Emerging Markets

Chinese private sector credit demand remained weak in February, sending a negative signal about domestic economic conditions. Total social financing growth slowed from a record CNY6.5 trillion in January to CNY1.56 trillion, below consensus forecasts of…

Chinese stocks are experiencing their longest rally since the country’s exit from Covid restrictions over a year ago. The MSCI Onshore and Investable indices (in USD terms) have gained 15.8% and 9.1% respectively since February 5th, with the former…

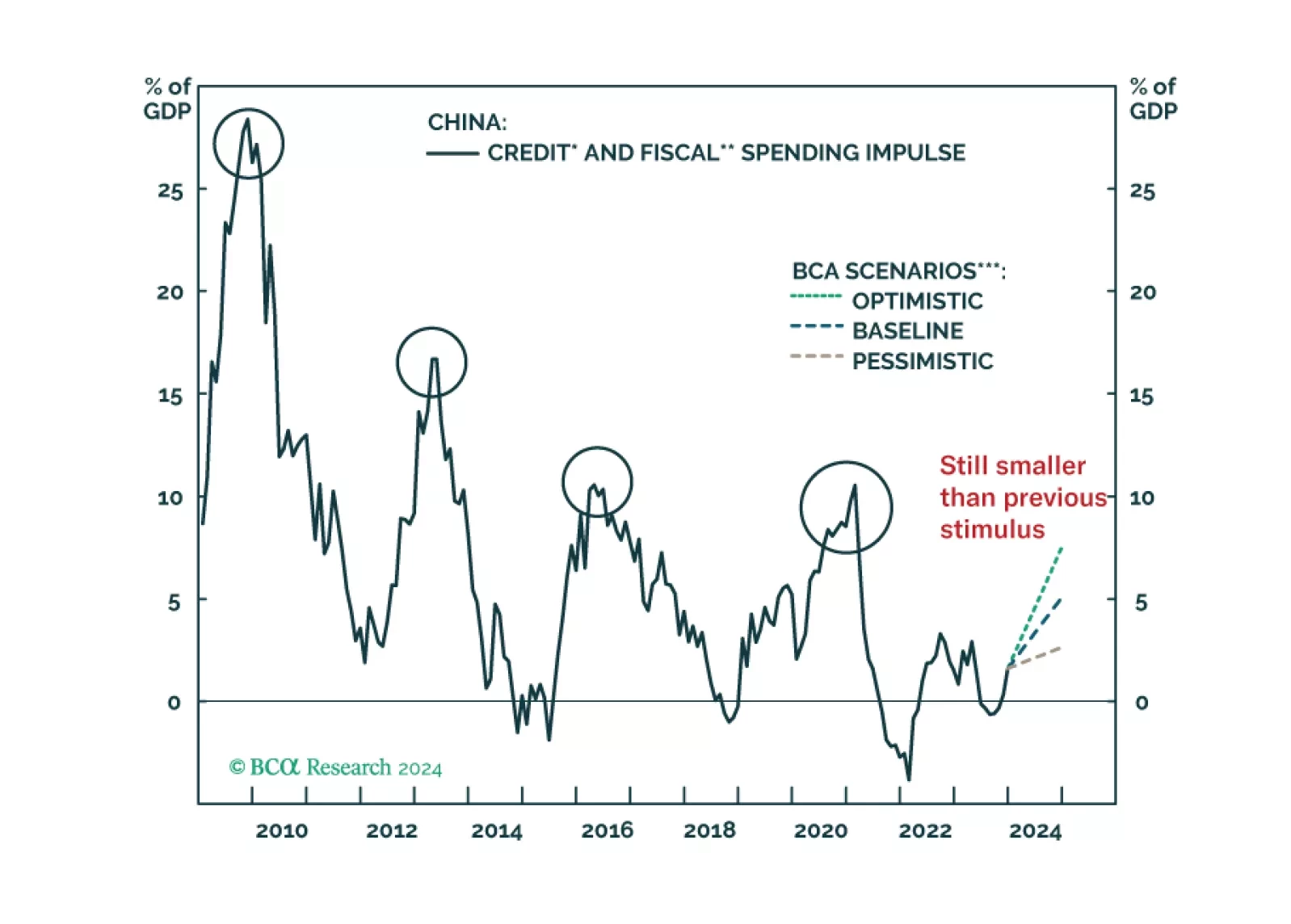

According to BCA Research’s China Investment Strategy service, a very substantial PSL financing scheme for housing, a large LG and LGFV debt swap, and considerable fiscal transfers to households—or a combination thereof— might lead them to upgrade their…

The stimulus measures announced at last week's NPC were not a game changer. As in 2023, we expect aggregate government spending will fall short of the budgeted amount again this year.

Our Emerging Markets Strategy team posits that the South African economy is heading into a recession later this year. The South African government refrained from announcing any stimulus measures in its recent budget proposals. The fiscal plan for 2024-25…

Presently, our four high-conviction themes are: (1) the US dollar will rally as US growth continues to outpace the rest of the world; (2) US equities will continue to outperform EM and European stocks until a major sell-off occurs; (3) a US profit margin squeeze is imminent; (4) EM domestic bonds and sovereign USD bonds are due for a setback.

In the past couple of years, Mexico has been among the favorite markets for investors within the EM space. As our Emerging Markets Strategy team argued in a recent report, the cyclical and structural outlook for Mexican risk assets remains brighter than ever.…

Our Emerging Market Strategy (EMS) colleagues recommended booking an 11.4% gain on their Egyptian T-bill trade initiated earlier in the year. Now that currency-devaluation risk has been removed from the picture for the foreseeable future, they are…

A market-cap weighted index of CE3 economies (Poland, Hungary and Czechia) returned a whopping 64% in common currency terms since its 2022 low. Polish and Hungarian equities led the rally, advancing by a respective 86% and 78% in local currency terms…