Equities

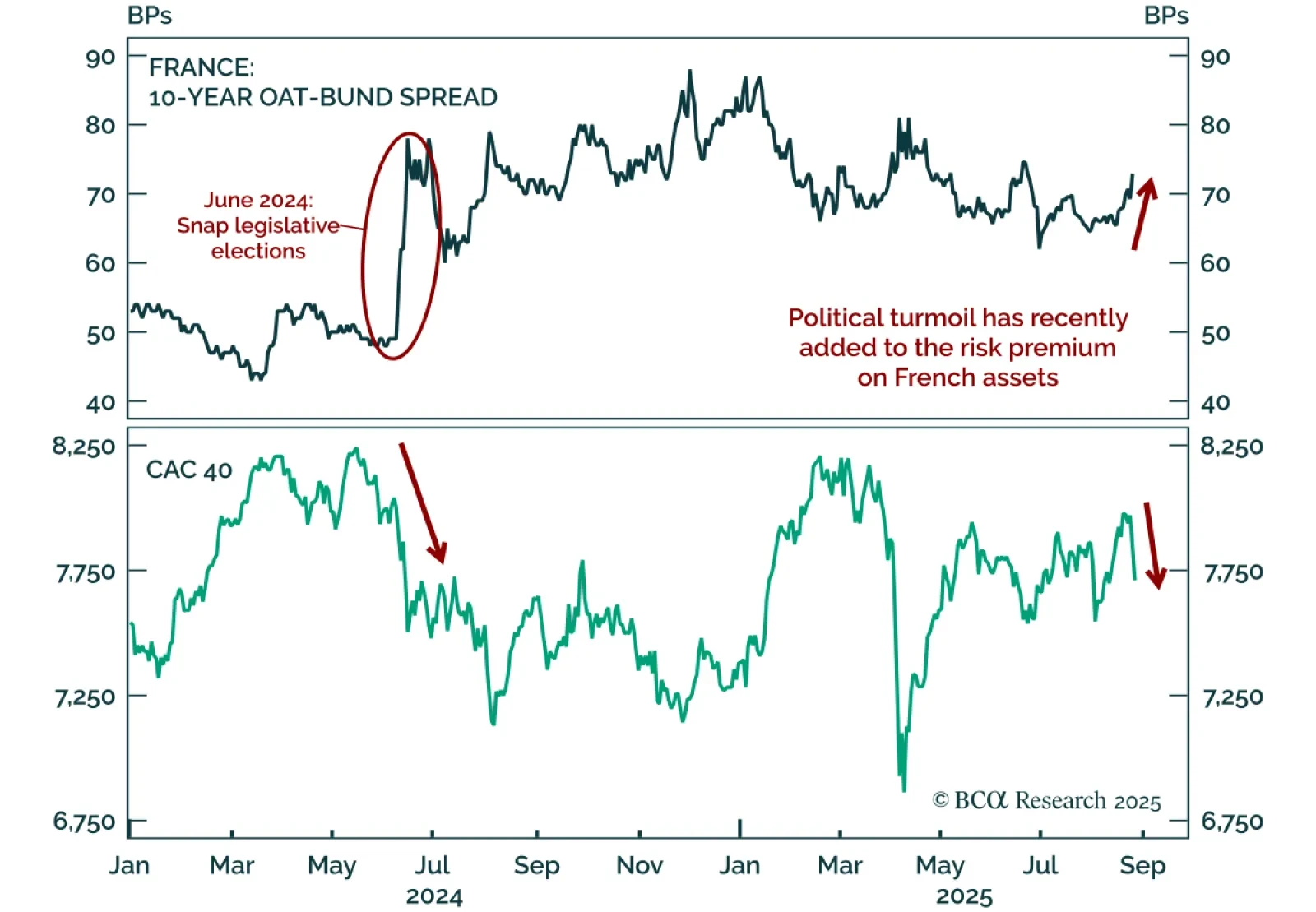

Core Europe’s industrial sector will relapse in the coming months due to US tariffs and a strong euro. Investors can play the imminent deflationary shock by being long Central European bonds. They should, however, hedge the currency risk vis-à-vis the euro.

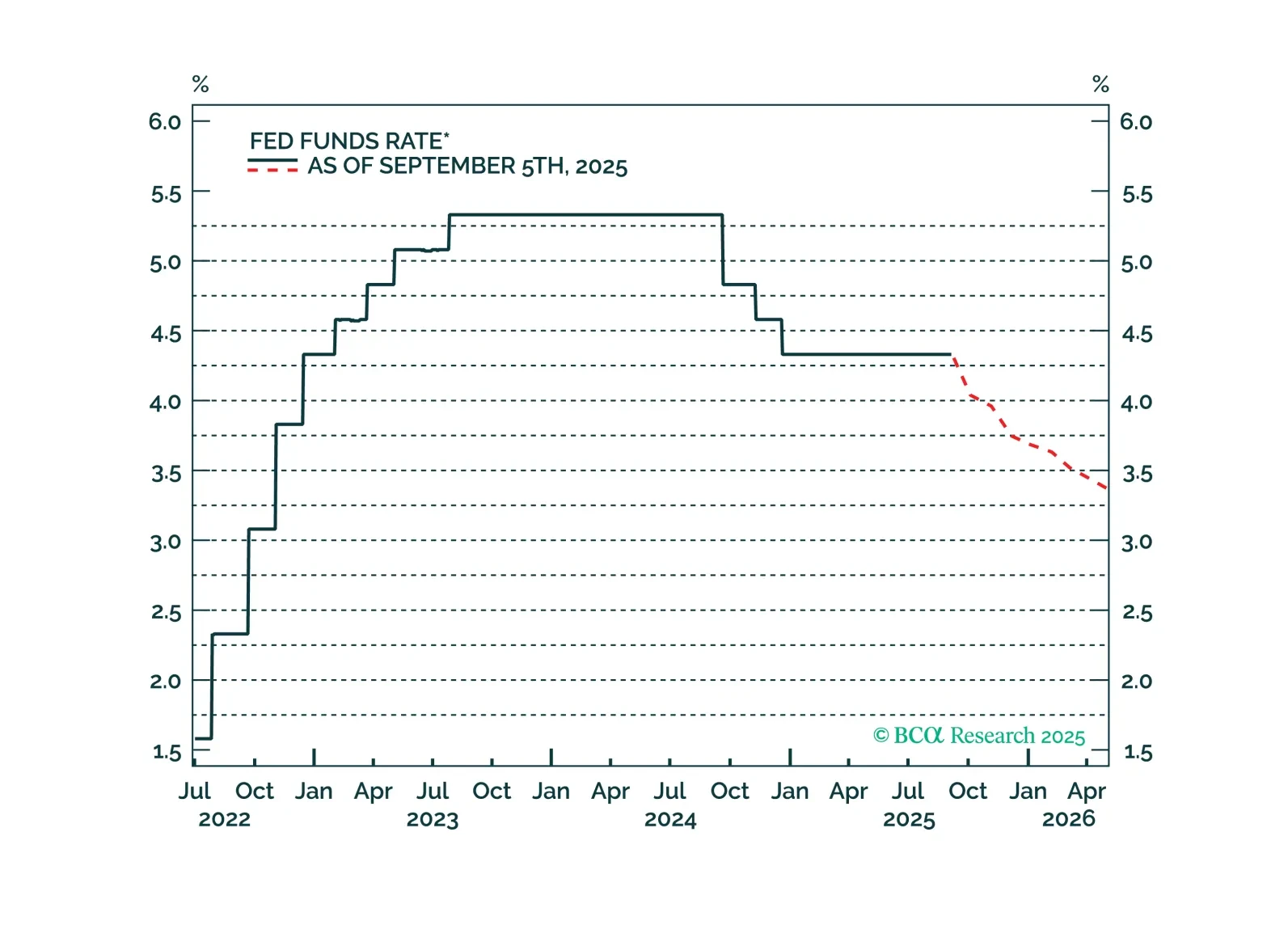

The economy is slowing, but not collapsing, and monetary easing is imminent — a backdrop that will benefit equities. We remain strategically bullish, with a close eye on GenAI and resilient earnings, even amid numerous risks. However, we are tactically cautious, as seasonality, elevated valuations, and stretched technicals present near-term headwinds.

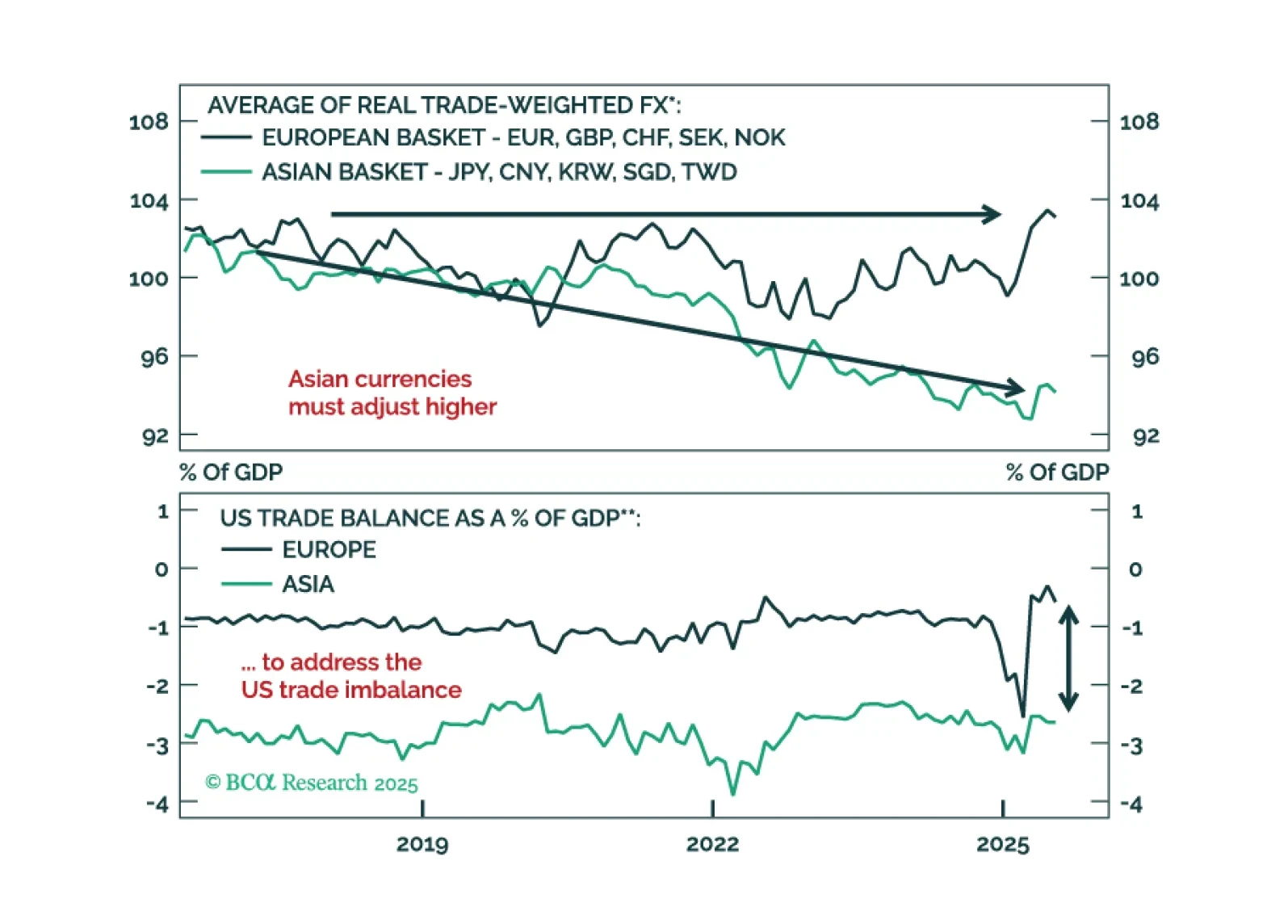

A fleeting greenback rally post Fed rate cut will offer a final chance to reset short dollar exposures. See why undervalued Asian FX are poised to lead the next leg lower in USD and how to position now.

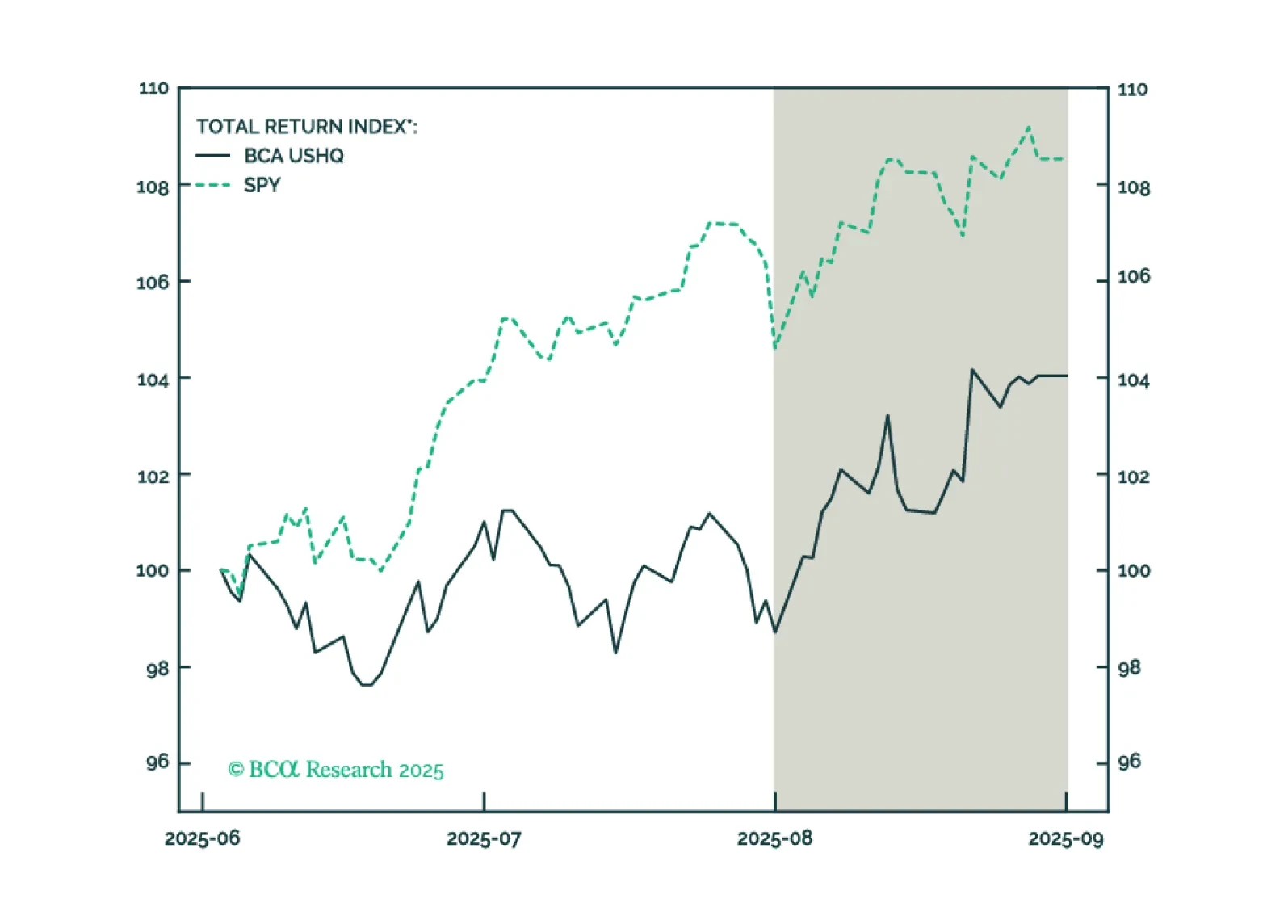

The US High Quality (USHQ) portfolio outperformed its benchmark through August, returning 5.39%, whilst its SPY benchmark returned 3.75%. On a trailing three-month basis, the USHQ portfolio’s performance was weaker than the benchmark, but the gap narrowed, with USHQ underperforming by approximately 450bps.

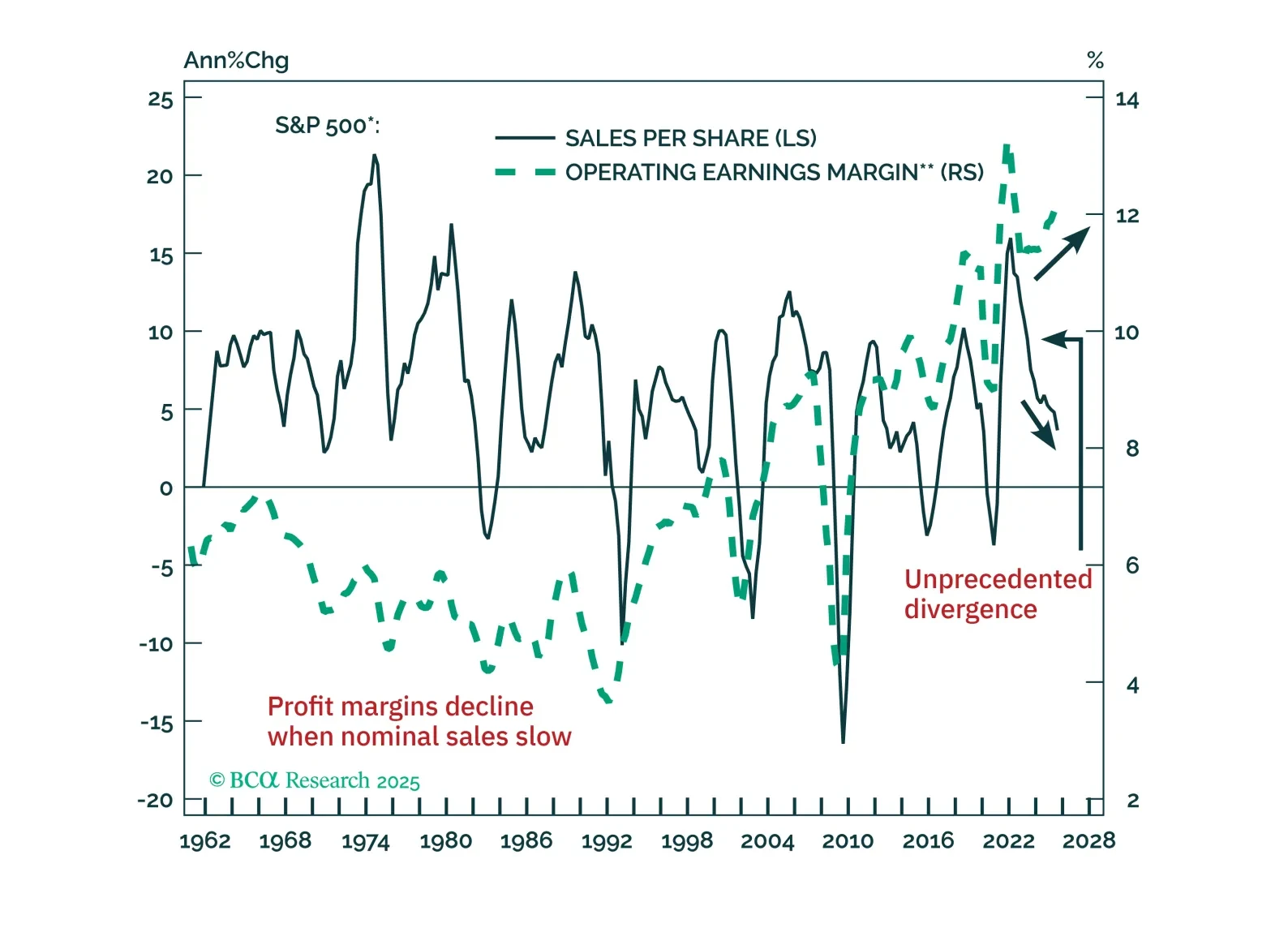

The resilience of US non-tech companies' profitability has not been driven by top-line growth but by falling costs, which safeguarded profit margins. Presently, risks in US stocks outweigh the potential rewards – margin sustainability is uncertain while equity valuations are very stretched.

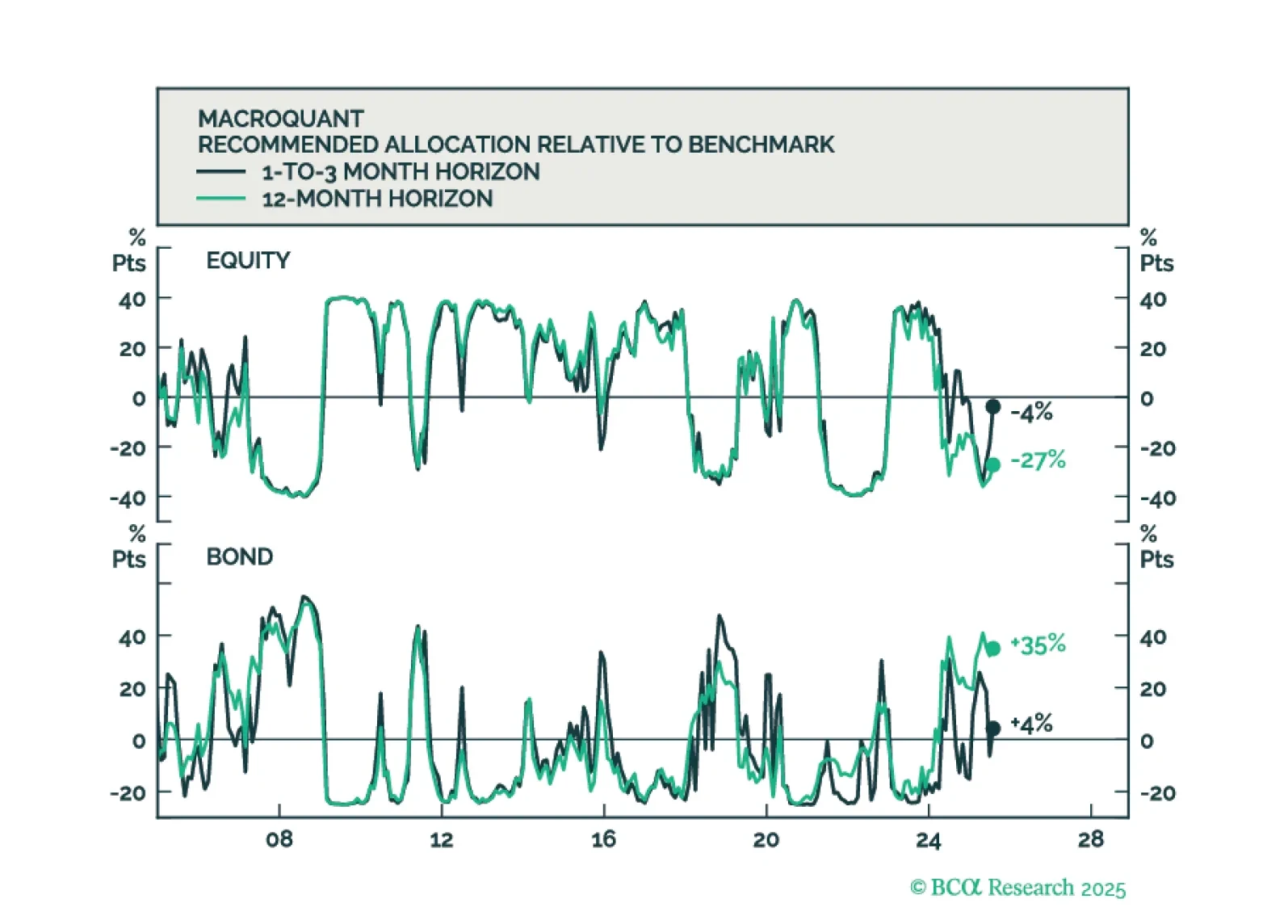

MacroQuant sees downside risks to stocks over a long-term horizon but is not yet saying that we are at imminent risk of an equity bear market.

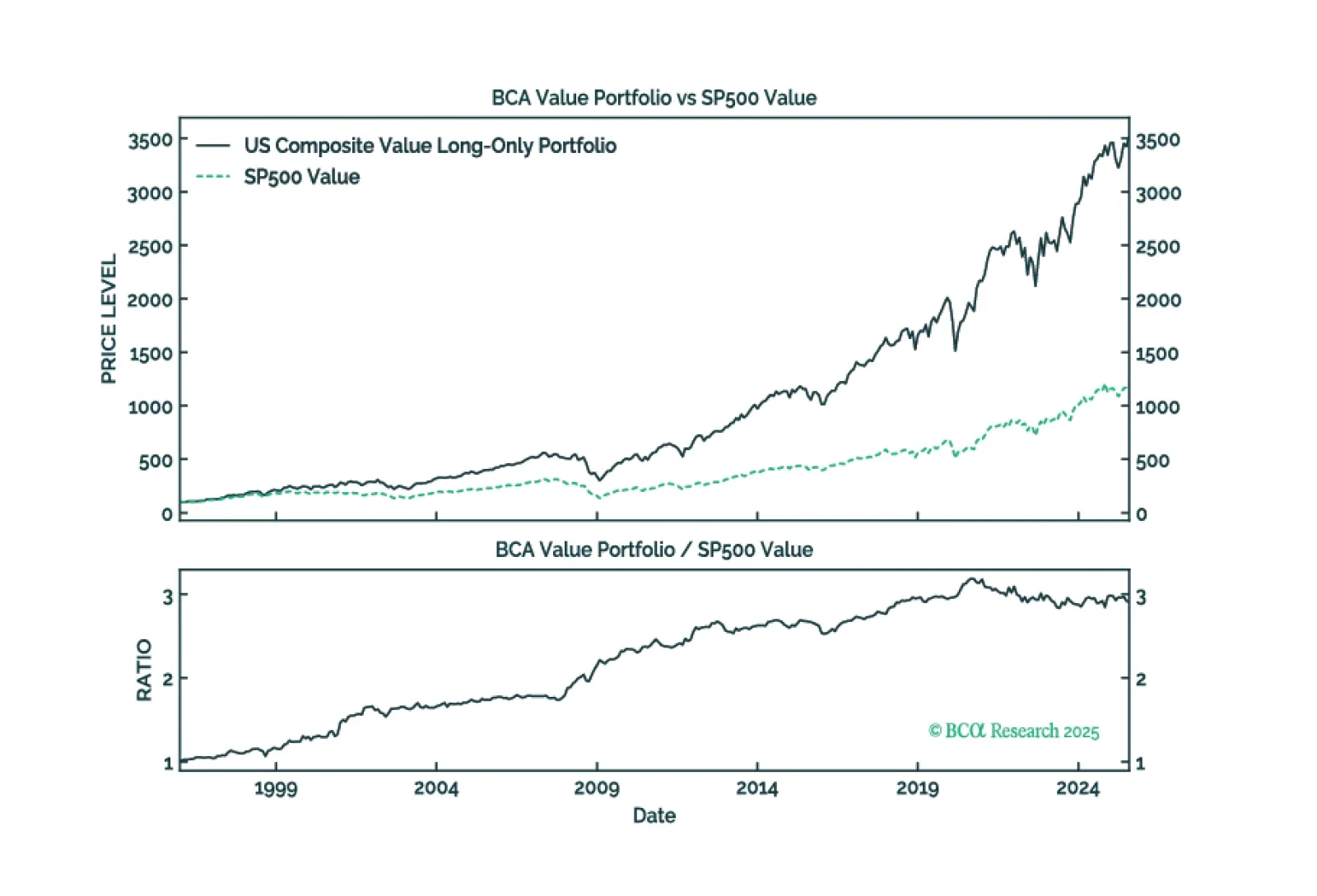

Commercial indices’ limitations have made Value a fertile ground for stock pickers. Our Composite Value model has shown promise in circumventing these flaws and capturing alpha.