Equities

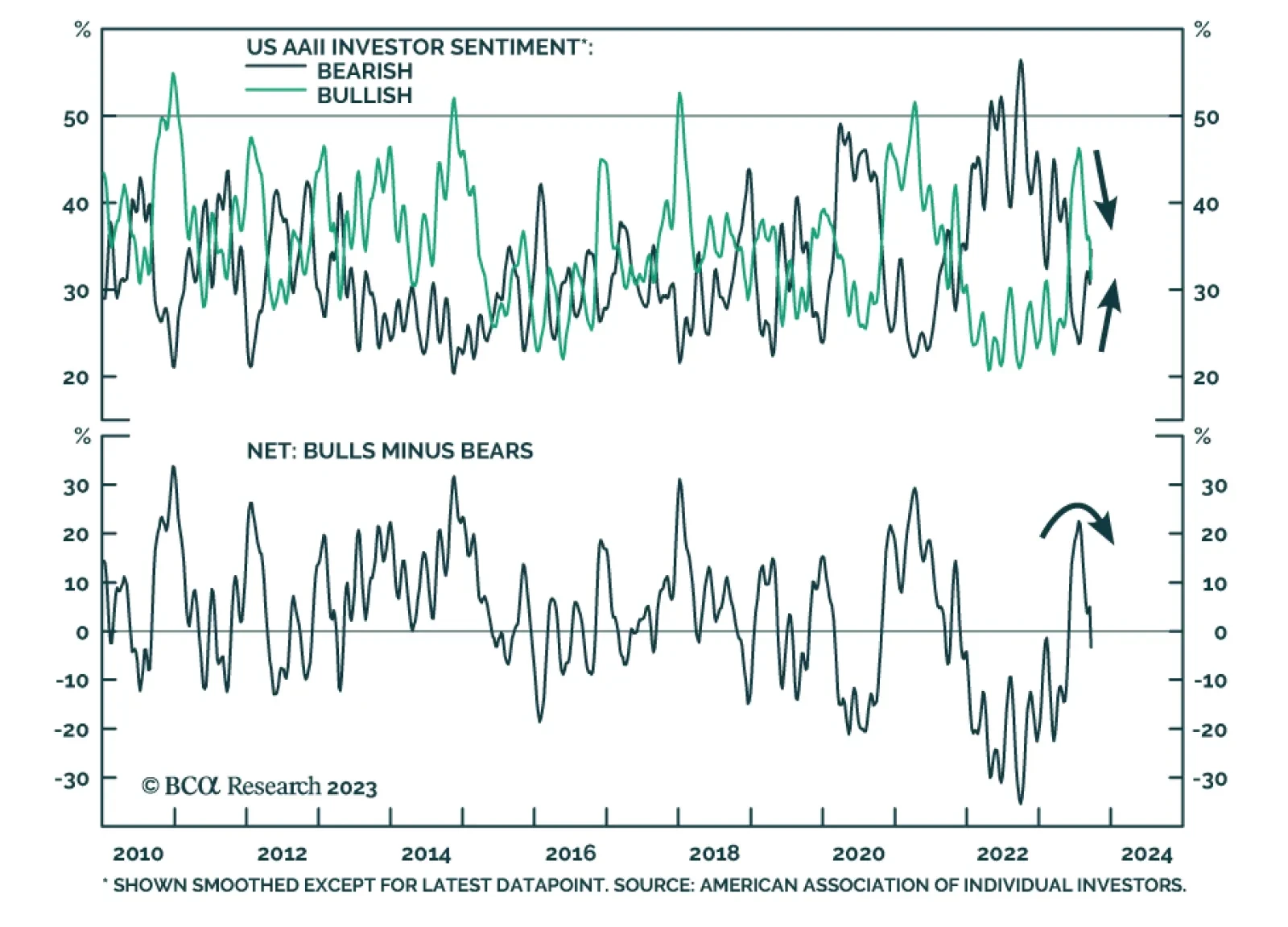

Bulls and bears have capitulated, and the majority of the clients surveyed expect a rangebound market in the near term. Our fair value PE NTM indicates that the S&P 500 is only modestly overvalued. The continued outperformance of the Magnificent Seven faces multiple hurdles. Meanwhile, fiscal spending is unlikely to create an impetus for another leg up in equity performance.

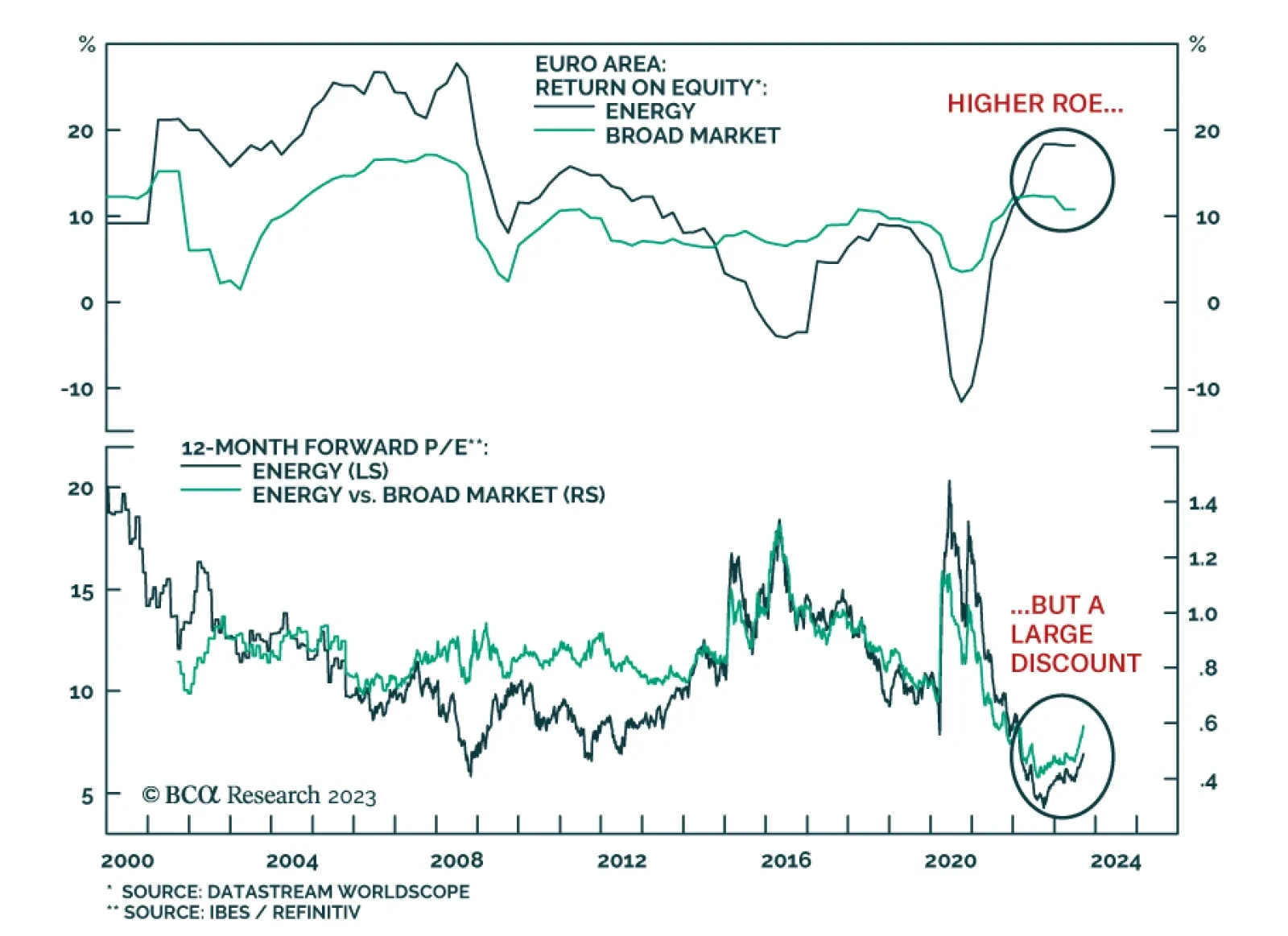

European stocks and the euro continue to weaken; soon, they will test the bottom of their recent trading range. Which sectors can protect investors against this downdraft?

US fiscal, monetary, and foreign policies are unlikely to deliver any dovish surprises for investors in Q4, due to the impending government shutdown, persistent inflation, and instability among OPEC+ and China.

Emergency pandemic fiscal and monetary policy measures buffered households and nonfinancial corporate businesses in ways that have acted to lengthen the lags between monetary policy changes and their effect on the economy. We believe, however, the extended lags are merely delaying the recession, not cancelling it. We expect to downgrade equities on a tactical basis from equal weight to underweight soon.

The global downturn will be shallower than it was in 2008 and in 2020 but will last for longer. The primary reason for a more prolonged downturn is that policymakers in the US, Europe, and China will be reluctant to proactively and aggressively stimulate. The combination of rising oil prices, an appreciating US dollar, and mounting US bond yields constitutes a triple whammy for US share prices.

The biggest misunderstanding in the markets right now is that to keep expected inflation well-anchored at 2 percent, inflation must <i>undershoot</i> 2 percent for some time. This implies that interest rate futures curves are mispriced, and that the probability of a ‘soft landing’ is lower than assumed. Plus: we show that the rally in oil has become fractally fragile, and recommend a tactical underweight.

The Chinese economy will not recover without significant “irrigation-style” stimulus. The latter is still unlikely for the time being. Dim economic fundamentals justify lower valuations of Chinese equities. Lingering deflationary pressures entail even lower interest rates, which is bearish for the RMB.