Equities

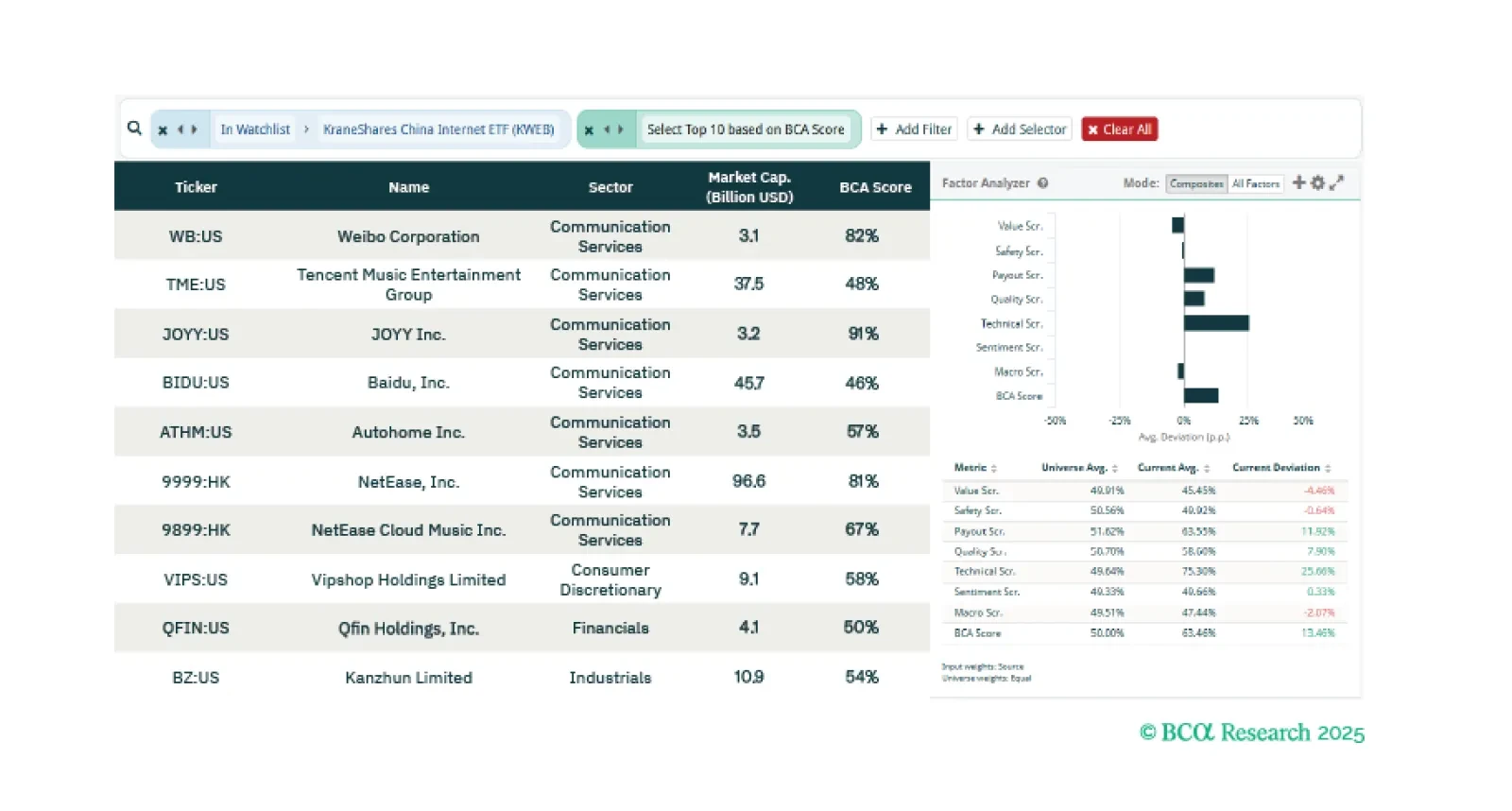

This week our screeners explore offshore Chinese internet stocks, US Healthcare equities, and sectoral opportunities in the Canadian bourse.

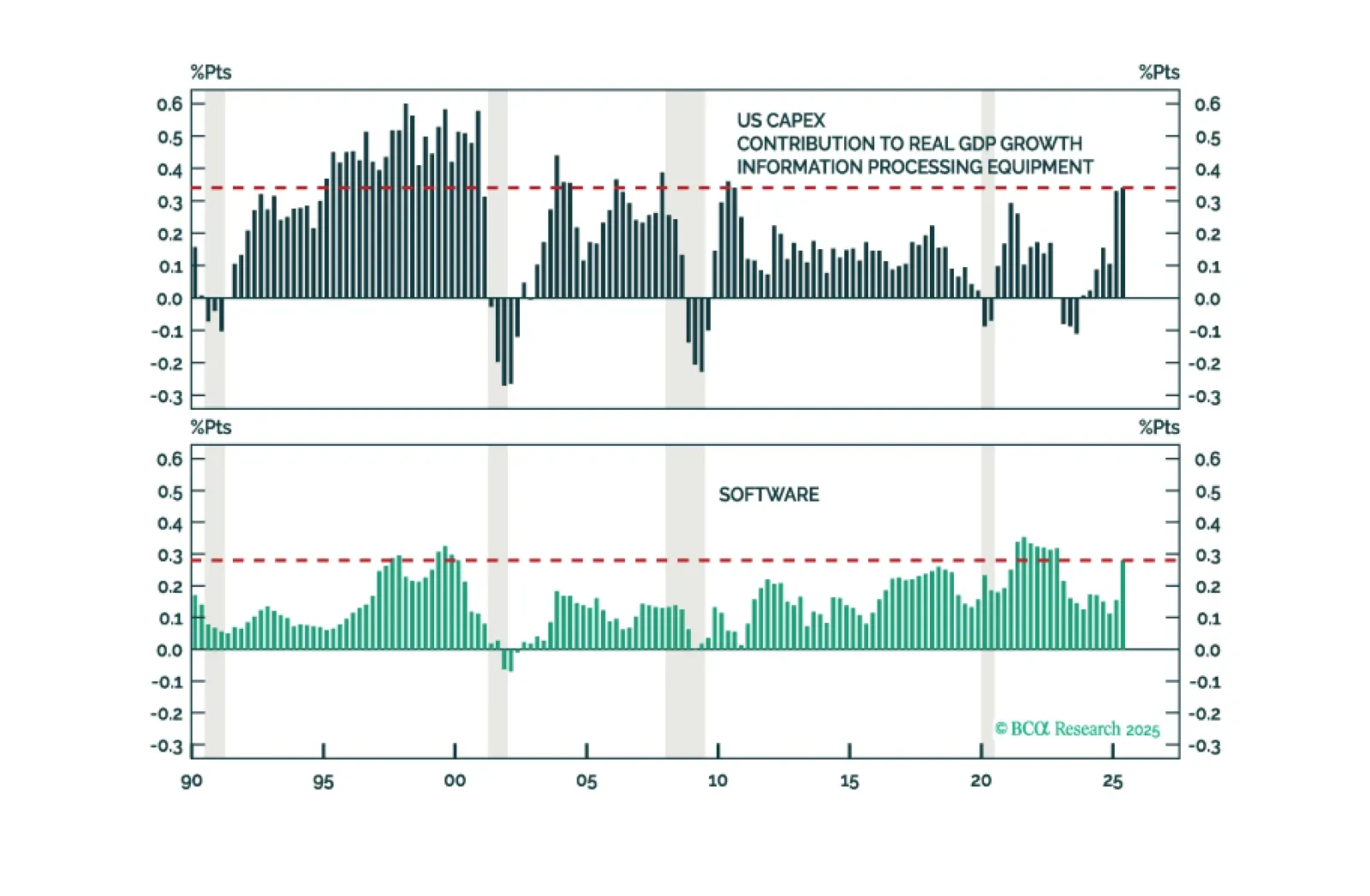

The AI capex boom is having a measurable impact on the economy but, so far, it is more muted than often cited.

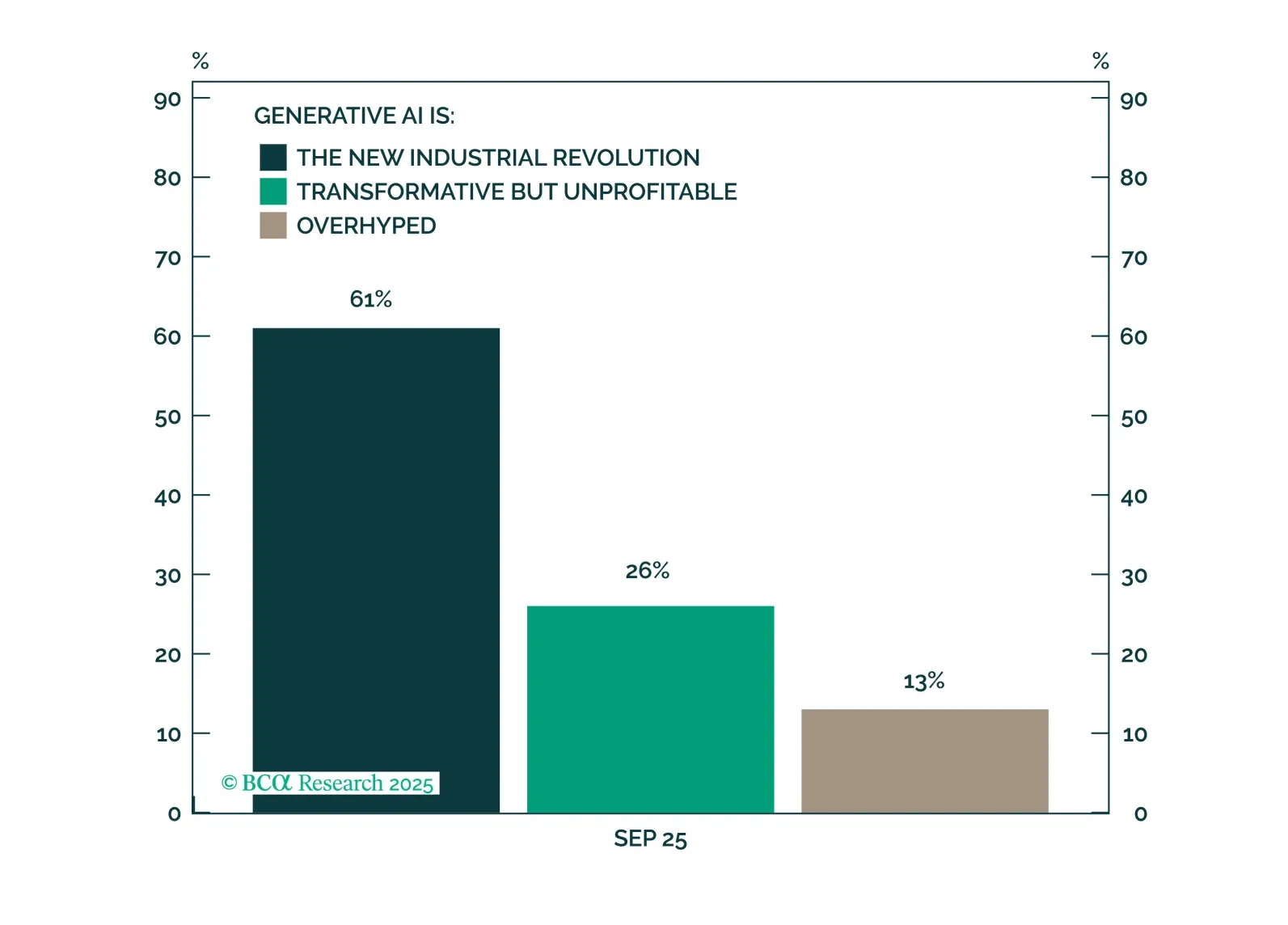

According to our latest client poll, most respondents are optimistic about the Generative AI's potential. Investors remain divided on whether current equity valuations reflect a bubble. Economic concerns continue to center on bond yields and the risk of stagflation, while relatively few clients anticipate a recession. In terms of portfolio positioning, an overweight in Technology received the strongest endorsement.

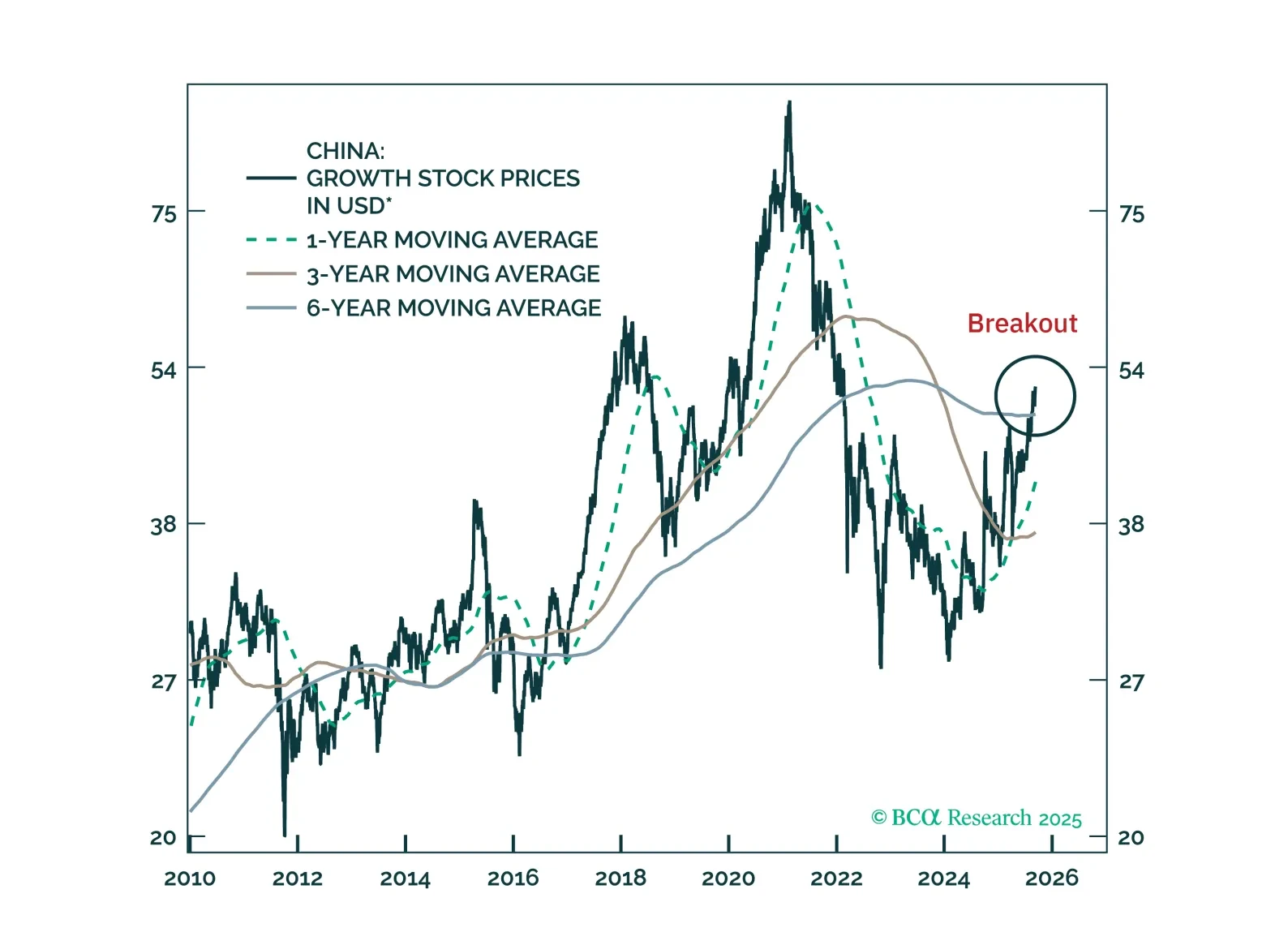

We are turning more constructive on Chinese internet stocks after several years of caution. We recommend going long offshore internet equities in absolute terms and upgrading MSCI China to overweight in a global equity portfolio.