Emerging Markets

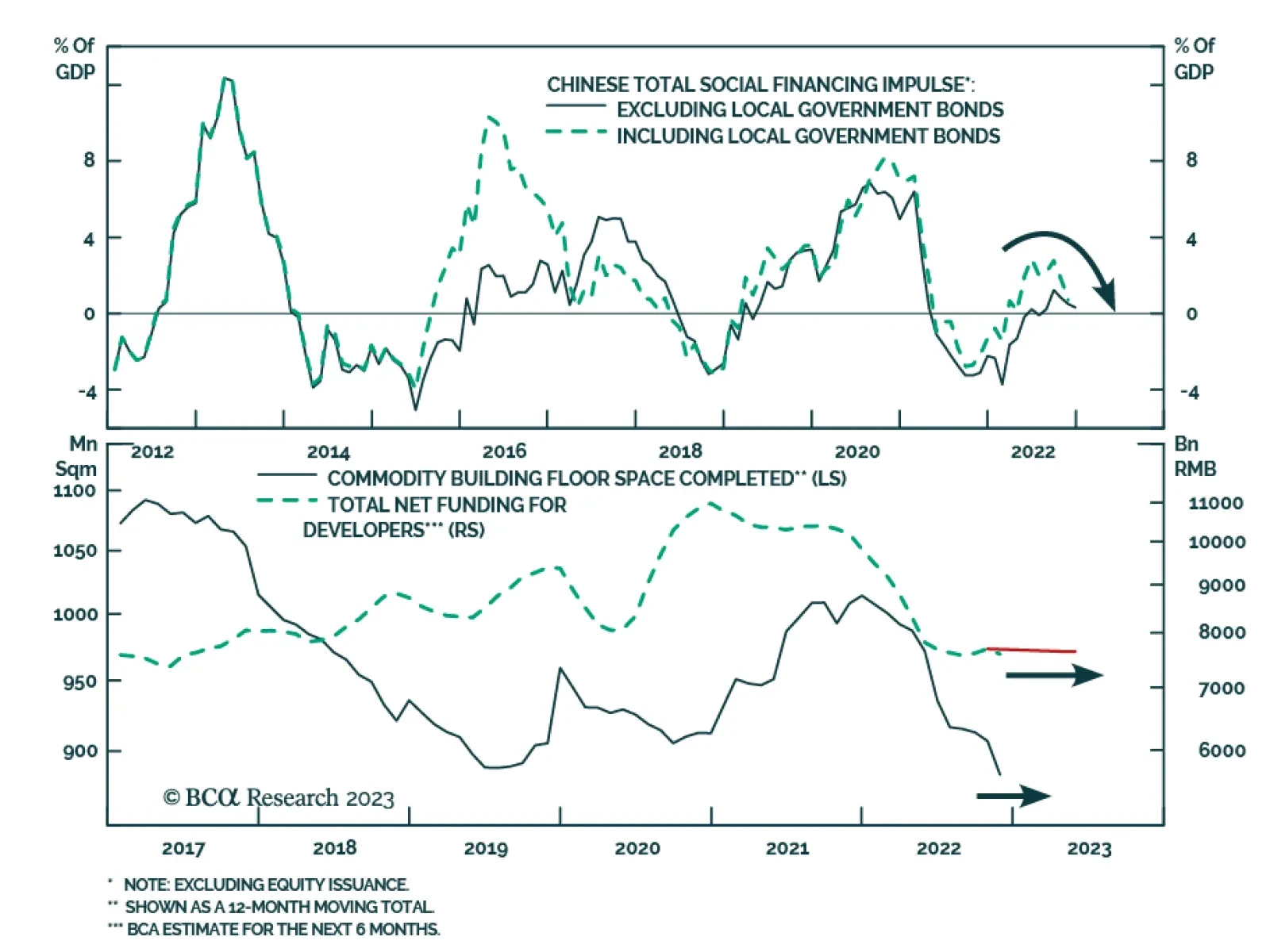

CCP policy stimulus will boost growth in China this year. Copper prices breached $4.00/lb on COMEX this week, as expected. We continue to forecast $4.50/lb this year, with upside price risk dominating. Iron ore also will rise, but economic and regulatory policy uncertainty clouds the outlook. We remain long the COMT and XME ETFs. We are getting tactically long BRL/USD and AUS/USD on the back of our metals view, which is constrained by China’s reversion to absolute autocracy and ability to reverse policy suddenly and unpredictably.

Why will Chinese consumer spending recover but not its industrial sectors? Will China's reopening boost the global business cycle and inflation? How fast will US core inflation fall and what are the implications for corporate profits? Are global equities pricing in enough bad news/profit contraction?

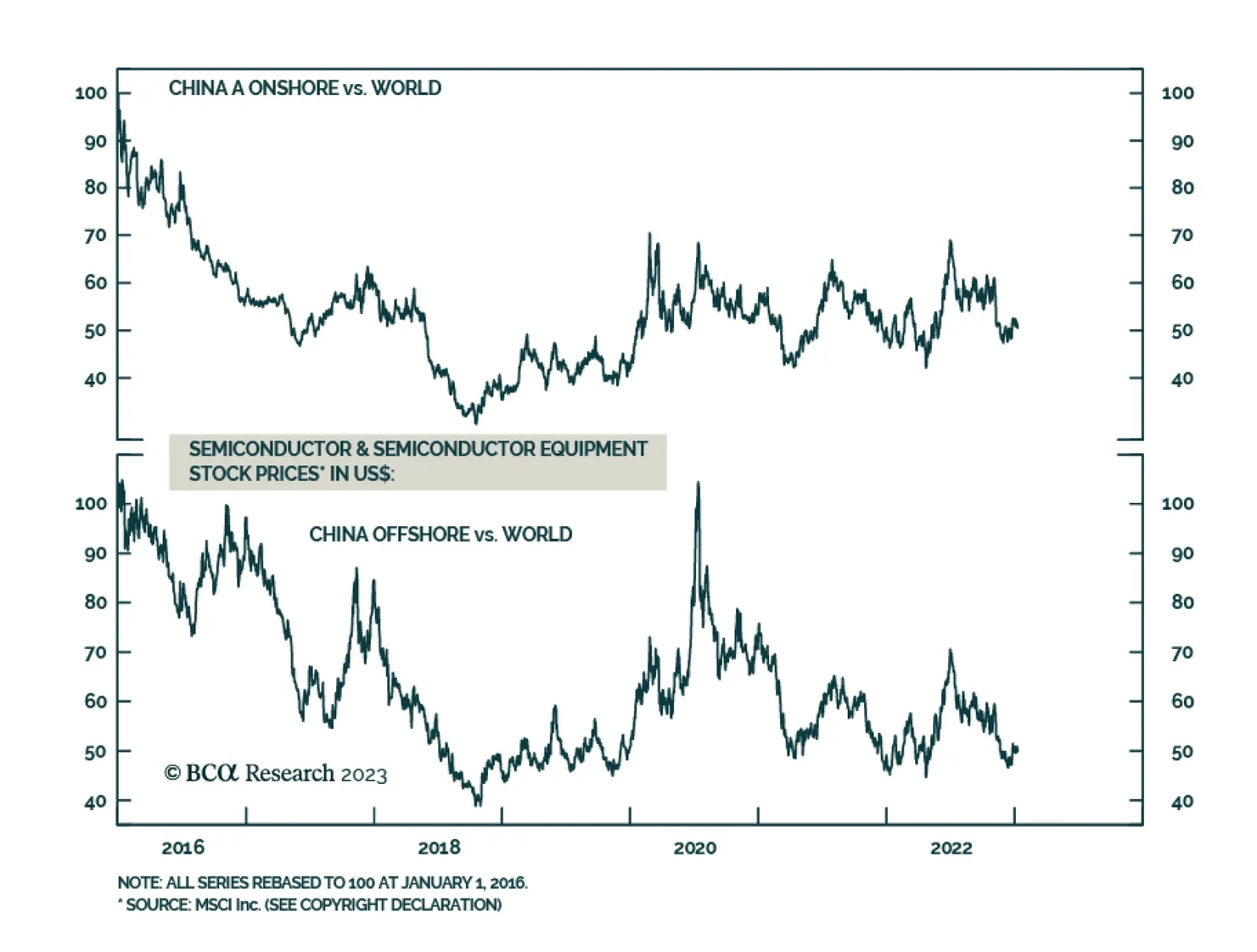

China’s semiconductor demand and imports will continue to contract in 2023H1. Despite economic reopening, Chinese consumers will hold back spending on smartphones, personal computers (PC) and other consumer electronics over the next six months. Meanwhile, overseas customers will continue to reduce their orders for electronic goods made in China following the excessive consumption experienced during the pandemic. There is more downside for both Chinese and global semiconductor share prices. We recommend a relative trade: long Chinese semiconductor stocks / short global semi stocks.

This week we present our Portfolio Allocation Summary for January 2023.

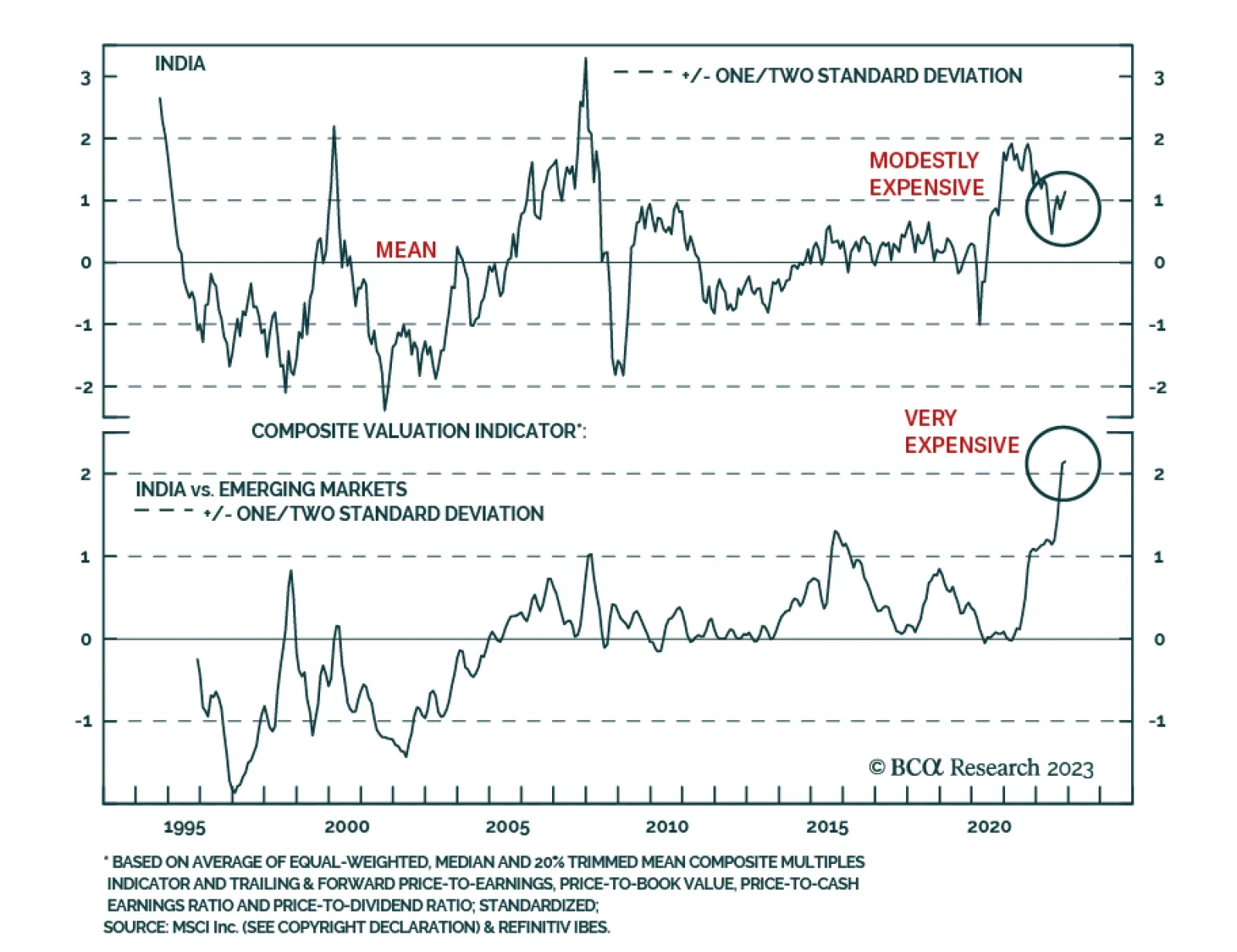

India’s lofty EPS growth expectations are set for a major disappointment. The RBI has overtightened monetary policy despite the absence of any genuine inflationary pressures in India. Fiscal stance is also restrictive. Stay underweight this bourse in EM and Emerging Asian equity portfolios.