Emerging Markets

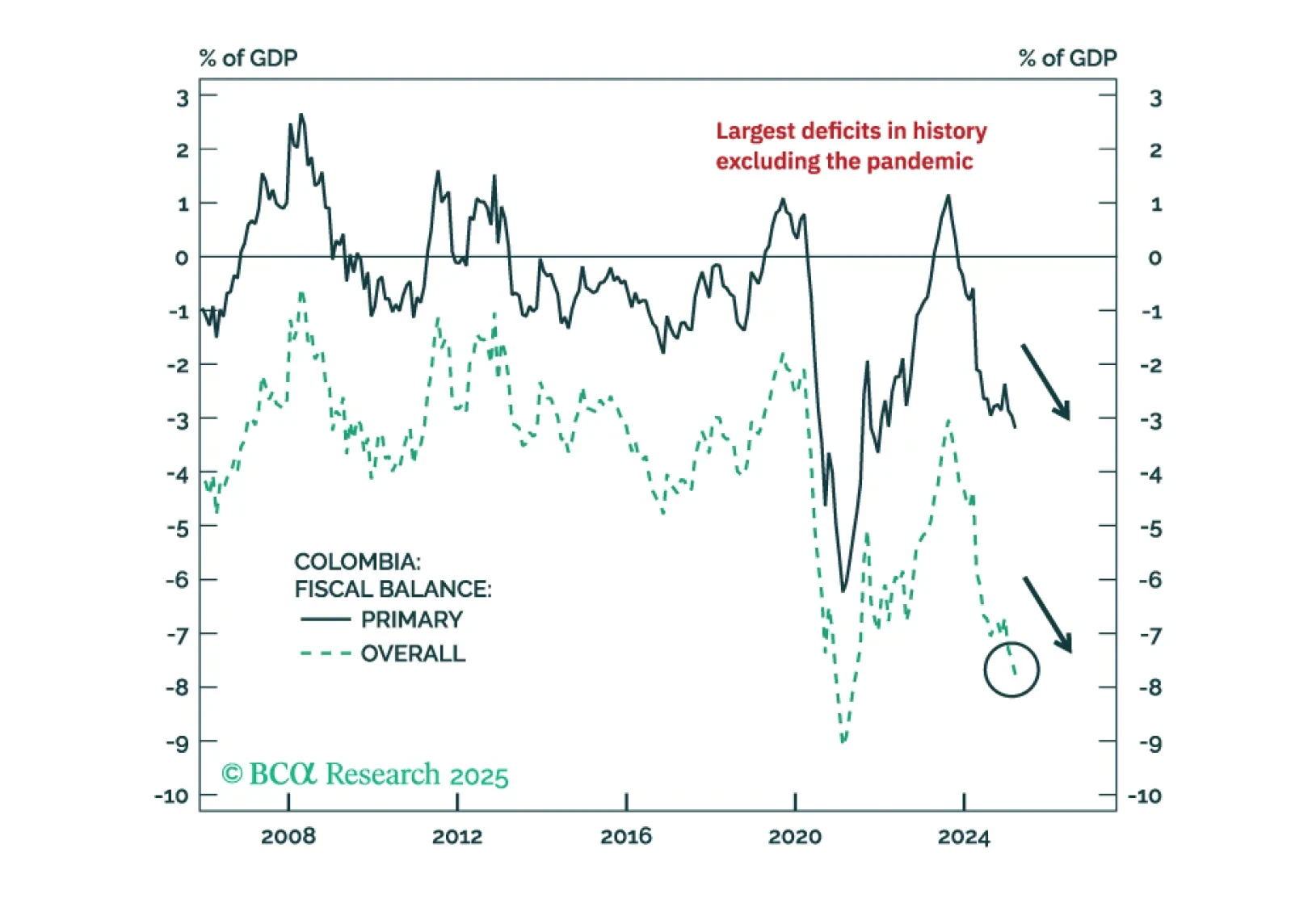

Colombian markets will be torn between expectations of future orthodox policies and the reality of a worsening macro backdrop in the next 12 months. To balance risks, we are upgrading Colombian equities, local bonds, and sovereign credit from underweight to neutral versus their respective EM benchmarks.

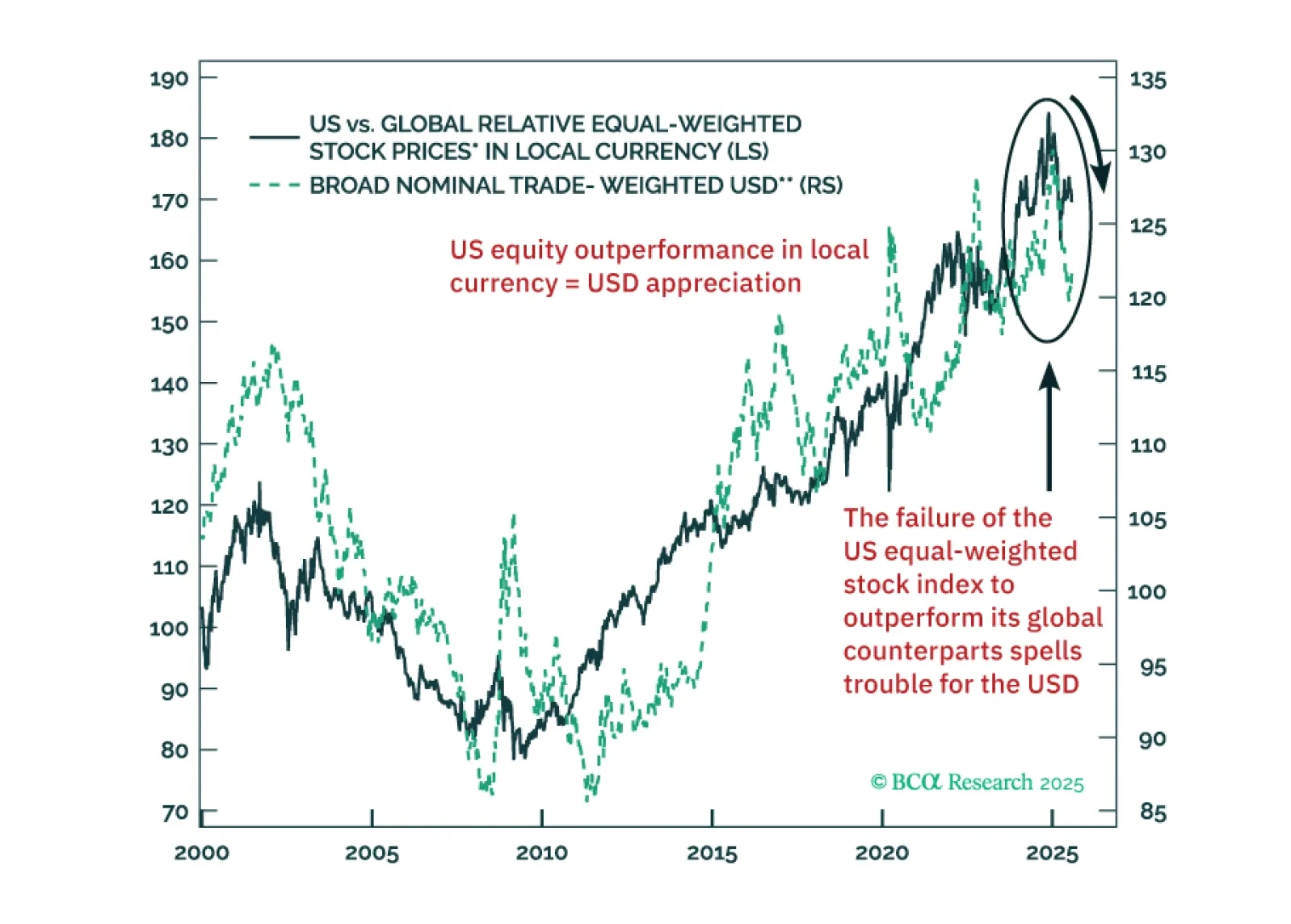

US TMT stocks have been delivering miraculous profit performance. Yet, outside US large tech, global equity fundamentals and technicals are troublesome. A near-term USD rebound should be faded.

Our Portfolio Allocation Summary for August 2025.

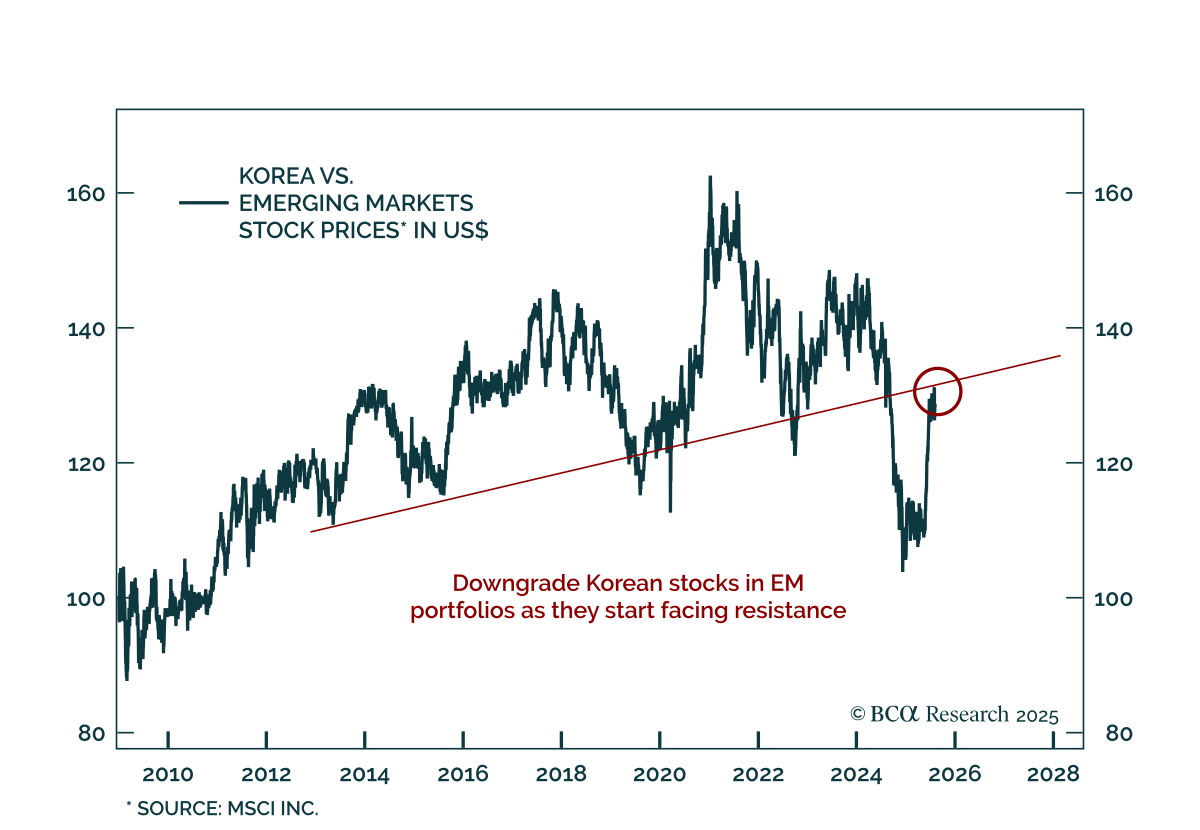

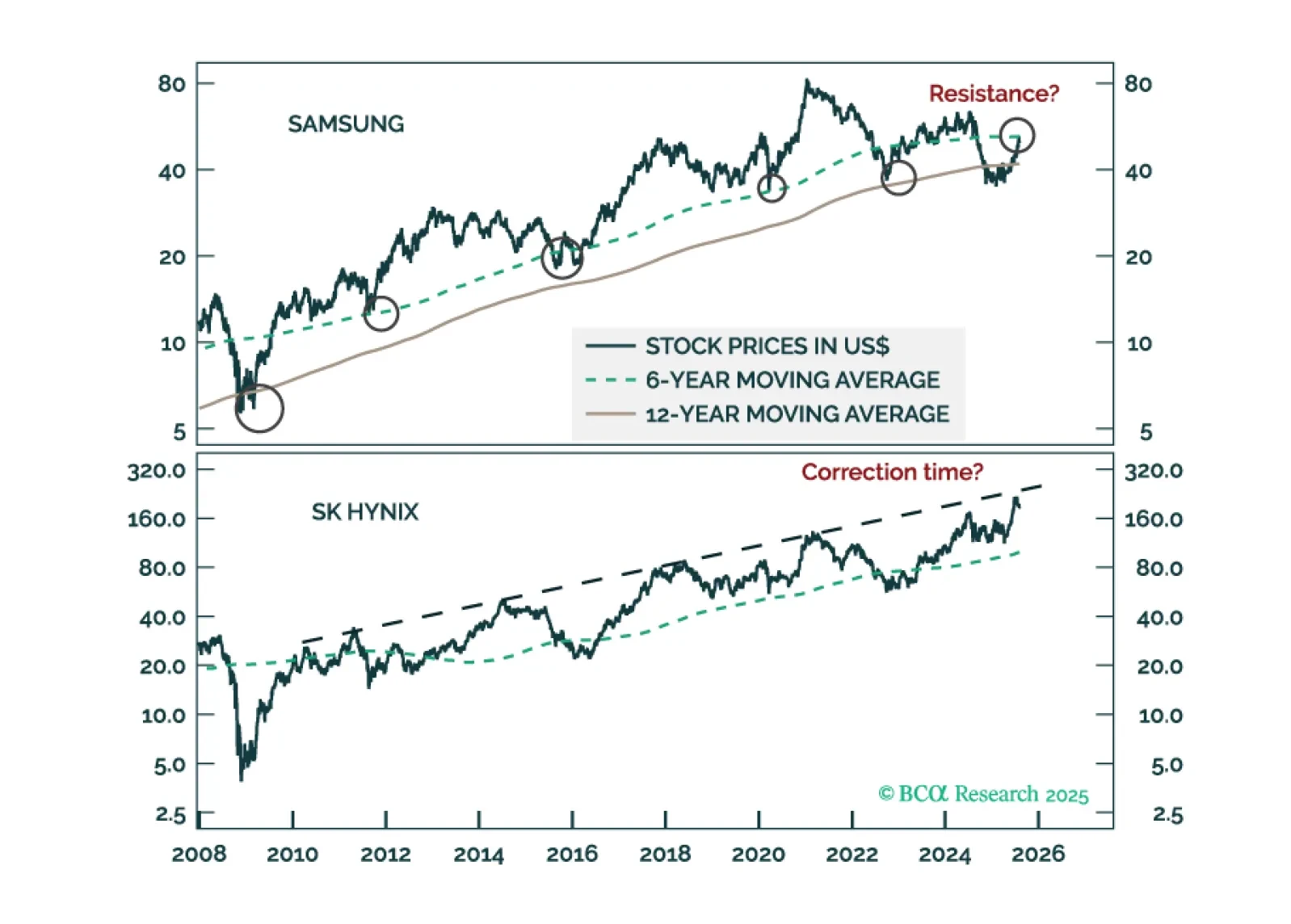

A deflationary shock from shrinking exports will ripple throughout the Korean economy. We are downgrading the KOSPI from overweight to neutral and reiterating a long position in 10-year domestic bonds, currency unhedged.

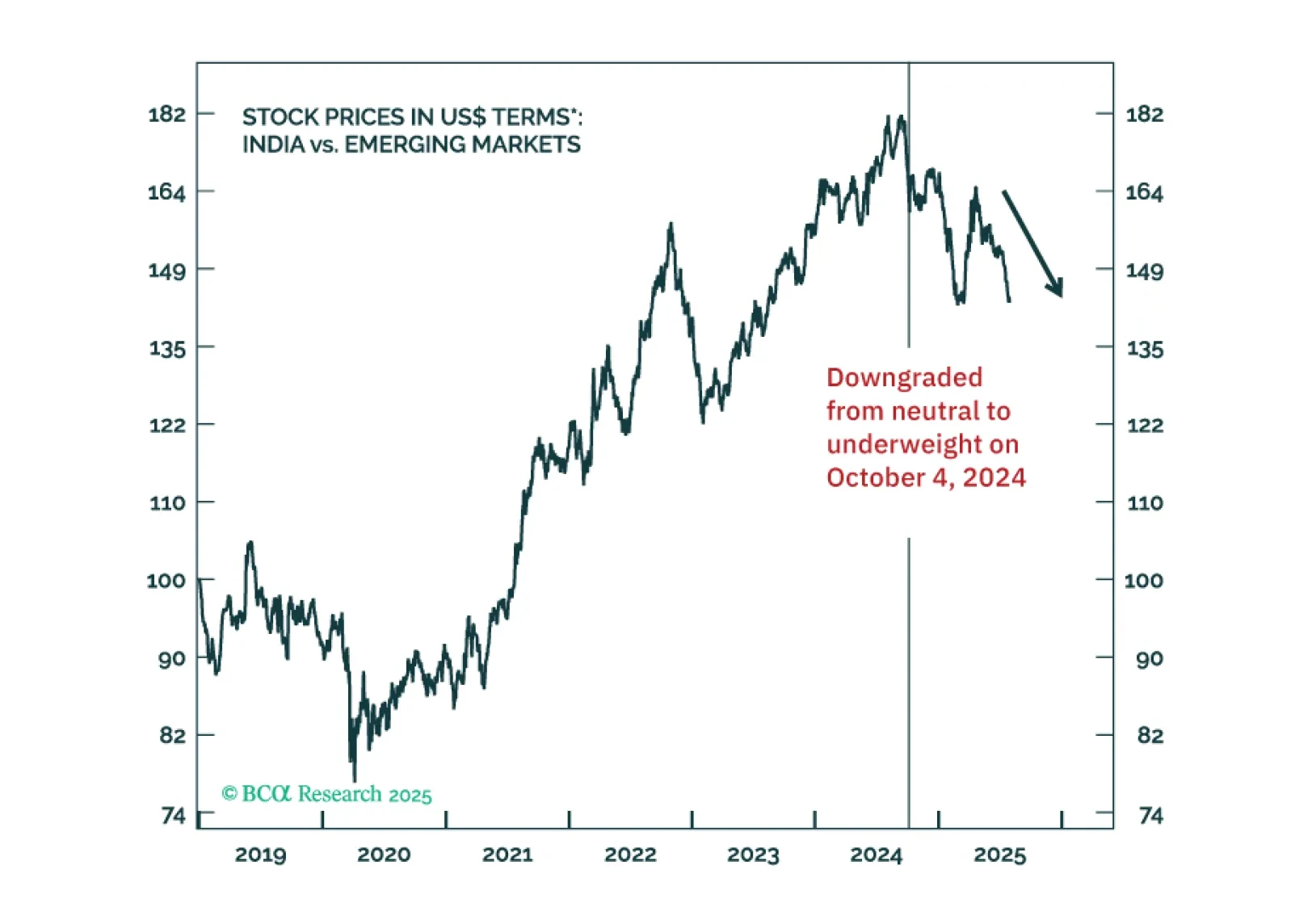

A high US tariff and the lingering uncertainties on the US-India trade deal will hurt investors sentiment. This and contracting corporate profits will push share prices lower. Stay underweight Indian stocks.

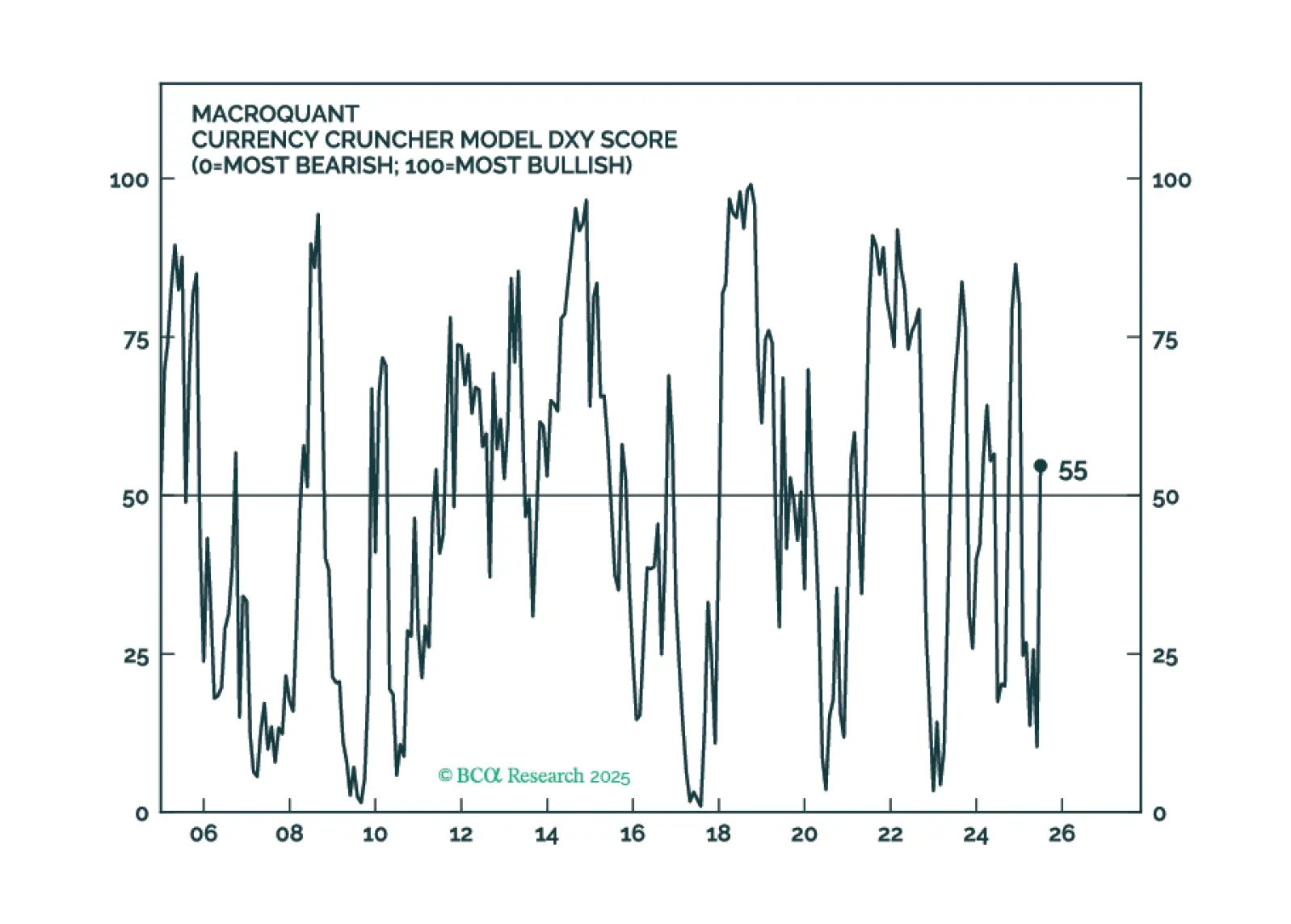

MacroQuant is recommending that equity investors keep their finger near the eject button but avoid pressing it for now. The model is warming up to the dollar again and sees scope for oil prices to rise.

Thanks to the tight monetary and fiscal policies so far, inflation and growth are heading lower in Turkey. Buy 2-year local currency bonds, currency unhedged. Also, upgrade Turkey's domestic bonds from neutral to overweight and stocks from underweight to neutral within their respective EM portfolios.