Energy

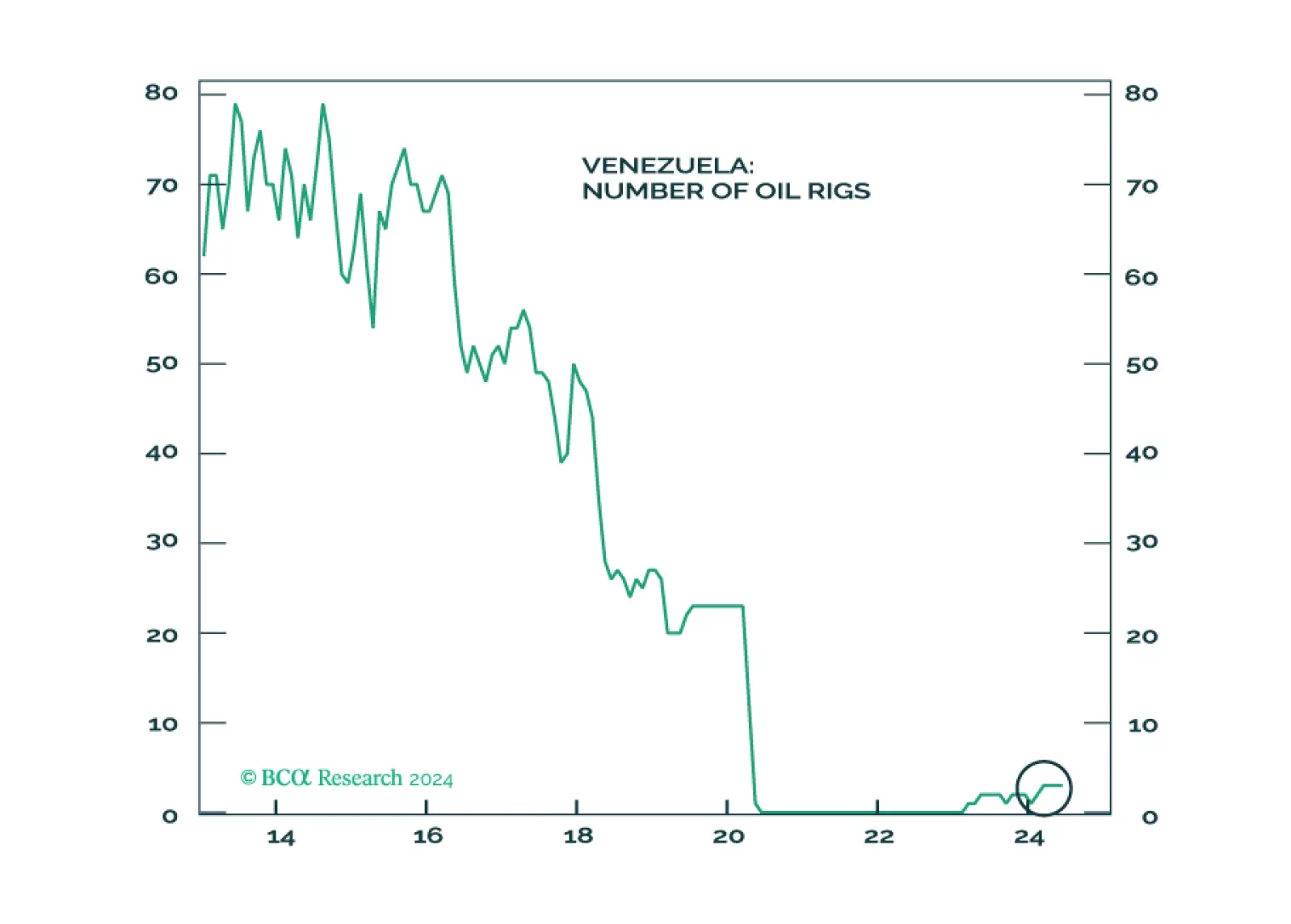

Oil markets will not be impacted by Venezuela in the near term, but by shocks from the Middle East. Maduro’s ability to stay in power in the short-term removes an avenue of oil supply relief. The same avenue is cut off if Trump is reelected. Geopolitical shocks in Venezuela could present tactical buying opportunities for Chile, Peru, and Colombia.

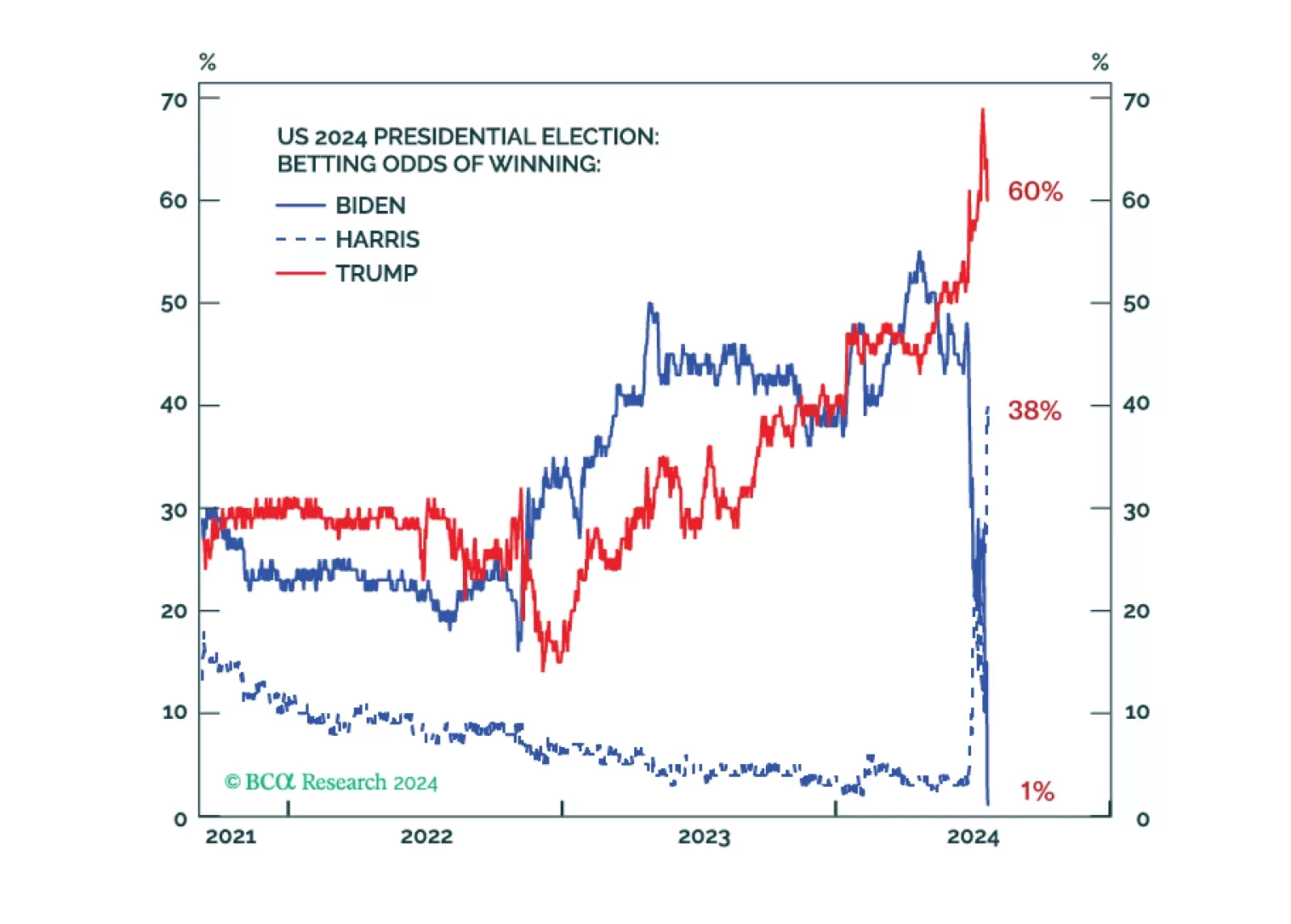

Investors should focus on growth concerns rather than the “Trump trade.” Bond yields will fall in the short run due to cyclically disinflationary economic slowdown, rather than rise in anticipation of a Republican full sweep and inflationary policies, which are likely but not yet a done deal.

Investors should overweight US assets and de-risk their portfolios in anticipation of a major increase in policy uncertainty and geopolitical risk surrounding the US election and its global ramifications.

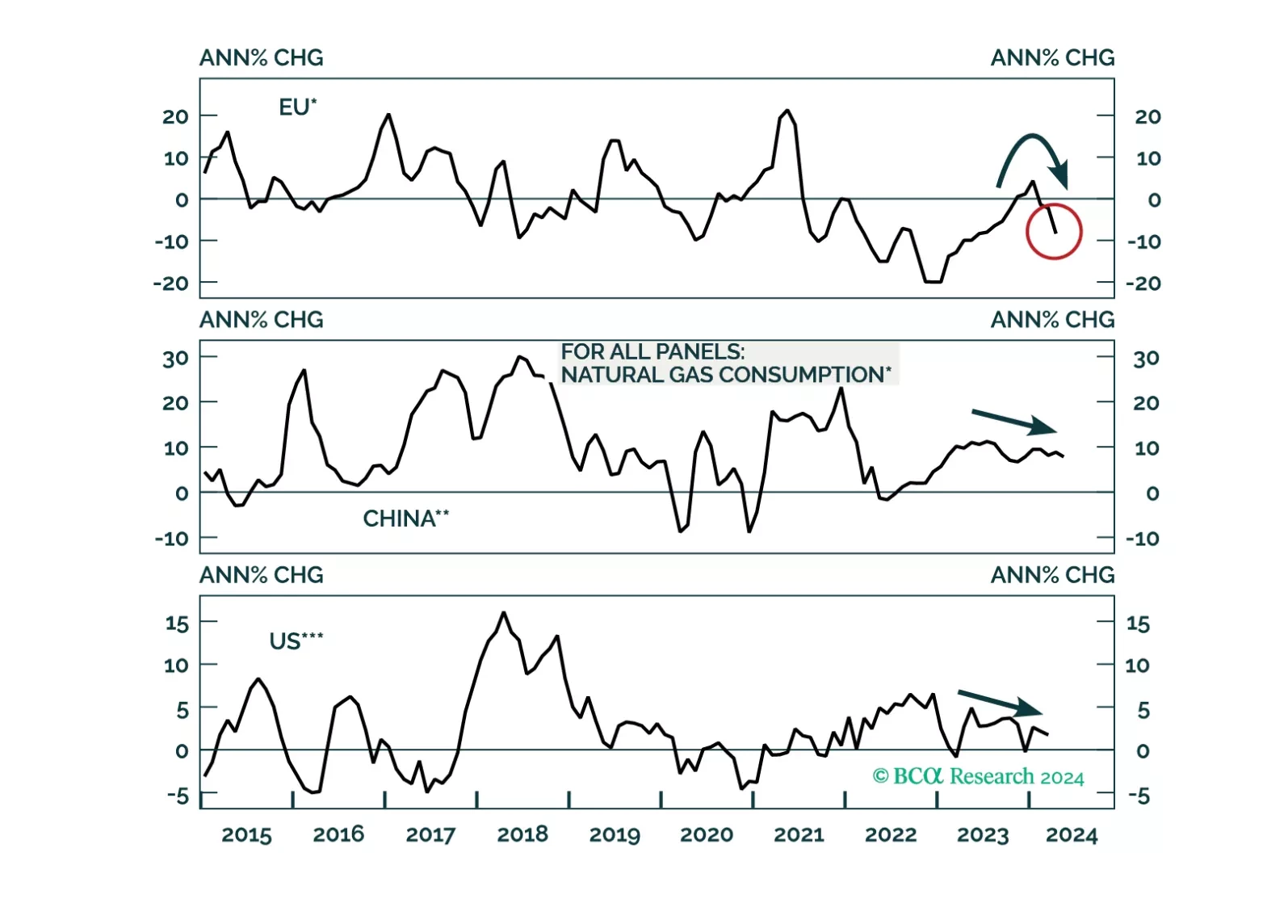

A global economic downturn will be a headwind for natgas prices over the cyclical horizon. Thereafter, LNG capacity additions will help keep the market in balance into the end of the decade. That said, Europe’s increased dependence on global LNG flows raises its exposure to market dynamics in the rest of the world. This will keep volatility elevated versus pre-Ukraine war.

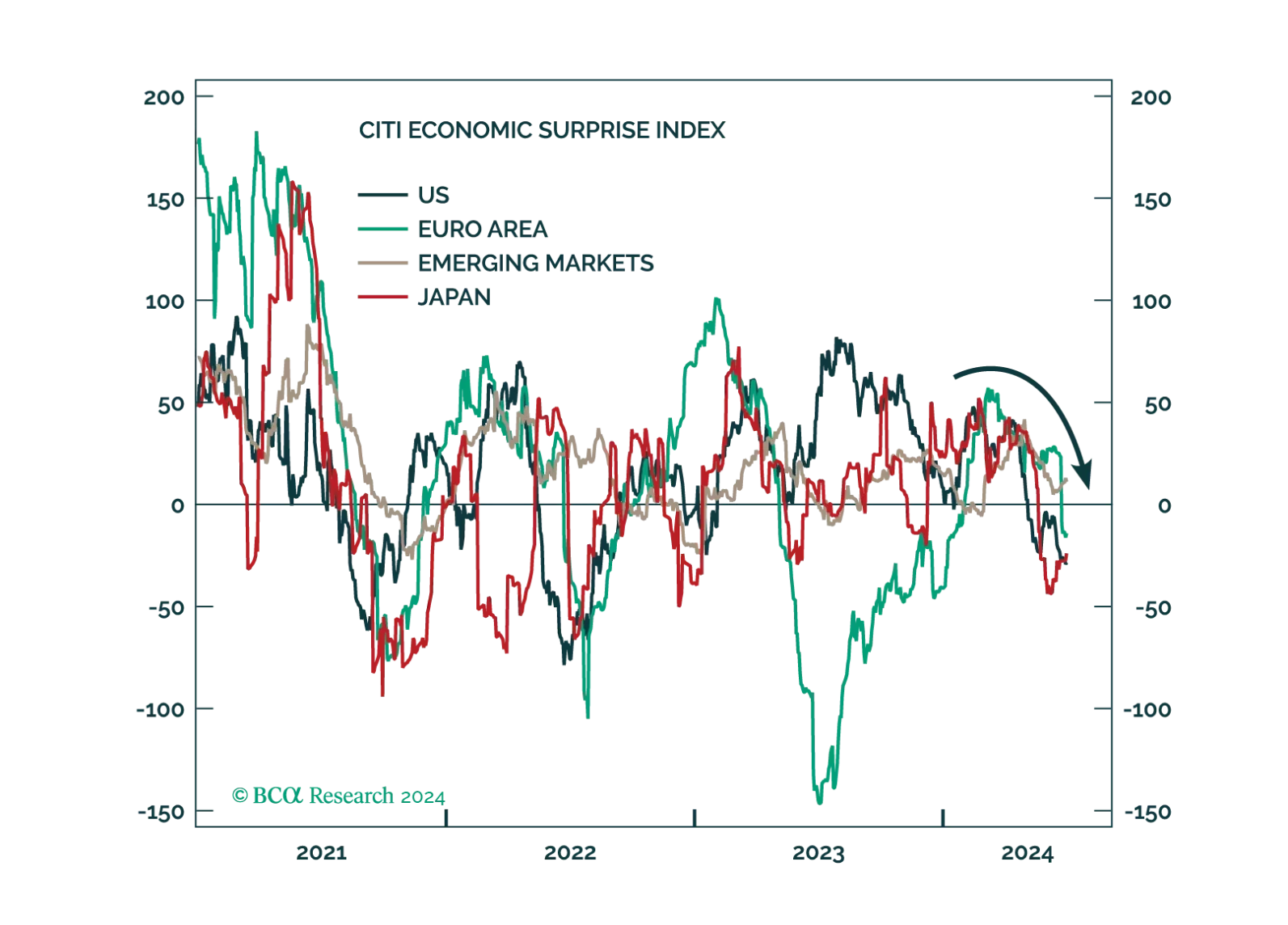

Concerns about the global economy have shifted from sticky inflation to faltering growth. Tight monetary policy is finally starting to bite. We suggest increasing portfolio defensiveness.

We close our overweights to Energy and Aerospace & Defense. The macroeconomic backdrop is deteriorating for Energy. As for A&D, the good news is already priced in.

Generative AI-related rally resumed in May. Much of the recent market gains are down to excess liquidity that was begotten by the massive pandemic stimulus, creating a dichotomy between multiple economic challenges and exuberant markets. The Fed is unlikely to step in to prevent the bubble as it is currently more worried about the near-term downside for growth than financial stability.