Equities

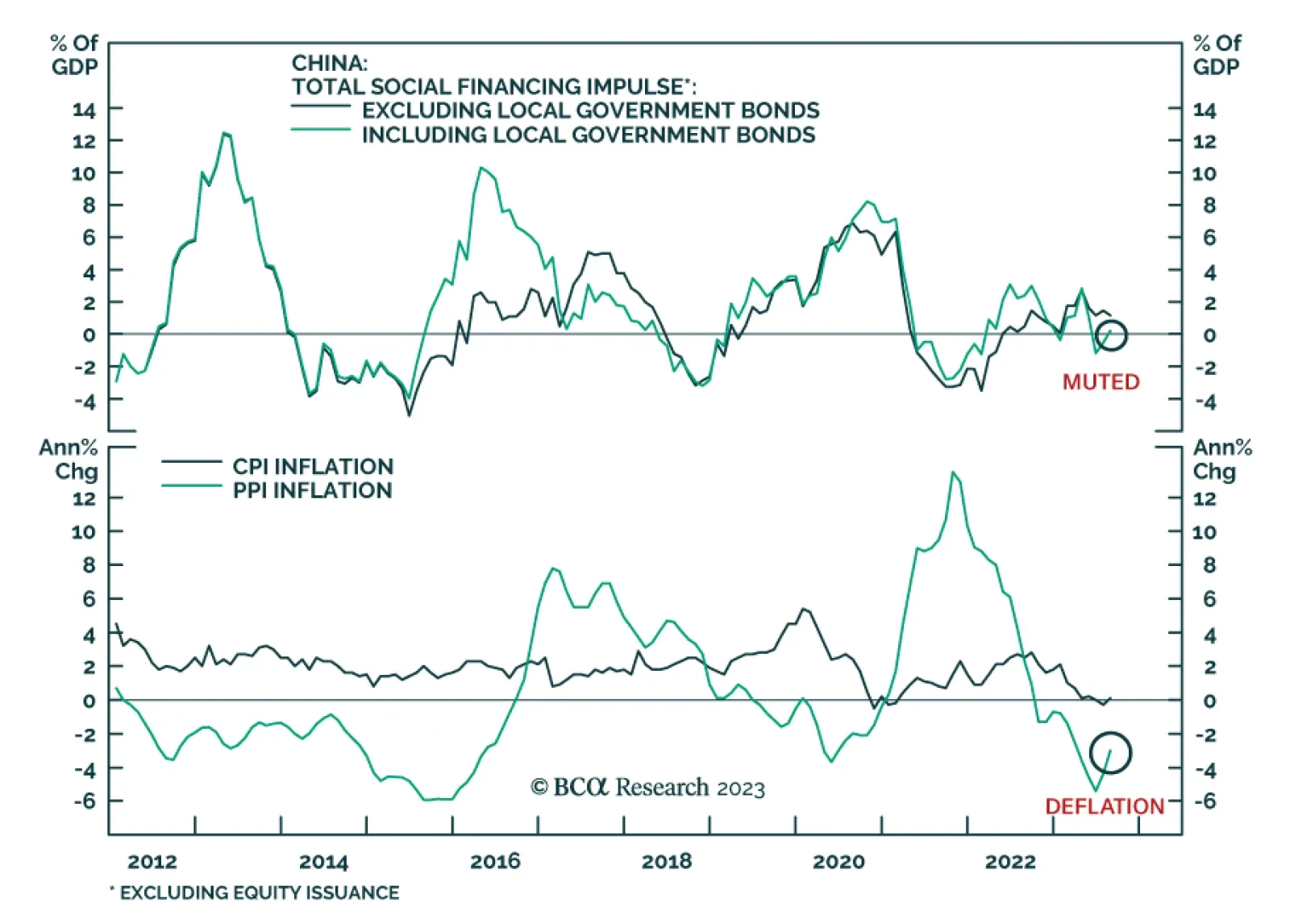

The Chinese economy will not recover without significant “irrigation-style” stimulus. The latter is still unlikely for the time being. Dim economic fundamentals justify lower valuations of Chinese equities. Lingering deflationary pressures entail even lower interest rates, which is bearish for the RMB.

The ECB is done lifting interest rate for the cycle and its next move will be a cut next year. Yet, European rates will climb even higher in the second half of the decade.

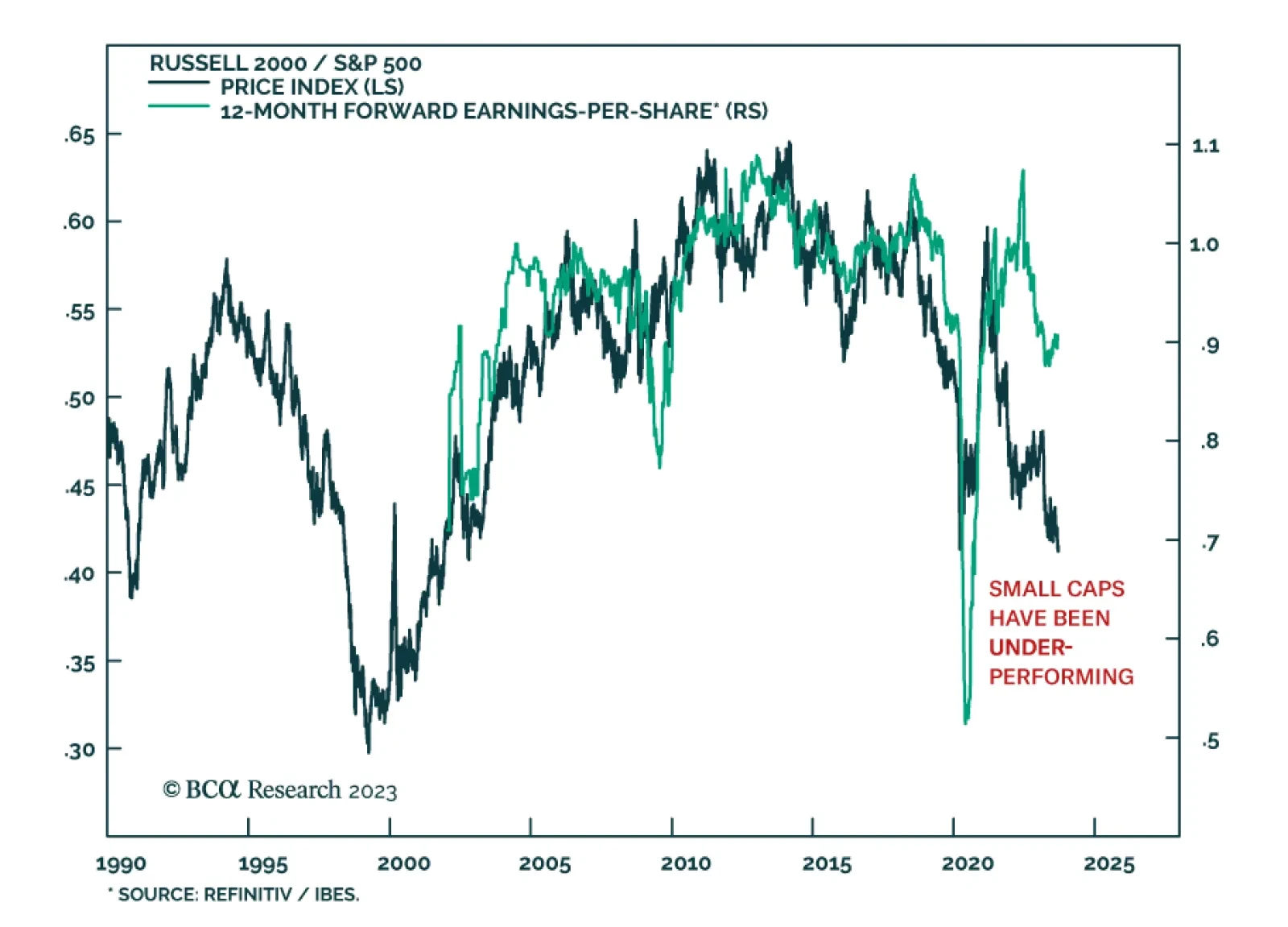

While we are sympathetic to the view that the Fed could temporarily achieve a soft landing, we are skeptical that it could stick that landing for very long. Stocks could strengthen into year-end, with small caps potentially leading the charge. But the rally will fizzle out next year as the global economy begins to sink into recession.

This Special Report is a timely reprise of a speech that I gave at the London School of Economics on our understanding and misunderstanding of generative AI. In neurological terms, generative AI has a ‘super-neocortex’ which means that it can thrash humans in abstract thinking, or IQ. But crucially, generative AI does not have a ‘limbic system’ which means that it will lag well behind humans in emotional intelligence, or EQ. I hope you find the speech insightful and provocative, especially on how we might have completely misunderstood human intelligence and super-intelligence, and the economic and societal implications for the coming decade.

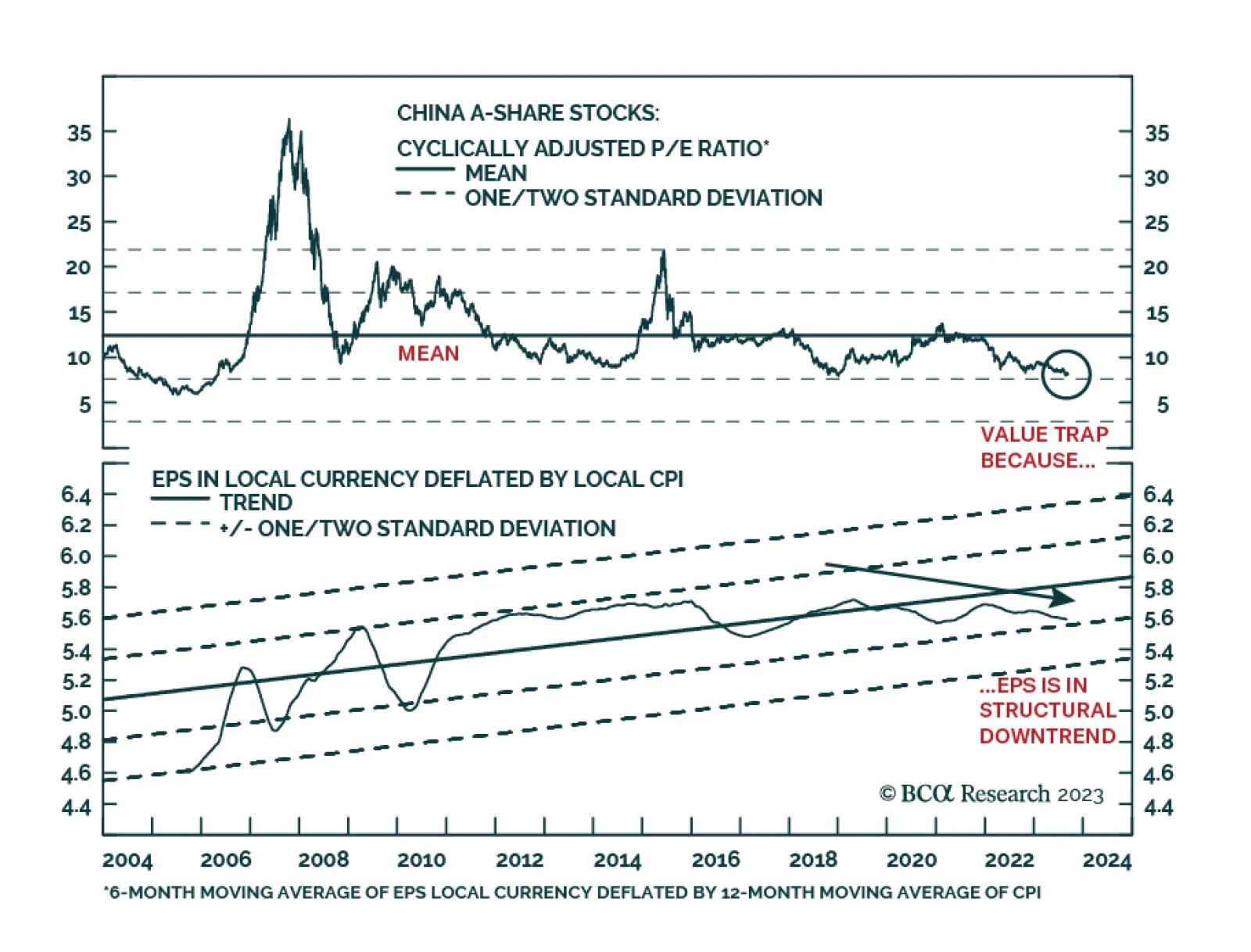

While Chinese stocks have low valuations and are oversold, their attractiveness is dampened by uncertainties in the magnitude of stimulus and the dismal outlook for corporate profits in the next six to nine months.

Real wages are set to rise in CE3 economies with implications for their asset markets and currencies. Of the three, Polish assets and the zloty are the most vulnerable.