Equities

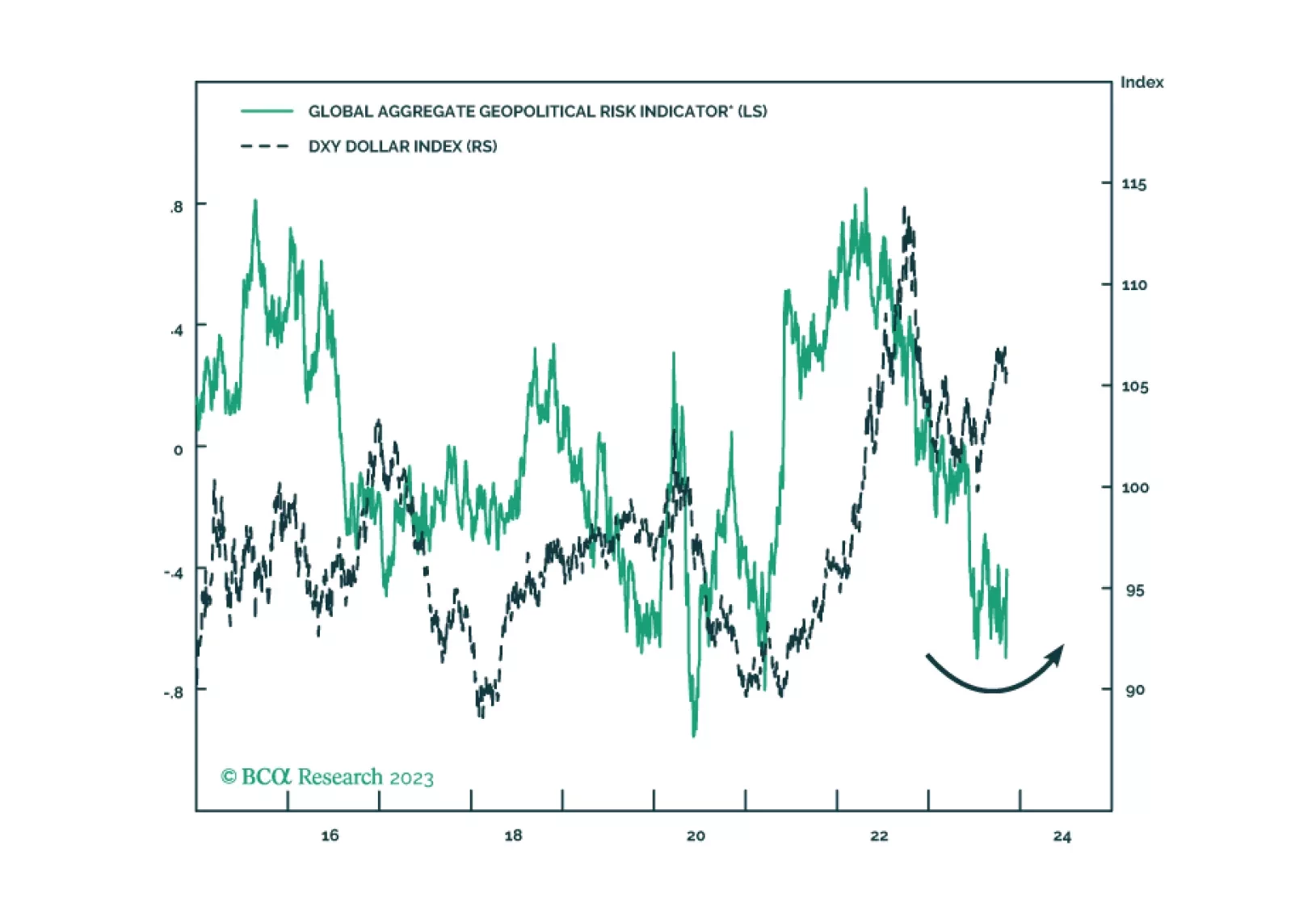

Amid a range of geopolitical narratives, what matters is that the US strategy of economic engagement with its rivals is failing, giving rise to a new strategy of containment that will reinforce the secular rise in geopolitical risk. Our market-based quantitative indicators of geopolitical risk are set to rise in the coming year.

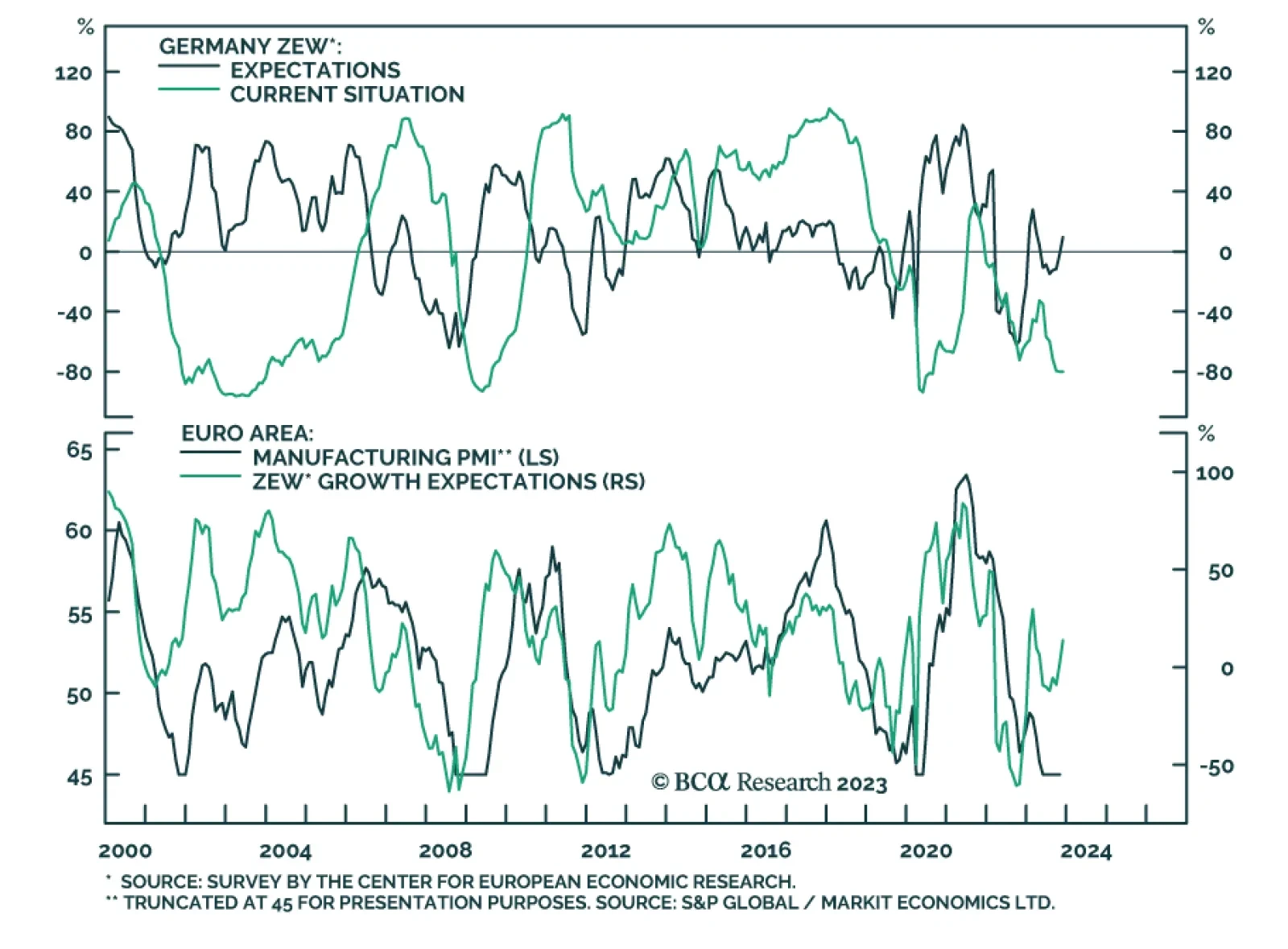

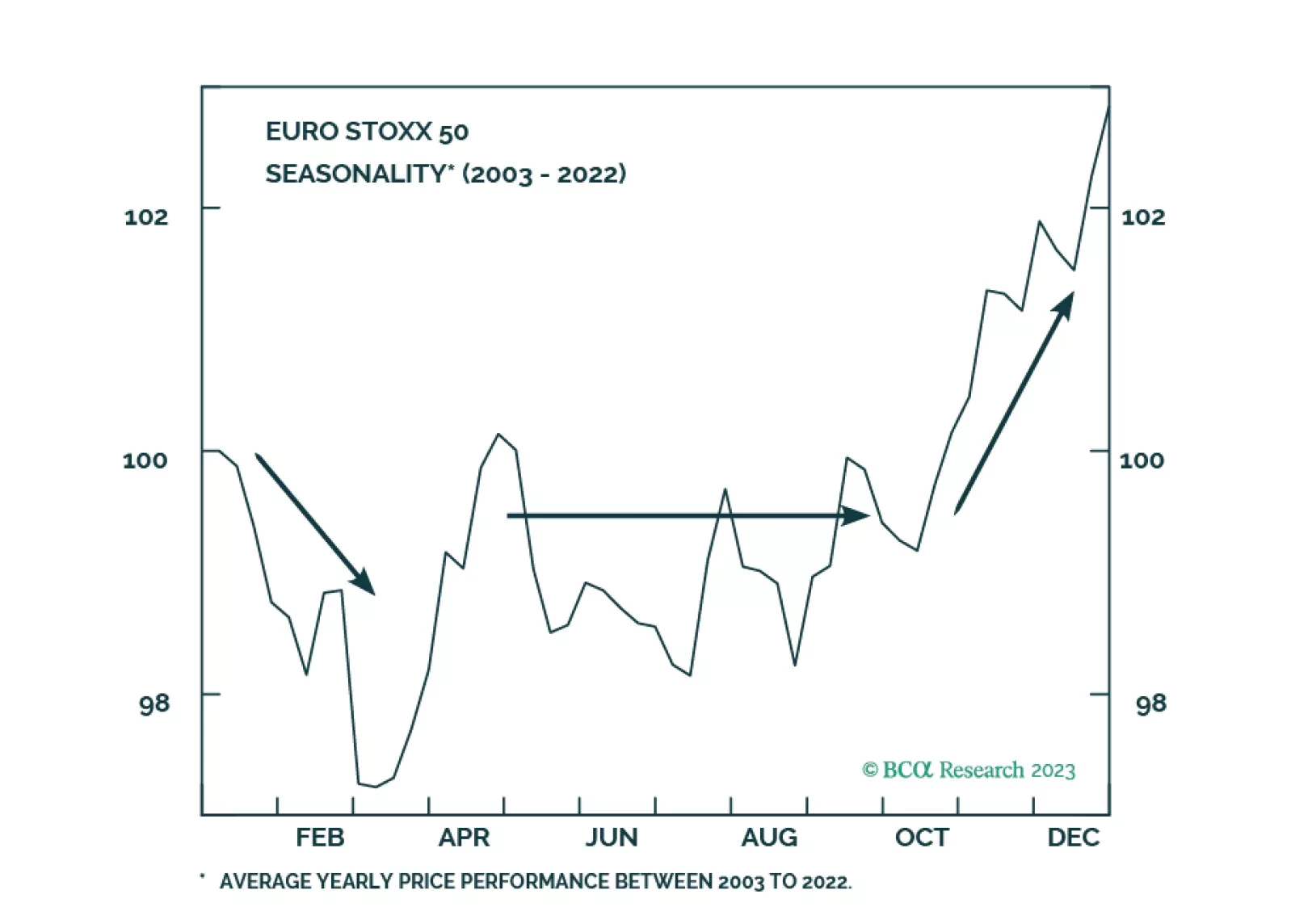

European markets have room to rebound in the coming weeks, however, a recession looms. What are the lessons from history that investors can use to position themselves under these conditions?

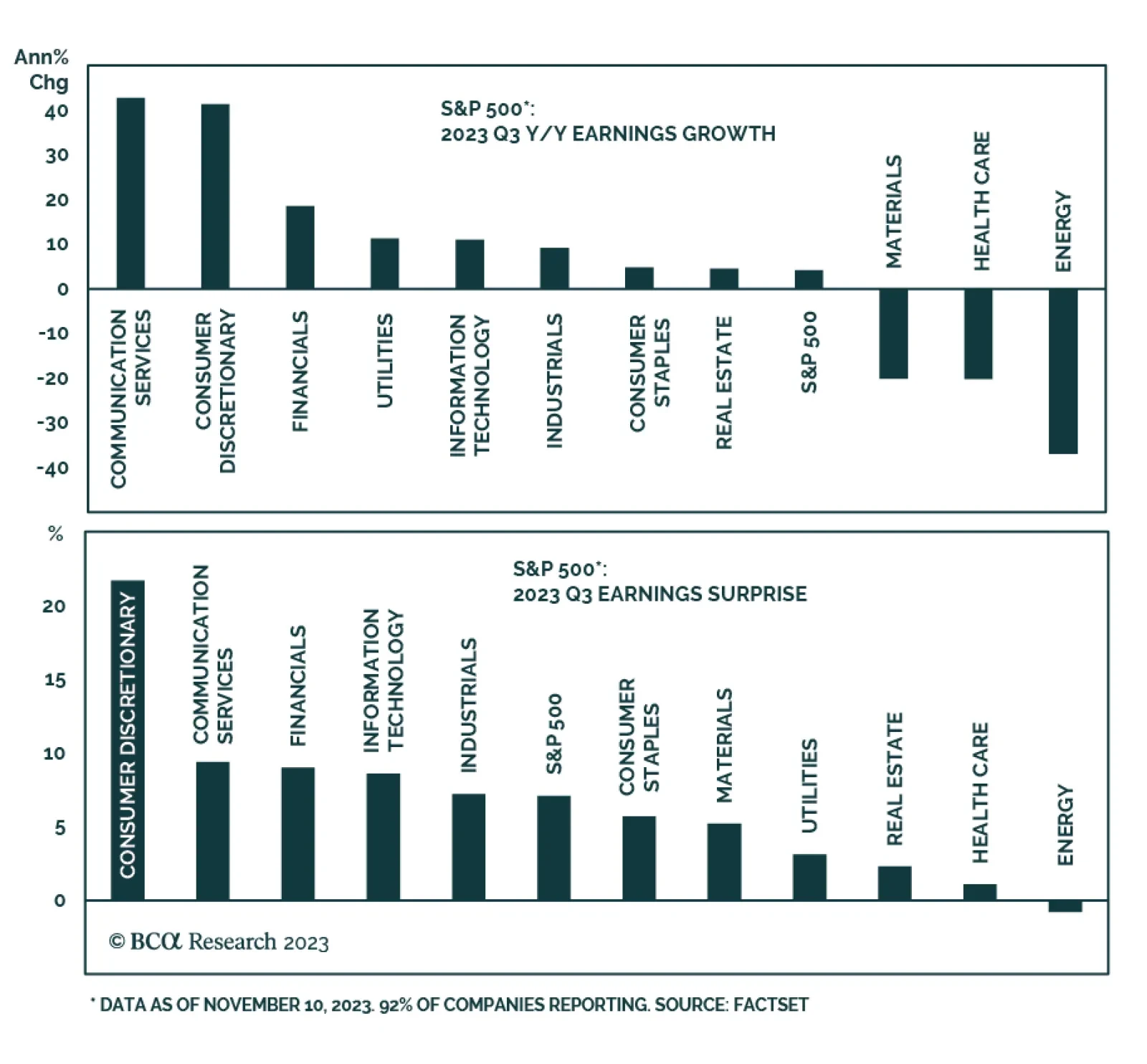

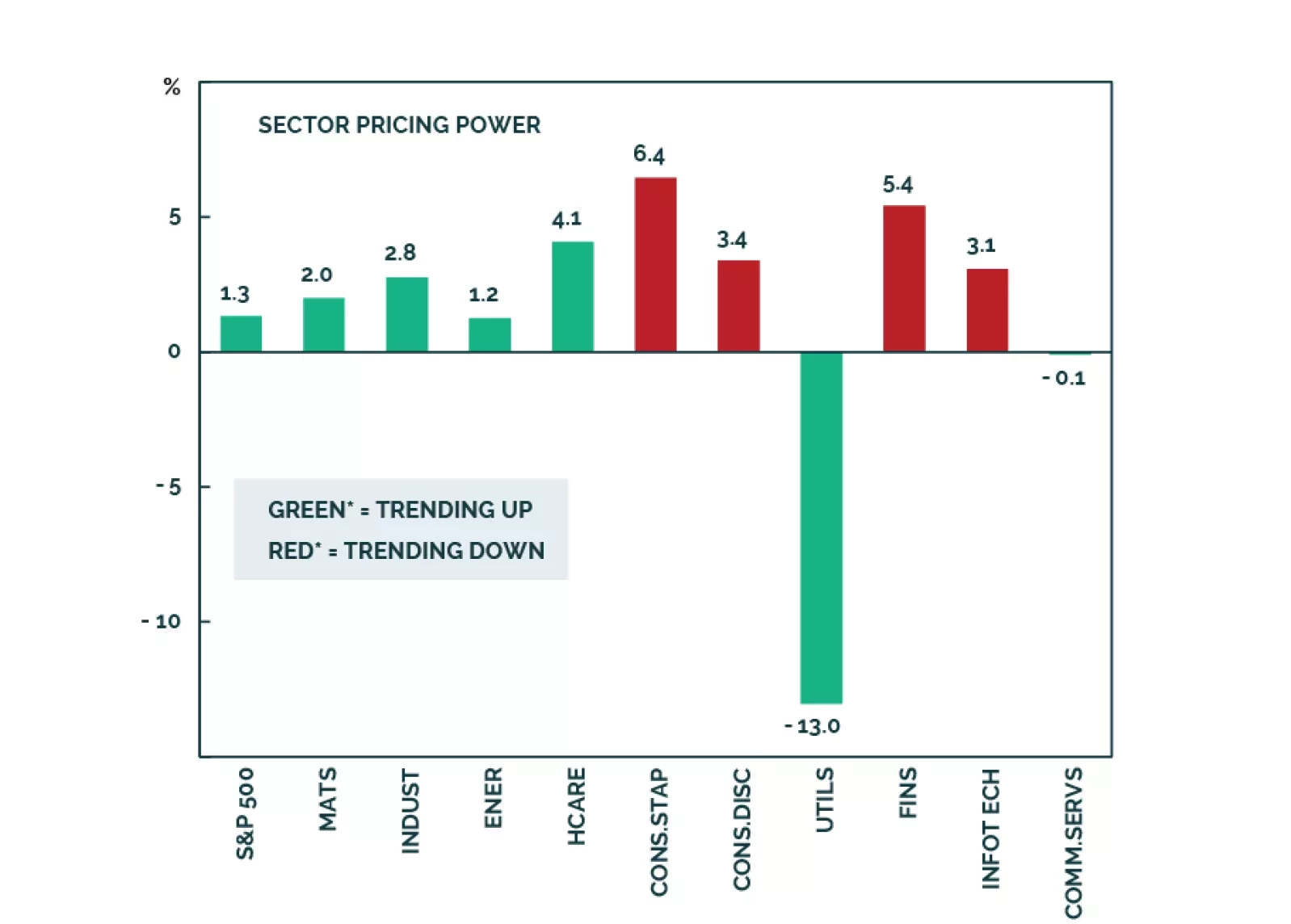

Q3 earnings commentary has been broadly positive, despite intensifying macro headwinds. Going forward, a negative growth outlook and geopolitical risks, are a threat to buoyant earnings expectations. We project that earnings growth for 2024 will move lower than currently projected - a negative for equities. This Santa Claus rally is unlikely to be the start of a new bull market.

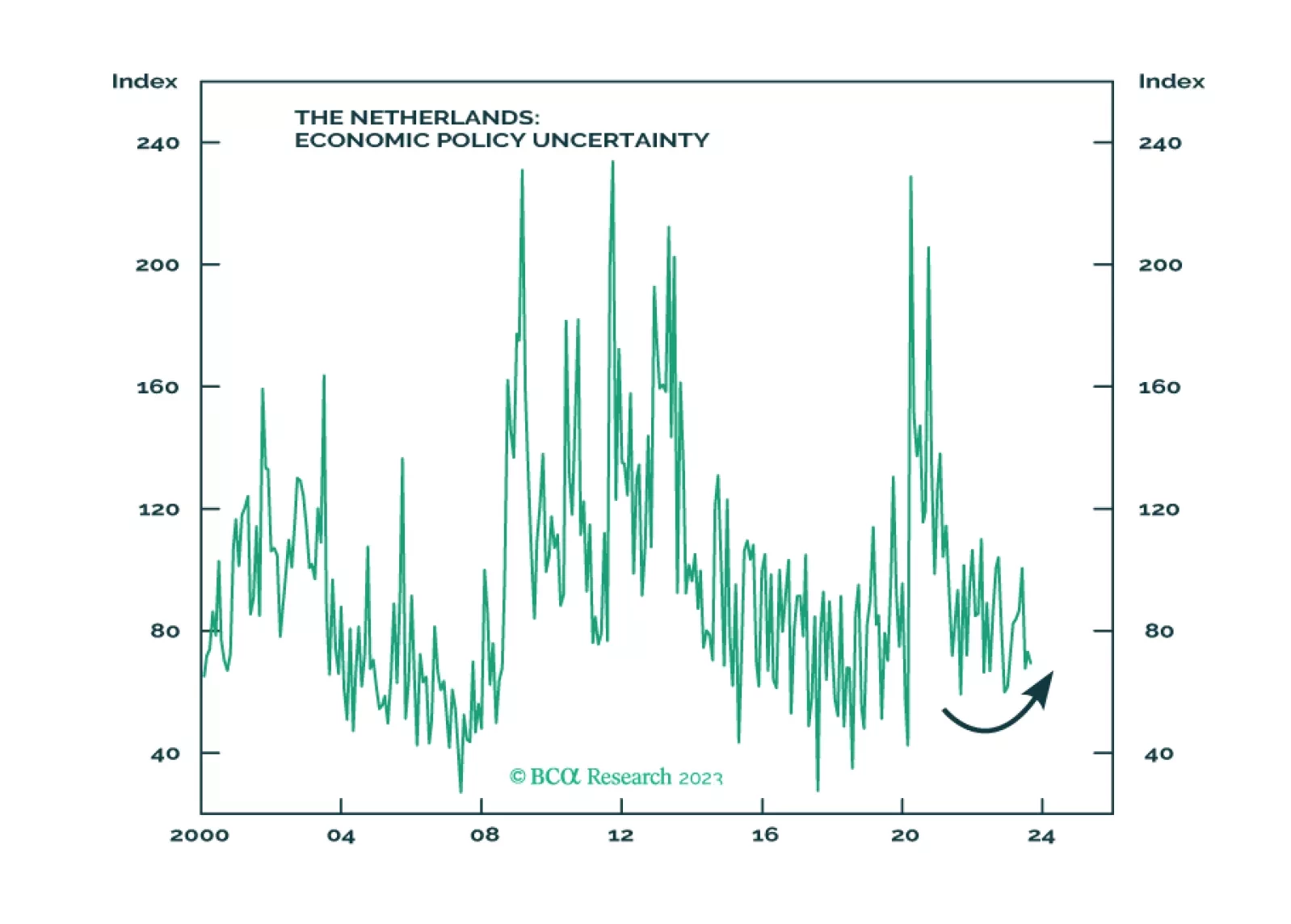

The Netherlands has a healthier and more stable economy and demography than its European peers. Investors should stay overweight developed European equities, including Dutch equities, relative to emerging European equities.