Energy

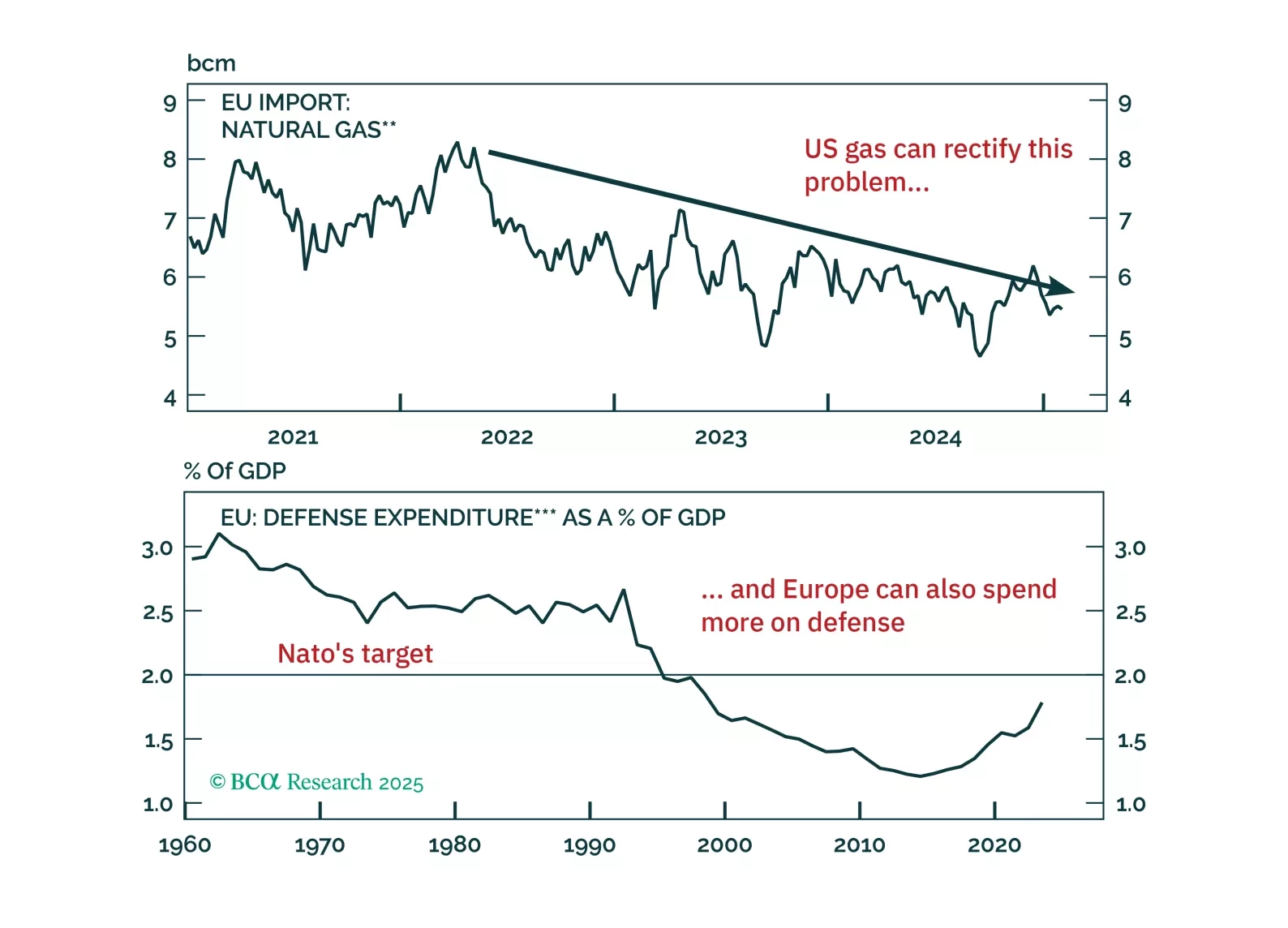

Europe is about to become President Trump’s next target. The good news: a US/EU trade war will be short as common ground to achieve a deal exists. The bad news: European assets remain at the mercy of heightened uncertainty. How should investors position themselves in this tricky context?

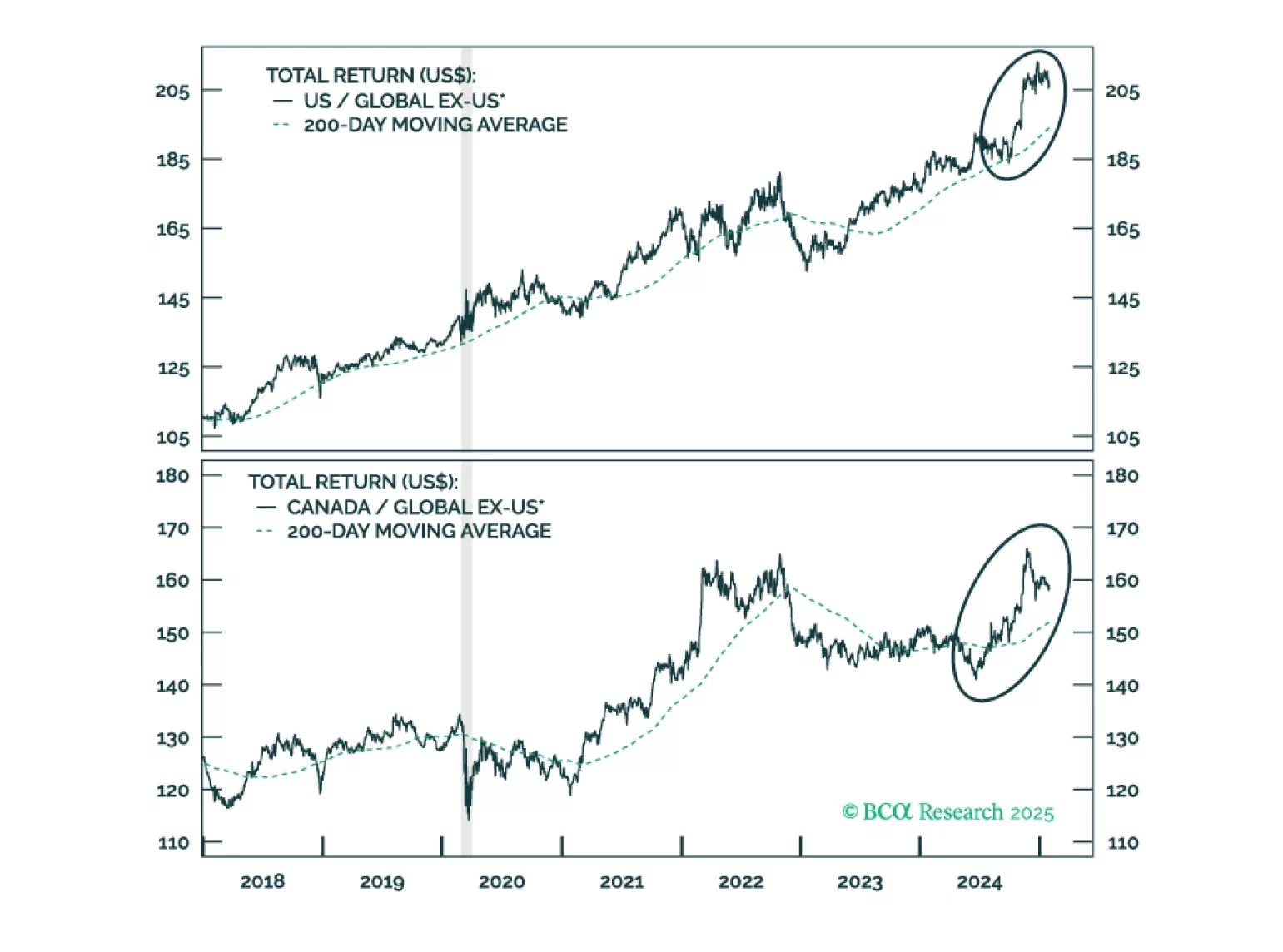

Jonathan provides an update on Canada following strong performance from Canadian stocks last year. On a tactical basis, underweight Canada versus global ex-US on the expectation of tariffs targeting Canada and Mexico. Following a sell off, or if a trade war is avoided, investors should place Canadian stocks on upgrade watch with the goal of moving to a modest overweight versus global ex-US.

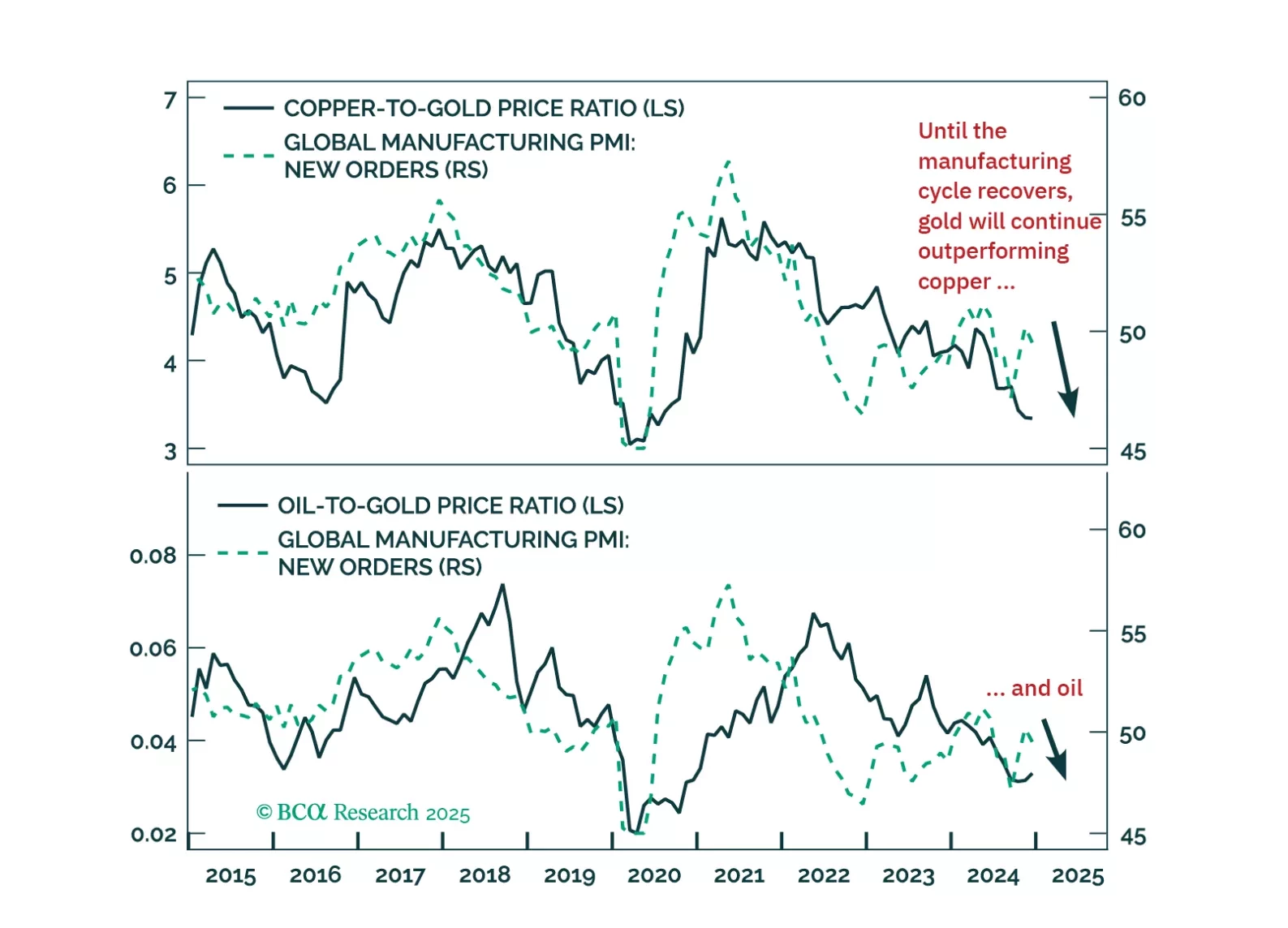

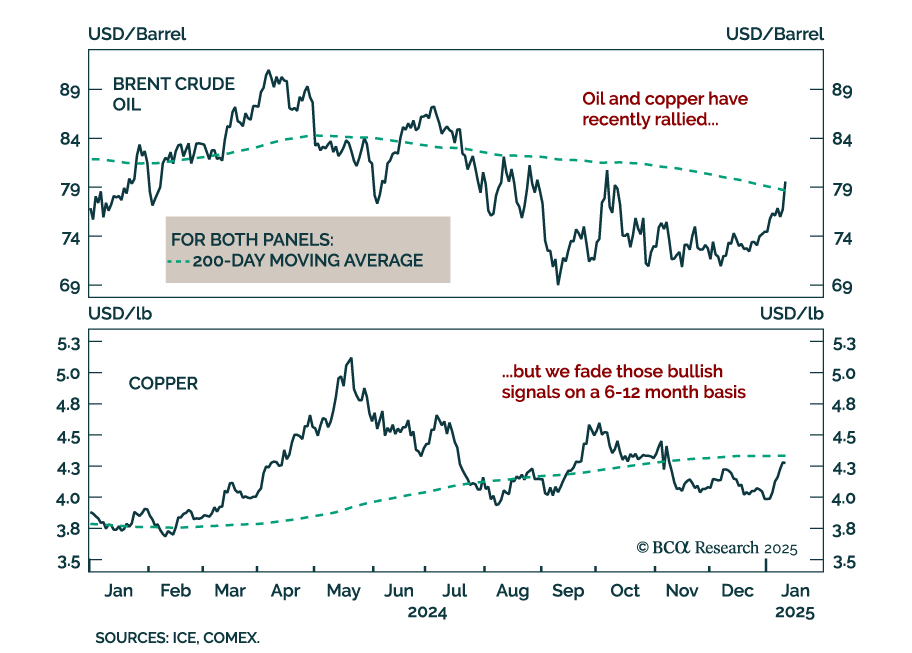

In this Special Report, we outline the three themes that we believe will drive commodity markets this year: (1) demand growth will remain sluggish across cyclical commodities (2) supply-side developments will ultimately be bearish for oil prices, and (3) traditional relationships between commodity prices and financial variables may not hold.

Every year we highlight five low-odds scenarios that would have a major impact on global financial markets if they happened. This year we contemplate a total reversal of Chinese policy, a US-Iran nuclear deal, a breakdown of NATO, US military action across the Americas, and an internationally coordinated FX intervention.

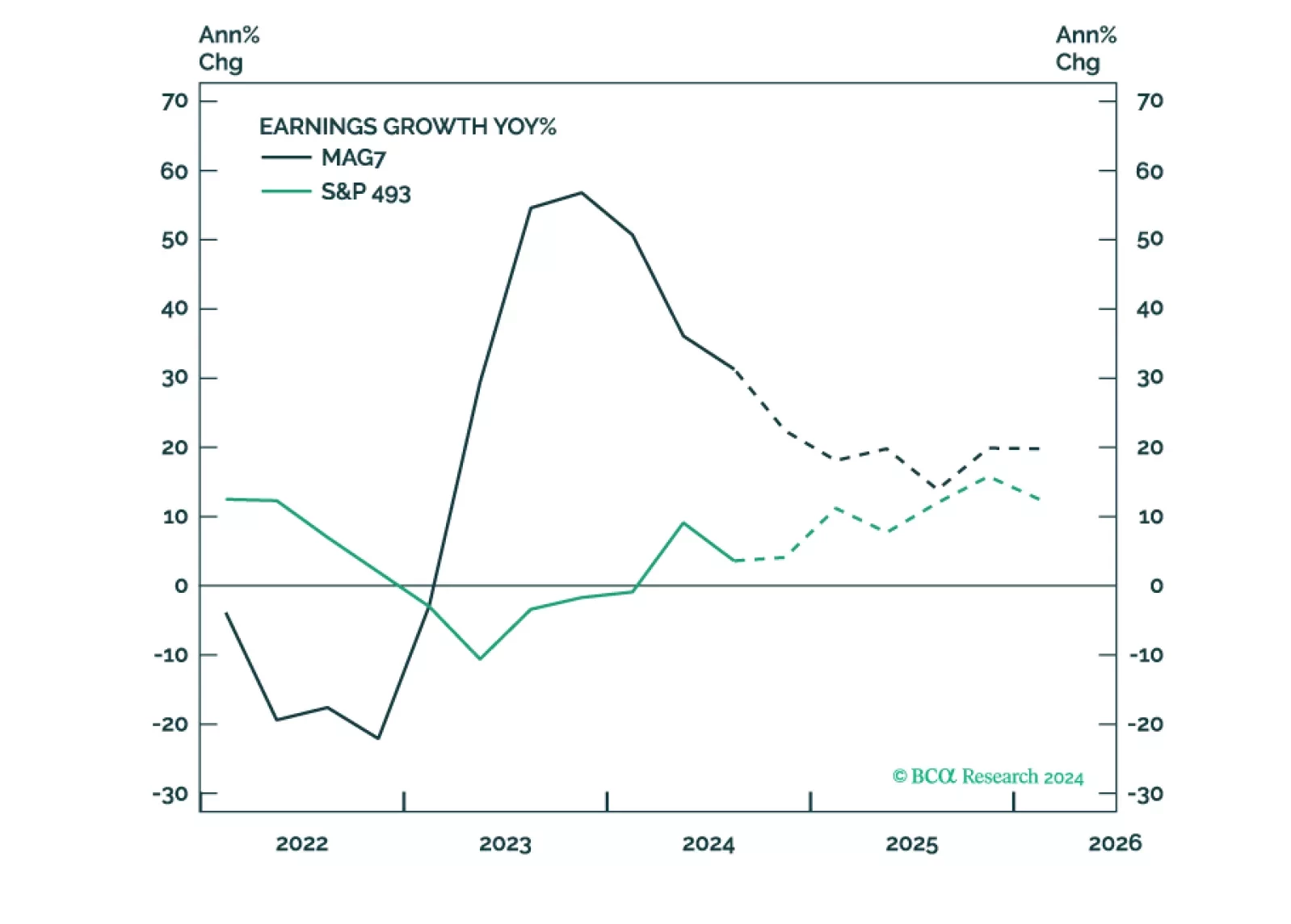

Trump's policies aim to support domestic producers and will be pro-growth and inflationary, at least initially. This environment is supportive of equities. Earnings will likely be strong, but elevated valuations make equities prone to a correction. Earnings growth broadening will translate into performance broadening – the S&P 493, Cyclicals, Value, Small and Mid are likely to outperform.

- Congress will pass tax cuts by end of 2025 producing a fiscal thrust of about 0.9% of GDP in 2026.

- Trump will count on that stimulus as a basis for slapping tariffs on leading trade partners.

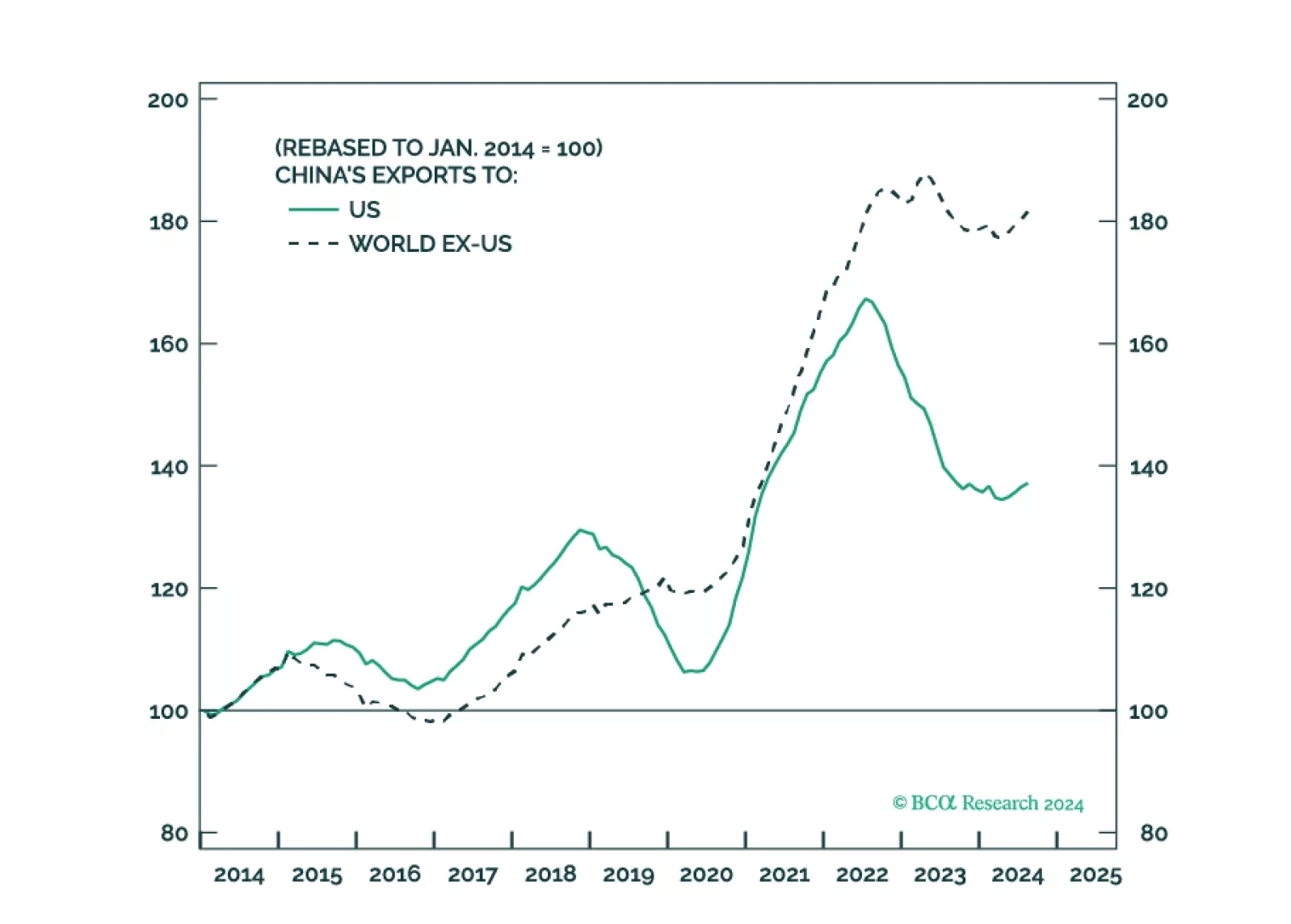

- China will retaliate against Trump and stimulate its domestic economy, while pursuing stronger trade ties with other countries. Europe will also retaliate.

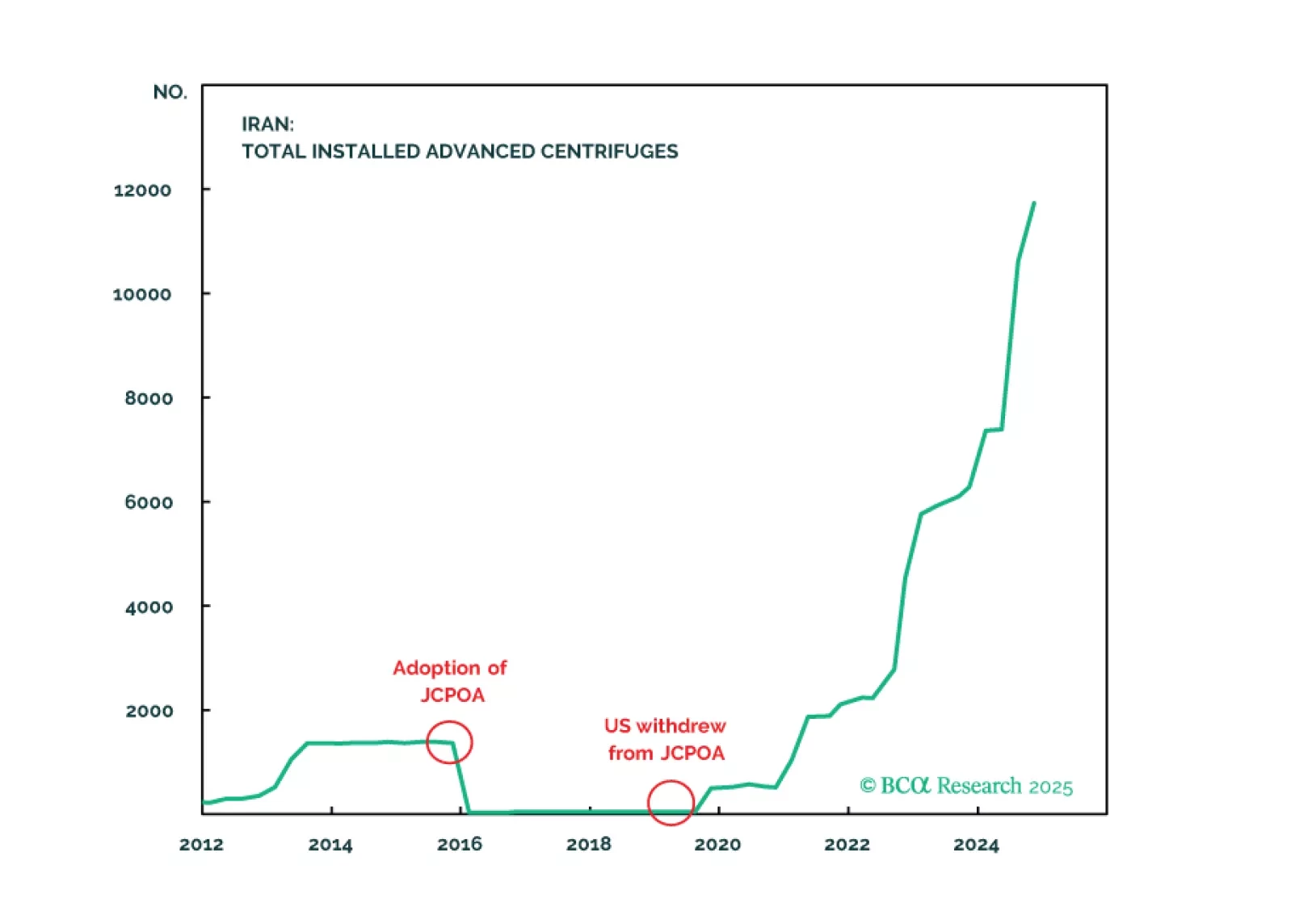

- Geopolitical risk will shift from Ukraine-Russia to Israel-Iran, where the conflict will continue to escalate until a crisis point is reached within 2025.