Emerging Markets

Copper markets will remain tight on the back of growing physical deficits and pressure on capex. Policy-rate increases by central banks, uncertainty over re-opening in China and its fiscal-stimulus plans in the short run restrain risk taking. In the long run, the implications of China’s inward turn will keep supply-concentration risk for metals high, given its dominance of base-metals refining globally. Notwithstanding the disconnect between physical and futures markets, we remain bullish metals mining equities, and remain long the XME ETF.

Provided that US inflation is due to excess demand rather than supply constraints, demand destruction will likely be needed to bring core inflation below 3.5%. Such growth contraction is positive for counter-cyclical currencies like the US dollar. In China, the Party's focus is to alleviate structural inequality and a long-term confrontation with the US; and authorities are not yet panicking about the cyclical state of the economy. Hence, an economic recovery is unlikely in the coming months.

Expect the Middle East to create new and unexpected energy supply disruptions on top of the Russian energy shock.

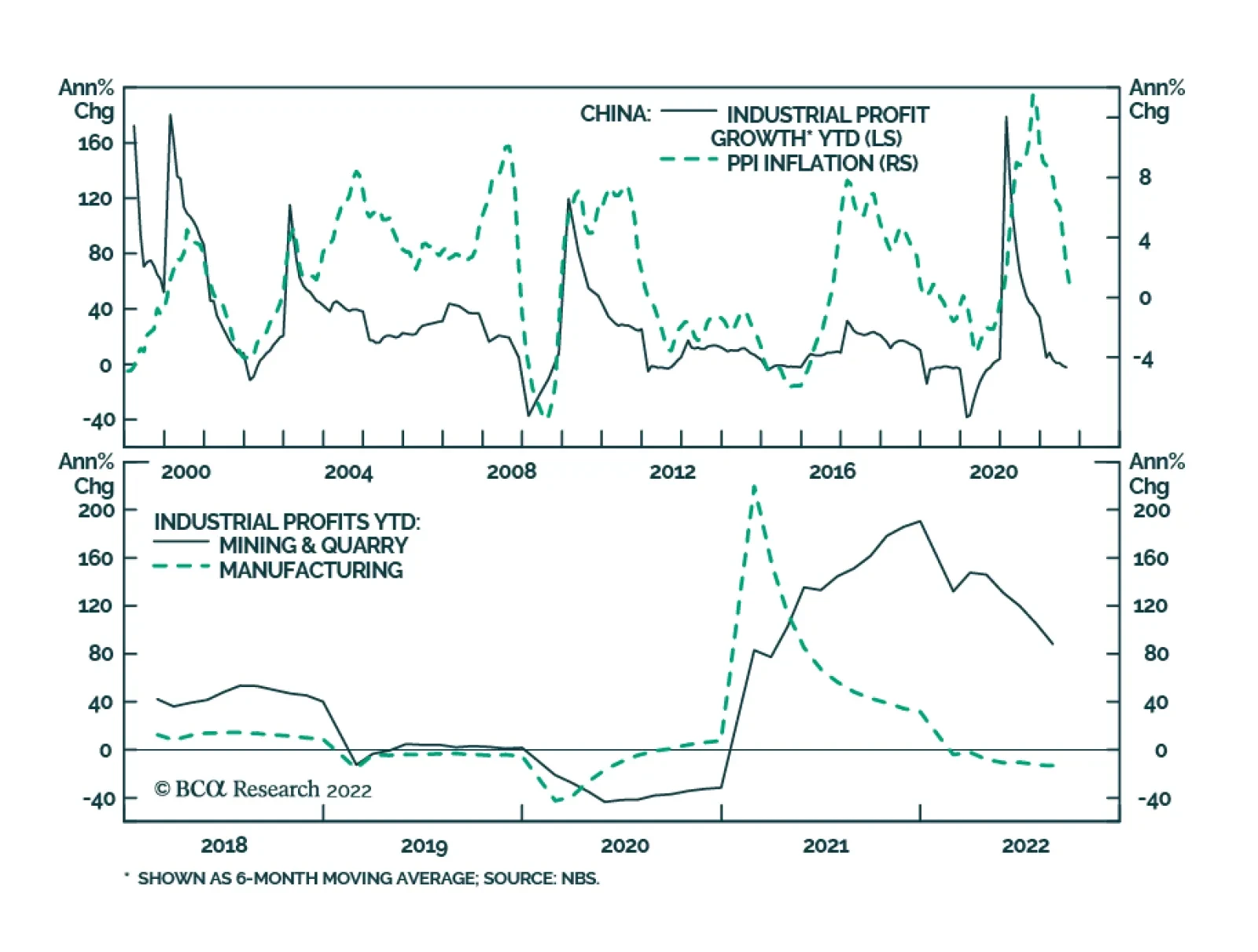

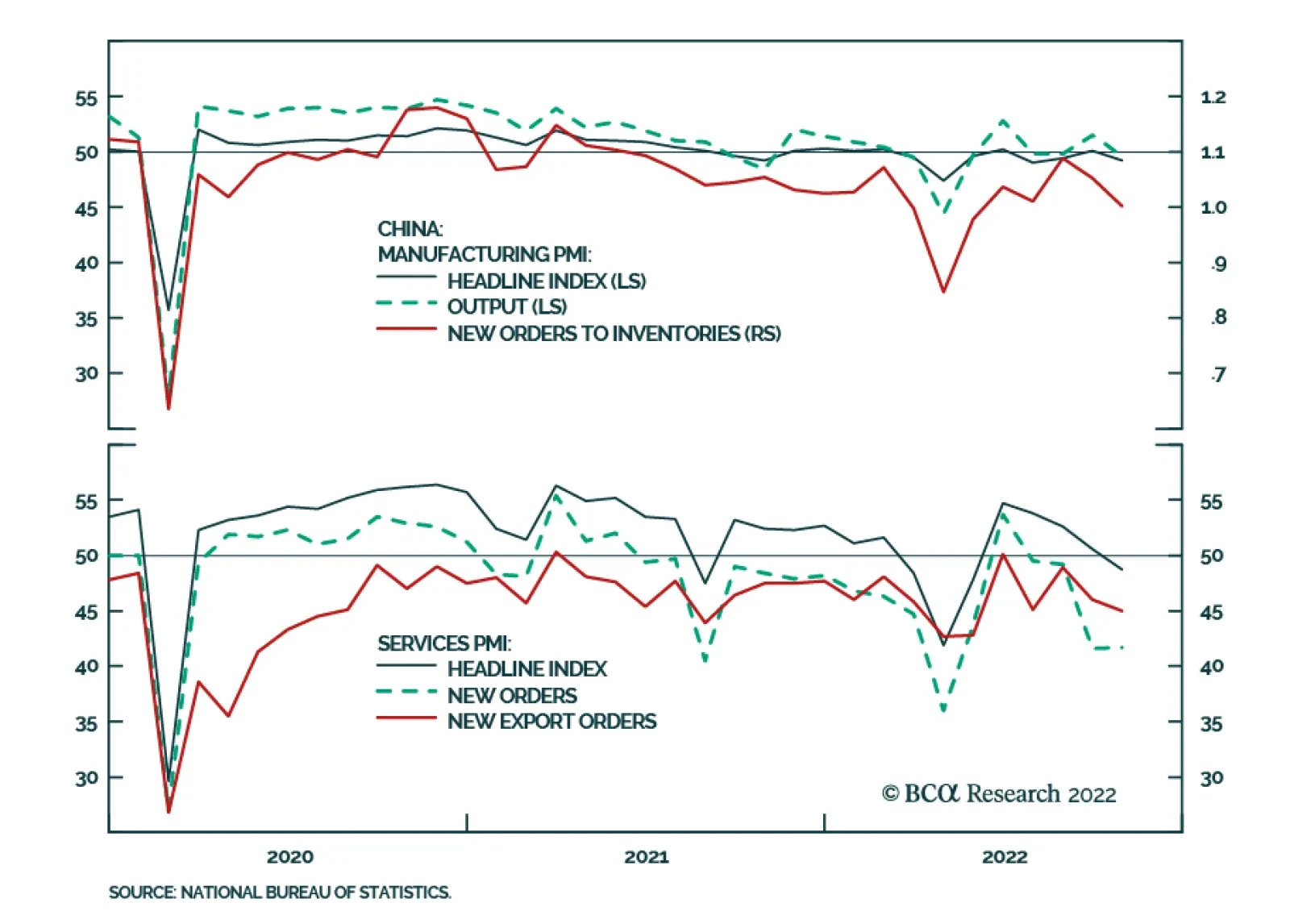

China's economy is about to experience demand-driven deflation. The lack of an economic recovery and falling producer prices will depress corporate profits and, hence, share prices. Beijing will allow the yuan to depreciate more to prop up its economy.

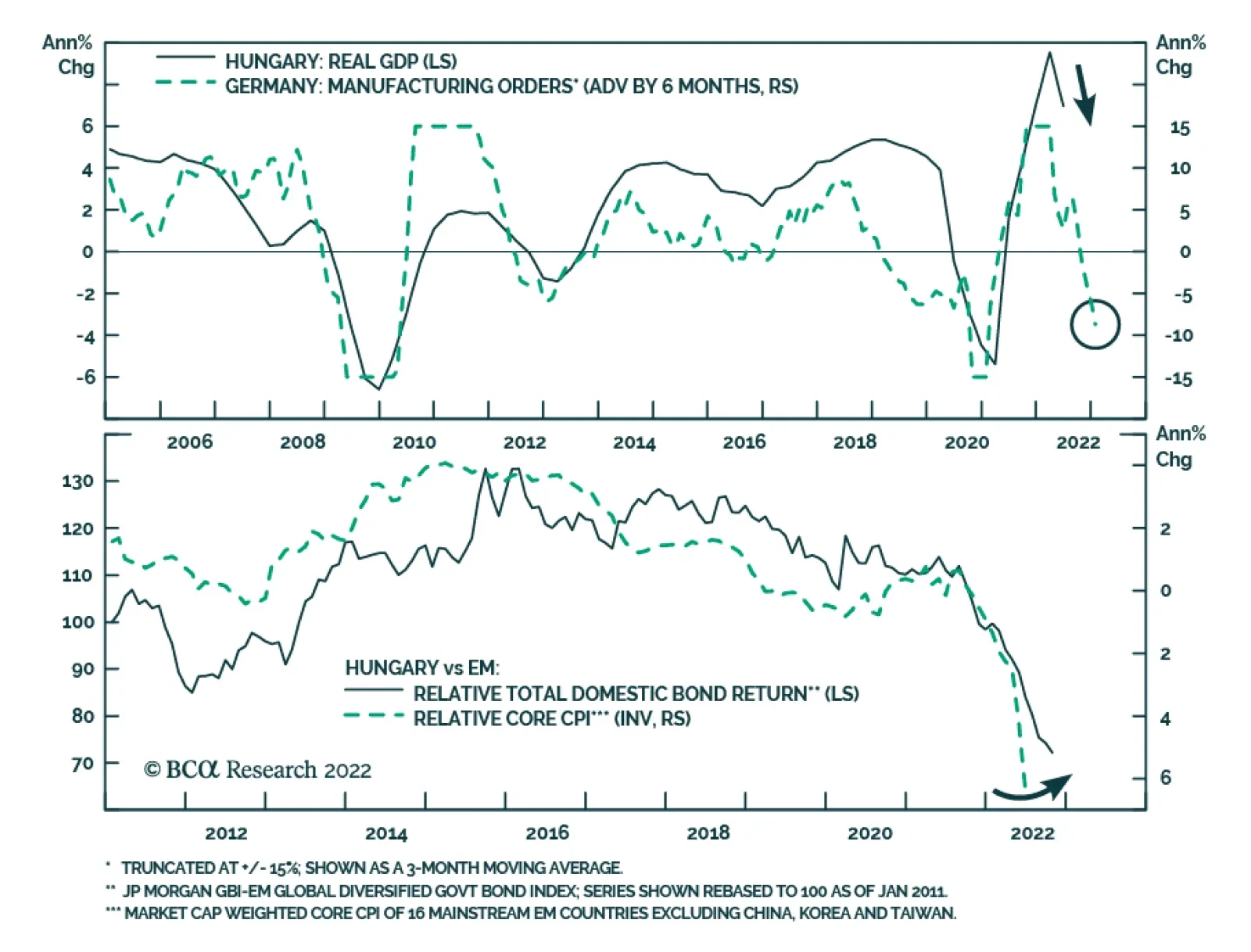

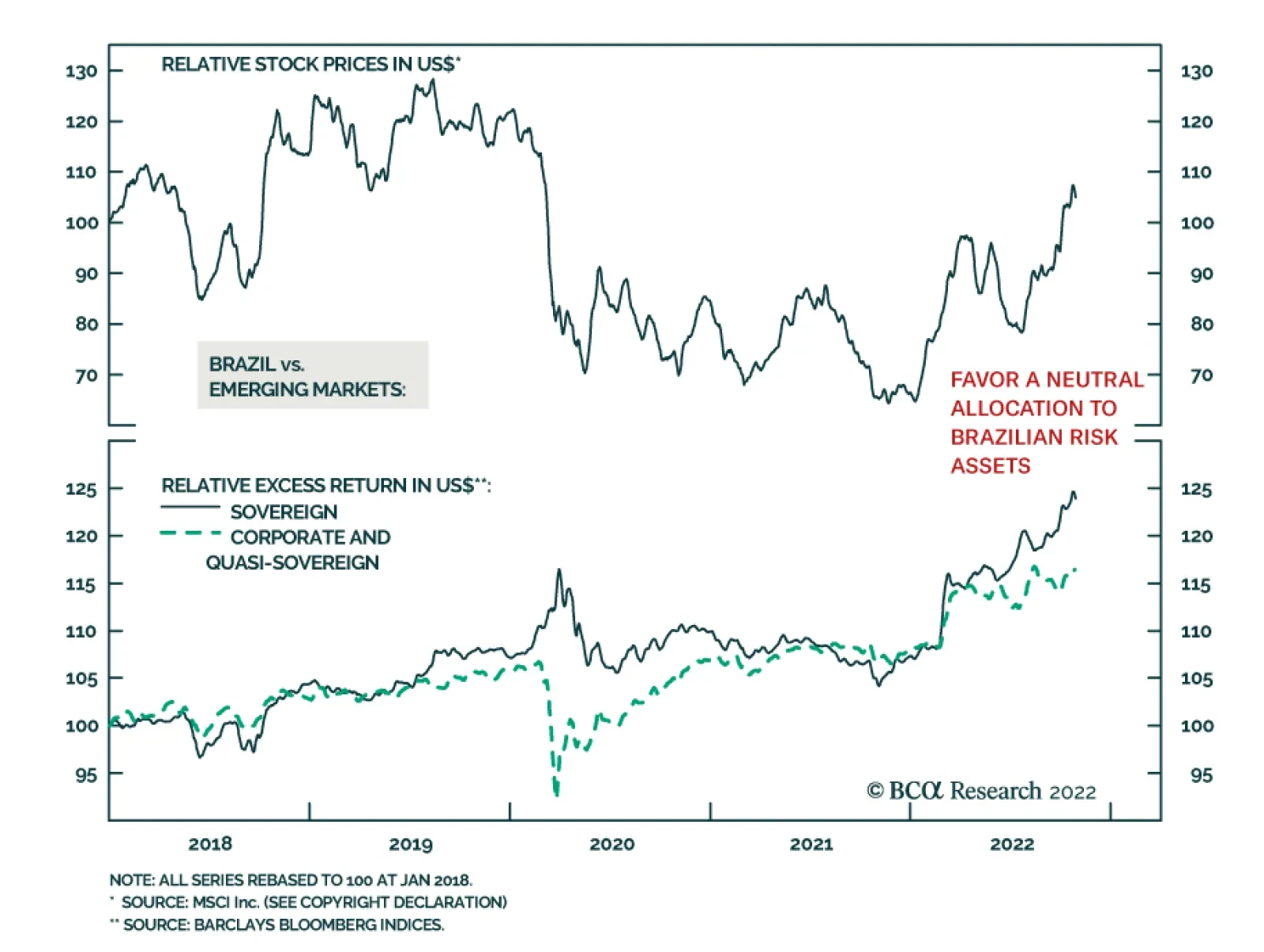

Stay short Greater China assets. Stay long Japanese yen. Hold back on Brazil for now but look forward to opportunities in future.