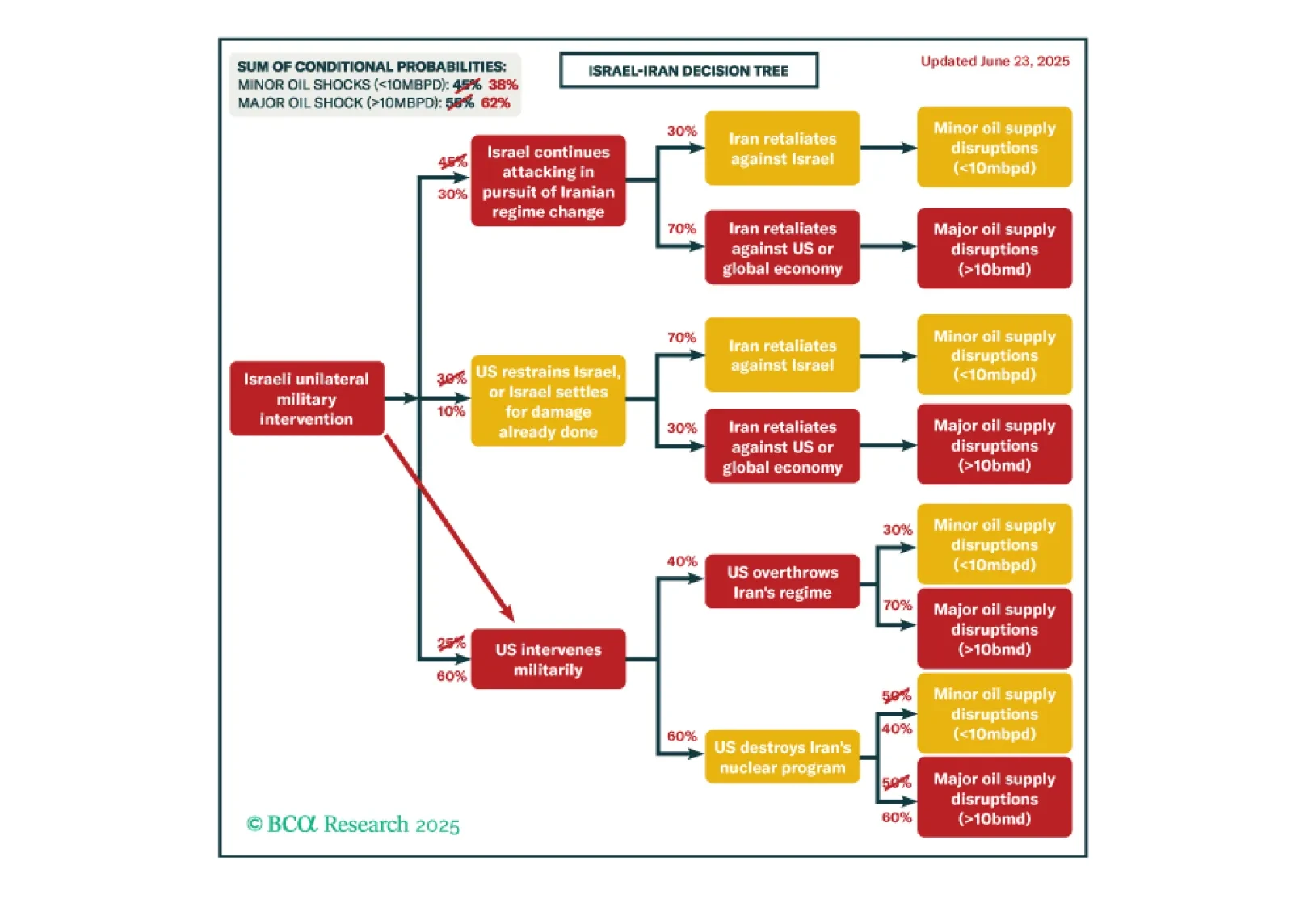

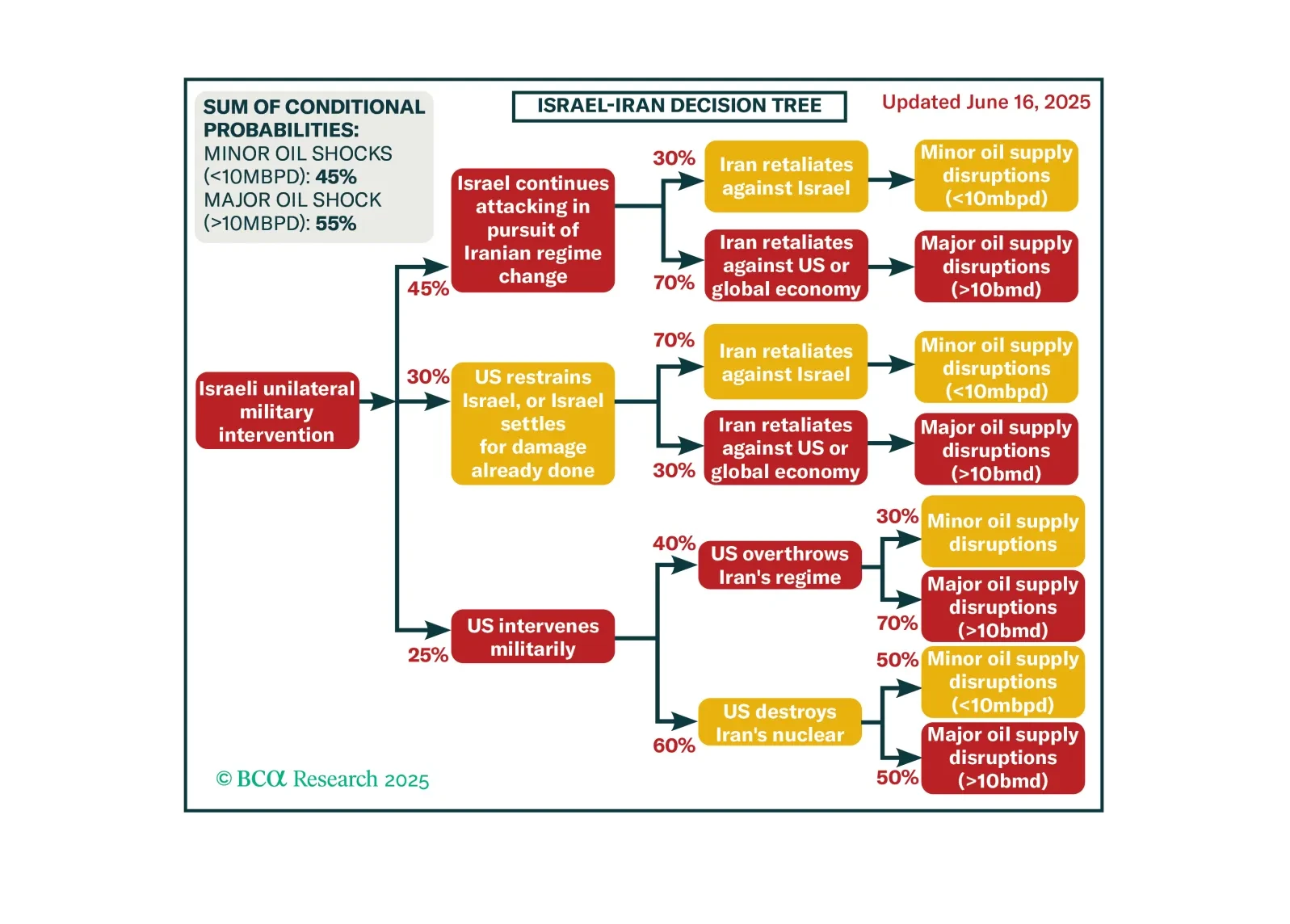

It is not yet clear that the Iran war is deescalating, despite the best efforts of global financial markets to dismiss its significance. True, Iran’s missile attacks on US military bases in Qatar and Iraq appear ineffectual as we go to press. Oil and gold both slid while equities gained on Monday (Chart 1), though oil has risen by 15% over the past two weeks while haven assets rallied.But Israel will keep striking until the US forces it to back down. Earlier we gave a 60/40 chance of a major oil shock if the US intervened to destroy the Iranian nuclear program (Diagram 1). But for that pessimistic scenario to come true, one would need to see Iran strike regional oil production or interfere with oil shipping. So far that has not happened. By major shock we mean a war that disrupts production throughout the Persian Gulf – for example, a disruption in excess of eight million barrels per day in OPEC+ spare capacity. Or one that causes the Brent price to rise by 50%-100%. So far physical oil supply has not really been hit, though investors should assume that Iran will retaliate against oil as well as US military bases. The risk event will subside for now given Iran’s pathetic response. But we are not sounding the “all clear” just yet. Investors should continue to position in a way that benefits even if the war escalates again, such as by overweighting US equities and defensive assets. Iran’s Refusal To SurrenderEverybody knows that Iran is a mountain fortress with a population of 90 million so there is no way that the US or its allies are going to invade with ground forces.The Iranian regime also believes it can survive bombardment campaigns by the Israeli and American air forces. Leaders have refused to surrender despite American ultimatums and demands, ultimately leading to the US attacks. If the regime believed that its nuclear program would be permanently extinguished and its regime certainly toppled, then it would have surrendered to try to stay alive via negotiations. Instead its choice was to fight.Hence the regime believes that it can survive air campaigns. It is very difficult to knock out a regime from the air. The Iranian people will rally around the flag in the short run while the country is bombarded by foreign powers. The Iranian youth, and others disenchanted by the regime, are now forced to recognize the regime’s enemies and the threat of the foreign invader. Eventually, economic collapse and social unrest could still topple the government, but that would require a bloody battle with ruthless internal security and the Iranian Revolutionary Guard Corps. It will not happen overnight.Meanwhile Israel and the US are domestically divided and have limited commitment to the war. The Trump administration does not want to see an economic shock that undermines its narrow grip on Congress and the US public. In short, Iran believes it will sustain these attacks and survive, with a new generation initiated into supporting the regime by seeing firsthand what they are up against. It even believes it will resuscitate its nuclear program. All of this means that Israel will escalate its attacks on critical infrastructure, the missile program, and the remnants of the nuclear program. The US will support Israel until it is satisfied that the job is done.Why Would Iran Take Any Further Action?As long as Israel continues its campaign, Iran’s leaders will need to raise the economic and political cost to the Trump administration, to encourage it to restrain Israel and refrain from additional US attacks. Striking US military bases is a way of saving face. President Trump would retaliate if soldiers were killed, but later the risk could encourage the US to draw down some of its forces. So this form of retaliation may not be finished, despite Iran’s official rhetoric, and the US will continue to expect it. Investors do not care about the war so far because it is not affecting global oil supply. But as Israel’s attacks continue, Iran will try to force the US to change policy.Striking oil production or distribution, in Iraq or elsewhere in the region, will push up the global oil price, undermine domestic political support for the Trump administration, and attract international pressure on the US to conclude the war.Iran can adjust the magnitude of the oil disruption without immediately closing the Strait of Hormuz or forcing the US to act with maximum aggression. For example, the IRGC or foreign militant proxies can disrupt production in Iraq or shipping in the Gulf of Oman or Indian Ocean. While the US would respond initially, the Trump administration would be tempted to declare victory and reduce operations, for fear of escalating further and triggering a massive economic and political shock. For those who say that Iran can sustain Israel and American bombardment without retaliating, if that is true, then Iran can sustain the bombardment while retaliating.So Iran has an incentive to strike regional energy supply, suffer the US retaliation, and wait as pressure builds on the US economy and political system for a change of foreign policy. A retaliatory cycle of this nature will cause minor oil shocks and increase the odds of a major oil shock. A major shock would require Iran to attack Saudi Arabia or the other major Gulf Arab oil producers, which is not yet likely – and will not happen if the escalatory cycle that we are describing never takes place. Similarly, Iran will not close the Strait of Hormuz unless the US has already done much greater damage and Iran believes its regime already faces collapse and has nothing to lose. But a lack of trust means that any sign that Iran could move, or the US could preempt it, could precipitate some kind of crisis in the strait.A major oil shock would short-circuit the business cycle, so investors should remain cautious for now. It may not happen, but the downside for global risk assets is larger than the upside at this juncture. Investment TakeawaysThe conflict underscores our contention that the US remains “exceptional” and US assets retain their safe-haven properties.US stocks have outperformed global stocks by 0.3% over the past two weeks – while US energy shares have outperformed their global counterparts by 1.1% (Chart 2).The Middle East as a region has underperformed in line with our expectations.Global energy has outperformed other cyclicals.These trends will fall back temporarily while the crisis seems to abate, but we are not yet convinced that we should close our trades on a genuine de-escalation.Matt Gertken Chief Geopolitical Strategist mattg@bcaresearch.comFollow me onLinkedIn & X