Equities

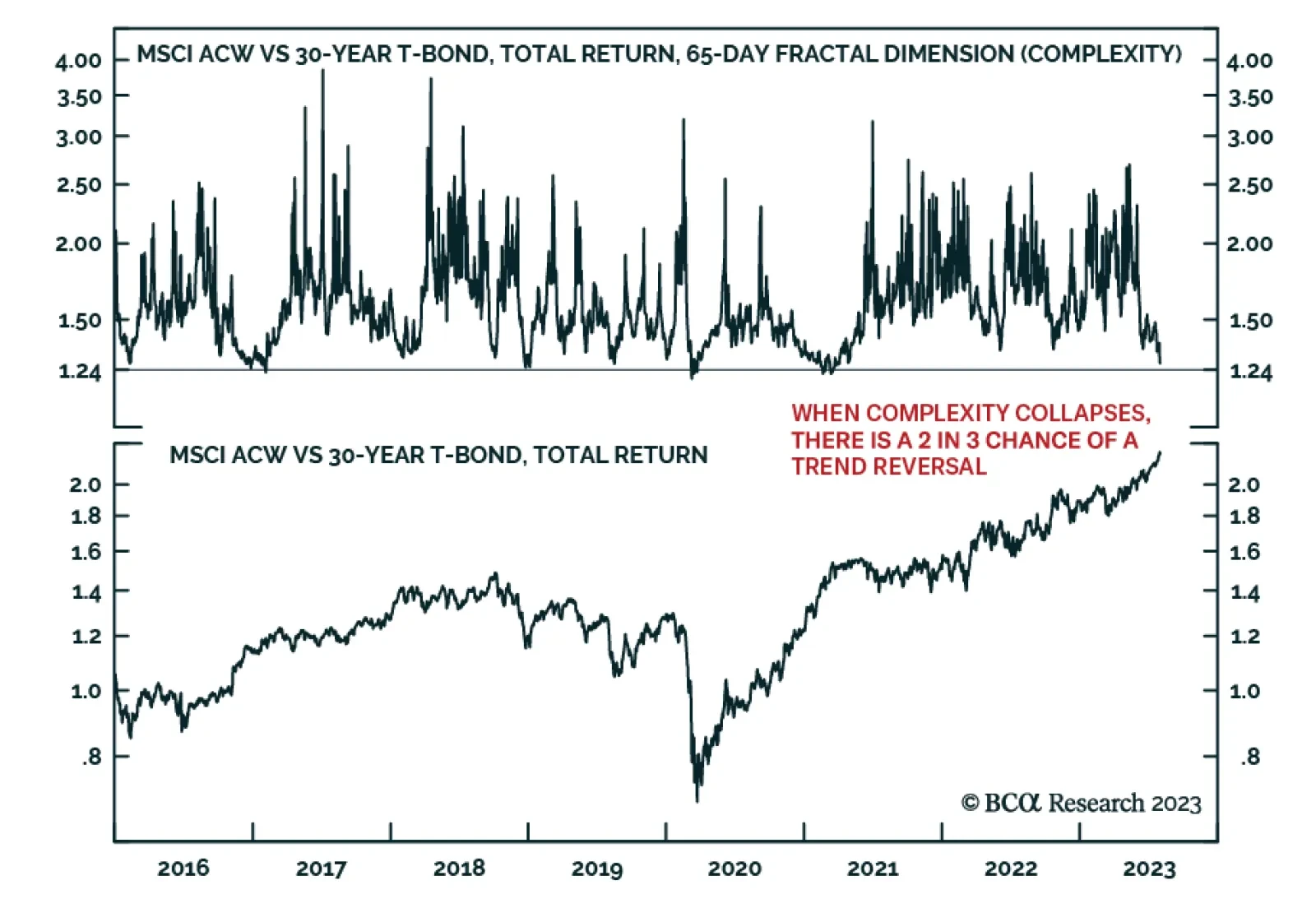

The recent ‘Goldilocks’ stock market rally is predicated on the hope that developed countries really can kill inflation without killing their economies. But one important warning sign suggests that the rally has gone too far too fast, and is vulnerable to…

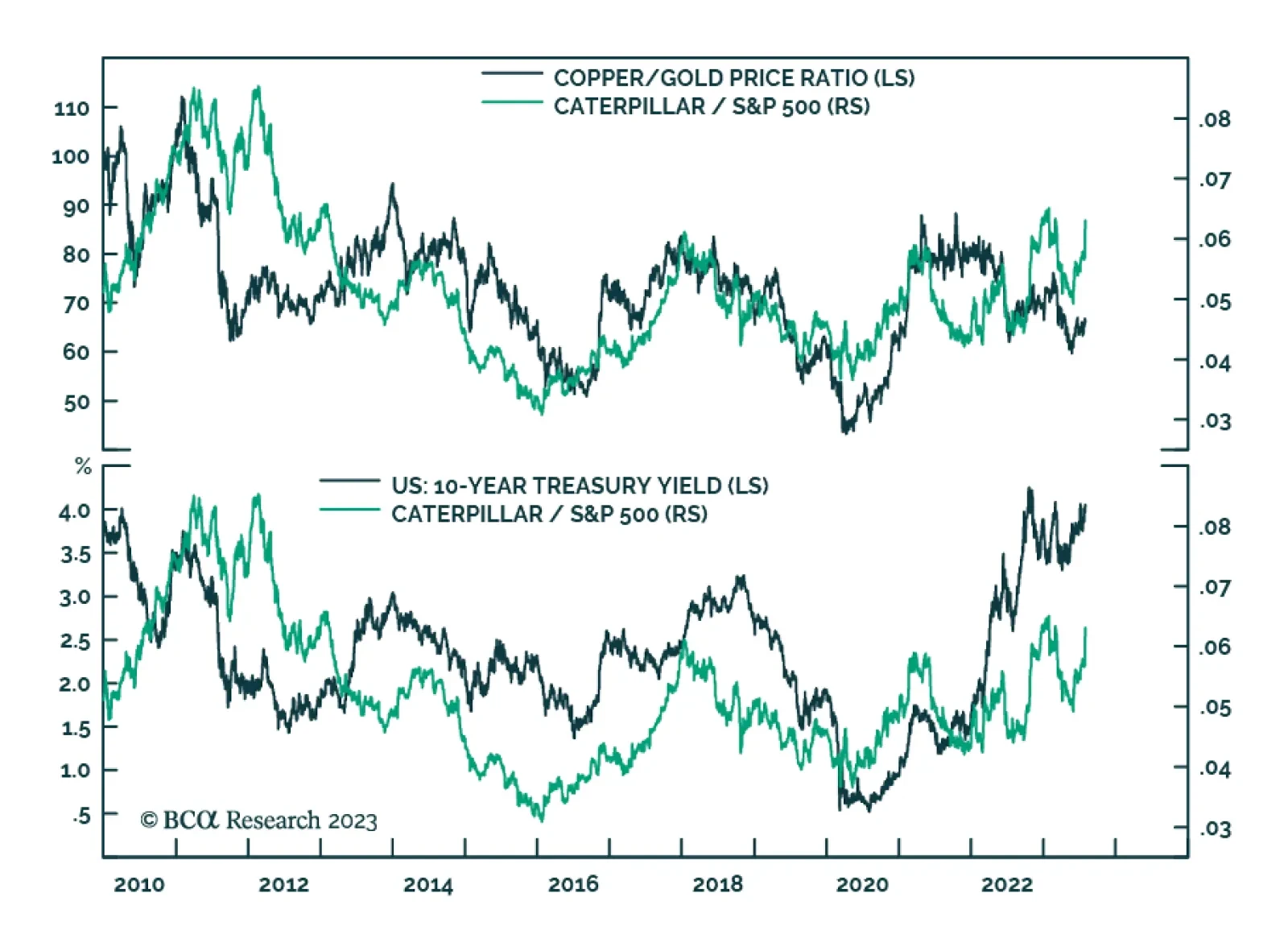

Caterpillar’s Q2 earnings results released on Tuesday beat consensus estimates by a wide margin. Second quarter profit of $2.92 billion ($5.67 per share) came in well above expectations of $2.38 billion ($4.46 per share). The stock jumped to an all time high…

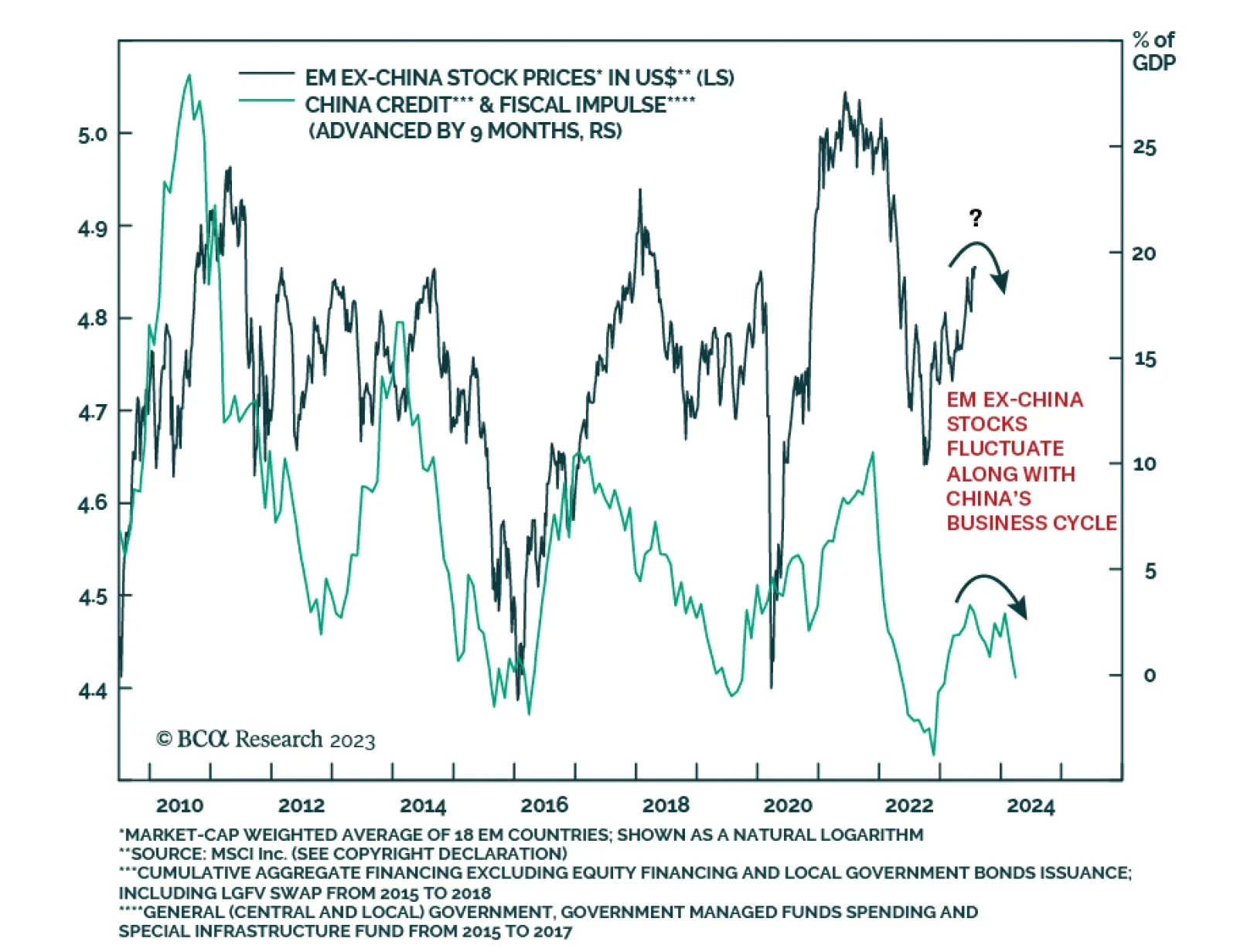

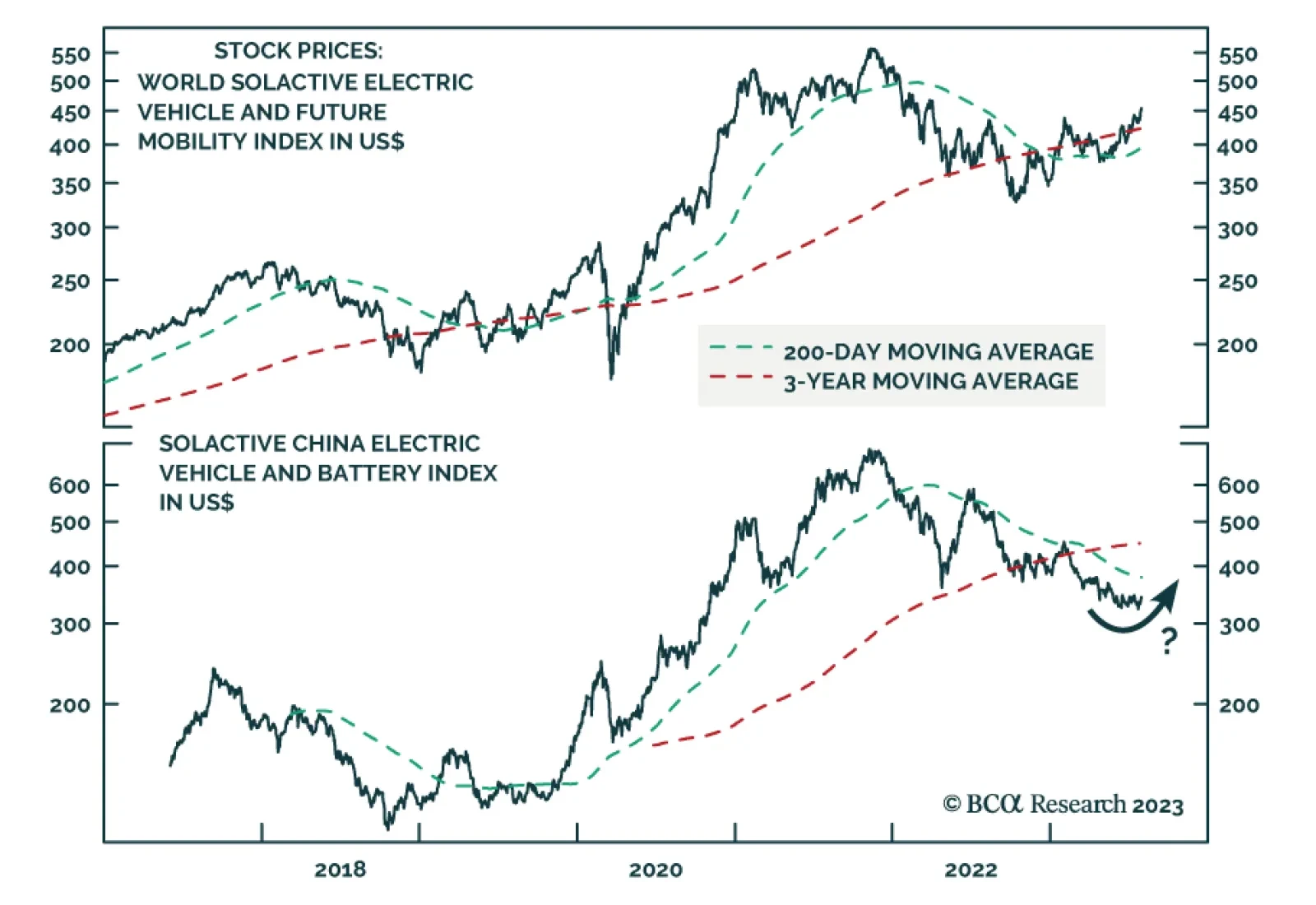

According to BCA Research’s Emerging Markets Strategy service, while EM ex-China markets are set to continue outperforming Chinese investable/offshore equities, they are unlikely to deliver superior absolute returns. Generally, investors are reluctant to…

Collapsed complexity, plus the unwinding of favourable base effects and favourable seasonal adjustments to the inflation and jobs numbers, all pose a danger to the Goldilocks market.

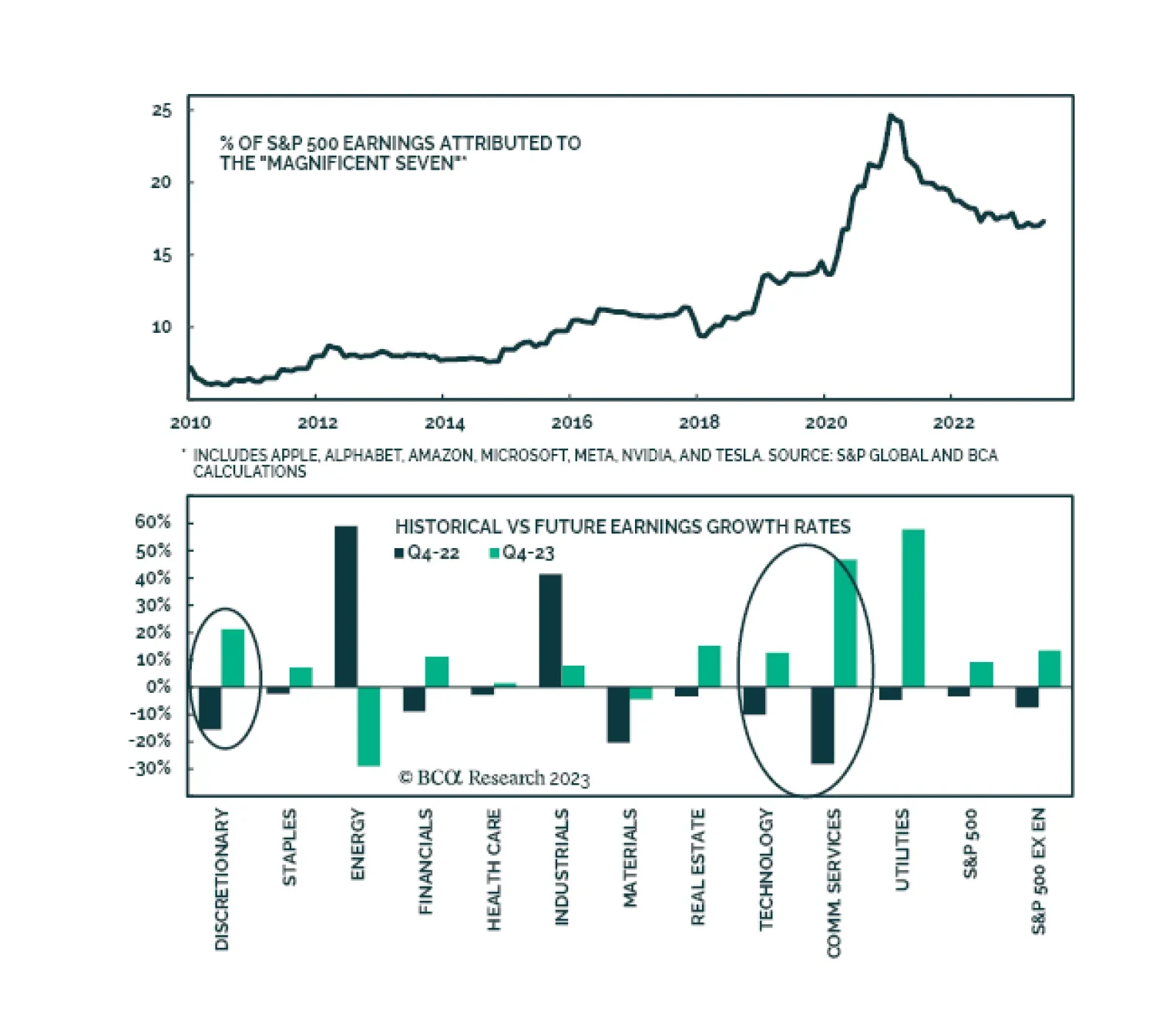

It is widely expected by consensus that earnings growth will rebound into the year-end and into 2024. Multiple factors will drive the reacceleration in earnings growth. Sales growth will pick up: In the remainder of the year, sales growth will pick up from…

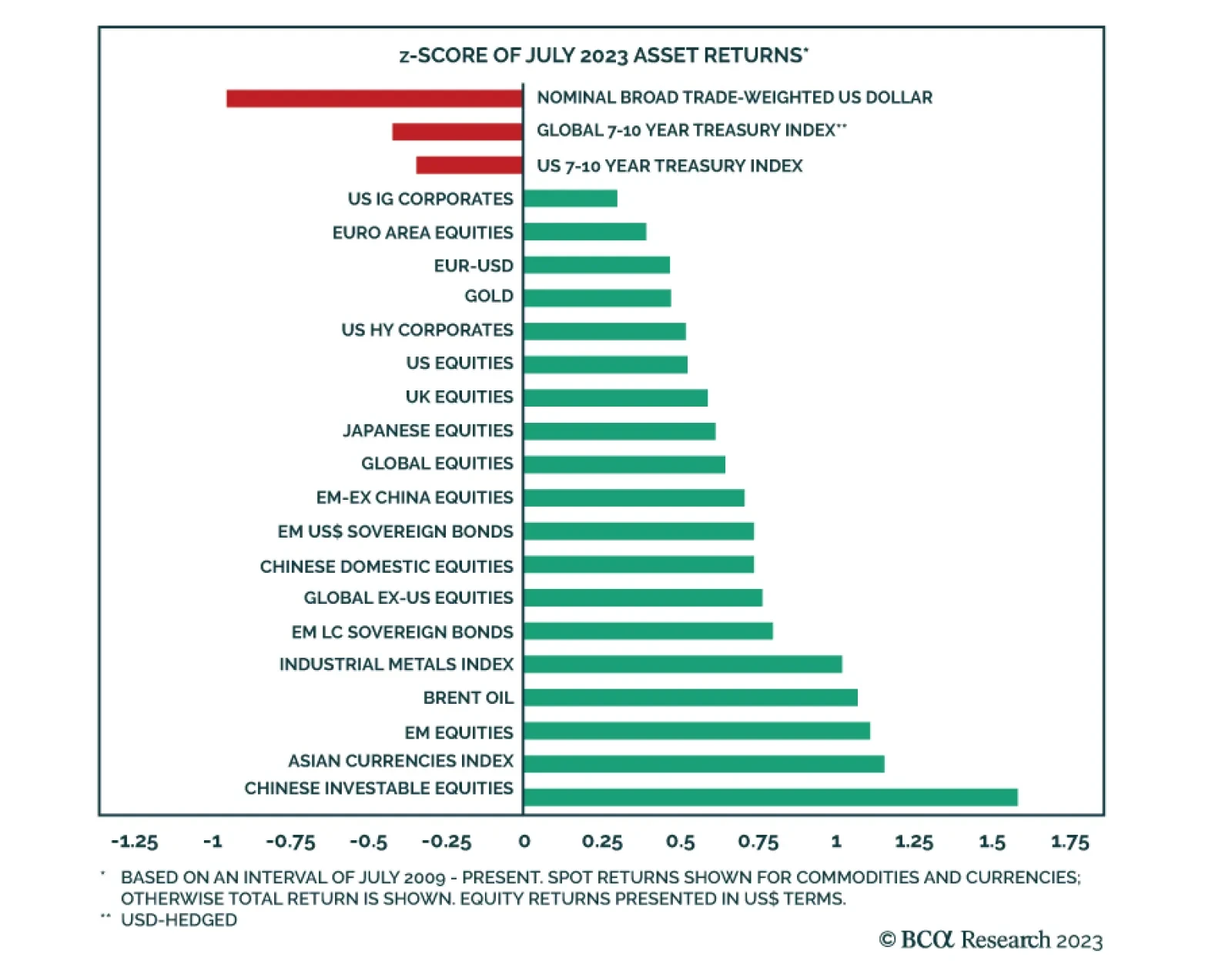

The performance of global financial markets continued to improve in July, with most of the major financial assets we track generating positive abnormal returns for the second consecutive month. Asian markets led this dynamic with Chinese investable stocks…

According to BCA Research’s China Investment Strategy service, Beijing’s investment focus is shifting from traditional infrastructure to new economy infrastructure, which includes clean energy and high-tech sectors. Due to funding constraints,…

Some investors have thrown in the towel on investing in Chinese equities, instead deploying capital in EM ex-China – or at least contemplating doing so. This report examines the merits of investing in EM ex-China stocks and concludes that EM – whether including or excluding China - will continue underperforming DM equities.

History suggests that a “soft landing” is highly unlikely after such an aggressive Fed tightening cycle. The rally could continue for a little longer but, on the 12-month horizon, market risks are very skewed to the downside.

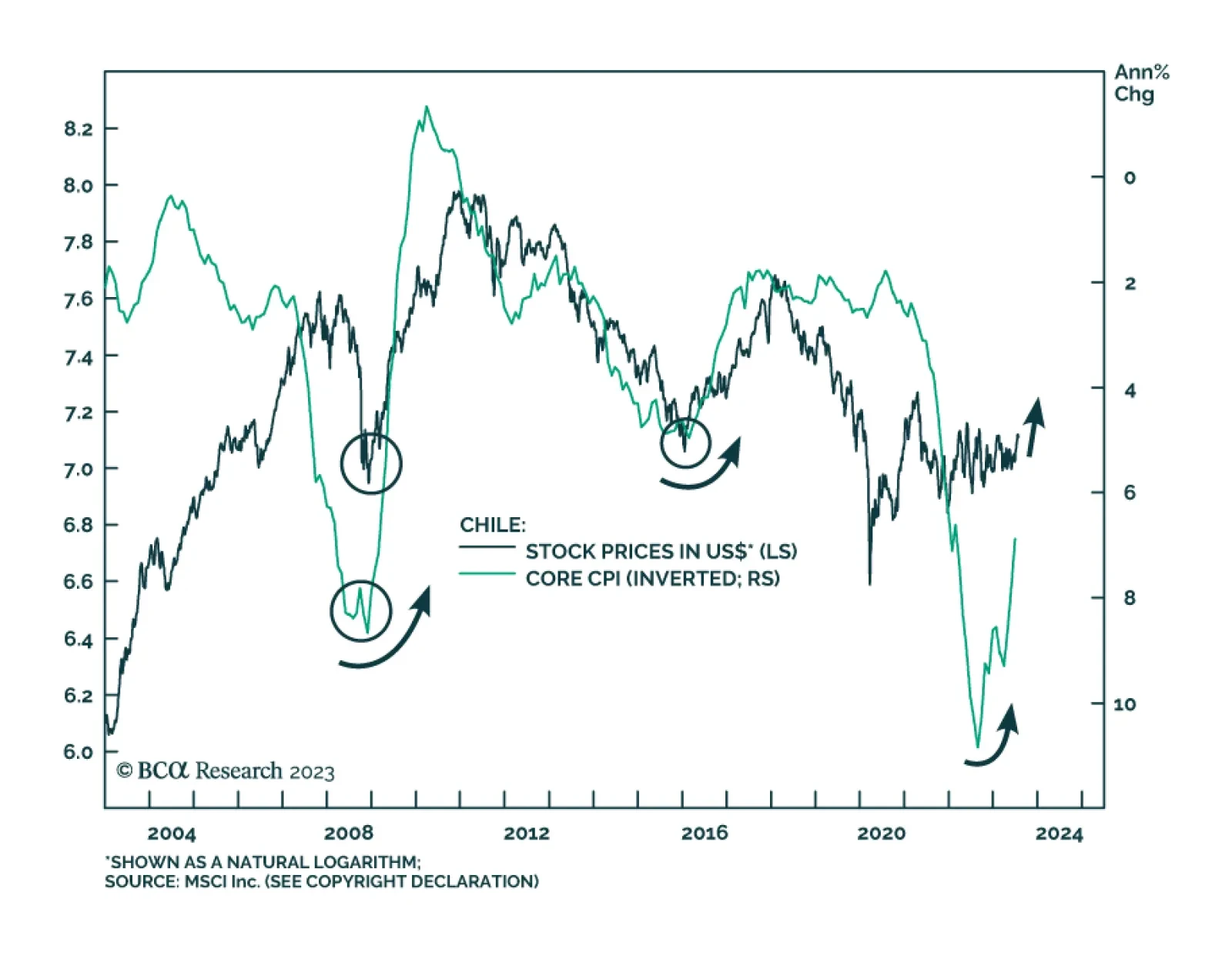

Last Friday, the Central Bank of Chile became the first major Latin American monetary authority to cut rates, thereby beginning the EM monetary easing cycle. In its latest meeting, board members decided to reduce the policy rate by a whopping 100 basis…