Emerging Markets

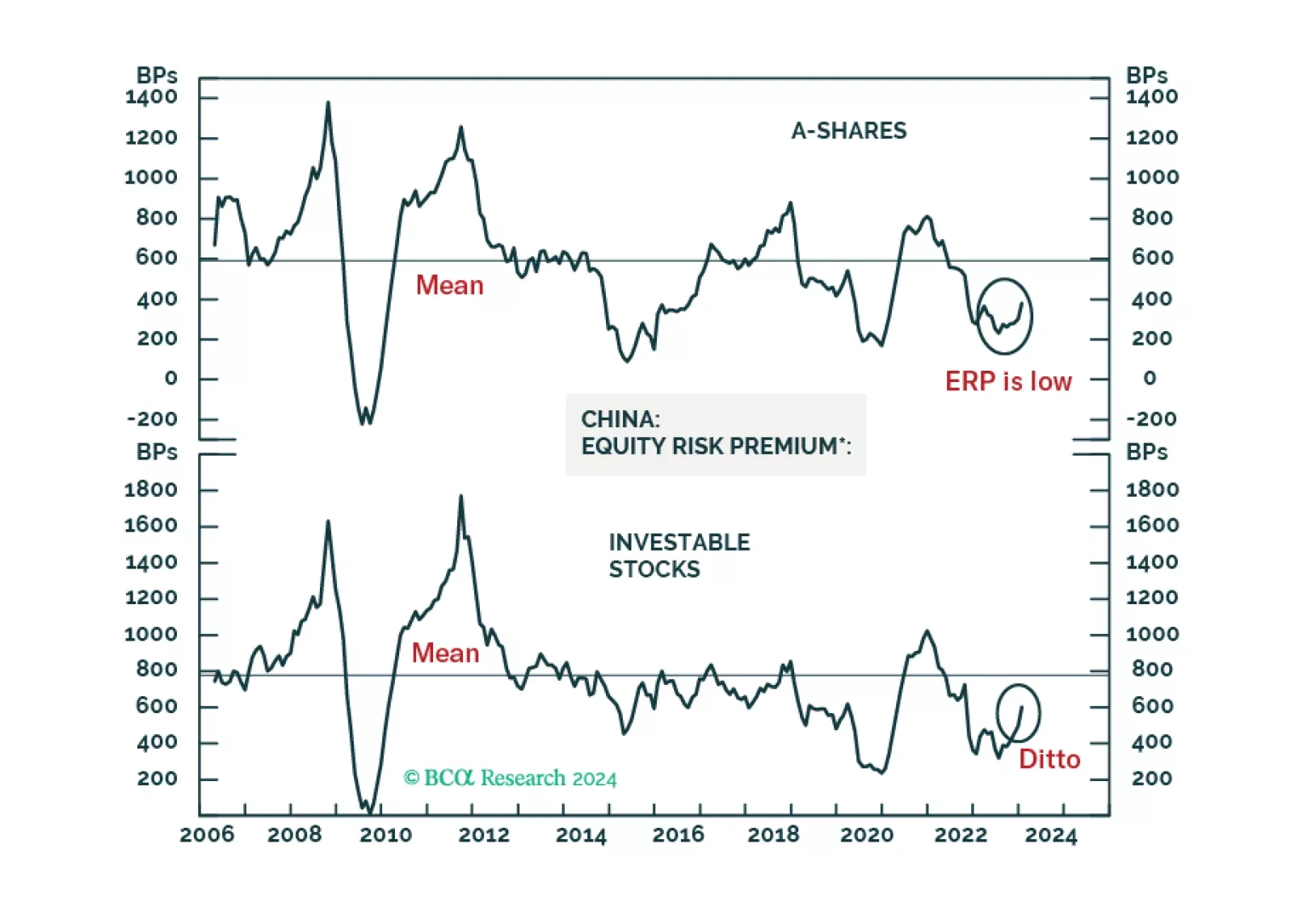

Chinese A-shares will probably begin forming a volatile bottom. The basis is that authorities will likely throw the kitchen sink at the onshore market in an attempt to stabilize share prices. The same is not true for offshore listed stocks. Hong Kong-traded Chinese share prices will likely continue to fall. Beijing is less concerned with offshore stocks as their holders are primarily foreign investors.

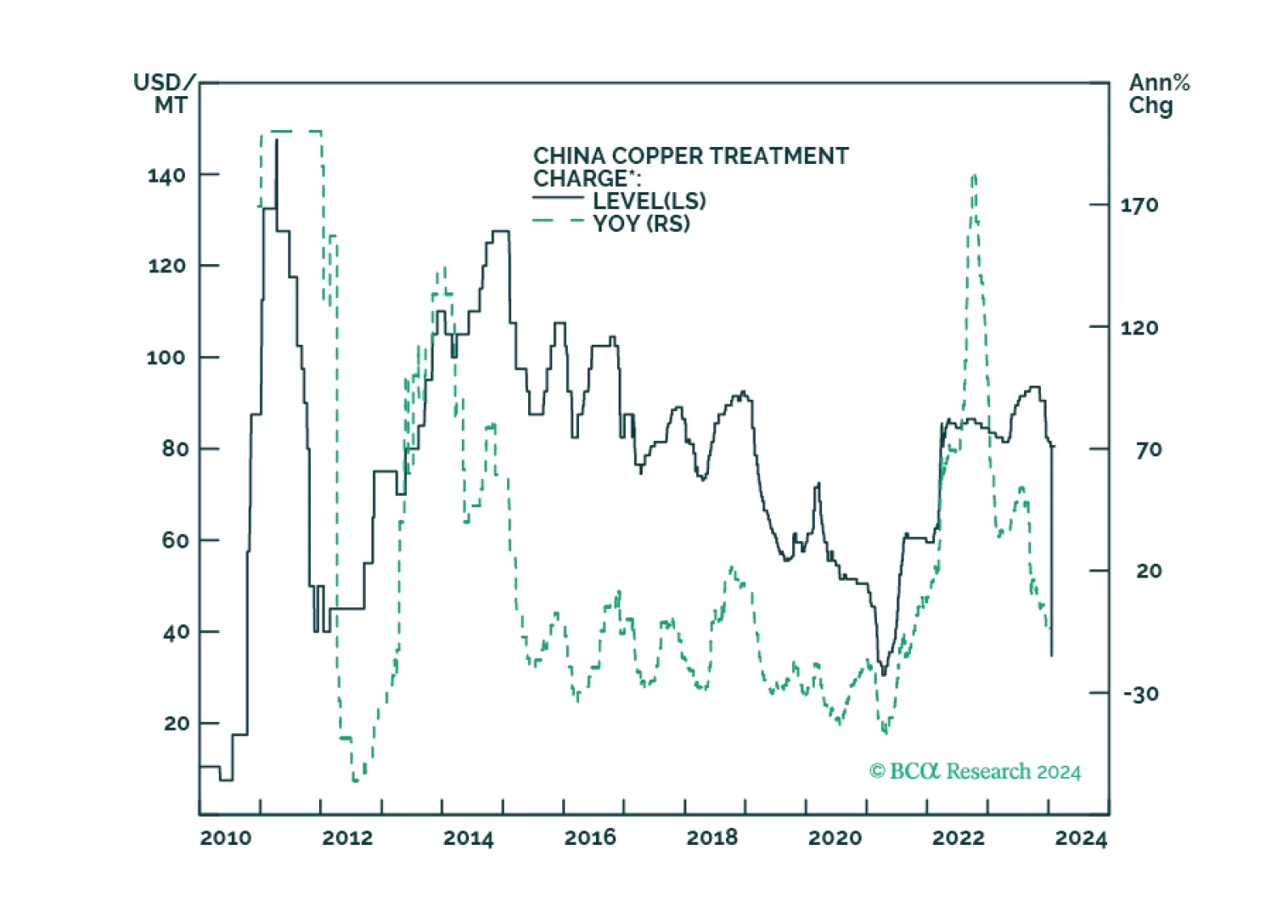

Supply and demand shocks in markets critical to the renewable-energy and defense industries will continue to play havoc with prices, which will negatively impact capex. In the short run, this benefits China given its already-dominant position in these markets. Longer term, investors already are providing capital for long-term projects needed for the energy transition. We remain long the XME ETF, given its low exposure to lithium and nickel holdings.

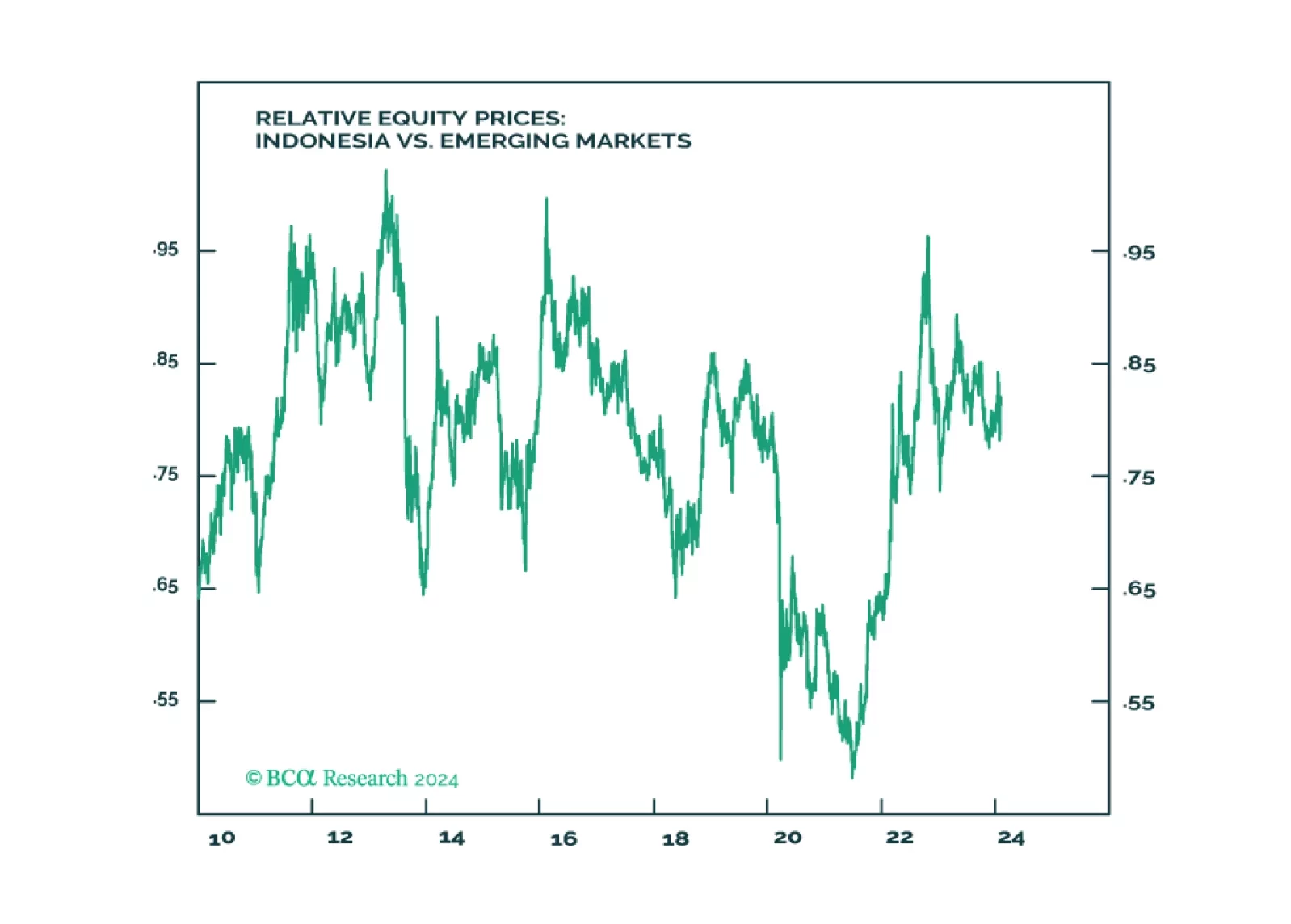

Indonesia will not revert to dictatorship. Yet the guardrails against authoritarianism are also constraining the actions of the next government in tackling near term domestic and regional challenges. For long-term positioning, use potential selloff from a “dictatorship scare” to build position as structural outlook for Indonesia is positive due to the China-West divorce and the global energy transition.