Emerging Markets

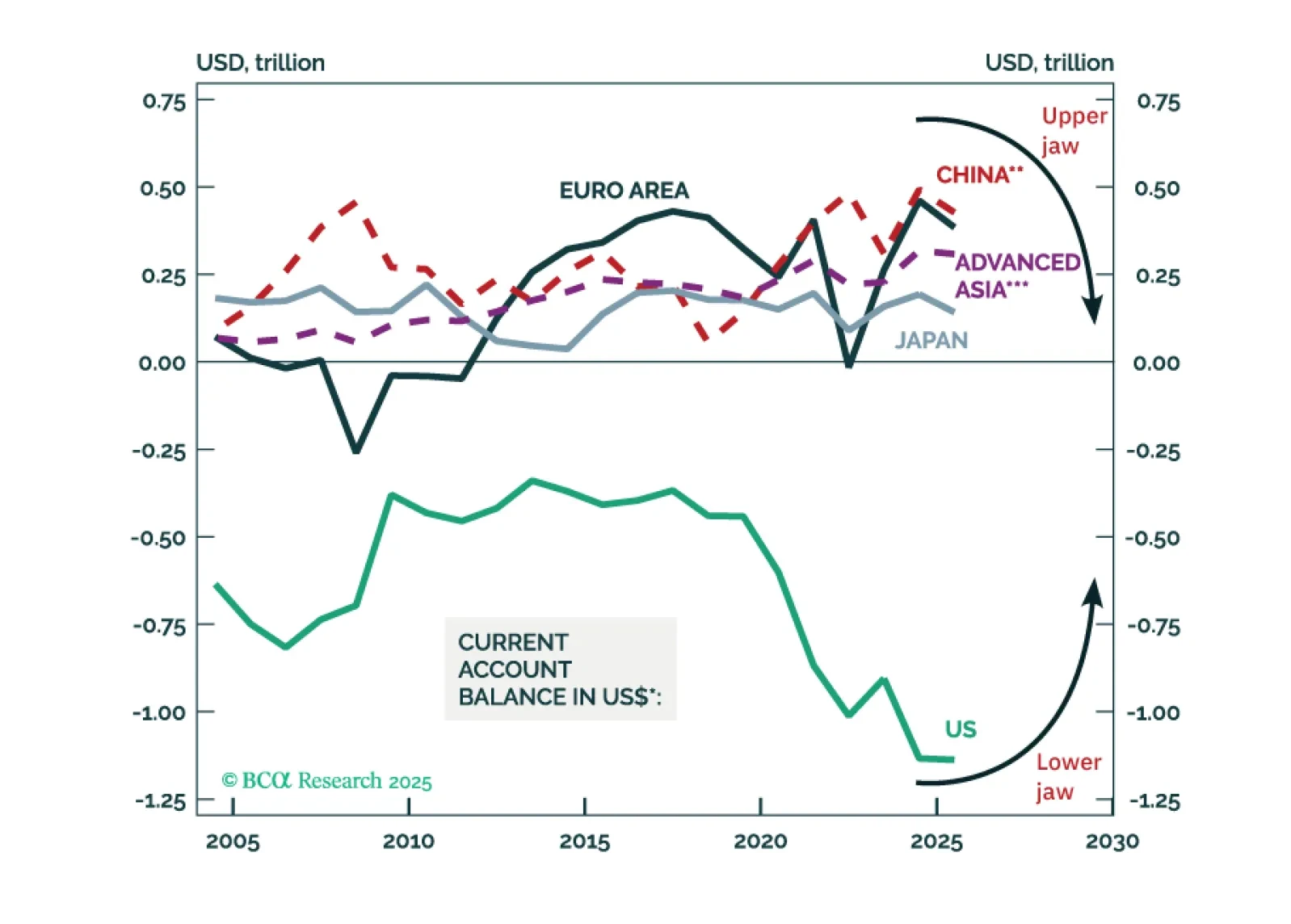

Alligator Bite #1: As US net portfolio inflows decline (the alligator's upper jaw closes), its current account deficit must narrow (the lower jaw will also shut). Alligator Bite #2: As the US current account deficit shrinks (the lower jaw closes), current account surpluses in the rest of the world will narrow (the upper jaw will come down).

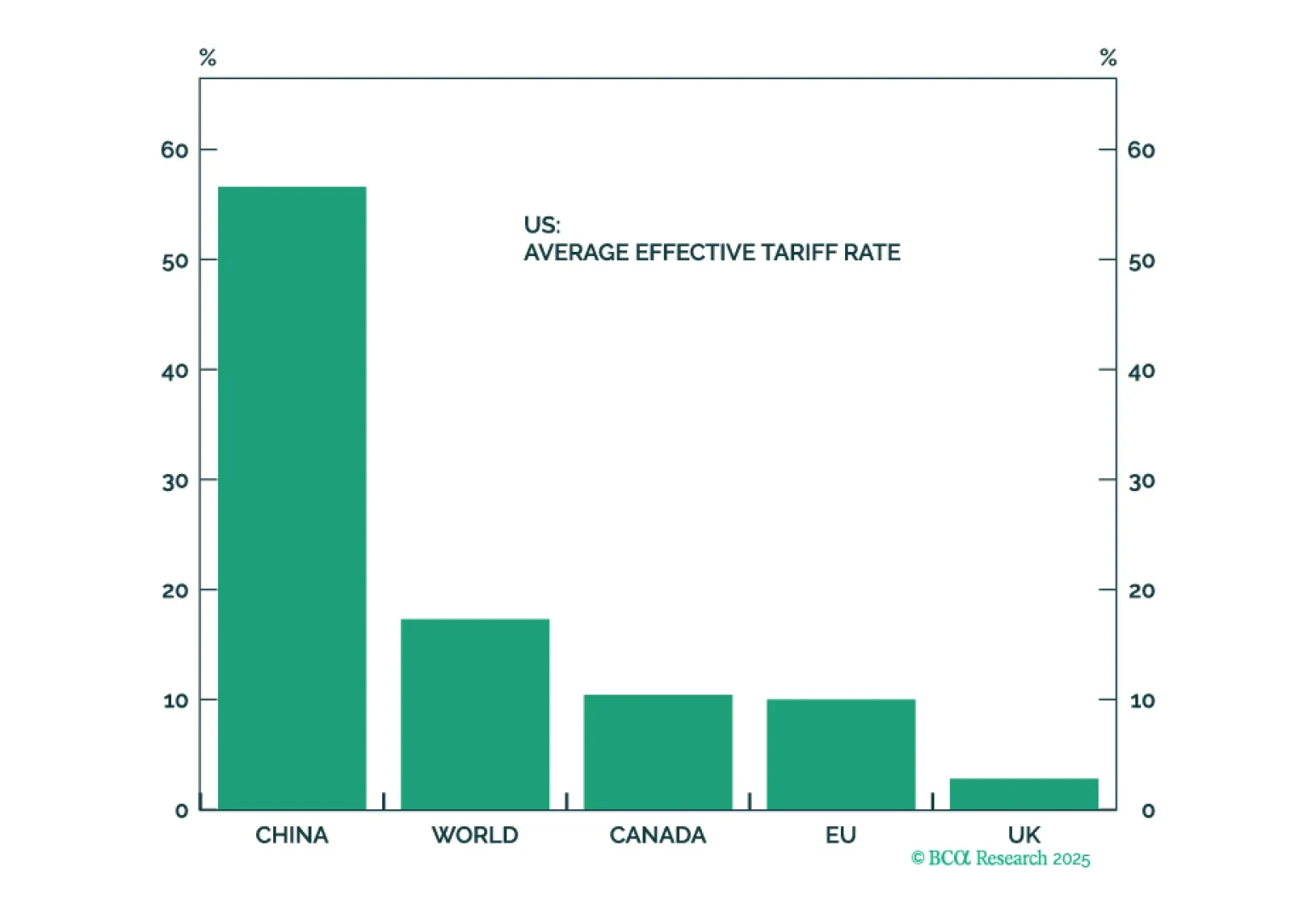

Acute geopolitical risks, like a massive oil shock, may be abating. But structural geopolitical risk remains high and could upset a blithe market. Cyclical economic risks are underrated as the US slows down and China continues to stumble. Investors should book some profits in anticipation of tariff implementation and a downturn in hard economic data.

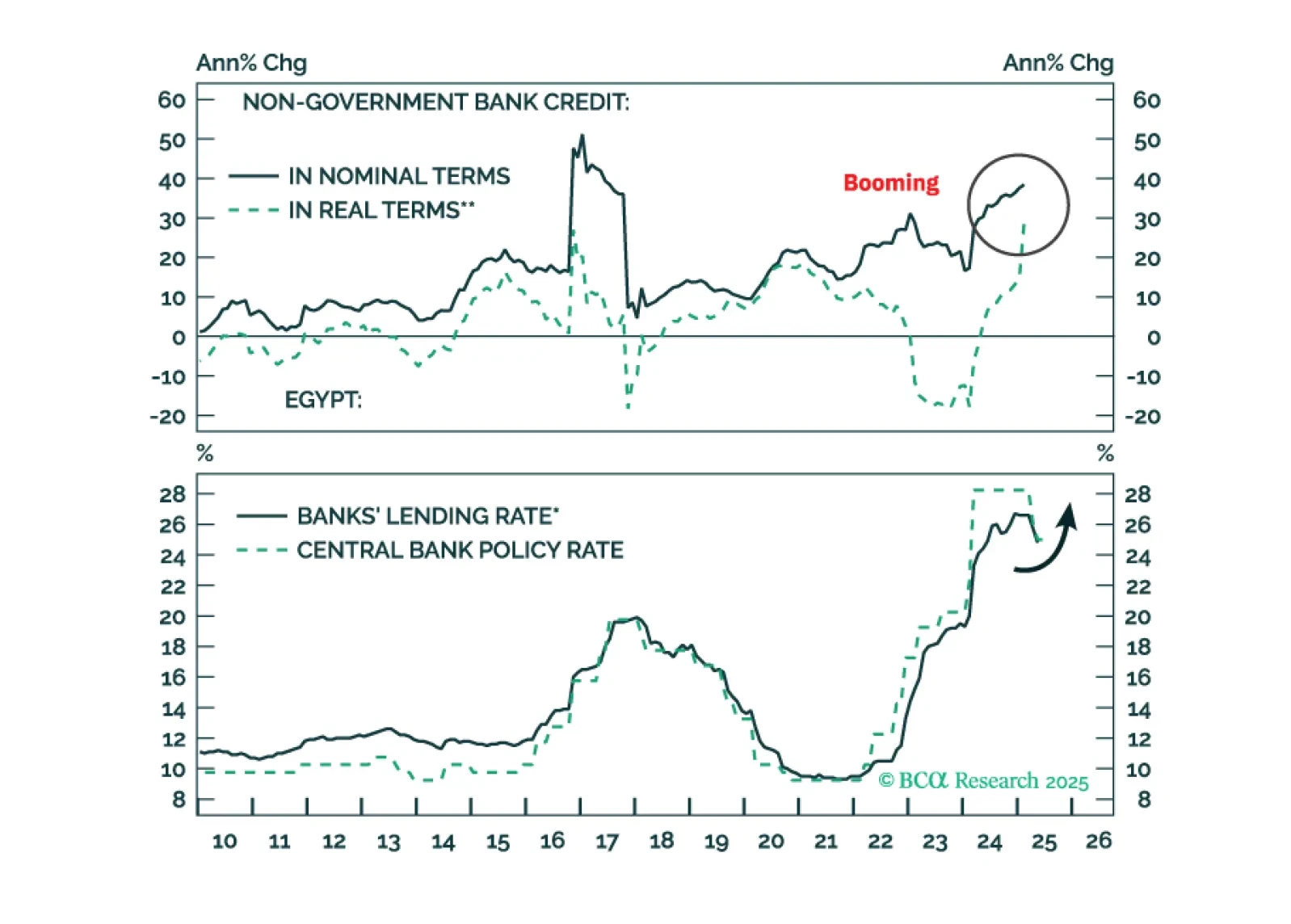

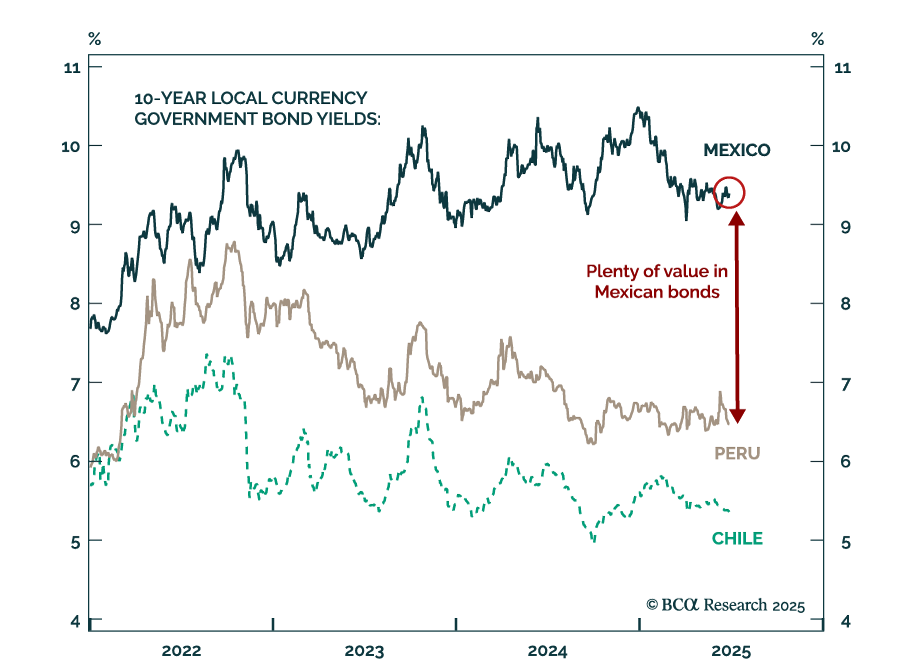

Downward pressure on the pound will rise in the coming months. Inflation will go up, so will bond yields. It’s time to book profits on Egyptian domestic bonds.

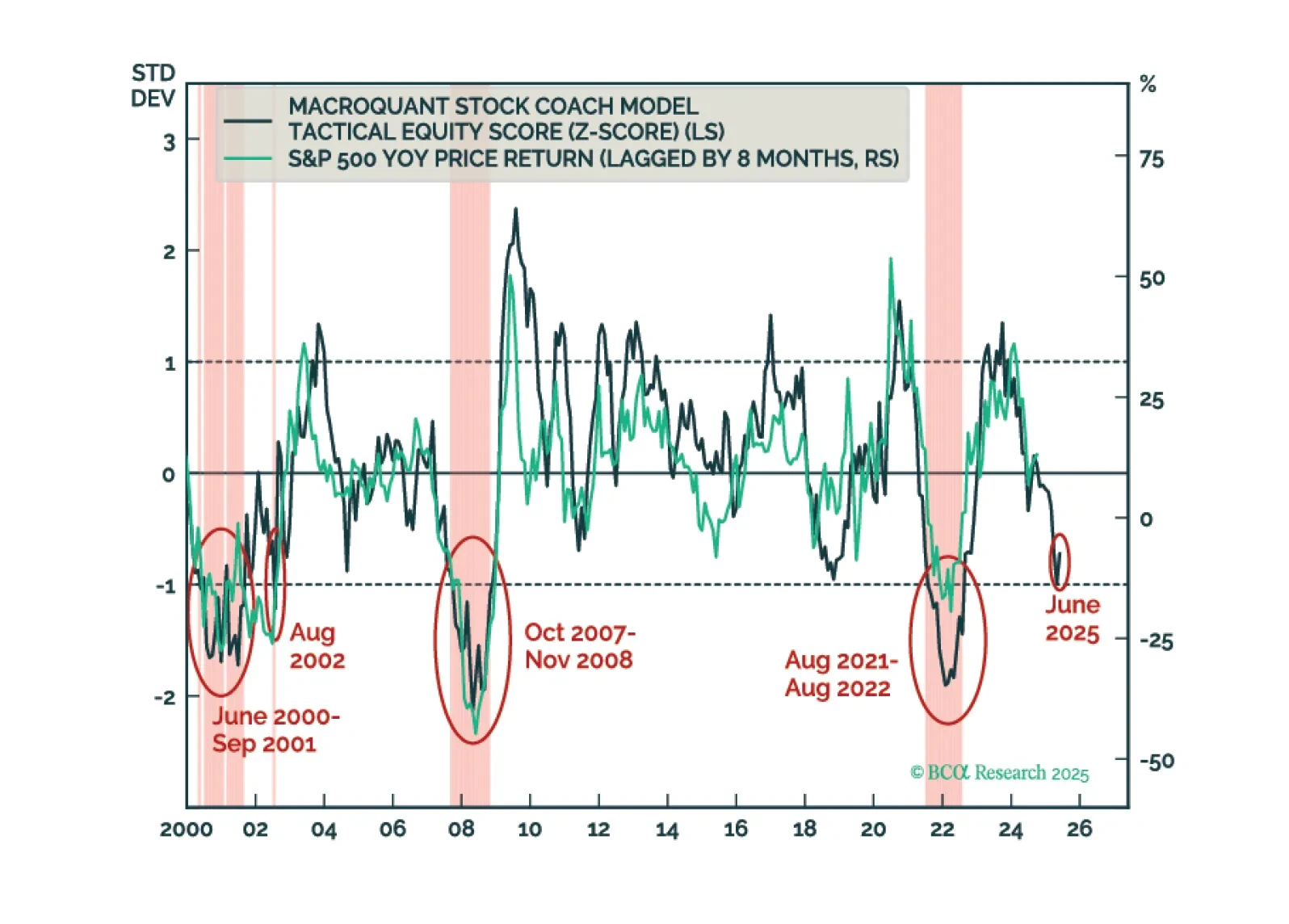

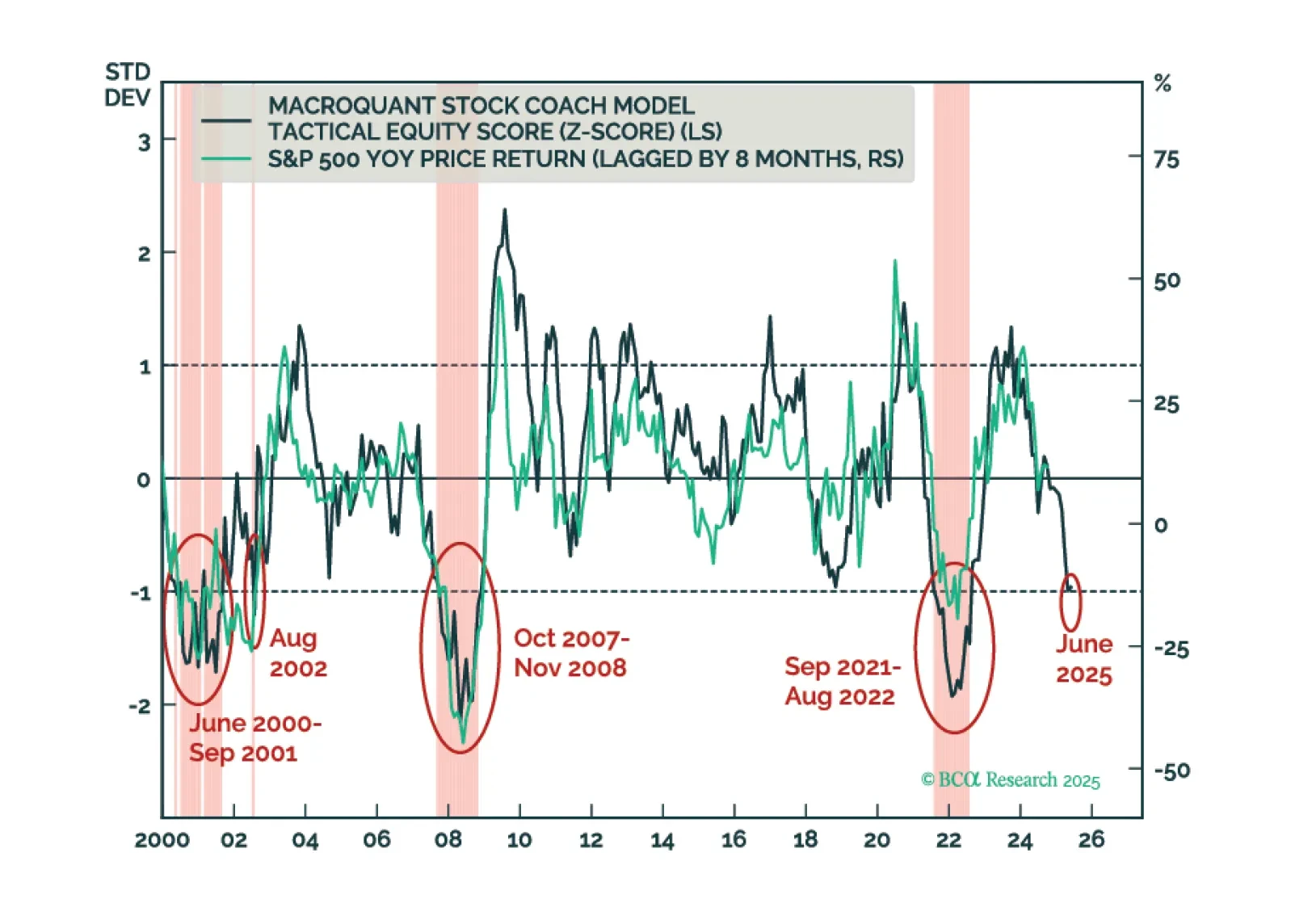

MacroQuant’s US equity z-score is dangerously close to the -1 threshold. Moves below that threshold have reliably coincided with equity bear markets in the past. As such, MacroQuant recommends an underweight on stocks, offset by an overweight on bonds and cash.

Investors should modestly underweight equities in their portfolios and look to turn more aggressively defensive once the whites of the recession’s eyes are visible. We think that will happen within the next few months.

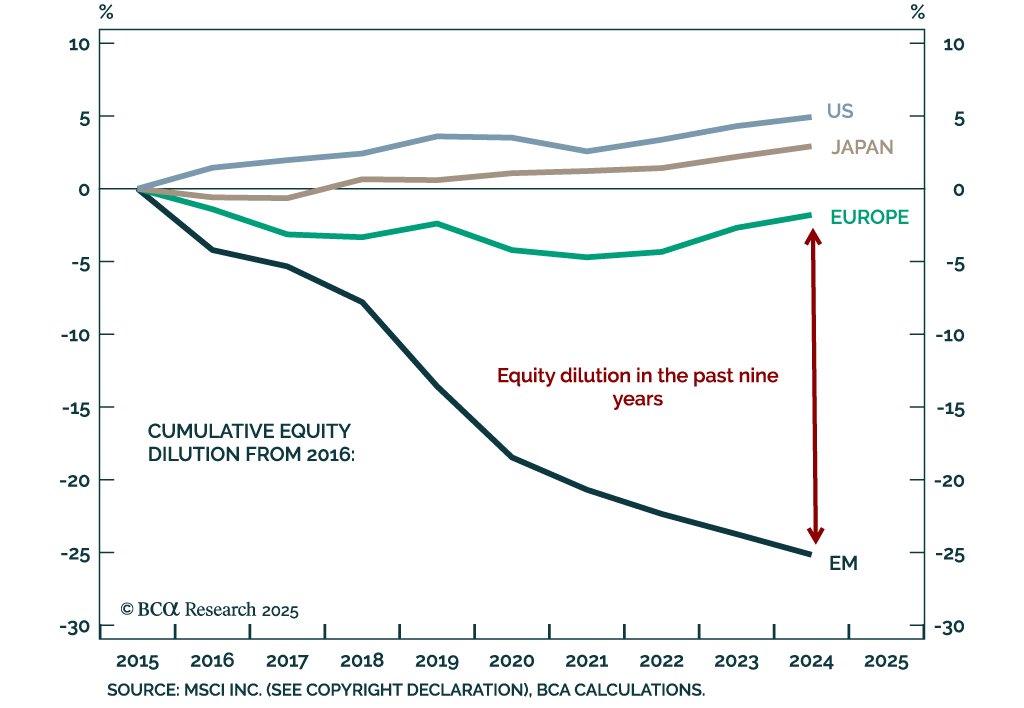

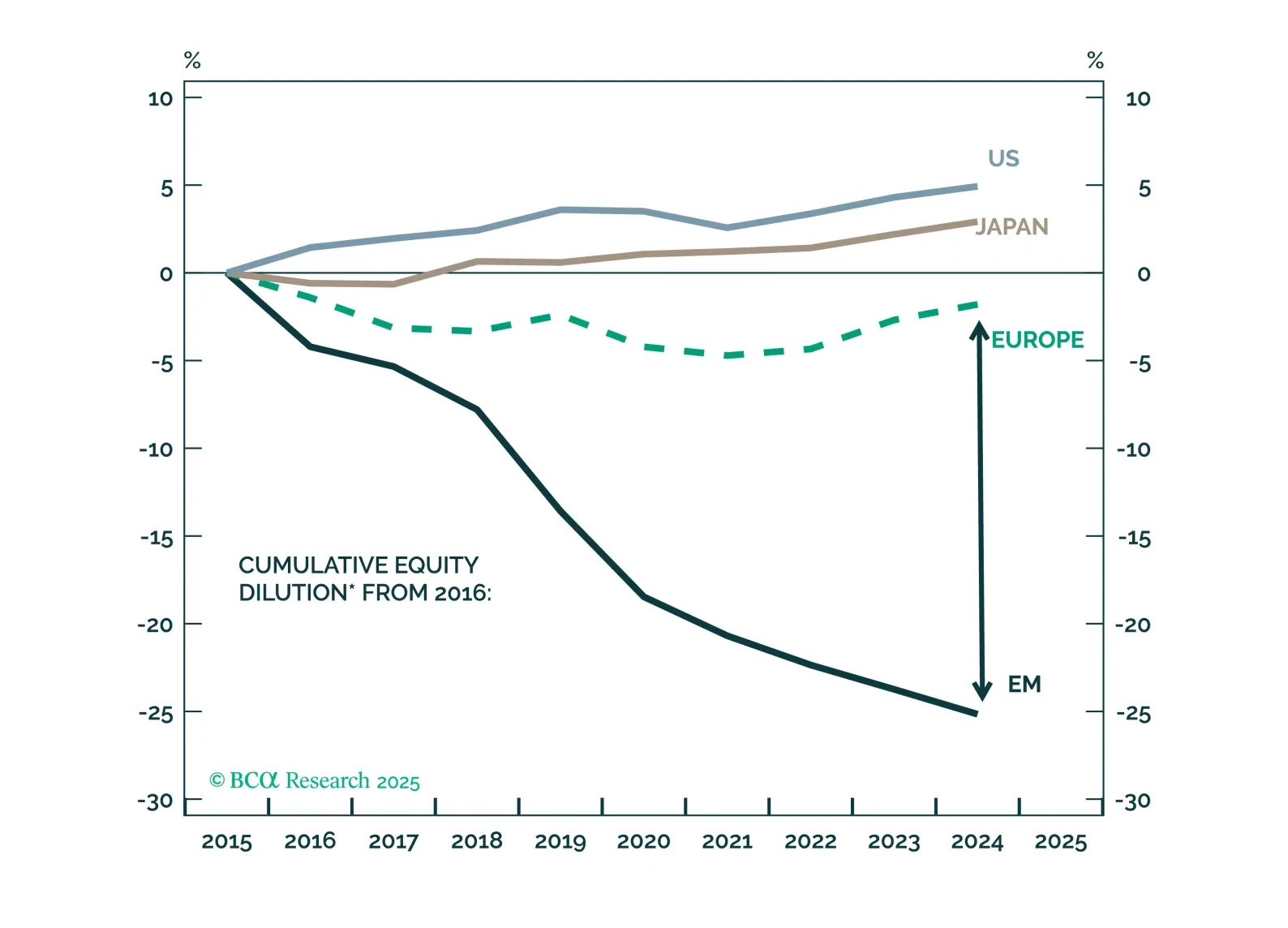

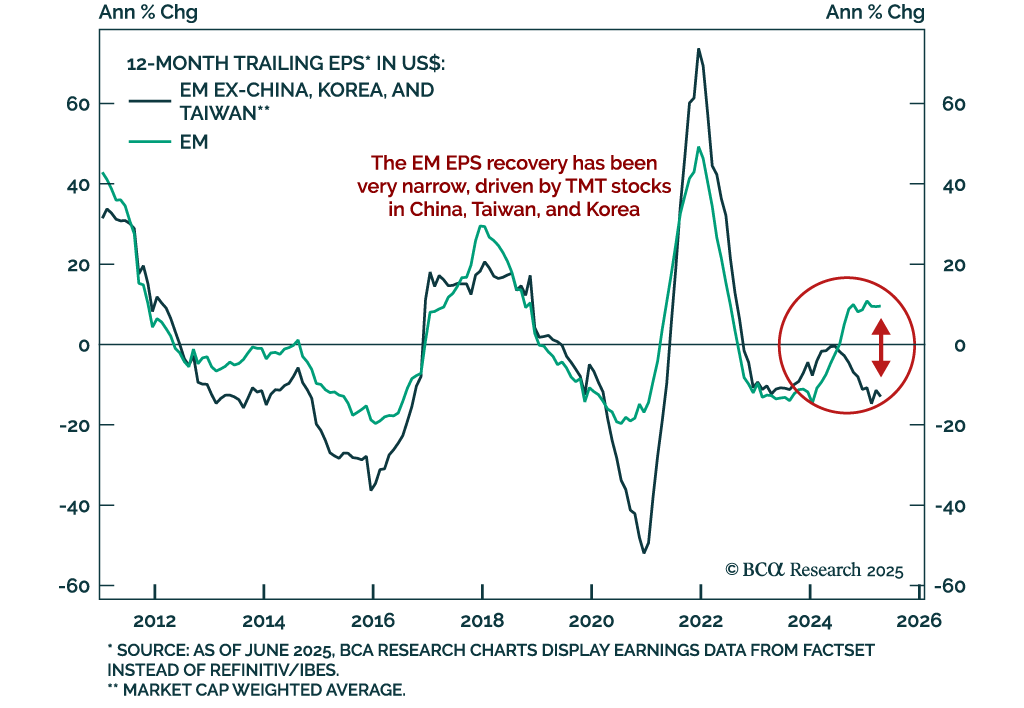

Dilution is one of the two main reasons why EM EPS has been much weaker than EM GDP and EM non-diluted profits. We calculate “pure” dilution – adjusted for companies’ inclusion and exclusion from the stock index – for various bourses around the world. To our knowledge, this is the first time this analysis has been conducted.

Investors should hold gold, build up some cash, tactically overweight US equities relative to global, and prepare for at least minor oil supply shocks – possibly major shocks – as the Israel-Iran war escalates.