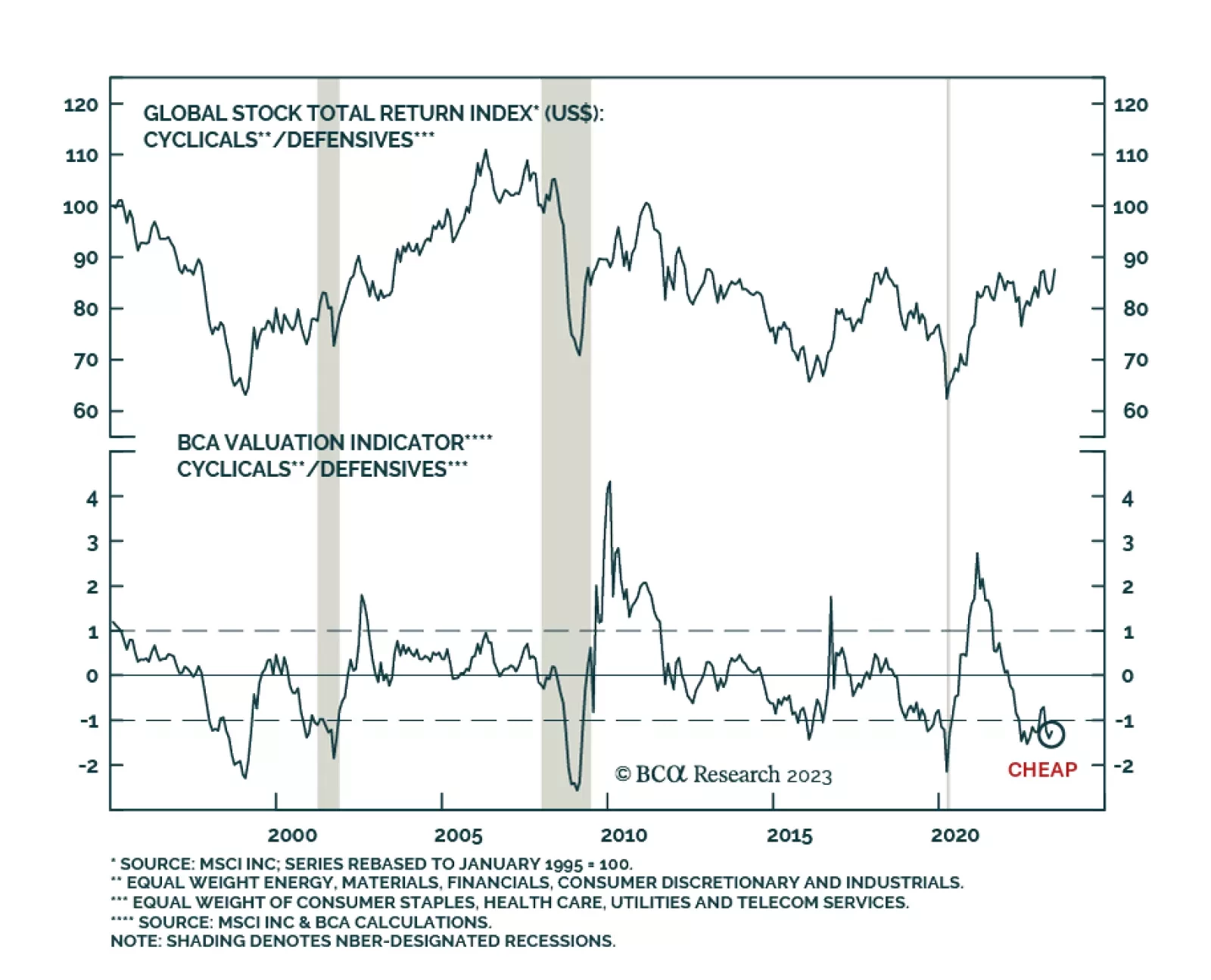

Equities

As the S&P 500 nears our 4,500 target, we review the rationale behind the call to assess its merit.

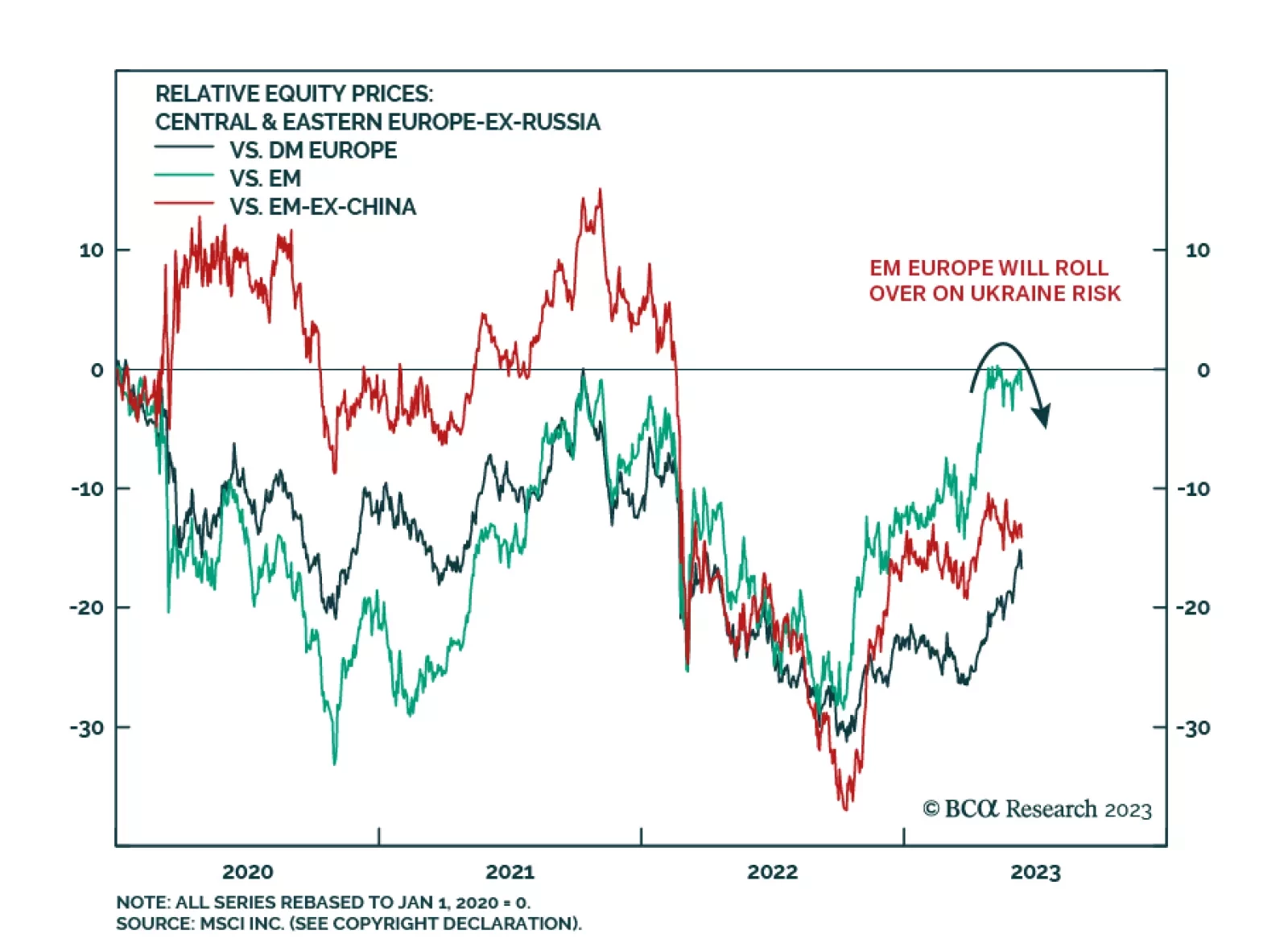

The Eurozone just experienced two consecutive quarters of GDP contraction. For the remainder of the year, can growth pick up or will the ECB decimate activity?

As the major central banks once again mull their policy options, they face a daunting task. They must phase-transition inflation back to imperceptible, without phase-transitioning unemployment to perceptible. This report explains why this will prove impossible, and what central banks will likely prioritise. Plus: the collapsed complexity of the recent stock market rally signals excessive trend-following. Until the complexity normalises, we are reluctant to chase the rally.

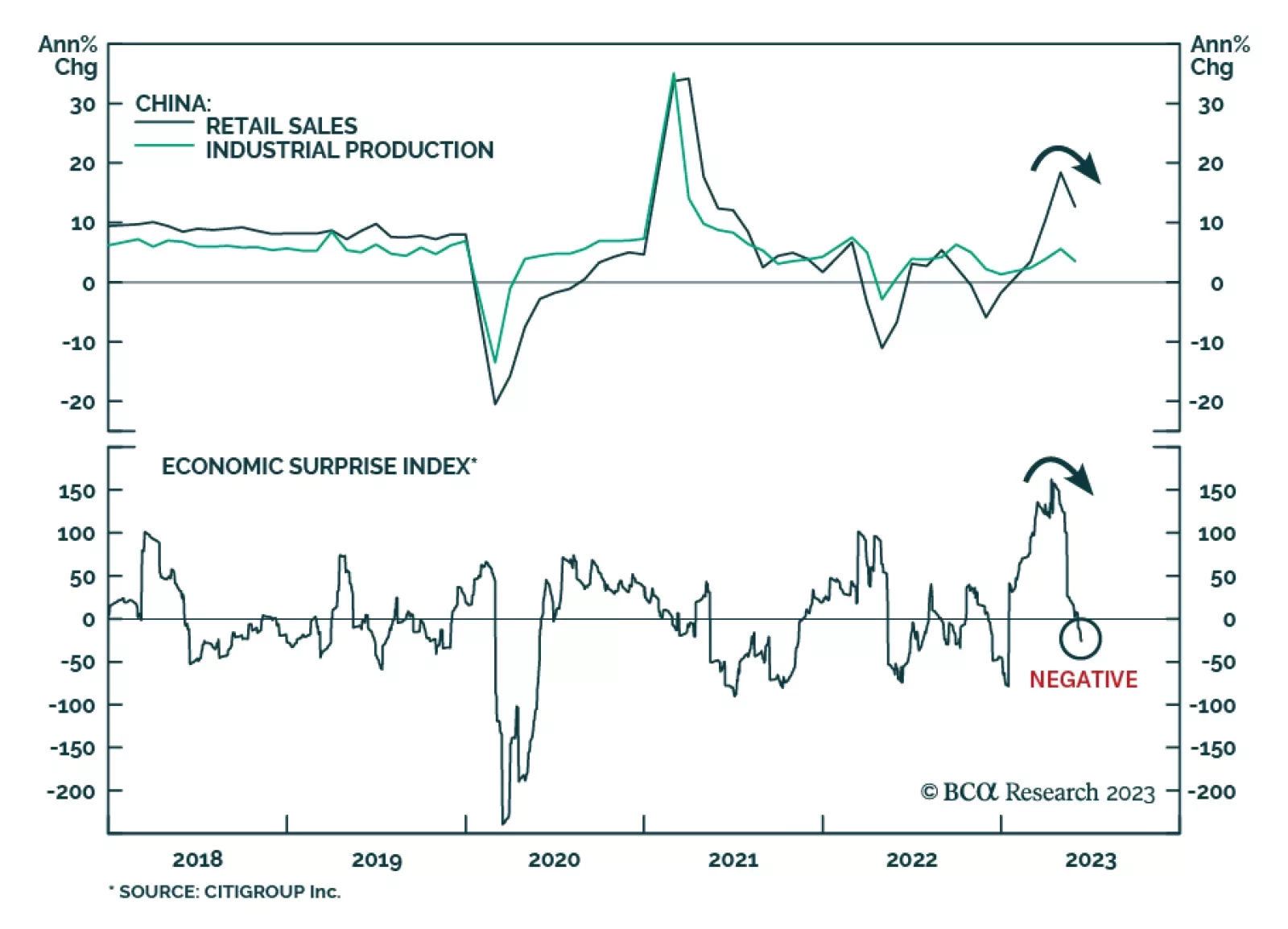

Policymakers will likely continue to stimulate domestic demand via targeted measures and piecemeal stimulus. Yet, the economy will disappoint unless Beijing provides “irrigation-style” stimulus. The latter is not our base case scenario.

Policymakers will likely continue to stimulate domestic demand via targeted measures and piecemeal stimulus. Yet, the economy will disappoint unless Beijing provides “irrigation-style” stimulus. The latter is not our base case scenario.

Policymakers will likely continue to stimulate domestic demand via targeted measures and piecemeal stimulus. Yet, the economy will disappoint unless Beijing provides “irrigation-style” stimulus. The latter is not our base case scenario.