Emerging Markets

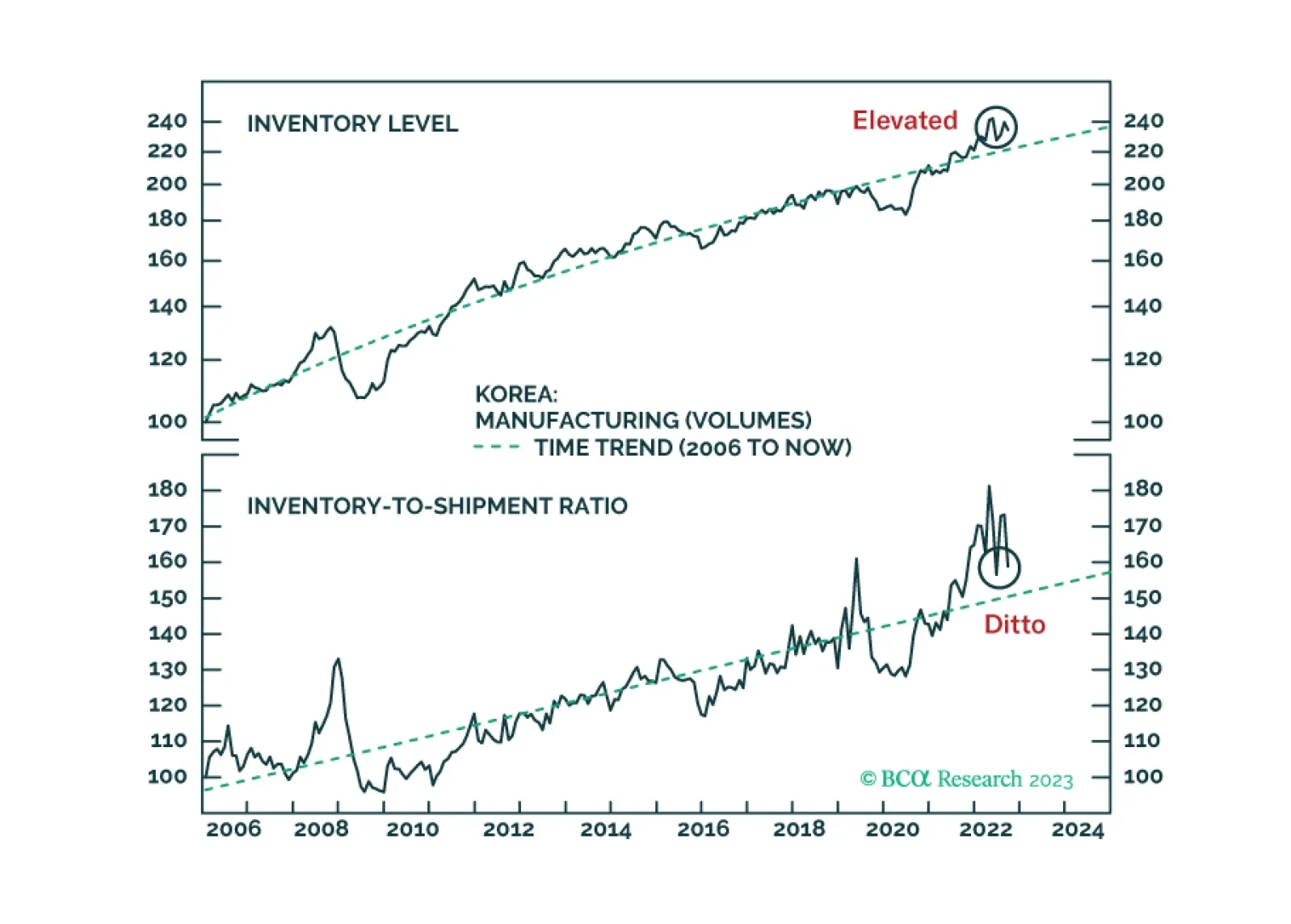

Contrary to the prevalent belief in the global investment community, goods/merchandise inventories in the US and East Asia are rather elevated. Financial markets respond to final demand fluctuations, not inventory restocking. Global manufacturing/trade will continue contracting, even though the pace of contraction might moderate in the near run. We recommend that investors fade the current rally.

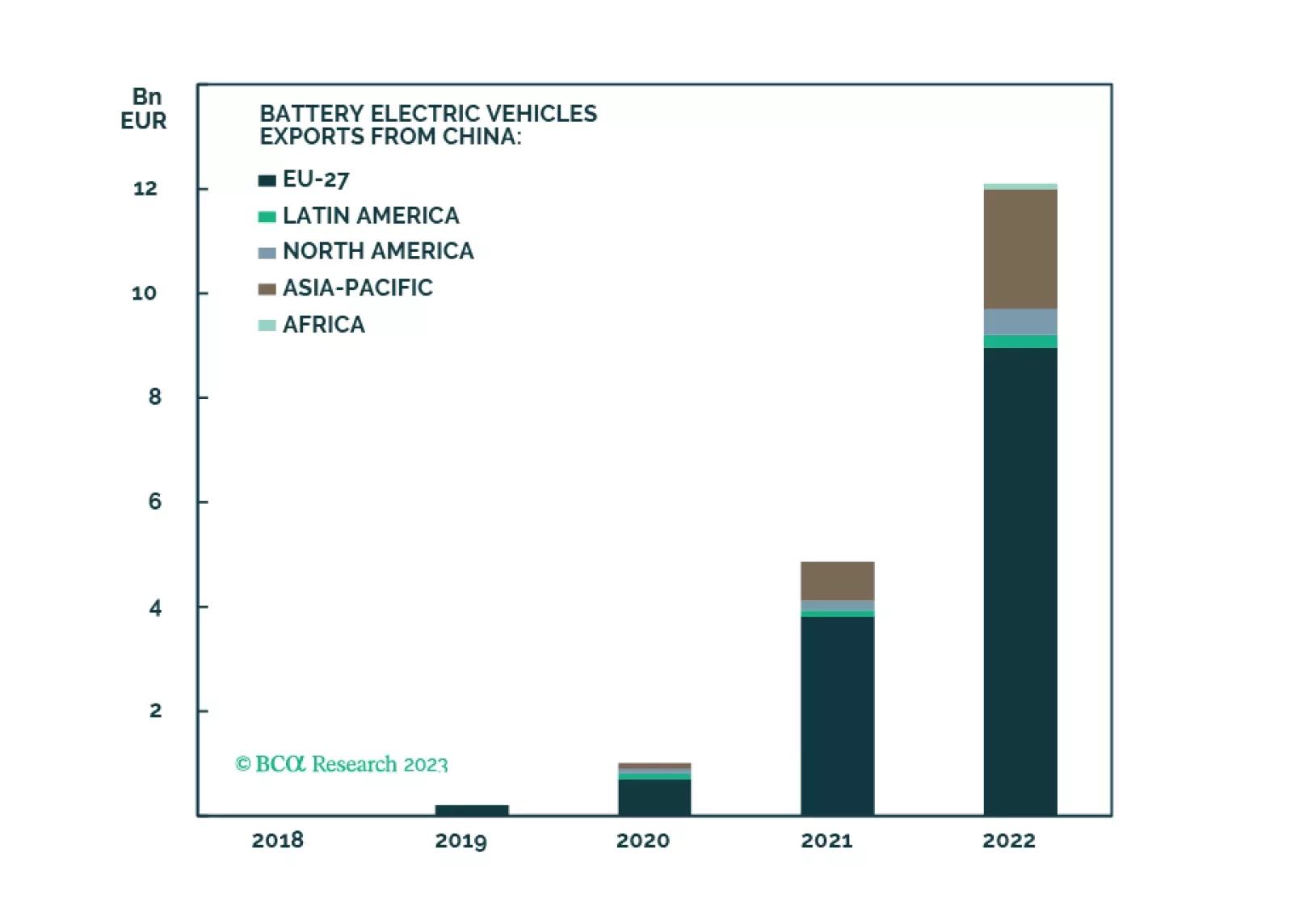

China’s push to dramatically expand its copper-refining capacity will be complemented by further vertical integration of mining assets. However, surplus refining capacity will push treatment and refining charges lower in the short run. The threat of EU tariffs on Chinese EV imports looms large, and could be costly to China’s expansion of its already-dominant supply-chain ecosystem for EVs and metals refining. We remain long the XME and COMT ETFs to retain exposure to metals miners and refiners.

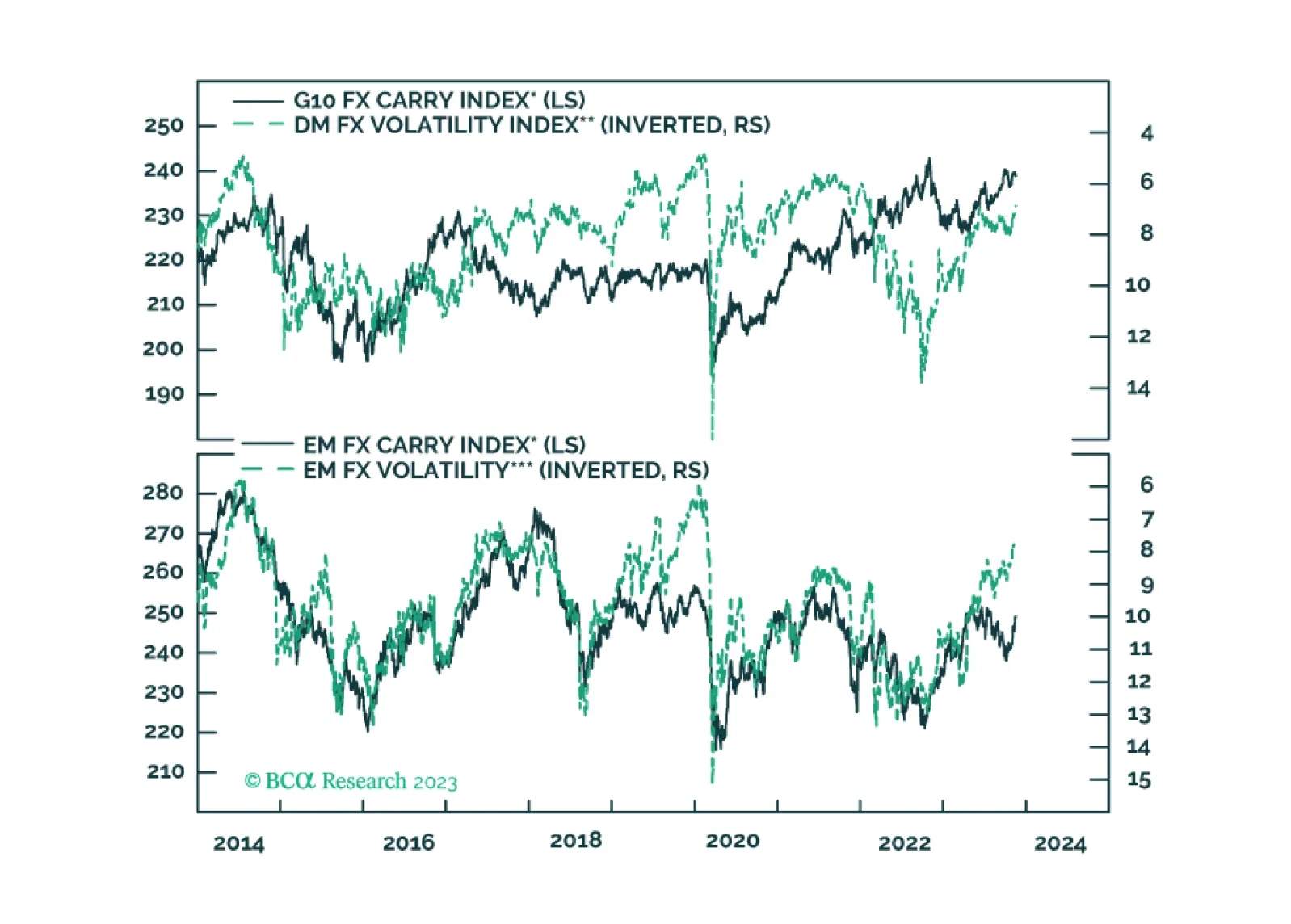

In this report, we evaluate the risk to carry trades in the coming months.

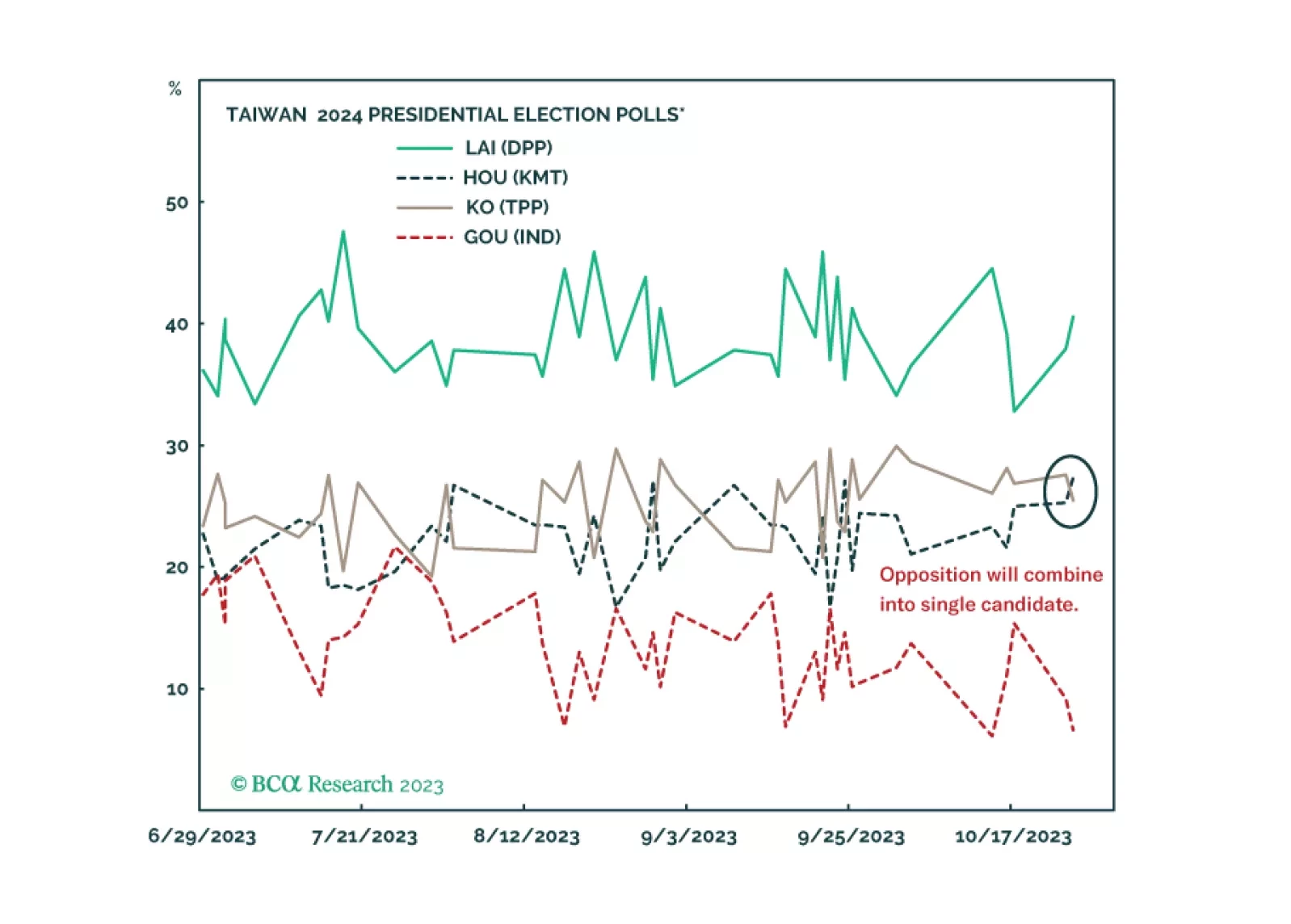

Investors should not get their hopes up about the Biden-Xi summit. Wait to see if a new ruling party is elected in Taiwan before downgrading geopolitical risk in the Taiwan Strait. US-China strategic détente is possible but neither the geopolitics nor the macro backdrop warrant a risk-on position next year.