (Chart 11). The homeowner vacancy rate stands near a record low. Judging by FICO scores, the quality of mortgage lending remains high. The labor market is also firm, with job openings hitting another record high in February (Chart 12). The combination of a healthy housing and labor market is invariably good for consumers. Chart 11U.S. Housing Fundamentals Are Solid

U.S. Housing Fundamentals Are Solid

U.S. Housing Fundamentals Are Solid

Chart 12The U.S. Labor Market Is Firm

The U.S. Labor Market Is Firm

The U.S. Labor Market Is Firm

Chart 13

The personal savings rate currently stands at 7.6%, notably higher than one would expect based on the ratio of household net worth-to-disposable income (Chart 13). A decline in the savings rate would allow consumer spending to increase more quickly than income. With the latter being propped up by rising wages, this will be bullish for consumption. Capital spending intentions have dipped over the past few months, but remain elevated by historic standards (Chart 14). The real nonresidential capital stock has grown by an average of only 1.7% since the start of the recovery, down from 3% in the pre-recession period (Chart 15). A cyclical upswing in productivity growth, rising labor costs, and low levels of spare capacity should all motivate businesses to invest in new plant and equipment. Chart 14Capital Spending Intentions Have Softened, But Remain Elevated

Capital Spending Intentions Have Softened, But Remain Elevated

Capital Spending Intentions Have Softened, But Remain Elevated

Chart 15There Is Room For More U.S. Capital Investment

There Is Room For More U.S. Capital Investment

There Is Room For More U.S. Capital Investment

Corporate Debt: How Much Of A Risk? Chart 16U.S. Corporate Debt Is Not Extreme By Global Standards

U.S. Corporate Debt Is Not Extreme By Global Standards

U.S. Corporate Debt Is Not Extreme By Global Standards

Corporate debt levels have increased significantly in recent years, while underwriting standards have deteriorated, as evidenced by the proliferation of covenant-lite loans. Nevertheless, the situation is far from dire. Relative to other countries, U.S. corporate debt is quite low (Chart 16). At 143% of GDP, corporate debt in France is twice that of the United States. This is not to suggest that everything is fine in the French corporate sector; but the fact is that France has not had a corporate debt crisis. This signals that the U.S. is not at imminent risk of one either. Netting out cash, U.S. corporate debt as a share of GDP is at the same level it was in 1989, a year in which the fed funds rate was close to nine percent. The ratio of corporate net debt-to-EBITD remains reasonably low. The interest coverage ratio is above its historic average. In addition, corporate assets have also risen quite briskly over the past few years, which has kept the corporate debt-to-asset ratio broadly stable (Chart 17). The corporate sector financial balance – the difference between corporate income and spending – is still in positive territory at 1% of GDP. Every recession in the past 50 years began when the corporate sector financial balance was in deficit (Chart 18). Chart 17U.S. Corporate Debt: How High?

U.S. Corporate Debt: How High?

U.S. Corporate Debt: How High?

Chart 18Corporate Sector Financial Balance Still In Surplus

Corporate Sector Financial Balance Still In Surplus

Corporate Sector Financial Balance Still In Surplus

Unlike mortgages, which are often held by leveraged institutions, most corporate debt is held by unleveraged players such as pension funds, insurance companies, mutual funds, and ETFs. Bank loans account for only 18% of nonfinancial corporate sector debt, down from 40% in 1980 (Chart 19). The share of leveraged loans held by banks has declined from about 25% a decade ago to less than 10% today. Moreover, banks today hold much more high-quality capital than in the past (Chart 20). This makes corporate debt less systemically important for the economy. Chart 19Banks Have Reduced Their Exposure To The Corporate Sector

Banks Have Reduced Their Exposure To The Corporate Sector

Banks Have Reduced Their Exposure To The Corporate Sector

Chart 20U.S. Banks Are Well Capitalized

U.S. Banks Are Well Capitalized

U.S. Banks Are Well Capitalized

One of the reasons we turned more bullish on risk assets in December was because stocks had plunged and corporate spreads widened without much follow-through in financial stress indices. For example, the infamous TED spread barely budged (Chart 21). Chart 21TED Spreads Are Well Behaved, Indicating No Major Signs Of Financial Stress

TED Spreads Are Well Behaved, Indicating No Major Signs Of Financial Stress

TED Spreads Are Well Behaved, Indicating No Major Signs Of Financial Stress

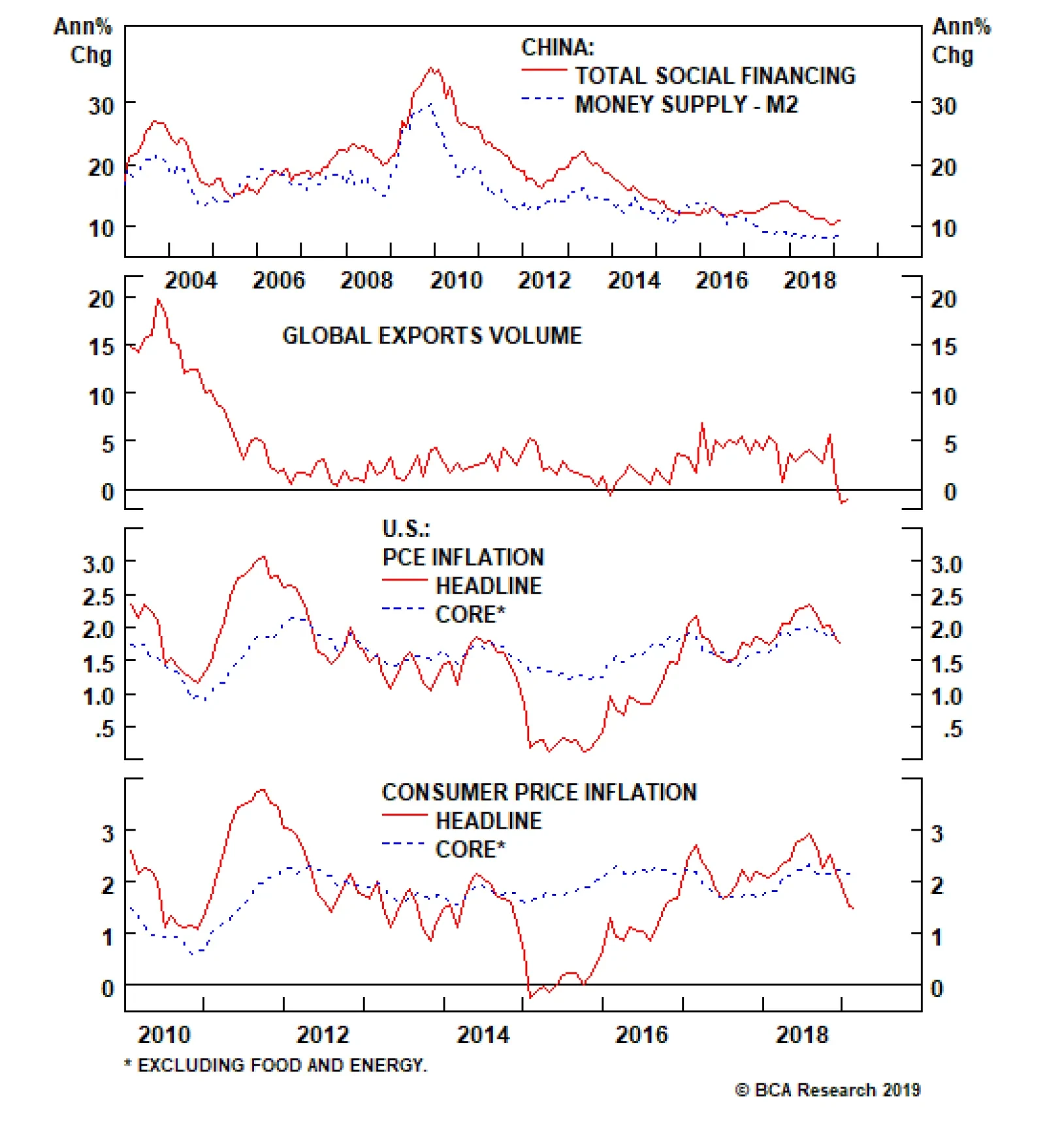

Everyone Agrees With Larry Given the lack of major imbalances in the U.S. economy, why do investors believe that the Fed cannot raise rates further even though the Fed funds rate in real terms is barely above zero? The answer is that investors appear to have bought into Larry Summers’ secular stagnation thesis, which posits that the neutral rate of interest is much lower today than it was in the past. We have some sympathy for this thesis, but it is important to remember that it is a theory about the long-term determinants of interest rates such as productivity and demographic trends. The theory says little about the cyclical drivers of interest rates, including the amount of spare capacity in the economy, the stance of fiscal policy, credit growth, and wage trends. Earlier this decade, when we were still very bullish on bonds, one could have plausibly argued that the economy needed extremely low interest rates: The output gap was still large; the deleveraging cycle had just begun; home and equity prices were depressed; wage growth was anemic; and fiscal policy had turned restrictive after a brief burst of stimulus during the Great Recession. Far From Neutral? All of the forces mentioned above have either fully or partially reversed course over the past few years. Take fiscal policy as one example. The IMF estimates that the U.S. structural budget deficit averaged 3.3% of GDP in 2014-15. In 2019-20, the IMF reckons the deficit will average 5.6% of GDP. To what extent has easier fiscal policy raised the U.S. neutral rate of interest? Let us conservatively assume that every $1 of additional fiscal stimulus adds $1 to aggregate demand. In this case, fiscal policy has added 2.3% of GDP to aggregate demand over the past five years. Suppose that a one-percentage point increase in aggregate demand raises the neutral rate of interest by 1%, which is in line with the specification of the Taylor Rule that former Fed Chair Janet Yellen favored. This implies that fiscal policy alone has raised the neutral rate by over two percentage points. The discussion above suggests that cyclical factors may have pushed up the neutral rate considerably, even if long-term structural factors are still dragging it down. Since the Fed is supposed to set interest rates with an eye on what is appropriate for the economy over the next year or two, rates may end up staying too low for too long. This will cause the economy to overheat, eventually leading to a surge in inflation. The Inflation Boogeyman The good news is that none of our favorite indicators point to a major imminent inflationary upswing (Chart 22): Despite higher tariffs, consumer import price inflation has slowed; core intermediate producer price inflation has decelerated; the prices paid components of the ISM and regional Fed surveys have plunged; inflation surprise indices have rolled over; and both survey and market-based measures of inflation expectations remain below where they were last summer. In keeping with these developments, BCA’s proprietary Pipeline Inflation Indicator has fallen to a two-and-a-half-year low. Wage growth has accelerated, but productivity growth has increased by even more. As a result, unit labor cost inflation has been coming down since the middle of last year. Unit labor costs lead core CPI inflation by about 12 months (Chart 23). This implies that consumer price inflation is unlikely to reach uncomfortably high levels at least until the second half of next year. Chart 22No Symptoms of An Imminent Major Inflationary Upswing In The U.S. ...

No Symptoms of An Imminent Major Inflationary Upswing In The U.S. ...

No Symptoms of An Imminent Major Inflationary Upswing In The U.S. ...

Chart 23... And Decelerating Unit Labor Costs Will Dampen Inflationary Pressures For The Time Being

... And Decelerating Unit Labor Costs Will Dampen Inflationary Pressures For The Time Being

... And Decelerating Unit Labor Costs Will Dampen Inflationary Pressures For The Time Being

At that point, risks are high that inflation will move up. This could force the Fed to start raising rates aggressively in early-2021, a course of action that will push up the dollar and cause equities and spread product to sell off. The resulting tightening in financial conditions will probably plunge the U.S. and the rest of the world into recession in mid-to-late 2021. Stay Bullish Global Equities For Now, Turn Defensive Late Next Year Chart 24Analyst Expectations Are Quite Muted

Analyst Expectations Are Quite Muted

Analyst Expectations Are Quite Muted

The two-stage Fed tightening cycle discussed above – gradual rate hikes starting in December and continuing into 2020, and more aggressive hikes thereafter in response to rising inflation – shapes our investment views over the next few years. The Key Financial Market Forecasts Chart at the beginning of this publication provides a rough sketch of where we think the main asset classes are heading. We suspect that equities and other risk assets will be able to digest the first stage of rate tightening, albeit with heightened volatility around the time when the Fed starts preparing the market for another hike later this year. Unlike last September, earnings estimates are much more conservative. Bottom-up estimates foresee EPS rising by 3.9% in the U.S. and 5.4% in the rest of the world in 2019 (Chart 24). The combination of faster growth, easier financial conditions, and ongoing share buybacks implies some upside to these numbers. Perhaps more importantly, unlike in September, the Fed will only start hiking rates if the economy is performing well. Powell erred in saying that “rates were a long way from neutral” just when the U.S. economy was starting to slow. Had he uttered those words when U.S. growth was still accelerating, investors would have probably disregarded them. Jay Powell won’t make the same mistake again. Rather, he will make a different one: He will let the economy overheat to the point where the Fed finds itself clearly behind the curve and forced to scramble to catch up. The resulting stagflationary environment – where growth is slowing due to a shortage of available workers and inflation is on the upswing – will be toxic for equities and other risk assets. While it is difficult to be precise about timing, we recommend that investors maintain a modestly pro-risk stance over the next 12-to-18 months. However, they should pare back exposure to equities and spread product late next year before the Fed ramps up the pace of rate hikes. Prepare To Temporarily Upgrade International Stocks The U.S. stock market tends to be “low beta” compared to other bourses. If global growth accelerates in the second half of this year, international stocks will outperform their U.S. counterparts. We sold our put on the EEM ETF for a gain of 104% on Jan 3rd, and now recommend being outright long EM equities. We will be looking to upgrade both EM and European equities to overweight in the coming weeks in currency-unhedged terms once we see more confirmatory evidence of a global growth revival. We have mixed feeling about Japanese stocks. Stronger global growth will benefit Japanese multinationals, but firms focused on the domestic market may suffer if the government goes ahead and raises the sales tax in October. We would hold off upgrading Japanese stocks for the time being. At the global sector level, we pared back our defensive tilt earlier this year, after having turned more cautious last summer. We recommend that investors overweight energy and industrials. We are also warming up to financials and materials. The former will benefit from a steepening in yield curves later this year as well as from faster credit growth. The latter will gain from a more robust Chinese economy. We would maintain a neutral allocation to health care, info tech, and communication services. Real estate and utilities will both suffer once bond yields start moving higher. Classically defensive sectors such as consumer staples will also underperform. Global Bond Yields Likely To Rise Global bond yields are likely to rise over the next 12-to-18 months as growth surprises on the upside. Yields will continue rising into the first half of 2021 as inflation accelerates. Unlike in past risk-off episodes, Treasurys will not provide much of a safe haven in the lead up to the next recession. As noted above, one of the reasons that bond yields are so low today is because the term premium is very depressed. The cumulative effect of Fed bond purchases has probably depressed the term premium, but the bigger impact has stemmed from the fact that investors see Treasurys as an insurance policy against various macro risks. Investors are accustomed to thinking that when an economy slides into recession, equity prices will fall, the housing market will deteriorate, wage gains will recede, job prospects will worsen, but at least the value of their bond portfolio will go up! The problem with this reasoning is that it is only valid when the Fed is hiking rates in response to stronger growth. If the Fed is hiking rates because inflation is getting out of hand, Treasury yields could end up rising while stocks are falling. This was actually the norm between the late-1960s and early-2000s (Chart 25). Chart 25Treasury Yields Could Rise While Stocks Fall

Treasury Yields Could Rise While Stocks Fall

Treasury Yields Could Rise While Stocks Fall

If Treasurys lose their safe-haven status, the term premium will move higher. A vicious circle could develop where rising bond yields weaken the stock market, causing investors to flood out of both stocks and bonds and into cash, leading to even higher bond yields and lower equity prices. Investors should maintain a modest short duration stance towards Treasurys over the next 12 months, and then move to maximum underweight duration in mid-2020 as inflation starts to break out. Going long duration will only make sense once the Fed has raised interest rates into restrictive territory and the economy slides into recession. That is not likely to occur until the second half of 2021. Regionally, we favor European, Canadian, Australian, New Zealand, and especially Japanese government bonds over the next 12 months relative to U.S. Treasurys. The U.S. economy is at the greatest risk of overheating. In currency-hedged terms, the 10-year U.S. Treasury yield is among the lowest in the world (Table 1). Japanese 10-year bonds, for example, offer 2.72% in currency-hedged terms, while German bunds command 2.94%. Table 1Bond Markets Across The Developed World

Second Quarter 2019 Strategy Outlook: From Dead Zone To End Zone

Second Quarter 2019 Strategy Outlook: From Dead Zone To End Zone

The U.S. Dollar: Heading Towards A Soft Patch Gauging the outlook for the U.S. dollar is a bit tricky. Even though the Fed will only be raising rates gradually over the next 12 months, it will still hike more than what is discounted by markets. With most other central banks still sitting on the sidelines, short-term rate differentials are likely to move in favor of the greenback. That said, aside from Japan, stronger global growth will likely prompt investors to price in a few more rate hikes in other developed economies in 2020 and beyond. Consequently, long-term yield differentials may not widen by as much as short-term differentials. Perhaps more importantly, the U.S. dollar is a countercyclical currency, meaning that it moves in the opposite direction of global growth (Chart 26). This countercyclicality stems from the fact that the U.S. economy is more geared towards services than manufacturing compared with the rest of the world (Chart 27). As such, when global growth accelerates, capital tends to flow from the U.S. to the rest of the world, translating into more demand for foreign currency and less demand for dollars. Chart 26The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

Chart 27The U.S. Is A Low-Beta Play On Global Growth

The U.S. Is A Low-Beta Play On Global Growth

The U.S. Is A Low-Beta Play On Global Growth

If global growth picks up in the back half of this year, the dollar will likely peak in the second quarter and weaken over the remainder of 2019 and into 2020. The dollar’s trajectory may thus follow a similar course to the one in 2017, a year in which the Fed raised rates four times, but the broad trade-weighted dollar nevertheless managed to weaken by 7%. Chart 28The Yen Is A Risk-Off Currency

The Yen Is A Risk-Off Currency

The Yen Is A Risk-Off Currency

As was the case in 2017, the euro will probably gain ground later this year against the U.S. dollar as will most EM and commodity currencies. However, just as the Japanese yen failed to participate in the rally that most currencies experienced against the dollar in 2017, it will struggle to gain much traction against the greenback. The yen is a “risk-off” currency and thus tends to fall whenever global risk assets rally (Chart 28). In addition, the yen will suffer if global bond yields move up relative to JGB yields later this year, as will likely be the case if the BoJ is forced to prolong its yield curve control regime in the face of tighter fiscal policy. We would go long EUR/JPY on any break below 123. After First Weakening, The Dollar Will Rally Again Late Next Year As the U.S. economy encounters ever more supply-side constraints in 2020, growth will slow and inflation will accelerate. The Fed will respond by hiking rates more quickly than inflation is rising. The resulting increase in real interest rates will put upward pressure on the dollar. In this stagflationary environment, equities will tumble and credit spreads will widen. Tighter U.S. financial conditions will reverberate around the world, causing global growth to decelerate even more than it would have otherwise. This will further turbocharge the dollar. The greenback will only peak once the Fed starts cutting rates in late-2021. Commodities: Getting More Bullish A weaker dollar later this year, along with stronger global growth led by a resurgent China, will be bullish for commodities. BCA’s commodity strategists recommend going long copper at current prices. They are also maintaining their bullish bias towards oil. They expect Brent to average $75/bbl this year and $80/bbl in 2020. Higher U.S. shale output will be offset by delays in building out deepwater export facilities, which will keep supply fairly tight. In past reports, we discussed the merits of buying gold as an inflation hedge. However, we held back from doing so because of our bullish dollar view. Now that we see the dollar peaking over the next few months, we would be buyers of gold on any break below $1275/ounce. Peter Berezin, Chief Global Strategist Global Investment Strategy peterb@bcaresearch.com Footnotes 1 Please see Global Investment Strategy Weekly Report, “Gretzky’s Doctrine,” dated March 1, 2019. 2 Please see Global Investment Strategy Weekly Report, “Low Odds Of An FCI Doom Loop,” dated January 4, 2019. 3 Please see Global Investment Strategy Weekly Report, “Is There Really Too Much Government Debt In The World?” dated February 22, 2019. Strategy & Market Trends MacroQuant Model And Current Subjective Scores

Chart 29

Tactical Trades Strategic Recommendations Closed Trades

Highlights Just when it looked like the agricultural complex was starting to perk up, it was slapped down again. After crawling its way back from a mid-2018 crash – retracing more than half of its decline – the CCI Grains and Oilseeds index plummeted in February, declining by nearly 9% (Chart Of The Week). The decline was broad-based, but was led by wheat, which was dragged down by muted demand and accounted for most of the index’s decline. Looking forward, we expect U.S. financial conditions and developments on the trade-war front to remain the main forces driving ag prices. Ample inventories will provide the cushion necessary to moderate the impact of potential supply-side shocks. Highlights Energy: Overweight. Venezuela suffered another power outage earlier this week, indicating the deterioration of its infrastructure is accelerating. While officials claim to have restored power, we expect more such outages going forward, which will severely reduce the country’s production and export capacity. Separately, Aramco announced it will buy 70% of Sabic, a Saudi state-owned petchem producer, for $69 billion, according to the Wall Street Journal. Base Metals: Neutral. China’s MMG Ltd was set to declare force majeure following protests at its Las Bambas mine in Peru earlier this week. The mine produces ~ 385k MT p.a., most of which goes to China. Precious Metals: Neutral. The inversion of the U.S. yield curve put a bid into the gold market this week, as investors sought a safe-haven refuge. Continued weakness in bond yields, and accommodative central banks responding to low inflation expectations globally will continue to support gold. Agriculture: Underweight. A more patient Fed will be supportive of ag prices in 2H19, as we discuss below. Feature Chart of the WeekWheat Had A Rough Start To 2019

Wheat Had A Rough Start To 2019

Wheat Had A Rough Start To 2019

A Patient Fed Will Support Ags In 2H19 While differences across ag markets will arise due to idiosyncratic supply shocks and targeted trade policies, a common determinant of ag price movements more generally is U.S. financial conditions. Since our last assessment of global ag markets, Fed policymakers have adopted a much more patient approach to monetary policy.1 In line with the pause in the Fed’s rates-normalization policy, financial conditions have eased considerably (Chart 2). We believe this will, ceteris paribus, bring relief to commodity markets in general, ags in particular, in the second half of this year. Chart 2Easier Financial Conditions Bode Well For Ags

Easier Financial Conditions Bode Well For Ags

Easier Financial Conditions Bode Well For Ags

The bulk of this relief will be transmitted through the impact of a weaker dollar. Since the dollar is a countercyclical currency, its weakness implies an improvement in global growth. This more solid economic backdrop is associated with greater aggregate demand, particularly in EM economies, as well as demand for agricultural products. The lagged effects of financial tightening, weak Chinese credit growth and the trade war will persist in 2Q19. Furthermore, when the USD weakens against the currencies of ag exporting countries, farmers there are incentivized to hoard or cut exports – thus reducing supply – awaiting periods when a stronger greenback will raise their profits. At the same time, ags priced in USD become relatively more affordable for importing nations, incentivizing them to raise consumption. The net impact of this contraction in supply amid greater demand will pull up prices – illustrated by the relatively tight inverse relationship between ag prices and the dollar (Chart 3). Chart 3A Weaker USD Will Be A Tailwind In 2H19

A Weaker USD Will Be A Tailwind In 2H19

A Weaker USD Will Be A Tailwind In 2H19

Going into mid-2019, we expect global economic indicators to continue to be uninspiring. The lagged effects of financial tightening, weak Chinese credit growth and the trade war will persist in 2Q19. However, as these factors fade and give way to an improvement in global economic conditions and easier financial conditions, we expect the dollar to peak around mid-year. As such, a resurgence in global growth in the second half of the year will be reflected in an improvement in the value of the currencies of major ag exporters ex-U.S. (Chart 4). Ceteris paribus, this also benefits ag prices. Chart 4Weak Local Currencies Supporting Farm Profits, Incentivizing Production

Weak Local Currencies Supporting Farm Profits, Incentivizing Production

Weak Local Currencies Supporting Farm Profits, Incentivizing Production

China’s Economy Remains Central Our outlook hinges on developments in the Chinese economy. Peter Berezin – our Chief Global Investment Strategist – expects Chinese authorities to not only stabilize credit growth, but also increase it, creating room for improvement in the world’s second largest economy.2 This combination of supportive global growth and a softer dollar bodes well for ag prices in 2H19. The Fed pause and associated easing in U.S. financial conditions will support global growth, causing the U.S. dollar to weaken – a bullish force for ag markets. Apart from the currency impact, easy financial conditions are supportive of global growth. A rise in income levels of emerging economies will support demand for goods and services generally, and agricultural commodities specifically.3 The market now expects 36 and 51 basis points of rate cuts over the coming 12 and 24 months, respectively. Similarly, following last week’s FOMC meeting, the median Fed dot indicates no rate hikes this year from the U.S. central bank, and only one in 2020. While our Global Investment Strategists would not be surprised to see a hike this year, the noticeably less hawkish tone in the Fed’s forward guidance and dot plots are positive for ag markets.4 Looking beyond that into late-2020 or early 2021, a potential pick-up in inflation will force the Fed to take a more hawkish stance, and once again support the U.S. dollar. This will weigh down on ag prices over the strategic time horizon. Bottom Line: The Fed pause and associated easing in U.S. financial conditions will support global growth, causing the U.S. dollar to weaken – a bullish force for ag markets. However, this is unlikely to occur before mid-year. In the meantime, a stronger dollar on the back of the lagged effects of growth dampening events in 2018, will remain a headwind. Ample Inventories Will Cushion Against Supply Shocks Putting aside the more or less uniform impact of U.S. financial conditions, individual supply-demand fundamentals will manifest as idiosyncratic risks and opportunities. The USDA has been revising its projections for ending stocks higher in its monthly World Agricultural Supply and Demand Estimates (WASDE) across the board since it released the first projections for the 2018/2019 crop year last May. However, we find that solely on the back of fundamentals, soybeans are more likely to resist upward pressure from easier U.S. financial conditions in 2H19 vs. wheat and corn. The USDA’s latest projections for the current crop year indicate that global bean markets are well supplied. Expectations of a global surplus this crop year – for the seventh consecutive year – will add to the growing cushion (Chart 5). Chart 5Beans Surplus Will Add To the Glut

Beans Surplus Will Add To the Glut

Beans Surplus Will Add To the Glut

Since May, global ending bean stocks have been revised higher by a total of 20.47mm MT. The change in projections comes on the back of upward revisions to production and beginning stocks, compounded by downward revisions to consumption. The latter will likely contract further if the U.S. and China do not reach an agreement on the trade front (see below). Consequently, unless a weather disruption weakens supply, we expect soybean inventories to stand at record highs relative to consumption at the end of the current crop year. In the case of wheat, the impact on prices will likely be marginal. The global balance is expected to shift to a deficit in the current marketing year, following five years of surplus (Chart 6). While this is a positive for wheat prices, given that global inventory levels are relatively elevated – capable of supporting 37% of consumption – and the current deficit is relatively small, we do not expect the deficit to pressure prices in the near term. Chart 6Elevated Wheat Inventories Will Cushion Against Minor Deficit

Elevated Wheat Inventories Will Cushion Against Minor Deficit

Elevated Wheat Inventories Will Cushion Against Minor Deficit

Despite continued downward revisions to the USDA’s wheat production projections, expectations of ending stocks have actually risen on the back of downward revisions to consumption. Similarly, corn fundamentals are also unlikely to sway prices much. The grain is expected to remain in deficit for the second consecutive year, which will pull inventories down off their 2016/17 peak to be capable of covering ~27% of global consumption (Chart 7). Despite this contraction in availability, global supplies remain relatively elevated, especially compared to the 2003 to 2012 period. Thus unless there is a significant supply shock, we don’t expect much support from fundamentals. Chart 7A Global Corn Deficit ...

A Global Corn Deficit ...

A Global Corn Deficit ...

Unlike wheat demand, which has been downgraded, the USDA has revised corn consumption up relative to the first projections for the crop year released last May. Nevertheless, stronger expectations of consumption have been overwhelmed by upward revisions to production and beginning inventory levels. Given that world inventories already are bloated, we do not expect the likely deficit in wheat and corn supplies this crop year to pressure prices much to the upside. Since the mid-1990s, U.S. farmers had been planting more corn and wheat at the expense of soybean acreage (Chart 8). On a global level, while wheat remains more popular in terms of acreage, it is generally trending downwards, while corn and soybean plantings are trending up. However, over the longer term, U.S. farmers are expected to dedicate more land to corn relative to soybeans. Chart 8... Will Be Met By Rising U.S. Acreage

... Will Be Met By Rising U.S. Acreage

... Will Be Met By Rising U.S. Acreage

Bottom Line: Given that world inventories already are bloated, we do not expect the likely deficit in wheat and corn supplies this crop year to pressure prices much to the upside. Similarly, a global glut in soybean supplies will only add to swelling inventories. The Trade War And Soybeans: It Ain’t Over Till It’s Over Aside from U.S. financial conditions and supply-demand balances, U.S. trade policy has also been roiling ag markets since China slapped U.S. soybeans with 25% tariffs in mid-2018. In fact, since the escalation of the trade dispute, soybean prices have been moving largely in response to developments on the trade front (Chart 9). As developments since the G20 Summit in Buenos Aires last December have been more favorable, soybean markets are on the path to recovery. Chart 9Markets Optimistic Of A Trade War Resolution

Markets Optimistic Of A Trade War Resolution

Markets Optimistic Of A Trade War Resolution

So far, even though U.S. soybean exports to China picked up over the past two months, total U.S. exports still lag levels typical for this time of year (Chart 10). This comes despite U.S. efforts to raise shipments to other trading partners. Furthermore, U.S. exports will now be in direct competition with the Brazilian crop, which usually dominates trade flows at this time of year (Chart 11).

Chart 10

While the U.S. tariff hike from 10% to 25% on $200bn of Chinese goods has been postponed, a resolution to the trade war has yet to occur. The path to a resolution is fraught with risks.

Chart 11

While the U.S. tariff hike from 10% to 25% on $200bn of Chinese goods has been postponed, a resolution to the trade war has yet to occur. The path to a resolution is fraught with risks. The Trump-Xi meeting that was expected to occur in late-March was postponed; the next most likely date for a meeting is at the G20 summit in end-June. This leaves another 3 months of trade uncertainty. Nevertheless, our models indicate that soybeans are now priced at fair value, based on U.S. financial variables – absent a trade war (Chart 12).

Chart 12

Furthermore, the premium priced into Brazilian beans above those traded on the CBOT has returned to its historical average (Chart 13). Thus, we do not expect a further reduction in the premium in the event Sino-U.S. trade negotiations are successful. Chart 13Premium For Brazilian Beans Has Normalized

Premium For Brazilian Beans Has Normalized

Premium For Brazilian Beans Has Normalized

Rather, markets will be disappointed if the U.S. and China are unable to conclude a deal. This would put CBOT prices at risk and support the premium on those traded in Brazil. Given that our geopolitical strategists assign a non-negligible 30% probability that the trade war escalates further, we believe markets are overly optimistic that a deal will be concluded.5 If the trade war drags on and turns into a multi-year conflict, soybean markets will likely take a more meaningful hit. According to the USDA’s latest long-term projections released earlier this month, China’s soybean imports were projected to rise 32.1mm MT during the 2018-28 period – a massive downward revision from the 46mm MT expected for the 2017-2027 period contained in the previous long-run projections. Furthermore, outbreaks of African swine fever in China may put demand there at risk. Over 100 cases have so far been reported in China, with several cases already reported in Vietnam as well. This threatens to depress China’s need for soybean as animal feed, regardless of what happens on the trade front. Bottom Line: A positive outcome from the U.S.-China trade negotiations is not a given. Nevertheless, soybean markets are treating it as such. Our geopolitical strategists assign 30% odds that a final deal falls through. This non-negligible probability threatens to cause soybean prices to relapse anew, should Sino-U.S. trade negotiations break down. Roukaya Ibrahim, Editor/Strategist Commodity & Energy Strategy RoukayaI@bcaresearch.com Footnotes 1 Please see “2019 Key Views: Policy-Induced Volatility Will Drive Markets,” published by BCA Research’s Commodity & Energy Strategy December 13, 2018. It is available at ces.bcaresearch.com. 2 Please see BCA Research’s Global Investment Strategy Weekly Report titled “What’s Next For The Dollar,” dated March 15, 2019, available at gis.bcaresearch.com. 3 Please see BCA Research’s Commodity & Energy Strategy Weekly Report titled “Global Financial Conditions Will Drive Grain Prices In 2018,” dated November 30, 2017, available at ces.bcaresearch.com. 4 Please see BCA Research’s Global Investment Strategy Weekly Report titled “Questions From The Road,” dated March 22, 2019, available at gis.bcaresearch.com. 5 Please see BCA Research’s Geopolitical Strategy Special Report titled “China-U.S. Trade: A Structural Deal?,” dated March 6, 2019, available at gps.bcaresearch.com. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades Commodity Prices and Plays Reference Table Trades Closed in 2019 Summary of Trades

Image

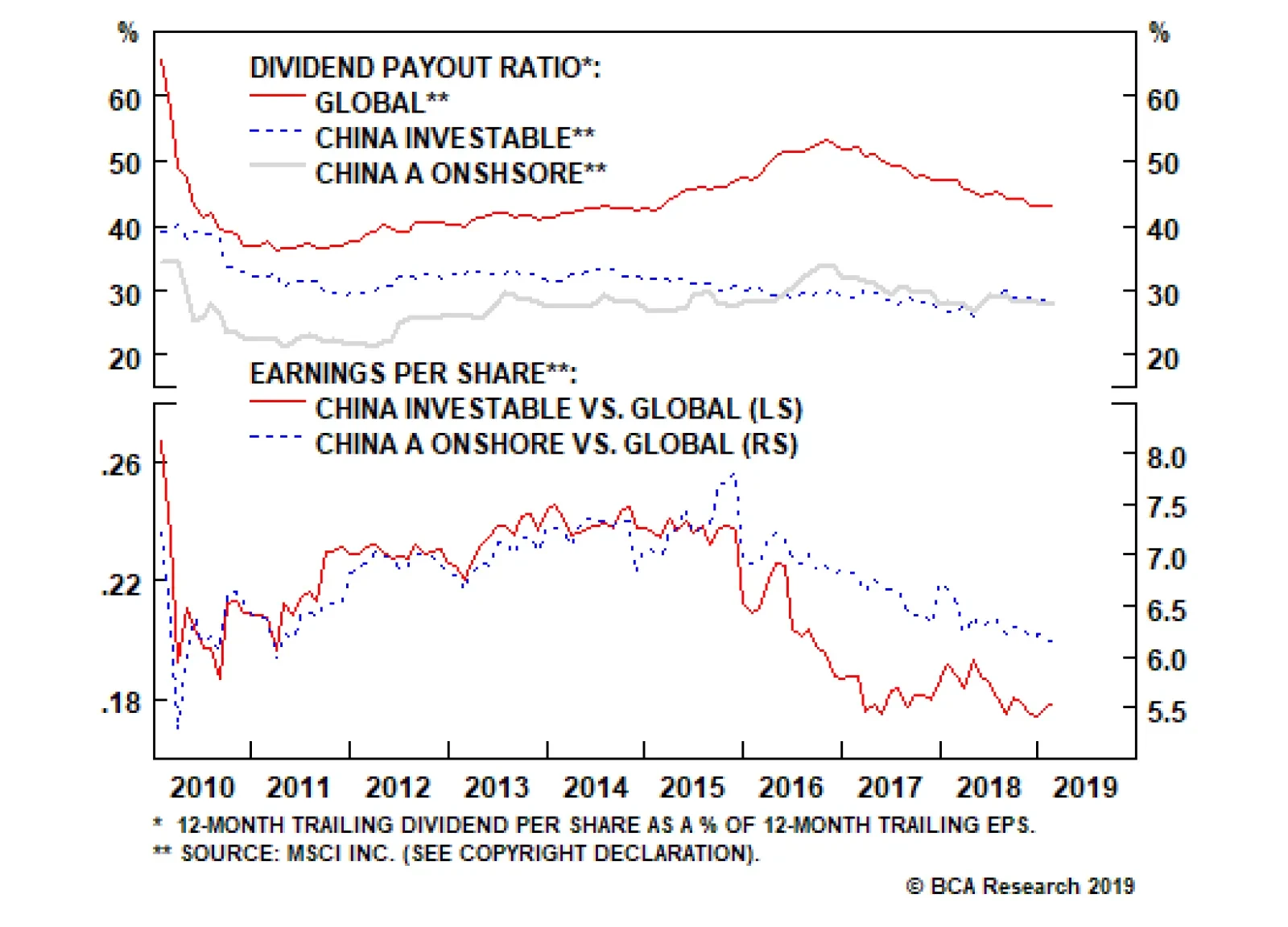

In a world where many financial assets are chronically expensive and where Chinese policymakers appear to be responding to weaker economic activity, some investors question whether Chinese stocks deserve to be priced at a discount. Our China Investment…

Certainly, several positive developments are pointing towards domestic demand meaningfully improving. Chinese monetary conditions have become extremely easy, credit is no longer contracting and even surged in January, the Caixin PMI rose markedly in February,…

Highlights Taiwan’s semiconductor sector is facing both cyclical and structural headwinds. Semiconductor exports will continue to contract over the next six months or so, on retrenching global demand. In the long run, Taiwan is facing increasing competition from Korea in the high-end supply, and from mainland China in the medium- to low-end supply of the semiconductor market. The latest rebound in Taiwanese share prices is unsustainable, and they are about to relapse anew. Within an EM equity portfolio, we recommend staying neutral on Taiwanese stocks for now. Feature Taiwan’s exports and manufacturing are in full-blown recession. The equity market has rebounded after a major selloff last year. However, the overall manufacturing PMI and its export sub-component are extremely weak, and do not justify the latest share-price rebound (Chart I-1). Chart I-1Taiwanese Equities: Unsustainable Rally

Taiwanese Equities: Unsustainable Rally

Taiwanese Equities: Unsustainable Rally

Are manufacturing activity and exports about to recover? Or will the stock market rally fade? Our answer is the latter. There are currently no signs suggesting a recovery in exports is imminent. Moreover, the engine of the economy – the semiconductor sector – is facing both cyclical and structural headwinds. We remain negative on Taiwanese stocks in absolute terms. Within an EM equity portfolio, we recommend a market-weight allocation to Taiwanese stocks for now. Importance Of Semiconductors Over the past 15 years, the semiconductor sector has become the cornerstone of the Taiwanese economy. The Taiwanese economy is highly dependent on its external sector, as exports contribute to nearly 70% of GDP. As such, Taiwan’s business cycle has often been closely associated with its export sector. This means the region’s growth outlook relies on both external demand (a cyclical factor) and the competitiveness of its export sector (more of a structural factor). Over the past 15 years, the semiconductor sector has become the cornerstone of the Taiwanese economy. It contributes to over one-third of the region’s total exports, up from 22% in 2009 (Chart I-2). Chart I-2Semiconductor: Cornerstone Of Taiwanese Economy

Semiconductor: Cornerstone of Taiwanese Economy

Semiconductor: Cornerstone of Taiwanese Economy

Consistently, tech stocks also account for the lion’s share of the Taiwanese stock market, representing nearly 60% of the MSCI Taiwan Index and 47% of the Taiwanese Stock Exchange (TSE) index in market-value terms. There have been two key forces behind the significant growth of Taiwan’s semiconductor sector: booming global demand for smartphones/tablets and increasing competitiveness among domestic semiconductor companies. However, looking forward, the Taiwanese manufacturing sector and its semiconductor exports are facing a double-whammy: cyclical weakness in global demand and a relative decline in Taiwan’s export ability. In the context of a negative structural outlook, a cyclical downtrend engenders substantial deterioration in manufacturing, and by extension corporate profitability. Cyclical Downturn In Global Semiconductor Demand The outlook for the Taiwanese semiconductor industry remains poor. The global semiconductor industry has already been in a cyclical downtrend since early 2018. Global smartphone sales are shrinking. Both DRAM and NAND prices have been falling (Chart I-3). Chart I-3Falling Memory Chips Prices

Falling Memory Chips Prices

Falling Memory Chips Prices

The freefall in Taiwan's new export orders seems to entail a further contraction in exports (Chart I-4). Chart I-4A Further Contraction In Exports Is Likely

A Further Contraction In Exports Is Likely

A Further Contraction In Exports Is Likely

Importantly, exports of electronics parts lead Taiwanese tech EPS growth, and currently point to an impending contraction in corporate earnings (Chart I-5). Chart I-5An Impending Contraction In Corporate Earnings

An Impending Contraction In Corporate Earnings

An Impending Contraction In Corporate Earnings

The outlook for the Taiwanese semiconductor industry remains poor. First, Taiwanese semiconductor producers are highly vulnerable to any further downside in global smartphone demand. There are two major pure-play wafer manufacturers in Taiwan: Taiwan Semiconductor Manufacturing Company (TSMC) and United Microelectronics (UMC). TSMC and UMC are the world’s largest and fourth-largest dedicated integrated circuit (IC) foundries, respectively. The smartphone sector has been the main revenue source for both companies, accounting for a 45% share for TSMC and 40% for UMC. Global smartphone demand is likely to decline further in 2019, as major markets such as mainland China and advanced economies have entered the saturation phase of mobile-phone demand. DRAMeXchange expects global smartphone production volume for 2019 to fall by 3.3% from last year following a 4% drop in 2018 (Chart I-6). Chart I-6Global Smartphone Demand Started A Downtrend

Global Smartphone Demand Started A Downtrend

Global Smartphone Demand Started A Downtrend

Smartphone sales in mainland China remain in deep contraction after two consecutive years of declines (Chart I-7). Odds are that smartphone shipments will remain sluggish amid the ongoing economic slump in the mainland’s economy. Chart I-7Smartphone Sales In Mainland China Are In A Deep Contraction

Smartphone Sales In Mainland China Are In A Deep Contraction

Smartphone Sales In Mainland China Are In A Deep Contraction

In addition, Taiwan’s TSMC is the sole chip supplier for Apple iPhones. A further decline in Apple smartphone shipments will reduce the company’s revenue and profits, damaging the region’s growth outlook. Mainland China now can produce top-notch quality smartphones at relatively cheaper selling prices. This will further crowd out higher-priced products from Apple, Samsung and others (Chart I-8). Chart I-8Apple Has Been Losing Market Share In Global Smartphone Market

Apple Has Been Losing Market Share In Global Smartphone Market

Apple Has Been Losing Market Share In Global Smartphone Market

Second, the significant surge in bitcoin prices greatly boosted cryptocurrency mining activity in 2016-‘17 as miners quickly expanded their computing power. This boosted demand for graphic process unit (GPU) chips and in turn brought higher revenue for Taiwan chipmakers between June 2016 and early 2018. However, with the bust in bitcoin prices (Chart I-3 on page 3), demand from cryptocurrency mining has vanished and is unlikely to revive soon. Indeed, Taiwan chipmakers have suffered from last year’s plunge in cryptocurrency mining activity. According to TSMC, revenue from the cryptocurrency mining-related high-performance computing (HPC) sector contracted by double digits in 2018. Given that HPC demand is the second-biggest source of revenue for TSMC, with 32% share, TSMC revenue will be curtailed as HPC chip demand will continue to decline on weak bitcoin prices. Last, developments in new technologies, such as foldable smartphones, artificial intelligence, fifth-generation (5G) mobile networks and the so-called Internet of Things (IoTs) could only produce a modest pick-up in semiconductor demand. Most of these developments are still in their infancy and early stages. Hence, their growth will not be large enough to make a cyclical difference in global semiconductor demand. For example, the foldable smartphone that Huawei recently announced is indeed appealing. However, a lack of stability in panel supply and quite-high selling prices will limit sales. WitsView, a division of TrendForce, predicts that the market penetration rate of the foldable phone will be only 0.1% in 2019, and could rise to 1% in 2020 if more panel providers join the game, enabling a significant reduction in panel costs. Moreover, these categories together account for only ~23% of TSMC’s revenue; their modest growth will not be able to make up for the losses from the smartphone and HPC sectors within Taiwan’s economy. Besides, there has been a slowdown in demand from high-growth areas such as data center servers, as well as the automotive and industrial sectors. Putting it all together, odds are that global semiconductor demand will only materially recover in 2020. By that time, more-mature 5G technology and the increasing adoption of the 5G network and 5G-related products may be able to shift global semiconductor demand from the current downturn to a cyclical uptrend. Hence, the cyclical weakness in global semiconductor demand is likely to persist over the next six months. Consequently, Taiwan’s major types of semiconductor production will likely remain in contraction, and inventory levels will stay elevated (Chart I-9 and Chart I-10). Chart I-9Taiwan: Semiconductor Output Contraction Will Likely Continue

Taiwan: Semiconductor Output Contraction Will Likely Continue

Taiwan: Semiconductor Output Contraction Will Likely Continue

Chart I-10Taiwan: Semiconductor Inventory Are Elevated

Taiwan: Semiconductor Inventory Are Elevated

Taiwan: Semiconductor Inventory Are Elevated

Bottom Line: There are no signs of an imminent recovery in exports. A Potential Decline In Taiwan’s Semiconductor Competitiveness Taiwan wafer manufacturers are facing an increasing threat from their Korean and mainland China competitors. Leadership in advanced process technologies has been a key factor in Taiwan’s strong market position in the global semiconductor industry. With cutting-edge technologies, Taiwan has been the global wafer capacity leader since 2015. As of last year, it held about 22% of global installed wafer capacity (Chart I-11).

Chart I-11

However, Taiwan wafer manufacturers are facing an increasing threat from their Korean and mainland China competitors. Korean Chipmakers While Taiwan will remain highly competitive in 7 nanometer (nm) and 10 nm wafer production, it is facing fierce competition from Korea. Manufacturing technologies designated by smaller nanometer numbers tend to have faster speeds and be more power-efficient than technologies designated by larger numbers. TSMC was the first company in the world to mass-produce 7 nm node wafers. Its 7 nm deep ultraviolet lithography (DUV) node has been in mass production since April 2018, producing chips for AMD, Apple, HiSilicon, and Xilinx. Beginning at the end of this month, TSMC will be ready to begin mass production of 7nm wafers using extreme ultraviolet lithography (EUV). The switch from 7nm DUV to 7nm EUV allows for fewer defects and fewer steps required during the production process. The company also aims to boost volume production of its 5 nm nodes in early 2020 and has a target of 3 nm wafers for 2022. Last year, wafer revenue from 7nm and 10nm chips accounted for 9% and 11% of TSMC’s total revenue, respectively (Chart I-12).

Chart I-12

Samsung has been closely following TSMC in terms of technological innovation. It started mass production of EUV-based 7nm chips last October, with a plan of risk production1 of 5nm wafers in 2019 and a target of 4nm wafers in 2022. Meanwhile, IBM announced last December that it signed an agreement with Samsung to produce its next-generation processors with Samsung’s 7nm technology. As Samsung seeks to diversify its revenue source away from memory chips, which last year contributed to about 80% of its operating profit, the company has been determined to ramp up the development of its foundry business. It aims to replace TSMC as the world’s largest foundry producer by 2030. In the near term, Samsung aims to secure a 25% market share in the global pure-play foundry market by 2023, a rise from 19% currently. Last year, Samsung surpassed Taiwan’s UMC to become the world’s second-largest dedicated chipmaker. Moreover, Samsung’s capital spending has been and will continue to be much higher than TSMC. Over the course of 2017 and 2018, Samsung spent about $46.9 billion on semiconductor capital expenditures, more than double TSMC’s $21 billion. Hence, the competition between TSMC and Samsung in the high-end chip market will intensify in the coming years. Chipmakers In Mainland China The competition between TSMC and chipmakers from mainland China is also escalating. Chart I-12 shows that 80% of TSMC’s wafer revenue comes from bigger node wafers (bigger than 10 nm). Taiwan’s second-biggest chipmaker, UMC, only produces wafers equal to or bigger than 28 nm. Therefore, the chip market using less-advanced technology than 10 nm will be the main battlefield between Taiwanese and mainland China’s chipmakers. Before 2014, there were few wafer manufacturers in mainland China, and those that did exist were too weak to compete with giant market players like TSMC. In 2014, the Chinese central government made a move to foster development within the local IC industry. Since then, the authorities have poured significant amounts of capital into semiconductor foundries, as well as companies focused on memory production, chip design and related equipment and materials. Semiconductor Manufacturing International Corporation (SMIC) is the world’s fourth-largest dedicated wafer manufacturer, and is the largest in mainland China. While 28nm will likely remain a large part of its business, SMIC plans to go into production on its 14 nm technology in the first half of 2019. The company is also working on 10nm and 7nm nodes with the use of EUV. SMIC currently counts HiSilicon and Qualcomm as customers, manufacturing smartphone chips with medium-to-low technology. As mainland China aims to increase its self-sufficiency rate for ICs significantly over the next five to 10 years, the nation’s producers will significantly expand their wafer capacity. Mainland China is likely to reduce its semiconductor imports from Taiwan considerably in the coming years, especially wafer imports. According to IC Insights, nine 300mm wafer fabs2 are scheduled to open worldwide in 2019, with five of them in mainland China. Based on another set of data from SEMI, the number of 200mm wafer fabs in the world will increase from 194 in 2017 to 203 by 2022, with an additional 56 established fabs planning to expand their manufacturing capacity. Mainland China is expected to account for 44% of the growth. In comparison, Taiwan only accounts for about 10% of the growth. Mainland China currently accounts for over 30% of Taiwanese electronic parts exports (wafers, PCBs, mainboards and others). As mainland China continues to build new wafer manufacturing capacity and gradually improve its existing technology, it will switch its consumption from imports to domestic production. Consequently, mainland China is likely to reduce its semiconductor imports from Taiwan considerably in the coming years, especially wafer imports (Chart I-13). This is structurally bearish for Taiwanese semiconductor companies. Chart I-13Mainland China’s Semiconductor Imports From Taiwan Will Drop

Mainland China’s Semiconductor Imports From Taiwan Will Drop

Mainland China’s Semiconductor Imports From Taiwan Will Drop

Bottom Line: Taiwan is facing increasing challenges from Korea in terms of defending its market share in the high-end wafer market. Meanwhile, Taiwan is also set to lose market share in the medium-to-low market to wafer producers from mainland China. What About The Rest Of The Economy? The rest of the economy is exhibiting mixed signals, with contracting major non-semiconductor export sectors but decent household consumption and property market. Table 1 shows Taiwan’s top 10 exported products, with the top three attributing to over half of total exports. Besides the semiconductor sector, exports of the other two major products – electrical machinery products and machinery – are beginning to contract (Chart I-14).

Chart I-

Chart I-14Taiwan: Contracting Non-Semiconductor Exports

Taiwan: Contracting Non-Semiconductor Exports

Taiwan: Contracting Non-Semiconductor Exports

However, the domestic economy seems to be running well at present. Production of construction materials in volume terms is growing rapidly, accompanied by a rebound in building permits granted (Chart I-15). While employment growth is decent, average wage growth has been quite strong (Chart I-16). With persistent contraction in exports and inflation very low, the central bank could cut rates in 2019. Chart I-15Decent Domestic Demand

Decent Domestic Demand

Decent Domestic Demand

Chart I-16Strong Wage Growth

Strong Wage Growth

Strong Wage Growth

Ongoing contraction in semiconductor exports will likely slow domestic demand with a time lag. In fact, the inverted 5-year/6-month yield curve is indeed signaling an economic slump in Taiwan (Chart I-17). Chart I-17Inverted Yield Curve Signals Continuing Economic Slump Ahead

Inverted Yield Curve Signals Continuing Economic Slump Ahead

Inverted Yield Curve Signals Continuing Economic Slump Ahead

Investment Recommendations The latest rebound in Taiwanese stocks is unsustainable and share prices will relapse again. Within an EM equity portfolio, we recommend maintaining a market-weight allocation to Taiwan for now. We are reluctant to downgrade Taiwan to underweight because some other emerging markets and sectors within the EM universe have a poorer outlook. In addition, Taiwanese shares have already underperformed the EM benchmark since last September (Chart I-18). Chart I-18Taiwanese Stocks: Staying Neutral Within EM

Taiwanese Stocks: Staying Neutral Within EM

Taiwanese Stocks: Staying Neutral Within EM

The Taiwanese currency is cheap (Chart I-19). The region has a massive current account surplus and foreigners do not hold any local bonds, which is very different from many other EM countries. Hence, Taiwan is less vulnerable to capital outflows than many current-account-deficit EM economies. The latter could be forced to raise rates, which will place pressure on their banks as well as on domestic demand. In contrast, Taiwan has the ability to cut rates. Chart I-19TWD Is Cheap

TWD Is Cheap

TWD Is Cheap

Ellen JingYuan He, Associate Vice President Emerging Markets Strategy ellenj@bcaresearch.com 1 "Risk Production" means that a particular silicon wafer fabrication process has established a baseline in terms of process recipes, device models, and design kits, and has passed standard wafer level reliability tests. 2 A fab, sometimes called foundry, is a semiconductor fabrication plant where devices such as integrated circuits are manufactured. Equity Recommendations Fixed-Income, Credit And Currency Recommendations

Highlights Driven by its fear that deflation is a more intractable danger than inflation, the Federal Reserve has enshrined its pause for the remainder of 2019 in order to lift inflation expectations. Since the U.S. business cycle expansion is not over, the Federal Reserve’s plan to put policy on hold this year raises the odds that the economy will overheat. Global growth is set to bottom during the second quarter in response to easier financial conditions. Accommodative policy, rebounding global economic activity and a softening dollar will boost risk asset prices during the remainder of the year. Safe-haven bonds, including Treasurys, will underperform cash over the coming 12 to 18 months. The rally in risk assets will ultimately prove the last hurrah as the Fed will resume tightening later this year or in 2020, and a bear market lies down the road. Only investors with tactical investment horizons should aggressively play this rally. Those with longer investment horizons should use this rally to lighten up their exposure to risk. Feature Introduction Following the introduction of the word “patience” into the Federal Reserve’s lexicon, a move lower in the so-called Fed dots was to be anticipated. The FOMC now expects no rate increases in 2019 and only one hike in 2020. The interest rate market remains skeptical that the Fed will be able to deliver on its forecast. For now, the OIS curve is pricing in a 75% probability of a cut this year, and rates at 1.9% by the end of 2020. With the 10-year/3-month yield curve inverting last week and the U.S. Leading Economic Indicator still decelerating, it is no wonder that investors are betting on the Fed becoming ever more dovish (Chart I-1). BCA is inclined to take the Fed at its word – the next move will be a hike, not a cut. This call rests on our view of the business cycle: The fed funds rate is still somewhat below neutral, U.S. economic activity can expand further, and global growth is likely to trough soon. The current dovish inclination of global central banks will only nurture the cycle a little bit longer. Consequently, we continue to recommend a positive stance on stocks for the coming quarters, while keeping in mind that the cycle is long in the tooth, and that beyond this last climb lies a significant bear market. The U.S. Business Cycle Has Further To Run… The Fed remains data dependent, but this now means that depressed inflation expectations in the private sector need to be vanquished before the hiking can resume (Chart I-2). With the view that low realized inflation has curtailed expectations now common across major central banks, this implies that a temporary overshoot in actual core PCE will be tolerated in order to lift expectations. Chart I-1Worrisome Signs For Growth

Worrisome Signs For Growth

Worrisome Signs For Growth

Chart I-2The Fed Wants To Lift Inflation Expectations

The Fed Wants To Lift Inflation Expectations

The Fed Wants To Lift Inflation Expectations

Since consumer prices are a lagging variable, lifting both realized and anticipated inflation will only be possible if we move ever further along the business cycle, further pressuring the economy. Our base case remains that the risk of a recession is low in 2019, and is even receding in 2020. First, U.S. credit-dependent cyclical spending currently constitutes only 25.3% of potential GDP. As Chart I-3 illustrates, this is in line with its historical average, and well below the levels recorded near the end of previous business cycles. This suggests that the amount of vulnerability caused by misallocated capital is not yet in line with previous cycles. It also indicates that the share of output generated by the sectors most sensitive to higher rates is also low. Chart I-3U.S. Cyclical Spending: Limited Signs Of Vulnerability

U.S. Cyclical Spending: Limited Signs Of Vulnerability

U.S. Cyclical Spending: Limited Signs Of Vulnerability

Second, the consumer remains in good shape. Households have deleveraged, and debt-service payments relative to disposable income are still near multi-generational lows (Chart I-4). Moreover, thanks to a saving rate of 7.6%, consumer spending is likely to move in line or even outperform income growth. On this front, the outlook is also good. As Chart I-5 demonstrates, the link between wages and salaries relative to the employment-to-population ratio for prime-age workers – a measure of labor utilization unaffected by the demographic changes that have muddied the interpretation of the unemployment rate – is still as tight as it was 20 years ago. Thus, as long as the labor market does not suddenly collapse, wage growth will continue to accelerate, supporting household income and consumption. Chart I-4Household Balance Sheets Are Solid

Household Balance Sheets Are Solid

Household Balance Sheets Are Solid

Chart I-5

Third, at 0.4% of GDP, the fiscal thrust remains positive. In other words, fiscal policy will still add to GDP in 2019. Fourth, we do not see the traditional symptoms associated with a fed funds rate above neutral. After dipping sharply in the second half of 2018, mortgage for purchase applications are back near their cycle highs (Chart I-6). Moreover, the performance of homebuilders’ equities relative to the broad market has begun to rebound, which is inconsistent with a fed funds rate above neutral. Chart I-6Mortgage Applications Do Not Suggest Policy Is Tight

Mortgage Applications Do Not Suggest Policy Is Tight

Mortgage Applications Do Not Suggest Policy Is Tight

Fifth, there is scope for the contribution from housing sector activity to morph from a negative to a positive. A fed funds rate below neutral historically is correlated with an improving housing market. Rising mortgage rates from 3.8% to 4.6% depressed home sales and construction output, and the fall in mortgage rates over the past x month 4.3% should stimulate housing activity (Chart I-7). Chart I-7Residential Activity Will Rebound This Year

Residential Activity Will Rebound This Year

Residential Activity Will Rebound This Year

Bottom Line: U.S. first-quarter GDP growth will be dismal, but one quarter does not make a trend. The low degree of economic vulnerability in the U.S., and the likelihood that the fed funds rate will stay below neutral for a while suggest that growth should rebound to the 2-2.5% range and should remain above-trend for the remainder of 2019. … And Global Growth Will Soon Trough As the cliché goes, it is darkest before the dawn. This is a fitting description of the world economy outside the U.S. right now. Global trade is depressed, global PMIs are moribund and nothing feels good. But it is exactly when nothing is going well that one needs to wonder what may cause the outlook to turn for the better. Thankfully, green shoots are emerging. To begin with, central banks around the world have taken a more dovish slant. This dovish forward guidance is nurturing global activity via a significant easing in global financial conditions, which is undoing the severe brake-pumping imposed on global growth in the fourth quarter of 2018 (Chart I-8). Chart I-8Global Financial Conditions Are Easing

Global Financial Conditions Are Easing

Global Financial Conditions Are Easing

This more dovish forward guidance has helped our Financial Liquidity Index, which sharply deteriorated through 2009, rebound. Historically, this presages an improvement in the BCA Global Leading Economic Indicator (Chart I-9). Improving liquidity conditions have already been reflected in lower real rates around the globe, creating a reflationary impulse. EM financial conditions are responding positively, pointing to an upcoming pick-up in industrial activity, as measured by our Global Nowcast (Chart I-10). Chart I-9Improving Global Liquidity Backdrop

Improving Global Liquidity Backdrop

Improving Global Liquidity Backdrop

Chart I-10A Tailwind From EM?

A Tailwind From EM?

A Tailwind From EM?

Our Global LEI diffusion Index has begun to reflect some of these developments. After forming a trough in 2018, more than 50% of the countries in our Global LEI are currently experiencing a sequential improvement in their LEIs. We are now entering the normal lag after which a broadening growth impulse converts into aggregate activity moving higher (Chart I-11). Most interestingly, investors do not seem to be anticipating such a rebound. There is therefore room for growth surprises around the world. Chart I-11Scope For Growth Surprises

Scope For Growth Surprises

Scope For Growth Surprises

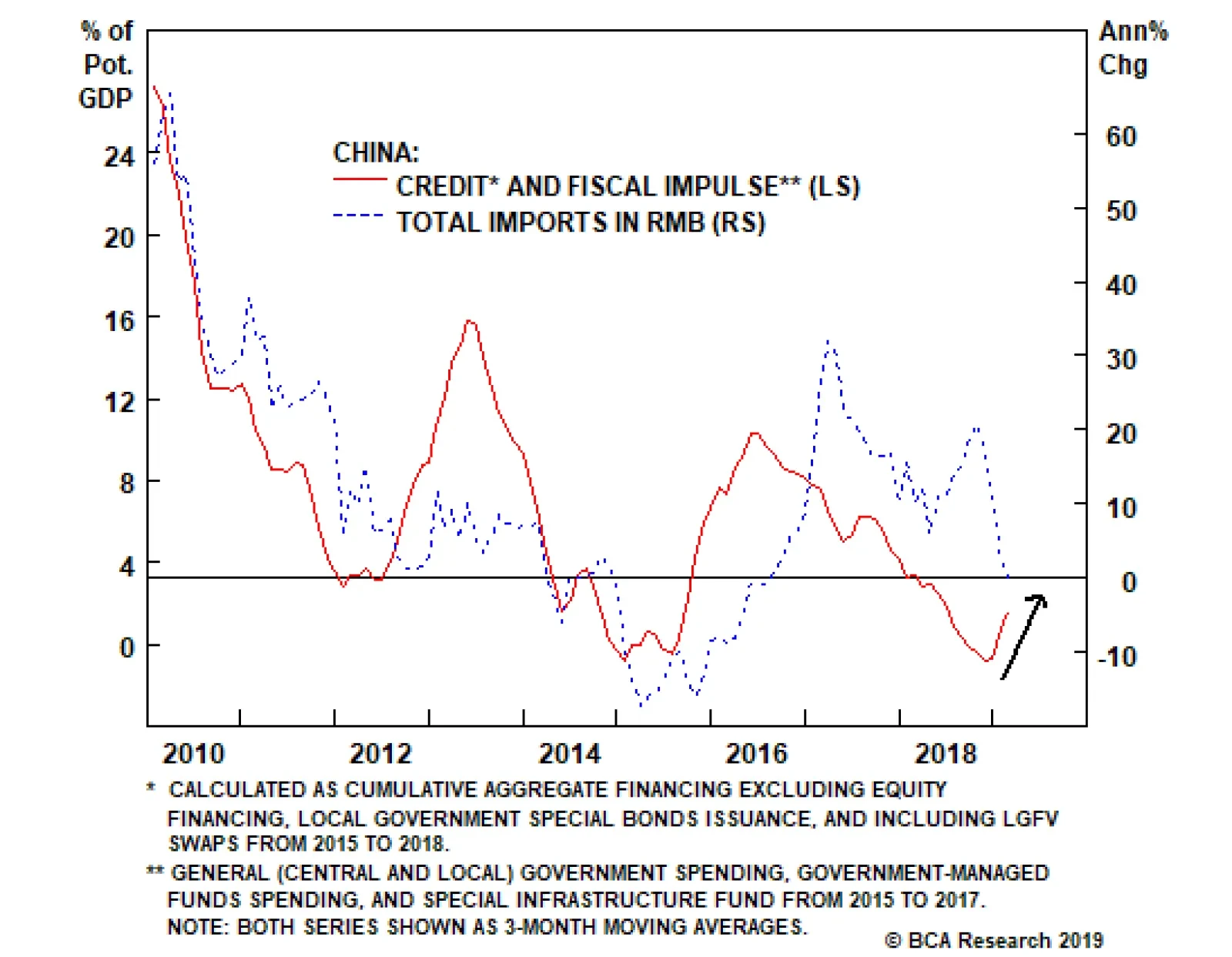

China has a role to play in this story, will likely morph from a headwind to global growth to a positive. Positive may be a strong word, but at the very least, we expect China to stop detracting from global growth. Premier Li-Keqiang recently put the accent on stability and preserving employment, suggesting Chinese policymakers are likely to de-emphasize deleveraging over the coming 12-18 months. For Chinese growth to improve, deleveraging does not even have to stop. As both theory and history have shown, a slower pace of deleveraging means that the credit impulse moves back into positive territory and growth re-accelerates, even if only temporarily (Chart I-12). Chart I-12Growth Can Improve Even If Deleveraging Continues

Growth Can Improve Even If Deleveraging Continues

Growth Can Improve Even If Deleveraging Continues

As a thought experiment, if Chinese leverage were to stabilize this year and nominal growth were to hit 8% – the lower bound of the real GDP target of 6-6.5% and inflation of 2% – the Chinese credit impulse would surge to more than 10% of GDP (Chart I-13)! We are not forecasting such a large rebound in the impulse, but this exercise clearly shows that if the Chinese authorities – who are cutting taxes and trying to ease credit conditions for small- and medium-sized enterprises – want to favor stability and employment for just one year, the impact on growth will be non-negligible, even if deleveraging continues. Since domestic demand responds to the credit impulse, and imports sport an elevated beta to domestic demand, Chinese imports are likely to soon morph from a negative to something more neutral – maybe even a small positive for the rest of the world. Chart I-13A Thought Experiment

A Thought Experiment

A Thought Experiment

Finally, as weak as Europe is right now, it will likely be an important source of positive surprises in the second half of the year. To begin with, Europe is much more sensitive to EM growth conditions than the U.S. (Chart I-14). In the same way as Europe felt the full force of the deceleration in global trade last year, it will benefit from any improvement in trade this year.

Chart I-14

A myriad of idiosyncratic shocks rammed through the euro area last year, worsening an already difficult situation. The new WLTP emission standards caused German auto production to collapse by nearly 20%. Nonetheless, as contracting domestic manufacturing orders and a large inventory pullback in the final quarter of last year suggest, the inventory overhang has been worked off (Chart I-15, top panel). Chart I-15Passing European Idiosyncratic Shocks

Passing European Idiosyncratic Shocks

Passing European Idiosyncratic Shocks