Emerging Markets

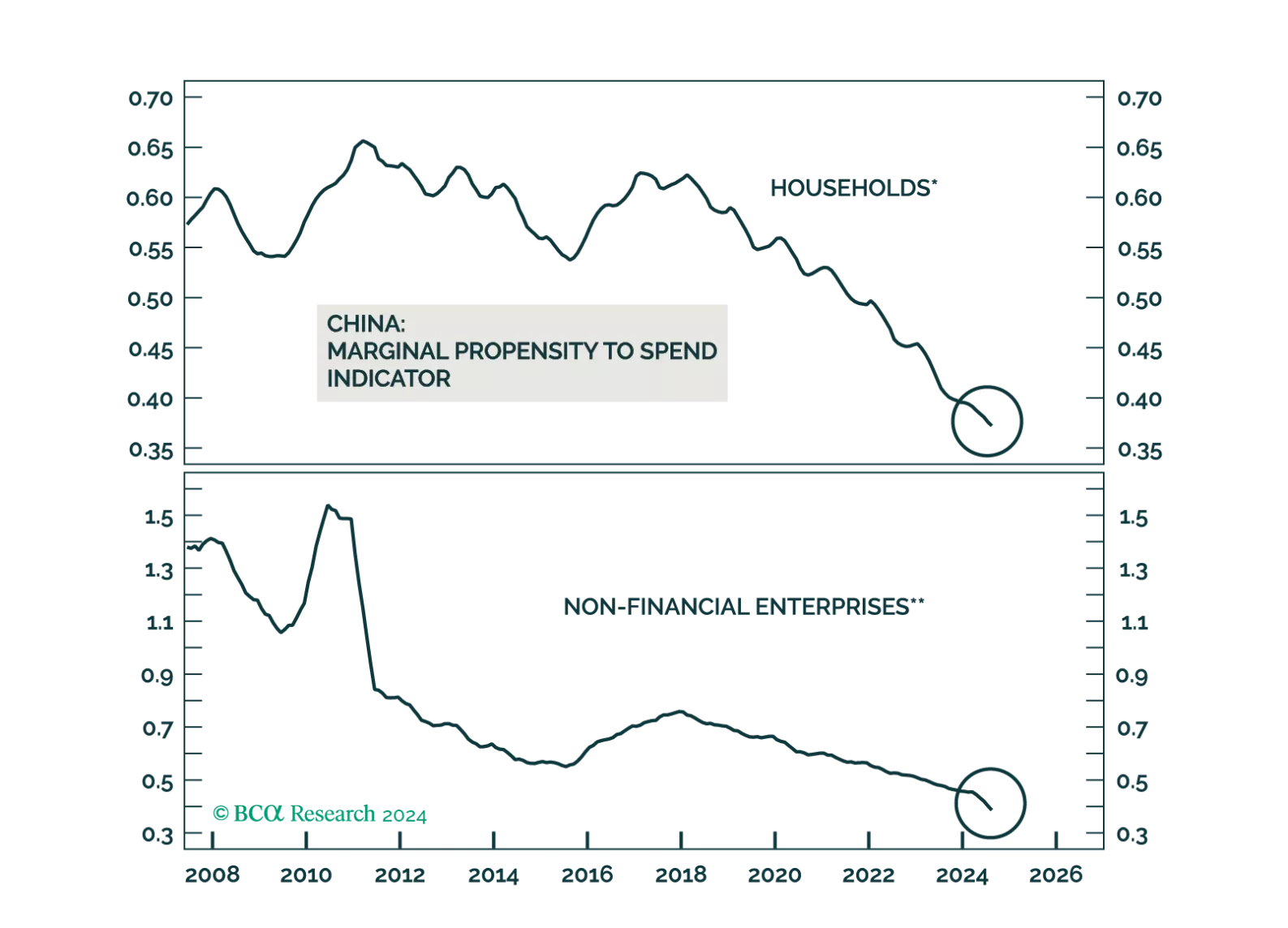

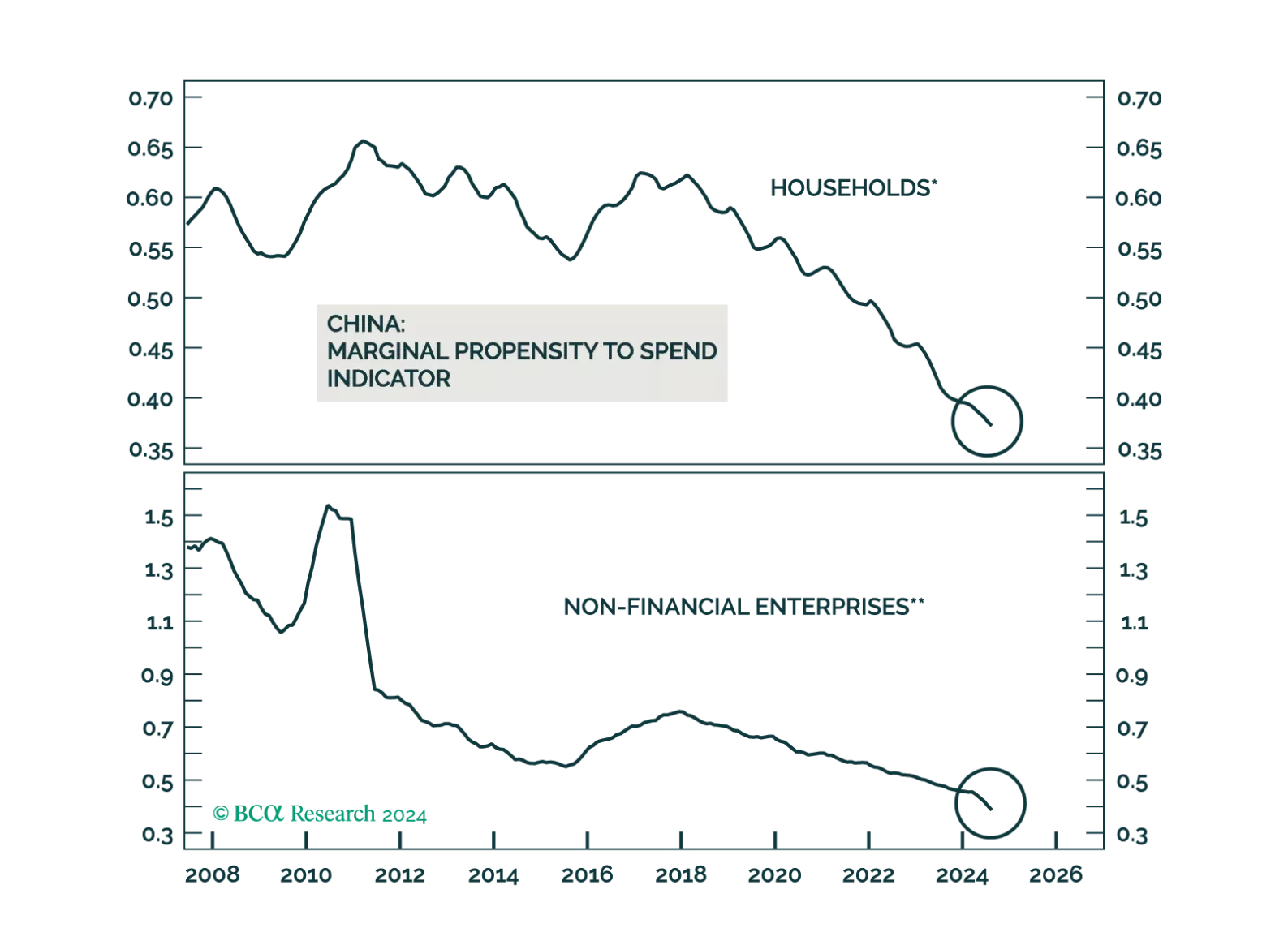

This week has not been short of developments on Chinese policy. After unleashing a monetary policy blitz, the authorities held an unscheduled Politburo meeting resulting in a pledge to take actions towards stabilizing the housing market and to support fiscal…

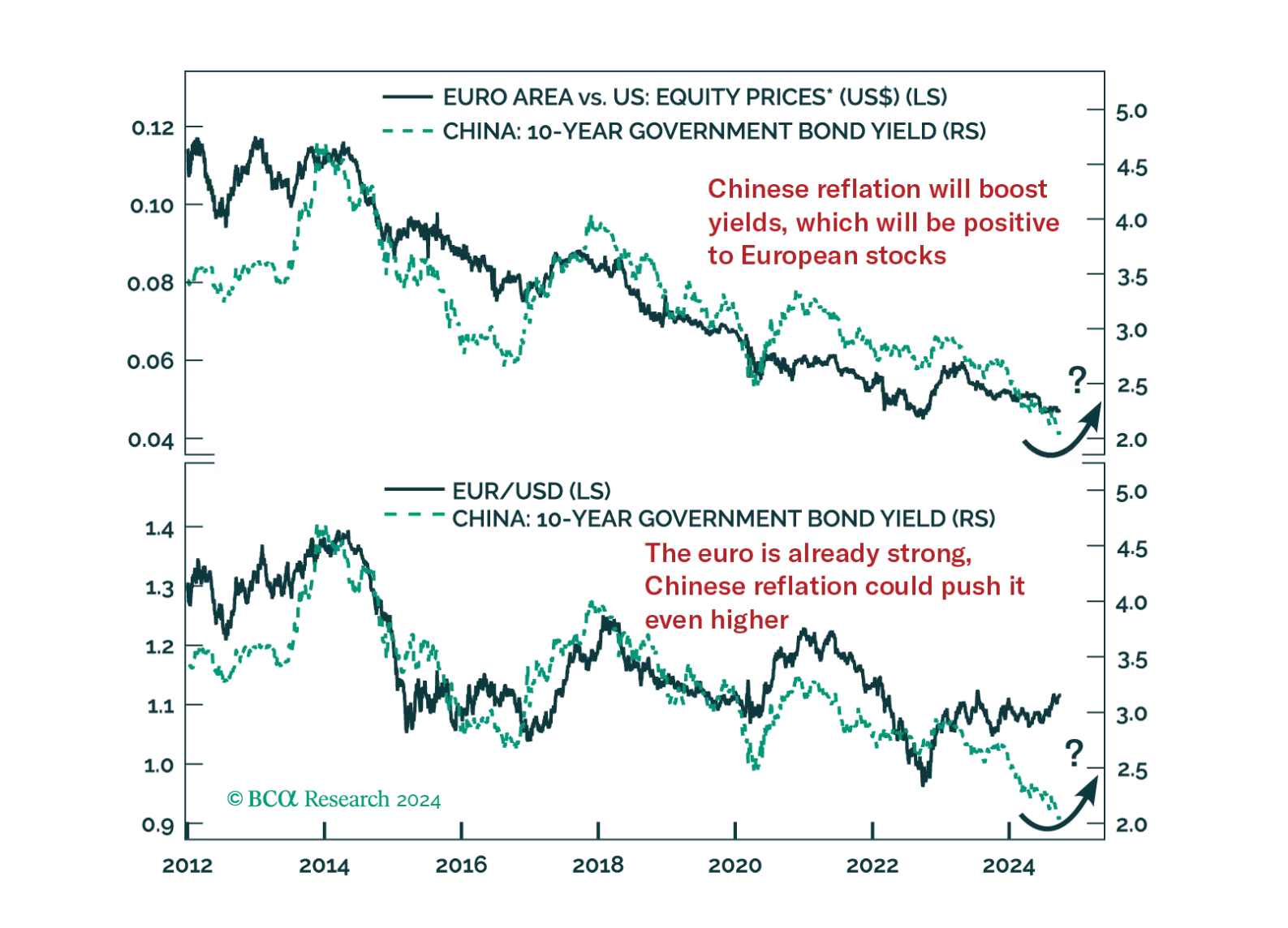

China’s Politburo announcement is likely to lead to a repricing of China’s growth in the near-term. Read how investors can hedge against this potent threat to our defensive investment stance.

BCA Research’s Geopolitical Strategy service introduced a Global Political Capital Index. Investors should favor countries with newly elected government, small government size, and ample room to cut policy rate. Ideally, they should also be in a stable…

We believe the PBoC’s recent policy stimulus might bolster investor confidence, potentially stabilize onshore Chinese equity prices, and provide modest support to offshore stocks. However, they are unlikely to significantly boost economic growth in the mainland.

We believe the PBoC’s recent policy stimulus might bolster investor confidence, potentially stabilize onshore Chinese equity prices, and provide modest support to offshore stocks. However, they are unlikely to significantly boost economic growth in the mainland.

Export dynamics from small open economies are a good bellwether for global growth conditions. Taiwan export orders accelerated from 4.8% y/y to a faster-than-anticipated 9.1% in August. The faster pace of growth was also broad-based among the country’s…

The PBoC announced further measures to stimulate the economy on Tuesday. It lowered the reserve requirement ratio from 10% to 9.5%, cut the 7-day reverse repo rate by 20 bps (following Monday’s 10 bps cut to the 14-day reverse repo rate), lowered borrowing…

According to BCA Research’s Emerging Markets Strategy service, Brazil’s decision to raise interest rates is supported by recent economic data. Back in January of this year, they noted that Brazil would overshoot its 2024 growth and inflation…

The PBoC lowered the 14-day reverse repo rate by 10 bps on Monday, a move that follows a string of easing measures in late July when the central bank lowered the 7-day reverse repo rate, several maturities of the loan prime rate and the 1-year medium-term…