Equities

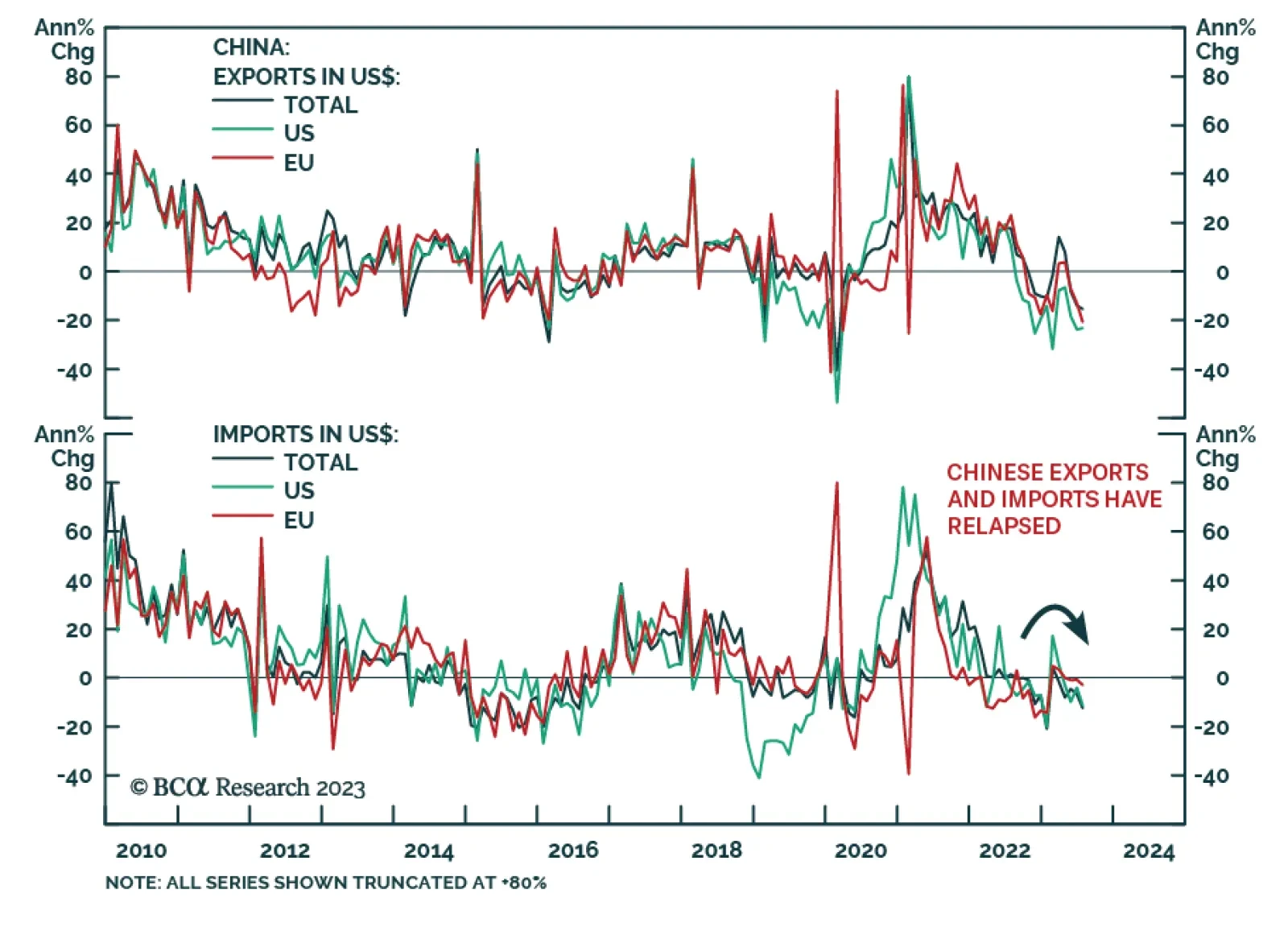

China has generated 41 percent of the world’s economic growth through the past ten years, al-most double the 22 percent contribution from the US. Now that the Chinese growth engine is failing, we explain why it is arithmetically impossible for world growth to maintain the altitude of the past few decades. And we discuss an important investment implication.

The global economy will not enjoy an “immaculate disinflation” but will suffer a very maculate one due to China’s growth slowdown and restrictive monetary policy in the developed world. Investors should stay overweight low-beta assets.

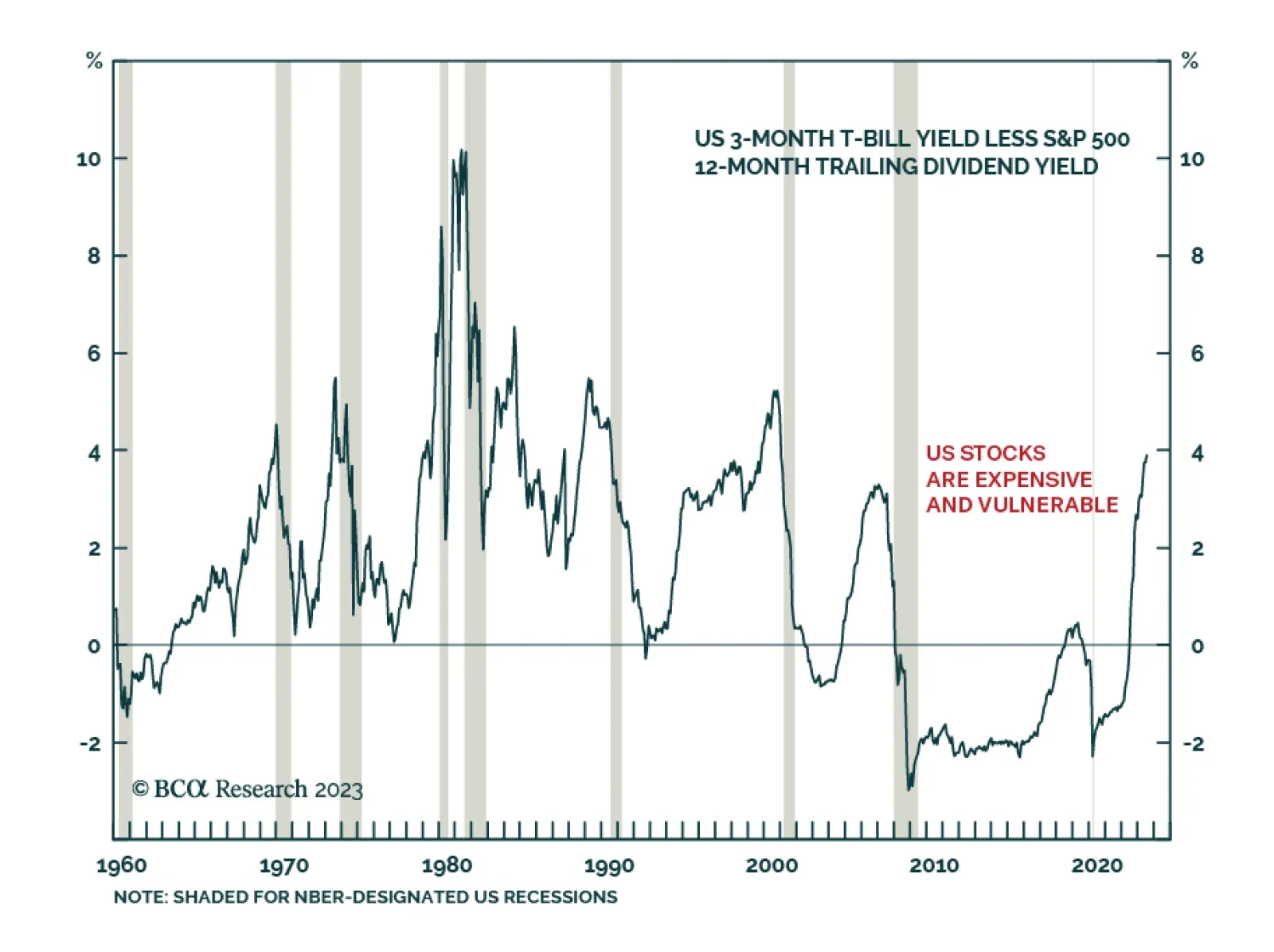

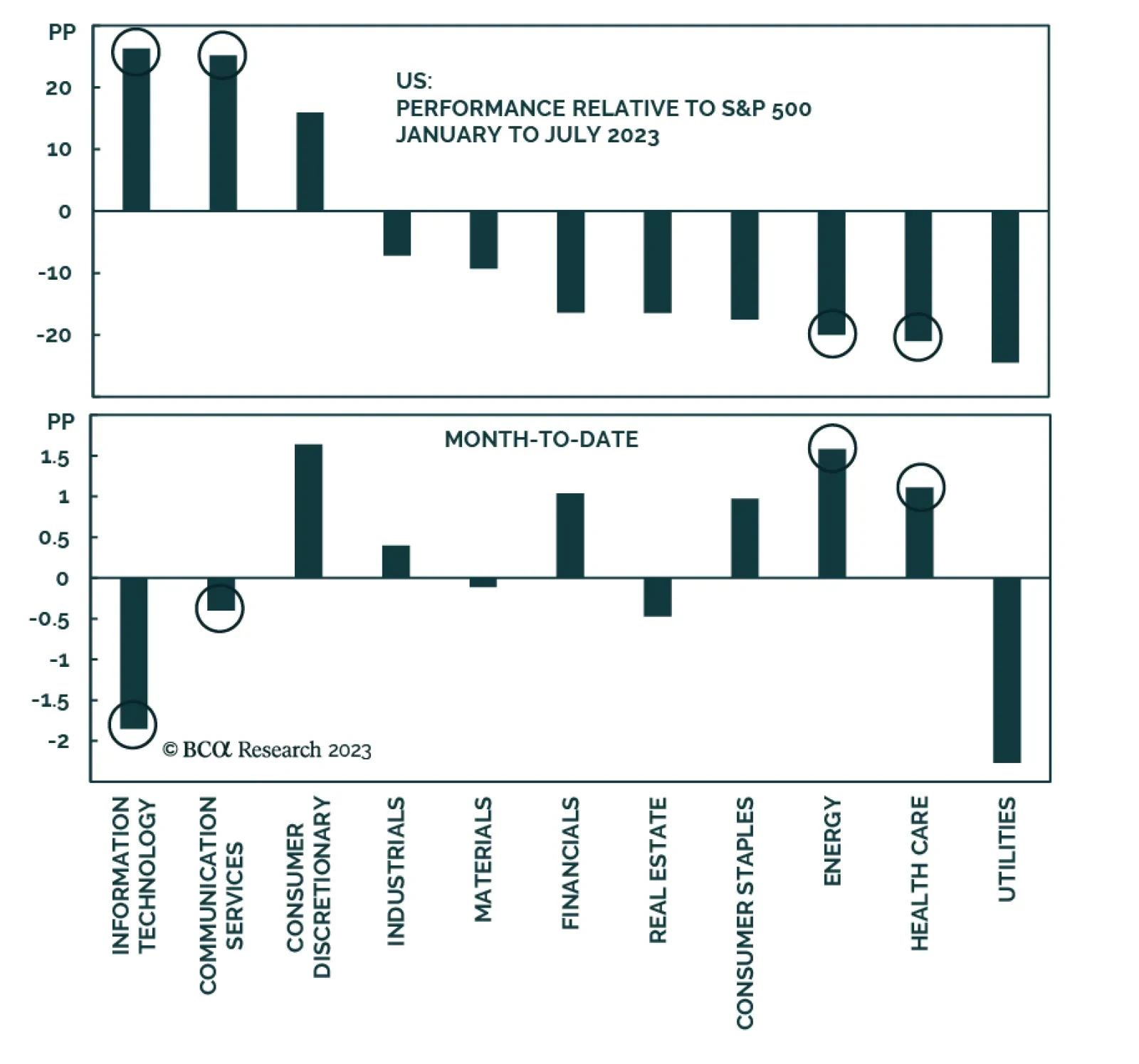

The S&P 500 rally broadened in July, lifting this year’s laggards. Surging long yields are altering the macroeconomic backdrop, as the market absorbs that monetary policy will stay restrictive for a long time. Yet, a move down in yields is more likely than a move up over a tactical horizon. Q2 earnings were better than expected but investors were unimpressed – the good news is already priced in. The market is overvalued and is close to being overbought, which makes it vulnerable to disappointment.

August offers an opportunity to review our key views. European growth is turning the corner and inflation is improving, but does it guarantee an imminent breakout in European stocks?

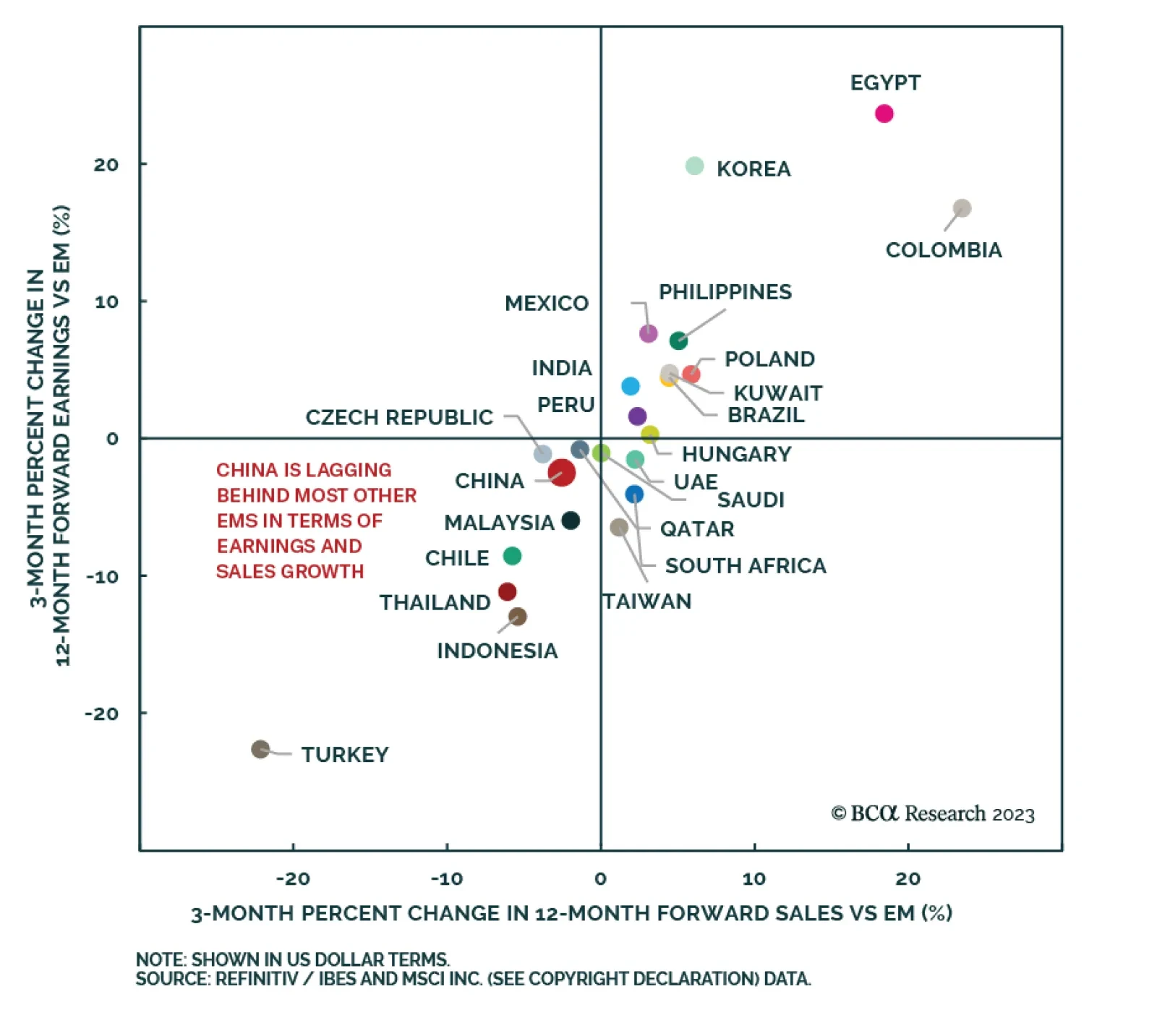

China’s extremely high savings rate is the real culprit behind its current economic woes. The authorities have been slow to stimulate the economy, and the risks of “Japanification” have increased. For now, the fact that China is exporting deflation is not such a bad thing. However, if global recession risks were to flare up again, a lethargic Chinese economy would be a cause for concern. Chinese stocks are quite cheap but lack a clear catalyst to move higher. Favor EM markets where earnings and sales estimates have been moving up lately.