Energy

We expect oil-demand growth to increase this year – to 1.7mm b/d from 1.4mm b/d (0.30% of total demand) – and anticipate tighter supply at the margin. Our balances estimates are unchanged, leaving our Brent price forecasts for 2024 and ’25 at $95/bbl and $105/bbl. We expect the US to deploy warships if Venezuela makes a move on Guyanese territory in a bid to grab deep-water oil production.

Qatar’s strategy to raise LNG output 84% by 2030 is a bold bet DM demand for energy security – and EM demand for affordable electricity to support economic and population growth – will remain a higher priority than eliminating fossil-fuel consumption over the next 20 years. This will accelerate the development of a global LNG spot market, which will increase demand for LNG tankers.

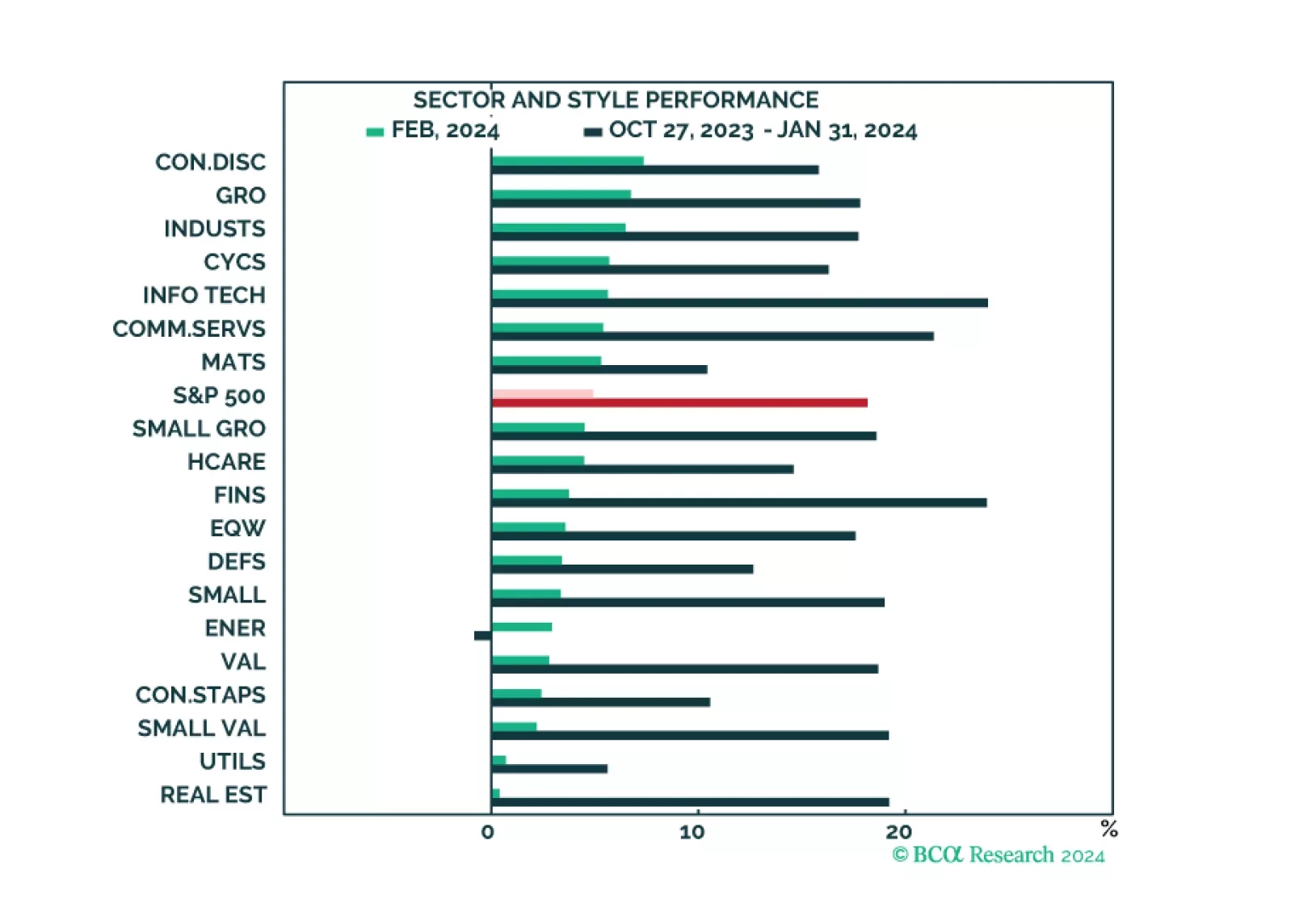

The market narrative continues to be dominated by the Magnificent Six, which drove both market performance and strong Q4 earnings results. While all sectors and styles have recently turned green, the rally is still mostly narrow. Earnings growth appears to be strong, but outside of the Magnificent Six, many companies are struggling. The market appears expensive and overbought, but that is mostly down to the high valuations and the popularity of the Magnificent Six.

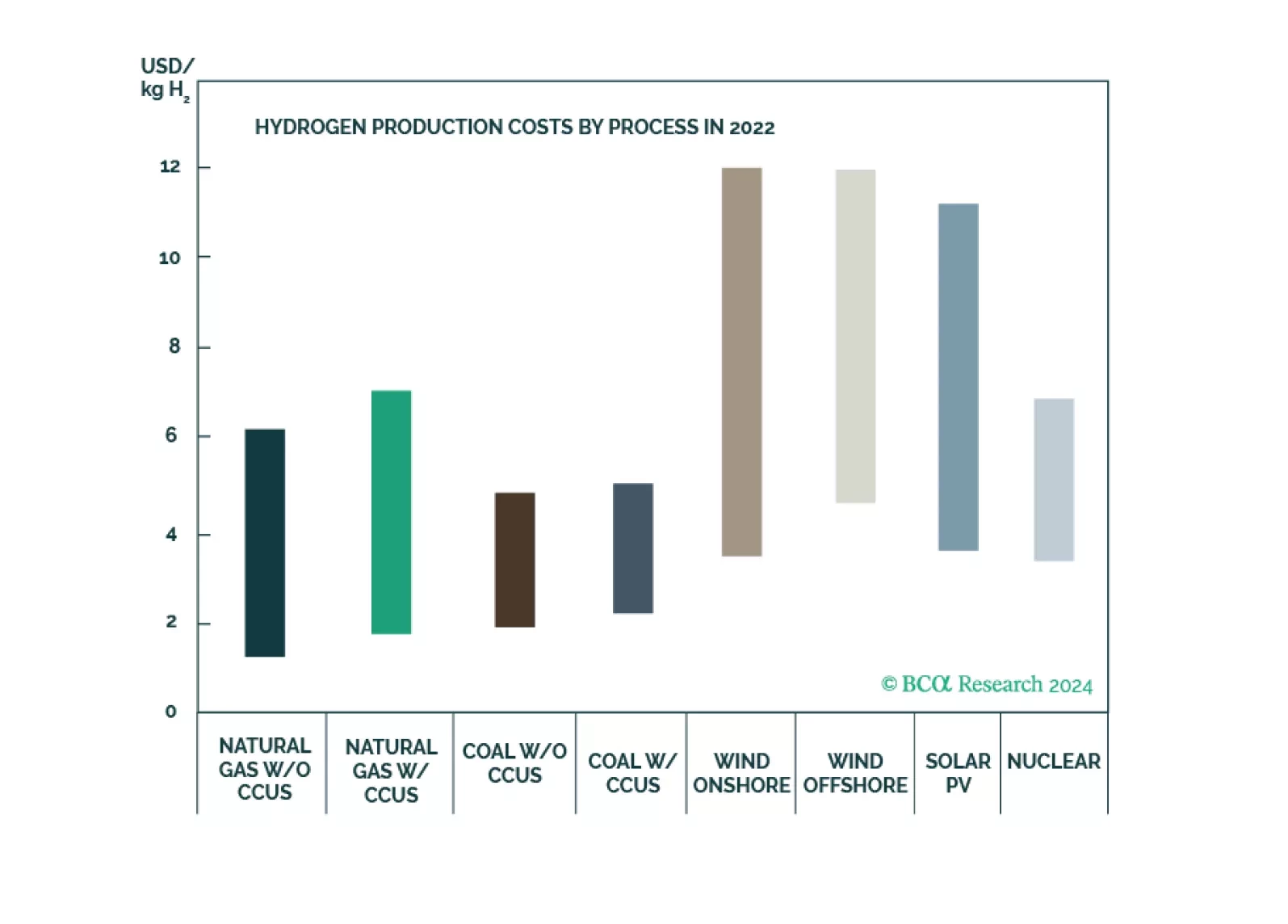

Naturally occurring hydrogen as a clean-energy source has the potential to satisfy significant energy demand growth at low cost. Oil and gas E+P companies and pipelines are ideally positioned to take a leading role in this clean-energy evolution, given their core competencies include large-scale resource extraction, storing and transporting gaseous commodities. Blending gold hydrogen with natural gas in pipeline systems could accelerate the industry’s learning curve in finding and delivering clean-energy fuels.

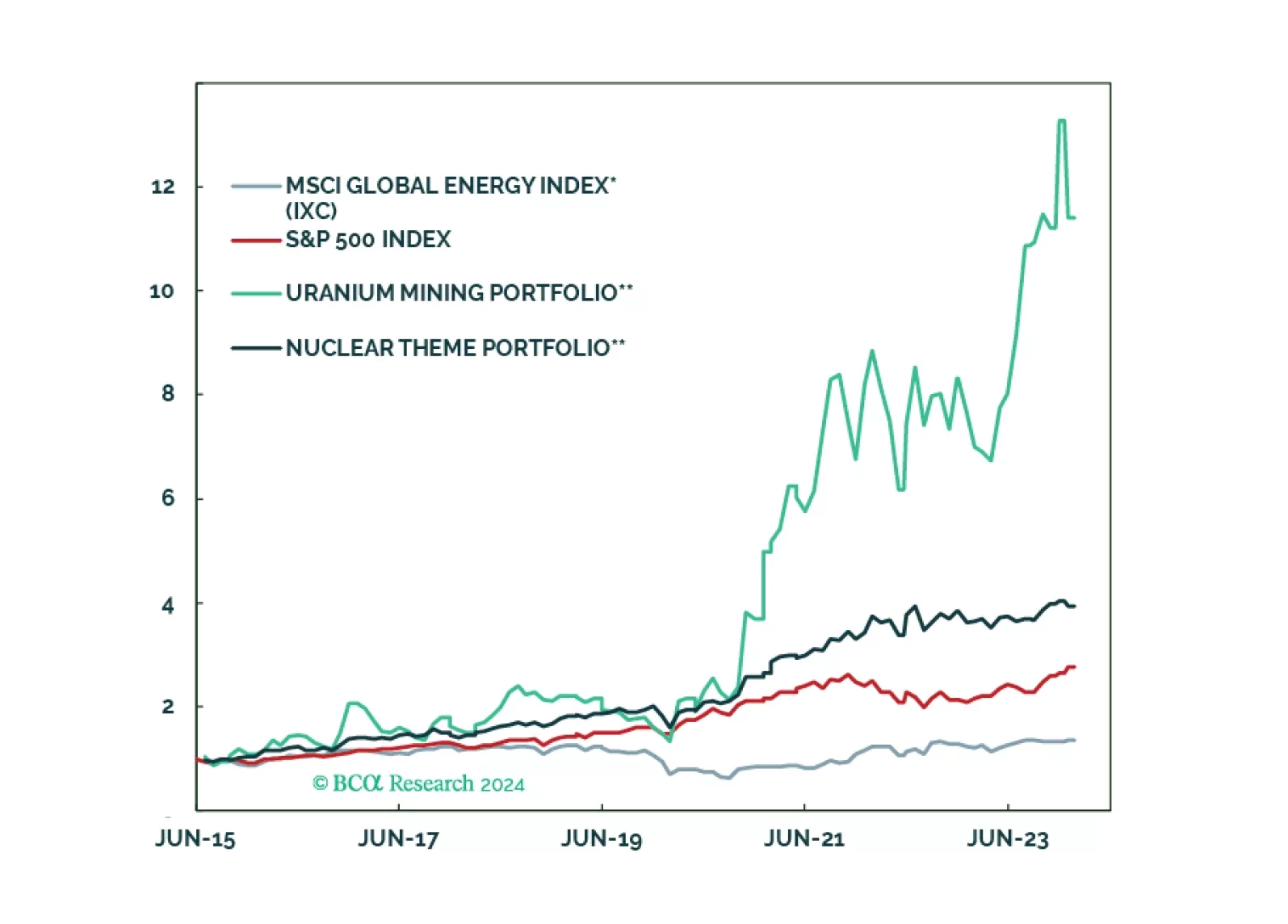

This report presents the main ways to invest in the Nuclear Renaissance; from exposure to physical uranium to equity plays alongside or outside the nuclear fuel cycle.

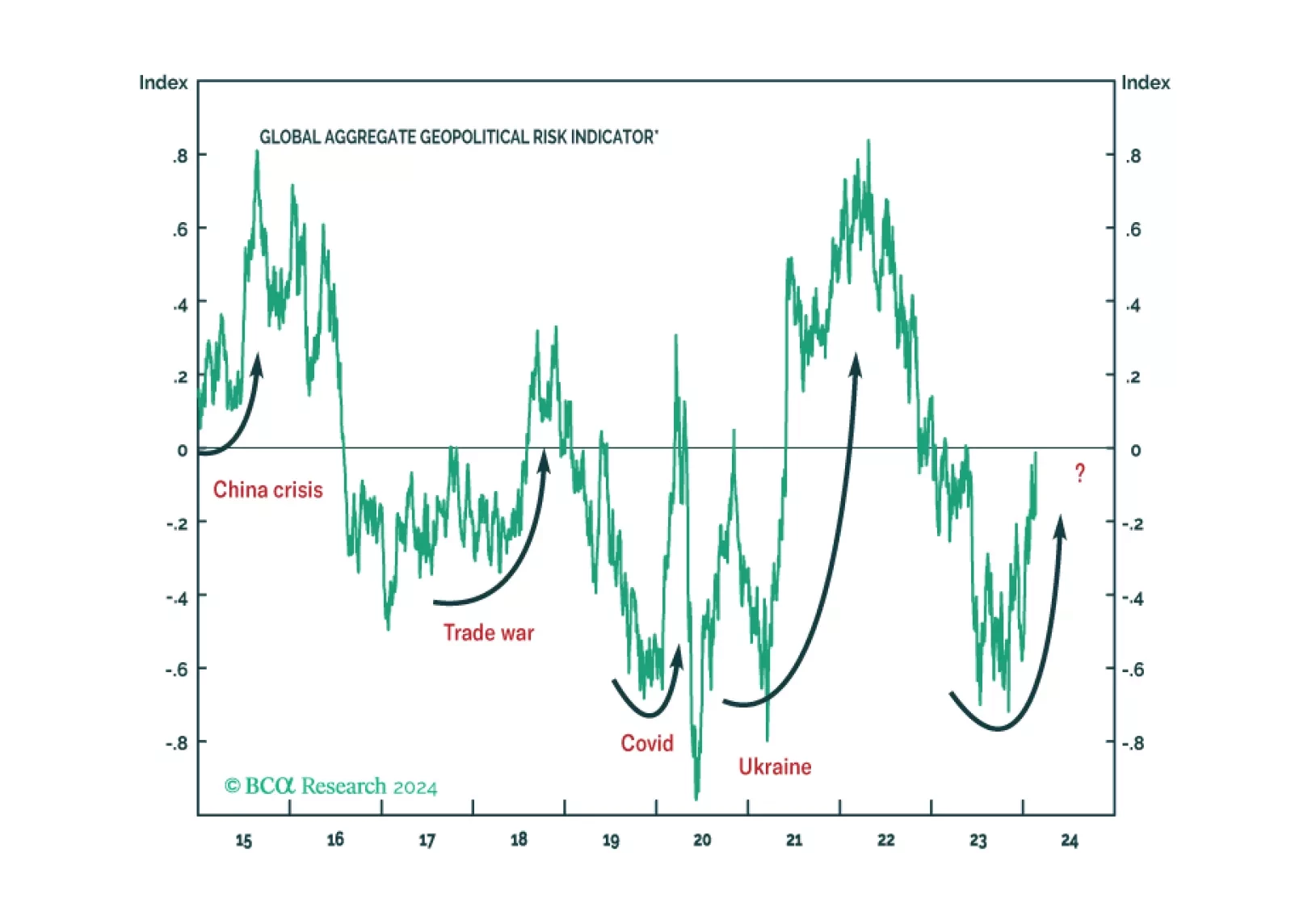

While 2024 will see various election risks, global geopolitical uncertainty is driven by the US election and its struggle with Russia, China, and Iran. The stock market can manage local domestic political risk. But it will correct upon a major outbreak of geopolitical uncertainty.

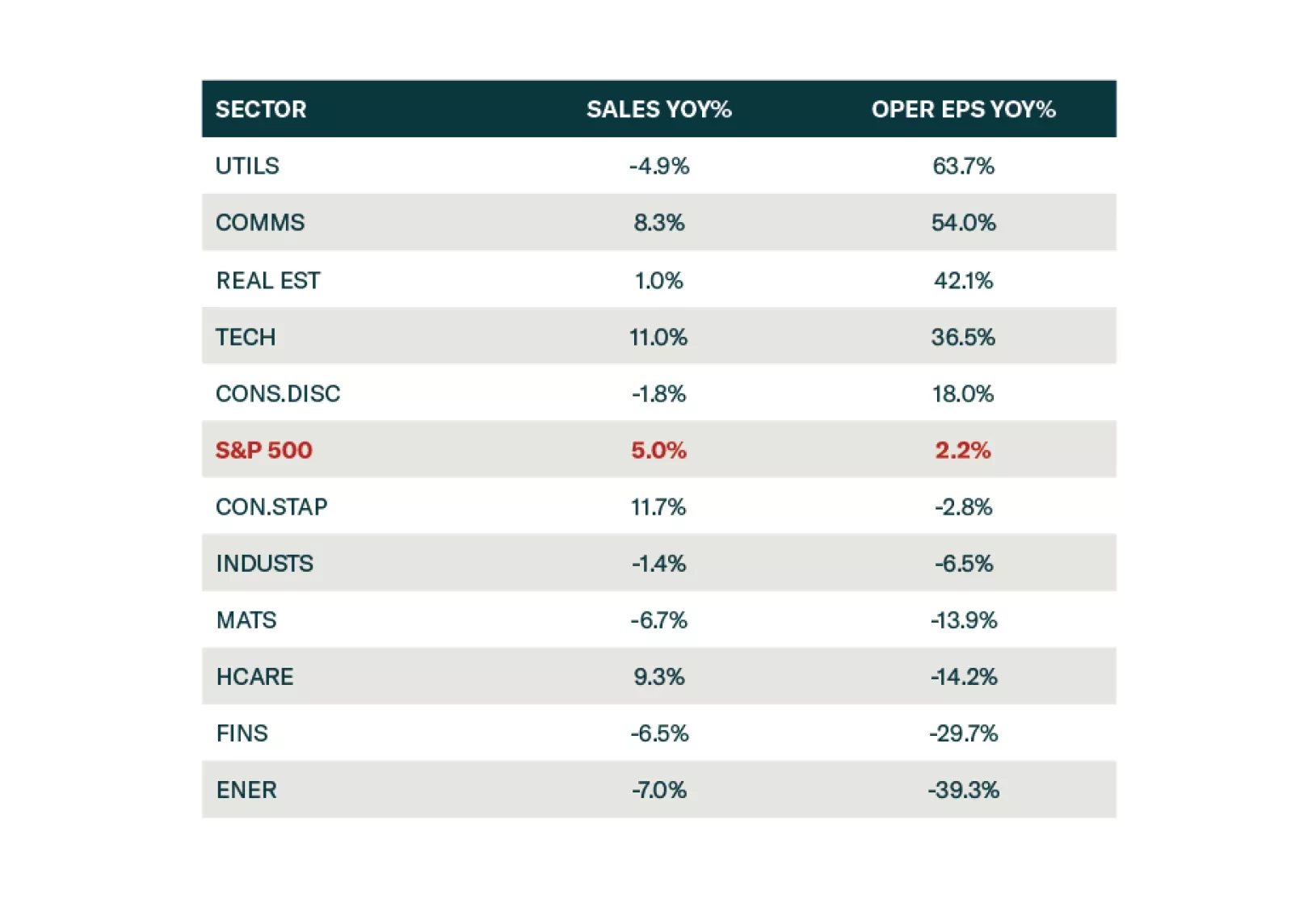

Reported earnings for Q4-2023 were rather underwhelming and prone to issues that we have identified over the past few months: Growth is concentrated in just a few sectors and companies, while the profitability of a broad swath of the equity market is under pressure from disinflation and sticky wages. Consumers are still spending, but less enthusiastically than before, while a switch from spending on services to spending on goods is in its very early innings. Downgrade Consumer Staples to neutral.