Emerging Markets

Economic fragmentation will accelerate in the wake of the Israel-Hamas and Russia-Ukraine wars. China’s fis-cal support for its economy; a still-strong US economy, and the preparation for a wider war in the Middle East involving Iran will elevate volatility and bias oil prices upward. We remain long equity and commodity exposure via the XOP, XME and COMT ETFs.

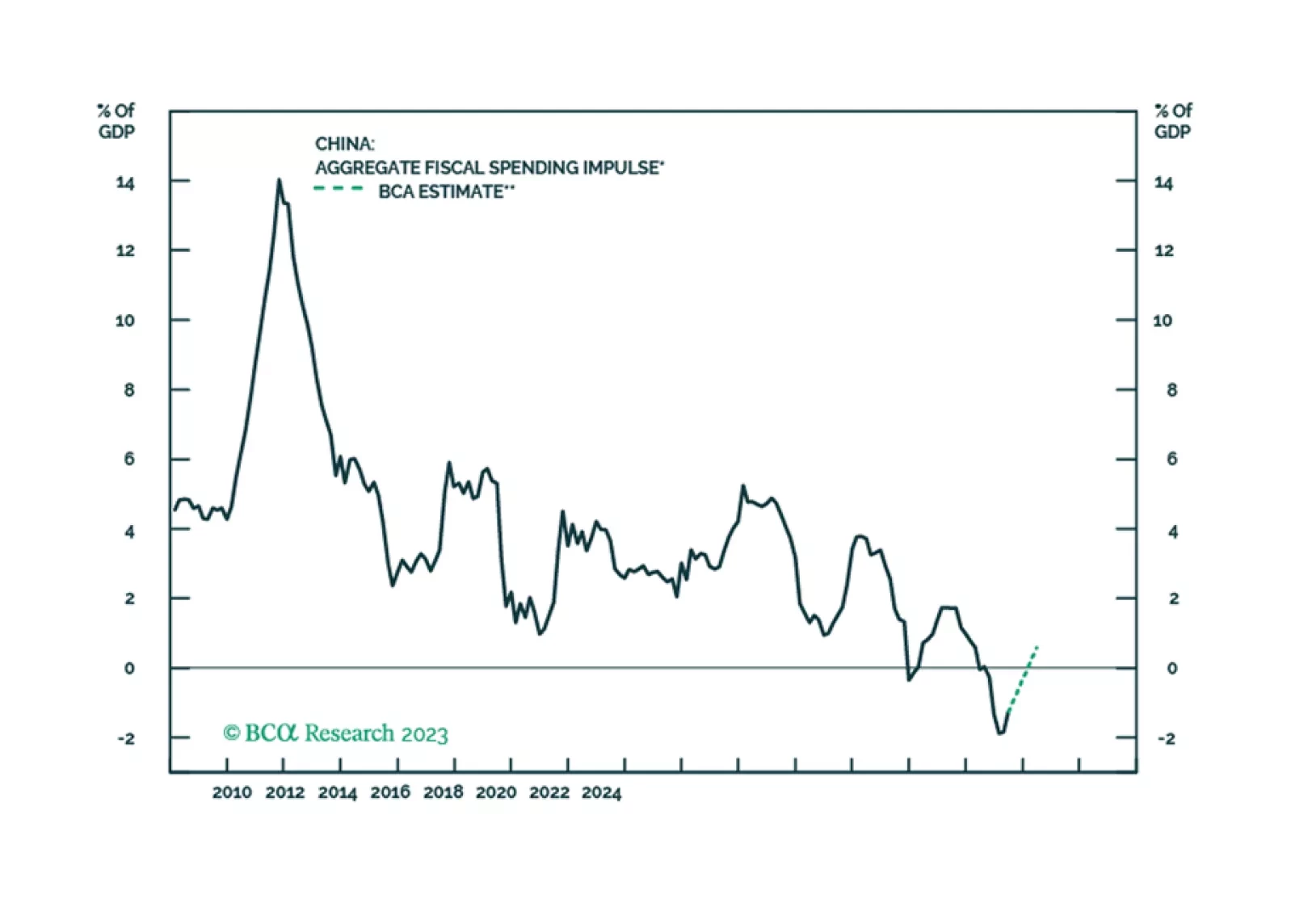

We maintain our view that China’s economic growth in the coming months will remain lackluster. Beijing's recent measures to provide additional financing may help to bridge the gap in government spending in the rest of 2023 and into 2024, but the impact on growth will be very limited.

Stronger US growth elicits a response from the House Republicans. But a government shutdown is not devastating to the economy. What is more devastating would be a crisis in the Middle East, Europe, and Asia. Stay long US defense, energy, and large caps stocks.

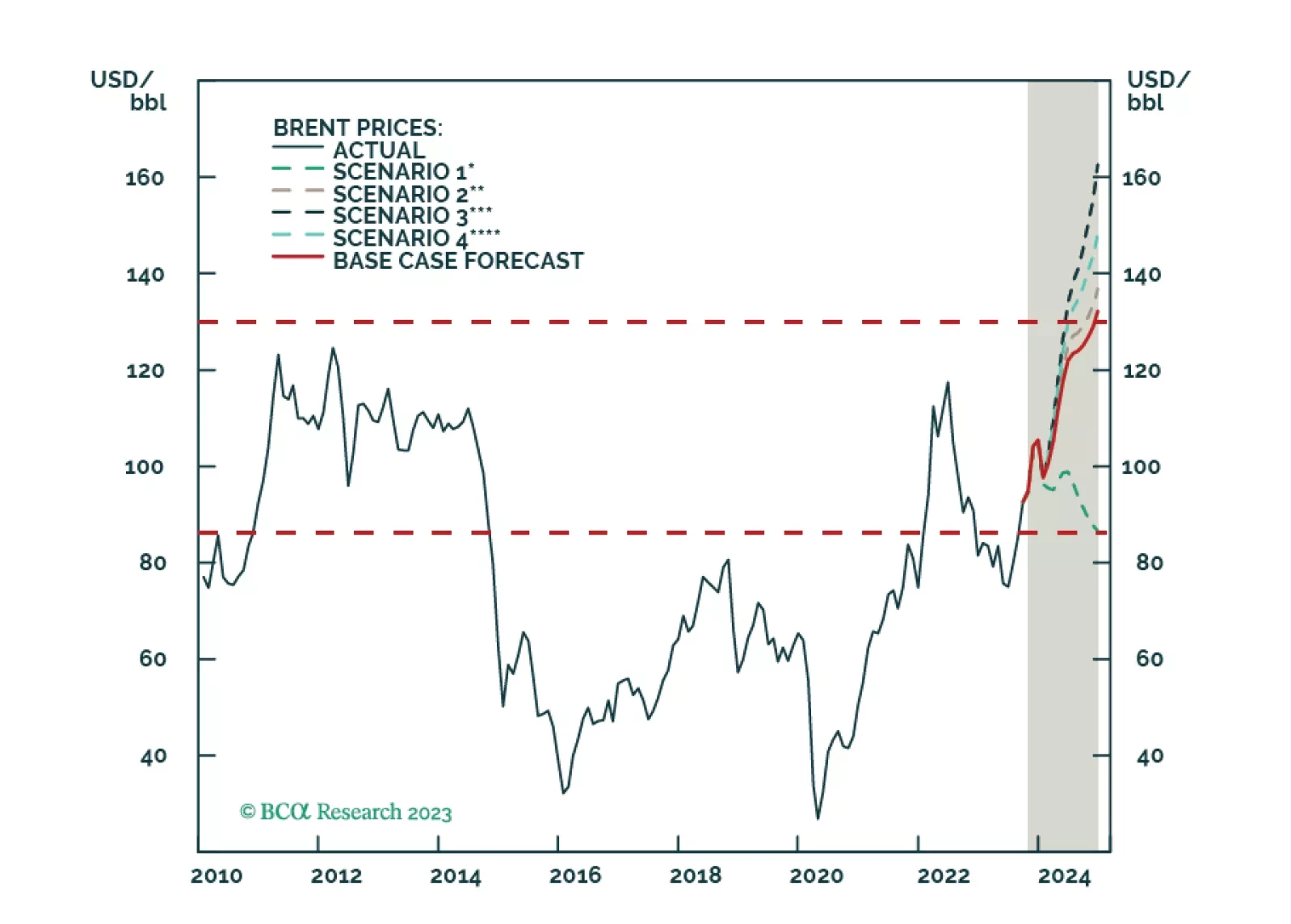

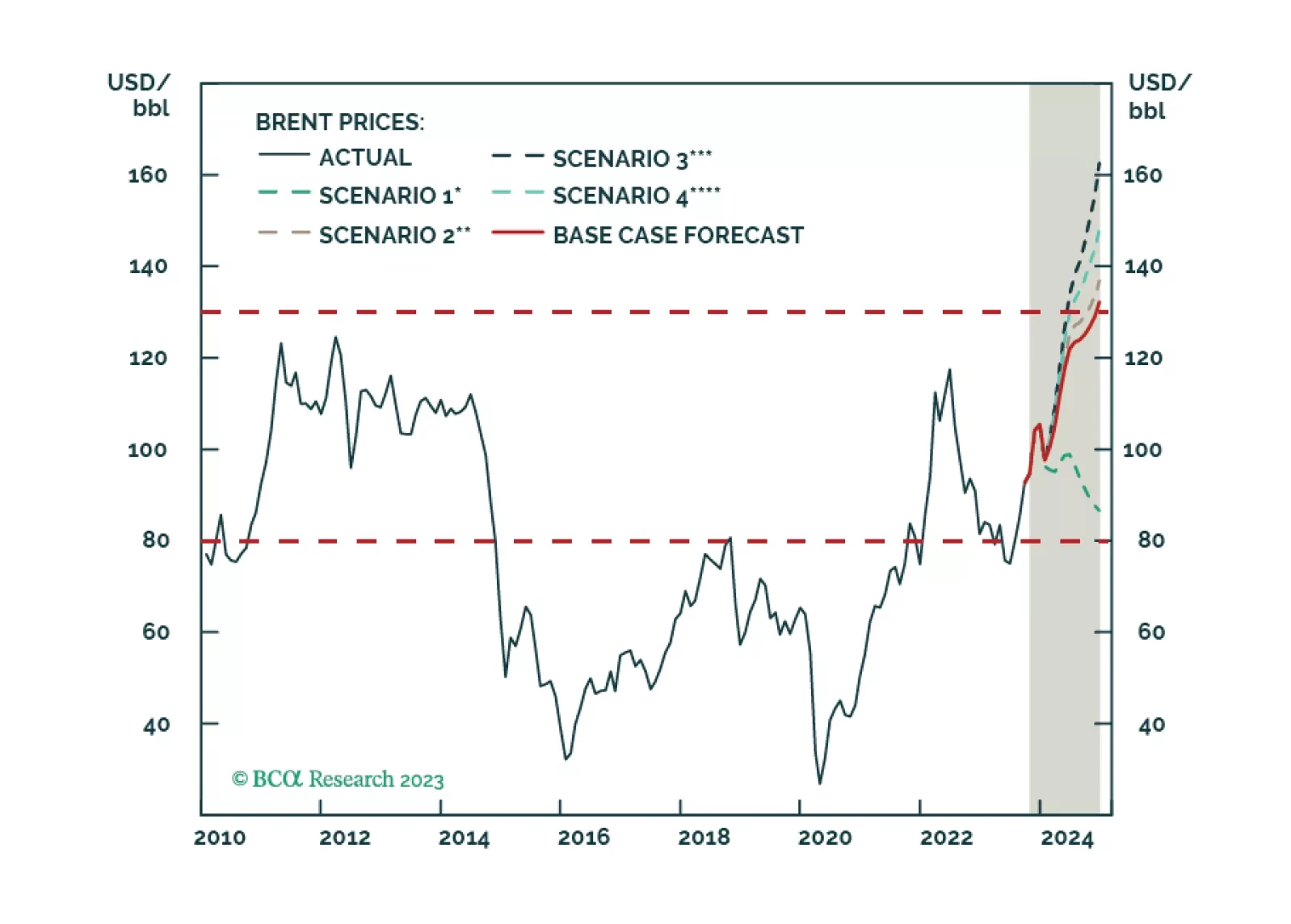

The US and core OPEC 2.0 are – wittingly or not – laying the groundwork for a price band with a floor and cap on oil prices – at $79/bbl and $130/bbl, respectively – “at least” to May 2024. This accommodates multiple goals for both. To meaningfully support policy, the US would need to scale up purchases to refill its SPR. We remain long the XOP and COMT ETFs for direct exposure to energy E+P equities and commodities.