Emerging Markets

Highlights Investors who are betting on a quick resolution to the U.S./China trade war following the "new NAFTA" deal and the U.S. midterm elections have likely been taken in by false hope. Stay neutral China relative to global stocks, and overweight low-beta sectors within the investable equity universe. The relative performance of Chinese industry groups since mid-June has been almost entirely determined by their beta characteristic, with almost all low-beta industry groups outperforming. Energy stocks have been among the top outperformers within the Chinese equity universe, and several factors support our recommendation that investors initiate an outright long position. While it is likely paused rather than stalled, broad "reform" as an investment theme will be less relevant over the coming 6-12 months. Consequently, we are closing our long ESG leaders / short benchmark trade. Feature September's PMI releases, both official and private, confirm that China's export outlook is deteriorating rapidly. Chart 1 highlights that the Caixin PMI is about to fall below the boom/bust line, and the new export orders component of the official PMI has sunk to a 2 ½ year low. Somewhat oddly, investors do not seem to be responding negatively to the de-facto announcement of a 25% rate on the second round of U.S. import tariffs against China. Chart 2 shows that domestic infrastructure stocks have actually been rising relative to global stocks since mid-September, and our BCA China Play Index appears to have entered a (so far very modest) uptrend. Chart 1The Export Shock Is Coming...

The Export Shock Is Coming...

The Export Shock Is Coming...

Chart 2...But Investors Have Been Incrementally Upbeat

...But Investors Have Been Incrementally Upbeat

...But Investors Have Been Incrementally Upbeat

One possible explanation for this is that investors are doubling down on the idea that China will have to aggressively stimulate in response to the shock. We have leaned against this narrative, by arguing in past reports that China's policy response to the upcoming export shock is not likely to be heavily credit-based, and that increases in fiscal spending today will involve more "soft infrastructure" than in the past.1 Chart 3 certainly shows no evidence of a spike in broad money or total credit; adjusted total social financing growth barely accelerated in August, against the backdrop of promises to front-run planned fiscal spending over the coming year. Chart 3No Major Acceleration In Credit Growth Evident Yet

No Major Acceleration In Credit Growth Evident Yet

No Major Acceleration In Credit Growth Evident Yet

Chart 4Americans Support A Tough Stance Against China

False Hope

False Hope

But a second explanation of recent investor behavior, one that we have been hearing more loudly from some market participants, is that China is waiting until after the midterm elections in the U.S. to make a deal, in anticipation that Republican losses in Congress will weaken Trump and change the political reality in terms of trade policy towards China. There are three reasons why investors holding this view are likely mistaken, and have been taken in by false hope: In the U.S., the actual implementation of tariffs lies within the control of the Presidency. Congress has delegated substantial authority to the president that would take time to be clawed back. Moreover, the president controls the execution of tariffs, and has a general prerogative over national security issues, which certainly includes the trade war with China. Democratic control of the House or Senate may cause President Trump to act even more forcefully against China, as trade will be among the few relatively unfettered policy options left to him. Chart 4 highlights that a sizeable majority of the American public views Chinese trade policy towards the U.S. as unfair, unlike the U.S.' other major trade partners. Reflecting this point, Democrats themselves maintain a hawkish stance on trade with China. This suggests that Trump will have a strong mandate to continue to demand major concessions from China even after the elections. We agree that Chinese stocks have already priced in a sizeable earnings decline, but we would still characterize buying now as an ill-advised case of trying to catch a falling knife. We highlighted in our September 19 Weekly Report that during the 2014-2016 episode Chinese stocks bottomed several months after stimulus began to take effect,2 because of a delayed decline in forward earnings. A similar situation would appear to be developing this time around: the third round of tariffs against China will likely soon be announced, the shock to Chinese export growth will soon manifest itself in the data, and yet Chinese forward earnings have only fallen 5-6% from their June peak. Bottom Line:Investors who are betting on a resolution to the U.S./China trade war following the U.S. midterm elections have likely been taken in by false hope. Stay neutral China relative to global stocks, and overweight low-beta sectors within the investable equity universe. Recent Sector Performance: A Beta Story, And A New Trade Idea Chart 5Last Week We Closed One Of Our Most Successful Calls

Last Week We Closed One Of Our Most Successful Calls

Last Week We Closed One Of Our Most Successful Calls

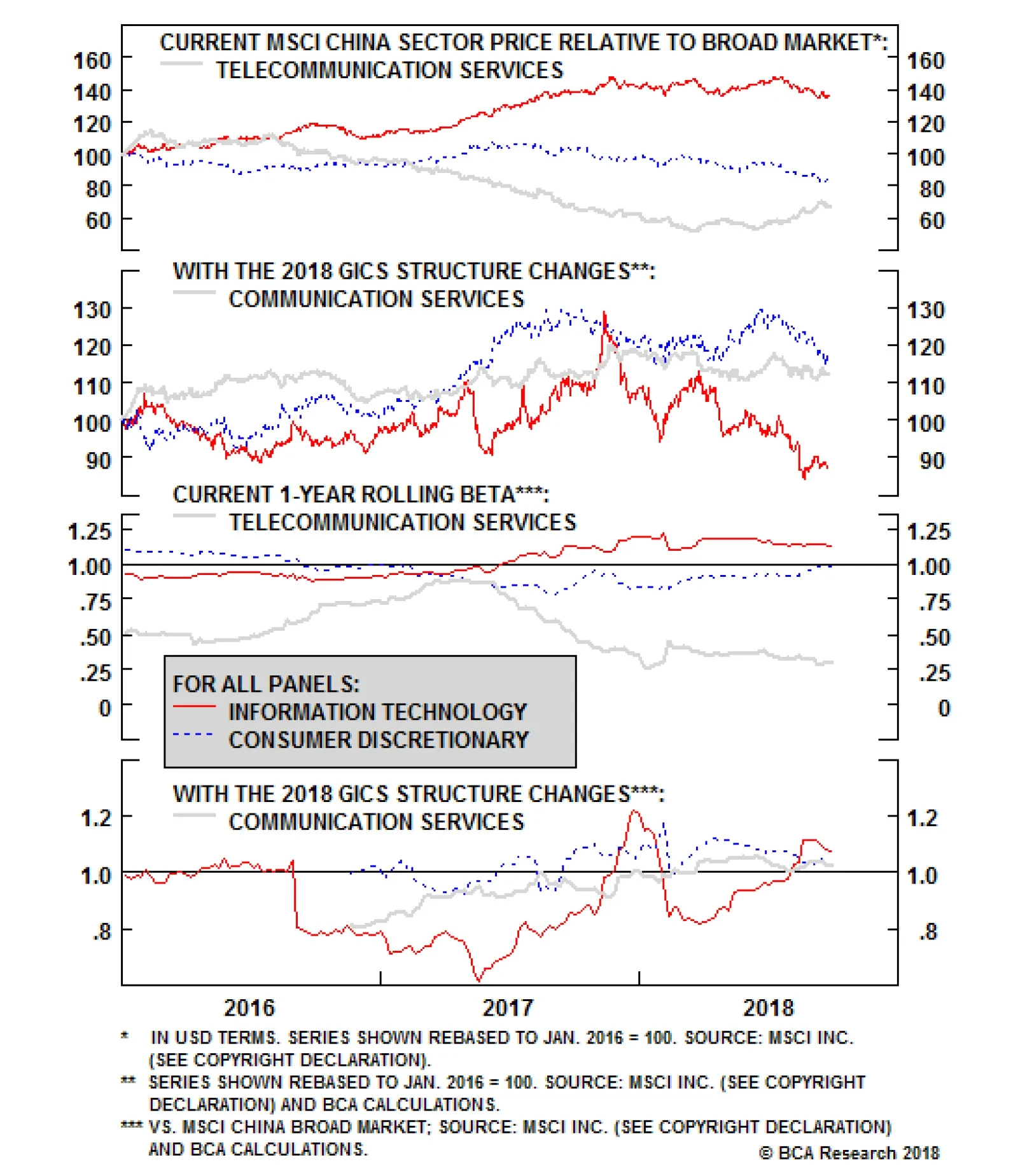

We recommended closing one of our most successful trades of the past year in a brief Special Report last week.3 The report outlined major changes to the global industry classification standard (GICS) that took effect this week, as well as the implications for China's stock market. One key change is that Alibaba, one of the "BATs", is now part of the consumer discretionary sector and makes up roughly 60% of its market capitalization. Given this fundamental shift in the risk/reward profile of the position, we recommended closing our long MSCI China Consumer Staples / short MSCI China Consumer Discretionary trade for a profit of 47% (Chart 5). With the goal of identifying new trade ideas that are likely to outperform within the context of a trade war, Chart 6 presents the alpha and beta characteristics of 23 industry groups in the MSCI China index (the investable benchmark) from mid-June to the end of September. The x-axis of the chart represents the group's beta versus the benchmark, whereas the y-axis shows standardized alpha over the period. The chart also distinguishes between out/underperforming sectors. Chart 6Since Mid-June, Sector Performance Has Largely Been Beta-Driven

False Hope

False Hope

Several points are notable: Largely speaking, the relative performance of Chinese industry groups since mid-June has been determined by their beta characteristic (with almost all low-beta industry groups outperforming). This supports our existing position of favoring low-beta sectors within the MSCI China index, a trade that we initiated on June 27.4 Four industry groups that belong to traditionally cyclical sectors have outperformed since mid-June and have had a beta less than 1: energy, capital goods, banks, and consumer durables and apparel. Energy and capital goods have been particularly notable, having outperformed by 24% and 15%, respectively. Technology-related industry groups have underperformed, including the pharma, biotech, and life sciences industry group within health care. Consumer services and retailers have significantly underperformed, due to the heavy influence of travel-related businesses in both indexes. Among the top performing industry groups over the past three months, Chinese energy stocks look like the most compelling trade in absolute terms. While we are normally reluctant to chase performance, several factors support an outright long position: BCA's Commodity & Energy Strategy service is bullish on oil prices, and recently increased their 2019 Brent price forecast to $95/bbl based on both supply and demand factors.5 Despite the recent outperformance of Chinese energy companies within the investable universe, they remain cheap versus global energy companies based on cash flow-based valuation metrics (Chart 7). This is true even after accounting for the fact that they are typically discounted relative to their global peers due to heavy state ownership. Chinese energy companies look reasonably priced relative to the value of global oil production (Chart 8). Chinese energy companies largely receive their revenue in U.S. dollars, which is an attractive hedge in an environment where CNY-USD may decline further. Chart 7Chinese Energy Stocks Are Cheap Versus Their Global Peers...

Chinese Energy Stocks Are Cheap Versus Their Global Peers...

Chinese Energy Stocks Are Cheap Versus Their Global Peers...

Chart 8...And Versus The Value Of Global Oil Production

...And Versus The Value Of Global Oil Production

...And Versus The Value Of Global Oil Production

Given this, we are updating our trade book and recommend that investors initiate an outright long position in Chinese energy stocks as of today. Chart 9Despite Outperforming, Absolute Capital Goods Performance Has Been Lackluster

Despite Outperforming, Absolute Capital Goods Performance Has Been Lackluster

Despite Outperforming, Absolute Capital Goods Performance Has Been Lackluster

What about Chinese capital goods companies? For now, we are content with relative rather than absolute exposure, which (surprisingly) exists in our low-beta sectors trade. Capital goods companies account for almost 70% of the Chinese industrial sector, and industrial stocks have been less volatile than the broad market over the past year, in large part because they underperformed so significantly in 2017. Given this, they have been included in our low-beta sectors portfolio, despite being typically pro-cyclical. In absolute terms, though, it is far from clear that Chinese capital goods stocks will trend higher (Chart 9). Some investors are hopeful that capital goods producers will benefit from a significant acceleration in infrastructure spending but, as we noted above, the bar is high for the type of stimulus that investors have come to expect. In addition, potential weakness in property construction could be a drag, and could offset gains from a pickup in infrastructure investment.6 We recommend that investors stick with a relative position, until compelling signs of a stimulus overshoot emerge. Bottom Line: The relative performance of Chinese industry groups since mid-June has been almost entirely determined by their beta characteristic, with almost all low-beta industry groups outperforming. Energy stocks have been among the top outperformers within the Chinese equity universe, and several factors support our recommendation that investors initiate an outright long position. A Pause In Broad "Reform" As An Investment Theme Following last November's Communist Party Congress, we noted that China was likely to step up its reform efforts in 2018, and would take meaningful steps to: Pare back heavy-polluting industry Hasten the transition of China's economy to "consumer-led" growth Slow or halt leveraging in the corporate/financial sector Eliminate corruption and graft We argued that Chinese policymakers would have to set the pace of reforms to avoid a significant slowdown in the economy, but we noted that a policy mistake (moving too aggressively) could not be ruled out. We introduced the BCA China Reform Monitor as a way of tracking the intensity of the reforms, which was calculated as an equally-weighted average of the four "winner" sectors that emerged in the month following the Party Congress (energy, consumer staples, health care, and technology) relative to an equally-weighted average of the remaining seven sectors (Chart 10). In particular, we argued that a rise in the monitor that was driven by the underperformance of the denominator would be a warning sign that reforms had become too aggressive for the economy to withstand. Chart 10Reform, As A Broad Theme, Will Be Less Relevant In The Year Ahead

Reform, As A Broad Theme, Will Be Less Relevant In The Year Ahead

Reform, As A Broad Theme, Will Be Less Relevant In The Year Ahead

Chart 10 highlights that the reform monitor rose for the first half of the year, driven by the gains of the numerator rather than losses in the denominator. The message of a sustainable pace of reforms, even against the backdrop of brewing trade tension, was consistent with the relative performance of Chinese stocks and was part of the reason we recommended staying overweight versus the global benchmark in Q1 and the majority of Q2.7 Since mid-June, however, the reform theme has been thrown into reverse: our reform monitor has declined, alongside absolute declines in both "winner" and "loser" sectors. The timing of this inflection point is clearly aligned with President Trump's announcement of the second round of tariffs. Given this, and our view that the U.S./China trade war is likely to get worse over the coming 6-12 months, it is likely that broad "reform" as an investment theme will be less relevant for the foreseeable future, at least relative to policymaker efforts to stabilize the economy. However, for several reasons, we view this as a pause in the theme, rather than an end: On the environmental front, Chart 11 highlights that China continues to pursue a clean air policy, at least in large population centers. Anti-pollution efforts are a signature policy of President Xi Jinping. They affect quality of life and ultimately the legitimacy of the regime, so they cannot be postponed entirely or indefinitely. Chart 11China Continues To Clamp Down On Air Quality

China Continues To Clamp Down On Air Quality

China Continues To Clamp Down On Air Quality

Shifting China's growth model away from primary and secondary industry remains a long-term goal of policymakers. Chart 12 highlights that tertiary industry has already risen non-trivially as a share of GDP. This trend is also clearly visible in the electricity consumption data, which shows that residential and tertiary industry consumption has risen quite materially over the past several years. Chinese policymakers will clearly ease up on the brake over the coming year in terms of deleveraging, but it is far from clear that they will aim for another wave of aggressive private sector debt growth. We highlighted one key reason for this in a recent Special Report: comparing adjusted state-owned enterprise (SOE) return on assets to borrowing costs suggests that the marginal operating gain from debt has become negative for these firms (Chart 13). This implies that further aggressive leveraging of SOEs could push them into a debt trap. In fact, if policymakers do refrain from promoting a major private sector credit expansion over the coming year, that restraint will directly reflect the reform agenda. Chart 12Policymakers Continue To Emphasize A Transition Towards Services

Policymakers Continue To Emphasize A Transition Towards Services

Policymakers Continue To Emphasize A Transition Towards Services

Chart 13SOEs Now Appear To Have A Negative Financial Gain From Debt

SOEs Now Appear To Have A Negative Financial Gain From Debt

SOEs Now Appear To Have A Negative Financial Gain From Debt

Chart 14 highlights that while anti-corruption cases involving gifts and the improper use of public funds are off of their high from early this year, they remain elevated and are not trending lower. As a final point, Chart 15 shows that our long MSCI China environmental, social, and governance (ESG) leaders / short MSCI China trade has been negatively impacted by the pause in reform as an investment theme. While MSCI's ESG indexes aim to generate low tracking error relative to the underlying equity market of each country, technology companies are typically overrepresented in ESG indexes because of the low emissions nature of their business model. In China's case, we noted above that technology industry groups have fared poorly since mid-June, and panel 2 of Chart 15 shows that the underperformance of Chinese investable technology companies since mid-June lines up with the latest leg of ESG underperformance. Chart 14China's Anti-Corruption Drive Is Still In Effect

China's Anti-Corruption Drive Is Still In Effect

China's Anti-Corruption Drive Is Still In Effect

Chart 15Favor ESG Leaders Again When The Reform Theme Reasserts Itself

Favor ESG Leaders Again When The Reform Theme Reasserts Itself

Favor ESG Leaders Again When The Reform Theme Reasserts Itself

It remains unclear how much of tech's underperformance has been due to rich multiples versus concerns that the U.S. crackdown on Chinese technology transfer and intellectual property theft will negatively impact the market share of China's tech companies (via an opening of the market and a rise in the market share of foreign competitors). But we believe that the latter is a factor, and we recommend closing our long ESG leaders / short benchmark trade until "reform", both environmental and otherwise, reasserts itself as a driving factor for the Chinese equity market. Bottom Line: While it is likely paused rather than stalled, broad "reform" as an investment theme will be less relevant over the coming 6-12 months relative to policymaker efforts to stabilize the economy. We are closing our long ESG leaders / short benchmark trade at a loss of 5.5%. Jonathan LaBerge, CFA, Vice President Special Reports jonathanl@bcaresearch.com 1 Pease see China Investment Strategy Special Report "China: How Stimulating Is The Stimulus?" dated August 8, 2018, available at cis.bcaresearch.com. 2 Pease see China Investment Strategy Weekly Report "Investing In The Middle Of A Trade War", dated September 19, 2018, available at cis.bcaresearch.com. 3 Pease see China Investment Strategy Special Report "GICS Sector Changes: The Implications For China", dated September 26, 2018, available at cis.bcaresearch.com. 4 Pease see China Investment Strategy Weekly Report "Now What?", dated June 27, 2018, available at cis.bcaresearch.com. 5 Pease see Commodity & Energy Strategy Weekly Report "Odds Of Oil-Price Spike In 1H19 Rise; 2019 Brent Forecast Lifted $15 To $95/bbl", dated September 20, 2018, available at ces.bcaresearch.com. 6 Pease see China Investment Strategy Special Report "China's Property Market: Where Will It Go From Here?", dated September 13, 2018, available at cis.bcaresearch.com. 7 The rapidly escalating trade war between China and the U.S. caused us to recommended putting Chinese stocks on downgrade watch at the end of March, and we recommended that investors cut their exposure to neutral on June 20. Pease see China Investment Strategy Weekly Report "Chinese Stocks: Trade Frictions Make For A Tenuous Overweight", dated March 28, 2018, and China Investment Strategy Special Report "Downgrade Chinese Stocks To Neutral", dated June 20, 2018, both available at cis.bcaresearch.com. Cyclical Investment Stance Equity Sector Recommendations

Highlights So What? Go long Brent / short S&P 500. The risk of a recession in 2019 is underappreciated. Why? The likelihood is increasing of a geopolitically-induced supply-side shock that pushes crude prices above $100 per barrel in the coming 6-12 months. Oil supply disruptions in Iran, Iraq, and Venezuela represent the primary source of risk. Historically, the combination of Fed rates hike and an oil price spike has preceded 8 out of the last 9 recessions. Also... A recession in 2019, ahead of the 2020 election, would set the stage for a confrontation between Trump and the Fed, adding fuel to market volatility. Feature Geopolitical tensions are brewing from the Strait of Hormuz to the Strait of Malacca. As we go to press, news is breaking that a Chinese naval vessel almost collided with the USS Decatur as the latter conducted "freedom of navigation" operations within 12 nautical miles of Gaven and Johnson reefs in the Spratly Islands. Given the trade tensions between China and the U.S., this alleged maneuver by the Chinese vessel suggests that Beijing is not backing off from a confrontation. Our view remains that Sino-American trade tensions can get a lot worse before they get better. The latest incident, which builds on a series of negative gestures recently in the South China Sea, suggests that both sides are combining longstanding geopolitical tensions with the trade war. This will likely encourage brinkmanship and further degrade U.S.-China relations. Yet China-U.S. tensions are not the only concern for investors in 2019. Another crisis is brewing in the Middle East, with the potential to significantly increase oil prices over the next 12 months. U.S. households may have to deal with a double-whammy next year: higher costs of imported goods as the U.S.-China trade war rages on and a significant increase in gasoline prices. In this report, we discuss this dire outlook. The Folly Of Recession Forecasting In mid-2017, BCA Research published two reports, one titled "Beware The 2019 Trump Recession" and another titled "The Timing Of The Next Recession."1 Both argued that if the Federal Reserve kept raising rates in line with the FOMC dots, then monetary policy would move into restrictive territory by early 2019 and increase the likelihood of recession thereafter. We subsequently adjusted the timing of our recession forecast to 2020 or beyond, based on a more positive assessment of the U.S. economy. In this report, we explore a risk to the BCA House View on the timing of the next recession. As BCA's long-time Chief Economist Martin Barnes has said, predicting recessions is a mug's game. There have been eight recessions in the past 60 years (excluding the brief 1980-81 downturn) and the Fed failed to forecast all of them (Table 1). Table 1Fed Economic Forecasts Versus Outcomes

2019: The Geopolitical Recession?

2019: The Geopolitical Recession?

The Atlanta Fed produces a recession indicator index which is designed to highlight the odds of recession based on trends in recent GDP data. At the moment, the indicator is at a historically sanguine 2.4%. Unfortunately, low readings are not a reliable cause for optimism. The 1974-75, 1981-82, and 2007-09 recessions were all severe and the Atlanta Fed's recession indicator had a low reading of 10%, 1.6%, and 7.7%, respectively - just as the recession was about to begin (Chart 1). Chart 1The Market Is Not Expecting A Recession

The Market Is Not Expecting A Recession

The Market Is Not Expecting A Recession

The 1974-75 recession is instructive, given the numerous parallels with the current environment: Energy Geopolitics: The 1973 oil crisis caused a massive spike in crude prices. This point is especially pertinent since the 1973 oil embargo is widely viewed as an important contributor to the 1974-75 recession. Real short rates had risen and the yield curve had inverted long before oil prices spiked, so recession was almost inevitable even without the oil price move. But the oil spike made the recession much deeper than otherwise. Protectionism: President Nixon imposed a 10% across-the-board tariff on all imports into the U.S. in 1971 to try to force trade partners to devalue the U.S. dollar. Dislocation: Competition from newly industrialized countries - Japan and the East Asian tigers in particular - laid waste to the steel industry in the developed world. Polarization: President Nixon polarized the nation with both his policies and behavior, leading to his resignation in 1974. Given the exogenous and geopolitical nature of oil supply shocks, today's recession indicators are missing a critical potential headwind to the economy. A geopolitically induced oil-price shock could create more pain than the economy is able to handle. Why An Oil Price Shock? America's renewed foray into the politics of the Middle East will unravel the tenuous equilibrium that was just recently established between Iran and its regional rivals. The U.S.-Iran détente that produced the signing of the 2015 Joint Comprehensive Plan of Action (JCPA) created conditions for a precarious balance of power between Israel and Saudi Arabia on one side, and Iran and its allies on the other side. This equilibrium led to a meaningful change in Tehran's behavior, particularly on the following fronts: The Strait of Hormuz: Tehran ceased to rhetorically threaten the Strait as soon as negotiations began with the U.S. (Chart 2). Since then, Iran's capabilities to threaten the Strait have grown, while the West's anti-mine capabilities remain unchanged.2 Iraq: Iran directly participated in the anti-U.S. insurgency in Iraq. Tehran changed tack after 2013 and cooperated closely with the U.S. in the fight against the Islamic State. In 2014, Iran acquiesced to the removal of the deeply sectarian, and pro-Iranian, Prime Minister Nouri al-Maliki. Bahrain and the Saudi Eastern Province: Iran's material and rhetorical support was instrumental in the Shia uprisings in Bahrain and Saudi Arabia's Eastern Province in 2011 (Map 1). Saudi Arabia had to resort to military force to quell both. Since the détente with the U.S. in 2015, Iranian support for Shia uprisings in these critical areas of the Persian Gulf has stopped. Chart 2Geopolitical Crises And Global Peak Supply Losses

2019: The Geopolitical Recession?

2019: The Geopolitical Recession?

Map 1Saudi Arabia's Eastern Province Is A Crucial Piece Of Real Estate

2019: The Geopolitical Recession?

2019: The Geopolitical Recession?

Put simply, the 2015 nuclear deal traded American acquiescence toward Iranian nuclear development in exchange for Iran's cooperation on a number of strategically vital regional issues. By unraveling that détente, President Trump is upending the balance of power in the Middle East and increasing the probability that Iran retaliates. Since penning our latest net assessment of the U.S.-Iran tensions in May, Iran has already retaliated.3 Our checklist for "kinetic" conflict has now risen from zero to at least 15%, if not higher (Table 2). We expect the probability to rise once the U.S. starts implementing the oil embargo in November. This will dovetail our Iran-U.S. decision tree, which sets the subjective probability of kinetic action by the U.S. against Iran at a baseline of 20% (Diagram 1). Table 2Will The U.S. Attack Iran?

2019: The Geopolitical Recession?

2019: The Geopolitical Recession?

Diagram 1Iran-U.S. Tensions Decision Tree

2019: The Geopolitical Recession?

2019: The Geopolitical Recession?

Bottom Line: The premier geopolitical risk to investors in 2019 is that President Trump's maximum pressure tactic on Iran spills over into Iraq, causing a loss of supply from the world's fifth-largest crude producer.4 We expect the U.S. oil embargo against Iran to remove between 1 million and 1.5 million barrels per day from the market. In addition, the loss of Iraqi production due to sabotage could be anywhere between 500,000 and 3.5 million barrels per day. Added to this total is the potential loss of Venezuelan exports due to the deteriorating situation there. When our commodity team combines all of these factors, they generate a worst-case scenario where the price of crude rises to $110 per barrel in 2019 or higher (Chart 3). And this scenario assumes that EMs do not reinstitute energy subsidies (and therefore their consumption falls faster than if they do reinstitute them). Chart 3Worst-Case Scenario Propels Oil Price Toward 0/Barrel

Worst-Case Scenario Propels Oil Price Toward $110/Barrel

Worst-Case Scenario Propels Oil Price Toward $110/Barrel

The Ayatollah Recession We believe that the midterm election is a dud from an investment perspective, no matter the outcome. However, the election does matter as a hurdle that, once cleared, will allow President Trump to renew his "maximum pressure" tactic against China, Iran, and perhaps domestic tech corporations.5 Iran is a critical risk in this strategy. If President Trump applies maximum pressure on Iran, then a reduction in crude exports from Iran, Iranian retaliation in Iraq, and the simultaneous loss of Venezuelan supplies could combine to increase the likelihood of U.S. recession in 2019. Readers might recall that no sitting president has gotten re-elected during a recession. Why would Trump pursue a policy that risks his re-election chances in 2020? Surely he would deviate from his maximum pressure tactic if faced with the prospect of a recession. However, it is folly to assume that policymakers are perfectly rational, or fully informed. American presidents are some of the most unconstrained policymakers in the world, given both the hard power of the United States and the constitutional lack of constraints on the president when it comes to national security. Trump may believe, for instance, that the 660 million barrels of crude in America's Strategic Petroleum Reserve can offset the impact of sanctions against Iran.6 Or he may believe that he can force OPEC to supply enough oil to offset the Iranian losses. The problem for President Trump is that Iran is not led by idiots. Iranian policymakers understand that the best way to reduce American pressure is to induce an oil price spike in the summer of 2019 that hurts President Trump's re-election chances, forcing him to back off. As such, sabotaging Iraqi oil exports, which mainly transit through the port of Basra - a city highly vulnerable to Shia-on-Shia violence that is already a risk to the country's stability - would be an obvious target. An oil price spike would serve as a negotiating tool against the U.S., and the additional revenue would help replace what Iran loses due to the embargo. Tehran and Washington will therefore play a game of chicken throughout 2019, and there is a fair probability that neither side will swerve. President Trump may be making the same mistake as many predecessors have made, assuming that the Iranian regime is teetering at a precipice and that a mere nudge will force the leadership to negotiate. Oil price shocks and recessions have a historical connection. In a recent report, our commodity strategists highlighted that a spike in oil prices preceded 10 out of the past 11 recessions in the U.S. since 1945 (Table 3). Admittedly, not all spikes were followed by recession. The combination of an oil price spike and Fed rate hikes has produced a recession 8 out of 9 times.7 If oil prices rose to $100 per barrel in the coming 6-12 months, there will be several negative macro consequences. In particular, gasoline prices will rise back toward $4 per gallon (Chart 4). Retail gasoline prices have already increased by more than 50% since they bottomed in February 2016. So how much more upside can the U.S. private sector take? Table 3History Of Oil Supply Shocks

2019: The Geopolitical Recession?

2019: The Geopolitical Recession?

Chart 4A Source Of Pressure For Consumers

A Source Of Pressure For Consumers

A Source Of Pressure For Consumers

The Household Sector Consumer confidence is currently near all-time highs, which tends to signal that the path of least resistance is flat or down (Chart 5). Household gasoline consumption has already declined in response to higher oil prices since the middle of 2017. Given that gasoline demand is relatively inelastic, consumers may already be near their minimum consumption level. Chart 5Nearing All-Time Highs

Nearing All-Time Highs

Nearing All-Time Highs

Instead, households will experience a decline in their disposable income. This will come on the back of both higher gasoline prices and an increase in the prices of other goods and services, as the oil spike spills across sectors. U.S. households - and most likely those in other markets - are stretched to the limit already. A recent Fed survey found that 40% of U.S. households do not have the funds needed to meet an unexpected $400 cost in any given month.8 Such an unexpected expense would require them to either sell possessions, borrow, or cut back on other purchases. Chart 6Most Americans Cannot Cut Saving To Spend

Most Americans Cannot Cut Saving To Spend

Most Americans Cannot Cut Saving To Spend

Left with few other options, households would react to their lower disposable income by reducing demand for other goods and services. This dent in consumer spending would bring down aggregate demand, leading to slower employment growth and even less income and spending. Households could save less to maintain their current purchasing levels, given the recent rise in the savings rate (Chart 6). But this is unlikely. Although the household savings rate has increased in recent years, we have previously argued that a material part of the increase was driven by small business-owner profits. These owners have much higher levels of income than the median consumer. For Americans living paycheck-to-paycheck, it would be difficult to reduce a savings rate that is already close to, or below, zero. Higher oil prices will also hurt growth in Europe and Japan, economies that are already struggling to gain economic momentum after grappling with a weaker growth impulse from China. In addition, EM economies that took the opportunity to reform their oil subsidies amid lower oil prices post-2014 will have to grapple with a much larger shock to consumers than usual. The Corporate Sector In theory, what consumers lose from rising oil prices, producers of crude can gain in stronger revenue. This is especially important in the U.S. as domestic energy production has increased significantly over the past 10 years. Nonetheless, the oil and gas extraction sector accounts for just 1.1% of GDP and 0.1% of total employment. The marginal propensity to spend out of every dollar of income is lower for producers than consumers. Moreover, if consumer confidence fell and consumer spending weakened, non-energy capex would decline as businesses reassessed household demand and held off from making investment decisions. Small business confidence is at record highs, and as with consumer confidence, vulnerable to downward revisions (Chart 7). Chart 7Dizzying Heights

Dizzying Heights

Dizzying Heights

Chart 8Only One Way To Go (Down)

Only One Way To Go (Down)

Only One Way To Go (Down)

Profit margins remain at a highly elevated level and also have only one way to go (Chart 8). If high oil prices should combine with rising borrowing costs and upward pressure on wages (which could develop in this macro environment) the result would be a triple hit to margins (Chart 9). Of course, rising wages would give consumers some offset to higher oil prices, so the question will be the net effect of all variables. And if the dollar bull market continues, as our FX team believes it will, the combination of higher oil prices and a strong USD would hurt U.S. companies with international exposure. The debt load held by the U.S. corporate sector would turn this bad dream into a nightmare. Many American companies have spent the past 10 years increasing leverage to buy back equity (Chart 10). Companies with high debt would need to revise down their profit expectations, with potentially devastating consequences. Elevated debt levels also increase the likelihood of financial market stress if bond investors get worried and spreads begin to widen significantly. Chart 9Rising Pressures On Earnings?

Rising Cost Pressures On Earnings

Rising Cost Pressures On Earnings

Chart 10Large Corporate Debts

Large Corporate Debts

Large Corporate Debts

According to all measures, U.S. stocks are at or near their all-time valuation peaks. Investors have also priced in a significant amount of optimism for profit growth (Chart 11). These expectations would be subject to quick revision if our oil shock scenario plays out. In other words, investor expectations for profit margins are not sufficiently factoring the triple hit of higher oil prices, higher interest rates, and higher wages. Chart 11The Market Has High Hopes

The Market Has High Hopes

The Market Has High Hopes

An additional geopolitical risk on the horizon for 2019 is the creeping "stroke of pen" risk from potential regulation of technology enterprises. This is unrelated to an oil price spike (other than that it would be an effect of U.S. policy) but could nonetheless combine with rising energy prices to sour investors' mood.9 Bottom Line: An oil price spike above $100 would produce negative consequences for the U.S. household and corporate sectors. Given the supply-side nature of the price shock, it would not be accompanied by the usual decline in USD, and could therefore hurt the foreign profits of U.S. corporations as well. If investors must also deal with mounting regulatory pressures on FAANG stocks, they could face a perfect storm. Given the high probability of such an oil price shock, why isn't a 2019 recession BCA's House View, rather than merely a risk to it? Because it is difficult to say how high oil prices need to rise to cause a recession. For example, 1973 both marked a permanent move up in oil prices and saw oil prices triple. In 2019 terms, that would mean an oil price above $200, a far less probable scenario than $100-$110. Nevertheless, the combination of elevated oil prices and the price impact on consumer goods of the U.S.-China trade war could combine to create a nightmare scenario for consumers. But it is impossible to gauge the level of both required to push the U.S. into a recession. Second, there are many ways in which today's macro environment is different from that in 1974. In the 1970s the inventory cycle was a key factor in the business cycle, with excesses building up ahead of recessions, forcing output cutbacks as demand weakened. That is no longer the case in today's world of just-in-time inventory management. Also, inflation was a much bigger problem back then, requiring tougher Fed action. On the other hand, debt burdens were much lower. Investment Implications To be clear, none of the usual recession indicators that BCA Research uses are flashing red at this time. The point of this analysis is to illustrate a credible, exogenous scenario that cannot be revealed through the usual data-driven recession forecasting methods. What happens if a recession does occur ahead of the 2020 election? How would President Trump react to a recession induced by his foreign policy adventurism in the Middle East? By doing what every other president would do: finding someone else to blame. In this case, we would put high odds on the Federal Reserve becoming the target of President Trump's fury. Ahead of 2020, the Fed and its independence may very well become an election issue.10 This could spell serious trouble for the Fed, which is at a massive disadvantage when it comes to explaining to voters why central bank independence is so important. The Fed had great difficulty managing public opinion regarding its extraordinary measures to combat the Great Recession - its attempts at public outreach largely failed. Compare the number of Trump's Twitter followers to that of the Fed's (Chart 12). Chart 12The Fed's PR Abilities Are Limited

2019: The Geopolitical Recession?

2019: The Geopolitical Recession?

Though most of our clients and colleagues will probably disagree, we do not see central bank independence as a static quality. It was bestowed upon central banks by politicians following widespread inflation fears throughout the 1970s and 1980s, although in the U.S. the current tradition goes back to the 1951 Treasury Accord that restored the independence of the Fed. Our colleague Martin Barnes penned a report on the politicization of monetary policy in 2013.11 His conclusion is that political meddling in monetary affairs is less pernicious than economic performance. The Fed will incur Trump's ire, in other words, but it will be its failure to generate economic growth that causes a break in independence. We are not so sure. The next recession is likely to be a mild one for Main Street given the lack of real economic bubbles. But given the slow recovery in real wages over the past decade and the general angst of the populace towards governing elites, even a mild recession that merely reminds voters of 2008-2009 could produce deep anxiety and significant public reactions. Further, the idea of "independent," non-politically accountable institutions is going out of style. President Trump - and other policymakers in the developed world - have specifically targeted the "so-called experts" and "institutions." President Trump has attacked America's foreign policy architecture, NATO, the WTO, and a slew of supposedly outdated norms and practices for being "out of touch" with the electorate. This policy has served him well thus far. If our nightmare scenario of an oil price-induced recession plays out, the immediate implication for investors will be a sharp downturn in risk assets. As such, we are recommending that investors hedge their portfolios with a long Brent / short S&P 500 trade. Alternatively we would recommend going long U.S. energy / short technology stocks. A longer-term, and perhaps even more pernicious implication, would be the end of the era of central bank independence and a full politicization of the economy. Laissez-faire capitalist system would give way to dirigisme. In the process, the U.S. dollar and Treasuries would be doomed. Jim Mylonas, Global Strategist Daily Insights & BCA Academy jim@bcaresearch.com Marko Papic, Senior Vice President Chief Geopolitical Strategist marko@bcaresearch.com 1 Please see BCA Research Special Report, "Beware The 2019 Trump Recession," dated March 7, 2017, and Global Investment Strategy Weekly Report, "The Timing Of The Next Recession," dated June 16, 2017, available at gis.bcaresearch.com. 2 Please see BCA Research Geopolitical Strategy and Commodity & Energy Strategy Special Report, "U.S., OPEC Talk Oil Prices Down; Gulf Tensions Could Become Kinetic," dated July 19, 2018, available at gps.bcaresearch.com. 3 Please see BCA Research Geopolitical Strategy Special Report, "Why Conflict With Iran Is A Big Deal - And Why Iraq Is The Prize," dated May 30, 2018, available at gps.bcaresearch.com. 4 Please see BCA Geopolitical Strategy Weekly Report, "Fade The Midterms, Not Iraq Or Brexit," dated September 12, 2018 and "Iraq: The Fulcrum Of Middle East Geopolitics And Global Oil Supply," dated September 5, 2018, available at gps.bcaresearch.com. 5 Please see BCA Research Geopolitical Strategy Weekly Report, "A Story Told Through Charts: The U.S. Midterm Election," dated September 19, 2018, available at gps.bcaresearch.com. 6 The Strategic Petroleum Reserve currently covers 100 days of net crude imports, or 200 days of net petroleum imports, and can be tapped for reasons of political timing as well as international emergencies. 7 Please see BCA Commodity & Energy Strategy Weekly Report, "Oil-Supply Shock, Rising U.S. Rates Favor Gold As A Portfolio Hedge," dated September 13, 2018, available at bcaresearch.com. 8 Please see the U.S. Federal Reserve, "Report on the Economic Well-Being of U.S. Households in 2017," May 2018, available at federalreserve.gov. 9 Please see BCA Geopolitical Strategy and U.S. Equity Strategy Special Report, "Is The Stock Rally Long In The FAANG?" dated August 1, 2018, available at gps.bcaresearch.com. 10 Please see BCA Daily Insights, "Politics And Monetary Policy," dated August 22, 2018, and "The Battle Of The Press Conferences: Trump Versus Powell," dated September 27, 2018, available at dailyinsights.bcaresearch.com. 11 Please see BCA Special Report, "The Politicization Of Monetary Policy: Should We Care?" dated April 15, 2013, available at bca.bcaresearch.com. Geopolitical Calendar

Highlights Q3/2018 Performance Breakdown: The Global Fixed Income Strategy (GFIS) recommended model bond portfolio outperformed its custom benchmark in the third quarter of 2018 by +9bps. This raised the overall 2018 year-to-date performance to +6bps. Winners & Losers: The outperformance came mostly from our defensive duration positioning, which benefitted as global bond yields rose during the quarter, but also from successful country selection (overweight Australia & New Zealand, underweight the U.S., Canada & Italy). Our underweight tilts on EM credit were the largest drag on performance after the sharp EM rally in September. Scenario Analysis: The combination of defensive overall duration positioning and underweight allocations to EM and European credit should allow the model bond portfolio to outperform its custom benchmark index over the next year. Feature This week, we present the performance numbers of the BCA Global Fixed Income Strategy (GFIS) model bond portfolio for the 3rd quarter of 2018. We also update our scenario analysis of the future expected performance of the portfolio based on the risk-factor based return forecasting framework we introduced earlier this year. As a reminder to existing readers (and for new clients), the portfolio is a part of our service that is meant to complement the usual macro analysis of global fixed income markets. The model portfolio is how we communicate our opinion on the relative attractiveness between government bond and spread product sectors, by applying actual percentage weightings to each of our recommendations within a fully invested hypothetical bond portfolio. Broadly speaking, the portfolio did slightly outperform its benchmark index over the past three months, driven mostly by defensive duration positioning during a period of rising developed market bond yields. The portfolio would have done considerably better if not for a September rally in emerging market (EM) credit that flew in the face of our maximum underweight position in EM. We still have strong conviction in those two main themes - higher global bond yields and EM underperformance - and we fully expect our model portfolio to generate larger outperformance over the next year. Q3/2018 Model Portfolio Performance Breakdown: Duration Underweights Pay Off The total return of the GFIS model bond portfolio was +0.12% (hedged into U.S. dollars) in the third quarter of the year, which outperformed the custom benchmark index by +9bps (Chart of the Week).1 The main driver of the outperformance was our structural below-benchmark portfolio duration stance, which benefited as the overall Bloomberg Barclays Global Treasury Index yield rose to 1.54% - the highest level since April 2014. The portfolio's excess return got as high as +19bps on September 4th, before seeing some pullback in recent weeks as our main spread product tilt - underweight EM hard currency sovereign and corporate debt - enjoyed a counter-trend rally in September from the bearish spread widening seen since the start of 2018. Chart of the WeekDefensive Duration Stance = Q3 Outperformance

Defensive Duration Stance = Q3 Outperformance

Defensive Duration Stance = Q3 Outperformance

Table 1GFIS Model Bond Portfolio Q3/2018 Overall Return Attribution

GFIS Model Bond Portfolio Q3/2018 Performance Review: Inching Ahead

GFIS Model Bond Portfolio Q3/2018 Performance Review: Inching Ahead

In terms of the specific breakdown between the government bond and spread product allocations in our model portfolio, the former generated +17bps of outperformance versus our custom benchmark index while the latter lagged the benchmark by -8bps (Table 1). The bar charts showing the total and relative returns for each individual government bond market and spread product sector are presented in Charts 2 and 3. Chart 2GFIS Model Bond Portfolio Q3/2018 Government##BR##Bond Performance Attribution By Country

GFIS Model Bond Portfolio Q3/2018 Performance Review: Inching Ahead

GFIS Model Bond Portfolio Q3/2018 Performance Review: Inching Ahead

Chart 3GFIS Model Bond Portfolio Q3/2018 Spread##BR##Product Performance Attribution By Sector

GFIS Model Bond Portfolio Q3/2018 Performance Review: Inching Ahead

GFIS Model Bond Portfolio Q3/2018 Performance Review: Inching Ahead

The main individual sectors of the portfolio that drove the excess returns were the following: Biggest outperformers Underweight Japanese government bonds (JGBs) with maturities beyond 10 years (+7bps) Underweight U.S. Treasuries with maturities beyond 7 years (+6bps) Underweight French government bonds with maturities beyond 7 years (+2bps) Underweight Italian government bonds (+2bps) Overweight JGBs with maturities up to 10 years (+1bp) Biggest underperformers Underweight EM USD-denominated sovereign debt (-3bps) Underweight EM USD-denominated corporate debt (-3bps) Underweight euro area investment grade corporate debt (-2bps) Underweight euro area high-yield corporate debt (-1bp) Chart 4 presents the ranked benchmark index returns of the individual countries and spread product sectors in the GFIS model bond portfolio. The returns are hedged into U.S. dollars (we do not take active currency risk in this portfolio) and also adjusted to reflect duration differences between each country/sector and the overall custom benchmark index for the model portfolio. We have also color coded the bars in each chart to reflect our recommended investment stance for each market during the third quarter (red for underweight, blue for overweight, gray for neutral weight). Chart 4Ranking The Winners & Losers From The Model Portfolio In Q3/2018

GFIS Model Bond Portfolio Q3/2018 Performance Review: Inching Ahead

GFIS Model Bond Portfolio Q3/2018 Performance Review: Inching Ahead

Spread product sectors dominate the left half of that chart, as credit spreads have tightened across the board since the early September peak. The best performing sector during Q3 in our model portfolio universe was EM hard currency sovereign debt, which has delivered a total return of +2.8% since September 4th (with spreads tightening by 50bps) after losing -0.7% in July and August. Similar performance stories occurred in corporate debt in the U.S. and Europe during the quarter. That credit outperformance comes after the sustained spread widening seen in virtually all global credit markets (excluding U.S. high-yield) since January of this year. The main drivers that prompted that widening - Fed tightening, a stronger U.S. dollar, diminishing asset purchases from the European Central Bank (ECB) and Bank of Japan (BoJ), some cyclical slowing of non-U.S. growth - are still in place. With our geopolitical strategists continuing to highlight the additional risks of U.S.-China and U.S.-Iran tensions intensifying after next month's U.S. Midterm elections, a cautious stance on global spread product - as we have maintained since downgrading our recommended overall credit exposure to neutral in late June - is still warranted.2 Outside of spread product, our model portfolio tilts generally lined up with the sector returns shown in Chart 4. We have overweights on two of the best performing government bond markets (Australia and New Zealand) and underweights on three of the worst performers (U.S., Canada, Italy). Interestingly, despite having overweights on two of the worst performing government bond markets - Japan and the U.K. - the excess return contribution from those countries did not hurt the model bond portfolio return in Q3 (+8bps and 0bps, respectively). This was due to the curve steepening bias embedded within our overweight country tilts (i.e. more duration allocated to shorter-maturity buckets, see the model portfolio details on Page 14), which benefitted as yield curves in those countries bear-steepened. Net-net, we are satisfied with the modest portfolio outperformance seen in Q3, given that the rally in global credit markets went against our more defensive posture on spread product exposure. Bottom Line: The GFIS recommended model bond portfolio outperformed its custom benchmark in the third quarter of 2018 by +9bps. This put the overall 2018 year-to-date performance into positive territory (+6bps). The outperformance came entirely from our defensive duration positioning, which benefitted as global bond yields rose during the quarter, and from successful country selection. Our underweight tilts on EM credit were the largest drag on performance after the sharp EM rally in September. Future Drivers Of Portfolio Returns Looking ahead, the performance of the model bond portfolio will continue to benefit from two primary trends: rising global bond yields and growth divergences that continue to favor the U.S. In terms of the specific weightings in the GFIS model bond portfolio, we still prefer owning U.S. corporate debt versus equivalents in Europe and EM. When we downgraded our recommended allocation to U.S. and investment grade corporates to neutral from overweight back in July, we also cut the portfolio exposure to euro area corporates, as well as to all EM hard currency debt, to underweight. The latter changes were necessary to maintain our desired higher exposure to U.S. corporate debt versus non-U.S. corporates, although it did leave the model portfolio with a small overall underweight stance on global spread product (Chart 5). Importantly, we are maintaining a below-benchmark stance on overall portfolio duration, which is now one full year shorter than our benchmark index duration (Chart 6), even as we have grown more cautious on credit exposure. This is because we still see potential medium-term upward pressure on bond yields coming from tightening monetary policies (Fed rate hikes, ECB tapering of bond purchases) and increasing inflation expectations. The majority of global central bankers are dealing with tight labor markets and slowly rising inflation rates. While global growth has cooled a bit from the rapid pace seen in 2017, it has not been by enough to force policymakers to shift to a more dovish bias. Chart 5Spread Product Allocation:##BR##Neutral U.S., Underweight Non-U.S.

GFIS Model Bond Portfolio Q3/2018 Performance Review: Inching Ahead

GFIS Model Bond Portfolio Q3/2018 Performance Review: Inching Ahead

Chart 6Maintaining##BR##Below-Benchnmark Duration

Maintaining Below-Benchnmark Duration

Maintaining Below-Benchnmark Duration

Our underweights on EM and euro area spread product have left the portfolio in a "negative carry" position where it yields 34bps less than the benchmark index (Chart 7). In a backdrop of stable markets and low volatility, being short carry will be a drag on the model bond portfolio performance as we saw over the past month. Yet we do not see the recent market calm as being sustainable, with all plausible outcomes pointing to more volatile markets, largely driven by U.S.-centric events (more Fed tightening, a stronger dollar, U.S. growth convergence to slower non-U.S. growth, increased trade protectionism, higher oil prices due to U.S.-Iran tensions). We continue to suggest a cautious allocation of investor risk budgets against this backdrop. We have been targeting a tracking error (relative volatility versus the benchmark) for our model bond portfolio in the 40-60bp range, well below our 100bps maximum. Our current allocations give us a tracking error right at the bottom of that range (Chart 8).3 Chart 7The Cost Of Being More Defensive On Credit

The Cost Of Being More Defensive On Credit

The Cost Of Being More Defensive On Credit

Chart 8Maintaining A Cautious Allocation Of The Risk Budget

Maintaining A Cautious Allocation Of The Risk Budget

Maintaining A Cautious Allocation Of The Risk Budget

Scenario Analysis & Return Forecasts Back in April of this year, we introduced a framework for estimating total returns for all government bond markets and spread product sectors, based on common risk factors.4 For credit, returns are estimated as a function of changes in the U.S. dollar, the Fed funds rate, oil prices and market volatility as proxied by the VIX index (Table 2A). For government bonds, non-U.S. yield changes are estimated using historical betas to changes in U.S. Treasury yields (Table 2B). This framework allows us to conduct scenario analysis based on projected returns for each asset class in the model bond portfolio universe by making assumptions on those individual risk factors. Table 2AFactor Regressions Used To Estimate##BR##Spread Product Yield Changes

GFIS Model Bond Portfolio Q3/2018 Performance Review: Inching Ahead

GFIS Model Bond Portfolio Q3/2018 Performance Review: Inching Ahead

Table 2BEstimated Government Bond##BR##Yield Betas To U.S. Treasuries

GFIS Model Bond Portfolio Q3/2018 Performance Review: Inching Ahead

GFIS Model Bond Portfolio Q3/2018 Performance Review: Inching Ahead

With these tools, we than can attempt to forecast returns for each bond sector under different scenarios. We can then use those forecasts to predict the expected return for our model bond portfolio under those same scenarios. In Tables 3A & 3B. we show three differing scenarios, with all the following changes occurring over a one-year horizon. Table 3AScenario Analysis For The GFIS Model Portfolio

GFIS Model Bond Portfolio Q3/2018 Performance Review: Inching Ahead

GFIS Model Bond Portfolio Q3/2018 Performance Review: Inching Ahead

Table 3BU.S. Treasury Yield Assumptions For The Scenario Analysis

GFIS Model Bond Portfolio Q3/2018 Performance Review: Inching Ahead

GFIS Model Bond Portfolio Q3/2018 Performance Review: Inching Ahead

Our Base Case: the Fed delivers another 100bps of rate hikes, the U.S. dollar rises +5%, oil prices rise by +10%, the VIX index increases by five points from current levels, and U.S. Treasury yields rise by 40bps across the curve. A Very Hawkish Fed: the Fed delivers 150bps of rate hikes, the U.S. dollar rises by +10%, oil prices rise by +10%, the VIX index increases by ten points from current levels and there is a sharp bear flattening of the U.S. Treasury curve (2yr yield +75bps, 10yr yield +40bps). A Very Dovish Fed: the Fed only hikes rates by 25bps, the U.S. dollar falls by -5%, oil prices fall by -20%, the VIX index increases by fifteen points from current levels and there is a modest bull steepening of the U.S. Treasury curve. In this scenario, the Fed puts the rate hiking cycle on hold in response to a sharp tightening of U.S. financial conditions. Table 3A shows the expected returns for all three scenarios based on our risk-factor framework. The model bond portfolio is expected to outperform the custom benchmark index in all three scenarios we have laid out. This occurs even with the negative carry coming from the credit underweights in EM and Europe, with losses from credit spread widening projected to be larger than the yield give-up from being underweight. The excess returns are modest, however, with only 6bps of outperformance expected in our base case scenario and 13bps expected in the "Very Hawkish Fed" and "Very Dovish Fed" scenarios. This return distribution, with better outcomes occurring in the "tails", is a desirable property to have as it relates to the VIX/volatility forecasts embedded in the scenarios. Both of the non-base case scenarios have a higher VIX (Chart 9), even in the case of the "Very Dovish Fed" outcome where a severe U.S. financial market selloff (coming complete with a higher VIX) would be the necessary trigger for the Fed to reverse course and begin cutting interest rates (Chart 10). Such a backdrop would obviously hurt our below-benchmark duration stance, but would help our underweight EM/Europe spread product recommendations. Chart 9Risk Factors For Scenario Analysis

Risk Factors For Scenario Analysis

Risk Factors For Scenario Analysis

Chart 10UST Yield Moves For Scenario Analysis

UST Yield Moves For Scenario Analysis

UST Yield Moves For Scenario Analysis

Of course, our recommendations will not be static at current levels throughout the next twelve months. We increasingly expect that our next major allocation move will be downgrade U.S. spread product exposure and raise U.S. Treasury allocations, especially after the Fed delivers a few more 25bps-per-quarter rate hikes and the U.S. dollar rises further. This will provide a boost to the portfolio's expected returns through renewed spread widening and, potentially, a reduction of our below-benchmark overall duration stance as Treasury yields reach likely cyclical peaks. Bottom Line: The combination of defensive overall duration positioning and underweight allocations to EM and European credit should allow the model bond portfolio to outperform its custom benchmark index over the next year. Robert Robis, CFA, Senior Vice President Global Fixed Income Strategy rrobis@bcaresearch.com 1 The GFIS model bond portfolio custom benchmark index is the Bloomberg Barclays Global Aggregate Index, but with allocations to global high-yield corporate debt replacing very high quality spread product (i.e. AA-rated). We believe this to be more indicative of the typical internal benchmark used by global multi-sector fixed income managers. 2 Please see BCA Global Fixed Income Strategy Weekly Report, "Time To Take Some Chips Off The Table: Downgrade Global Spread Product Exposure To Neutral", dated June 26th 2018, available at gfis.bcaresearch.com. 3 In general, we aim to target a tracking error no greater than 100bps. We think this is reasonable for a portfolio where currency exposure is fully hedged and less than 5% of the portfolio benchmark is in bonds with ratings below investment grade. 4 Please see BCA Global Fixed Income Strategy Weekly Report, "GFIS Model Bond Portfolio Q1/2018 Performance Review: A Rough Start", dated April 10th 2018, available at gfis.bcareseach.com. Recommendations Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

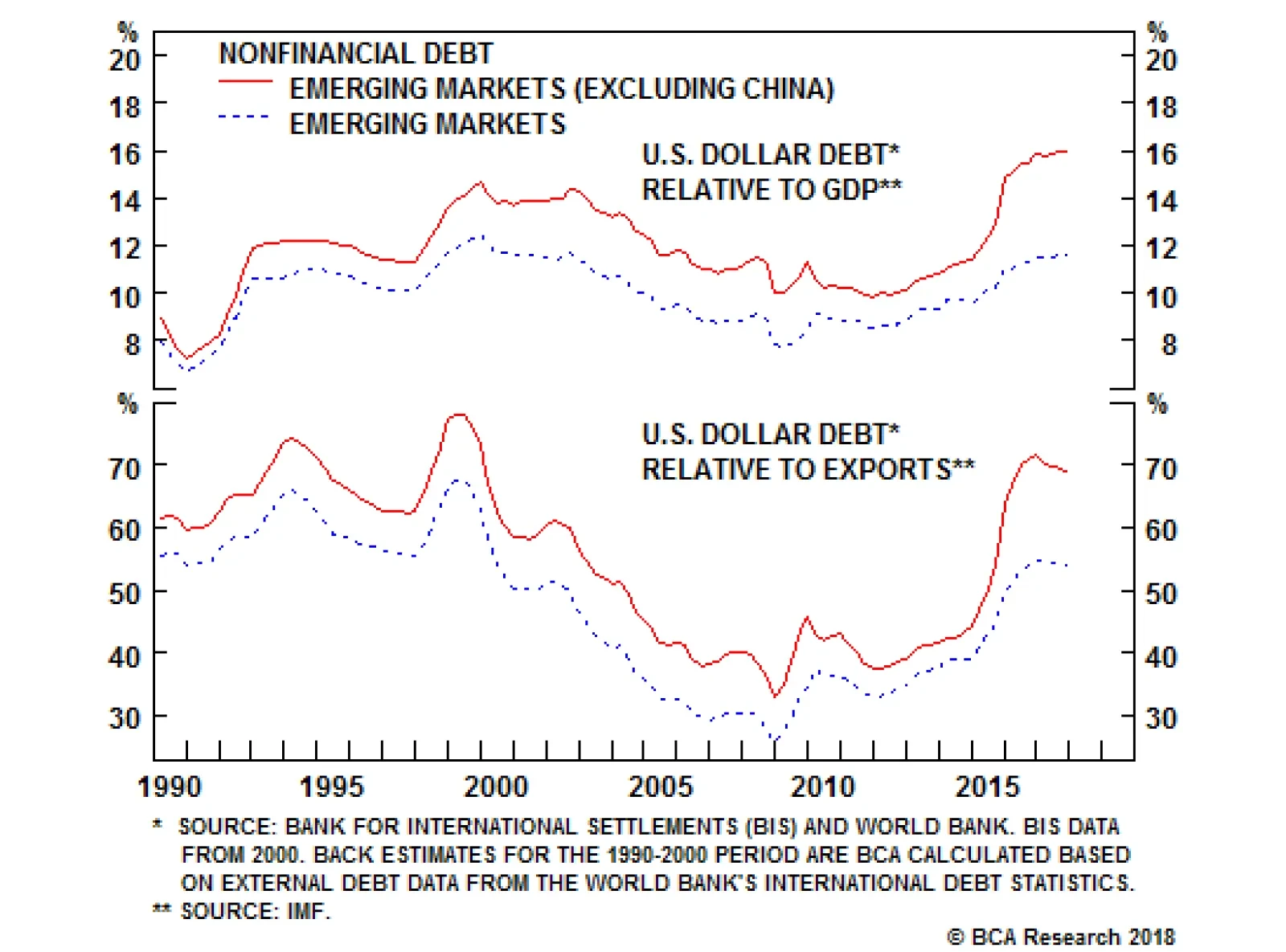

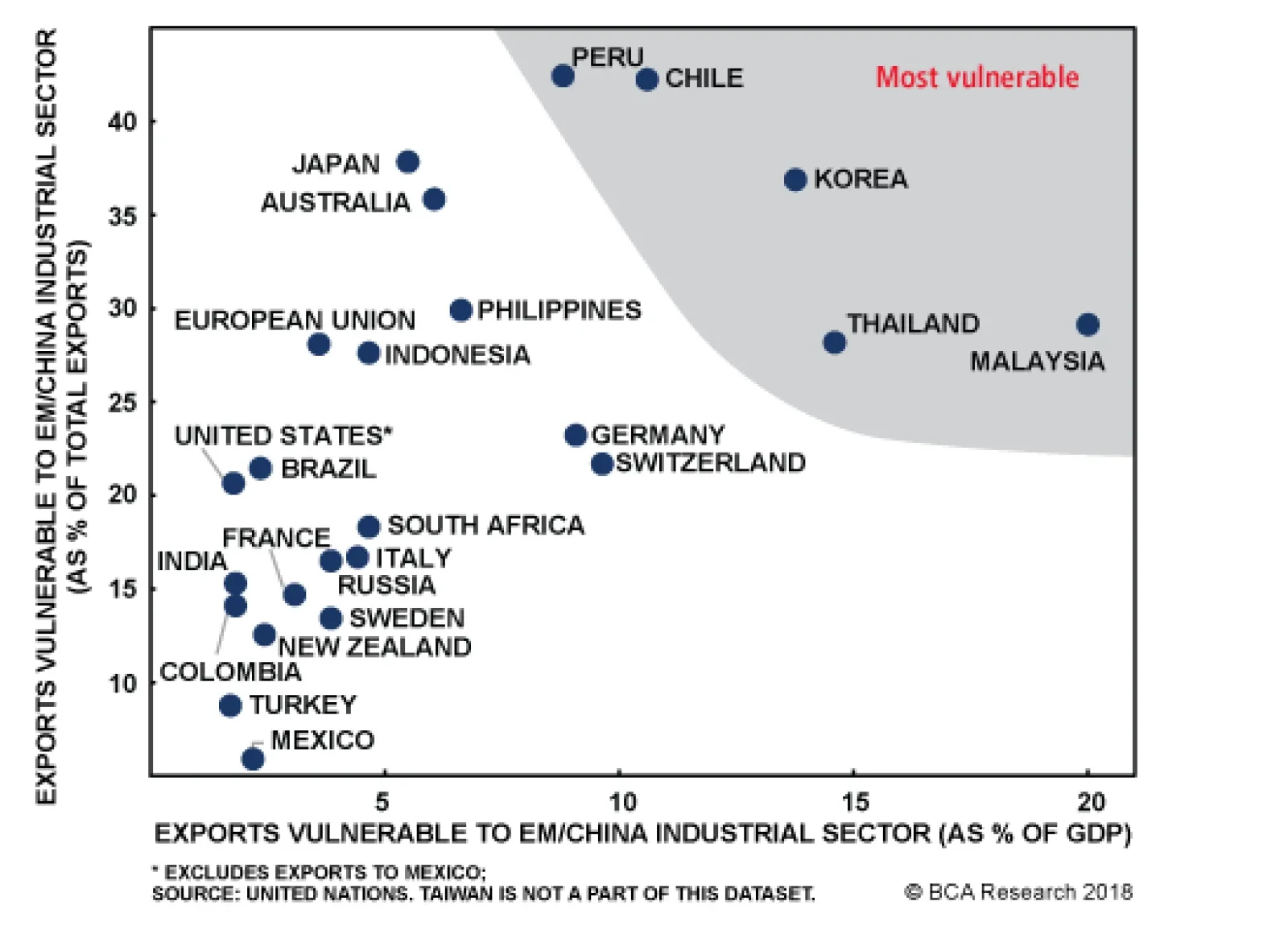

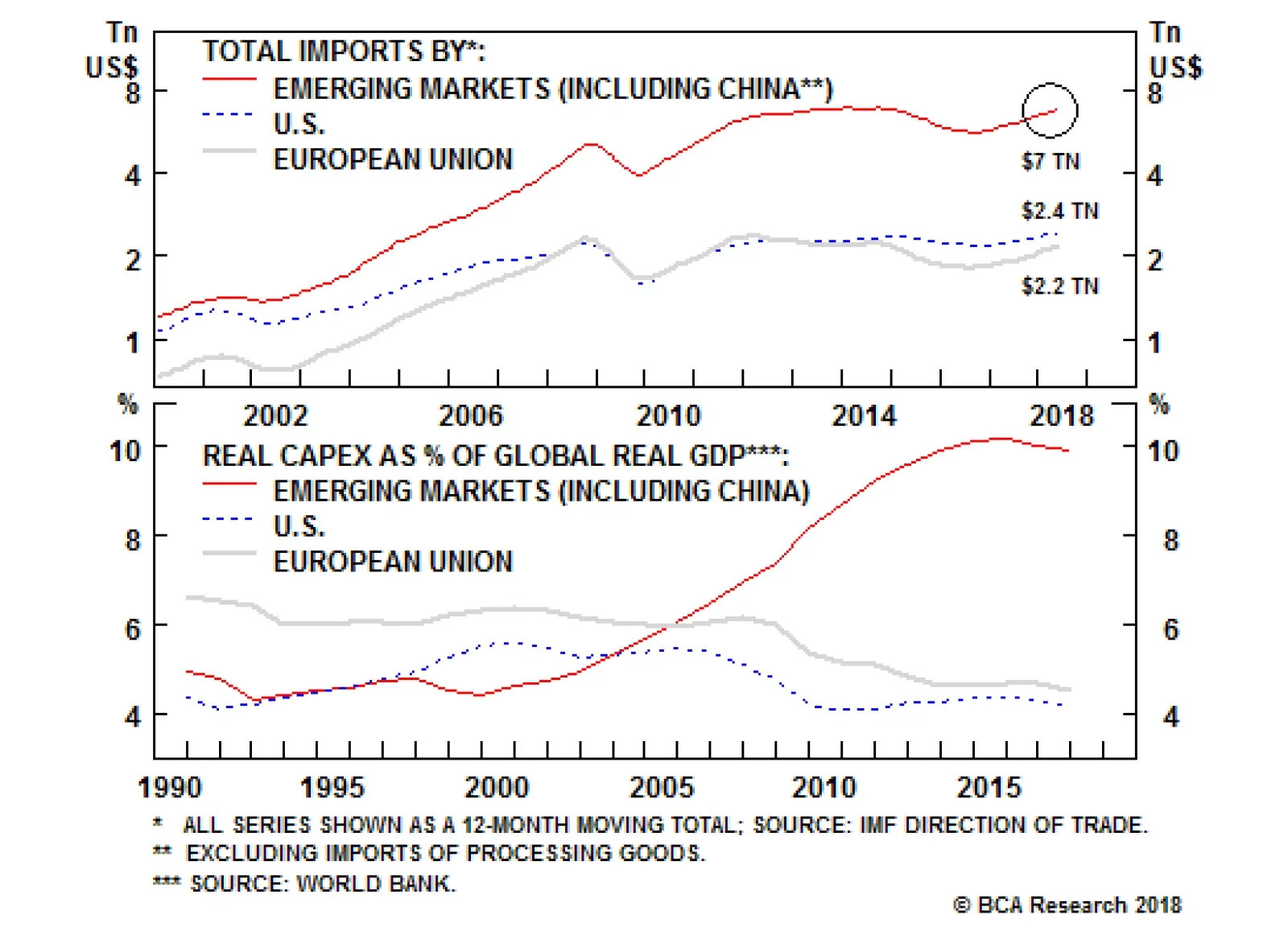

Eighty percent of EM foreign-currency debt is denominated in dollars. Outside of China, EM dollar debt is now back to late-1990s levels, as a share of both GDP and exports. The large stock of EM local-currency debt issued in recent years only complicates…

Highlights Recommended Allocation

Quarterly - October 2018

Quarterly - October 2018

We don't see any change over the next six to 12 months to the current trends of strong U.S. growth, continuing Fed hikes, rising long-term interest rates, and an appreciating dollar. We stay neutral on global equities and continue to favor the U.S. and, to a degree, Japan. Given rising rates, a strengthening dollar, ongoing trade war and moderate slowdown in China, we expect EM assets to sell off further. We forecast the 10-year U.S. Treasuries yield to rise to 3.5% by H1 2019, and so we stay underweight fixed income, short duration, and continue to prefer TIPs. We are only neutral on credit within the (underweight) fixed-income bucket. We shift our equity sector weightings to reflect the GICS recategorization. We recommend a neutral on the new internet-heavy Communication sector, and underweight on Real Estate. We have a somewhat defensive sector bias, with overweights in Consumer Staples and Healthcare. Alternative risk assets, such as private equity and real estate, look increasingly overheated. We prefer hedge funds and farmland at this stage of the cycle. Overview More Of The Same When there's been a strong trend, it's always tempting to be contrarian and argue for a reversal. Tempting but, at the moment, we think wrong. This year has been characterized by a strong U.S. economy but slowing growth elsewhere, the outperformance of U.S. equities (up 10% year-to-date, compared to a 4% decline in the rest of the world), rising U.S. interest rates, dollar appreciation, and a big sell-off in emerging markets. While a short-term correction is always possible, we don't see a fundamental end to these trends over the next 6 to 12 months. Chart 1U.S. Growth Still Looks Strong

U.S. Growth Still Looks Strong

U.S. Growth Still Looks Strong

Chart 2Growth In Europe And Japan Has Slipped

Growth In Europe And Japan Has Slipped

Growth In Europe And Japan Has Slipped

U.S. growth is likely to remain strong. Consumer and business sentiment are both close to record highs; wage growth is beginning (finally) to accelerate; capex intentions are buoyant; and fiscal stimulus will add 0.7% to GDP growth this year and 0.8% next, as the budget deficit widens to close to 6% of GDP (Chart 1). Europe and Japan, by contrast, have slowed this year: both are more exposed to emerging markets than is the U.S.; fiscal policy in neither is particularly accommodative; and European banks suffer from weak loan growth and their EM exposure (Chart 2). The one trigger that would cause global ex-U.S. growth to accelerate relative to U.S. growth is a massive stimulus in China similar to 2009 and 2015. We think this unlikely because the authorities have reiterated their commitment to deleveraging and structural reform. Chinese credit growth and money supply data have as yet shown no signs of picking up, but they should be monitored carefully (Chart 3). Chart 3Chinese Stimilus, What Stimilus?

Chinese Stimilus, What Stimilus?

Chinese Stimilus, What Stimilus?

Chart 4Republicans Like Trump's Tough Trade Talk

Quarterly - October 2018

Quarterly - October 2018

An end to the trade war might also reverse the trends. U.S. markets have shrugged off the risk of escalating retaliatory tariffs on the (reasonable) grounds that trade has relatively little impact on the U.S. It is hard to see an end-game to the tariff war. President Trump's popularity has risen since he got tough on trade (Chart 4). He has changed his mind on many areas of policy during his career, but he's always consistently argued that the U.S. deficit shows that its trading partners treat it unfairly. The probability is high that the 10% tariff on $200 billion of Chinese goods will rise to 25% in January, and is eventually extended to all Chinese imports. It is equally unlikely that Xi Jinping will make concessions, since he can't be seen to bend to U.S. pressure and won't put at risk the crucial "Made in China 2025" plan. Chart 5Phillips Curve Working Again

Phillips Curve Working Again

Phillips Curve Working Again

Although tariffs may not hurt U.S. growth much, they could be inflationary. The price of washing machines, the subject of the earliest tariffs in January, rose by 18% over the next four months. This is just another reason why it's unlikely that the Fed will slow its pace of rate hikes. With the labor market now clearly tight, there are signs that the Phillips curve is beginning to reassert itself (Chart 5), and wage growth is accelerating. With core PCE inflation at its 2% target and the impact of fiscal stimulus still coming through, the Fed will feel comfortable about maintaining its current schedule of one 25 basis point hike a quarter until there are signs that the economy is slowing.1 Could the sell-off in emerging markets cause the Fed to move to hold? In the 1990s Asia Crisis, only when the fall in Asian stocks started to affect the U.S. economy (with, for example, the manufacturing ISM going below 50) and the U.S. stock market, did the Fed ease policy (Chart 6). Eventually, the slowdown in the rest of the world might start to hurt the U.S. In the past, when the global ex-U.S. Leading Economic Indicator has fallen below zero, it has usually been followed by U.S. growth also faltering (Chart 7). Chart 6In 1998, Fed Cut Only When EM Hurt The U.S.

In 1998, Fed Cut Only When EM Hurt The U.S.

In 1998, Fed Cut Only When EM Hurt The U.S.

Chart 7When The World Slows, Often U.S. Does Too

When The World Slows, Often U.S. Does Too

When The World Slows, Often U.S. Does Too

Table 1What To Watch For

Quarterly - October 2018

Quarterly - October 2018

Having in June lowered our recommendation on global equities to neutral (but keeping our overweight on U.S. stocks), we continue to monitor the factors that would make us turn negative on risk assets (Table 1 and Chart 8). None of them is yet flashing a warning signal, but it seems likely that we will need to move to an outright defensive stance sometime in H1 2019. One final key thing to watch: any signs that U.S. earnings growth is slipping. Much of the outperformance of U.S. equities this year is simply explained by better earnings growth, partly due to the tax cuts. Analysts' forecasts for 2019 have so far been very stable. If they start to be revised down, perhaps because of higher wages and export sales being dampened by the strong dollar, that would also be a signal to switch out of U.S. equities (Chart 9). Chart 8What To Watch For?

What To Watch For?

What To Watch For?

Chart 9Will Analysts Revise Down EPS Forecasts?

Will Analysts Revise Down EPS Forecasts?

Will Analysts Revise Down EPS Forecasts?

Garry Evans, Senior Vice President Global Asset Allocation garry@bcaresearch.com What Our Clients Are Asking Is The Fed Turning Dovish? Chart 10Fed Policy Still Accomodative

Fed Policy Still Accomodative

Fed Policy Still Accomodative

Many investors interpreted Fed Chair Powell's speech at Jackson Hole in August dovishly. Powell questioned whether "policymakers should navigate by [the] stars": r* (the neutral rate of interest) and u* (the natural rate of unemployment), since these are uncertain. He emphasized that policy will be data dependent. We read it differently. Powell also pointed out that "inflation is near our 2 percent objective, and most people who want a job are finding one", and concluded that a "gradual process of normalization remains appropriate". A speech in September by Lael Brainard, a dovish FOMC member, reinforced this. She separated the long-run neutral rate (the terminal rate in the Fed dot plot) from the short-term neutral rate (Chart 10, panel 1). Her conclusion was that "with fiscal stimulus in the pipeline and financial conditions supportive of growth, the shorter-run neutral interest rate is likely to move up somewhat further, and it may well surpass the long-run equilibrium rate." In other words, the Fed needs to continue its gradual pace of hikes. The market does not see it that way. Futures markets have priced in that the Fed will raise rates until June (when the Fed Funds Rate will be 2.75-3% in nominal terms) and then stop (panel 2). But this implies that the Fed will halt once the FFR is at the (current estimate of the) neutral rate. But inflation is likely to pick up further over the next 12 months. And the Fed is worried that, despite rate hikes, financial conditions haven't tightened much (panel 3). So we expect the Fed to keep tightening until there are signs that growth is slowing. Is The Worst Over For Emerging Markets? Chart 11Excess Debt Is Underlying Cause Of EM Sell-Off

Excess Debt Is Underlying Cause Of EM Sell-Off

Excess Debt Is Underlying Cause Of EM Sell-Off

Since the plunge in the Argentinian peso and Turkish lira, currencies in most emerging markets have fallen sharply. Does this present a buying opportunity for investors, or is there more contagion to come? While a short-term rebound is not impossible, we remain very negative on the outlook for most emerging market assets. Fed policy and rising U.S. interest rates can be seen as the trigger for, but not the underlying cause of, the recent sell-off. Since 1980 (Chart 11), there have been only two instances where EM stock prices collapsed amid rising U.S. rates: the 1982 Latin American debt crisis and the 1994 Mexican Tequila crisis. But both occurred because of poor EM fundamentals. We see similar underlying problems today. EM dollar-denominated debt as a share of GDP and exports is as high as it was during the Asia Crisis in the late 1990s. In addition, the EM business cycle will continue to decelerate in the medium term, as evidenced by falling manufacturing PMIs. Consequently, EM corporate earnings growth is slowing, and we expect it to fall meaningfully in this downturn. EM economies have become increasingly dependent on Chinese growth for their export demand. China is slowing, but we expect limited credit and fiscal stimulus from the authorities given their shift in focus towards de-leveraging and reforming the financial sector. Additionally, global trade is also weakening as seen by falling Asian exports and sluggish container freight movements. EM central banks have responded to currency weakness by raising rates, which in turn will lead to rising local currency bond yields and tightening financial conditions. A tightening of liquidity will slow money and credit creation, ultimately weighing on domestic demand. Moreover, with an accelerating U.S. economy, the U.S. dollar will continue to strengthen, eventually tightening global liquidity. We continue to advocate an underweight position in EM assets. Share prices will not bottom until EM interest rates fall on a sustainable basis, or until valuations reach clearly over-sold levels, which they have not yet. Chart 12The New Sectors Look Very Different

Quarterly - October 2018

Quarterly - October 2018

What Just Happened To GICS? Following Real Estate's 2016 separation from Financials to become the 11th sector within GICS, September 28 2018 marked an even more disruptive change to equity classification. The change, aimed at keeping up with innovation and the current market structure, affects three of the 11 sectors: Telecommunication Services, Consumer Discretionary, and Information Technology (Chart 12). In short, the Telecommunication Services sector, once a value, low-weight, low-beta, high-yield, defensive sector is broadened and renamed Communication Services, offering broad-based coverage of content on various internet and media platforms. It includes the Media group, as well as selected companies from Internet & Direct Marketing Retail, taken out of Consumer Discretionary. Additionally, selected companies from the Internet Software & Services, as well as Application and Home Entertainment Software move into the new sector from IT. The E-commerce group also grows, with selected companies moving out of IT into Consumer Discretionary. Telecom/Communication, which previously behaved like Utilities, has turned into a high-growth, low-dividend sector. It is also a cyclical rather than defensive. It should trade at much higher multiples than its previous incarnation. IT is also no longer be the same. The sector, which once represented nearly 20% of the ACWI index, has shrunk to 13%, now mostly comprises hardware and software companies, after losing constituents such as Alphabet, Facebook, and Tencent. Chart 13Three Ideas To Enhance Risk-Adjusted Return

Three Ideas To Enhance Risk-Adjusted Return

Three Ideas To Enhance Risk-Adjusted Return

Where To Find Yield In A Low-Return Environment? BCA's House View in June downgraded equities to neutral and moved cash to overweight. For U.S. investors, holding cash is quite attractive, as the yield on three-month Treasury bills is above 2%, higher than the 1.8% dividend yield on equities. But investors in Europe and Japan face negative yields on cash. Our recent Special Report analyzed three investment instruments that could enhance a balanced portfolio's risk-adjusted returns (Chart 13).2 Floating-Rate Notes. FRNs tend to be issued by government-sponsored enterprises and investment-grade corporations. They offer a nice yield pick-up over short-term U.S. Treasuries with significantly shorter duration. However, they do carry credit risk and so performed poorly in the 2007-9 recession. We, therefore, recommend investors fund these positions from their high-yield bucket. Leveraged Loans. These are floating-rate senior-secured bank loans. However, secured does not mean safe. Most are sub-investment grade and can be very illiquid, because physical delivery is often needed. They tend to be positively correlated with junk bonds but negatively correlated with the aggregate bond index. This suggests that adding bank loans to a portfolio can add diversification, and that replacing some high-yield holdings with bank loans can generate a sub-investment grade basket with a better risk/reward profile. Danish Mortgage Bonds. DMBs are covered mortgage bonds, with an average duration of five years and offering a yield to maturity of around 2% in Danish Krone. They have a strong track record: not a single bond has defaulted in the 200-year history of the market. This makes the market very attractive to euro zone and Japanese investors struggling with low bond yields. We find that adding DMBs to a standard bond portfolio significantly improves its risk/return profile. The main snags are that this is a fairly small market with a total outstanding market value of DKR2.7 trillion (around USD400 billion) - and is already 23% owned by foreigners. Global Economy Overview: The global economy will continue to be characterized by significant divergences. U.S. growth remains robust, pushing up inflation to the Fed's 2% target. By contrast, European and Japanese growth has weakened so far this year, meaning that central banks there remain cautious about tightening. Meanwhile, emerging markets will continue to deteriorate, faced with an appreciating dollar, rising U.S. interest rates, and lack of a big stimulus in China. U.S.: The ISM manufacturing index hit a 14-year high, above 60, in September before falling back slightly, to 59.8, in October. Core PCE inflation has reached 2%, the Fed's target. Wage growth, as measured by average hourly earnings, has finally begun to accelerate, reaching 2.9% YoY. With consumption and capex likely to remain robust, and the effect of fiscal stimulus not peaking until early next year, the U.S. economy will continue to grow strongly through 2019 (Chart 14). Only the recent slowdown in housing (probably caused by higher interest rates) remains a concern, but the sector is probably too small to derail overall economic growth. Chart 14Divergences Continue: U.S. Strong...

Divergences Continue: U.S. Strong...

Divergences Continue: U.S. Strong...

Chart 15...Rest Of The World Weakening

...Rest Of The World Weakening

...Rest Of The World Weakening