Emerging Markets

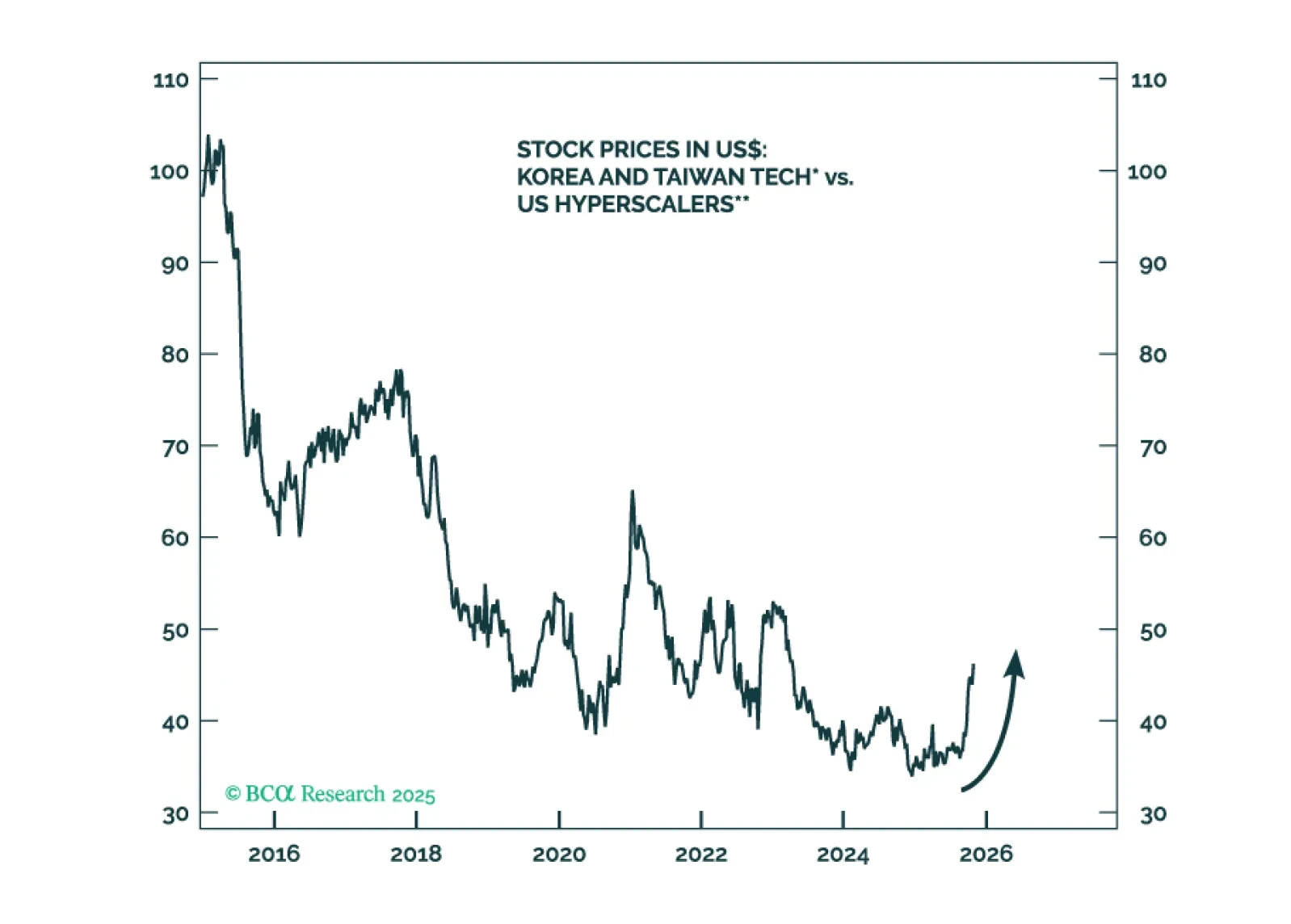

We recommend a new relative tech equity trade that will likely produce positive returns over the next six to 12 months, regardless of whether the AI hype continues or reverses.

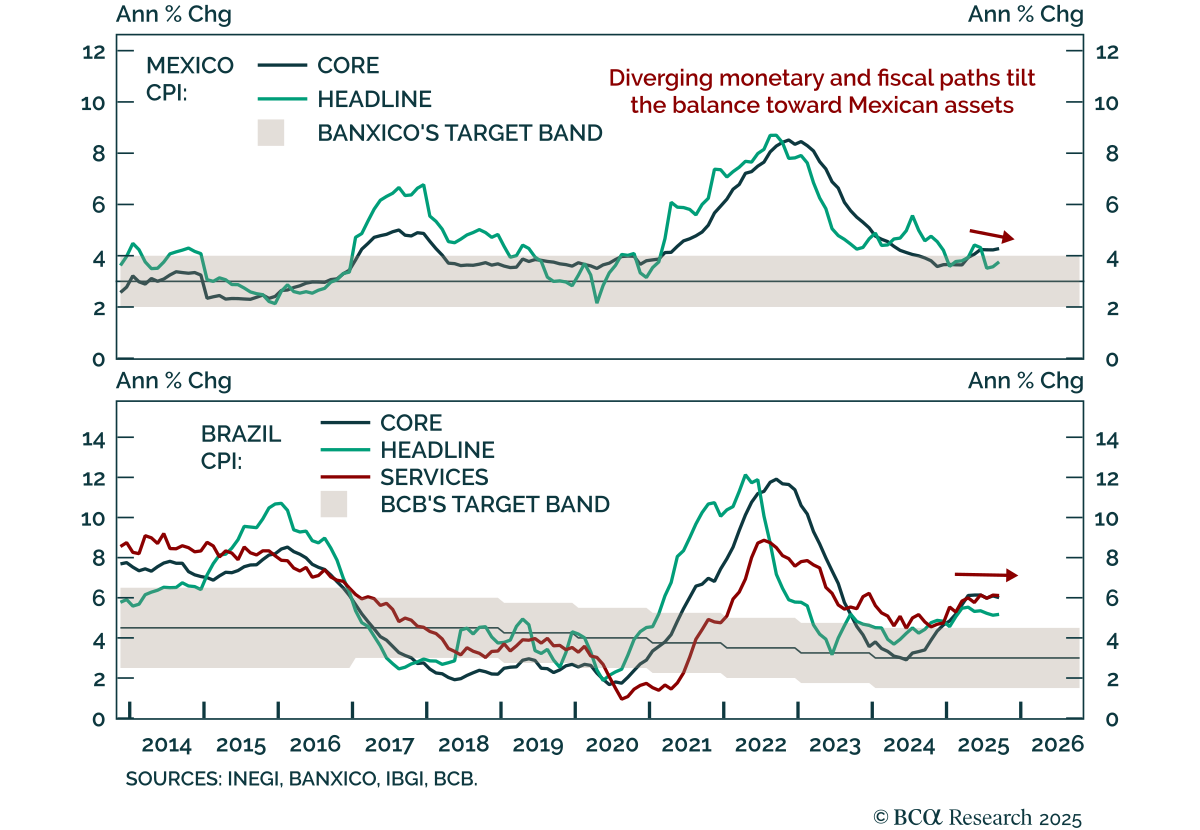

Brazil’s bleak macro outlook persists – rising debt, weak productivity, and political inertia. With 2026 elections looming, genuine reform seems unlikely, though Argentina’s bold turnaround could pressure Brasília to rethink its cycle of governability over growth.

MacroQuant is tactically overweight equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is bullish on gold and copper.

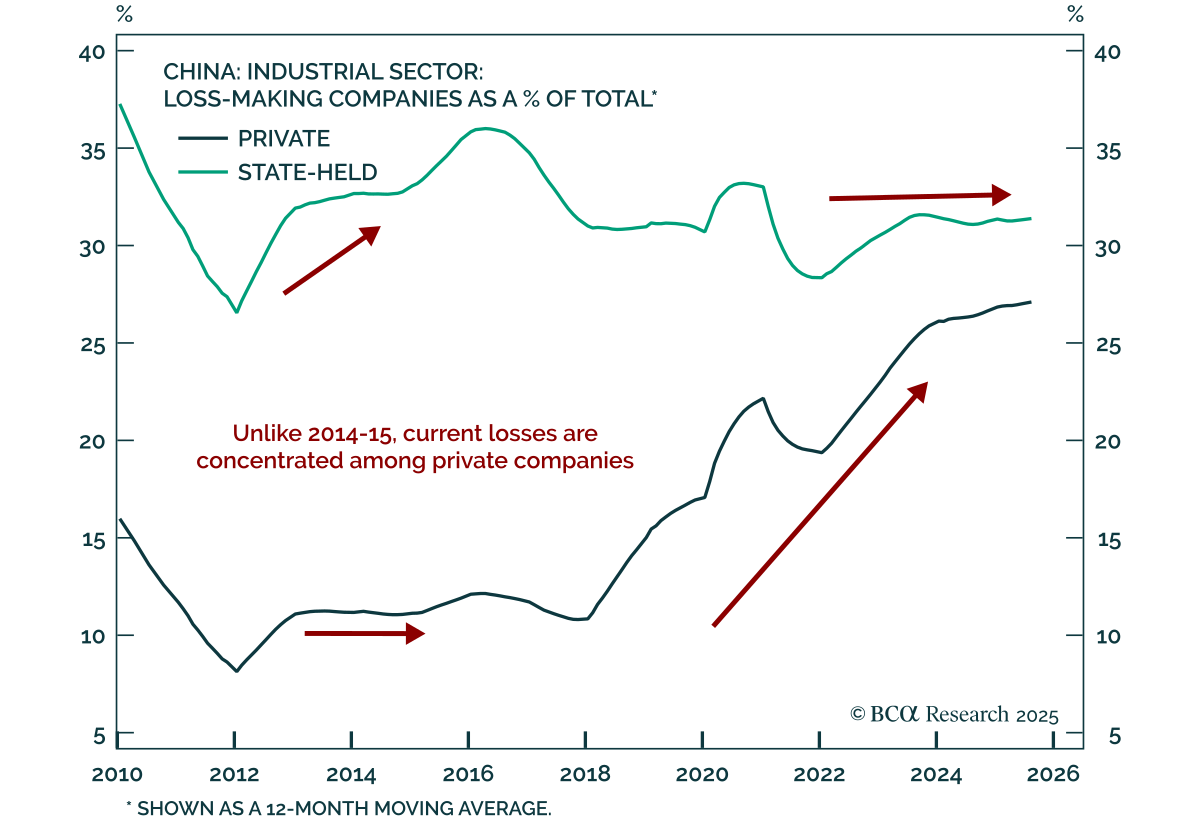

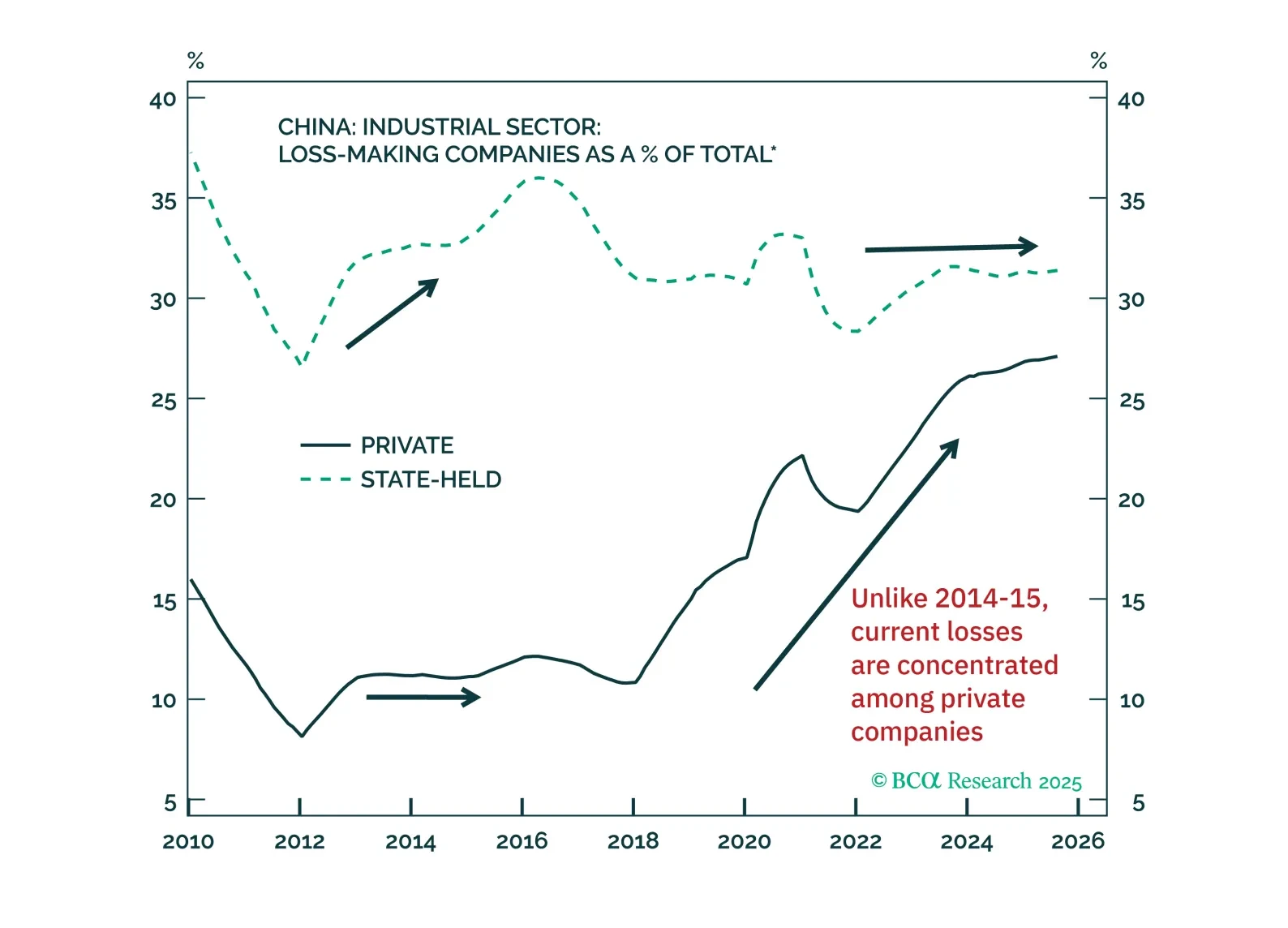

China's anti-involution policies will not end deflation or boost corporate profits on a sustainable basis. Authorities will be reluctant to cut industrial capacity as doing so would lead to layoffs. Consequently, production will continue to exceed demand, and price deflation will persist.

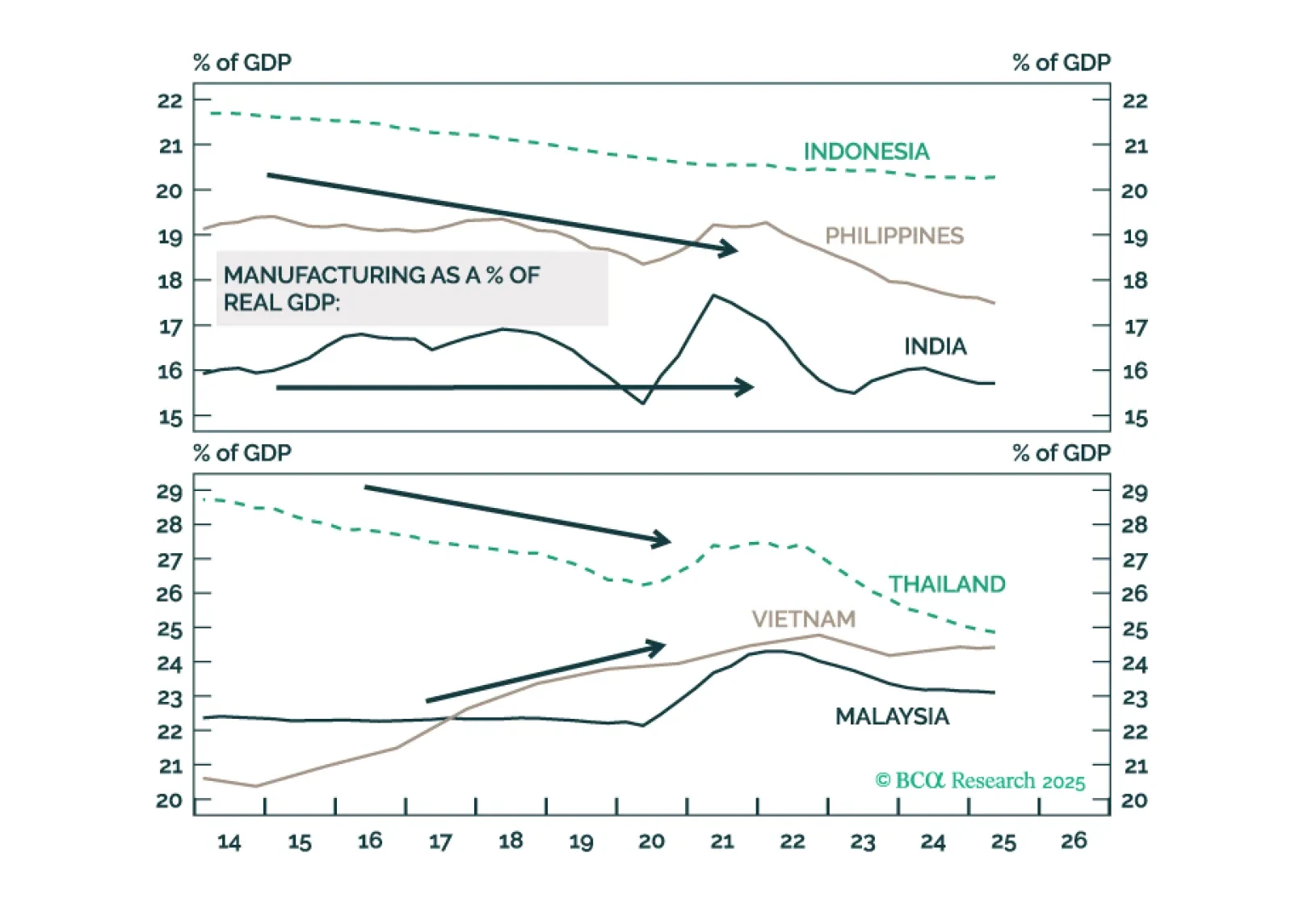

Investors should not count on buoyant growth in the ASEAN and Indian economies because of manufacturing relocation away from China in the next couple of years.

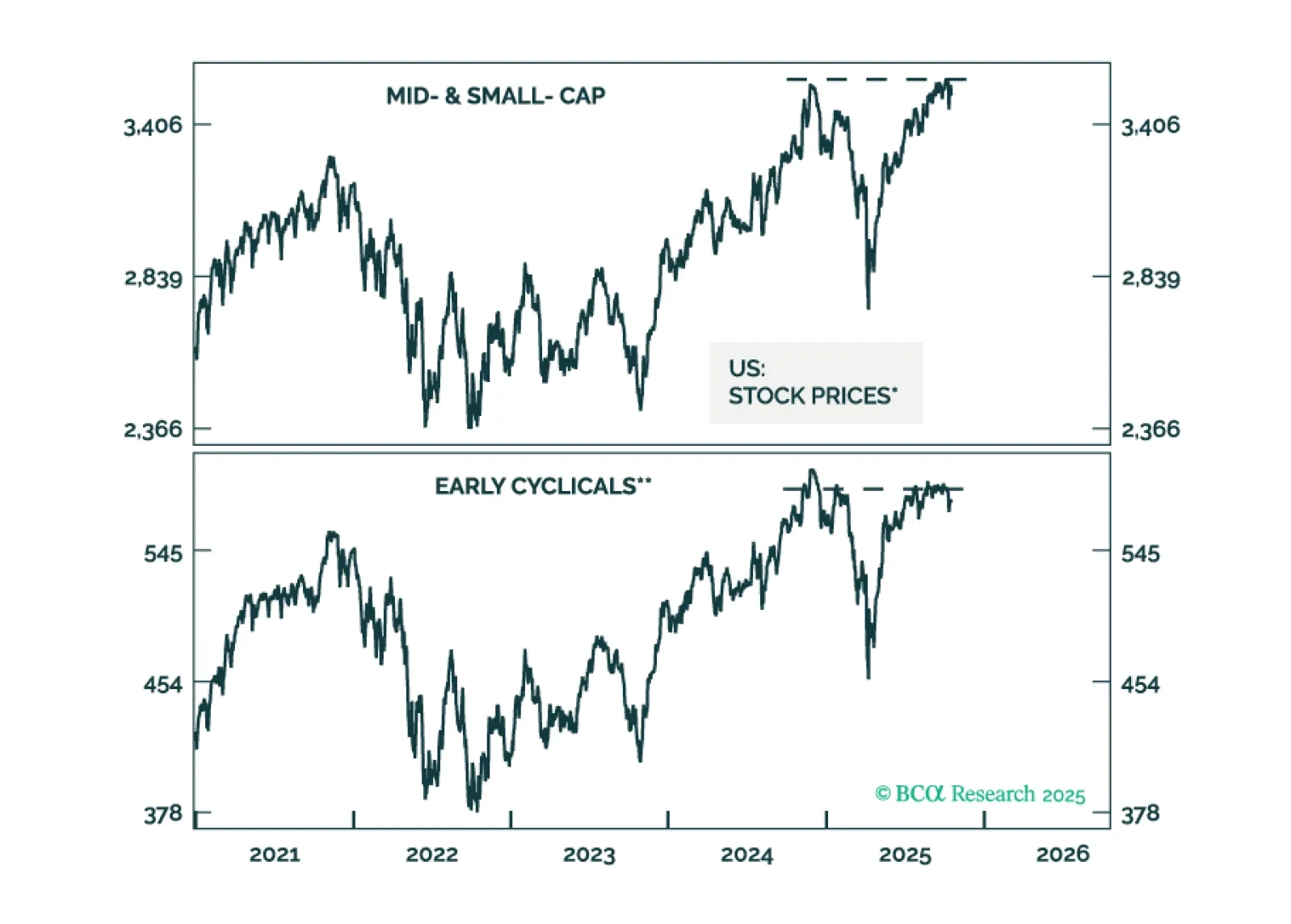

In global markets, speculative forces have intertwined with the sound fundamentals of specific equity segments, perplexing investors. This report aims to distinguish between excessive price run-ups and healthy fundamentals.

Our Portfolio Allocation Summary for October 2025.

Chilean equities are undergoing a structural re-rating. A political swing back to a pro-business administration, a benign macro backdrop, and a resilient exchange rate will drive Chilean markets’ outperformance versus EM peers.