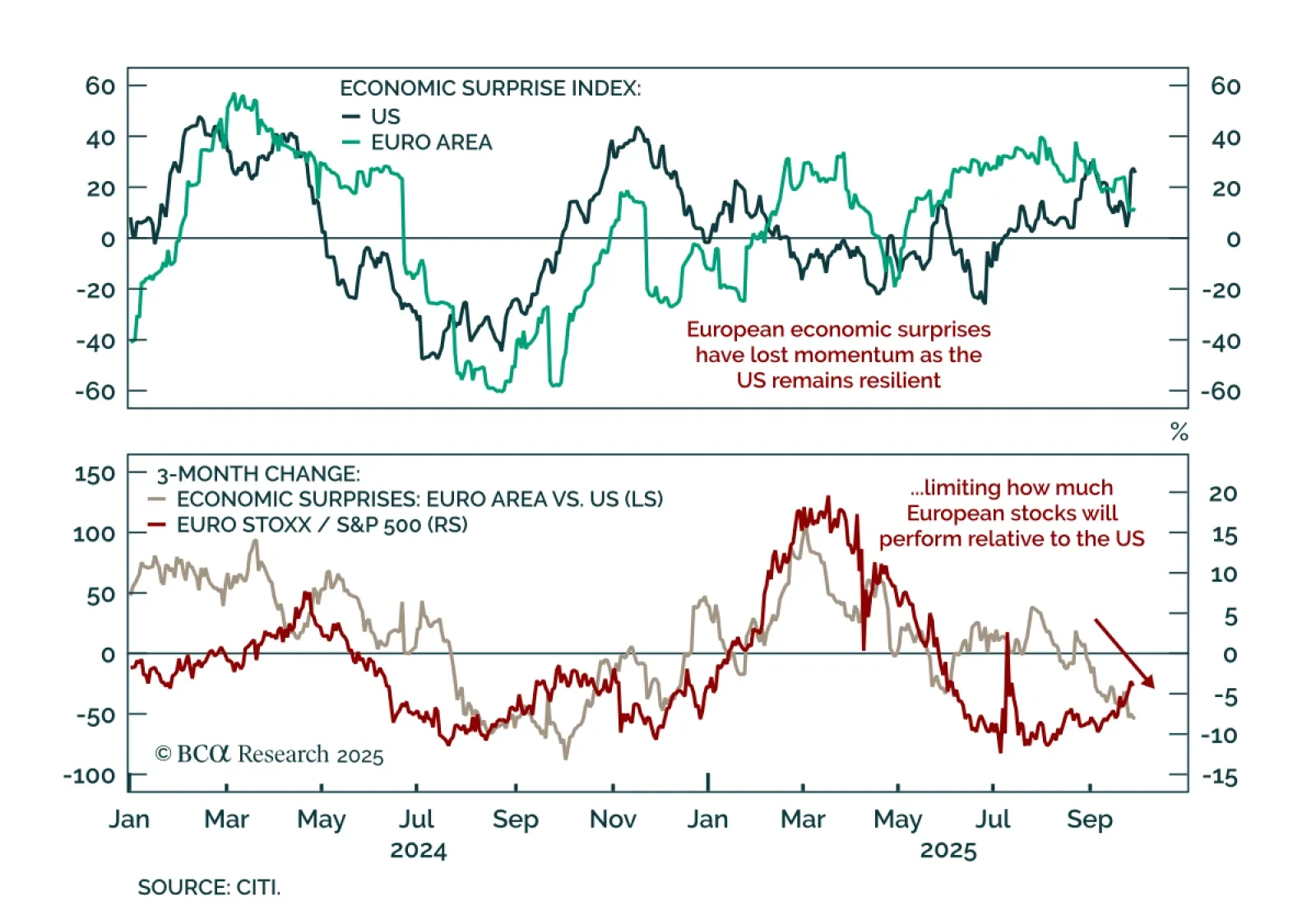

Equities

In this update, we apply our Macro Surprises framework to equities for the first time. Overall, the message is broadly consistent with our current equity views: Investors should favor Eurozone equities and continue to overweight cyclical sectors relative to defensive ones.

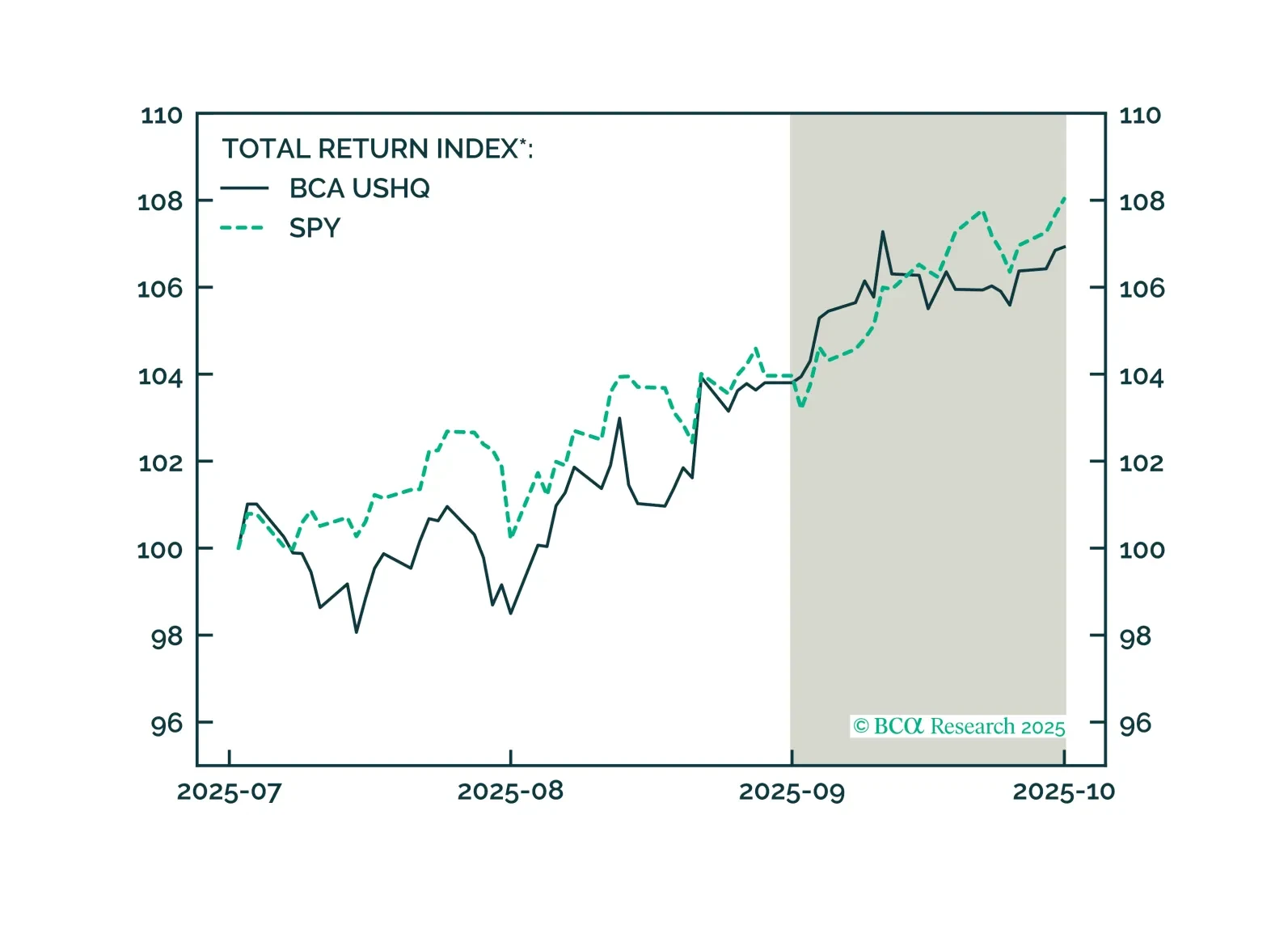

The US High Quality (USHQ) portfolio underperformed its benchmark through September, returning 3.01%, whilst its SPY benchmark returned 3.91%. However, our US High Quality SMID (USHQ SMID) portfolio continues to show strength, with another solid month of performance. The portfolio returned 2.69%, outperforming its MSCI US Mid Cap benchmark by 169bps.

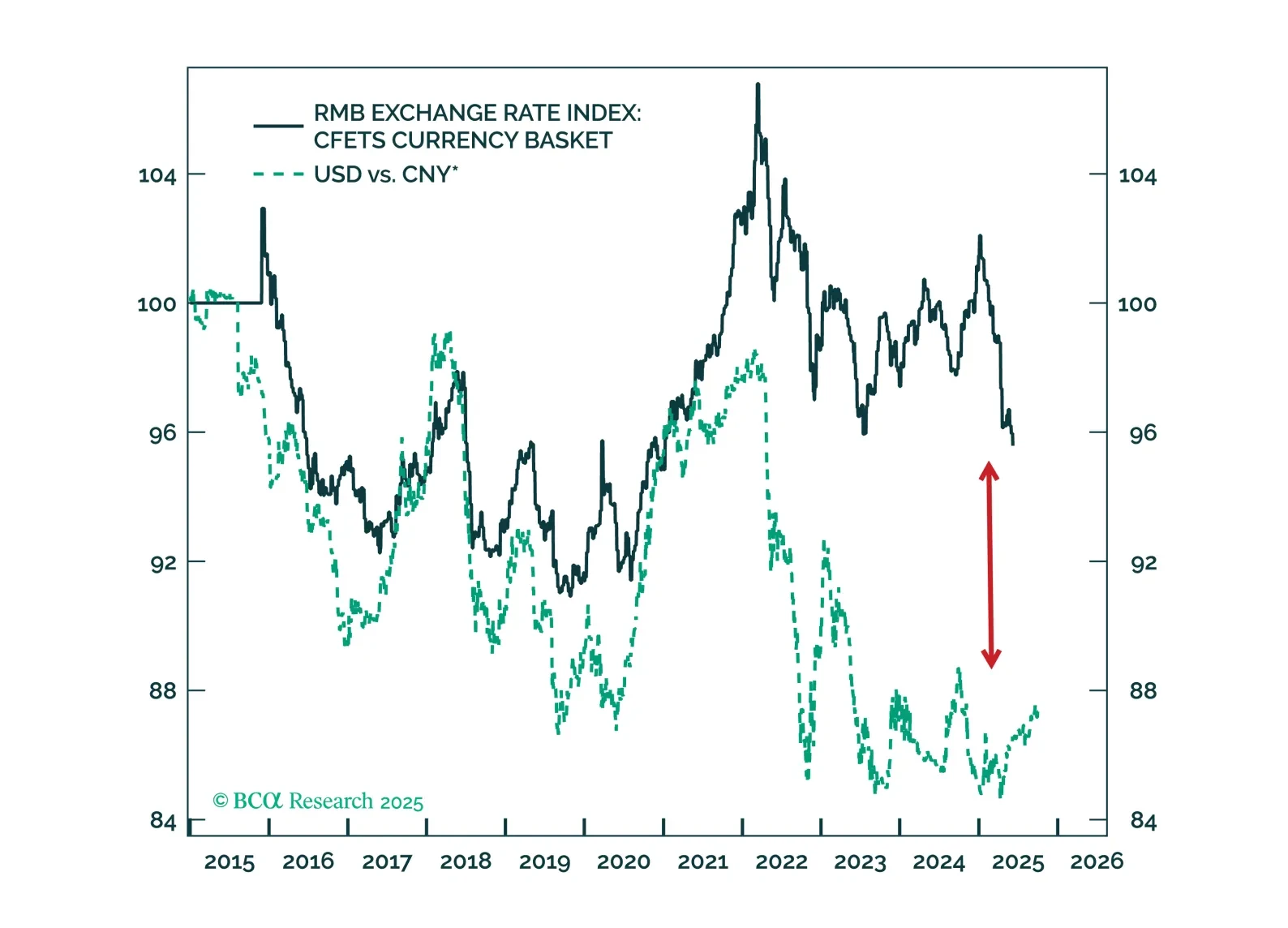

The CNY/USD has room to appreciate both cyclically and structurally, while nominal yields on China’s long-duration government bonds are set to fall. This combination supports Chinese equities.

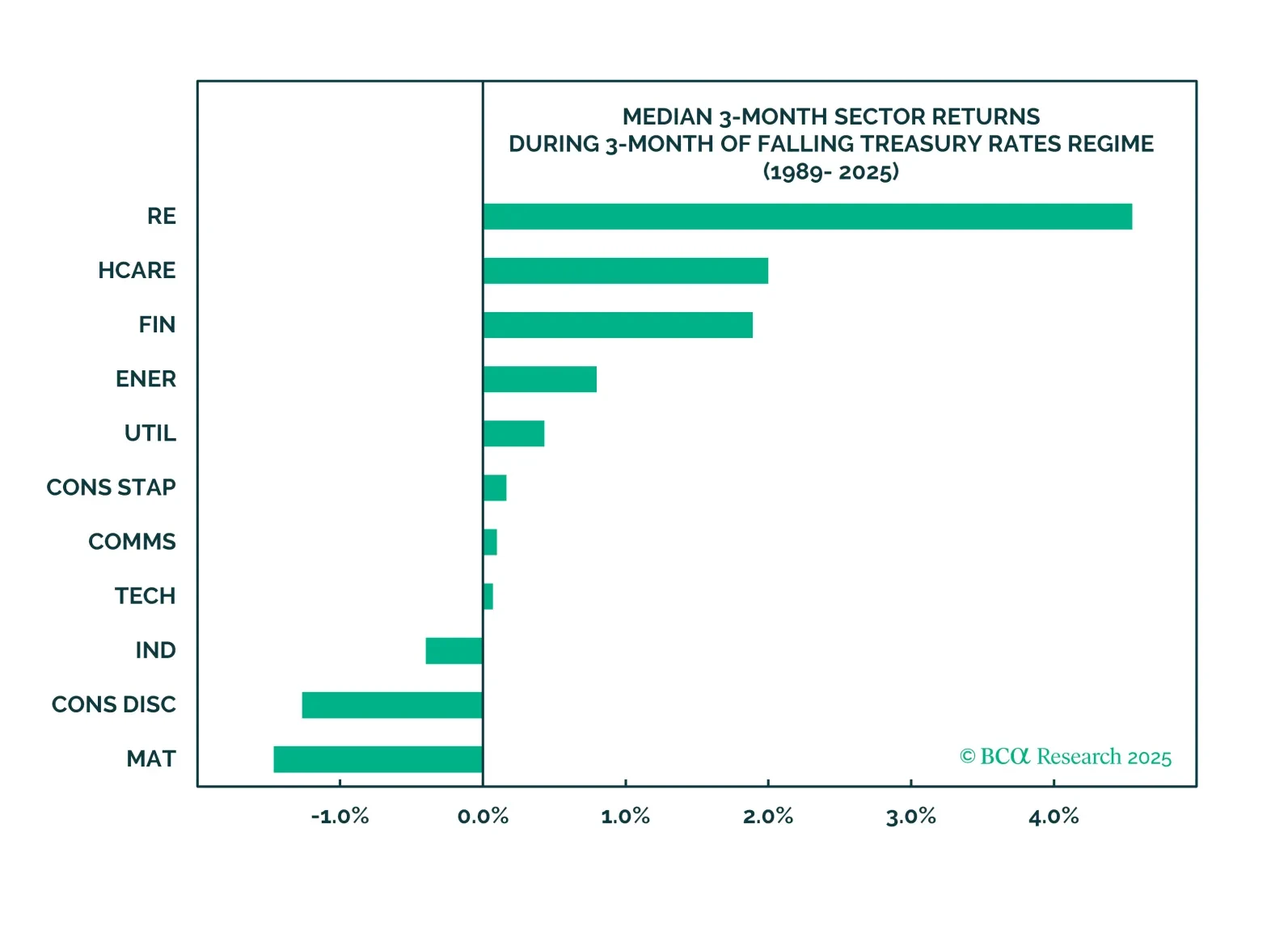

Real Estate performance is contingent upon the Fed rate-cutting cycle. Yet, we worry about a hawkish Fed surprise and are closing our overweight in the sector. We also recommend a granular approach to subsector selection.