Emerging Markets

Investor sentiment on China and EM has become bullish. Meanwhile, the reflation plays have begun fraying on the edges. Cracks always appear first in the most sensitive reflation plays and then spread to the core. The narratives of the Fed's imminent pivot and China's recovery will be questioned in the coming months. Thus, China/EM assets and related plays will sell off, and the US dollar will rebound.

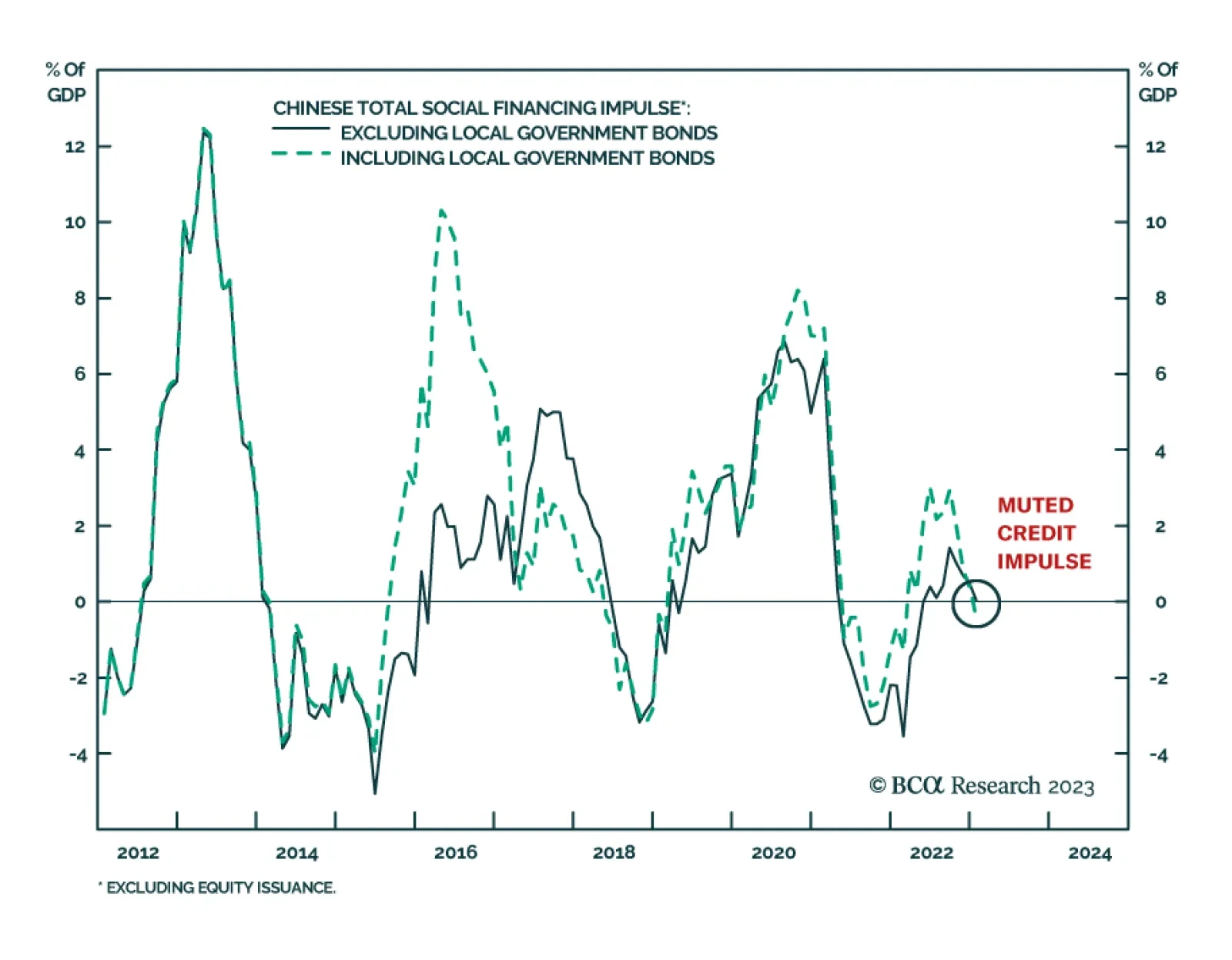

Two developments this week reinforce our key views for 2023. First, Russia’s threat to reduce oil production by 500,000 barrels per day, while escalating the war in Ukraine, confirms that geopolitical risk will rebound and new oil supply shocks are likely. Second, China’s credit numbers for January confirm that the country is trying to stabilize the economy but also that stabilization will not come quickly. Moreover, stimulus does not resolve structural problems over the long run. We remain defensively positioned overall and underweight Chinese assets.

The tempo of China’s and the US’s military operations is picking up sharply. The risk of a sudden, perhaps unintended, escalation of military conflict, therefore, is rising in the South China Sea. So is the risk of another shooting war in the Middle East. Against this backdrop, China’s reopening, marginally stronger GDP growth, and massive fiscal stimulus to support renewables and defense is being rolled out. In states with high debt-to-GDP ratios like the EU and US, the risk of fiscal dominance is rising, and with it higher inflation. We remain long the XOP oil and gas ETF; the XME metals and mining ETF, and long the commodity COMT ETF to hedge this risk.

Copper prices are vulnerable to the downside in the coming months on a narrowing global supply-demand deficit. We expect that copper prices will plummet by 15-20% from the current level. However, the lingering structural supply deficit will put a floor under copper prices after this correction.

This week we present our Portfolio Allocation Summary for February 2023.

The risk-on rally is challenging our annual forecast so we are cutting some losses. But we still think central banks and geopolitics will combine to reverse the rally later this year.